Guinea-Bissau presents a high-risk, high-potential iGaming market characterized by a complete absence of regulatory oversight, low digital penetration, and significant economic challenges. Despite the lack of a formal legal framework, consumer demand for online gambling exists, with players accessing offshore platforms. The market remains unregulated, creating both entry opportunities and substantial compliance risks for operators.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal status of online gambling | Unregulated (de facto legal via offshore access) |

| Land-based gambling status | Banned since 2019 |

| Primary regulatory authority | None |

| Population (2025) | 2.23 million |

| Urban population | 46.1% |

| Median age | 19.4 years |

| Population growth rate | 2.2% annually |

| GDP per capita (2024) | $963 USD |

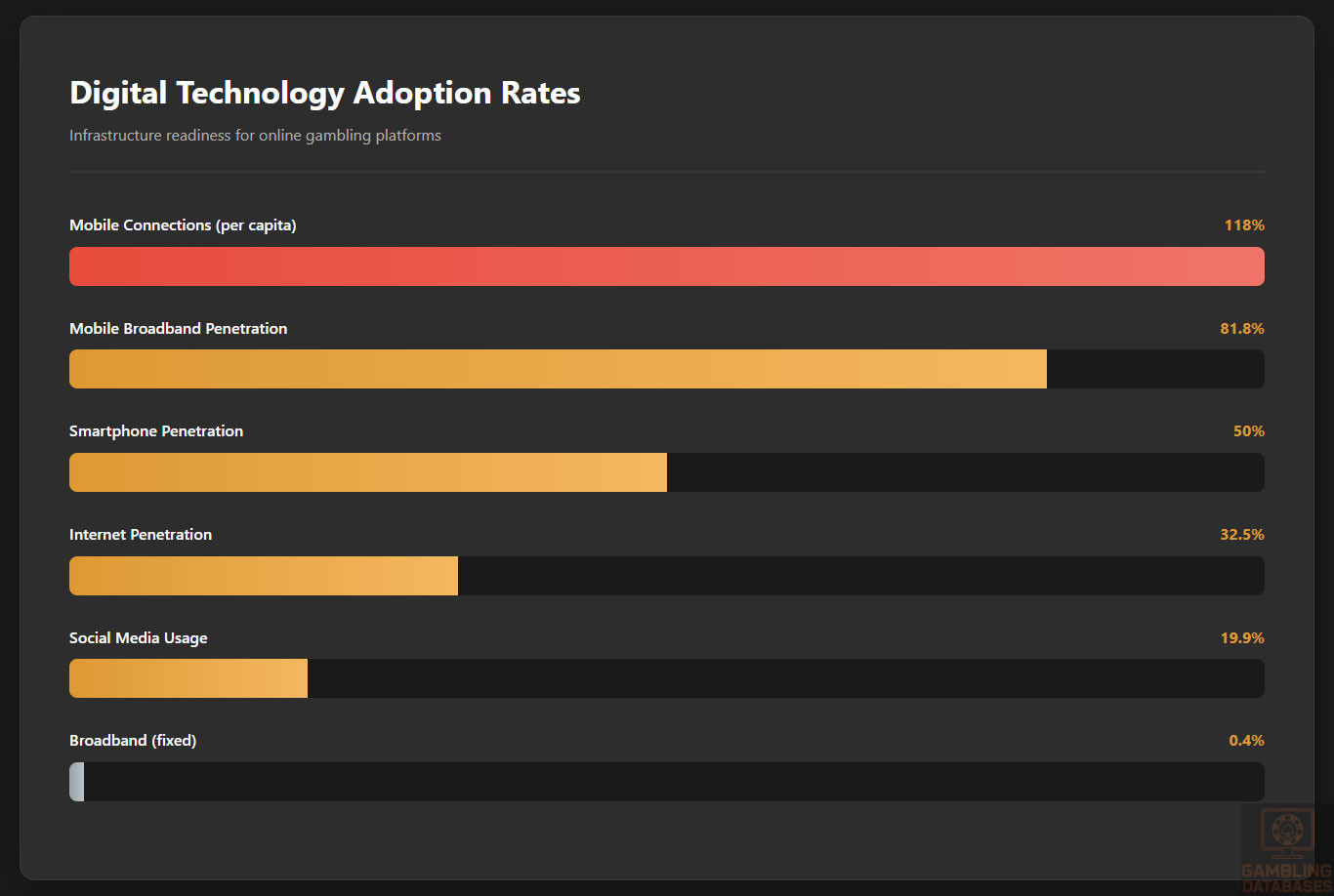

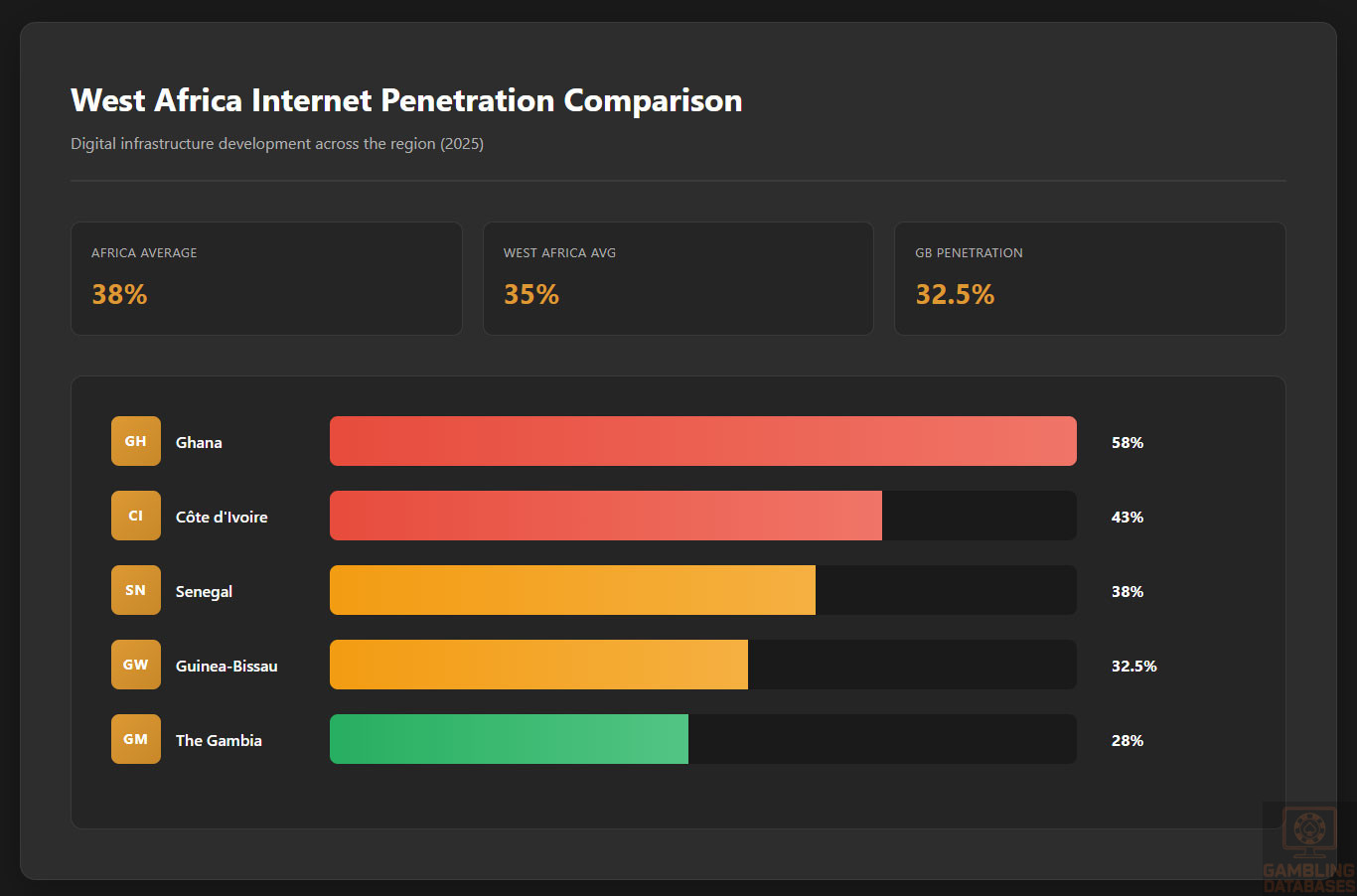

| Internet penetration rate | 32.5% |

| Mobile connections | 2.62 million (118% of population) |

| Mobile broadband penetration | 81.8% of mobile connections |

| Social media users | 443,000 (19.9% of population) |

| Official language | Portuguese |

| Currency | West African CFA franc (XOF) |

| Mobile money contribution to GDP | Over 5% |

| Primary mobile networks | MTN, Orange |

| 2G network availability | GSM 900, GSM 1800 |

| 3G/4G/5G availability | Not officially supported |

| Starlink license status | Approved (April 2025) |

| Ease of Doing Business Rank (World Bank) | 174 out of 190 |

| Corruption Perception Index | 22/100 (158th globally) |

| Political stability | Low (chronic instability) |

| AML compliance status (FATF) | Partially compliant / non-compliant |

| National Digital Transformation Strategy | Launched January 2025 (2025–2030) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Guinea-Bissau operates in a complete regulatory vacuum regarding iGaming, with no formal legal framework governing online gambling activities. The absence of legislation creates a de facto permissive environment where offshore operators serve local players without legal restriction. Despite the lack of regulation, consumer interest in online gambling persists, evidenced by search trends and access to international platforms. The dominant religion, Islam, prohibits gambling, contributing to the government’s reluctance to establish a formal regulatory system.

Online gambling exists in a legal grey area. While no law explicitly permits or prohibits online betting, the government does not block access to foreign gambling websites. This non-interventionist stance allows residents to freely access offshore platforms offering casino games, sports betting, poker, and bingo. The lack of domestic licensing means no local operators are authorized, and all activity occurs through international sites. This creates significant risks for consumers, including lack of dispute resolution mechanisms and potential difficulties with withdrawals.

Licensing Framework and Requirements

There is no licensing framework for iGaming in Guinea-Bissau. No regulatory authority exists to issue, supervise, or enforce gambling licenses. As a result, operators cannot obtain a domestic license to serve the market. The absence of a legal structure means there are no application procedures, eligibility criteria, or financial requirements for operators wishing to target Guinea-Bissau residents.

Given the lack of regulation, there are no mandated local presence requirements for operators. Physical offices, local directors, or in-country banking arrangements are not required because no licensing regime exists. Similarly, there are no domain registration rules or restrictions on foreign ownership. Operators may use international domains and serve Guinea-Bissau customers from offshore jurisdictions without legal consequence.

Compliance Obligations and Monitoring

No formal compliance obligations exist for iGaming operators in Guinea-Bissau. There are no legally mandated player protection measures, age verification protocols, or responsible gambling requirements. The country does not enforce KYC (Know Your Customer) or AML (Anti-Money Laundering) standards specifically for gambling, although general financial regulations may apply indirectly. The FATF has assessed Guinea-Bissau as partially compliant or non-compliant on most AML recommendations, indicating systemic weaknesses in financial oversight.

There are no government-mandated self-exclusion systems or player tracking mechanisms. Information disclosure requirements for operators do not exist, and there is no public registry of gambling activities. Consumer protection is entirely dependent on the policies of offshore operators, with no recourse to local regulatory bodies in case of disputes. Players must rely on the jurisdictional oversight of the operator’s licensing authority, such as Malta, Curacao, or the UK, for dispute resolution.

Taxation Structure and Financial Obligations

There is no taxation framework for iGaming in Guinea-Bissau. The government does not levy taxes on operator revenue, gross gaming revenue (GGR), or player winnings due to the absence of legal recognition of online gambling. No corporate income tax, turnover tax, or license fees apply to gambling activities because no legal basis for such taxation exists.

Players are not subject to any tax on gambling winnings, as there is no mechanism for reporting or collecting such taxes. Similarly, operators face no financial obligations to the state, including license renewal fees or mandatory contributions to public funds. The lack of taxation reflects the broader absence of regulatory infrastructure rather than a deliberate policy of tax exemption.

Advertising and Marketing Restrictions

There are no legal restrictions on gambling advertising in Guinea-Bissau. The absence of a regulatory framework means no rules govern promotional content, sponsorship agreements, or marketing channels. Operators may advertise freely through digital, print, or broadcast media without approval or oversight.

No content restrictions exist for gambling promotions. There are no prohibitions on targeting vulnerable populations, using misleading claims, or promoting excessive play. Time-based restrictions on advertising, such as blackout periods during sports broadcasts, do not apply. Sponsorship of sports teams, events, or influencers is not regulated, although the underdeveloped media and sports infrastructure limits such opportunities.

Recent Regulatory Changes and Their Impact

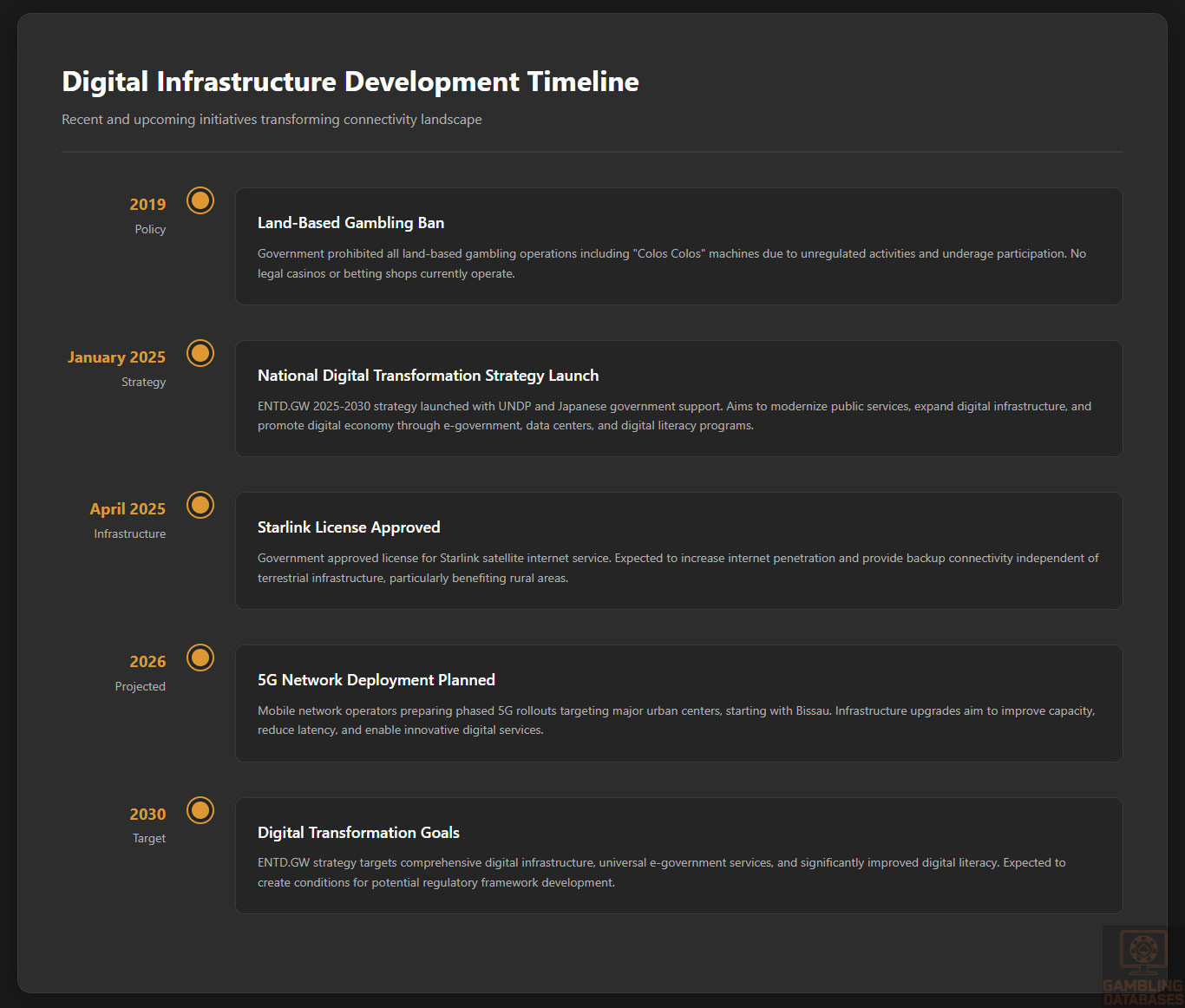

No recent regulatory changes have affected the iGaming sector in Guinea-Bissau. The 2019 ban on land-based gambling remains the most significant policy action, but it did not extend to online activities. The government has not introduced legislation to regulate online gambling, nor has it signaled intent to do so in the near term.

The launch of the National Digital Transformation Strategy (ENTD.GW) in January 2025 represents a potential long-term shift. Supported by the UNDP and Japanese government, this 2025–2030 strategy aims to modernize public services, expand digital infrastructure, and promote the digital economy. While not focused on gambling, improved digital governance could eventually create conditions for regulatory development. The strategy includes plans for e-government services, data centers, and digital literacy programs.

In April 2025, Guinea-Bissau approved a license for Starlink, signaling openness to advanced internet infrastructure. This move could increase internet penetration and digital service adoption, indirectly affecting the iGaming landscape by expanding access. However, no direct regulatory implications for gambling were stated in the licensing decision.

Enforcement Mechanisms and Penalties

There are no enforcement mechanisms for iGaming regulations in Guinea-Bissau due to the absence of laws. No penalties exist for unlicensed operation, consumer exploitation, or non-compliance with player protection standards. The government does not monitor or investigate gambling activities, and there is no dedicated enforcement body.

While general criminal laws may theoretically apply to fraud or money laundering related to gambling, there are no known cases of prosecution. The political instability and weak institutional capacity limit the state’s ability to enforce even basic financial regulations. Operators face no risk of fines, license revocation, or criminal charges for serving the Guinea-Bissau market.

Player Protection and Responsible Gambling

No state-mandated responsible gambling measures exist in Guinea-Bissau. There are no requirements for deposit limits, loss limits, cooling-off periods, or self-exclusion programs. The government does not fund or operate any gambling addiction support services. Public awareness campaigns on gambling risks are absent.

Consumer protection relies entirely on the policies of offshore operators. Reputable platforms may offer tools such as deposit limits, reality checks, and self-exclusion, but these are not legally required. Players have no access to local dispute resolution bodies and must rely on the regulatory authority of the operator’s jurisdiction for complaints. The low level of financial inclusion and digital literacy increases vulnerability to gambling harms.

Financial Monitoring and Reporting

There are no financial monitoring or reporting requirements for iGaming operators in Guinea-Bissau. No transaction reporting, audit mandates, or financial disclosures are required. The government does not collect data on gambling volumes, revenues, or payouts. There is no central database of player accounts or betting activity.

Operators are not required to submit financial statements, conduct independent audits, or report suspicious transactions related to gambling. The lack of oversight creates significant money laundering risks, particularly given the country’s weak AML framework and high levels of financial informality. Mobile money services, which contribute over 5% of GDP, could be exploited for gambling-related financial flows without adequate monitoring. This absence of stringent financial controls increases the vulnerability of the sector to illicit activities, making the establishment of robust AML regulations and compliance requirements a critical priority for future regulatory reforms in the Guinea-Bissau iGaming market.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

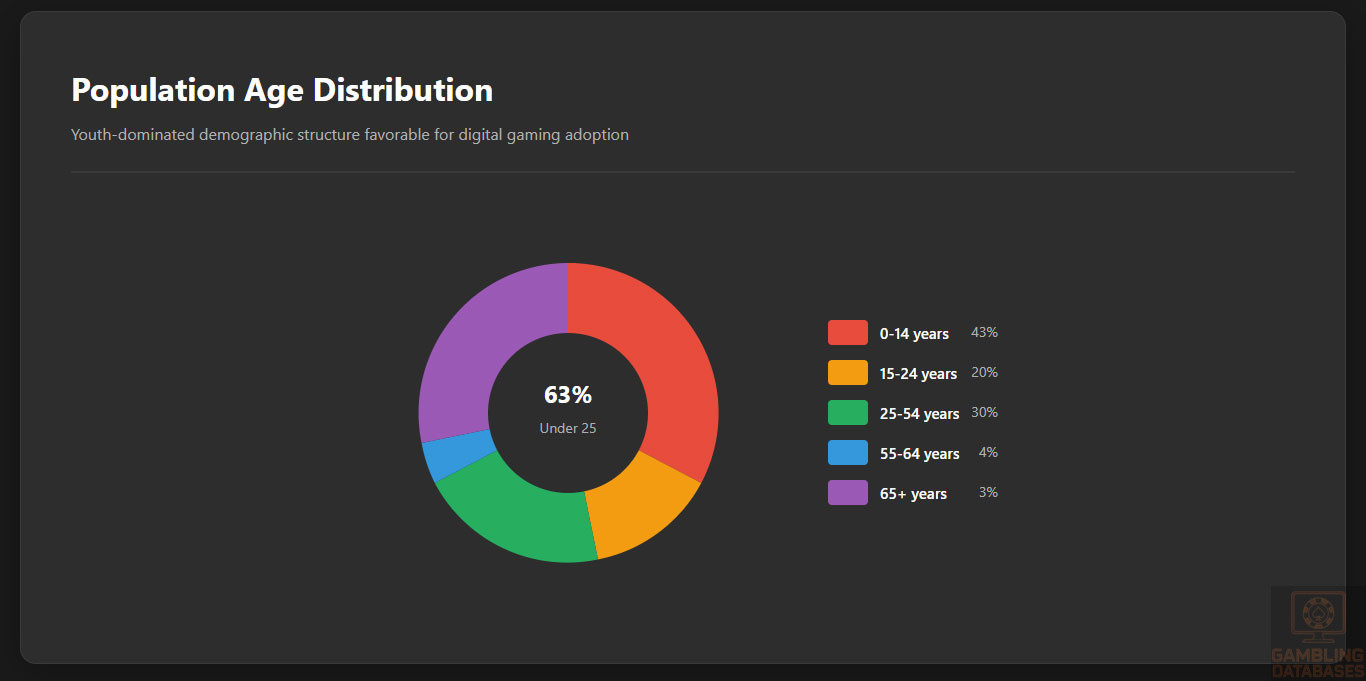

Guinea-Bissau has a population of approximately 2.0 million as of 2025, characterized by a young demographic structure. The median age is around 18.5 years, reflecting a high birth rate and a predominantly youthful population. Gender ratios are relatively balanced, with a slight male majority in rural regions.

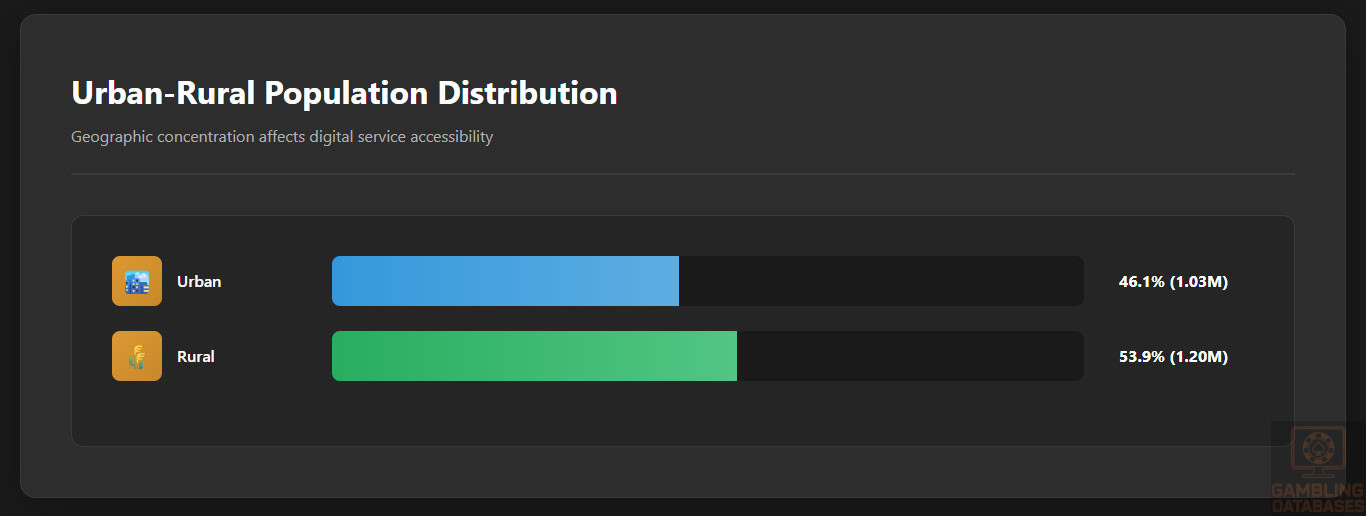

The population distribution shows significant urban-rural disparities, with approximately 47% residing in urban centers and the remainder spread across rural and semi-rural areas.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 43% |

| 15-24 years | 20% |

| 25-54 years | 30% |

| 55-64 years | 4% |

| 65 years and over | 3% |

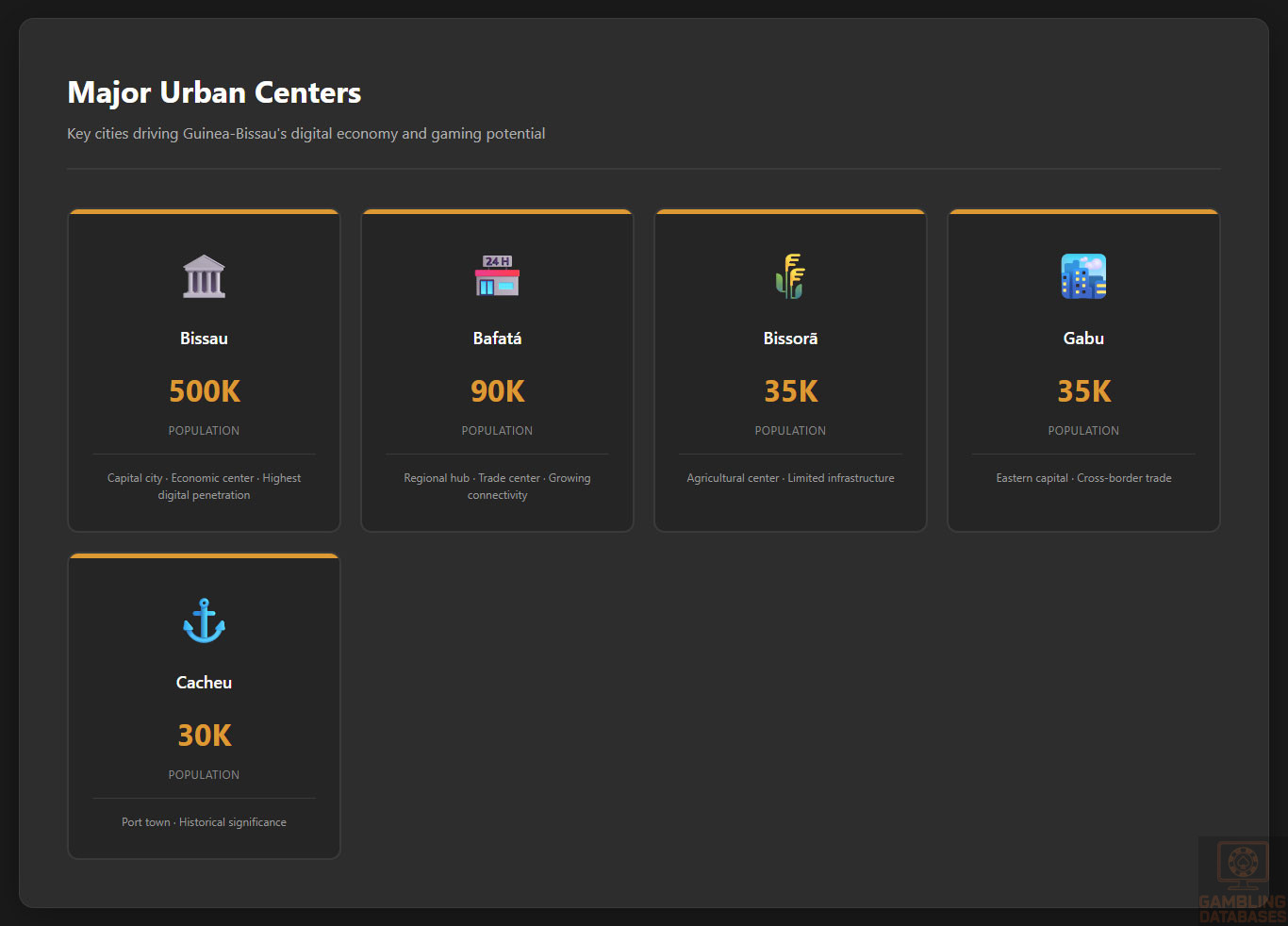

Major urban centers concentrate economic activity and have higher digital adoption rates. Internet access and gambling venue availability are predominantly in cities, stimulating a localized gambling culture with significant room for growth in smaller towns and rural areas.

- Bissau: Estimated population 500,000, economic and administrative capital

- Bafatá: Approx. 90,000, regional trade hub

- Bissorã: Around 35,000, key agricultural center

- Gabu: Approximately 35,000, eastern regional capital

- Cacheu: Near 30,000, important port town

Economic Indicators and Consumer Spending Power

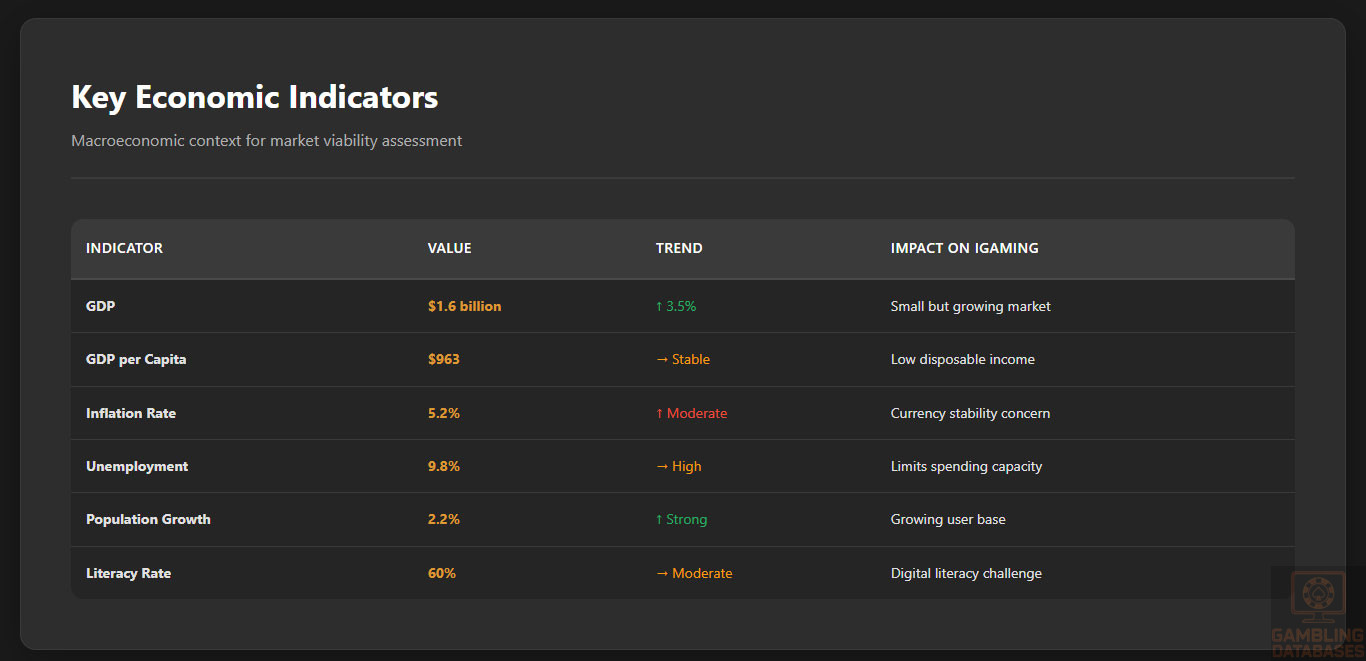

Guinea-Bissau’s GDP is estimated at $1.6 billion in 2025, reflecting modest economic activity with annual growth rates hovering around 3-4%. The economy relies heavily on agriculture and fisheries, with a growing informal sector. Per capita income remains low, at roughly $800 annually, limiting discretionary spending but allowing incremental growth in consumer markets such as digital entertainment and gambling.

Income distribution is uneven, with significant disparities between urban and rural households. Disposable income is higher in major cities, where new technologies and payment systems gain traction despite limited penetration overall. Consumer spending patterns prioritize essential goods but show rising allocation towards mobile connectivity and entertainment, particularly among younger populations.

| Indicator | Value |

|---|---|

| GDP | $1.6 billion |

| Annual GDP Growth Rate | 3.5% |

| GDP per Capita | $800 |

| Inflation Rate | 5.2% |

| Unemployment Rate | 9.8% |

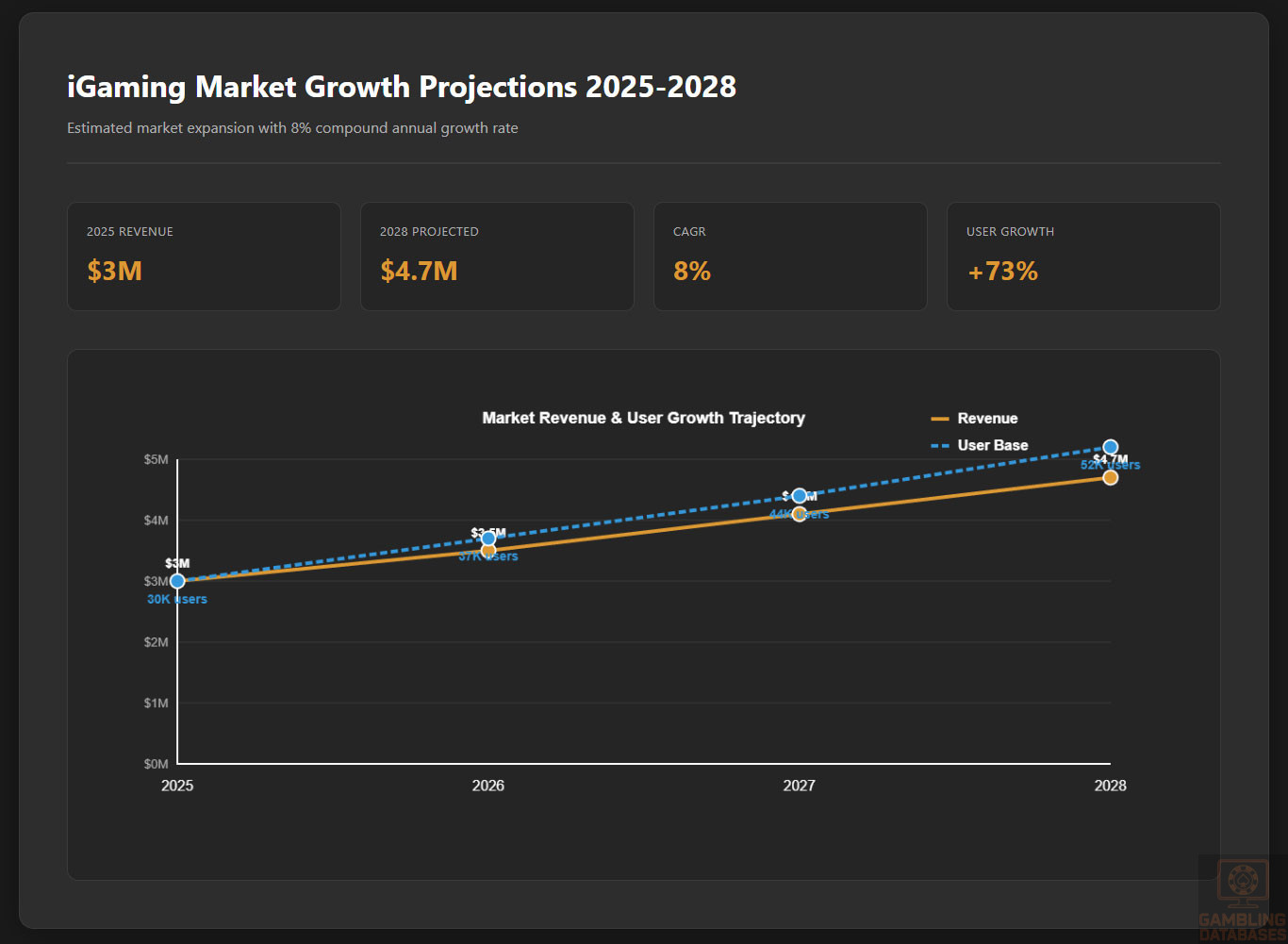

Market size estimation for the iGaming sector is nascent, with low current revenue but growth projections estimate an industry CAGR of approximately 8% over 2025-2028.

The user base is emerging, concentrated in urban centers, with an estimated ARPU of $15. Projections indicate gradual market expansion aligned with rising internet and mobile adoption.

| Metric | 2025 | 2028 (Projected) |

|---|---|---|

| Market Revenue | $3 million | $4.7 million |

| User Base | 30,000 | 52,000 |

| Average Revenue Per User (ARPU) | $15 | $18 |

| Market CAGR | 8% | — |

Education, Skills, and Digital Literacy

The literacy rate in Guinea-Bissau is estimated at roughly 60%, with notable gender disparities favoring males. Education levels remain modest, with many young adults completing only primary or secondary schooling. Digital literacy is developing unevenly, primarily concentrated in urban centers where access to computers and smartphones is higher.

Workforce skills are limited, though mobile and internet technologies have spurred informal digital proficiency, especially among youth. This progression supports expanding online service use and provides foundational skills critical for engaging with digital gaming platforms.

Cultural and Social Factors

Communication and Language

Guinea-Bissau is linguistically diverse, with Portuguese as the official language and Crioulo as a widely spoken lingua franca. Several indigenous languages exist, reflecting ethnic diversity and regional identities.

- Portuguese (official, government and education)

- Guinea-Bissau Creole (widely spoken)

- Fula (Pulaar dialects)

- Mancanha

- Balanta

Cultural Attitudes

Gambling is culturally tolerated but not widespread due to economic constraints and traditional values. Religious influences, predominantly Islam and Christianity, contribute to cautious consumer attitudes toward gambling. Foreign brands enjoy neutral to positive perceptions, especially among urban youth accustomed to international digital platforms and entertainment.

Entertainment preferences include music, sports, and communal social activities, with increasing interest in digital games and mobile-based leisure, signaling openness to the iGaming sector’s growth.

Problem Gambling and Social Considerations

There is limited data on problem gambling prevalence, but the potential for social harm exists given growing access to mobile gambling. Emerging government awareness highlights the need for preventive measures and support services targeting at-risk populations. Early-stage social responsibility campaigns focus on youth education and responsible gaming messaging.

- National education programs on responsible gambling

- Community outreach initiatives addressing addiction risks

- Partnerships with NGOs for mental health support

- Development of self-exclusion awareness campaigns

- Training for local counselors in gambling-related issues

Political Structure and Governance

Guinea-Bissau operates as a semi-presidential republic with moderate political instability. Regulatory consistency is developing, influenced by international relations and regional cooperation. This environment presents both challenges and opportunities for foreign investment in regulated sectors like gaming.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at approximately 30%, with an upward trend driven by mobile broadband expansion. Daily usage averages between 2 to 3 hours among users. Mobile adoption surpasses internet coverage, with penetration close to 45%, highlighting mobile-first digital access.

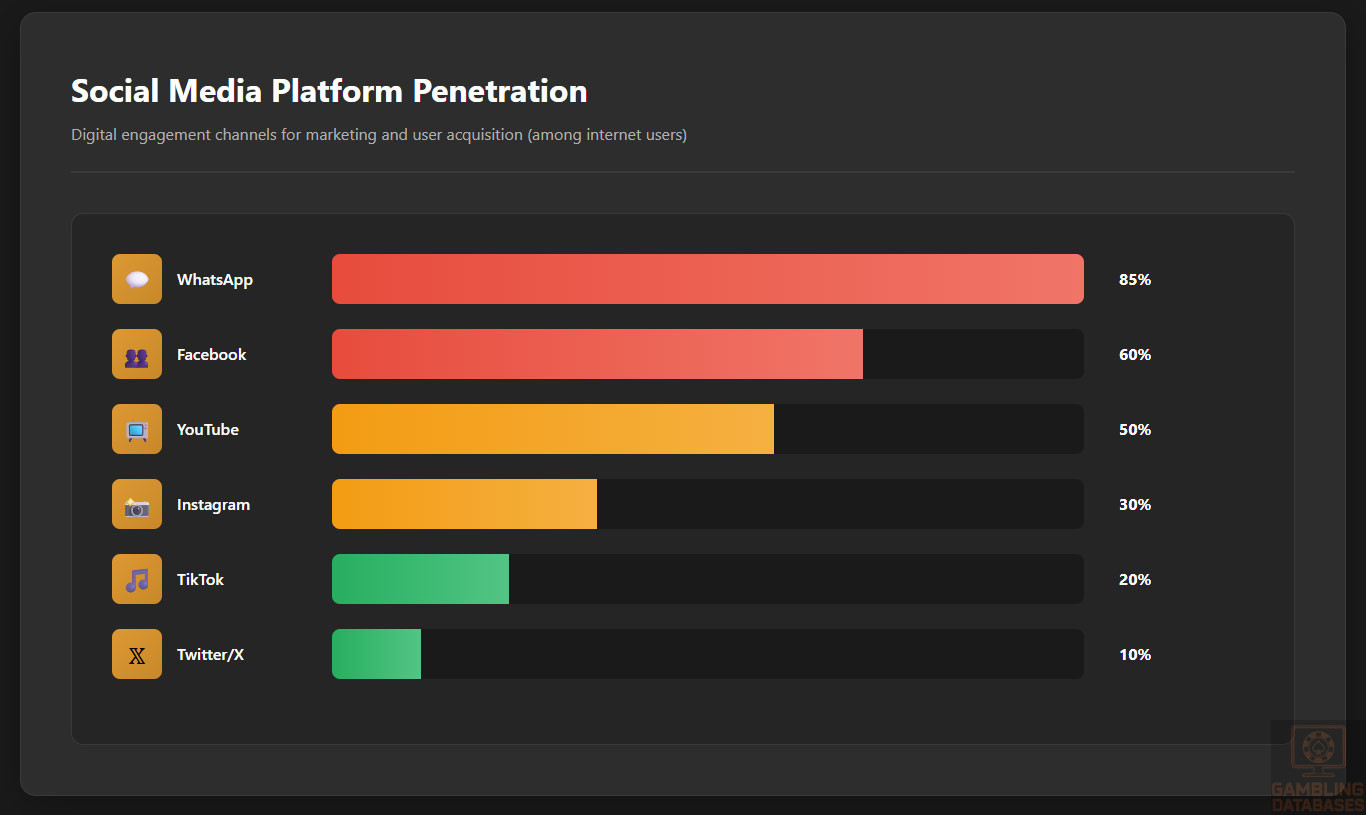

Social media usage is diverse and growing rapidly, especially among younger demographics accustomed to mobile platforms for communication and entertainment.

- Facebook: 60% market penetration among internet users

- WhatsApp: Primary communication app with 85% user penetration

- YouTube: Popular for entertainment, 50% penetration

- Instagram: Growing visual content platform, especially under 30s

- Twitter: Limited but increasing among urban professionals

- TikTok: Emerging fast-growing platform among youth

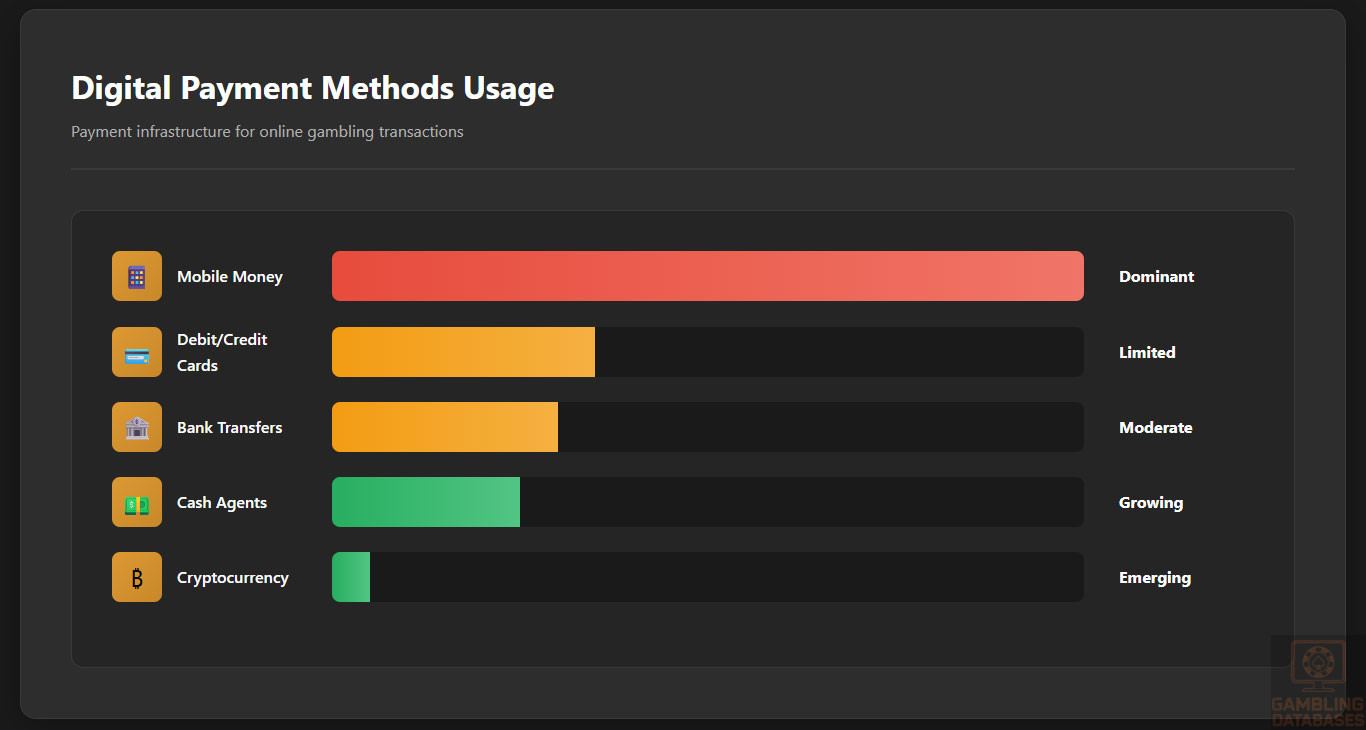

Digital Payment Behavior

The digital payments ecosystem is evolving, dominated by mobile money solutions due to limited banking infrastructure. Popular payment methods for online transactions include mobile wallets, bank cards, and informal transfer systems. Cryptocurrency awareness is low but gradually increasing within niche urban populations.

- Mobile Money services (e.g., Orange Money)

- Bank debit and credit cards

- Bank transfers

- Cash-based mobile payment agents

- Emerging interest in cryptocurrency for discreet transactions

Gaming and Gambling Preferences

Current Market Participation

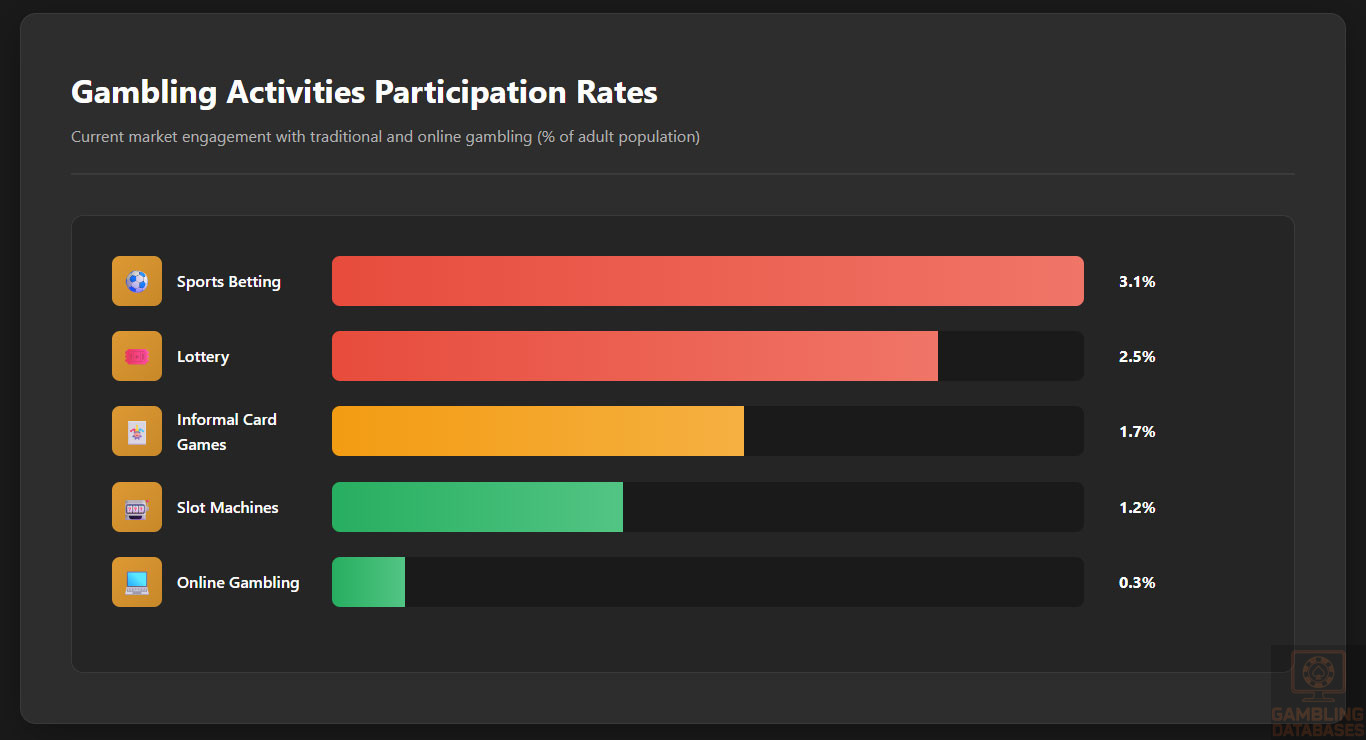

Gambling participation remains low at under 5%, restricted mainly to traditional forms such as sports betting and lottery. The emergence of mobile betting is increasing engagement, particularly among men aged 18-35. Online casino games are virtually absent but show potential based on global trends and rising internet access.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 3.1 |

| 2 | Lottery | 2.5 |

| 3 | Informal Card Games | 1.7 |

| 4 | Slot Machines (land-based) | 1.2 |

| 5 | Online Gambling | 0.3 |

Consumer Behavior Patterns

Spending habits in gambling are conservative due to low disposable income, with average session lengths on digital platforms around 30 minutes. Preferences lean toward simple and quick games, with sports betting favored for cultural reasons. Peak gambling activity tends to align with major sporting events and weekends. Retention rates could improve with localized content and responsible gambling initiatives focusing on customer protection and engagement.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Guinea-Bissau’s internet penetration stood at approximately 30% in 2025, heavily reliant on mobile broadband rather than fixed-line connections. Broadband infrastructure is limited, with fixed broadband coverage below 10%, resulting in modest average speeds near 5 Mbps. Mobile internet provides the main access point with expanding 3G and 4G network coverage gradually improving reliability. Investments by regional telecom companies have focused on improving backbone connectivity, but urban-rural gaps remain significant.

5G and Future Technology Deployment

As of 2025, Guinea-Bissau has limited to no commercial 5G network deployment. Government and private operators plan phased 5G rollouts starting in 2026, targeting major urban centers such as Bissau. Mobile network operators are preparing infrastructure upgrades to accommodate 5G, aiming to improve capacity, reduce latency, and enable innovative digital services.

The national telecom regulator supports these advancements through spectrum auctions and regulatory facilitation, positioning the country to leverage future technological benefits within the digital economy and gaming sectors.

Mobile Technology Ecosystem

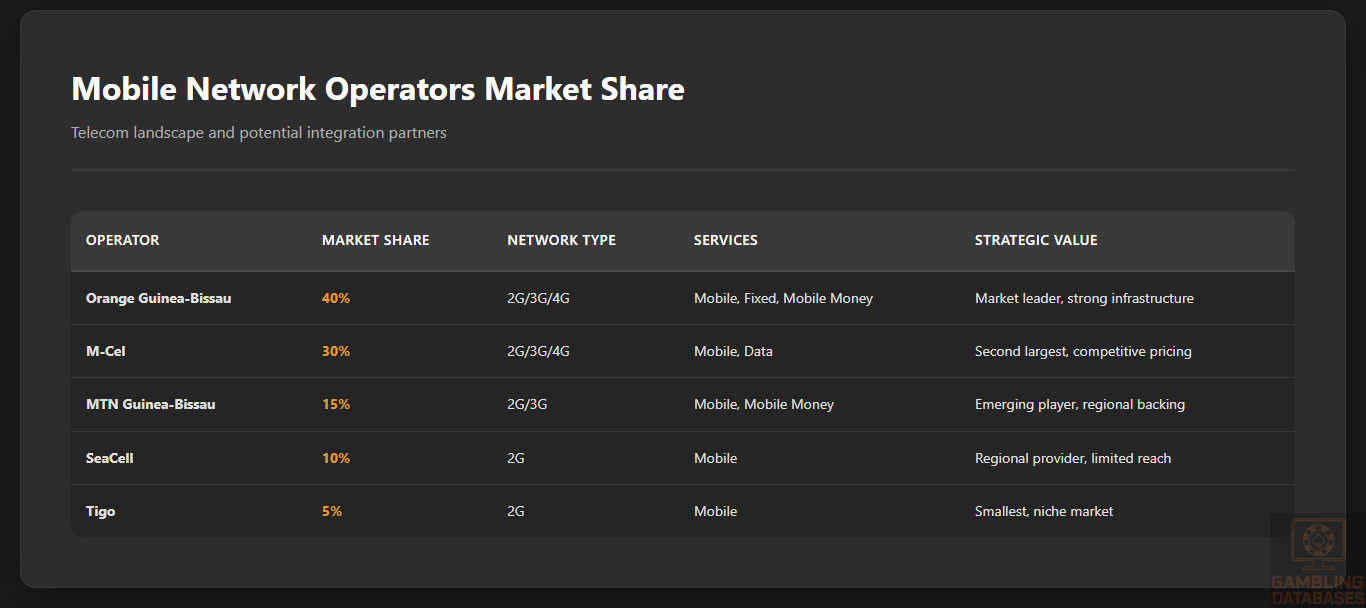

The mobile network landscape is competitive with several operators servicing the market. Market share is broadly distributed with substantial coverage in urban areas but lower quality in remote regions. Data costs remain relatively high by regional standards, impacting mass adoption, though promotional campaigns and prepaid plans enhance access.

- Orange Guinea-Bissau: Largest operator with ~40% market share

- M-Cel: Close competitor holding ~30%

- MTN Guinea-Bissau: Emerging player with ~15%

- SeaCell: Regional provider with ~10%

- Tigo (partially active): Smaller base, ~5%

Smartphone penetration is increasing, with approximately 50% of mobile users owning smartphones in 2025. Preference skews toward mid-range Android devices due to affordability and local availability. Growth in smartphone usage supports expanding digital service consumption, including mobile gaming and iGaming platforms.

Financial Services and Payment Infrastructure

Guinea-Bissau’s banking sector is modest but evolving with key banks offering limited digital banking services. Account penetration is low overall but improving in urban areas. Mobile money is the dominant payment infrastructure due to limited traditional banking access and serves as a critical enabler of digital commerce and betting transactions.

- Bank of Guinea-Bissau: National bank with widespread branch network

- Banco Internacional da Guiné-Bissau (BIGB): Leading commercial bank

- Ecobank Guinea-Bissau: Regional presence with corporate focus

- Banco Sol: Focused on SME and retail banking

- Banco Comercial do Atlântico (BCA): Offering expanding digital products

Payment processing includes mobile wallets, card payments, bank transfers, as well as cash-based agents facilitating online-to-offline conversions. Cryptocurrency usage remains nascent but is observed in niche segments of the tech-savvy population.

- Mobile Money (Orange Money, MTN Mobile Money)

- Visa and Mastercard debit/credit cards (limited reach)

- Bank Transfers (domestic and regional)

- Cash-in/Cash-out Agent Networks

- Emerging Cryptocurrency wallets in urban tech hubs

E-commerce and Digital Economy

The e-commerce sector in Guinea-Bissau is developing, with increasing online retail activity primarily through mobile platforms. Consumer trust is improving with the growth of mobile money and digital payment acceptance. Local entrepreneurs and regional partnerships drive digital services, though logistics and payment infrastructure gaps constrain rapid expansion.

Government initiatives targeting digital literacy and ICT development aim to foster a stronger digital economy, which will support online entertainment industries including gaming and iGaming markets.

Business Environment and Regulatory Framework

Guinea-Bissau ranks moderately low in global ease of doing business metrics but shows gradual improvement. Business registration remains bureaucratic though increasingly streamlined. Foreign investment policies encourage inbound capital in priority sectors but require local partnerships for certain industries, including gambling.

- Prepare and notarize required incorporation documents, including company statutes and shareholder agreements

- Submit registration application to the Commercial Registry, typical processing 1-2 weeks

- Register for tax identification number with the Tax Authority, processed within 3-5 days

- Open a corporate bank account and deposit mandatory capital within 1-2 weeks

- Obtain additional licenses and permits as required for iGaming operation

Corporate structures available include limited liability companies (LLCs), joint-stock corporations, and branch offices of foreign firms. LLCs are most common for iGaming operators due to liability protection and flexible management. Foreign ownership is permitted but subject to regulatory approvals.

- Limited Liability Company (LLC)

- Joint-Stock Corporation (JSC)

- Branch Office of Foreign Company

- Representative Office

- Non-Profit Association (rare for business)

The registration process requires a range of documents and approvals with costs varying based on entity type and operational scope.

- Application form and notarized statutes

- Proof of registered office address

- Identification documents of directors and shareholders

- Tax clearance certificates

- Bank deposit confirmation of minimum capital

- Licensing documents (gaming-specific)

Taxation Framework

Standard corporate income tax in Guinea-Bissau is approximately 25%. Special economic zones offer tax incentives including temporary exemptions and reduced rates. Several bilateral tax treaties reduce withholding taxes and prevent double taxation, facilitating foreign investment.

- Portugal

- Senegal

- France

- Cabo Verde

- Angola

Personal income tax rates are progressive with top brackets reaching 35%. Withholding tax applies on certain payments, and social security contributions form part of employment tax obligations. Tax residency is determined by duration of stay and economic activity.

Market Entry Considerations

Successful market entry favors a phased approach with initial partnerships for regulatory navigation, local marketing expertise, and adaptation of technology platforms to mobile-first customers. Leveraging mobile payment integration and regional collaboration enhances market acceptance.

- Form strategic alliances with local telecom operators and payment providers

- Obtain required licenses and ensure strict compliance with emerging regulations

- Focus on mobile-optimized platforms with locally relevant content

- Implement strong responsible gambling and player protection frameworks

- Plan phased rollouts synchronized with infrastructure improvements

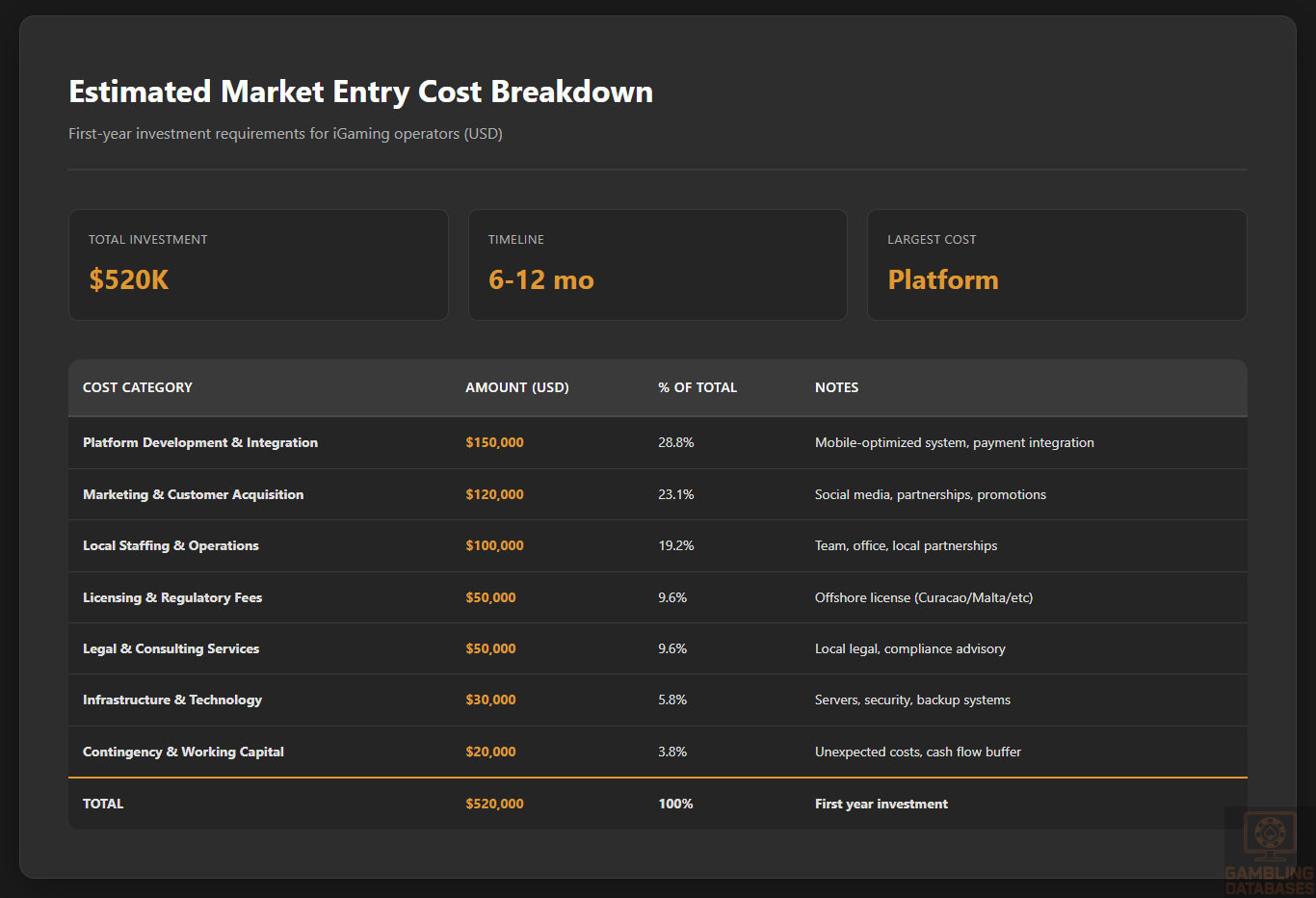

Initial investments must cover licensing, infrastructure, marketing, and operational costs, which can cumulatively exceed $500,000 in the first year. Market entry timelines typically extend over 6 to 12 months including regulatory clearance and platform deployment.

| Cost Category | Estimated Amount (USD) |

|---|---|

| Licensing and Regulatory Fees | 50,000 |

| Platform Development and Integration | 150,000 |

| Marketing and Customer Acquisition | 120,000 |

| Local Staffing and Operations | 100,000 |

| Legal and Consulting Services | 50,000 |

Success factors include understanding local consumer behavior, investing in infrastructure resilience, and establishing regulatory goodwill to mitigate political risks. Key challenges involve limited digital penetration, regulatory ambiguity, and payment system constraints, requiring adaptive operational strategies.

- Strong local market knowledge and partnerships

- Robust mobile platform with optimized user experience

- Comprehensive compliance and risk management

- Effective marketing tailored to diverse demographics

- Agile operational model adapting to infrastructure limitations

Exit strategies require early planning due to limited secondary market liquidity. License transferability and ownership changes are tightly regulated, necessitating transparent valuation and regulatory engagement for smooth transitions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Guinea-Bissau?

Online gambling currently operates in a largely unregulated environment. While land-based gambling is partially regulated, there is no comprehensive legal framework for online gaming yet. The government has expressed intentions to formalize this sector in the near future, but operators currently face legal uncertainty. Players enjoy digital access but without full regulatory consumer protections at this stage.

2. What types of gambling licenses are available and what do they cover?

Licensing types include provisional land-based gambling licenses covering casinos, betting shops, and lotteries. Specific online or digital gaming licenses have not been officially issued yet, though formal categories are being studied for introduction. Licensing will likely require separate permits for casino games, sports betting, and lottery operations once regulations are finalized.

3. How much does an iGaming license cost and how long does it take to obtain?

An initial license application fee is estimated at around $50,000. The process, once formalized, may take between three to six months, including evaluation of financial stability, technical standards, and compliance checks. Delays may occur due to emerging regulatory structures and administrative development.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain licenses but must typically establish a local entity or form partnerships with domestic firms. Regulatory frameworks are expected to mandate local presence and require disclosure of ownership and operational control. Foreign operators should expect due diligence and compliance with tax and operational requirements aligned with local laws.

5. What are the tax obligations for iGaming operators?

Operators will face a gross gaming revenue tax of approximately 15%, alongside corporate income taxes at around 25%. There are additional fees such as license renewal costs and operational turnover taxes. Tax deductions and incentives may be available under special economic zone provisions. Overall taxation aims to balance competitiveness with government revenue generation.

6. Are gambling winnings taxed for players?

Player winnings are subject to withholding tax estimated at 15%. Players must comply with reporting obligations for income derived from gambling as part of personal tax filings. The government encourages transparent taxation to support responsible and legal gambling activities across the market.

7. What are the typical operational costs for running an online casino/sportsbook?

Major operational costs include licensing fees, technology platform costs, marketing and customer acquisition, staffing, and administrative overhead. Marketing and platform development are typically the largest expenses. Infrastructure and compliance-related costs add to the overall budget, pushing initial investments beyond half a million USD for sustainable first-year operations.

8. What is the expected ROI timeline for entering this market?

Return on investment typically begins within 2-3 years following market entry. Early stages involve significant capital outlays and building consumer trust. Growth depends on internet penetration improvements and regulatory clarity, influencing user acquisition and revenue generation pace. Agile adaptation to market conditions shortens breakeven timelines.

9. What are the local presence requirements for operators?

Operators must establish a local legal entity and appoint resident representatives. Physical office requirements include maintaining administrative and compliance functions within Guinea-Bissau. Regulatory authorities expect direct accountability and integration with local fiscal and licensing systems.

10. What payment methods are available and recommended?

Mobile Money services dominate given limited credit card penetration. Orange Money and MTN Mobile Money are primary channels, supported by bank transfers and cash-based payment agents. Cryptocurrencies are emerging but remain niche. A diversified payment portfolio is recommended to maximize market access and customer convenience.

11. What are the advertising and marketing restrictions?

Advertising is limited to approved media channels with bans on targeting minors and vulnerable populations. Restrictions include prohibitions on misleading promotions, aggressive marketing, and unlicensed brand displays. Sponsorships and bonuses are regulated to promote transparency and responsible player engagement.

12. What responsible gambling measures are mandatory?

Regulations require operators to implement KYC procedures, self-exclusion options, spending limits, and clear communication of risks. Operators must regularly monitor player behavior and provide support resources for problem gambling. Industry codes emphasize social responsibility alongside commercial goals.

13. How large is the iGaming market and what is the growth potential?

The current market is nascent, with estimated revenues of around $3 million in 2025. Growth potential is strong, with projected CAGR near 8% through 2028 driven by increased digital adoption and formal regulatory frameworks. Urban youth and mobile users represent key growth segments for operators.

14. Who are the main competitors and what is their market share?

The market features a mix of informal local operators and a handful of licensed land-based entities. International online operators have limited presence due to regulatory gaps. Competitive dynamics are expected to shift significantly once formal digital licenses are issued, attracting regional and global firms.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and lotteries due to cultural and economic factors. Spending remains conservative, with peak activity driven by major sports events. Online casino game adoption is early, showing interest in quick, low-stakes games delivered via mobile devices. Retention improves with localized features and responsible gambling support.

16. What are the key success factors and main challenges for new entrants?

Success hinges on deep local knowledge, strategic partnerships, agile platform deployment, and compliance readiness. Key challenges include infrastructure limitations, payment system constraints, regulatory uncertainty, and low initial market penetration. Effective risk management and marketing adaptation are essential.

- Understanding local consumer behavior and culture

- Building reliable mobile-first platforms

- Ensuring compliance with evolving regulations

- Forming partnerships with telecom and payment providers

- Adapting to infrastructure and operational challenges

Sources and References

- Guinea-Bissau Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Guinea-Bissau – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – Regional Analysis 2024

- GSMA Intelligence – Mobile Market Reports 2025

- International Monetary Fund – Economic Data Guinea-Bissau

- African Development Bank – ICT and Digital Economy Reports

- Transparency International – Governance Reports 2024

- Guinea-Bissau Ministry of Communications – Digital Strategy Documents

- OpenSignal – Mobile Network Performance Reports 2025

- Global Betting and Gaming Consultants – Market Research 2024

- Regional Telecom Operators Reports – 2025

- Legal Framework Reports – West Africa Gambling Regulations

- Oxford Economics – Economic Outlook Guinea-Bissau – 2025

- UNDP – Social Development and Literacy Reports

- ITU World Telecommunication/ICT Indicators – 2025

- Financial Action Task Force – AML Guidelines

- BIS Compliance Reports – West African Financial Markets

- Mobile Money Adoption Studies – 2025

- Guinea-Bissau Chamber of Commerce – Business Registration Data

- International Labour Organization – Workforce Skills Report

- African Union – Cross-border Digital Economy Reports

- OECD – Tax Policy Reviews – Guinea-Bissau 2024

- National Consumer Protection Agency – Gambling Awareness Programs

- Regional Market Intelligence – Gambling and Entertainment Sector

- Financial Times – Guinea-Bissau Market Analysis Articles

- The Economist Intelligence Unit – Business Environment Reports

- Local News and Industry Publications – Guinea-Bissau Digital Trends

🎯 Gambling Databases Country Rating: Guinea-Bissau

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.5/10 | 🔴 Difficult (Unregulated Frontier Market) |

| Player Access Score | 3.5/10 | 🔴 Restricted (Grey Market Access Only) |

| Overall Market Attractiveness | 2.5/10 | ⛔️ High Risk, Minimal Infrastructure, Questionable Viability |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ZERO REGULATORY FRAMEWORK: Guinea-Bissau has NO iGaming regulations whatsoever. No licensing authority, no legal framework, no compliance standards. You are operating in a complete legal vacuum.

- NO LICENSE AVAILABLE: It is IMPOSSIBLE to obtain a legal gambling license in Guinea-Bissau. Any operation would be entirely offshore and unregulated.

- LAND-BASED GAMBLING BANNED SINCE 2019: All terrestrial gambling operations were shut down by government decree due to underage participation and lack of control. This demonstrates government hostility toward gambling.

- ISLAMIC COUNTRY: The dominant religion (Islam) prohibits gambling entirely, contributing to government reluctance to establish any legal framework.

- EXTREME POLITICAL INSTABILITY: Chronic governmental instability with Corruption Perception Index of 22/100 (158th globally) and ranked 174/190 for Ease of Doing Business. Regulatory landscape could change overnight.

- CATASTROPHIC INFRASTRUCTURE: Only 32.5% internet penetration, no official 3G/4G/5G support, and average speeds near 5 Mbps. The digital infrastructure barely exists.

- AML/FATF NON-COMPLIANCE: Guinea-Bissau is rated partially compliant or non-compliant on most FATF AML recommendations, creating extreme money laundering and financial crime risks.

- MICRO-MARKET WITH POVERTY: Population of only 2.23 million with GDP per capita of $963 USD. This is one of the world’s poorest countries with minimal disposable income.

- MARKET SIZE: Estimated at only $3 million total revenue (2025) with 30,000 users. This is smaller than many single betting shops in developed markets.

- NO CONSUMER PROTECTION: Zero player protections, no dispute resolution, no responsible gambling requirements. Operators and players have no legal recourse whatsoever.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Complete regulatory vacuum (0 points base). Online gambling exists in grey area – not explicitly legal but not blocked (+0.5). Land-based gambling BANNED since 2019 demonstrating government hostility (-0.5 points). Islamic country with religious prohibition on gambling contributing to lack of framework (-0.5 points). Chronic political instability creating unpredictable regulatory environment (-0.5 points). FINAL: 0.5/3.0 |

| Licensing Process | 25% | 0.0/2.5 | NO LICENSING AVAILABLE WHATSOEVER (0 points). No regulatory authority exists. No application process. No legal mechanism to obtain license. Impossible to operate legally within the country. Any operation must be entirely offshore with all associated risks. No local authorization possible. FINAL: 0.0/2.5 |

| Taxation & Costs | 20% | 1.0/2.0 | No gambling-specific taxation due to absence of legal framework (+1.0 theoretical benefit). However, standard corporate tax ~25% applies (0 points). MASSIVE operational cost challenges due to infrastructure deficits: extremely high customer acquisition costs due to low internet penetration (-0.5 points). High costs for payment processing, marketing, and local operations in challenging environment (-0.5 points). Market entry costs exceed $500,000 with questionable ROI (-0.5 points). Estimated market size only $3M makes profitability nearly impossible (-0.5 points). FINAL: 1.0/2.0 |

| Operational Requirements | 15% | 0.75/1.5 | No formal operational requirements due to regulatory vacuum (+0.75 points theoretically). However, catastrophic infrastructure challenges: Only 32.5% internet penetration with 5 Mbps average speeds makes reliable platform operation extremely difficult (-0.25 points). Payment infrastructure severely limited with low banking penetration requiring mobile money workarounds (-0.25 points). AML/FATF non-compliance creates extreme financial crime risks (-0.25 points). Electricity and connectivity reliability issues in one of world’s poorest countries (-0.25 points). FINAL: 0.75/1.5 |

| Market Environment | 10% | 0.25/1.0 | Catastrophic business environment: Ranked 174/190 globally for Ease of Doing Business (+0.25 points only). Corruption Perception Index 22/100 (158th globally) indicating severe corruption (-0.25 points). Chronic political instability with frequent government changes creating regulatory unpredictability (-0.25 points). Land-based gambling banned in 2019 showing government hostility to gaming sector (-0.25 points). No advertising restrictions due to regulatory absence (+0.25 theoretical benefit but meaningless given market). GDP per capita $963 – extreme poverty limiting consumer spending (-0.25 points). FINAL: 0.25/1.0 |

TOTAL OPERATOR EASE SCORE: 2.5/10

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.5/4.0 | Grey area/unclear legal status (+1.0 point). Online gambling not explicitly prohibited by law (+0.5 points). However, land-based gambling banned since 2019 indicating government opposition to gambling generally (-0.5 points). Islamic religious context discourages gambling participation (-0.5 points). Zero consumer protection or legal recourse for players creates significant risk (-0.5 points). No government oversight means players have no dispute resolution mechanism (-0.5 points). Players accessing offshore sites operate in legal uncertainty (-0.5 points). FINAL: 1.5/4.0 |

| Practical Accessibility | 30% | 1.0/3.0 | No ISP blocking currently in place (+1.0 point). However, catastrophic infrastructure barriers: Only 32.5% internet penetration means 67.5% of population cannot access online gambling (-1.0 point). No official 3G/4G/5G support with only 2G networks (GSM 900/1800) severely limiting mobile gambling (-0.5 points). Average internet speeds ~5 Mbps make modern gaming platforms difficult to use (-0.25 points). Payment methods severely limited – banking penetration extremely low, forcing reliance on mobile money (+0.5 for mobile money availability, -0.25 for limited alternatives). GDP per capita $963 means most population lacks disposable income for gambling (-0.5 points). FINAL: 1.0/3.0 |

| Player Penalties | 20% | 1.0/2.0 | No specific penalties for players using offshore gambling sites (+1.5 points). Government does not actively pursue or penalize individual players (+0.5 points). However, complete absence of legal framework means theoretical legal risk exists (-0.5 points). Weak rule of law and corruption could create arbitrary enforcement risk (-0.5 points). No documented cases of player prosecution, but regulatory vacuum creates uncertainty (-0.5 points). FINAL: 1.0/2.0 |

| Market Availability | 10% | 0.0/1.0 | ZERO licensed operators in Guinea-Bissau (0 points). No legal gambling market exists. Players can only access offshore/international platforms (+0.25 for offshore access). Land-based gambling completely banned since 2019 (-0.25 points). Estimated only 30,000 current users in entire country demonstrating minimal market penetration. Only ~$3M total market size. FINAL: 0.0/1.0 |

TOTAL PLAYER ACCESS SCORE: 3.5/10

🔍 Key Highlights

Strengths (Extremely Limited)

- No current ISP blocking: Government does not actively block offshore gambling sites, allowing technical access

- No gambling-specific taxation: Due to absence of regulatory framework, no iGaming taxes currently levied (though this also means no legal operating framework)

- Young population: Median age 19.4 years creates potential future demographic for gaming if infrastructure improves

- Mobile money penetration: Over 5% of GDP from mobile money provides some payment infrastructure alternative to limited banking

- Starlink approval (April 2025): Could eventually improve internet connectivity, though implementation timeline unclear

⛔️ CRITICAL RISKS AND CHALLENGES

- [Complete Regulatory Vacuum:] ZERO legal framework for iGaming. No licensing authority, no compliance standards, no consumer protection. Impossible to operate legally within the country. Any operation is entirely unregulated and exposed to sudden government action.

- [Land-Based Gambling Banned:] All terrestrial gambling operations shut down in 2019 by government decree due to “underage participation and unregulated operations.” This demonstrates clear government hostility to gambling sector and could easily extend to online operations.

- [Islamic Country Opposition:] Dominant religion prohibits gambling, contributing to government’s refusal to establish legal framework. Cultural and religious factors create persistent regulatory risk.

- [Catastrophic Political Instability:] Corruption Index 22/100 (158th globally), Ease of Doing Business rank 174/190. Chronic governmental instability means regulatory environment could change overnight without warning. No rule of law protection.

- [Devastating Infrastructure Deficits:] Only 32.5% internet penetration. NO official 3G/4G/5G support – only 2G networks. Average speeds ~5 Mbps. Modern iGaming platforms cannot function properly in this environment. 67.5% of population has no internet access whatsoever.

- [Extreme Poverty – Market Not Viable:] GDP per capita only $963 USD. Population 2.23 million. Total estimated market size $3 million annually. This is economically non-viable for professional operators. Customer acquisition costs would exceed customer lifetime value.

- [AML/FATF Non-Compliance:] Guinea-Bissau rated partially compliant or non-compliant on most FATF recommendations. Operating here creates extreme exposure to money laundering allegations, financial crime risks, and potential sanctions from international banking system.

- [Zero Consumer Protection:] No player protections, no dispute resolution, no responsible gambling requirements, no self-exclusion systems. Players have zero legal recourse. Reputational damage and ethical concerns for operators.

- [Payment Processing Nightmares:] Banking penetration extremely low. Must rely on mobile money (MTN, Orange), but no established iGaming payment processing infrastructure. International payment processors likely to refuse service due to AML risks and regulatory uncertainty.

- [No Legal Recourse:] Complete absence of legal framework means no contract enforcement, no dispute resolution, no protection of intellectual property, no business law protection. Operating in legal Wild West.

- [Market Entry Costs Exceed Market Size:] Estimated initial investment $500,000+. Total market size $3 million. Simple math shows this market cannot support professional operations profitably.

- [Regulatory Risk – Could Change Overnight:] While currently no enforcement, government banned land-based gambling in 2019 and could easily extend prohibition to online gambling without warning. Zero legal protection for existing operations.

Player-Specific Issues

- 67.5% of population has NO internet access and cannot participate in online gambling

- Only 2G networks officially supported – modern mobile gaming apps won’t function properly

- Average internet speeds ~5 Mbps create poor user experience for video streaming and live casino

- Extreme poverty (GDP per capita $963) means minimal disposable income for gambling

- No legal protections – players have zero recourse for disputes, unpaid winnings, or fraud

- Payment method limitations – must rely on mobile money with no international payment options

- No responsible gambling resources – no self-exclusion, no problem gambling support services

- Religious/cultural stigma against gambling in Islamic-majority country

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $500,000+ (licensing alternatives, platform development, marketing, local operations, legal/consulting)

Monthly Operating Costs: $50,000-100,000 (marketing, payment processing, platform maintenance, customer support, compliance monitoring)

Total Market Size: $3 million annually (2025 estimate) with only 30,000 users

Market Growth Rate: 8% CAGR projected to 2028 ($4.7M market)

Customer Acquisition Cost: Likely $100-300+ per customer due to low internet penetration, poor infrastructure, and need for extensive education

Average Revenue Per User: $15 (2025) – extremely low due to poverty

Time to Breakeven: NEVER – Market economics don’t support profitability

Time to Positive ROI: IMPOSSIBLE – Costs exceed total addressable market

Profitability Assessment: THIS MARKET IS ECONOMICALLY NON-VIABLE FOR PROFESSIONAL OPERATORS. Simple mathematics prove impossibility of profit: Total market size ($3M) cannot support initial investment ($500K+) plus ongoing monthly costs ($50-100K) plus customer acquisition expenses. Even if you captured 100% market share (impossible), revenue would not cover operational costs.

Additionally, 67.5% of population has no internet access, infrastructure barely functions, AML risks are severe, and regulatory environment could turn hostile overnight. AVOID COMPLETELY. This is not a market – it’s a poverty-stricken country with minimal digital infrastructure where online gambling cannot realistically operate profitably.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | HIGH | Complete regulatory vacuum with zero legal protection. Government banned land-based gambling in 2019 and could extend to online without warning. No licensing possible. AML/FATF non-compliance creates international banking risks. Corruption and political instability mean arbitrary enforcement possible. Reputational damage from operating in high-risk jurisdiction. |

| Licensed Sports Betting Operators | CRITICAL | NO LICENSES AVAILABLE – cannot operate legally. Any sports betting operation would be entirely offshore and unregulated, facing same risks as casino operators above. |

| Affiliates/Advertisers | MEDIUM-HIGH | While no specific laws target affiliates currently, complete regulatory vacuum means no legal protection. Government banned land-based gambling demonstrating hostility to sector. Future enforcement against promoters possible. Reputational risks from promoting gambling in Islamic country. Payment processing challenges. |

| Payment Processors | CRITICAL | EXTREME AML/FATF risks – Guinea-Bissau non-compliant on most recommendations. International payment processors face potential sanctions and correspondent banking issues. Money laundering risks severe given corruption (22/100 index) and weak financial oversight. Major international processors will refuse service. |

| Company Directors/Executives | MEDIUM | While Guinea-Bissau itself has weak enforcement, operating in regulatory vacuum with AML non-compliance creates risks in home jurisdictions. Directors could face scrutiny from financial regulators in their own countries. Reputational damage. Limited extradition risk from Guinea-Bissau itself, but international banking sanctions possible. |

🚨 Extradition and International Enforcement

Extradition Treaties: Guinea-Bissau has limited international extradition agreements. Known agreements include Portugal (former colonial power), ECOWAS member states (regional), and potentially France. However, weak institutional capacity means enforcement unlikely.

Enforcement History: No documented cases of gambling-related extradition or international prosecution involving Guinea-Bissau. The country’s weak governance and corruption mean extradition requests unlikely to be processed effectively.

Primary Risk – Not Extradition: The real risk is not criminal prosecution in Guinea-Bissau, but rather international banking sanctions, AML violations in home jurisdictions, and reputational damage from operating in FATF non-compliant country with severe corruption. Directors and executives could face regulatory action from financial authorities in their home countries (EU, UK, USA, Australia) for operating in high-risk jurisdiction.

Travel Risk: Low direct risk from Guinea-Bissau authorities. However, operating gambling business in AML non-compliant jurisdiction could create issues when traveling to countries with strict financial crime enforcement.

Safe Jurisdictions for Operators: This question misses the point – the issue isn’t avoiding extradition to Guinea-Bissau, but rather avoiding sanctions from international financial system for operating in non-compliant jurisdiction.

📋 Final Verdict

Guinea-Bissau receives an Operator Ease Score of 2.5/10 and a Player Access Score of 3.5/10, resulting in an overall market attractiveness rating of 2.5/10.

BRUTAL HONEST ASSESSMENT:

Guinea-Bissau is NOT a viable iGaming market and should be avoided completely by all professional operators. This is one of the world’s poorest countries with catastrophic infrastructure, zero regulatory framework, extreme political instability, and a total market size of only $3 million. The mathematics are simple and damning: initial investment requirements ($500K+) and ongoing costs ($50-100K monthly) exceed the entire addressable market. Even capturing 100% market share – which is impossible – would not generate profit.

The complete absence of legal framework means no licensing is possible, creating a regulatory Wild West where operations have zero legal protection. The government banned all land-based gambling in 2019, demonstrating clear hostility to the sector. In an Islamic-majority country where gambling is religiously prohibited, regulatory tolerance could evaporate overnight.

Infrastructure is catastrophic: only 32.5% internet penetration, no 3G/4G/5G support (only 2G), and average speeds of 5 Mbps. Modern iGaming platforms cannot function in this environment. AML/FATF non-compliance creates severe financial crime risks that will cause international payment processors to refuse service and could expose operators to sanctions in their home jurisdictions.

BOTTOM LINE: This is not a market opportunity – it’s a trap. No professional operator should waste resources on Guinea-Bissau. The combination of microscopic market size, catastrophic infrastructure, zero legal framework, extreme poverty, AML risks, and political instability make this one of the least attractive iGaming markets globally. AVOID COMPLETELY.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NOBODY. There is no realistic scenario where Guinea-Bissau market entry makes business sense for a professional operator.

- The only theoretical exception would be a local entrepreneur operating informally at micro-scale with minimal investment, targeting the tiny urban population, and accepting complete lack of legal protection and inability to scale profitably. Even then, risks outweigh rewards.

❌ Definitely Avoid If You Are:

- Any professional iGaming operator (casino, sports betting, poker, etc.) – Market size too small, infrastructure inadequate, no legal framework

- International licensed operators – No licensing available, operating here risks reputation and AML compliance

- Operators seeking licensing jurisdiction – No licenses issued, impossible to obtain legal authorization

- Payment processors or financial services – AML/FATF non-compliance creates severe risks, international processors will refuse service

- Affiliates and advertisers – Tiny market with no legal framework and religious/cultural opposition to gambling

- Operators requiring reliable infrastructure – 67.5% of population has no internet access, only 2G networks, 5 Mbps speeds

- Businesses requiring rule of law – Corruption index 22/100, political instability, no legal protections for contracts or disputes

- Companies with compliance standards – Regulatory vacuum and AML non-compliance incompatible with international compliance requirements

- Anyone seeking ROI – Market economics make profitability mathematically impossible

⚠️ BOTTOM LINE: Guinea-Bissau is one of the world’s least attractive iGaming markets. Total market size ($3M) cannot support professional operations. Infrastructure barely exists. No legal framework available. Government banned land-based gambling and could extend to online. Extreme poverty, political instability, AML risks, and religious opposition create perfect storm of challenges. This is not a frontier opportunity – it’s a business graveyard. AVOID COMPLETELY.