Guinea presents a promising but early-stage opportunity for iGaming market entry with progressive efforts to regulate online gambling activities. While national lotteries and sports betting enjoy some regulation, the broader legal environment for online and land-based gaming remains developing.

The country aims at gradual modernization of its regulatory frameworks to create a safer, transparent, and revenue-generating environment. This analysis explores Guinea’s current legal landscape, licensing procedures, compliance requirements, taxation, and enforcement mechanisms critical for market participants.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

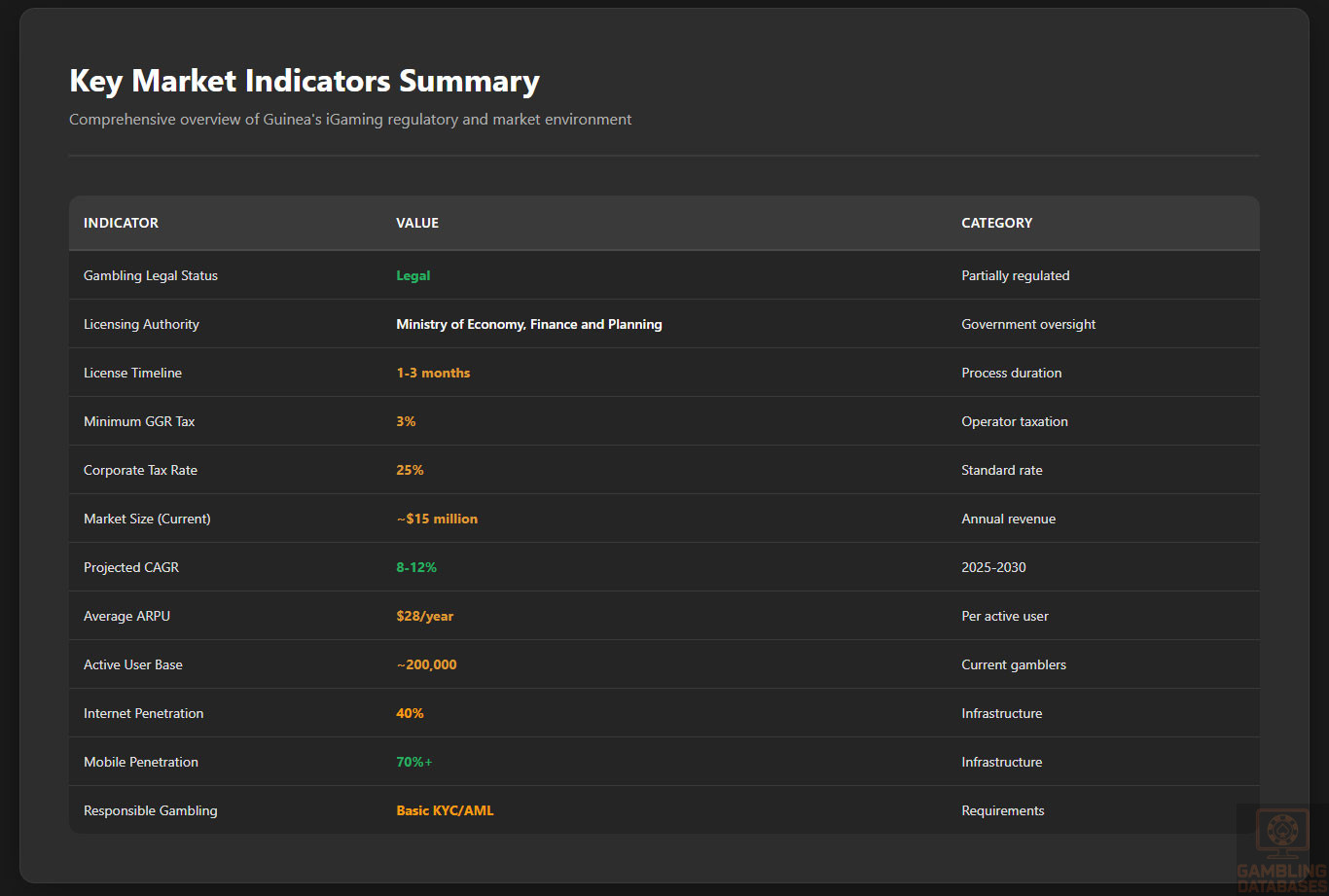

| Gambling Legal Status | Legal; partially regulated with state lotteries and licensed sports betting; limited framework for online casinos |

| Licensing Authority | Ministry of Economy, Finance and Planning |

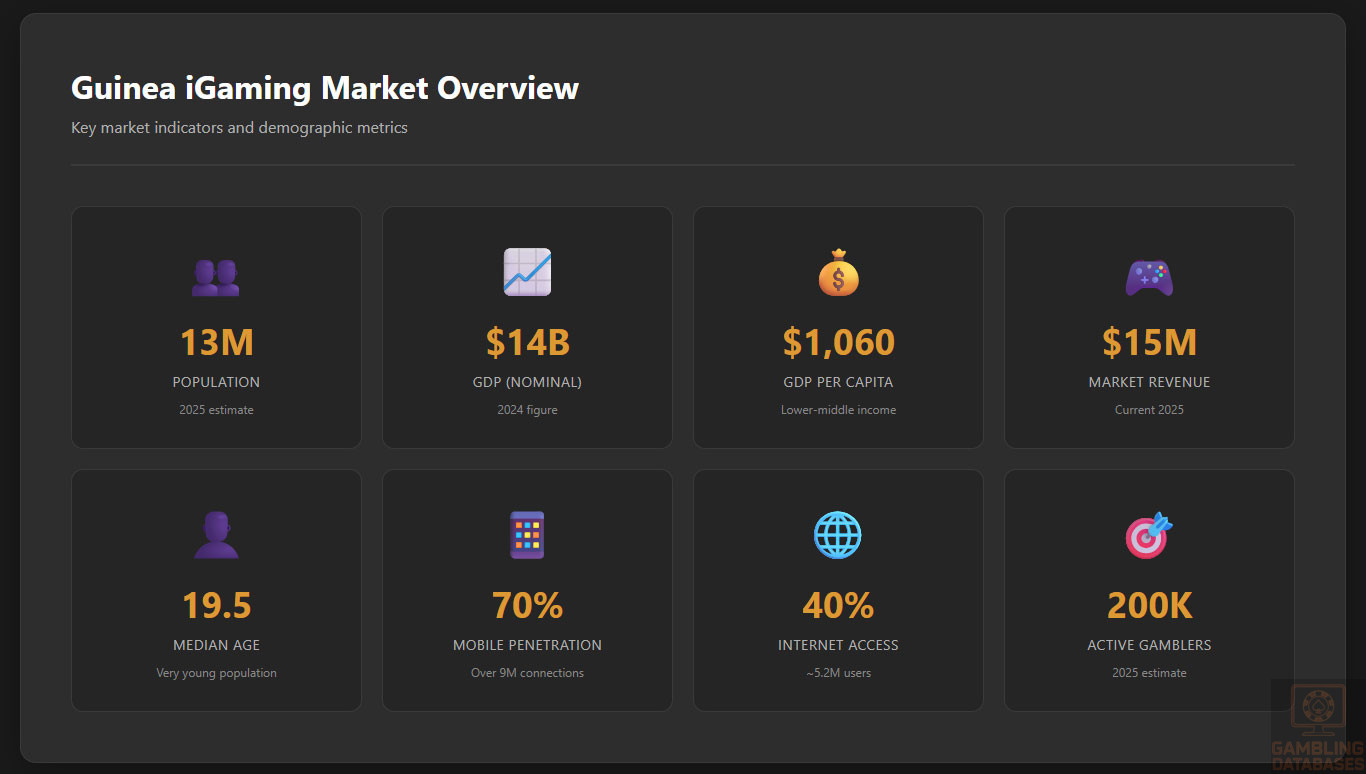

| Population | ~13 million (2025 estimate) |

| Median Age | 19.5 years |

| GDP (Nominal) | ~$14 billion USD (2024) |

| GDP Per Capita | ~$1,060 USD (2024) |

| Internet Penetration | ~40% of population |

| Mobile Penetration | Over 70% |

| Available Payment Methods (Licensed Operators) | Local banks, mobile money, international cards |

| Online Gambling Licensing Cost | Varies; typical license fees modest but financial guarantees required |

| Tax Rate on Gross Gaming Revenue (GGR) | ~3% turnover tax minimum, with other tax obligations |

| Corporate Income Tax | 25% |

| Tax on Player Winnings | Currently no direct player tax reported |

| License Application Timeline | Typically 1-3 months |

| Enforcement Agency | Ministry of Economy, Finance and Planning; no independent gaming regulator |

| Responsible Gambling Measures | Basic KYC and AML required for licensed operators |

| Market Entry Barriers | Limited formal regulations for online casinos; licensing process underdeveloped |

| Land-Based Casinos | Almost non-existent, no clear regulation framework |

| Sports Betting | Most regulated sector; licensed operators active with kiosks and betting shops |

| National Lottery | State-operated with exclusive licenses |

| Technology Infrastructure | Developing; reliable mobile networks but internet broadband still limited |

| Market Size Revenue (Est.) | Small but growing; regulated sectors contribute limited public revenue |

| Average Revenue Per User (ARPU) | Low; reflective of GDP and market maturity |

| Market Growth Forecast (CAGR) | Projected 8-12% over next 5 years driven by mobile adoption |

| Operational Requirements | Financial stability proof, compliance with tax and AML laws |

| Advertising Restrictions | Basic; no strict gambling advertising laws but promotional activities monitored |

| Recent Regulatory Developments | Efforts to modernize licensing and enforcement ongoing but incremental |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Guinea’s gambling regulations are in a formative stage, with significant variation across gambling categories. State-run national lotteries represent the most established sector, operated under exclusive licenses aimed at raising public funds. Sports betting, particularly on football, is also actively regulated, with licensed operators permitted to run local betting shops and kiosks.

Other forms of gambling, such as land-based casinos and slot machine halls, lack clear regulatory frameworks. These activities remain largely undeveloped commercially and legally, with minimal government oversight. Online gambling is legal but not yet comprehensively regulated. Guinea’s existing laws do not fully address online sportsbooks or casino operations, though licensing is required where applicable under general commercial regulations.

Land-Based Gambling Activities

Land-based gambling primarily consists of the national lottery and a limited number of licensed sports betting outlets. Formal casino operations and slot machine venues are absent, resulting from lack of clear legal guidelines. This gap reflects the nascent stage of Guinea’s land-based gambling industry, which is focused mainly on traditional and more accessible forms of gaming.

Online Gambling Framework

Online gambling operates in a partially regulated environment. While online betting and digital lottery sales exist, no formal regulatory body dedicated solely to online gaming has been appointed. Operators must acquire licenses through the Ministry of Economy, Finance and Planning, but detailed requirements specific to remote gambling platforms are under development. Key compliance areas include mandated financial reporting, anti-money laundering (AML) protocols, and player identification verification.

Licensed Operators and Market Players

The licensed gambling market in Guinea is dominated by state-run or state-sanctioned entities for lotteries and a small number of sports betting operators serving local demand. The absence of an independent regulatory authority has resulted in a relatively informal market structure. Business entities operating in the licensed sectors generally apply for licenses directly with the Ministry, facing variable procedural transparency.

International iGaming operators have limited presence due to the lack of a defined online licensing framework tailored to digital platforms. Entry strategies for new entrants focus on partnership with local firms and compliance with overarching commercial laws, pending clearer online gambling regulations from the government.

Licensing Framework and Requirements

Application Process and Eligibility

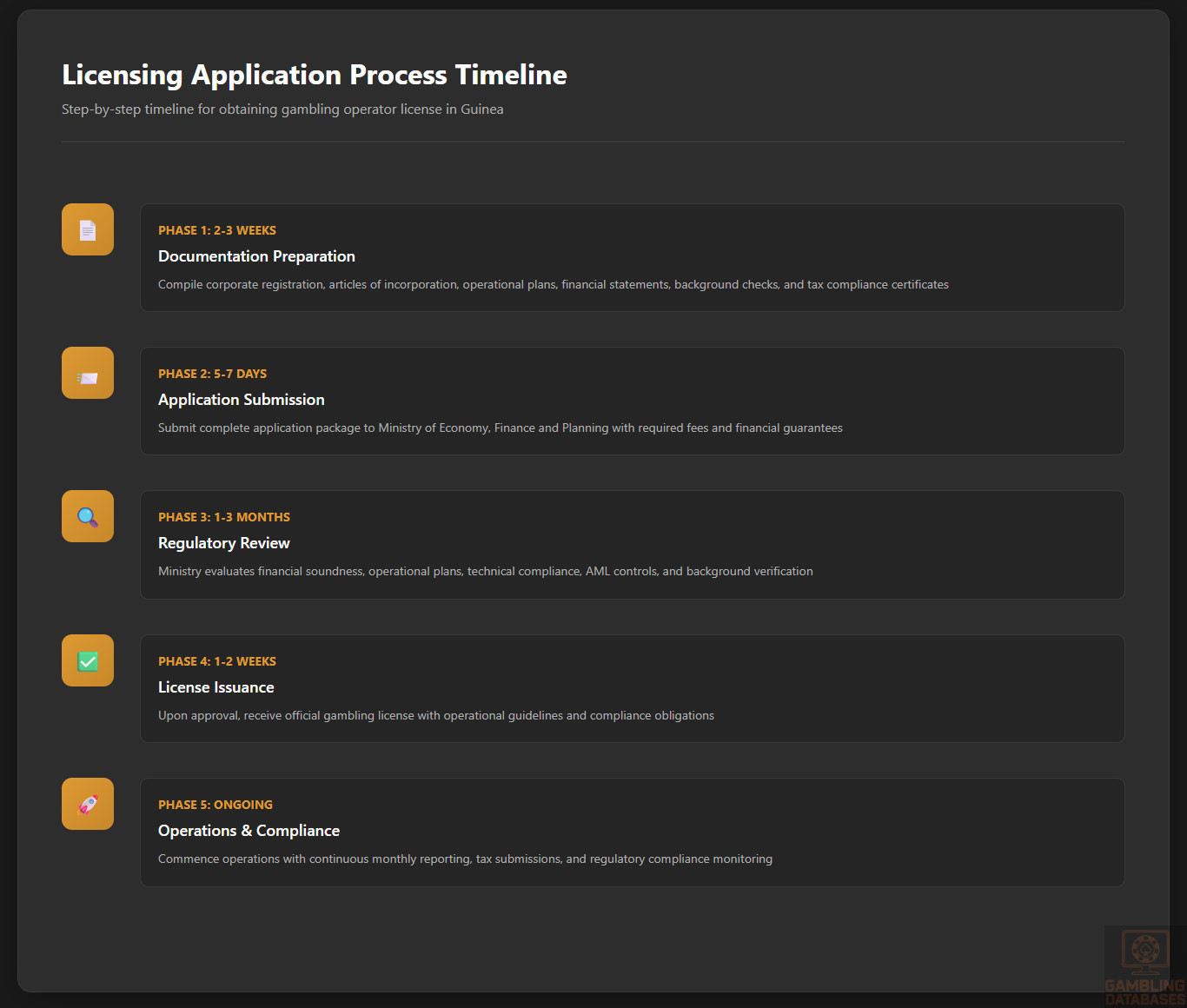

The Ministry of Economy, Finance and Planning oversees licensing for gambling activities. Applicants must demonstrate financial soundness, submit operational plans detailing proposed gaming activities, and ensure compliance with tax obligations. The licensing process generally takes between 1 to 3 months depending on the completeness of documentation and regulatory review workload.

Application fees are modest relative to more mature iGaming markets, but operators must provide proof of financial stability, including audited financial statements or financial guarantees. Technical compliance standards are evolving, with increasing emphasis on secure transaction systems, data protection, and AML controls.

The licensing regime requires applicants to submit these following documents:

- Corporate registration certificate and articles of incorporation

- Operational plan including market strategy and risk management

- Proof of financial solvency and banking references

- Technical system documentation and platform security details

- Criminal background checks for directors and major shareholders

- Tax compliance certification or registration with the tax authority

Local Presence and Operational Requirements

Guinea’s regulatory environment favors operators with a local corporate presence or a designated agent located within the jurisdiction. Physical offices are not universally mandated but having a registered local address aids licensing approval. There are no explicit domain ownership restrictions for online operators, but the ability to maintain operational control and compliance with Guinean law must be demonstrable.

Foreign ownership is permitted; however, partnerships with local businesses can facilitate smoother regulatory engagement. Personnel obligations typically include appointing a compliance officer responsible for liaison with government authorities and ensuring all AML and responsible gambling measures are implemented effectively.

Compliance Obligations and Monitoring

Player Protection and Identification

Licensed operators must incorporate robust player verification systems to prevent underage gambling and mitigate fraud. Anti-money laundering measures include monitoring player transaction patterns and reporting suspicious activities. Operators are mandated to deploy responsible gambling measures such as self-exclusion tools and clear communication of betting risks.

The following player protection measures are required:

- Mandatory age verification at registration

- KYC procedures aligned with national AML laws

- Transaction monitoring for suspicious activity

- Provision of self-exclusion and time-out options for players

- Disclosure of odds, betting rules, and potential risks

Financial Monitoring and Reporting

Operators are required to submit periodic financial and operational reports to the Ministry, detailing gross gambling revenue, tax contributions, and compliance with AML obligations. Routine financial audits assess adherence to reporting requirements and internal controls. The regulatory body enforces standards through routine inspections and the authority to impose sanctions for non-compliance.

- Submission of monthly revenue and tax reports by operators

- Review and validation of reports by Ministry officials

- Notification of discrepancies or compliance issues

- Enforcement actions including fines or license suspensions for violations

Taxation Structure and Financial Obligations

Player Taxation

Currently, players in Guinea are not directly taxed on gambling winnings. The government focuses on taxation at the operator level to ensure efficient revenue capture. The absence of player-level taxation aligns with regional practices designed to encourage market growth.

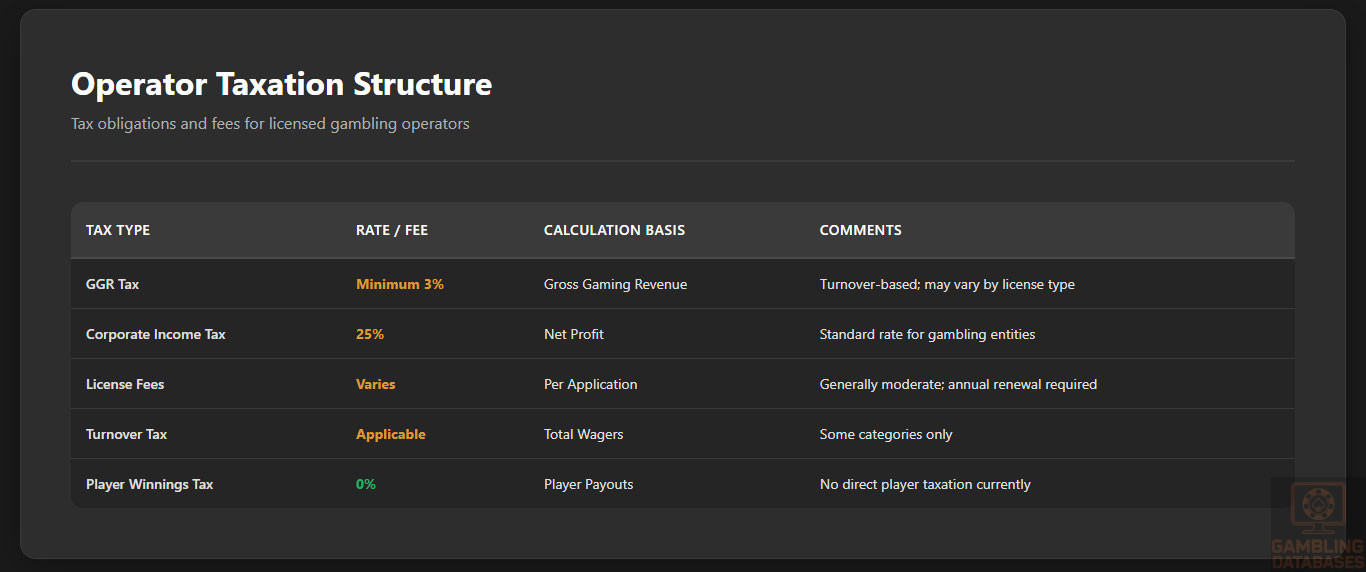

Operator Taxation

| Tax Type | Applicable Rate or Fee | Comments |

|---|---|---|

| Gross Gaming Revenue (GGR) Tax | Minimum 3% | Turnover-based; may vary by license type |

| Corporate Income Tax | 25% | Standard corporate tax for gambling entities |

| License Fees | Varies; generally moderate | Annual renewal fees apply |

| Turnover Tax | Applicable to some categories | Based on total wagers |

Operators are also subject to filing requirements to ensure all tax obligations are met fully. License renewals trigger additional fees which vary depending on the scale and type of gambling operation conducted.

Gambling Market Financial Performance

The market’s total wagered amounts and tax revenues are comparatively low due to the limited regulatory depth and professionalization of the sector. However, Ghana’s strong growth trajectory in adjacent markets provides a benchmark. Guinea’s market is expected to expand as infrastructure and legal clarity improve, supporting a more substantial contribution to public coffers.

Advertising and Marketing Restrictions

Advertising is lightly regulated with no comprehensive law specifically targeting gambling promotions. Basic restrictions focus on prohibiting advertising to minors and banning false or misleading claims about gaming outcomes. Promotions and sponsorships are monitored but not heavily legislated, offering flexibility to marketing strategies.

The allowed advertising channels and restrictions include:

- Television and radio under general advertising standards

- Online platforms with basic content guidelines

- Outdoor advertising monitored for age-restriction compliance

- Sponsorships permitted with content transparency requirements

- Time-of-day restrictions for broadcast gambling ads

Recent Regulatory Changes and Their Impact

The Guinean government has initiated incremental updates to its gambling laws since 2023, aiming for modernization and greater international compliance. These changes include raising licensing standards, enhanced AML protocols, and clarifying taxation rules. Operators have faced moderate increases in compliance costs but benefit from clearer guidance and improved market credibility.

Enforcement Mechanisms and Penalties

Penalties for non-compliance include fines, suspension, or revocation of licenses, and potential criminal charges in severe cases. Enforcement is managed by the Ministry of Economy, Finance and Planning with periodic inspections and audits. The penalty regime is designed to uphold market integrity while encouraging voluntary compliance.

- Fines for operating without a valid license

- License suspension for breaches in AML or KYC

- Financial penalties for late or inaccurate reporting

- Confiscation of gaming equipment for illegal activities

- Criminal prosecution for fraud or money laundering

Section 2: Demographics and Consumer Analysis

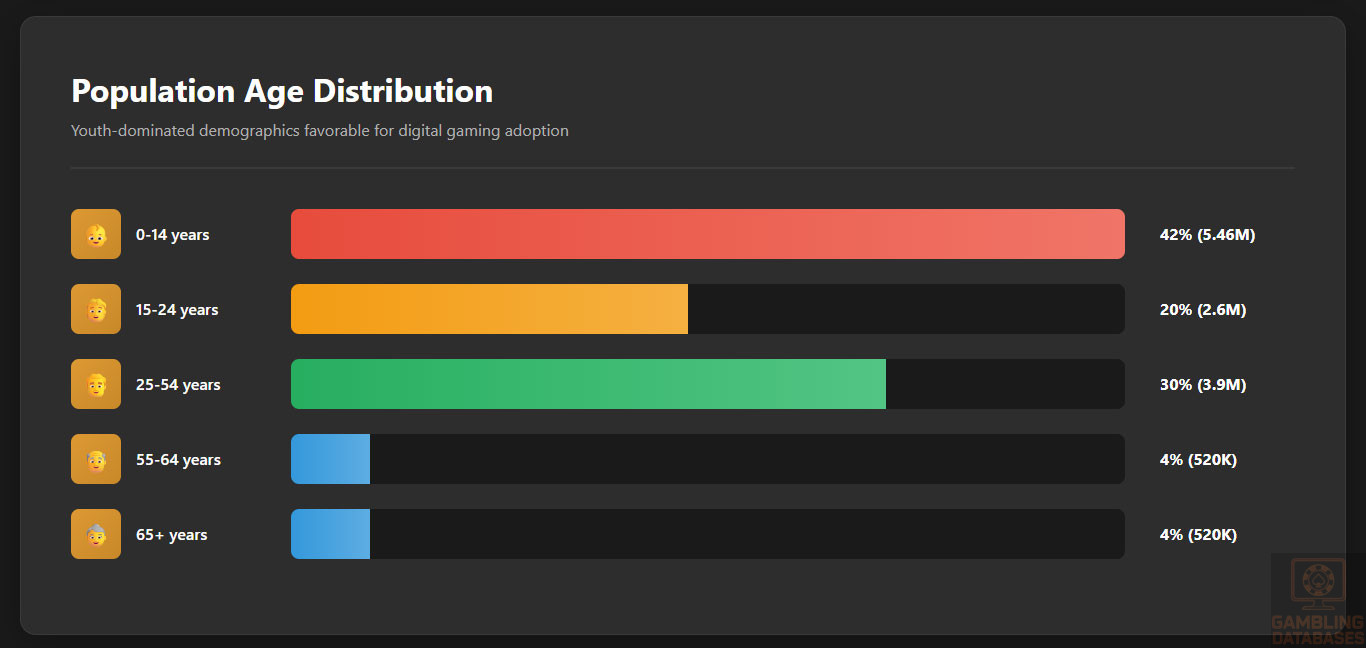

Population Demographics and Distribution

Guinea’s population is estimated at approximately 13 million in 2025, characterized by a very young demographic profile. The median age is under 20 years, reflecting a high proportion of children and young adults. Gender distribution is nearly balanced, with a slight male majority common to the region.

Urbanization is moderate; about 40% of the population resides in urban centers while the remaining majority lives in rural areas largely engaged in agriculture. This urban-rural divide directly influences internet access and gambling participation.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 42% |

| 15-24 years | 20% |

| 25-54 years | 30% |

| 55-64 years | 4% |

| 65 years and over | 4% |

Geographic Distribution

Population concentration centers mainly in the capital Conakry and the surrounding coastal regions, with gradual dispersal towards inland cities. Economic activities are more diversified in urban areas, driving higher disposable income and entertainment demand.

Internet connectivity and gambling infrastructure are heavily skewed towards these major cities where digital penetration is highest. Local sports betting shops and lottery outlets cluster in populated urban districts, while rural regions face accessibility challenges.

- Conakry – population ~2.3 million

- Kankan – population ~500,000

- Labé – population ~300,000

- Nzérékoré – population ~250,000

- Kindia – population ~200,000

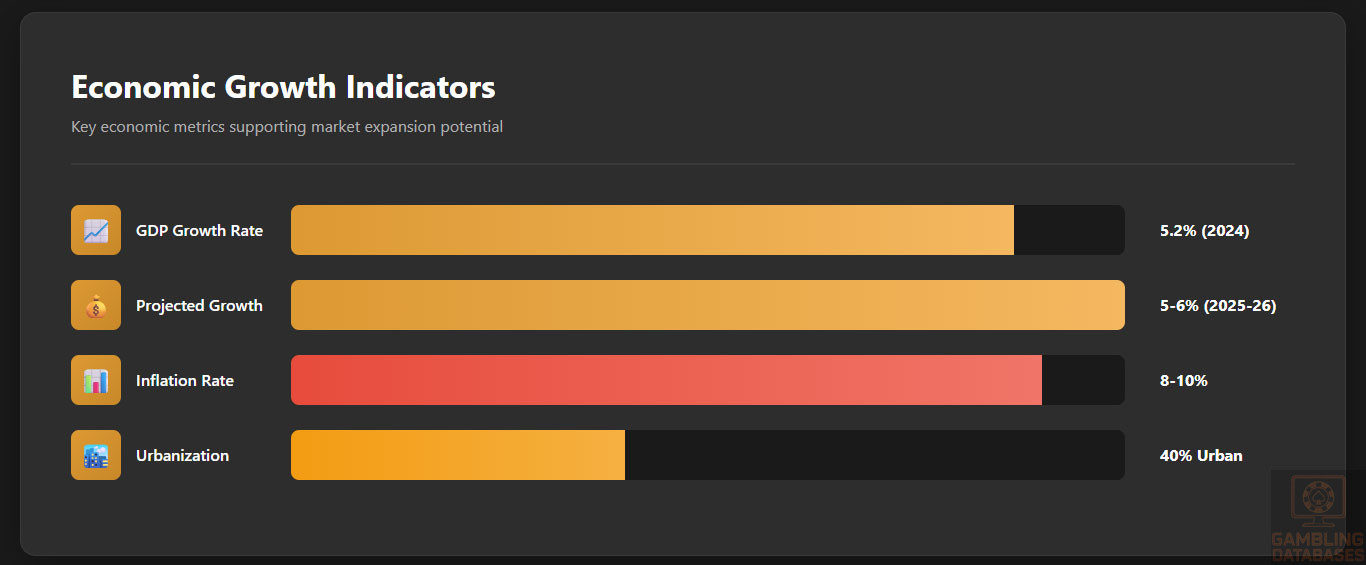

Economic Indicators and Consumer Spending Power

Guinea’s economy is modest, with a nominal GDP near $14 billion USD and per capita income around $1,060 USD as of 2024. The economic structure leans heavily on mining, agriculture, and nascent services sectors. Growth forecasts remain positive, anticipating moderate annual GDP growth near 5-6% over the next 5 years.

Household incomes are constrained by high inequality, with significant portions living below the poverty line. Consumer discretionary spending is limited but rising, particularly in urban areas where younger demographics are adopting digital lifestyles aligned with entertainment consumption.

Disposable income is predominantly channeled into food, basic services, and increasingly mobile communication, with leisure and gaming a small but emergent category.

| Indicator | Value / Projection |

|---|---|

| GDP Nominal (2024) | $14 billion USD |

| GDP Growth Rate (Annual) | 5.2% |

| GDP Per Capita (2024) | $1,060 USD |

| Projected GDP Growth (2025-2026) | 5-6% annually |

| Inflation Rate | 8-10% range |

Market Size and Growth Projections

The overall iGaming market in Guinea is small but poised for growth given improving digital access and rising urban incomes. Current regulated gambling sectors generate limited revenue, but projections estimate compound annual growth rates (CAGR) of 8-12% over five years for sports betting and digital lottery channels. The average revenue per user (ARPU) remains low compared to mature markets, averaging under $30 USD annually due to economic constraints.

| Metric | Value |

|---|---|

| Current Market Revenue | ~$15 million USD |

| Forecast Market Revenue (2030) | ~$30 million USD |

| Projected CAGR | 8-12% |

| User Base (2025) | ~200,000 active gamblers |

| ARPU | ~$28 USD per year |

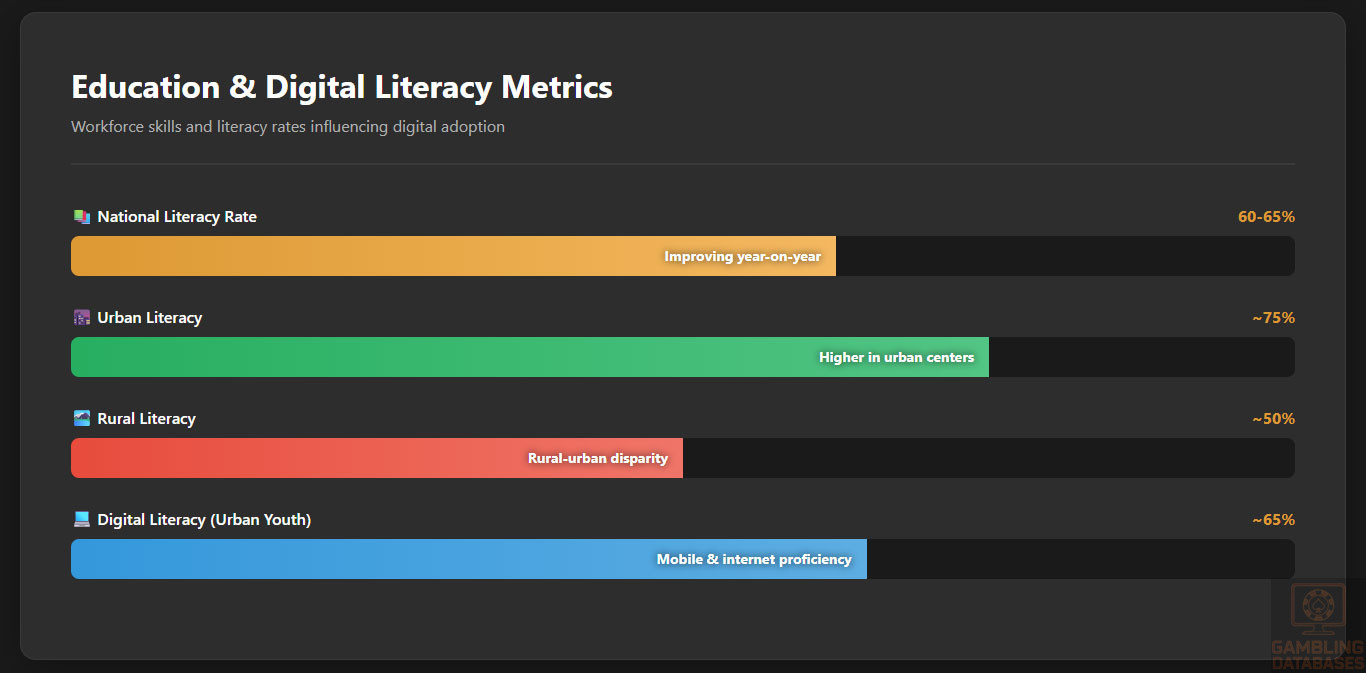

Education, Skills, and Digital Literacy

Guinea has made strides in improving literacy, reaching rates near 60-65% nationally, although disparities persist between urban and rural populations. Secondary and tertiary education levels remain low overall but are increasing year-on-year.

Digital literacy is uneven, with most users in urban areas proficient in basic internet functions and mobile applications. This growing digital familiarity among youth supports the adoption of online entertainment services, including iGaming platforms. Workforce skills are primarily technical in urban centers, where the digital economy shows the most promise for expansion.

Cultural and Social Factors

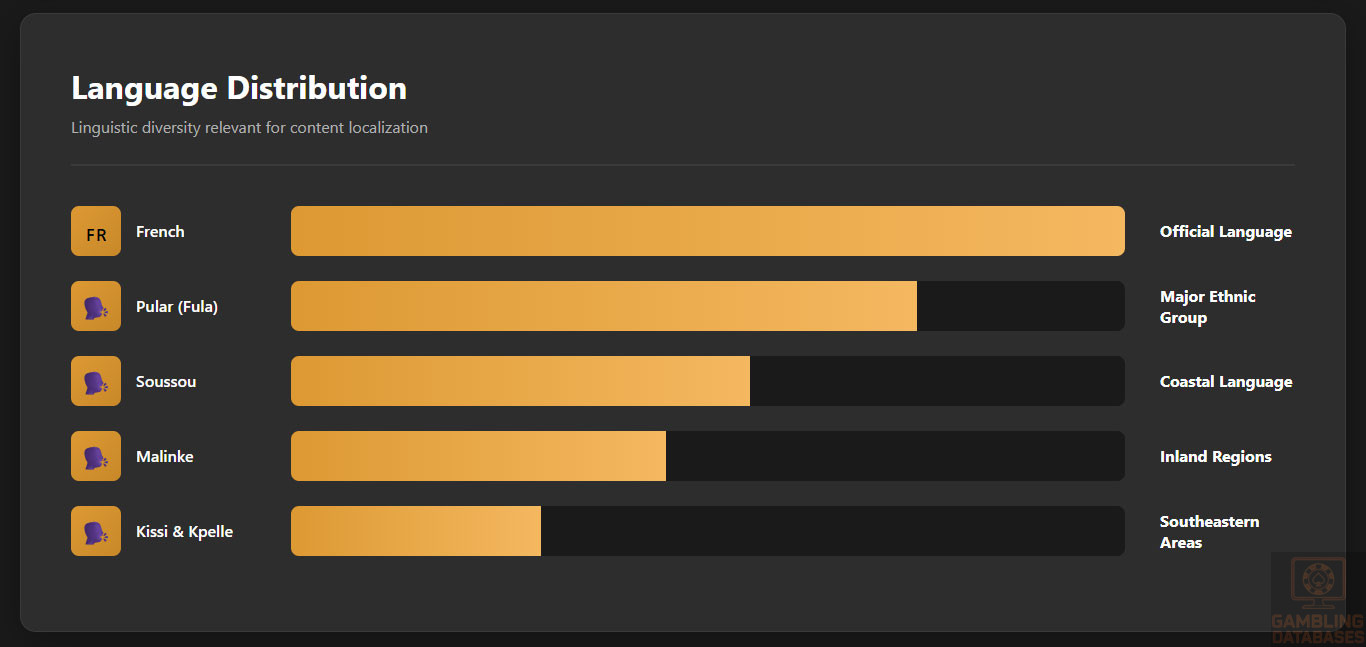

Communication and Language

Guinea is linguistically diverse with multiple ethnic groups and languages spoken. The official language is French, widely used in formal communications and online content. Several regional languages and dialects coexist, influencing media consumption and digital communication patterns.

- French (official, used in government and education)

- Pular (spoken by the Fula ethnic group)

- Soussou (major coastal language)

- Kissi and Malinke dialects prevalent in inland regions

- Kpelle and other local languages in southeastern areas

Cultural Attitudes

Gambling acceptance varies culturally, with traditional games and lotteries generally viewed positively when state-endorsed. Religious and social norms in some communities discourage gambling, associating it with moral concerns. Foreign brand penetration is cautious due to local preference for domestic or regional operators and limited digital trust.

Entertainment preferences among youth favor mobile-based social and gaming apps, aligning with increasing smartphone penetration and social media engagement. This suggests a receptive market for convenient iGaming products tailored to local language preferences and cultural nuances.

Problem Gambling and Social Considerations

There is limited data on problem gambling prevalence, though anecdotal evidence suggests increasing concerns among urban youth and frequent bettors. Government and NGO responses include nascent awareness campaigns and integration of responsible gambling messaging within licensed operator programs.

Social responsibility obligations for operators are emerging but lack detailed legal mandates, relying instead on voluntary compliance. Measures such as self-exclusion programs, counseling referrals, and deposit limits are recommended but not rigorously enforced yet.

- Public awareness programs on gambling risks

- Support services via health and social ministries

- Collaboration with community organizations to address addiction

- Implementation of self-exclusion schemes by licensed operators

- Monitoring and reporting of suspicious betting patterns

Political Structure and Governance

Guinea is a presidential republic with a centrally governed political system emphasizing economic reform and regulatory stability. Political stability has improved since 2022 with strengthened institutional frameworks, though governance challenges remain in enforcement consistency. International relations focus on attracting foreign investment and enhancing trade partnerships, supporting a business-friendly environment for licensing and economic activities.

Technology Adoption and Digital Behavior

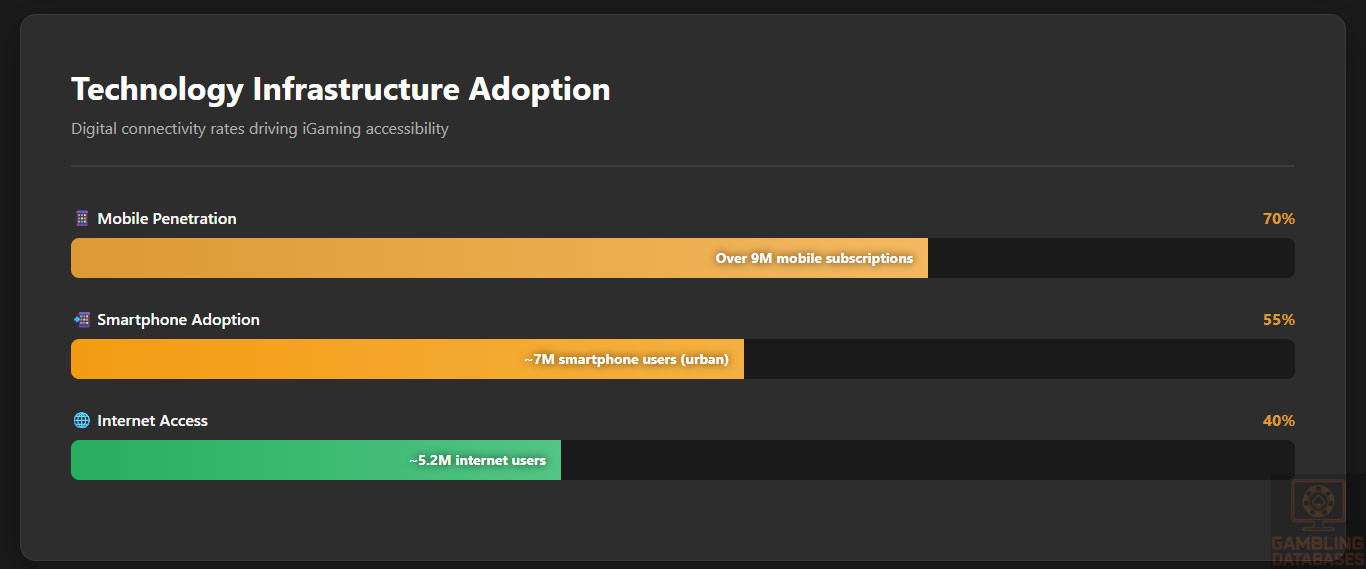

Internet and Digital Usage

Internet penetration stands at approximately 40%, constrained by infrastructure and cost barriers outside urban areas. Mobile telephony networks are more extensive, covering over 70% of the population, driving online activities predominantly through smartphones.

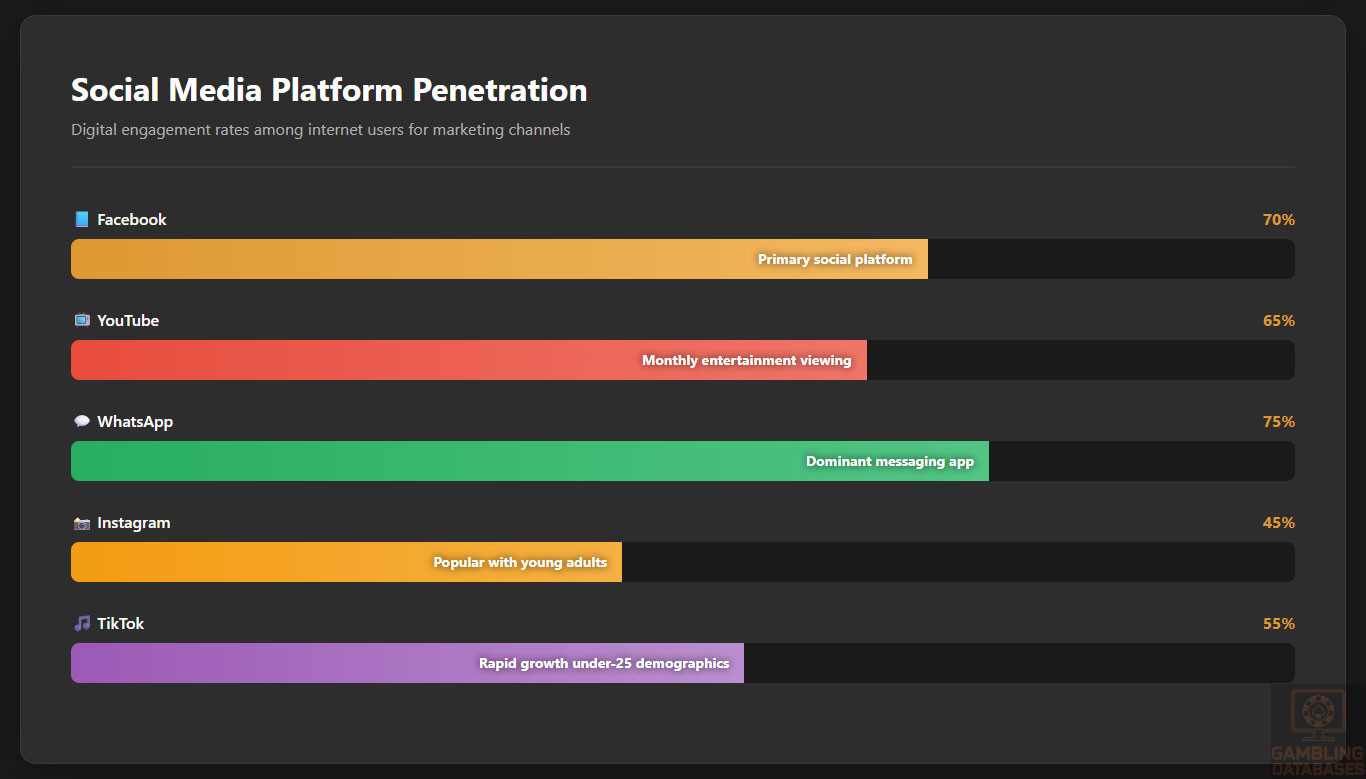

Social media engagement is robust in urban centers, fueling consumer awareness and digital entertainment consumption. Platforms serve as marketing channels for gambling operators, enhancing brand presence and customer interaction.

- Facebook with over 70% penetration among internet users

- YouTube accessed by 65% monthly for entertainment content

- WhatsApp dominant for messaging and social communication

- Instagram popular with urban youth and young adults

- Twitter used selectively for news and public discourse

- TikTok growing fast among under-25 demographics

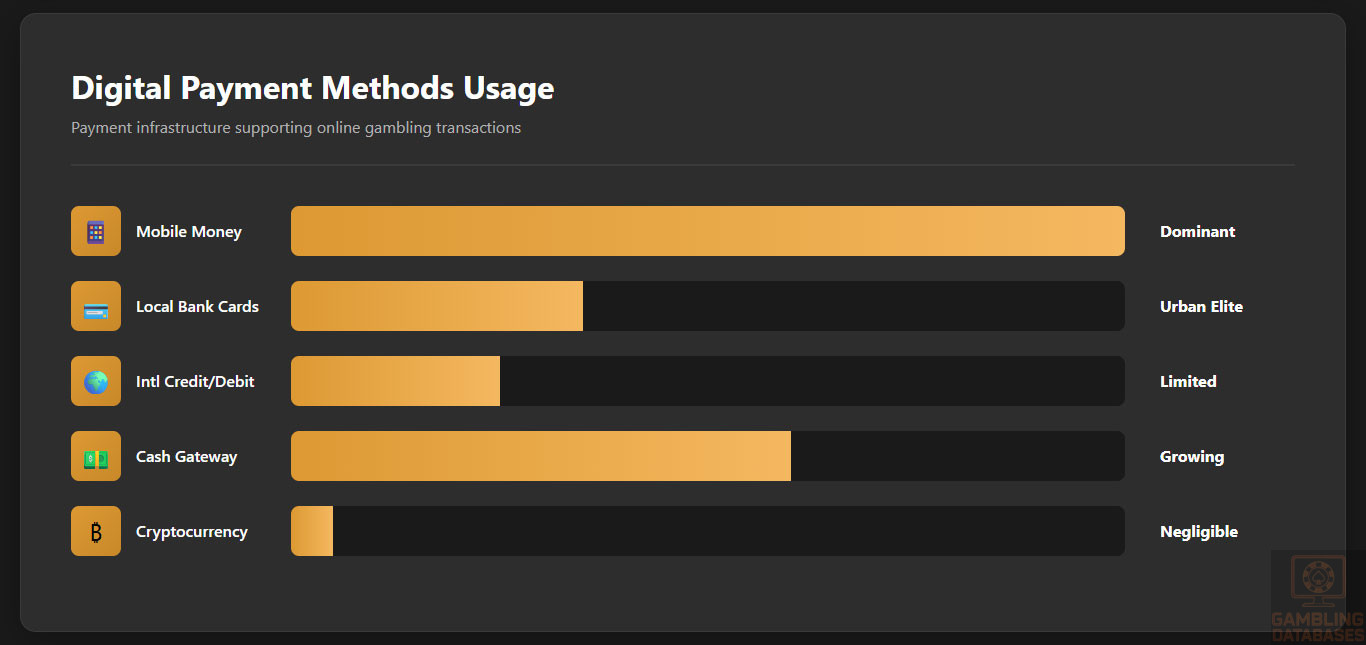

Digital Payment Behavior

Payment methods for online transactions increasingly favor mobile money solutions due to limited banking penetration. Debit and credit cards are used primarily by the urban elite, while cash remains dominant in rural areas, slowing broader iGaming monetization.

Cryptocurrency adoption is negligible but observed as a growing trend among younger, tech-savvy users cautious of formal financial institutions. Digital wallets and mobile payment integration form critical enablers of market growth.

- Mobile money services (e.g., Orange Money, MTN Mobile Money)

- Local bank card transactions

- International credit/debit cards

- Cash-to-digital gateway services for unbanked users

- Emerging interest in cryptocurrency payments among niche groups

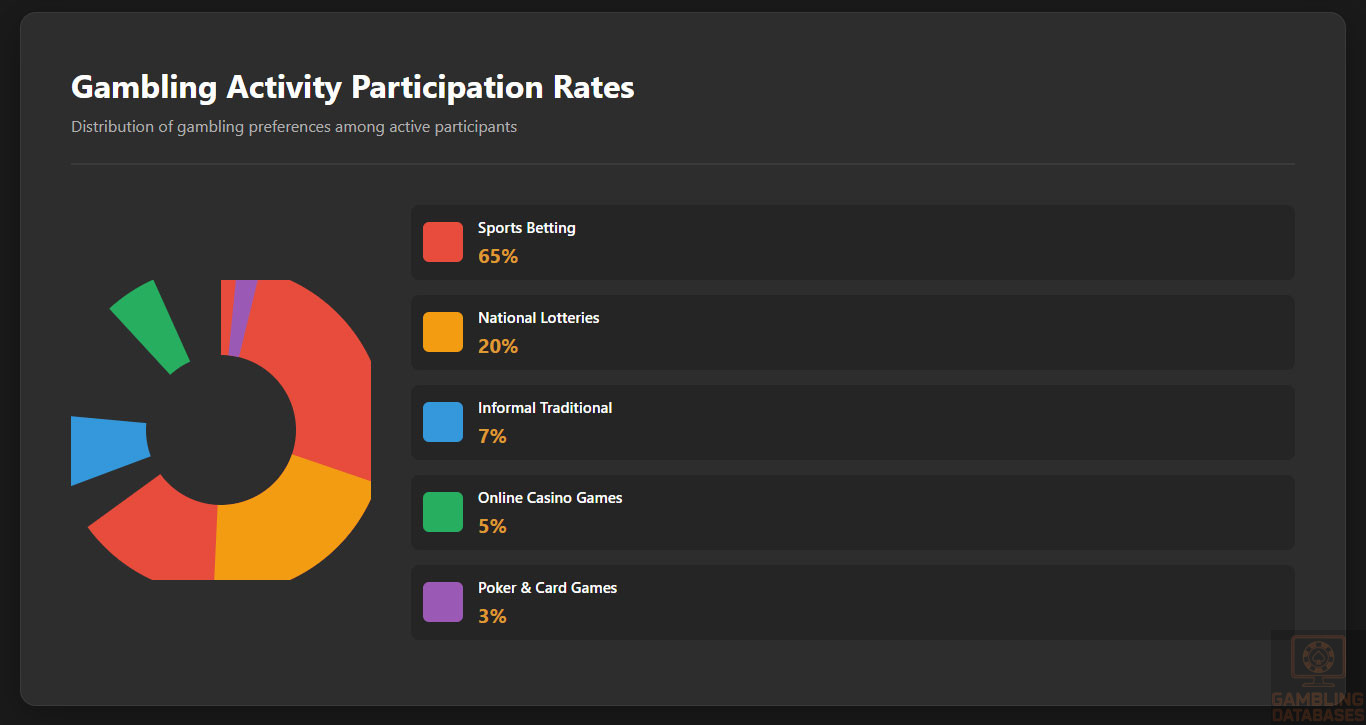

Gaming and Gambling Preferences

Current Market Participation

Sports betting dominates Cambodia’s existing gambling participation, with lottery games as the second most popular activity. Casino gaming and online poker remain marginal but attracting attention from urban demographics familiar with digital platforms.

- Sports Betting (~65% participation)

- National Lotteries (~20% participation)

- Informal Traditional Gambling (~7%)

- Online Casino Games (~5%)

- Poker and Card Games (~3%)

Consumer Behavior Patterns

Consumers typically engage in betting activities during weekends and major sporting events, with session lengths averaging 30-45 minutes online. Retention correlates strongly with localized content offerings and reliable payment options.

The young demographic shows a preference for mobile-first gaming experiences, social interaction features, and promotional incentives. Spending is cautious but rising as disposable income and trust in digital platforms improve.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Guinea’s population is approximately 13 million in 2025, with a notably young age profile. The median age is under 20 years, driven by a high proportion of children and youth in the population. Gender distribution is balanced with a slight male majority.

Urbanization is moderate; roughly 40% of residents live in urban areas, primarily concentrated in a few major cities, while the majority remains rural. This urban-rural spread influences internet access availability and concentration of gambling venues.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 42% |

| 15-24 years | 20% |

| 25-54 years | 30% |

| 55-64 years | 4% |

| 65 years and over | 4% |

Geographic Distribution

Population is mainly concentrated in urban centers, notably the capital Conakry and the surrounding coastal zone. Economic opportunities and infrastructure are most developed here, supporting higher consumption and entertainment activities, including gambling.

Internet access and gambling services are focused in these cities, while rural regions experience lower penetration due to infrastructural limitations.

- Conakry – ~2.3 million

- Kankan – ~500,000

- Labé – ~300,000

- Nzérékoré – ~250,000

- Kindia – ~200,000

Economic Indicators and Consumer Spending Power

Guinea’s nominal GDP is around $14 billion USD, with a per capita income near $1,060. The economy heavily depends on mining, agriculture, and emerging services. GDP growth is forecast at around 5-6% annually for the next five years, indicating moderate economic expansion.

Income inequality is notable, with many households below the poverty line, limiting broad consumer spending power. Nonetheless, urban populations show increased discretionary income, contributing to a budding entertainment and digital services market.

| Indicator | Value/Projection |

|---|---|

| GDP (Nominal, 2024) | $14 billion |

| GDP Growth Rate | 5.2% |

| GDP Per Capita | $1,060 |

| Inflation Rate | 8-10% |

| Projected GDP Growth (2025-26) | 5-6% annually |

Market Size and Growth Projections

The iGaming market remains small but poised for growth. Estimated market revenue is near $15 million USD with projections anticipating near doubling by 2030.

CAGR is expected to reach 8-12%, driven by mobile penetration and urban consumer adoption. Average revenue per user remains modest at below $30 USD, reflecting income limitations.

| Metric | Value |

|---|---|

| 2025 Market Revenue | $15 million |

| 2030 Forecast Revenue | $30 million |

| Projected CAGR | 8-12% |

| User Base | ~200,000 active gamblers |

| Average Revenue Per User (ARPU) | $28 |

Education, Skills, and Digital Literacy

Literacy rates have improved to approximately 60-65%, though rural-urban disparities remain. Secondary and tertiary education participation is growing but still below regional averages.

Digital literacy aligns closely with education and urban residency. Urban youth are increasingly proficient with internet and mobile technologies, supporting online entertainment uptake including iGaming products. Workforce skill levels are rising in urban hubs alongside technology adoption.

Cultural and Social Factors

Communication and Language

French is the official language used in formal settings and digital content. Multiple indigenous languages shape cultural communication, relevant for localizing content and marketing.

- French (official language)

- Pular (Fula ethnic group)

- Soussou (coastal areas)

- Kissi and Malinke (inland regions)

- Kpelle (southeastern areas)

Cultural Attitudes

Gambling acceptance varies by community; state lotteries and traditional games enjoy broad social acceptance, while religious and social norms in some groups discourage gambling. Foreign brands face cautious reception, often relying on local partnerships.

Entertainment preferences tilt toward mobile-based and social media-driven content, reflecting youthful demographics and growing smartphone ownership.

Problem Gambling and Social Considerations

Data on problem gambling is limited but urban youth show rising risk patterns. Government and NGOs have initiated public awareness programs, though social responsibility frameworks remain at early stages.

- Public education programs on gambling risk

- Support services via health and social ministries

- Community outreach for addiction mitigation

- Self-exclusion schemes by some licensed operators

- Suspicion reporting and transaction monitoring

Political Structure and Governance

Guinea is a presidential republic with increasing political stability since 2022 reforms. The government prioritizes economic reform and foreign investment attraction, underpinning a more predictable regulatory environment for businesses.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration is about 40%, concentrated in urban and peri-urban areas, while mobile phone coverage exceeds 70% nationwide, driving digital adoption. Social media is a critical engagement platform for urban populations and youth.

- Facebook (70%+ penetration among internet users)

- YouTube (65% monthly users)

- WhatsApp (dominant messaging app)

- Instagram (popular with young adults)

- Twitter (focused on news consumers)

- TikTok (rapid growth among under-25s)

Digital Payment Behavior

Mobile money solutions dominate digital payments due to limited banking access. Card payments are mainly urban and elite, while cash-to-digital gateway services assist unbanked users. Cryptocurrency use is negligible but emerging among tech-savvy niches.

- Mobile Money (Orange Money, MTN Mobile Money)

- Local Bank Cards

- International Credit/Debit Cards

- Cash-to-Digital Gateway Services

- Early Cryptocurrency Adoption

Gaming and Gambling Preferences

Current Market Participation

Sports betting leads with a majority participation rate. Lotteries remain popular, while online casinos and poker gain gradual traction, especially among urban youth.

- Sports Betting (~65% participation)

- National Lotteries (~20% participation)

- Informal Traditional Gambling (~7%)

- Online Casino Games (~5%)

- Poker and Card Games (~3%)

Consumer Behavior Patterns

Betting preferences peak during weekends and major sports events, with average online session lengths of 30-45 minutes. Mobile-first experiences with localized content and promotions drive user retention. Spending is cautious but growing with economic and digital confidence.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Guinea’s internet penetration stands at approximately 40%, mainly concentrated in urban areas like Conakry. Broadband connectivity remains limited, with mobile networks providing the bulk of internet access. Average connection speeds reach around 10 Mbps in cities but drop significantly in rural zones due to weaker infrastructure.

Network reliability is improving, driven by government initiatives and foreign investment aimed at expanding fiber-optic cables and enhancing mobile capacities. Despite these efforts, intermittent power supply and geographic challenges hinder seamless connectivity outside major urban centers.

5G and Future Technology Deployment

5G technology adoption is in nascent stages, with pilot rollouts initiated by key mobile operators in Conakry since late 2024. Full national 5G coverage is projected over the next five years, focusing initially on business districts and high-density urban corridors. This upgrading supports faster data transmission essential for real-time gaming and streaming services.

The mobile operator landscape remains dynamic, with competition fostering accelerated technology adoption backed by infrastructural development funds. Expansion plans emphasize rural inclusivity to broaden digital service access.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Guinea’s telecom sector comprises multiple mobile network operators with varying market shares and service coverage. The market is dominated by three major players that collectively hold over 85% of subscriptions, ensuring competitive pricing and broad coverage.

- Orange Guinea – approximately 45% market share, widespread network including rural areas

- MTN Guinea – around 30% market share, strong urban presence and data services

- Cellcom – 12% market share, regional focus with growing 4G investment

- Areeba (now part of Orange) – legacy smaller operator with network overlap

- Liberty Telecom – emerging player focusing on urban digital innovations

Device Penetration

Smartphone adoption exceeds 55% among urban adults, driven by affordable devices and increasing mobile broadband coverage. Entry-level Android models dominate due to price sensitivity, while premium devices are rare but rising among younger professionals. Usage patterns reveal predominant engagement in social media, messaging, and entertainment apps including betting platforms.

Financial Services and Payment Infrastructure

Banking System Structure

The banking system in Guinea is developing, characterized by local and regional banks experimenting with digital services. Account penetration remains below 20%, limited by economic factors and infrastructural challenges. Urban areas show more rapid adoption of digital banking frontline services enhancing consumer accessibility.

- Banque Centrale de la République de Guinée (BCRG) – central bank with regulatory oversight

- Banque Internationale pour le Commerce et l’Industrie de Guinée (BICIGUI) – market leader with extensive branches

- Banque de Développement de Guinée (BDG) – focused on sector financing

- Orabank Guinea – regional operator expanding digital banking

- NSIA Banque Guinée – emerging player promoting digital financial inclusion

- UBA Guinea – international bank with corporate service strength

Payment Processing Options

Payment landscape strongly favors mobile money services, which account for the majority of digital transactions especially in the unbanked population segments. Card payments are confined largely to urban elites, with limited rural penetration. Bank transfers and cash-to-digital mechanisms support e-commerce and betting transactions.

- Mobile Money (Orange Money, MTN Mobile Money) – dominant for P2P and merchant payments

- Debit and Credit Card payments – limited urban usage, growing with ATM installations

- Bank transfers – used mainly by companies and high-value transactions

- Cash-to-digital services – bridging the gap in rural and cash-dominant environments

- Online payment gateways (local and regional) – integrating with e-commerce and gaming platforms

E-commerce and Digital Economy

Guinea’s e-commerce sector is modest but progressing, with online retail accounting for under 5% of total retail sales. Consumer trust and logistical challenges constrain rapid growth. However, digital service adoption, including mobile entertainment and financial services, is driving ecosystem expansion. Cross-border e-commerce and digital freight solutions are beginning to lower barriers.

This expanding digital economy creates foundational opportunities for iGaming platforms that can leverage mobile payment integration and localized content to unlock new customer segments.

Business Environment and Regulatory Framework

Ease of Business Operations

Guinea ranks moderately in global business ease indices, with improving but still complex procedures for establishing companies and regulatory compliance. Foreign investment policies are welcoming but require navigation of bureaucratic hurdles. Operational costs are relatively low, balanced by challenges such as inconsistent utility provision and regulatory transparency.

- Documentation preparation and notarization (2-3 weeks)

- Registration submission with Companies Registry (5-7 days)

- Tax registration and obtaining tax ID (3-5 days)

- Opening bank account and minimum capital deposit (1-2 weeks)

- Business license application and final approvals (2-4 weeks)

Corporate Structure and Registration

Common corporate entities include Limited Liability Companies (LLCs), Corporations, and Branch Offices. LLCs are preferred for local operations due to flexible governance and liability protection. Foreign investors favor branch offices for market testing under parent company oversight. Compliance requirements incorporate standard reporting and tax obligations.

Required registration documents typically include these items:

- Certificate of incorporation or equivalent

- Articles of association and bylaws

- Proof of valid address and contact details

- Identification documents of directors and shareholders

- Tax registration certificate

- Bank reference letters

- Proof of minimum capital deposit (if applicable)

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate is 25%. Guinean tax policy includes incentives such as tax holidays in special economic zones, aiming to attract foreign direct investment. Several double taxation treaties exist with regional and international partners to mitigate fiscal burdens on cross-border transactions.

- Benin

- France

- Morocco

- Senegal

- South Africa

Personal Income Tax

Personal income tax rates range from 0% to 35% based on progressive brackets. Withholding taxes apply to remunerations including gambling winnings for residents and non-residents. Social security contributions combine employee and employer payments per statutory rates. Tax residency is determined by physical presence exceeding 183 days annually.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry requires blending local partnerships, compliance with regulatory frameworks, and digital platform adaptability. Operators should prioritize mobile-first gaming solutions, integrate prevalent payment methods, and align marketing with cultural contexts. Strategic collaboration with local stakeholders and gradual expansion helps mitigate regulatory uncertainties.

- Establish local partnerships for regulatory navigation and market insight

- Develop mobile-optimized platforms compatible with low-bandwidth environments

- Implement flexible payment integrations focusing on mobile money

- Adopt robust compliance systems for AML and responsible gambling

- Leverage social media and localized marketing for customer acquisition and retention

Typical Costs and Timelines

Initial market entry costs involve license fees, legal consulting, platform development, and marketing investments. Operational costs include staff salaries, compliance management, and technical maintenance. License application typically takes 1-3 months, with full operational readiness achieved within 6-12 months.

- License application fees and compliance deposits

- Legal and compliance advisory services

- Technology platform development and integration

- Marketing and customer acquisition budget

- Operational overheads including payroll and administration

| Phase | Duration |

|---|---|

| Preparation and Documentation | 2-3 months |

| Regulatory Application and Approval | 1-3 months |

| Platform Development and Testing | 2-4 months |

| Market Launch and Initial Operations | 1-2 months |

| Ongoing Compliance and Expansion | Continuous |

Success Factors and Challenges

Major success factors include responsive regulation, high mobile penetration, and growing youth engagement. Key challenges involve infrastructure gaps, limited banking inclusion, and evolving compliance landscapes. Understanding cultural nuances and local consumer behavior enhances market penetration.

- Strong regulatory compliance and good governance

- Mobile-friendly gaming experience optimized for local conditions

- Effective localization of content and customer support

- Reliable payment processing aligned with consumer habits

- Adaptation to political and economic volatility

Exit Strategy Planning

Exit possibilities are primarily through acquisition or license transfer, subject to regulatory approval. Market liquidity remains limited but is improving with growing investor interest. Proper valuation considers license tenure, local market penetration, and technological assets.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Guinea?

Online gambling is legal but only partially regulated under broader commercial gaming laws. The government requires operators to obtain licenses primarily through the Ministry of Economy, Finance and Planning. While licensed sports betting and lotteries operate legally, comprehensive regulation for online casinos remains limited but evolving.

2. What types of gambling licenses are available and what do they cover?

Licenses primarily cover sports betting outlets, national lottery operations, and general commercial gaming activities. Regulatory frameworks for online casinos and digital sportsbooks are in development. Operators must comply with AML, KYC, and tax regulations as part of licensing conditions.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees are relatively modest versus mature markets, with application costs depending on the scope of operations. The licensing process generally spans 1 to 3 months contingent on submission completeness and regulatory workload. Renewal fees and financial guarantees are also required annually.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain licenses provided they demonstrate local compliance capability, financial stability, and operational transparency. Local partnerships or designated representatives facilitate regulatory engagement. No explicit foreign ownership restrictions exist but regulatory approval can be more straightforward with domestic presence.

5. What are the tax obligations for iGaming operators?

Operators face a gross gaming revenue (GGR) tax of around 3% turnover, alongside the standard 25% corporate income tax. Additional licensing fees and turnover taxes may apply depending on the gaming category. Operators must file regular financial reports ensuring transparency and tax compliance.

| Tax Type | Rate | Comments |

|---|---|---|

| GGR Tax (Turnover) | 3% | Minimum rate; varies by license |

| Corporate Income Tax | 25% | Standard corporate rate |

| License Renewal Fees | Variable | Annual payment required |

6. Are gambling winnings taxed for players?

Currently, gambling winnings are not directly taxed by the Guinean government at the player level. Taxation is focused on the operators to streamline revenue collection. This policy encourages player participation by eliminating withholding duties on winnings.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, platform development, compliance management, marketing expenses, and staffing. Maintenance of payment integrations and customer support systems also contributes substantially to ongoing costs. Generally, initial setup and first-year operational costs require significant capital allocation but taper as market penetration matures.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines typically range from 2 to 4 years depending on market entry strategy, operational efficiency, and customer acquisition success. Early movers benefit from regulatory developments and growing consumer demand but must manage volatility in infrastructure and regulatory enforcement.

9. What are the local presence requirements for operators?

Operators must have a local legal entity or register a local representative to comply with licensing conditions. A physical registered address and a designated compliance officer are usually required to interact with regulatory authorities and ensure ongoing compliance.

10. What payment methods are available and recommended?

Mobile money services dominate as preferred payment methods due to their accessibility and consumer familiarity. Card payments are recommended for urban customers, while cash-to-digital services help in broader coverage. Integration with popular wallets and bank transfer systems is advised to maximize payment flexibility.

11. What are the advertising and marketing restrictions?

Advertising restrictions focus on prohibiting promotions targeting minors and banning deceptive or false claims. Marketing through social media, broadcast, and outdoor advertising is permitted with monitoring for compliance. Sponsorships are allowed but subject to transparency and content restrictions during certain hours.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification, robust KYC protocols, transaction monitoring, and provision of self-exclusion options. Operators must also promote awareness of gambling risks and allow players to access their betting history and limits.

13. How large is the iGaming market and what is the growth potential?

The current market is valued near $15 million USD, with expected compounded growth at 8-12% annually. Increasing mobile penetration and urbanization suggest substantial expansion potential, particularly in sports betting and digital lottery segments.

14. Who are the main competitors and what is their market share?

The market primarily features local lottery providers and licensed sports betting operators. International online casino operators are largely absent due to nascent regulation. Competition remains fragmented with scope for consolidation and foreign investment as regulatory clarity improves.

15. What are the player preferences and typical spending patterns?

Players prefer sports betting mainly on football events, with growing interest in lottery and casual online games. Spending is cautious, aligned with income levels, with higher engagement during weekends and sports tournaments. Mobile platforms with flexible payment options attract the largest user base.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, mobile-first technology adaptation, local market understanding, and secure payment integration. Challenges include infrastructural limitations, low banking inclusion, and evolving policy frameworks requiring agility and strong local partnerships.

- Effective regulatory compliance and transparent operations

- Robust mobile platform optimized for low connectivity

- Localization of gaming content and payment methods

- Strong marketing and customer engagement strategies

- Adaptive risk management considering economic volatility

Sources and References

- Guinea Gambling Regulatory Authority – Official Ministry Websites

- National Institute of Statistics, Guinea – Population and Demographic Data 2025

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics 2025

- Ministry of Economy, Finance, and Planning – License and Tax Regulations

- Central Bank of Guinea – Financial and Banking Sector Reports 2024

- Orange Guinea and MTN Guinea – Network Coverage and Market Data 2025

- Guinea National Institute of Statistics – Economic and Social Surveys

- GSMA Intelligence – Mobile Market Analysis Sub-Saharan Africa 2025

- PwC – African Tax and Regulatory Framework Reports 2024

- UNDP Reports on Digital Literacy and Education in Guinea

- Guinea Ministry of Communication – Media Statistics 2025

- GameTech Industry Reports – 2024 Africa iGaming Market Overview

- Consulting Reports – Market Entry Strategies in African iGaming Sectors

- Local News Outlets – Updates on Regulatory Changes 2024-2025

- Financial Times – Emerging African Digital Markets Report 2025

- World Economic Forum – Digital Economy and Infrastructure Reports 2024

- International Monetary Fund – Economic Outlook Guinea 2025

- Oxford Economics – Regional Consumer Behavior Studies

- European Gaming and Betting Association – African Market Profiles 2024

- Guinean Ministry of Health – Responsible Gambling and Social Programs

- TeleGeography – African Internet and Data Networks Analysis 2025

- Mobile Money Network Providers – Market Penetration Reports

- Financial Action Task Force (FATF) – AML Standards for Africa

- Guinea Chamber of Commerce – Business Registration Guidelines

- Industry Whitepapers – Online Gambling Platform Adaptations for Africa

- Local NGOs – Gambling Awareness and Support Initiatives

- Mintel Reports – African Consumer Trends and Digital Adoption

- International Labour Organization – Workforce Development Guinea

- GlobalData – African Telecom Sector Forecasts 2025

- Various Academic Journals on African Digital Markets and Regulatory Frameworks

🎯 Gambling Databases Country Rating: Guinea

| Evaluation Dimension | Score | Rating |

|---|---|---|

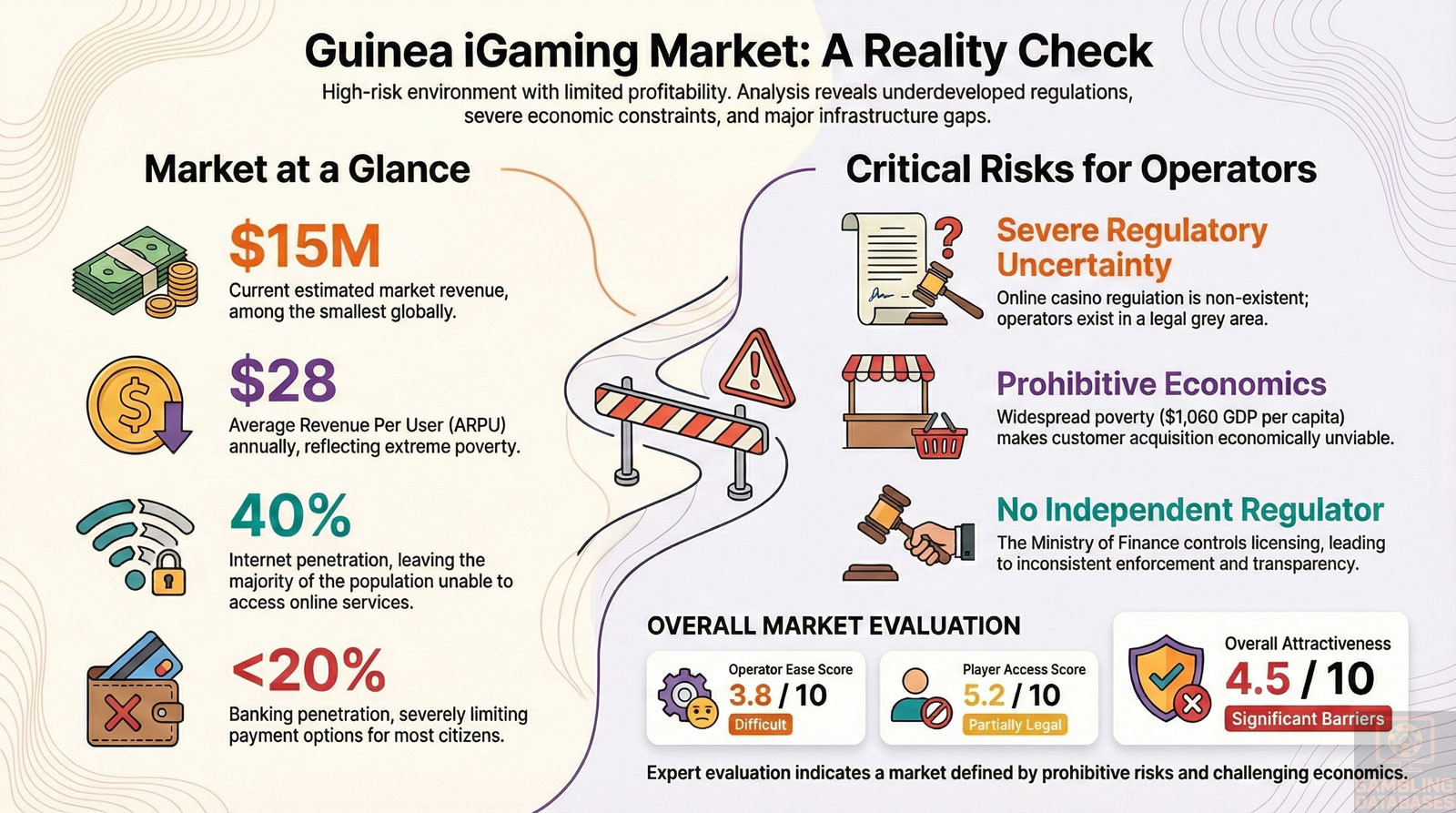

| Operator Ease Score | 3.8/10 | 🔴 Difficult |

| Player Access Score | 5.2/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 4.5/10 | Emerging market with significant barriers and regulatory uncertainty |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- NO COMPREHENSIVE ONLINE CASINO REGULATION: Online casinos operate in a legal grey area with no formal regulatory framework specifically tailored to remote gambling platforms. This creates massive legal uncertainty.

- NO INDEPENDENT GAMING REGULATOR: All licensing controlled by Ministry of Economy, Finance and Planning, resulting in inconsistent enforcement and variable procedural transparency.

- REGULATORY FRAMEWORK IS “FORMATIVE” AND “DEVELOPING”: The country explicitly acknowledges its gambling regulations are in early stages with “significant variation” across categories and “practical implementation challenges.”

- LAND-BASED CASINOS HAVE NO LEGAL FRAMEWORK: Casino operations and slot machine venues lack clear regulatory guidelines and remain “largely undeveloped commercially and legally.”

- OFFSHORE OPERATORS FACE UNCERTAINTY: No defined online licensing framework for international operators, limited government monitoring of offshore sites, unclear enforcement mechanisms.

- EXTREME POVERTY LIMITS PROFITABILITY: GDP per capita only $1,060 USD (2024), with “significant portions living below poverty line” – this severely constrains consumer spending power.

- INFRASTRUCTURE CHALLENGES: Only 40% internet penetration, less than 20% banking penetration, “intermittent power supply” outside cities, unreliable connectivity in rural areas.

- TINY MARKET SIZE: Total estimated market revenue only ~$15 million USD with ~200,000 active gamblers and ARPU under $30 annually – among the smallest markets globally.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.75/3.0 | Sports betting partially legal (+1.5). Online casinos NOT comprehensively regulated – operate in grey area with “no formal regulatory body dedicated solely to online gaming” (-1.5). Land-based casinos have NO clear legal framework (-0.5). Regulatory provisions “under development” creating massive uncertainty (-0.5). Monitoring of offshore operators explicitly described as limited (-0.25). Final: 0.75/3.0 |

| Licensing Process | 25% | 1.0/2.5 | Licensing available but process described as “underdeveloped” (+1.0). Timeline 1-3 months is reasonable (+0.5). License fees “modest” but vague (+0.25). However: “Variable procedural transparency” (-0.25). No independent regulator, all through Ministry (-0.25). “Detailed requirements specific to remote gambling platforms are under development” means no clear standards (-0.25). International operators have “limited presence due to lack of defined online licensing framework” (-0.25). Total costs unclear but likely under €100k (+0.25). Final: 1.0/2.5 |

| Taxation & Costs | 20% | 1.25/2.0 | GGR tax minimum 3% is excellent (+2.0). Corporate income tax 25% is reasonable (no deduction). However: “Other tax obligations” mentioned but not specified creating uncertainty (-0.25). Turnover tax “applicable to some categories” adds complexity (-0.25). Operational costs appear low which is positive (+0.25). Extremely low ARPU ($28 annually) means high customer acquisition costs relative to revenue potential (-0.5). Final: 1.25/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | No explicit mandate for physical offices (+0.5). Foreign ownership permitted (+0.25). However: “Regulatory environment favors operators with local corporate presence” effectively requiring local setup (-0.25). Must provide “proof of financial stability” including financial guarantees (-0.25). Banking penetration under 20% severely limits payment options (-0.25). No cryptocurrency adoption mentioned, mobile money dominates (-0.25). “Routine financial audits” and “periodic reporting” add compliance burden (-0.25). Final: 0.5/1.5 |

| Market Environment | 10% | 0.3/1.0 | Business environment described as “moderately ranked” with “improving but still complex procedures” (+0.5). However: “Bureaucratic hurdles” for foreign investment (-0.25). “Inconsistent utility provision” including intermittent power supply outside cities (-0.25). Described as “nascent stage” and “formative” market (-0.1). “Enforcement consistency” identified as governance challenge (-0.1). No strict advertising laws is positive but promotional activities “monitored” without clear guidelines (-0.1). Market structure “relatively informal” due to lack of independent authority (-0.25). Regulatory updates “incremental” and slow (-0.1). Final: 0.3/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Sports betting legal for players (+2.0). National lottery legal (+0.5). Online gambling described as “legal” but “not yet comprehensively regulated” (+0.5). However: Online casinos operate in grey area with no clear legal framework (-1.0). Land-based casino access essentially non-existent due to no regulation (-0.5). Massive legal uncertainty for players using online casinos (-0.5). Final: 2.0/4.0 |

| Practical Accessibility | 30% | 1.5/3.0 | Multiple payment methods available including mobile money (+1.0). No evidence of ISP blocking (+0.5). However: Banking penetration under 20% severely limits options (-0.5). International card use “limited urban usage” only (-0.25). Internet penetration only 40% leaving 60% of population without access (-0.5). Rural areas face “accessibility challenges” (-0.25). “Reliable mobile networks but internet broadband still limited” (-0.25). Cryptocurrency adoption “negligible” (-0.25). Final: 1.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | Currently no direct player tax on winnings (+2.0). No evidence of penalties for players using gambling services. No enforcement actions against individual players mentioned. Final: 2.0/2.0 |

| Market Availability | 10% | 0.4/1.0 | Licensed market “dominated by state-run or state-sanctioned entities” indicating very limited operator choice (+0.4). “Small number of sports betting operators” (+0.2). International operators have “limited presence” (+0.1). Land-based casinos “almost non-existent” (-0.2). No independent regulatory authority results in “relatively informal market structure” limiting quality options (-0.1). Final: 0.4/1.0 |

🔍 Key Highlights

Strengths (Minimal)

- Low taxation: 3% minimum GGR tax is among the lowest globally, plus 25% corporate tax is reasonable

- No player penalties: Players face no direct taxation or criminal penalties for gambling activities

- No ISP blocking: No evidence of government blocking offshore gambling websites

- Growth potential: Young demographic (median age 19.5 years) and mobile penetration over 70% provide foundation for future growth

- Projected market growth: 8-12% CAGR forecast over next 5 years, though from tiny base

⛔️ CRITICAL RISKS AND CHALLENGES

- REGULATORY UNCERTAINTY – MAJOR RED FLAG: Framework explicitly described as “formative,” “developing,” “nascent stage” with regulations “under development.” Online casino regulation is NON-EXISTENT – platforms operate in legal grey area with no formal regulatory body.

- NO INDEPENDENT GAMING REGULATOR: Ministry of Economy, Finance and Planning controls everything, resulting in “variable procedural transparency” and “relatively informal market structure.” This is a massive governance red flag.

- LAND-BASED CASINOS HAVE NO LEGAL FRAMEWORK: Document explicitly states casinos and slot machines “lack clear regulatory frameworks” and remain “largely undeveloped commercially and legally, with minimal government oversight.”

- EXTREME POVERTY KILLS ECONOMICS: GDP per capita $1,060 USD (one of world’s lowest), “significant portions living below poverty line,” household incomes “constrained by high inequality.” ARPU only $28 annually – this makes customer acquisition economically unviable for most operators.

- TINY MARKET SIZE: Total market revenue only ~$15 million USD with ~200,000 active users. For context, this is smaller than a single successful casino in mature markets. Market is “small but growing” but starting from almost nothing.

- INFRASTRUCTURE IS INADEQUATE: Only 40% internet penetration, banking under 20%, “intermittent power supply” outside cities, “unreliable connectivity in rural areas,” broadband “still limited.” Document admits “infrastructure gaps” as major challenge.

- PAYMENT METHOD LIMITATIONS: Credit/debit cards “limited urban usage,” cryptocurrency “negligible,” 80% population unbanked. Mobile money dominates but creates dependency on telecom providers.

- OFFSHORE MONITORING LIMITED: Document explicitly states “monitoring of offshore operators” faces “practical implementation challenges.” Government lacks capacity to regulate international operators effectively.

- LICENSING PROCESS UNDERDEVELOPED: Requirements for online platforms “under development,” “variable procedural transparency,” no clear standards for remote gambling. International operators have “limited presence due to lack of defined online licensing framework.”

- ENFORCEMENT INCONSISTENCY: “Enforcement consistency” identified as governance challenge. “Practical implementation challenges remain” in monitoring and regulatory updates are only “incremental.”

- MARKET LIQUIDITY NEAR ZERO: Document admits “market liquidity remains limited” for exit strategies. If you enter, getting out will be extremely difficult.

- LOCAL PARTNERSHIP REQUIRED: While not mandatory, “partnerships with local businesses can facilitate smoother regulatory engagement” – effectively requires finding reliable local partner in underdeveloped market.

Player-Specific Issues

- 60% of population has NO internet access – majority of country cannot access online gambling at all

- 80% unbanked – vast majority cannot fund gambling accounts through traditional banking

- Legal uncertainty for online casino players – no clear regulatory framework means players don’t know if their activity is truly legal

- Limited operator choice – market dominated by state-run entities with “small number” of licensed private operators

- Rural accessibility challenges – betting shops and lottery outlets “cluster in populated urban districts” leaving rural areas underserved

- Quality concerns – “relatively informal market structure” due to lack of independent regulator raises questions about operator standards

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $200,000-500,000 USD (licensing, legal, platform development, marketing, local setup)

Monthly Operating Costs: $20,000-40,000 USD (staff, compliance, technical maintenance, marketing)

Effective Tax Rate on Revenue: ~28-30% (3% GGR minimum + 25% corporate income tax + potential turnover tax)

Customer Acquisition Cost: Likely $50-150 per customer (marketing difficult in low-income market with limited digital channels)

Time to Breakeven: 3-5 years MINIMUM (if ever) given tiny market size and low ARPU

Time to Positive ROI: 5-7+ years assuming market develops as projected and regulations stabilize

Profitability Assessment: ECONOMICS ARE PROHIBITIVE FOR MOST OPERATORS. With total market size only $15 million and ARPU of $28 annually, even capturing 10% market share would generate only $1.5 million annual revenue. Against $240,000-480,000 annual operating costs, this market cannot support profitability except for the smallest, lowest-cost operators willing to operate at minimal scale for 5+ years waiting for market development.

The combination of extreme poverty ($1,060 GDP per capita), tiny user base (200,000 total), infrastructure challenges, and regulatory uncertainty makes this market suitable ONLY as a long-term speculative play for operators with significant capital who can afford losses for years. Any operator requiring positive ROI within 3-5 years should avoid Guinea entirely.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | Operating in legal grey area with no formal regulatory framework. No evidence of blocking but also no legal protection. Regulatory clarity could change at any time. Limited government monitoring capacity means current tolerance could end abruptly. |

| Licensed Sports Betting Operators | Medium | Clearer legal framework but “variable procedural transparency” and “relatively informal market structure” create uncertainty. Regulatory requirements “under development” means rules can change. No independent regulator means inconsistent enforcement. |

| Affiliates/Advertisers | Medium | No evidence of prosecution but “promotional activities monitored” without clear guidelines. Operating in grey area for online casinos. Regulatory environment could tighten at any time given “incremental” ongoing updates. |

| Payment Processors | Medium | Banking system “developing” with less than 20% account penetration. Regulatory oversight of financial services exists but gambling-specific payment rules unclear. Mobile money providers dominate but regulatory treatment uncertain. |

| Company Directors/Executives | Low-Medium | No evidence of personal liability for directors. However, criminal prosecution possible “in severe cases” for fraud or money laundering. Governance challenges and enforcement inconsistency create unpredictability. |

🚨 Extradition and International Enforcement

Extradition Treaties: Limited information available. Guinea maintains diplomatic relations with France, USA, and regional African nations, but specific gambling-related extradition precedents are not documented in available materials.

Enforcement History: No documented cases of international prosecution or extradition related to gambling violations. Enforcement capacity appears limited given “practical implementation challenges” in monitoring offshore operators.

Safe Jurisdictions: Not applicable – no evidence of aggressive international enforcement.

Travel Risk: Low – no documented history of pursuing gambling operators internationally. However, regulatory environment is “developing” and could evolve.

📋 Final Verdict

Guinea receives an Operator Ease Score of 3.8/10 and a Player Access Score of 5.2/10, resulting in an overall market attractiveness rating of 4.5/10.

HONEST ASSESSMENT:

Guinea represents one of Africa’s most challenging iGaming markets despite relatively low taxation. The regulatory framework is explicitly described as “formative,” “developing,” and “nascent” with online casino operations existing in a legal grey area without formal regulation.

The complete absence of an independent gaming regulator, combined with “variable procedural transparency” and a “relatively informal market structure,” creates massive uncertainty for operators. Most critically, the economics are simply prohibitive: with GDP per capita of only $1,060, total market size of ~$15 million, ARPU of $28 annually, and only 200,000 active users, this market cannot support profitable operations for the vast majority of operators.

The 40% internet penetration, under 20% banking penetration, and infrastructure challenges including “intermittent power supply” further constrain growth potential. Unless you are a micro-operator willing to operate at minimal scale for 5-7+ years waiting for market development, or a large operator making a long-term speculative bet on eventual market maturity, Guinea should be avoided. The regulatory uncertainty alone disqualifies this market for serious consideration by professional operators.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Micro-operator with total annual operating costs under $100,000 who can survive on minimal revenue

- Pan-African operator already established in neighboring markets seeking portfolio diversification

- Long-term speculative investor with 7-10 year horizon willing to accept losses for years

- Sports betting specialist focusing ONLY on licensed betting shops (not online casino)

- Mobile money or telecom company with existing infrastructure seeking adjacent revenue

- Willing to accept extreme regulatory uncertainty and “formative” legal framework

❌ Definitely Avoid If You Are:

- Casino-focused operator (online casinos have NO regulatory framework, operate in grey area)

- Any operator requiring positive ROI within 5 years (economics make this impossible)

- Medium or large operator with operating costs exceeding $200,000 annually (market too small)

- Operator requiring regulatory clarity and strong legal protections (framework is “under development”)

- Banking-dependent business model (less than 20% banking penetration)

- Operator targeting rural populations (60% have no internet access)

- Any business requiring functioning independent gaming regulator (doesn’t exist)

- Operators seeking market with established rules and enforcement (structure is “relatively informal”)

- Premium brand operator (extreme poverty with $1,060 GDP per capita limits market to ultra-budget segment)

⚠️ BOTTOM LINE: Guinea’s combination of extreme poverty, tiny market size, non-existent online casino regulation, absence of independent regulator, and infrastructure challenges make it suitable only for micro-operators or long-term speculators willing to lose money for 5+ years. The $15 million total market size and $28 ARPU make profitability mathematically impossible for most operators. Avoid unless you meet very specific criteria and can tolerate extreme uncertainty, minimal legal protections, and years of losses.

The landscape here changed drastically after the state-run LONAGUI reclaimed the marketing rights from private operators like Guinée Games. It’s a classic case of market nationalization. For any foreign operator looking to enter, the political risk is now the primary metric to consider, rather than just player LTV.