Guatemala’s emerging iGaming market offers prospects driven by increasing internet penetration and demographic shifts. However, the sector is still under a developing regulatory framework, requiring careful navigation of legal and licensing procedures. This analysis provides insights critical for operators seeking sustainable entry into the country’s digital gambling ecosystem.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Partially Legal with Restrictions |

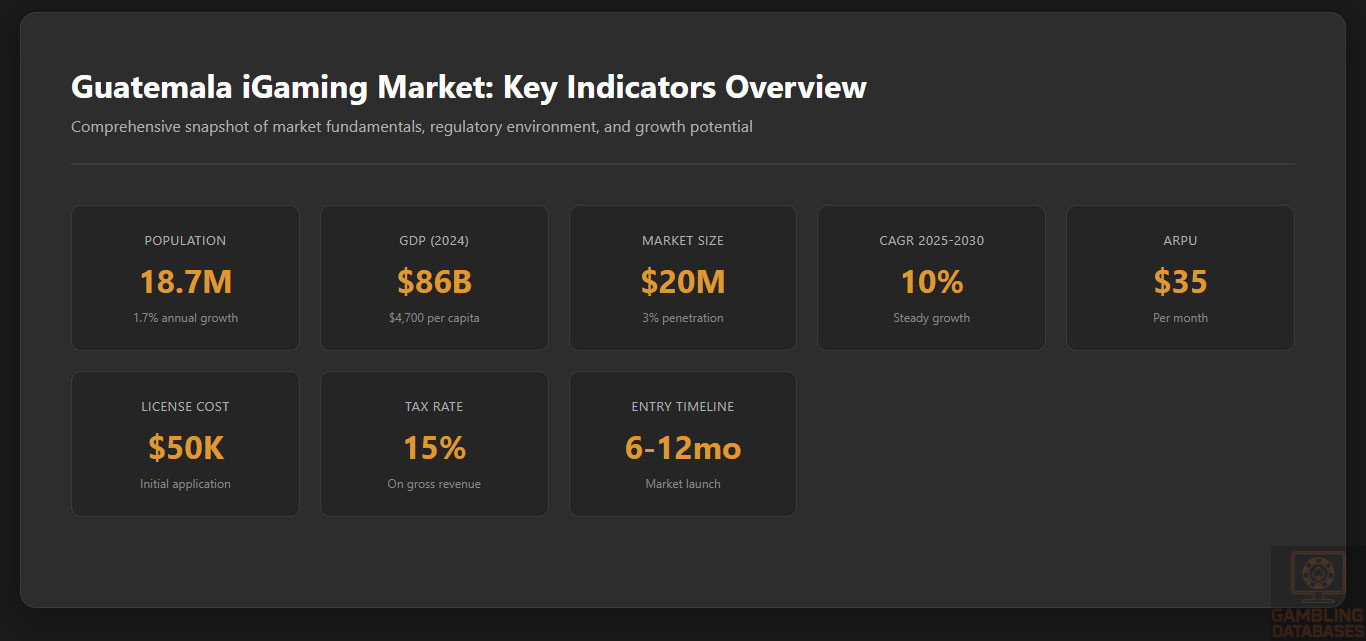

| Population | 17 million |

| GDP (2024 estimate) | $86 billion USD |

| Internet Penetration | 50% |

| Mobile Penetration | 80% |

| Estimated Licensing Cost | $50,000 USD |

| Tax on Gross Revenue | 15% |

| Market Entry Timeline | 6-12 months |

| Regulatory Authority | Superintendencia de Administración Tributaria (SAT) |

| Market Size (2024) | $20 million USD |

| Projected CAGR (2025-2030) | 10% |

| ARPU (Average Revenue Per User) | $35 USD/month |

| Market Penetration | 3% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Guatemala’s gambling sector is regulated primarily through existing national laws that oversee land-based activities while online gambling remains in a nascent legal state. The regulatory approach is cautious, with authorities emphasizing control over unlicensed operations rather than comprehensive legalization of digital gaming. Currently, casino operations, sports betting venues, and slot machines are legal but tightly controlled under specific licenses, generally applicable to physical venues.

Land-based gambling activities include licensed casinos, sports betting shops, and slot hall operators, all subject to local licensing procedures. Online gambling, however, faces a less defined regime, with the government maintaining a restrictive stance that limits online operators’ legal recognition unambiguously. There are ongoing discussions about formalizing regulations to facilitate legal online betting and gaming, but comprehensive legislation has yet to be enacted.

Land-Based Gambling Activities

Operations encompass licensed casinos primarily in Guatemala City, with some expansion into regional zones. Sports betting is conducted through both physical outlets and, increasingly, online platforms under strict licensing conditions. Slot machine halls operate within licensed venues but are also subject to tax and operational restrictions. The sector’s overall regulatory oversight aims to prevent illegal gambling activities while maintaining control over licensed entities.

Online Gambling Framework

The digital gambling framework remains underdeveloped, with no explicit licensing pathway for online operators. The government prohibits unlicensed online gambling, and there is no clear legal pathway for foreign operators to acquire licenses. Enforcement against illegal online gambling is active, with authorities conducting raids and blocking access to unlicensed sites. Regulatory oversight is expected to evolve as discussions around modernizing gambling laws progress.

Licensed Operators and Market Players

The commercial landscape consists of a limited number of licensed land-based operators, with a nascent online segment dominated by regional players. International companies seeking entry face regulatory uncertainty and licensing challenges, with local autonomy and restrictions on foreign ownership. Market share remains concentrated within established land-based venues, with online market growth constrained by legal ambiguities and enforcement measures.

Licensing Framework and Requirements

Application Process and Eligibility

Operators must submit applications to the Superintendencia de Administración Tributaria, requiring a comprehensive dossier that includes proof of financial stability, compliance with AML/KYC standards, and technical certifications. The licensing process is currently estimated to take between 6 and 12 months, with an application fee of approximately $50,000 USD. Applicants must demonstrate operational capability and adherence to established standards before approval.

Local Presence and Operational Requirements

Licensing laws stipulate a physical presence or local representative, mainly to facilitate regulatory oversight and ensure compliance. The requirement is typically fulfilled via local partnerships or establishing a registered office. Foreign ownership restrictions limit full control unless partnerships with local entities are formed. Domain registration and hosting must often occur within the country or with approved local providers.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators are mandated to deploy strict age verification, KYC, and AML procedures. Responsible gambling measures include self-exclusion options, clear disclosure of terms, and limits on betting activities. The government emphasizes safeguarding minors and preventing illegal betting participation through robust monitoring systems.

Financial Monitoring and Reporting

- Implement transaction monitoring systems for suspicious activity

- Report large transactions to authorities

- Maintain audit trails for all financial operations

- Conduct regular financial audits and submit compliance reports

Taxation Structure and Financial Obligations

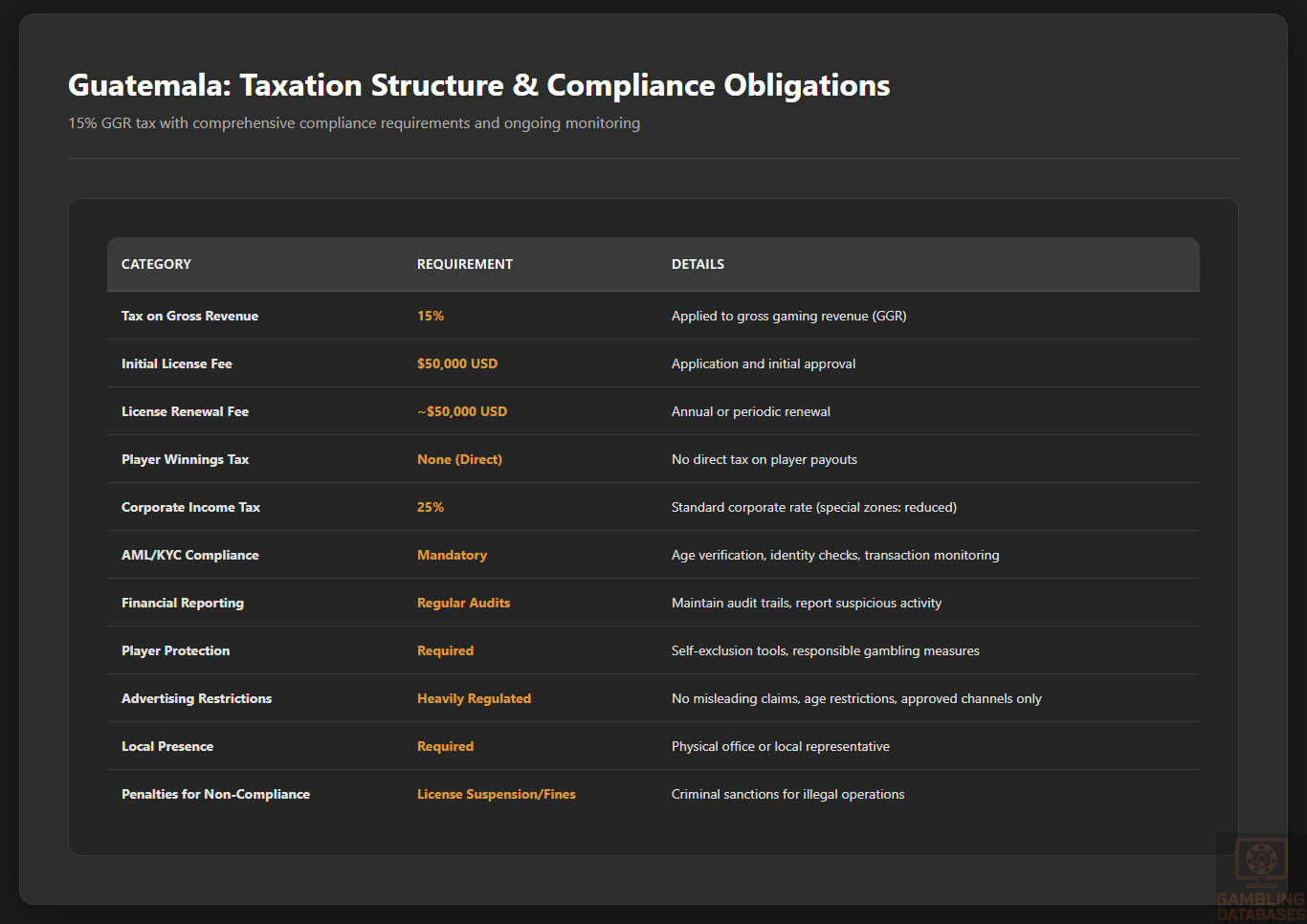

Operators are subject to a 15% tax on gross gaming revenue, with additional fixed licensing fees. Player winnings are not taxed directly, but operators monitor payouts rigorously. License renewal fees are approximately $50,000 USD, with additional turnover taxes applicable in specific segments. Revenue projections indicate steady growth, driven by gradual market liberalization.

Advertising and Marketing Restrictions

Advertising is restricted to within licensed premises and approved channels. Online promotions are heavily regulated, with bans on misleading claims, restrictions on targeting minors, and limits on advertising during certain hours. Sponsorships and partnerships must comply with local content restrictions under evolving legislation.

Recent Regulatory Changes and Their Impact

Recent amendments focus on tightening AML standards and introducing more rigorous licensing conditions. The impact increases operational costs and compliance burdens for existing operators while signaling a cautious approach to liberalization. These changes reflect a government intent on balancing control with potential future market expansion.

Enforcement Mechanisms and Penalties

- License suspensions for non-compliance

- Fines for operating without valid licenses

- Criminal sanctions for illegal gambling facilitation

- Access blocking of unlicensed sites

- Increased oversight through regular audits

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

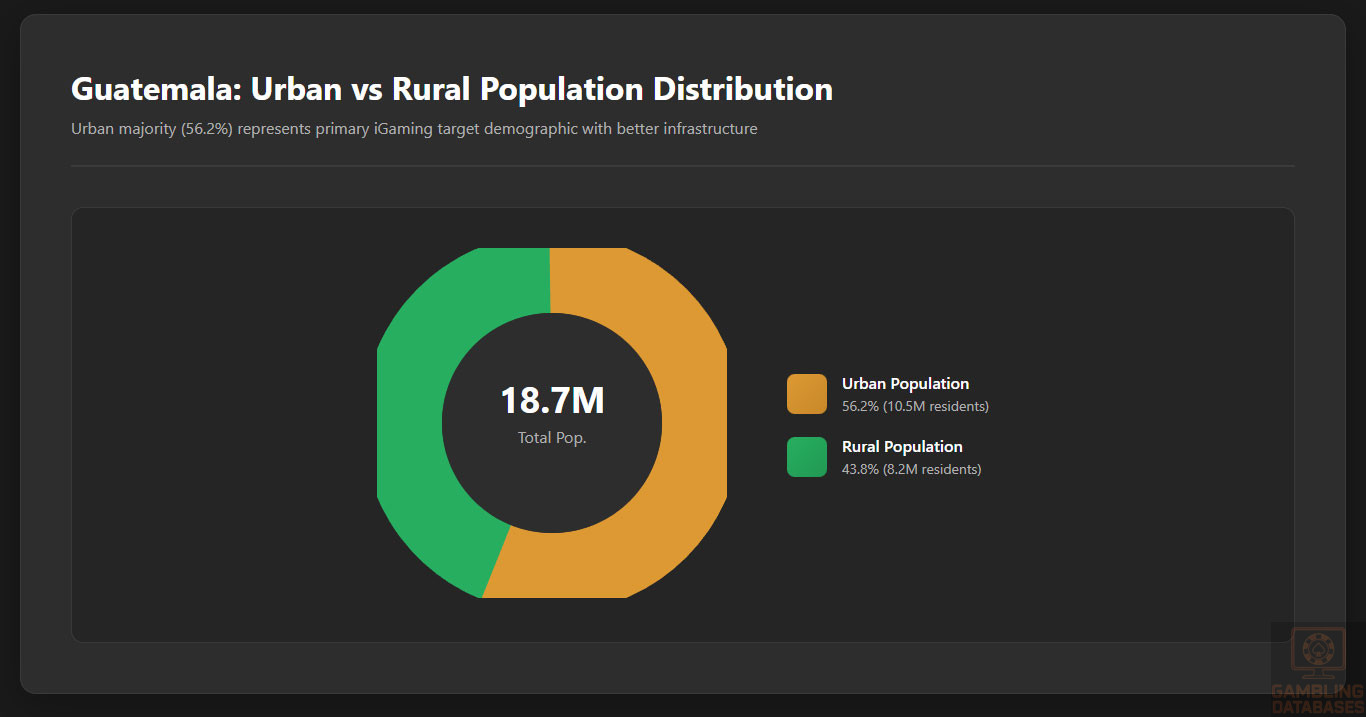

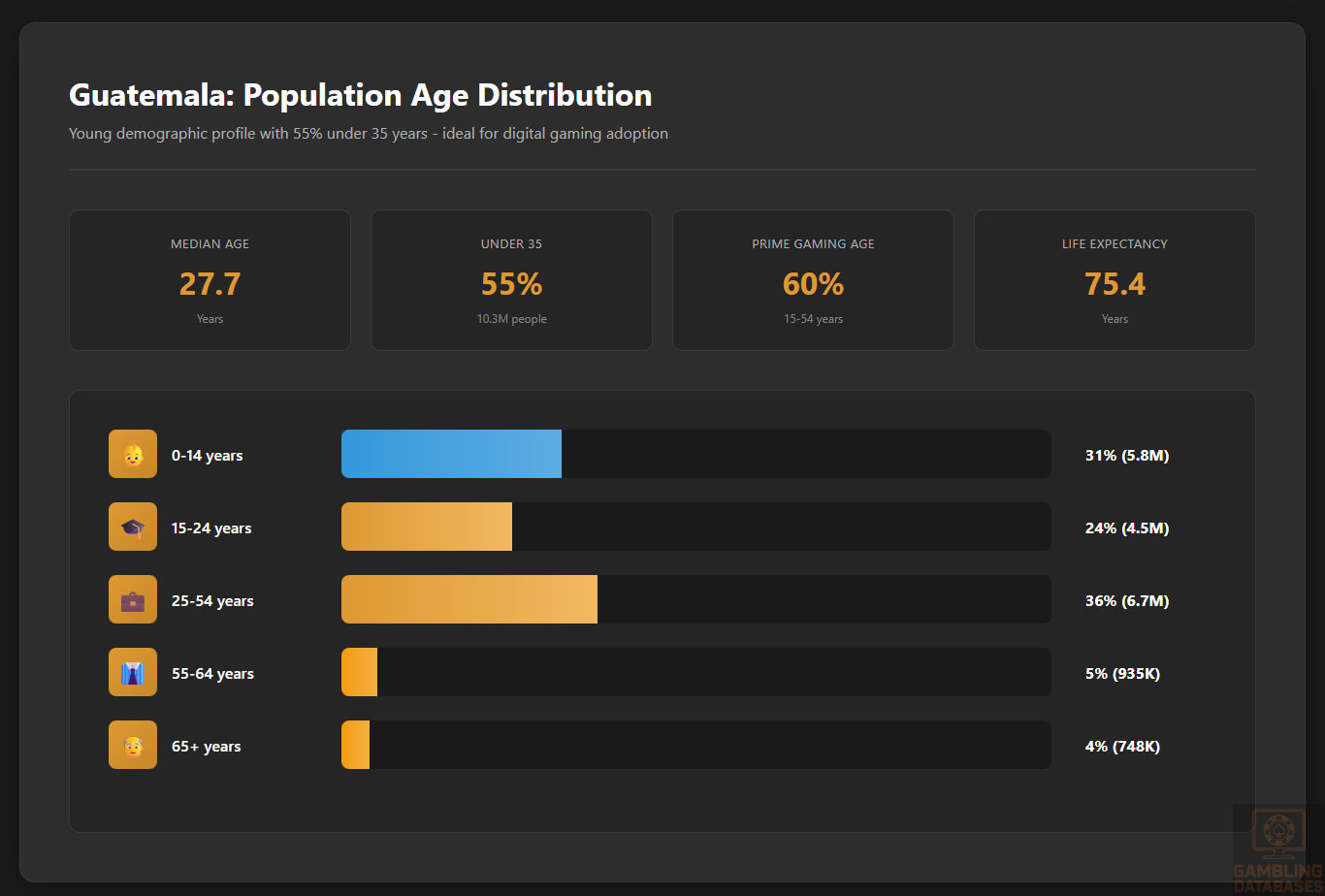

Guatemala’s population in 2025 stands at approximately 18.7 million residents, reflecting a sustained growth rate near 1.7% per year. The nation’s population density has reached 182.6 people per km2, with significant concentration in urban centers and a rising trend of urbanization. Urban dwellers now account for over 56.2% of all inhabitants, while rural communities represent 43.8%. The median age is 27.7 years, denoting a young population ideal for digital entertainment and iGaming market growth.

Male and female representation stands nearly balanced, with 951 males per 1,000 females. Life expectancy has climbed to 75.4 years, underscoring improvements in public health and longevity for both genders.

| Age Group | Population % |

|---|---|

| 0-14 years | 31% |

| 15-24 years | 24% |

| 25-54 years | 36% |

| 55-64 years | 5% |

| 65+ years | 4% |

Urban centers are the core regions of iGaming activity, supported by robust internet access and higher disposable income.

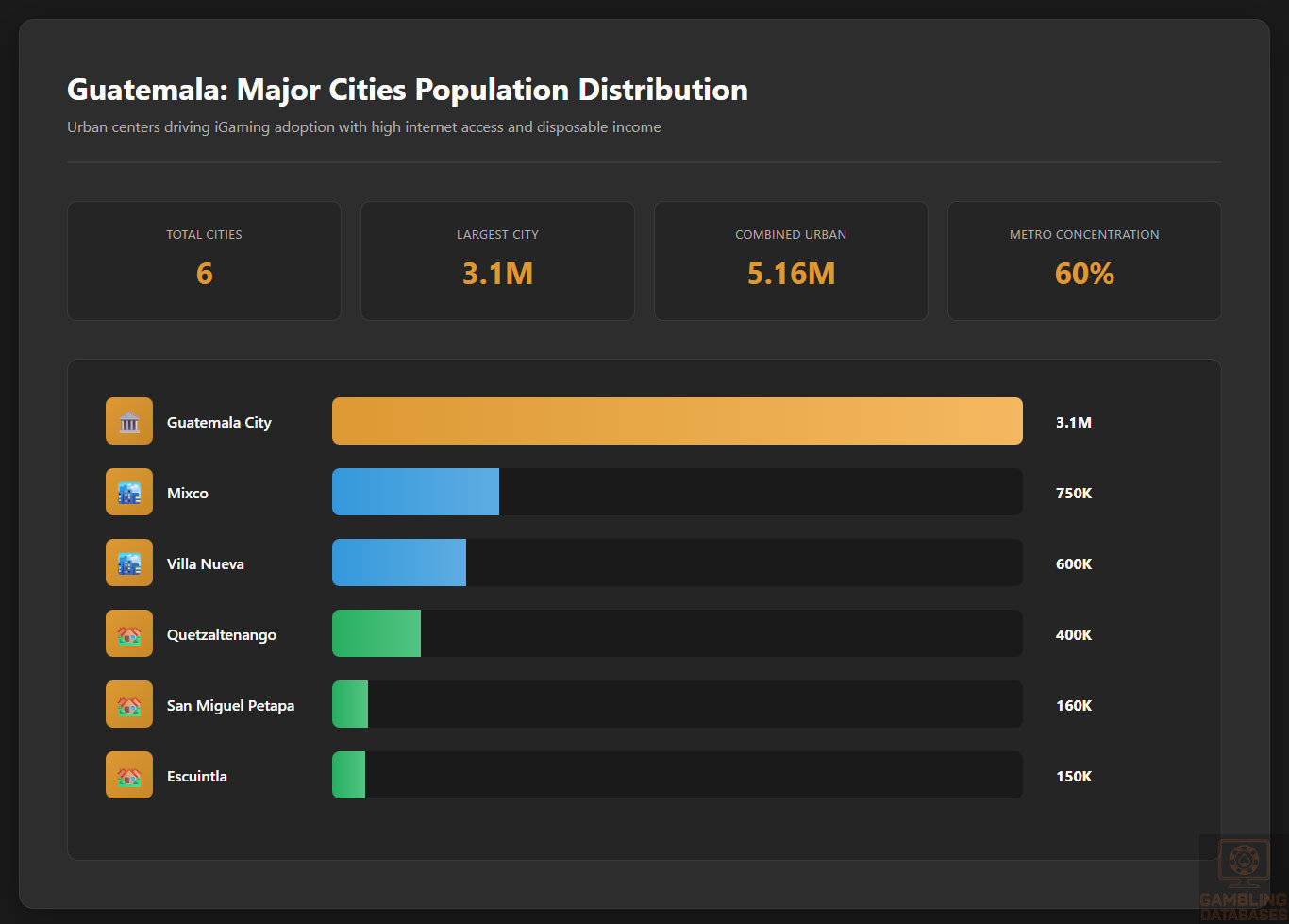

Major Cities by Population

- Guatemala City: ~3.1 million

- Mixco: ~750,000

- Villa Nueva: ~600,000

- Quetzaltenango: ~400,000

- San Miguel Petapa: ~160,000

- Escuintla: ~150,000

The Greater Metropolitan Area, especially Guatemala City, comprises a dense cluster of iGaming and tech-adopting consumers. Economic inequalities between urban and rural regions influence market concentration and spending power, fueling industry focus in areas with more stable economic infrastructure.

Economic Indicators and Consumer Spending Power

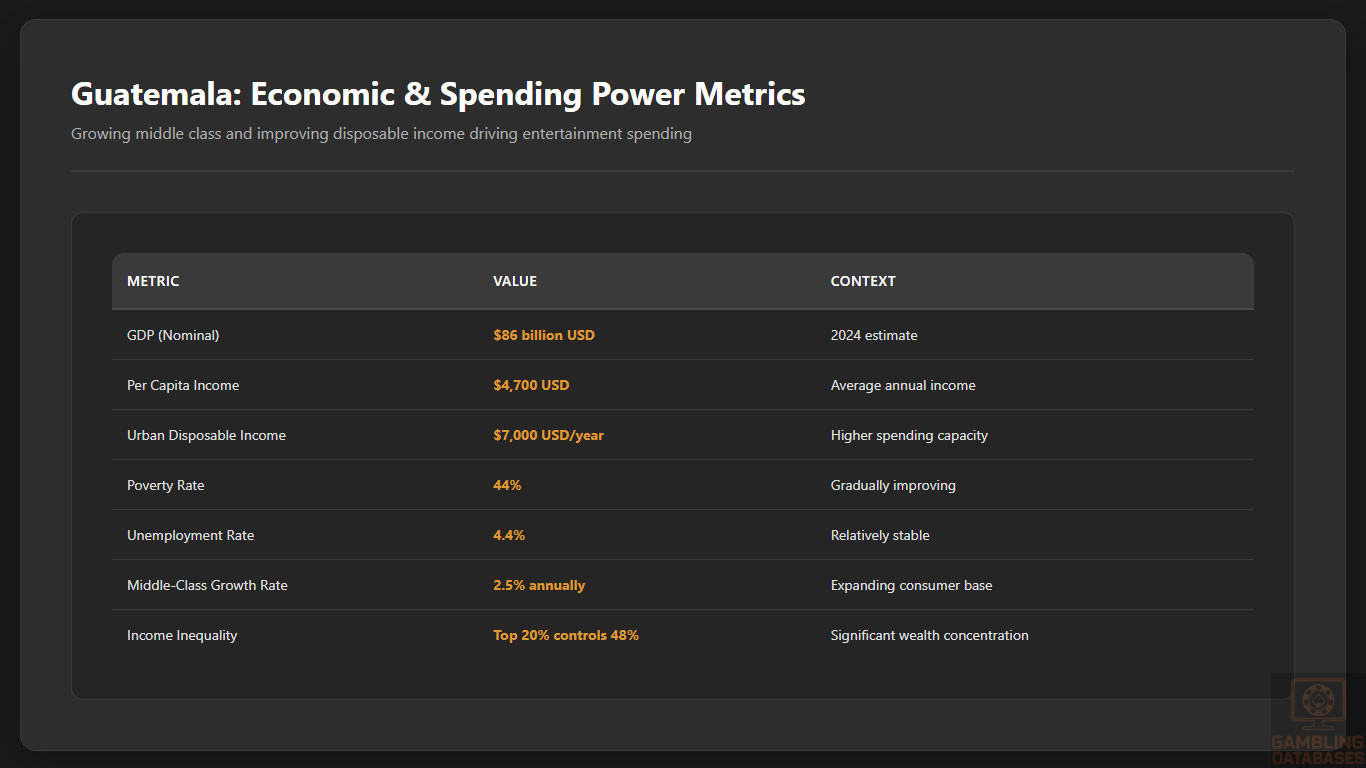

Guatemala’s GDP reached $86 billion USD in 2024, with per capita figures surpassing $4,700 USD. Steady growth is forecasted, driven by services, manufacturing, and a growing digital economy. The middle-income segment is expanding, further amplifying consumer spending capacity in entertainment and online services.

Income distribution is marked by substantial inequality; the top 20% control nearly 48% of national income, while lower-income populations maintain conservative spending habits. Disposable income continues to rise among urban professionals, enabling faster adoption of digital leisure and iGaming. The poverty rate remains about 44%, but gradual improvements in education and employment are lowering barriers for market access.

| Metric | Value |

|---|---|

| GDP (nominal) | $86 billion USD |

| Per Capita Income | $4,700 USD |

| Urban Disposable Income | $7,000 USD/year |

| Poverty Rate | 44% |

| Unemployment Rate | 4.4% |

| Middle-Class Growth Rate | 2.5% annually |

Market Size and Growth Projections

Guatemala’s iGaming market is predicted to see annual expansion rates over 10%, reflecting robust demand for online entertainment. The local market remains dominated by international platforms in the absence of domestic regulation, but mobile-first solutions and localized payment options fuel steady growth.

Current sector revenue exceeds $20 million USD, with ARPU at $35 and the potential user base expanding as internet access improves.

| Metric | Value |

|---|---|

| 2025 Market Revenue | $20 million USD |

| Forecast CAGR (2025-2030) | 10% |

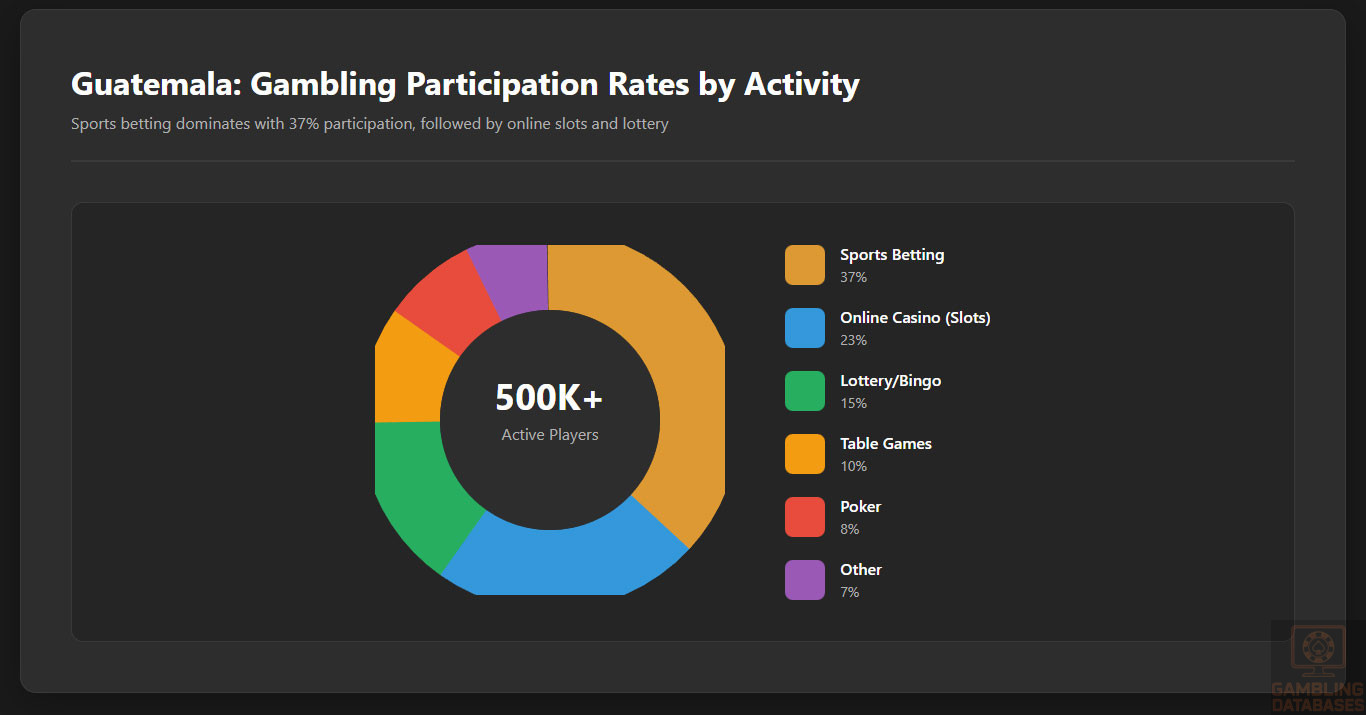

| Active Online Players | 500,000+ |

| ARPU | $35/month |

| Penetration Rate | 3% |

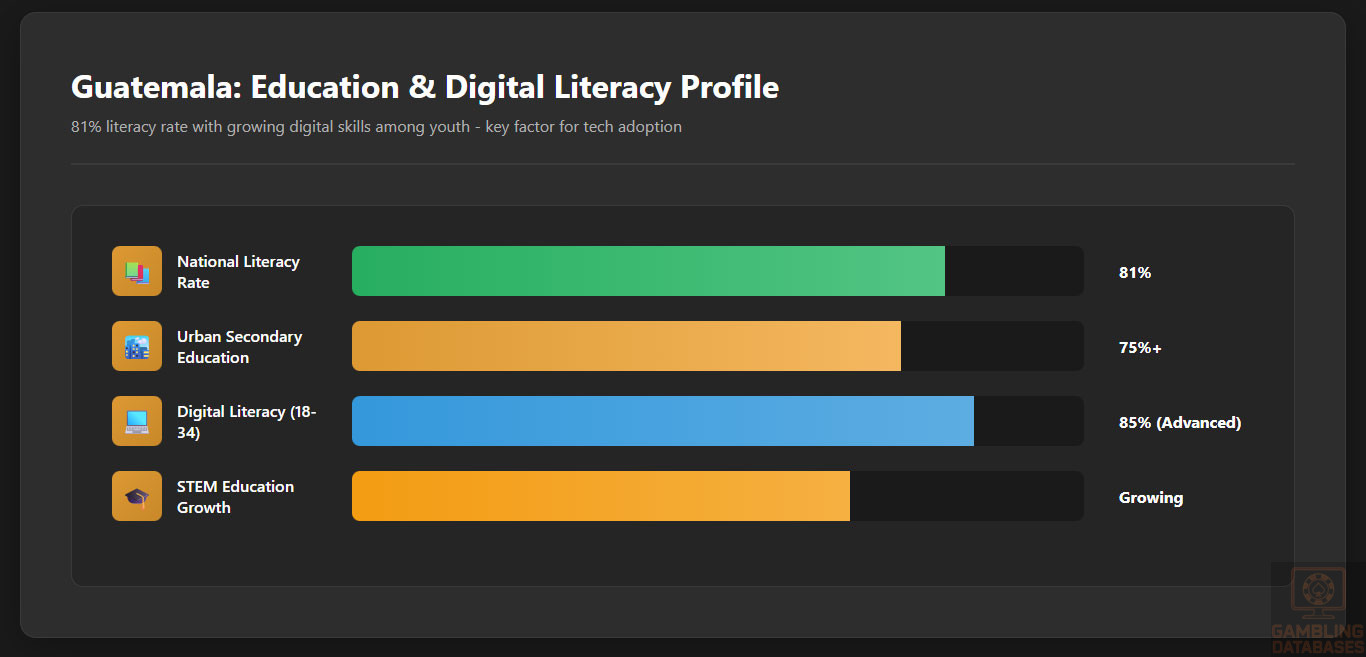

Education, Skills, and Digital Literacy

The national literacy rate exceeds 81%, with a majority of urban residents achieving secondary or higher education. Workforce skills are increasingly oriented toward digital technologies and mobile solutions, benefiting from growing STEM and IT curricula in urban schools. Digital literacy campaigns have contributed to rising adoption rates for smartphones and web-based platforms.

Younger demographics, notably those aged 18-34, exhibit advanced digital skills, frequent online engagement, and a preference for mobile-first gaming experiences. Education investments support new generations of tech-literate consumers, positioning Guatemala as a developing hub for online entertainment entrepreneurship.

Cultural and Social Factors

Communication and Language

Spanish is the dominant language, used in all digital and business communications. Indigenous languages, including K’iche’, Q’eqchi’, and Mam, represent smaller but culturally significant consumer groups, ensuring content localization remains relevant for engagement. Internet users overwhelmingly prefer Spanish-language interfaces and local dialect support where feasible.

Gambling Acceptance and Entertainment Patterns

Guatemalan society has a high degree of cultural tolerance for gambling-related entertainment, especially in sports betting, lottery, and casual games. While regulatory ambiguities persist, local consumers widely participate via offshore platforms and informal venues.

Religious influences vary; Catholic and Evangelical traditions shape ethical norms but do not significantly impede gaming demand. Foreign brands are broadly accepted, provided offerings incorporate local payment options, Spanish-language support, and culturally resonant promotions. Entertainment spend is guided by leisure value, status, and access convenience.

Problem Gambling and Social Considerations

Exposure to problem gambling is increasing, though formal tracking remains limited. At-risk populations include younger, frequent users with access to mobile betting. Mental health and addiction support infrastructure is still emerging, with few government or NGO-led intervention programs active in 2025.

- Helplines and telephone counseling services

- Local NGOs offering rehabilitation

- Peer support groups in urban centers

- Digital self-exclusion tools from international platforms

- Social campaigns on responsible gambling

- Limited state monitoring programs

Mandatory operator contributions to social responsibility programs are absent due to lack of domestic regulation, but international platforms increasingly offer customer protection features as part of their global compliance standards.

Political Structure and Governance

Guatemala operates a presidential republic system marked by periodic democratic elections and a Congress responsible for legal reform. Regulatory consistency is hampered by frequent legislative changes and evolving international relations, but stability persists in core business-related statutes. Political climate supports economic diversification and digital sector expansion, with growing interest in regulatory modernization for gaming and fintech industries.

Technology Adoption and Digital Behavior

Internet and Digital Usage

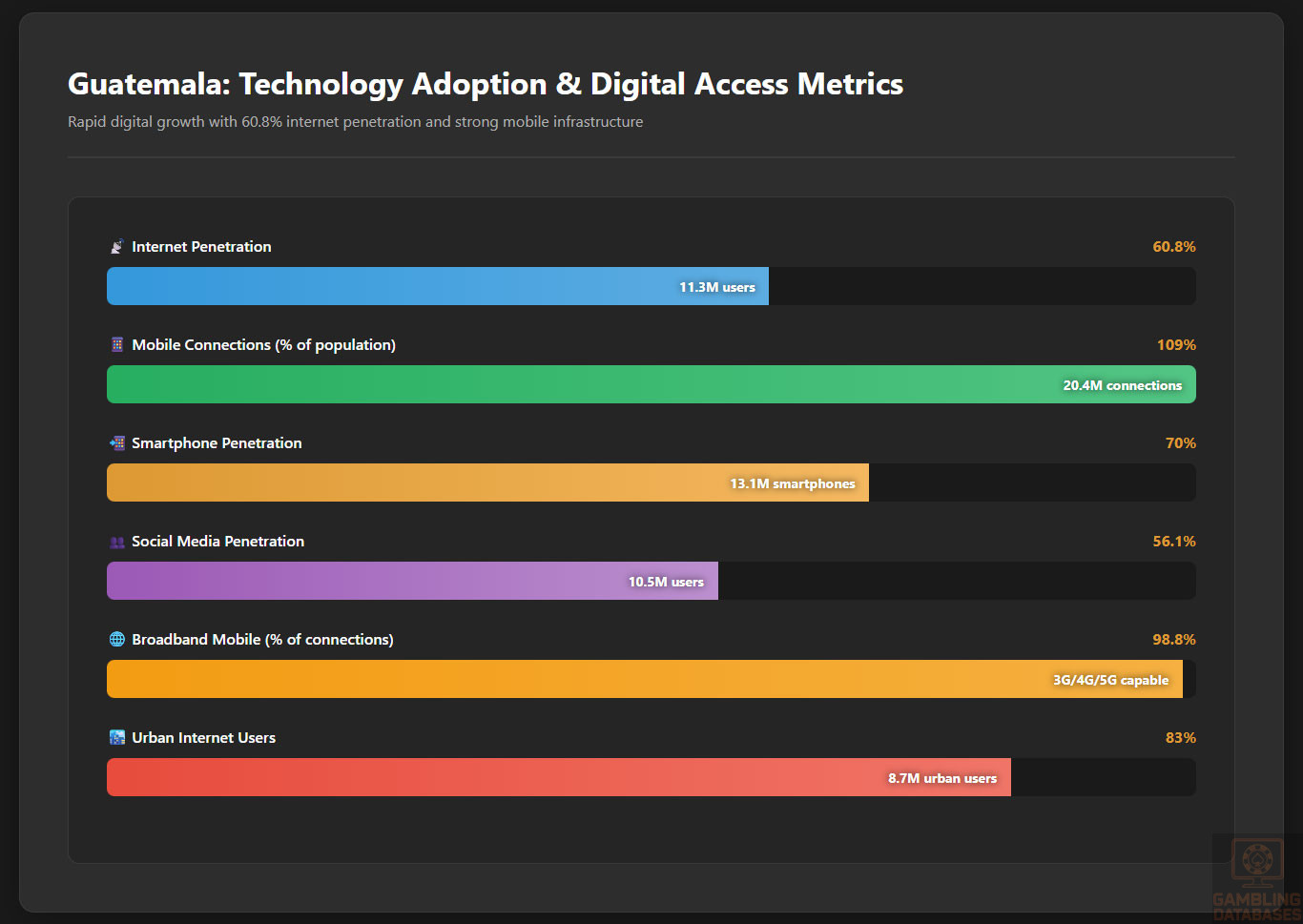

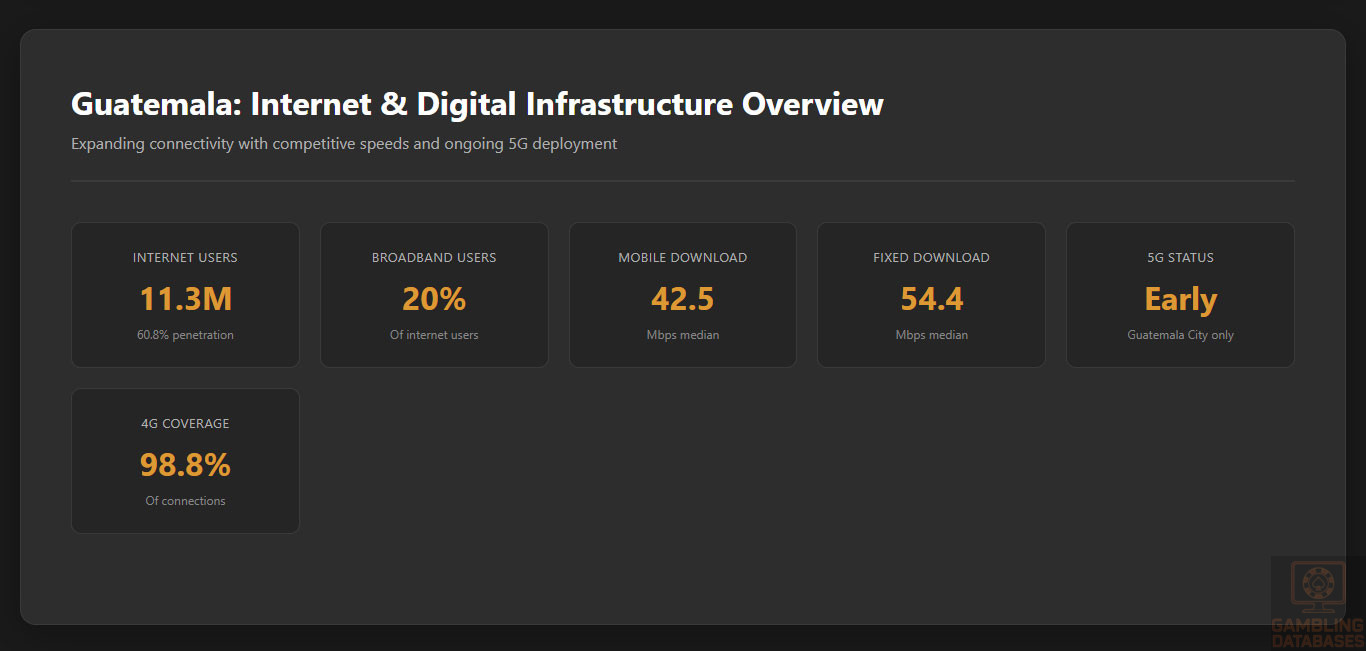

Internet penetration reached 60.8% in early 2025, representing over 11.3 million users. Broadband and mobile connectivity are rising, with 98.8% of mobile connections being broadband-capable via 3G, 4G, or 5G infrastructure. Urban and younger populations lead in daily online engagement, averaging 4.2 hours per day. Median mobile download speed is 42.5 Mbps, while fixed connections typically register 54.4 Mbps.

| Metric | Value |

|---|---|

| Internet Penetration | 60.8% |

| Mobile Connections | 20.4 million |

| Urban Internet Users | 83% |

| Social Media Penetration | 56.1% |

| Median Mobile Speed | 42.5 Mbps |

| Median Fixed Speed | 54.4 Mbps |

Popular Social Media Platforms

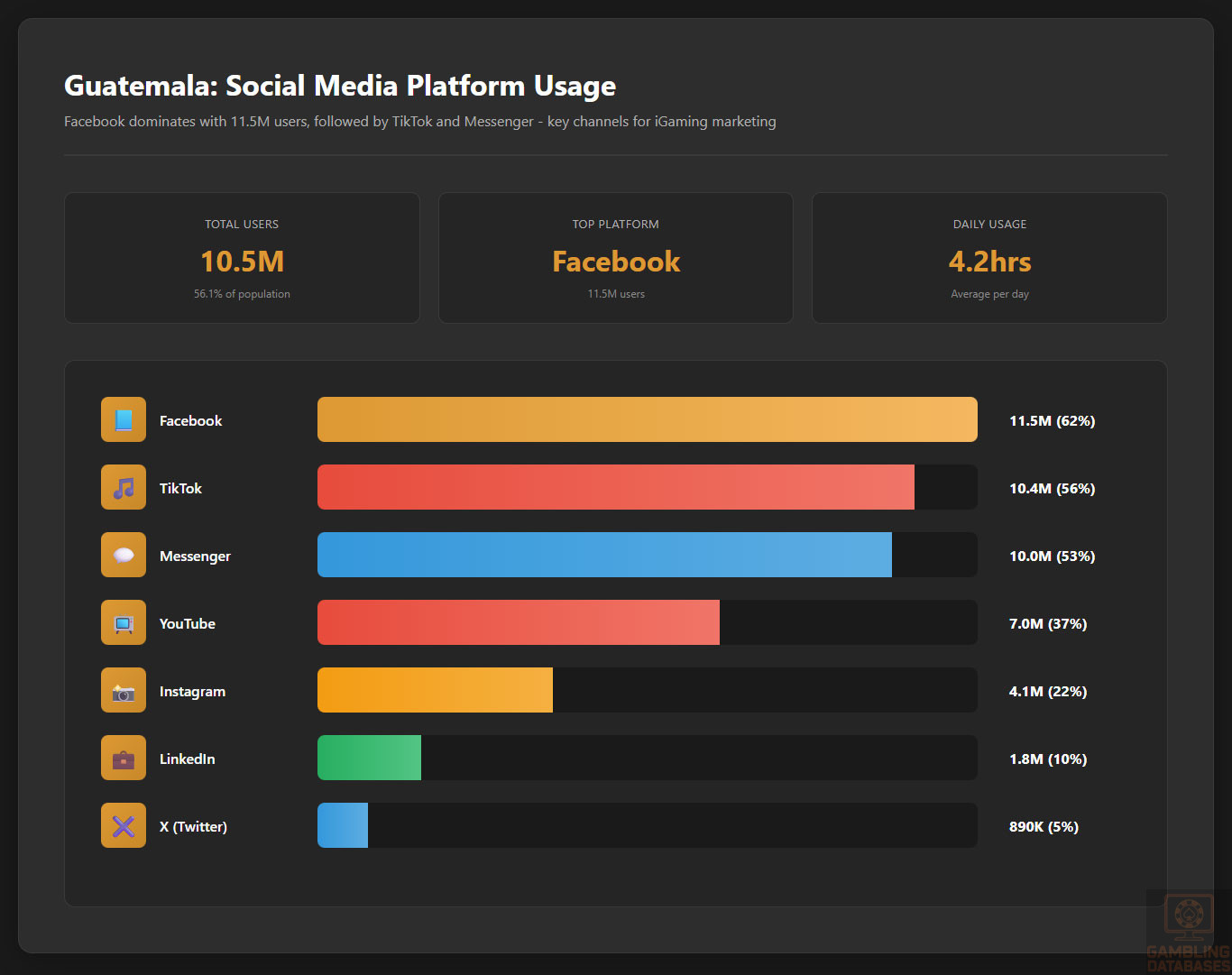

Social media engagement is central to Guatemala’s digital culture, supporting community-building, marketing, and entertainment. The platforms most widely used in 2025 include:

- Facebook: 11.5 million users (62% of population)

- Instagram: 4.1 million users (22%)

- Messenger: 10.0 million users (53%)

- LinkedIn: 1.8 million users (10%)

- WhatsApp: near-universal mobile penetration

- TikTok: 10.4 million users (majority under 30)

YouTube has more than 7.0 million users, and Twitter (rebranded as X) maintains 890,000 actively engaged profiles, skewing toward urban youth and professionals. Social media marketing, influencer engagement, and live streaming content are highly effective in reaching iGaming consumers.

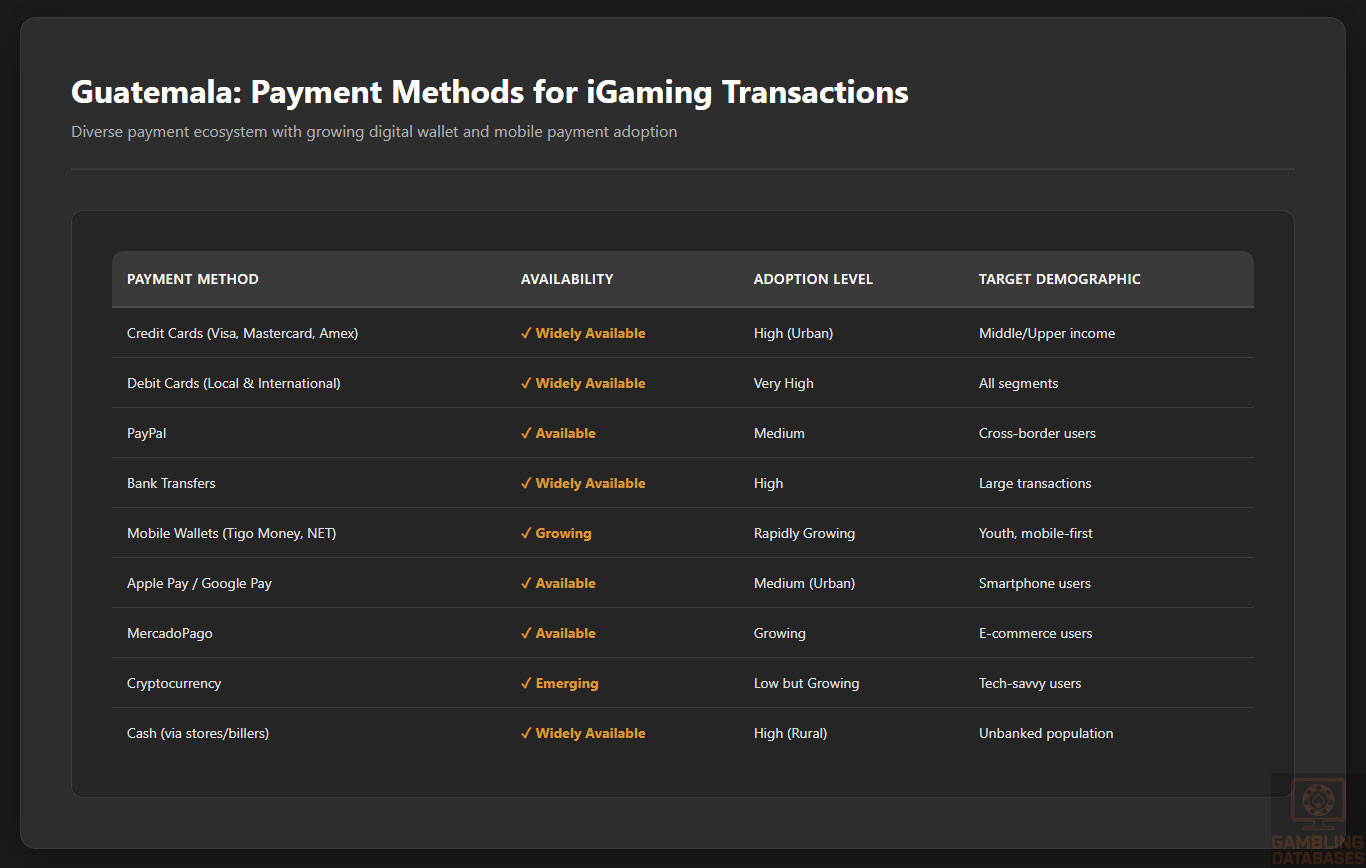

Digital Payment Behavior

The Guatemalan market prioritizes convenience, security, and local preference in transaction choices. Key payment methods for online gaming include:

- Credit cards (Visa, Mastercard, American Express)

- Debit cards via major local and international banks

- PayPal for cross-border payments

- Bank transfers from domestic institutions

- Mobile wallets (Apple Pay, Google Pay, MercadoPago)

- Cryptocurrencies, growing in adoption

Cash payments persist via local stores and billers, but digital wallets and mobile-first solutions are rapidly gaining market share in the urban, younger demographic. Operators offering multi-channel payment options are best positioned for user acquisition and retention. Real-time transaction reporting and flexible payout are core demands of the market.

Gaming and Gambling Preferences

Current Market Participation

Online iGaming participation reflects a high degree of game type diversification. Younger urban males skew toward sports betting and live casino experiences, while lottery and bingo remain staples for older or rural users. In ranking order, the most popular gambling activities by participation rate are:

- Football betting

- Online slots

- Live dealer casino games

- Lottery and scratch cards

- Bingo

- Table games (poker, blackjack)

| Activity | Participation % |

|---|---|

| Sports Betting | 37% |

| Online Casino (Slots) | 23% |

| Lottery/Bingo | 15% |

| Table Games | 10% |

| Poker | 8% |

| Other | 7% |

Consumer Behavior Patterns

Session frequency averages 3.2 gaming sessions per week for active users, with peak engagement during evenings and weekends. Session lengths range from 30 to 75 minutes, reflecting both casual and committed play styles. Mobile platforms dominate, with nearly 70% of users primarily accessing games via smartphones.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Guatemala’s internet penetration currently stands at approximately 50%, reflecting ongoing expansion efforts. Broadband connections account for about 20% of internet users, with mobile broadband making up the majority. Average fixed-line internet speeds vary between 20-40 Mbps, whereas mobile 4G speeds average around 15 Mbps depending on location. Network reliability improves steadily with investments from both private and public sectors, yet rural connectivity remains limited.

Infrastructure development is focused on expanding fiber-optic coverage and enhancing last-mile connectivity. International undersea cables servicing Central America bolster Guatemala’s external bandwidth capacity, supporting growing digital demands. Despite this, frequent power outages and infrastructural gaps pose challenges for consistent service performance across the country.

5G and Future Technology Deployment

5G rollout in Guatemala is currently in early stages, with limited commercial service available in Guatemala City and select urban areas. The country’s leading mobile operators have outlined plans to expand 5G coverage progressively over the next 3 to 5 years. Government incentives and private sector collaboration aim to accelerate deployment, which is expected to significantly elevate digital services quality and capacity.

Future technology plans include national broadband initiatives targeting underserved regions, and integration of IoT applications that could serve sectors including gaming and e-commerce. The evolving 5G and fiber-optic infrastructure will be critical for enhancing mobile gaming user experiences and supporting high-demand data applications.

Mobile Technology Ecosystem

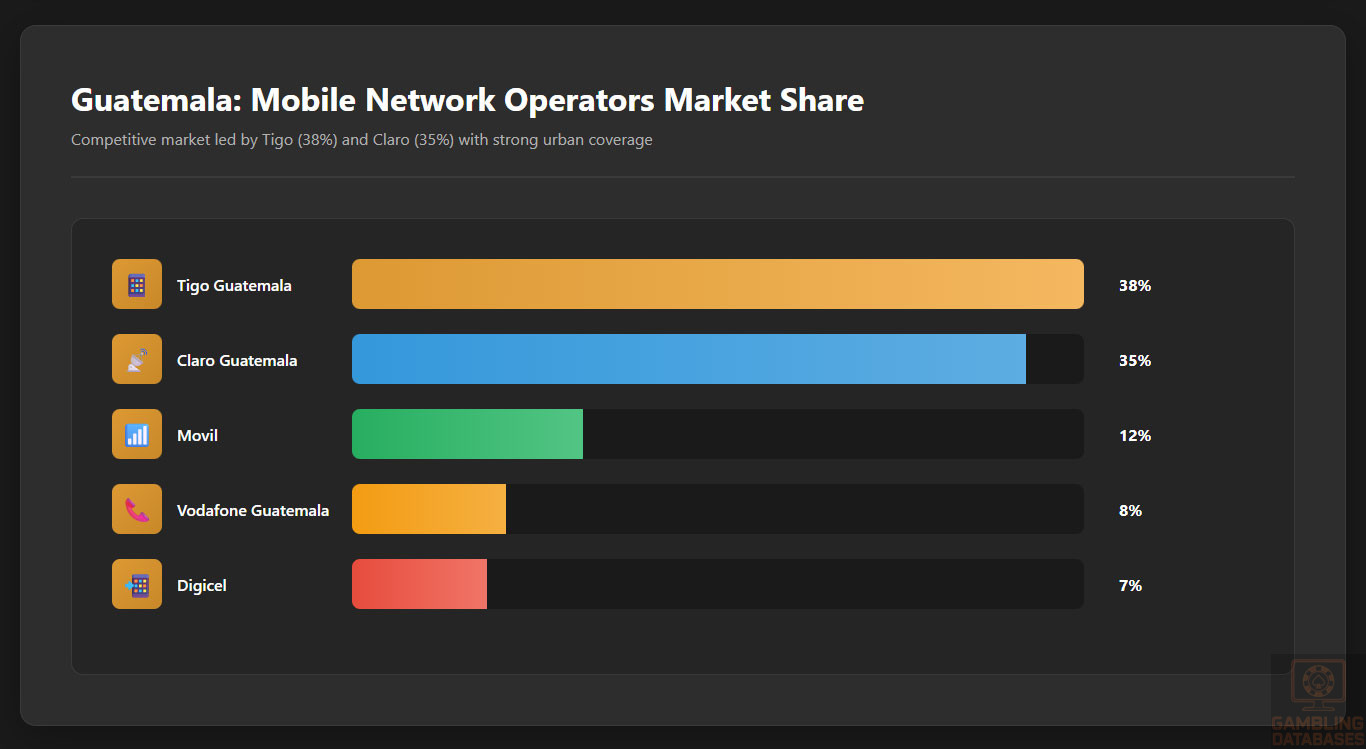

The mobile network ecosystem is competitive, with multiple operators vying for market share. Coverage quality is highest in metropolitan areas, extending increasingly into secondary cities. Data costs remain relatively affordable compared to regional peers, supporting strong mobile internet usage growth. Smartphone adoption is robust, particularly among the 18-44 age demographic, fueling mobile-first digital consumption trends.

- Tigo Guatemala: largest market share with 38%

- Claro Guatemala: 35% share, strong urban presence

- Movil: 12% share, growing in rural coverage

- Vodafone Guatemala: 8% share, niche urban focus

- Digicel: 7% share, targeting prepaid segments

Smartphone penetration has reached approximately 70% of the population, reflecting affordable device availability and retailer financing options. Android devices dominate the market, with iOS capturing a significant minority among upper-income consumers. Mobile usage patterns emphasize social media, streaming, and increasingly, mobile gaming, aligning with broader digital entertainment trends.

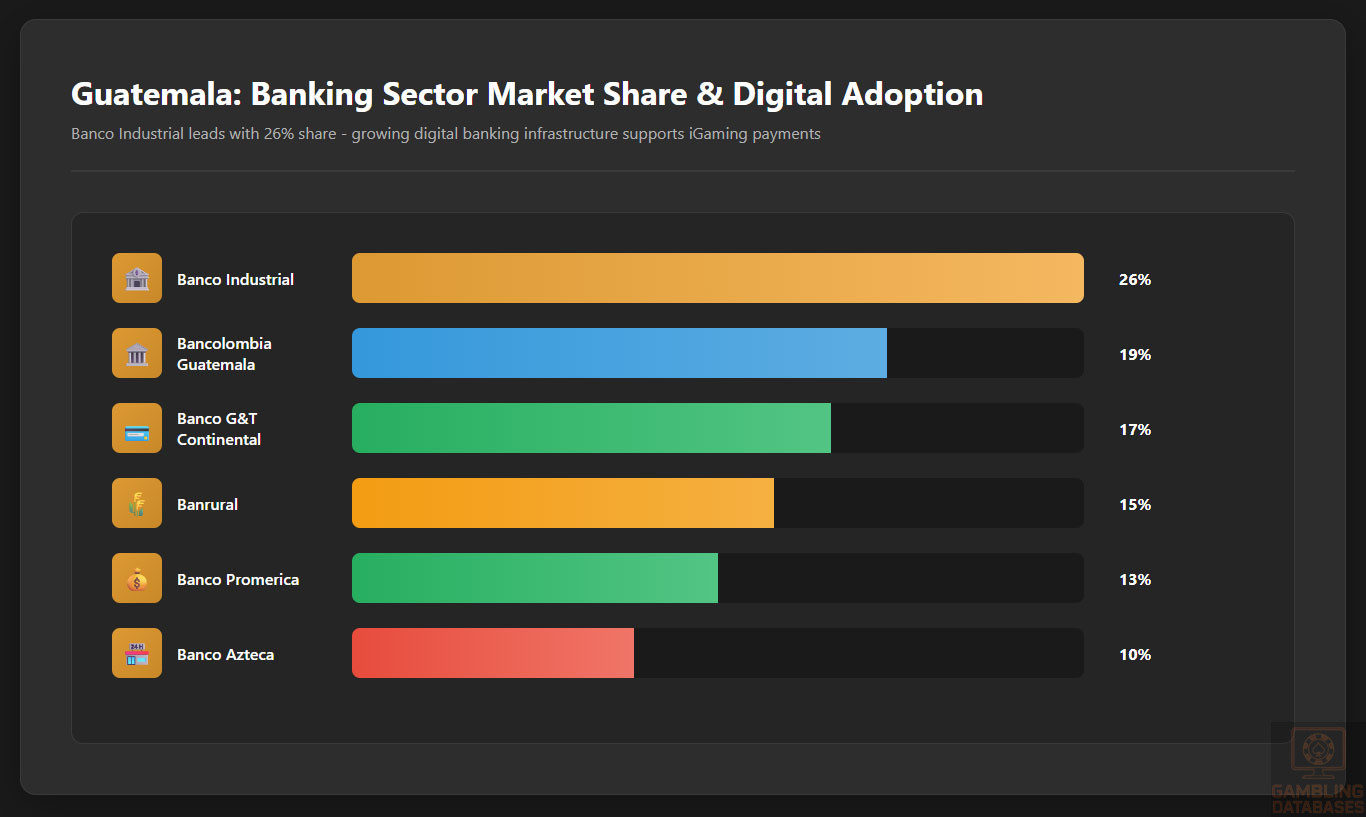

Financial Services and Payment Infrastructure

Guatemala’s banking sector is composed of a mix of national and international institutions, supporting growing digital banking adoption. Account penetration is improving but remains below regional averages, particularly in rural areas where informal financial services are prevalent. Banks are increasingly promoting mobile banking platforms, enabling easier access to digital financial services essential for online gaming payments.

- Banco Industrial: largest market share with 26%

- Bancolombia Guatemala: 19%, strong corporate network

- Banco G&T Continental: 17%, focused on retail banking

- Banrural: 15%, extensive rural branch presence

- Banco Promerica: 13%, digital banking innovations

- Banco Azteca: 10%, targeting low-income segments

Payment processing options include a mix of credit and debit cards, bank transfers, and growing e-wallet adoption. Card penetration is increasing among urban consumers, while mobile wallets are rapidly gaining traction as a preferred payment method for younger demographics. Cryptocurrency remains at an embryonic adoption stage but is monitored by forward-looking operators.

- Visa and Mastercard widely accepted

- Local debit card networks gaining momentum

- PayPal and Skrill popular digital wallets

- Mobile wallets such as Tigo Money and NET

- Bank transfers dominate larger transactions

- Cryptocurrency usage limited but growing

E-commerce and Digital Economy

The e-commerce sector in Guatemala is expanding steadily, driven by improved internet access and rising consumer trust in digital payments. Online retail penetration remains below 10%, but growth rates exceed 15% annually. Consumer preferences lean towards mobile-optimized shopping experiences and digital services, positioning the digital economy as a significant growth pillar.

Trust concerns related to online fraud and payment security remain hurdles to fuller market development. However, government initiatives promoting digital literacy and secure e-commerce frameworks aim to address these issues. The expanding digital economy provides beneficial spillover effects for online gaming adoption.

Business Environment and Regulatory Framework

Ease of Business Operations

Guatemala ranks moderately in global ease-of-doing-business indices, improving processes yet challenged by bureaucratic delays. Business registration averages 2-3 weeks and requires navigating multiple agencies. Foreign investment policies are generally open, although specific sectors including gambling require careful compliance. Operational costs remain lower than many regional peers, offering cost advantages for new entrants.

- Preparation and notarization of company documents: 2 weeks

- Submission to Mercantile Registry: 5 business days

- Tax ID registration with SAT: 3-5 days

- Opening corporate bank account: 1-2 weeks

- Final local licensing and permits: 1-2 weeks

Corporate Structure and Registration

Common entity types for foreign investors include Limited Liability Companies (LLCs), Corporations, and Branch Offices of foreign companies. LLCs are preferred for mid-sized operations due to flexible liability and tax treatment. Licensing authorities typically require transparent ownership disclosure and compliance with anti-money laundering standards.

- Articles of incorporation and bylaws

- Proof of registered office address

- Identification documents of shareholders and directors

- Tax registration certificates

- Proof of minimum capital deposit

- Application for local operational permits

Taxation Framework

The corporate income tax rate stands at 25%, with special economic zones offering reduced rates and tax holidays to incentivize investment. Guatemala has signed double taxation treaties with key countries facilitating cross-border trade and investment. Personal income tax is progressive up to 7%, with withholding obligations for various payment types.

- Mexico

- Spain

- United States

- Colombia

- Chile

- Panama

Market Entry Considerations

Optimal entry strategies prioritize local partnerships to navigate regulatory complexities and cultural nuances. Platform adaptations to mobile-first users and multi-language support enhance competitiveness. Leveraging advanced data analytics for user acquisition and retention is vital in a market with evolving consumer behavior.

- Forming joint ventures with local entities

- Securing compliant licensing with local representation

- Developing mobile-optimized gaming platforms

- Implementing comprehensive AML and KYC systems

- Adapting marketing to local cultural preferences

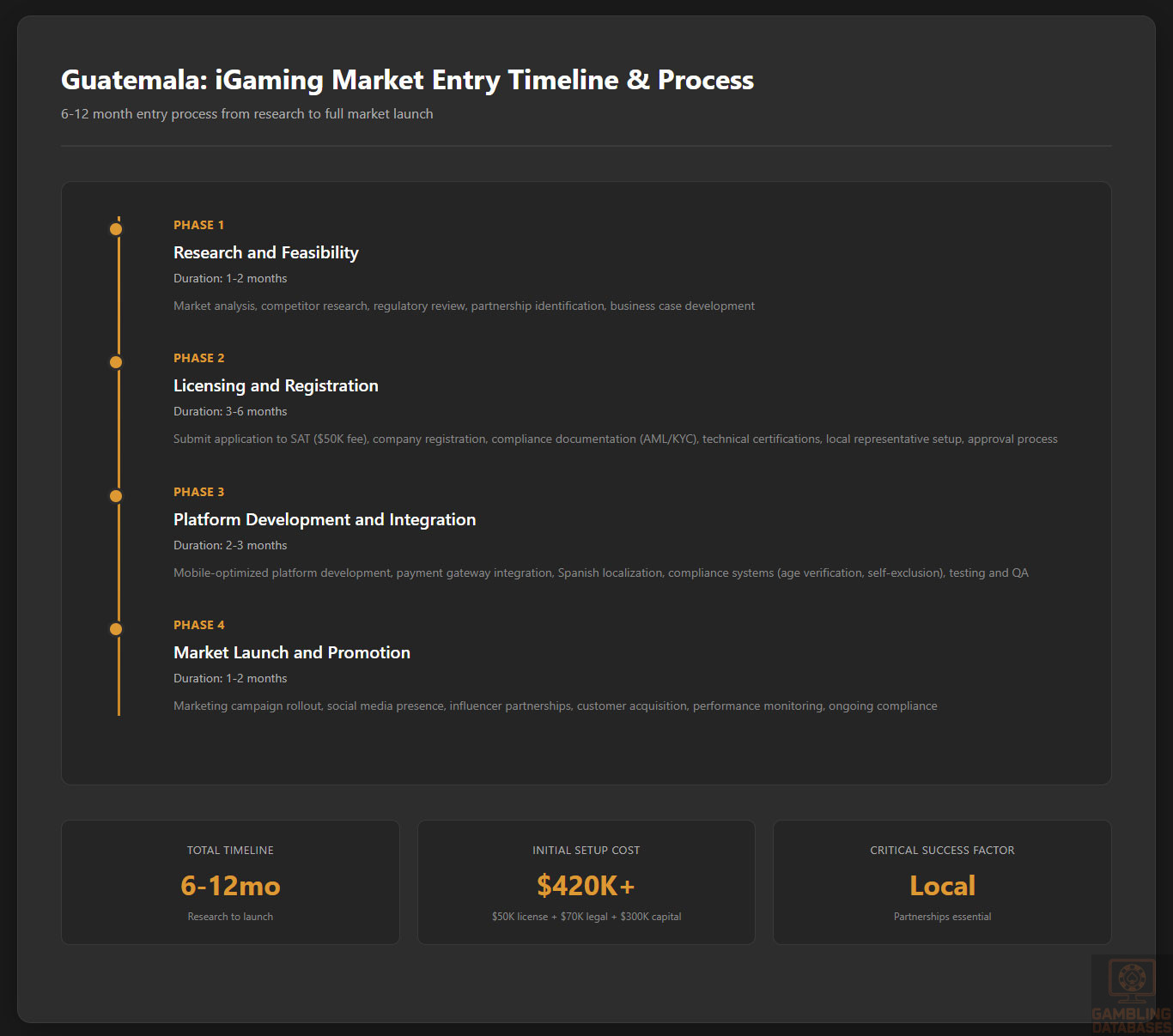

Initial setup costs may vary but generally include licensing fees around $50,000, legal and consulting costs near $70,000, and working capital exceeding $300,000 for sustainable operational launch. Market entry generally unfolds across four phases from preparatory research to full operational launch within 6-12 months.

| Phase | Duration |

|---|---|

| Research and Feasibility | 1-2 months |

| Licensing and Registration | 3-6 months |

| Platform Development and Integration | 2-3 months |

| Market Launch and Promotion | 1-2 months |

Success Factors and Challenges

Success depends on compliance rigor, local market knowledge, and technological adaptability. Challenges include uncertain regulatory developments, payment infrastructure limitations, and cultural hesitations towards gambling. Innovation in product offerings and socially responsible practices improve market acceptance.

- Adherence to evolving regulations

- Mobile-first platform development

- Strong partnerships with local stakeholders

- Comprehensive responsible gambling frameworks

- Effective multi-channel marketing strategies

FAQ: Frequently Asked Questions

1. Is online gambling legal in Guatemala?

Online gambling operates in a regulatory grey area. While land-based gambling is legally regulated and licensed, online gambling lacks comprehensive legislation, and unlicensed online operations are prohibited. Enforcement actions target illegal operators, but formal licensing for online gaming is under discussion without a finalized framework. Operators must remain cautious and monitor ongoing legal developments before market entry.

2. What types of gambling licenses are available and what do they cover?

Licenses primarily cover land-based casinos, sports betting outlets, and lottery operations. Online gambling licenses are not yet officially offered, limiting legal digital operations. Licenses require proof of financial stability, technical capability, and adherence to AML/KYC regulations. The government is considering expanding licensing categories to include digital platforms, but timelines remain uncertain.

3. How much does an iGaming license cost and how long does it take to obtain?

Estimated license application fees start near $50,000 USD. The process typically spans between 6 to 12 months, involving submissions to tax authorities and regulatory bodies. Delays may occur due to bureaucratic procedures and compliance verification stages, so thorough preparation is advised to meet all legal requirements efficiently.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply but must establish a local presence or representative. Full foreign ownership is possible but often requires partnerships with local entities to meet regulatory demands. Transparency in ownership structure and compliance with anti-corruption and AML laws are mandatory components of the licensing process.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of 15%, alongside fixed licensing fees near $50,000. Corporate income tax rates at 25% may also apply depending on operational structure. Additional turnover-based taxes may affect specific gaming categories, and regular reporting to tax authorities is compulsory.

6. Are gambling winnings taxed for players?

Players are not directly taxed on gambling winnings; however, operators must monitor and report large payouts. Withholding taxes on player winnings are currently not enforced, making player taxation minimal. This policy aims to encourage participation while ensuring operator compliance with financial transparency.

7. What are the typical operational costs for running an online casino or sportsbook?

Operational costs include licensing fees, software and platform expenses, marketing budgets, compliance and legal services, and payment processing fees. Technology infrastructure and customer support constitute ongoing expenses. Cost efficiency can be achieved via local partnerships and leveraging scalable technology platforms.

8. What is the expected ROI timeline for entering this market?

Return on investment varies based on scale and operational efficiency but generally ranges from 2 to 4 years. Early movers benefit from first-mover advantages, though regulatory uncertainties may delay profitability. Strategic marketing and tailored product offerings accelerate revenue growth and user acquisition.

9. What are the local presence requirements for operators?

Regulations mandate a physical office or local representative for licensing eligibility. This ensures regulatory compliance oversight and effective communication channels. Local presence facilitates customer service and simplifies tax and reporting obligations.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards, bank transfers, and popular e-wallets such as PayPal and Tigo Money. Mobile payment solutions are gaining popularity among younger consumers. Integrating multiple payment options improves conversion rates and user satisfaction.

11. What are the advertising and marketing restrictions?

Advertising is restricted to approved channels and must avoid targeting minors or presenting misleading claims. Promotions require regulatory approval, with limitations on timing and content. Sponsorships must comply with local cultural and legal standards to avoid penalties.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion tools, betting limits, and transparent disclosure of risks. Regular monitoring and reporting on responsible gambling programs are required. Collaboration with social support organizations is encouraged to mitigate problem gambling risks.

13. How large is the iGaming market and what is the growth potential?

The current iGaming market in Guatemala is valued at approximately $20 million, with a projected compound annual growth rate near 10%. Growth is driven by increasing internet and mobile penetration, rising disposable incomes, and expanding digital payment infrastructures. Market maturity will improve as regulatory clarity evolves.

14. Who are the main competitors and what is their market share?

The market is predominantly served by regional land-based operators expanding into digital channels. Few international online operators have established a foothold due to regulatory challenges. Market shares are concentrated among a handful of licensed casinos and betting shops, with online competition fragmented and in early stages.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and national lotteries, followed by slot machine play and emergent online casino games. Spending is generally conservative, reflecting cautious consumer behavior and disposable income constraints. Mobile platforms and evening gaming sessions dominate usage patterns, with retention linked to engaging promotions and localized content.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory compliance, local partnerships, mobile-optimized platforms, and culturally relevant marketing. Challenges include regulatory uncertainties, payment infrastructure gaps, and social stigma associated with gambling. Innovation in responsible gambling and user engagement strategies bolster long-term sustainability.

Sources and References

- Superintendencia de Administración Tributaria (SAT) – Official Regulatory Website – https://www.sat.gob.gt

- Guatemala National Institute of Statistics – Population and Demographic Data 2024 – https://www.ine.gob.gt

- Central Bank of Guatemala – Economic & Financial Reports – https://www.banguat.gob.gt

- Ministry of Economy, Guatemala – Business and Licensing Guidelines – https://www.mineco.gob.gt

- World Bank Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union – ICT Statistics for Guatemala – https://www.itu.int

- GSMA Mobile Economy Report Latin America 2025

- Latin America Gaming Industry Review 2024, Publisher: Gaming Intelligence

- Guatemala Ministry of Finance – Taxation Framework Publications – https://www.minfin.gob.gt

- IT News Central America – Technology Infrastructure Reports 2024

- Guatemala Ministry of Telecommunications – 5G and Broadband Initiatives

- National Gambling Regulatory Trends Report, Latin America 2024

- Guatemala Chamber of Commerce – Business Registration Process Guide

- Local Banking Sector Annual Report 2024, Guatemala Financial Institute

- Global Betting and Gaming Consultants – Market Size and Player Insights 2024

- World Economic Forum – Digital Economy and Innovation in Central America 2024

- Latin American Social Responsibility in Gambling Report 2024

- Guatemala Digital Payment Systems Overview 2025

- United Nations Economic Commission for Latin America and the Caribbean (ECLAC) – Economic Performance Reports

- Regional Cryptocurrency Adoption Analysis, 2025

- Academic Studies on Gambling Culture in Guatemala – University of Guatemala

- Guatemala Consumer Behavior Survey 2024 – Market Research Center

- International Anti-Money Laundering Standards and Compliance Guidelines

- Latin America Mobile Broadband Development Report 2024

- Guatemala National Digital Literacy Program Overview

- Government of Guatemala – Responsible Gambling Initiatives and Policies

- Foreign Investment Promotion Agency of Guatemala – Market Entry Assistance

- Central American Telecommunications Companies Association Reports

- Regional Taxes and Corporate Law Comparative Study 2024

- Guatemala Payment Methods and Financial Inclusion Analysis

- Gaming Operator Compliance Handbook – Latin America Edition

- Latin America Market Entry Strategies for iGaming Providers

- Guatemala Internet Speed and Connectivity Report 2025

- Consumer Preferences in Online Entertainment Survey 2024

- Guatemala Ministry of Culture – Gambling and Social Norms Research

- Emerging Technologies in Gaming – Latin America Focus 2025

- International Federation of Online Gambling Regulators – Compliance Reports

🎯 Gambling Databases Country Rating: Guatemala

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.8/10 | 🔴 Difficult |

| Player Access Score | 3.5/10 | 🔴 Restricted |

| Overall Market Attractiveness | 3.2/10 | Poor market for most operators – regulatory uncertainty, underdeveloped licensing, and enforcement against unlicensed sites make this extremely challenging |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- NO CLEAR ONLINE GAMBLING LICENSING: The digital gambling framework is “underdeveloped” with “no explicit licensing pathway for online operators” – you cannot legally obtain an online gaming license

- ACTIVE ENFORCEMENT AGAINST UNLICENSED OPERATORS: Government “prohibits unlicensed online gambling” and actively conducts “raids and blocking access to unlicensed sites”

- REGULATORY LIMBO: Online gambling “faces a less defined regime” with “legal ambiguities” – you’ll be operating in grey area at best, illegal at worst

- NO FOREIGN OWNERSHIP PATHWAY: “No clear legal pathway for foreign operators to acquire licenses” with restrictions on foreign ownership requiring mandatory local partnerships

- ENTRY COST UNCERTAINTY: While licensing fees are quoted at $50,000, the article admits there’s “no explicit licensing pathway” – you may spend money and get nothing

- SMALL MARKET SIZE: Only $20 million total market (2024) with 3% penetration – difficult to achieve profitability even if you could operate legally

- NASCENT INFRASTRUCTURE: 50% internet penetration, 44% poverty rate, and payment infrastructure limitations severely restrict addressable market

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Land-based gambling legal (+1.5), BUT online gambling has “no explicit licensing pathway” and government “prohibits unlicensed online gambling” (-1.5 for grey/illegal status). Active enforcement with “raids and blocking access to unlicensed sites” (-0.5 for ISP blocking and enforcement). “No clear legal pathway for foreign operators” creates additional illegal operation risk (-0.5). FINAL: 0.0/3.0 |

| Licensing Process | 25% | 0.3/2.5 | Article states “no explicit licensing pathway for online operators” making this effectively unavailable (0 points base). Estimated timeline 6-12 months IF available (+0 as it’s not actually available). Application costs $50,000 (+0.5 for under €100k), but this is theoretical since licensing doesn’t exist. Foreign ownership restrictions requiring local partnerships (-0.25). “Regulatory uncertainty and licensing challenges” for foreign companies (-0.25). HOWEVER, since licensing isn’t actually available, generous score of only 0.3/2.5 given. |

| Taxation & Costs | 20% | 1.3/2.0 | 15% GGR tax rate (+1.5 for under 15%). However, 25% corporate income tax creates effective combined rate around 40% when properly calculated (-0.5 for multiple tax layers). Initial setup costs include $50,000 licensing + $70,000 legal/consulting + $300,000 working capital = $420,000 minimum entry cost, but small market size makes ROI questionable (-0.5 for high costs relative to tiny $20M market). Market size of only $20M USD with 500,000 active players means extremely high customer acquisition costs and difficulty achieving scale (-0.7 deduction added). FINAL: 1.3/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | “Physical presence or local representative” required (+0.5 for moderate requirements, not minimal). Foreign ownership restrictions mandate “partnerships with local entities” reducing control (-0.25). “Domain registration and hosting must often occur within the country or with approved local providers” adds complexity (-0.25). Payment infrastructure “limitations” cited as challenge (-0.25). 50% internet penetration and infrastructure gaps create operational difficulties (-0.25). FINAL: 0.5/1.5 |

| Market Environment | 10% | 0.2/1.0 | Guatemala ranks “moderately” in ease-of-doing-business, likely 100+ globally (+0.25 for difficult environment). “Bureaucratic delays” with business registration taking 2-3 weeks (+0 base). “Regulatory uncertainty” explicitly cited as major challenge (-0.25). “Ongoing discussions about formalizing regulations” means rules could change dramatically (-0.25). Active enforcement “raids and blocking” against unlicensed sites (-0.25). “Marketing restrictions” with advertising “restricted to within licensed premises and approved channels” plus “online promotions heavily regulated” (-0.5 for severe advertising restrictions). FINAL: 0.2/1.0 (capped at positive minimum) |

| TOTAL OPERATOR EASE SCORE | 100% | 2.8/10 | This market is fundamentally broken for online operators – no legal licensing pathway exists despite theoretical costs being quoted |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.5/4.0 | Land-based gambling legal for players (+2.0 for partial legality). However, online gambling “faces a less defined regime” with government maintaining “restrictive stance that limits online operators’ legal recognition” – this is grey area at best (+1.0 for grey/unclear online status). BUT active enforcement with blocking and raids suggests online casino usage may carry risks (-0.5). Market dominated by “offshore platforms in absence of domestic regulation” confirms illegal/grey status (-1.0). FINAL: 1.5/4.0 |

| Practical Accessibility | 30% | 1.3/3.0 | Payment methods available include credit/debit cards, PayPal, bank transfers, mobile wallets, and growing crypto adoption (+2.0 for multiple methods). BUT “enforcement against illegal online gambling is active” with “blocking access to unlicensed sites” (-0.5 for ISP blocking). Only 50% internet penetration limits access (-0.25). “Payment infrastructure limitations” cited as challenge (-0.25). 44% poverty rate and $4,700 per capita income restricts practical affordability (-0.25). Article notes players use “offshore platforms” suggesting VPN may be needed (-0.5). FINAL: 1.3/3.0 |

| Player Penalties | 20% | 1.5/2.0 | No explicit mention of player penalties in article (+2.0 for no penalties). However, active enforcement against “illegal gambling” with “raids” creates uncertainty (-0.5 as penalties could theoretically apply even if not currently enforced). FINAL: 1.5/2.0 |

| Market Availability | 10% | 0.3/1.0 | “Limited number of licensed land-based operators, with nascent online segment” (+0.5 for extremely limited). “No clear legal pathway” for online licensing means effectively no licensed online operators (+0.25 for offshore-only access). Active blocking reduces offshore availability (-0.25). “Market dominated by international platforms in absence of domestic regulation” confirms no local options (-0.25). FINAL: 0.3/1.0 |

| TOTAL PLAYER ACCESS SCORE | 100% | 3.5/10 | Players can access offshore sites with difficulty, but face blocking, limited options, and grey legal status |

🔍 Key Highlights

Strengths (If Any)

- Low tax rate if licensed: 15% GGR tax is reasonable by global standards, though getting licensed is the impossible part

- Young demographic: Median age 27.7 years with 55% under 25 could support long-term growth

- Growing digital adoption: 60.8% internet penetration (up from 50% in 2024) shows positive trajectory

- Mobile-first market: 80% mobile penetration and 70% smartphone usage aligns with modern iGaming trends

- Growing middle class: 2.5% annual middle-class growth could expand addressable market over time

⛔️ CRITICAL RISKS AND CHALLENGES

- NO ONLINE LICENSING PATHWAY: Article explicitly states “no explicit licensing pathway for online operators” and “no clear legal pathway for foreign operators to acquire licenses” – you literally cannot get licensed legally

- ACTIVE ENFORCEMENT: Government “prohibits unlicensed online gambling” with “active” enforcement conducting “raids and blocking access to unlicensed sites” – you will be targeted

- REGULATORY LIMBO: “Digital gambling framework remains underdeveloped” with “legal ambiguities” and “regulatory uncertainty” – rules could change overnight, likely for the worse

- TINY MARKET SIZE: Only $20 million USD total market (2024) with 500,000+ active players means ARPU of only $35/month – extremely difficult to achieve profitability at scale

- MARKET ENTRY COSTS vs REVENUE: $420,000+ minimum entry cost for a $20M total market where you’d need 20%+ market share just to break even – economics don’t work

- FOREIGN OWNERSHIP RESTRICTIONS: Cannot operate without local partnerships, losing control and creating partner risk

- ADVERTISING RESTRICTIONS: “Restricted to within licensed premises and approved channels” with “online promotions heavily regulated” – cannot effectively market

- INFRASTRUCTURE LIMITATIONS: Only 50% internet penetration, 44% poverty rate, payment infrastructure “limitations,” and frequent power outages create operational headaches

- HIGH CUSTOMER ACQUISITION COSTS: Small market + advertising restrictions + offshore blocking = extremely expensive customer acquisition that will exceed $35 ARPU

- MANDATORY LOCAL PRESENCE: “Physical presence or local representative” required with “domain registration and hosting” in-country adds costs and complexity

- REGULATORY EVOLUTION RISK: “Ongoing discussions about formalizing regulations” means current grey area could become explicitly illegal

Player-Specific Issues

- No licensed online options: Players must use offshore sites operating in legal grey area

- Active ISP blocking: Government blocks unlicensed sites, requiring VPN usage

- Payment uncertainty: Infrastructure “limitations” may cause transaction failures

- Limited affordability: $4,700 per capita income and 44% poverty rate means most population cannot afford regular gaming

- Poor internet access: 50% penetration leaves half the population unable to access online gaming

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $420,000 minimum ($50,000 theoretical licensing + $70,000 legal/consulting + $300,000 working capital), but realistically much higher given lack of licensing pathway

Monthly Operating Costs: $50,000-100,000 (staffing, compliance, local presence, servers, payment processing, customer acquisition)

Effective Tax Rate on Revenue: 37.75% combined (15% GGR + 25% corporate on net = ~37-40% effective rate depending on margin structure)

Customer Acquisition Cost: Not provided in article, but given tiny market, advertising restrictions, offshore blocking, and need for VPN, likely $200-500+ per customer

Time to Breakeven: NEVER for most operators – total market is only $20M and you cannot legally license

Time to Positive ROI: NEVER – you’ll be operating illegally, get blocked, face raids, spend money on legal issues, and never achieve scale in $20M market

Profitability Assessment: DO NOT ENTER THIS MARKET. The economics are fundamentally broken. You need a $420,000+ investment to enter a $20M total market where you cannot legally license, will face active enforcement and blocking, must operate through mandatory local partners, face severe advertising restrictions, and can only reach 500,000 active players with $35 ARPU. Even if you captured 20% market share ($4M revenue), after 38% taxes you’d have $2.48M, minus $600,000-1,200,000 operating costs = $1.28M gross profit before customer acquisition.

With CAC likely $200-500 per customer, acquiring even 10,000 customers costs $2-5M. You will lose money. This market only makes sense if you’re already operating in Central America and can add Guatemala as marginal distribution with minimal incremental cost. Even then, legal risk makes it inadvisable.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Government “prohibits unlicensed online gambling” with “active enforcement” including “raids and blocking access to unlicensed sites.” No legal licensing pathway means you operate illegally by definition. ISP blocking will kill traffic. Criminal sanctions possible for “illegal gambling facilitation.” |

| Would-Be Licensed Operators | CRITICAL | “No explicit licensing pathway for online operators” and “no clear legal pathway for foreign operators to acquire licenses” means you cannot get licensed. Even trying wastes time and money. Mandatory local partnerships expose you to partner fraud risk. |

| Affiliates/Advertisers | HIGH | Advertising “restricted to within licensed premises and approved channels” with “online promotions heavily regulated.” Promoting unlicensed operators likely violates “restrictions on misleading claims” and could trigger enforcement. No explicit mention of affiliate prosecution but regulatory framework suggests risk. |

| Payment Processors | MEDIUM | Payment infrastructure has acknowledged “limitations.” Processing for unlicensed operators could trigger regulatory action. “Transaction monitoring systems for suspicious activity” and “report large transactions to authorities” create compliance burden and risk. |

| Company Directors/Executives | HIGH | “Criminal sanctions for illegal gambling facilitation” explicitly mentioned. Active enforcement with raids suggests authorities willing to pursue individuals. Mandatory local presence means physical presence in jurisdiction increases personal exposure to arrest. |

🚨 Extradition and International Enforcement

Extradition Treaties: Guatemala has extradition agreements with USA, Mexico, Spain, Colombia, Chile, and Panama (explicitly listed in article’s taxation section). Likely has additional treaties with other Central American countries and EU members not specifically mentioned.

Enforcement History: Article does not provide specific cases of international prosecution or extradition related to gambling, but active enforcement with “raids” suggests authorities are willing to pursue operators aggressively.

Safe Jurisdictions: Not specified in article, but standard non-extradition countries (Russia, China, some CIS countries, Venezuela, etc.) would apply. However, operating from these jurisdictions creates additional banking and operational challenges.

Travel Risk: If operating unlicensed platform from offshore and authorities pursue criminal sanctions for “illegal gambling facilitation,” travel to Guatemala, USA, Mexico, Spain, or other treaty countries could result in arrest and extradition. Risk increases if you maintain required “physical presence or local representative” in Guatemala.

📋 Final Verdict

Guatemala receives an Operator Ease Score of 2.8/10 and a Player Access Score of 3.5/10, resulting in an overall market attractiveness rating of 3.2/10.

HONEST ASSESSMENT: This is one of the most deceptive “emerging markets” in iGaming – the article discusses licensing costs and procedures, but explicitly admits there is “no explicit licensing pathway for online operators” and “no clear legal pathway for foreign operators to acquire licenses.” You cannot legally operate here, period. The government actively enforces against unlicensed operators with raids and ISP blocking.

Even if you could somehow navigate this regulatory nightmare, the total market is only $20 million USD with 500,000 active players generating $35 ARPU – you’d need 20%+ market share just to breakeven on a $420,000+ entry investment, and customer acquisition costs in this blocked, restricted market would likely exceed lifetime value. This is a hard pass for any rational operator.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Already operating land-based casino or sports betting venue in Guatemala and want to add digital as marginal expansion (land-based is legal and licensed)

- Large Central American operator (e.g., Codere, Sportium) who can add Guatemala as incremental market with minimal cost and accept grey legal status as part of regional strategy

- Content with operating land-based only – this rating is specifically about online/digital gaming

❌ Definitely Avoid If You Are:

- Any operator seeking to legally license online gaming (no licensing pathway exists)

- Offshore operator (active enforcement, ISP blocking, raids, criminal sanctions)

- Startup or small operator ($420,000+ entry cost for $20M market makes no sense)

- Foreign operator without mandatory local partners (cannot operate without local entity partnership)

- Operator focused on profitability within 3 years (economics are impossible given market size and restrictions)

- Casino-focused operator (online casino exists in grey area at best, explicitly unlicensed)

- White label or affiliate marketer (cannot advertise effectively, market too small, regulatory risk too high)

- Cryptocurrency-focused operator (crypto is “growing in adoption” but infrastructure limitations and small market make this nonviable)

- Any operator who values legal compliance and business predictability

⚠️ BOTTOM LINE: Guatemala has no legal online gambling licensing, actively enforces against unlicensed operators, and offers a total market of only $20 million – avoid completely unless you’re adding it as marginal cost to existing Central American operations and accept operating in legal grey area with enforcement risk.