Guyana presents a unique opportunity in the iGaming sector, driven by recent regulatory developments and growing digital infrastructure. While land-based gambling is well-established, online gambling regulation is nascent and evolving, creating both challenges and opportunities for prospective operators.

The expanding internet penetration, combined with government initiatives toward digital market regulation, positions Guyana as a promising emerging market for iGaming entry in Latin America.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Land-based licensed; online sports betting legalized 2021; online casinos unregulated |

| Primary Regulatory Acts | Gambling Prevention Act (1902, amended 2012), Government Lotteries Act (1963) |

| Regulatory Authority | Guyana Gaming Authority (land-based only) |

| Population | Approx. 790,000 (2025) |

| GDP (Nominal) | ~USD 6.5 billion (2024) |

| GDP Per Capita | ~USD 8,200 |

| Internet Penetration | ~63% |

| Mobile Penetration | ~77% |

| Licensed Casinos (Land-Based) | 3 Premises licenses max per region |

| Online Gambling Licenses | None (no local framework for iGaming operators) |

| Licensing Fee (Casino Premises & Operator) | Application-based; fees vary; casino premises & operator licenses required |

| Taxation on Operators | Annual operational tax; no player winnings tax |

| Player Taxation | None on winnings |

| Compliance Requirements | Strict for land-based; minimal for online |

| Responsible Gambling Measures (Land-Based) | Mandatory implementation |

| Market Size (2025 est.) | USD 23-43 million (iGaming revenue) |

| Market Growth Forecast (CAGR 2025-2029) | 3.53% |

| Online Sports Betting CAGR | 4.62% |

| ARPU | Low; emerging market |

| Market Penetration (2028 forecast) | 0.7% population |

| Main Player Demographic | Males aged 21-40, urban centers |

| Business Operation Requirements | Local presence for casinos; no mandated for online |

| License Renewal | Annual process |

| Enforcement Mechanisms | Fines and imprisonment for unlicensed land-based operations |

| Advertising Restrictions | Moderate for land-based; largely undefined online |

| Digital Infrastructure Quality | Improving broadband; expanding mobile networks |

| Payment Systems | Supports cards, mobile money, growing crypto acceptance |

| Foreign Ownership Restrictions | Permissive; foreign investors active |

| Market Entry Timeline | 3-6 months for casino licenses; uncertain for online entry |

| Upcoming Regulatory Changes | Pending legislation for comprehensive online regulation |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Guyana’s gambling regulatory regime is primarily founded on the Gambling Prevention Act of 1902, amended in 2012, along with the Government Lotteries Act of 1963. These laws govern land-based gambling activities, including casinos, betting shops, and government-run lotteries.

Online gambling regulation remains in an early stage, with full legalization limited to online sports betting and government-operated online lotteries since 2021. Other forms of digital gambling, such as online casinos and poker, do not have comprehensive legal frameworks, resulting in a hybrid regulatory environment.

Land-Based Gambling Activities

Land-based gambling in Guyana is well-structured, with regulatory oversight centered on physical casinos and betting venues. The licensing framework restricts casino premises licenses to no more than three per each of the country’s ten administrative regions, ensuring controlled market saturation.

Casino licenses are highly regulated, with premises required to be part of new hotels or resort complexes meeting stringent accommodation thresholds, typically at least 150 rooms and minimum quality ratings. Admission rules limit access to paying guests and authorized personnel only, reinforcing exclusivity and compliance.

Online Gambling Framework

Online gambling holds a legally ambiguous position due to outdated legislation and ongoing reform discussions. Online sports betting and government lotteries are expressly allowed under recent amendments, but a formal licensing regime for other online games remains undeveloped.

The absence of clear, local licensing for online operators has led to dominance by international operators licensed offshore (e.g., Malta, Gibraltar, Curacao). These entities serve Guyanese players but operate without local regulatory oversight, creating challenges for consumer protection and taxation enforcement.

Licensed Operators and Market Players

The competitive landscape features a mix of international sportsbook giants and local government entities running lotteries and land-based casinos. International sportsbook operators with global licenses collectively hold over 70% of the digital betting market share in Guyana.

Local casinos remain fewer in number but maintain steady revenue streams, often linked to hotel resorts. Technology providers and payment processors play a critical role in facilitating digital market expansion through partnerships with both local and foreign operators.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing authority responsible for land-based gambling regulation is the Guyana Gaming Authority, which oversees casino premises and operator licenses. Applicants must meet “fit and proper” criteria, including financial stability and integrity checks.

Though there is no formal licensing system for online operators in Guyana, current discussions focus on introducing frameworks encompassing registration, compliance, and taxation of digital platforms.

- Corporate registration and incorporation documents

- Financial statements audited for at least three years

- Detailed business and market strategy plans

- Technical certifications for gaming platforms and systems

- Criminal background disclosures for directors and owners

- Proof of minimum capital deposits in authorized banks

- Demonstration of internal controls and anti-fraud measures

Local Presence and Operational Requirements

For land-based casinos, regulatory mandates include physical premises located within approved hotel or resort complexes, where player access and employee control are strictly monitored. This physical presence supports enforcement of licensing conditions and compliance onsite.

Online operators currently face no explicit local presence or operational requirements, largely due to the absence of a dedicated regulatory framework. Foreign ownership of gambling businesses is permitted, enhancing international investment potential.

- Physical casino must be part of a hotel/resort with ≥150 rooms

- Access limited to hotel guests and licensed personnel

- Anti-money laundering and fraud prevention controls on-site

- Local representatives or compliance officers recommended for land-based

- Foreign ownership is allowed without mandatory partnership mandates

Compliance Obligations and Monitoring

Player Protection and Identification

Land-based operators are legally required to implement responsible gambling measures, including age verification, self-exclusion programs, and deposit limits. These protections aim to reduce gambling-related harm and promote safe gaming environments.

Digital gambling platforms currently lack standardized consumer protection mandates under Guyanese law. However, plans to introduce more rigorous KYC (Know Your Customer) and AML (Anti-Money Laundering) standards are under governmental review to enhance player safety in the online sphere.

- Mandatory age verification at point of entry (18+ years)

- Self-exclusion programs accessible to players

- Deposit and betting limits to manage gambling exposure

- Information disclosure on responsible gambling practices

- Regular monitoring to detect fraud or suspicious behavior

Financial Monitoring and Reporting

Operators of physical casinos are subject to strict financial reporting requirements, including transaction audits, monthly and annual fiscal submissions, and compliance with anti-fraud mandates enforced by the Gaming Authority.

Online gambling platforms do not have prescribed local reporting obligations, as their operations are predominantly offshore. However, if future legislation is enacted, it will likely specify sequential reporting steps including registration, ongoing compliance audits, tax declarations, and data sharing.

Taxation Structure and Financial Obligations

Player Taxation

There is no tax imposed on players’ gambling winnings in Guyana. This policy favors consumer retention but shifts the fiscal responsibility to the operators and government for tax revenue from gambling activities.

Operator Taxation

Gambling operators, particularly land-based casinos, are subject to annual operational taxes. These fixed taxes complement general corporate income tax obligations and are part of licensing conditions. No differential tax rates by game type are currently stipulated in local law.

| Tax Type | Rate / Structure |

|---|---|

| Annual Operational Tax | Fixed fee assessed per licensed operator |

| Corporate Income Tax | Standard rate applies (~25%) |

| Withholding Tax on Payments | Applicable as per general tax code |

| Player Winnings Tax | None |

| Turnover or GGR Tax | Not currently established |

Gambling Market Financial Performance

The iGaming revenue in Guyana is estimated between USD 23 million and USD 43 million in 2025, reflecting early-stage market development. Growth forecasts predict a compound annual growth rate (CAGR) of 3.53% through 2029, with online sports betting leading expansion at 4.62% CAGR.

Market penetration remains modest at below 1%, with core player demographics concentrated in urban males aged 21 to 40. Revenue distribution skews heavily toward offshore-online operators, underscoring the importance of regulatory development to capture local taxation.

Advertising and Marketing Restrictions

Regulations on gambling advertising in Guyana primarily cover land-based activities with moderate restrictions on content and channels. Advertising for online gambling lacks clear guidance, reflecting the regulatory gap in the digital space.

- Permitted advertising on radio, television, and print for licensed venues

- Restrictions on targeting minors and vulnerable groups

- Prohibitions on misleading claims or guarantees of winnings

- Limited sponsorship opportunities regulated for sports events

- Time-of-day restrictions intended to minimize youth exposure

Recent Regulatory Changes and Their Impact

Recent amendments include full legalization of online sports betting in 2021 and updates to licensing protocols for land-based casinos in 2012. Legislative debate continues regarding digital gambling regulation, with proposals aiming to enhance consumer protection and tax compliance.

Enforcement Mechanisms and Penalties

The Guyana Gaming Authority holds enforcement powers including fines, license revocation, and criminal penalties for non-compliance. Offenses such as unlicensed casino operation carry fines exceeding one million Guyanese dollars and imprisonment from six months to two years.

- Monetary fines scaling with severity of infraction

- License suspension or permanent revocation

- Criminal sanctions for fraudulent activities

- Seizure of illegal gambling equipment

- Close monitoring of KYC/AML policy adherence

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

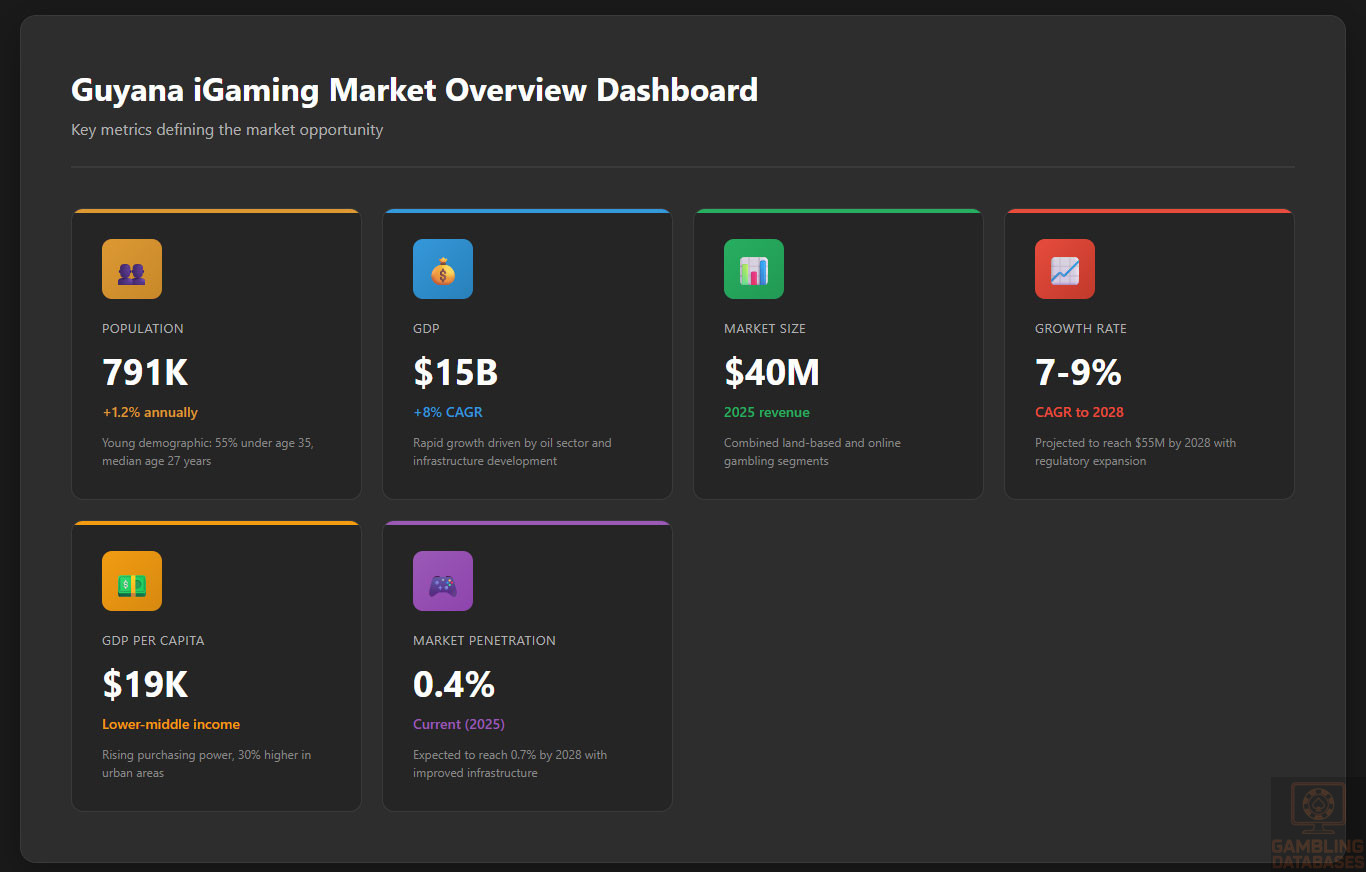

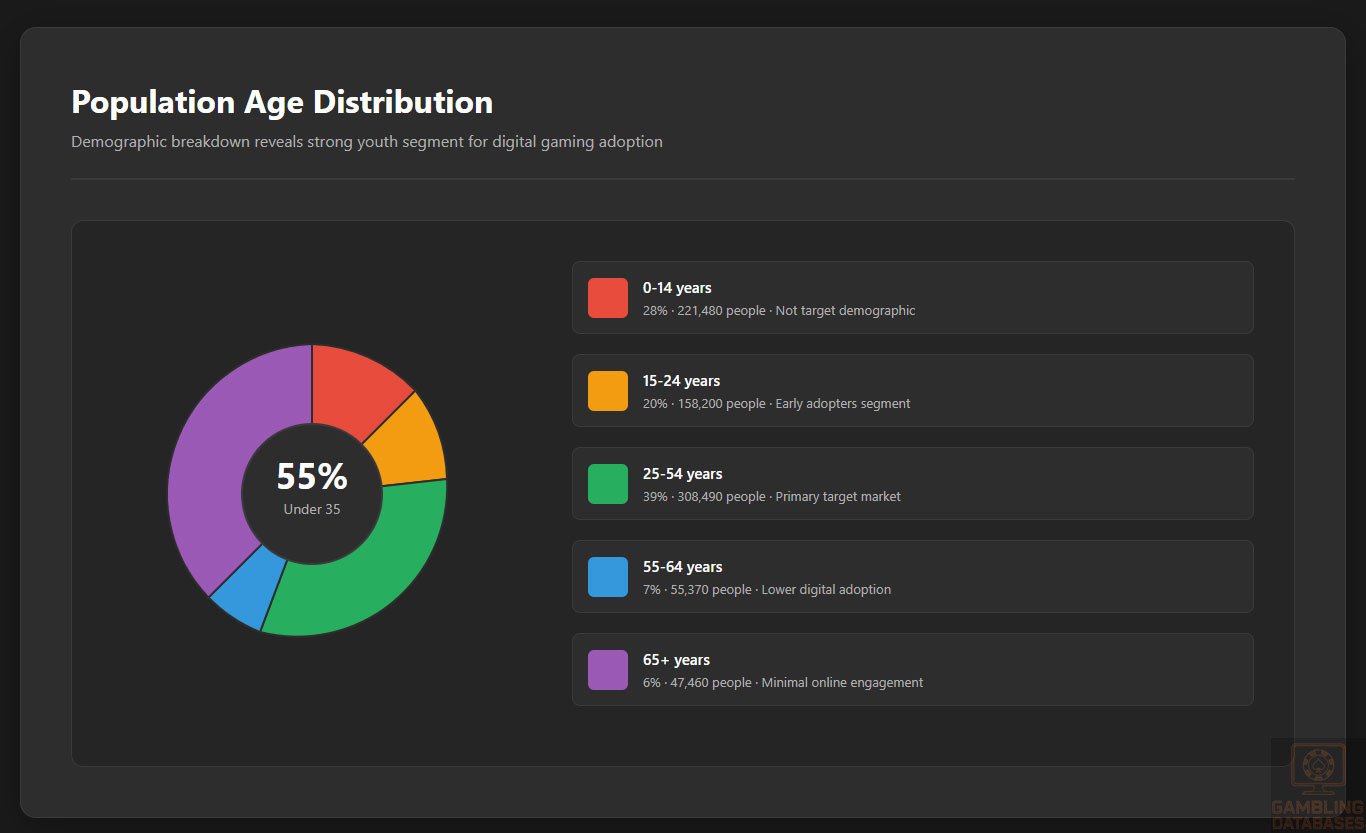

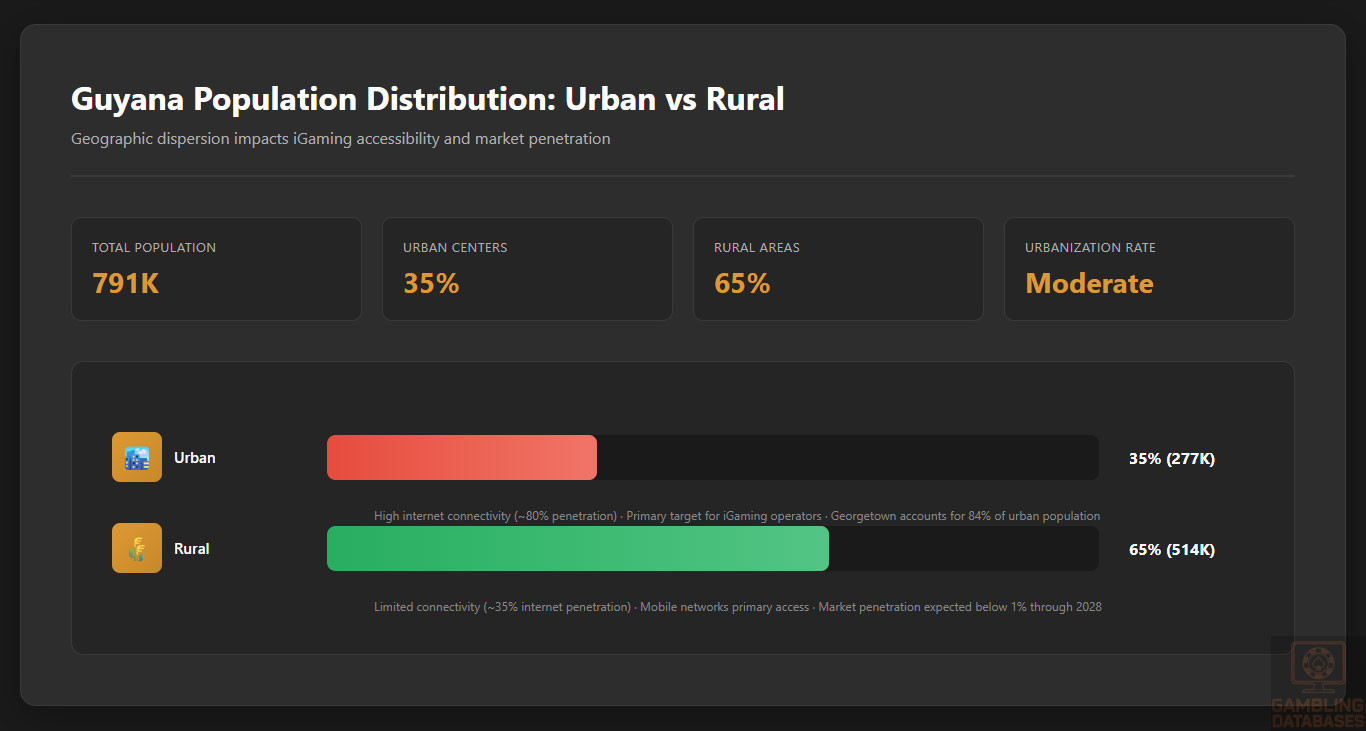

Guyana’s population stands at approximately 791,000 as of 2025, with a relatively young demographic profile. The median age is estimated at 27 years, with about 55% of the population below the age of 35, underscoring a sizable youth segment likely to engage with digital entertainment and mobile gaming.

Gender distribution is fairly balanced with males comprising 51% and females 49%. Urbanization is moderate, with around 35% of the population residing in urban centers while the majority live in rural or semi-rural areas, impacting access to gaming venues and internet connectivity differently across regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 28% |

| 15-24 years | 20% |

| 25-54 years | 39% |

| 55-64 years | 7% |

| 65 years and over | 6% |

Geographic Distribution

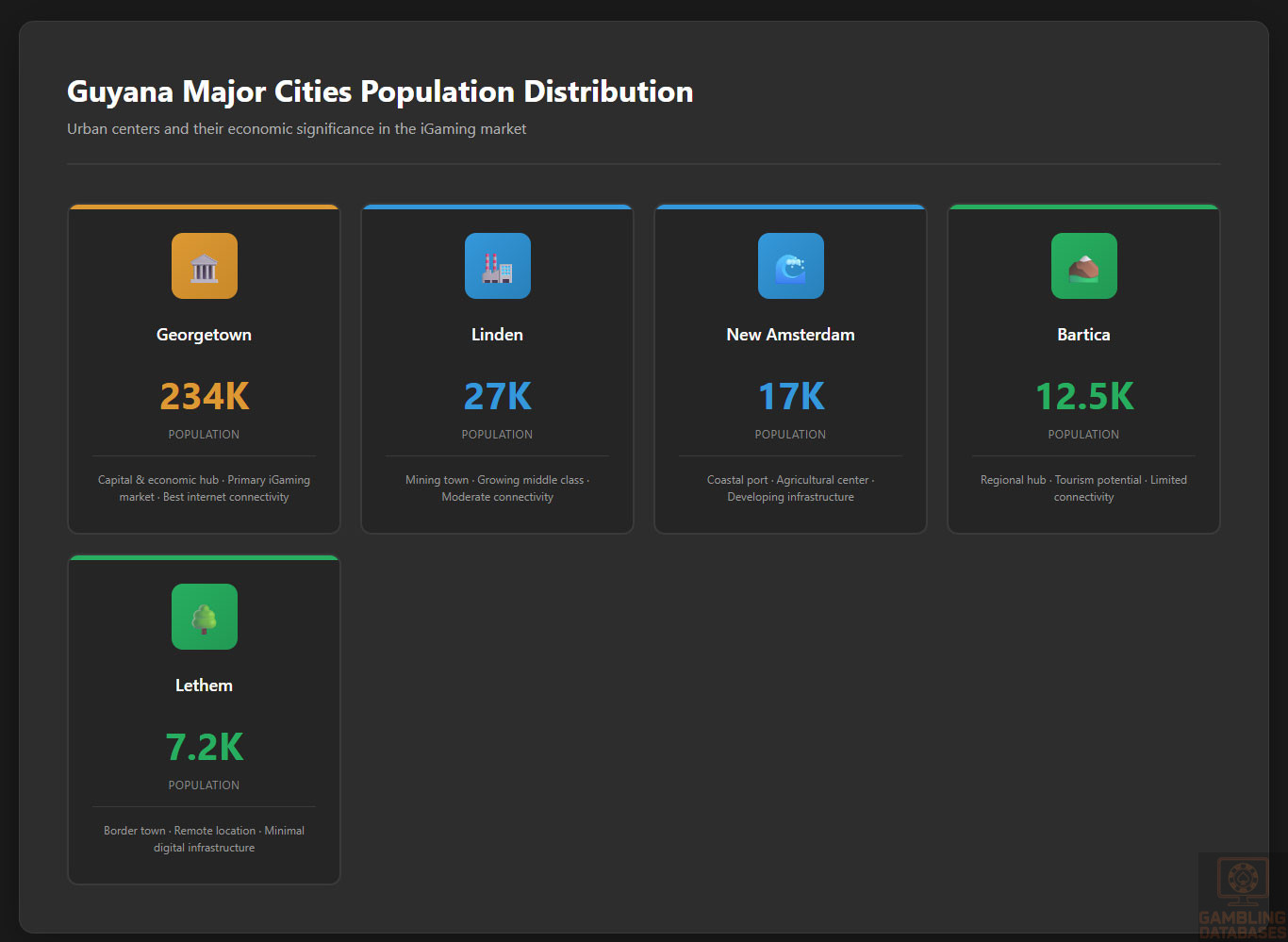

Geographically, Guyana is divided into coastal urban hubs and a vast interior of sparsely populated regions. The largest urban center and economic hub is Georgetown, home to approximately 234,000 residents, serving as the primary locus for gambling and entertainment industries.

Other significant towns include Linden, New Amsterdam, and Bartica, which have smaller populations but contribute to regional economic activity. Internet penetration and access to gambling venues are strongly concentrated in coastal and urban areas, while interior regions remain underserved.

- Georgetown (Population ~234,000)

- Linden (~27,000)

- New Amsterdam (~17,000)

- Bartica (~12,500)

- Lethem (~7,200)

Urban areas consistently exhibit higher internet and mobile penetration rates, creating localized hot spots for iGaming adoption compared to rural zones where connectivity and disposable income are lower.

Economic Indicators and Consumer Spending Power

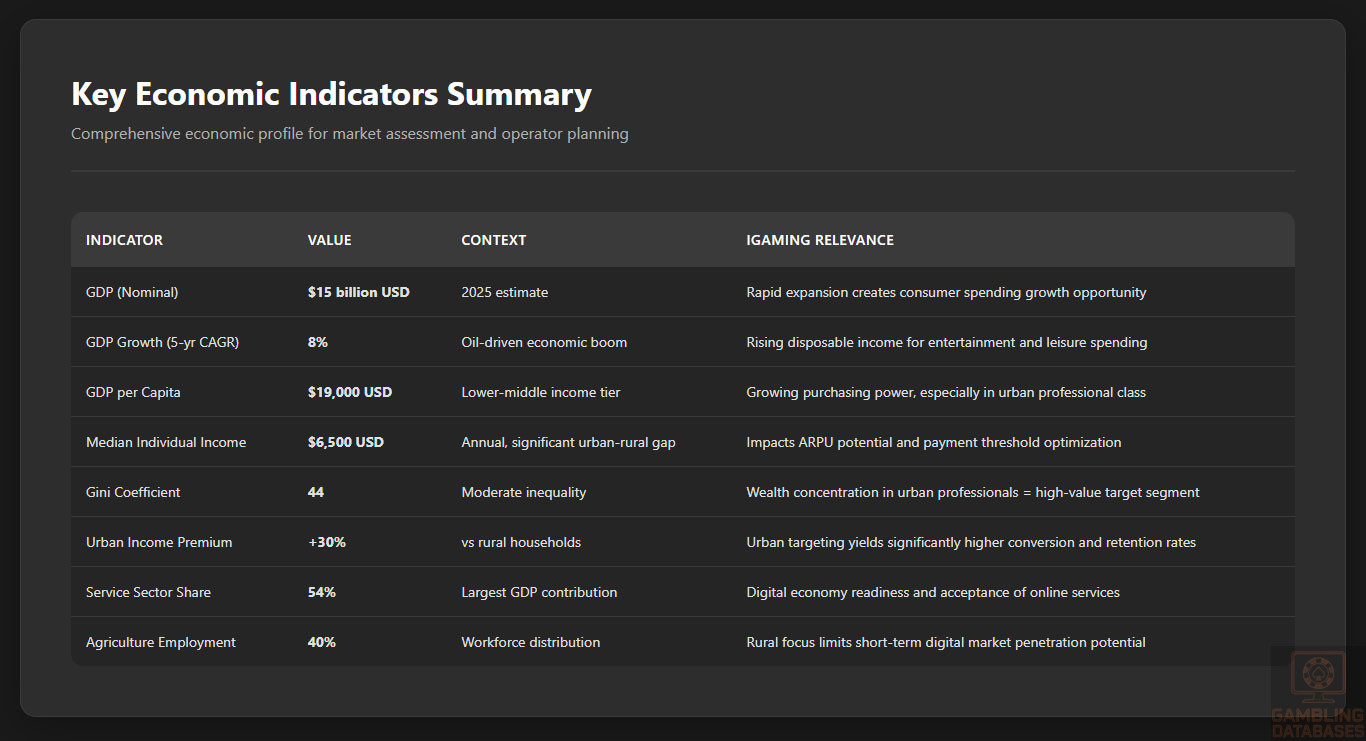

Guyana’s economy is rapidly expanding, buoyed by recent oil discoveries and upgrades in infrastructure. The nominal GDP reached approximately $15 billion USD in 2025, reflecting strong growth of around 8% annually over the past five years.

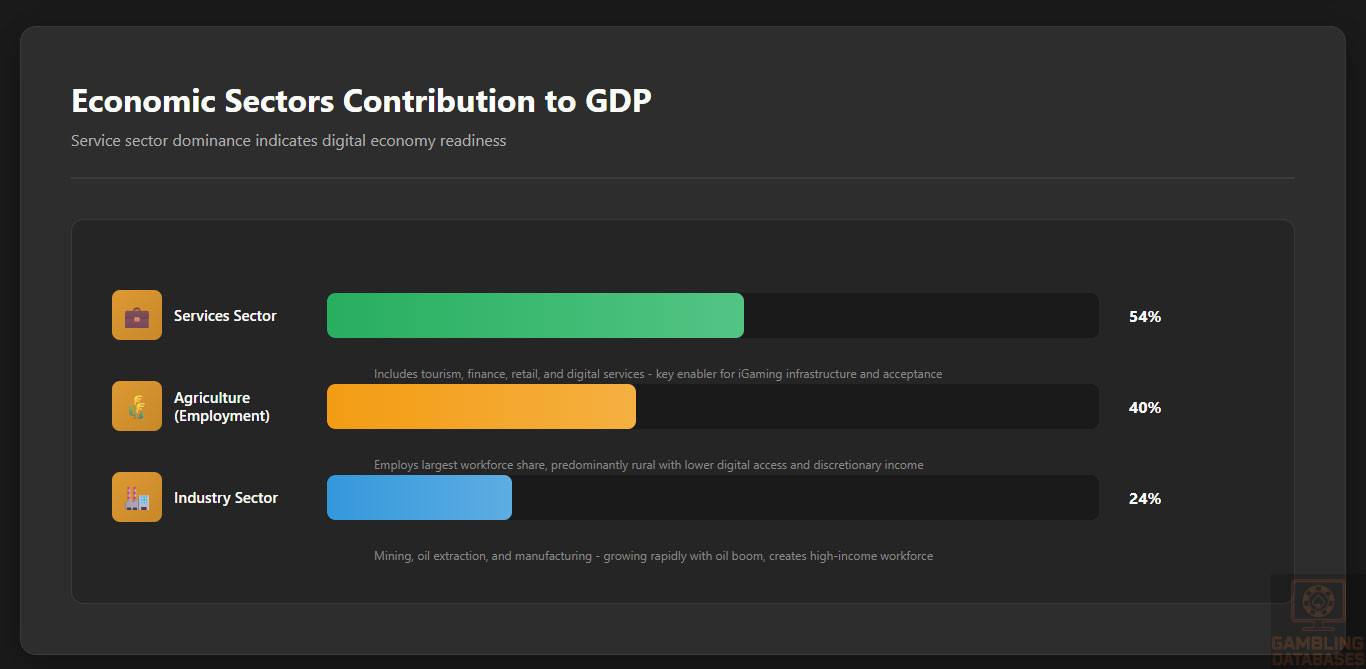

The economic structure is shifting from agriculture and mining towards services and oil extraction, with agriculture still employing a significant portion of the workforce. GDP per capita is around $19,000 USD, which positions Guyana as a lower-middle-income country within Latin America, showing rising consumer purchasing power and discretionary spending potential relevant to entertainment sectors.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $15 billion USD |

| GDP Growth Rate (5-year CAGR) | 8% |

| GDP per Capita | $19,000 USD |

| Service Sector Contribution | 54% |

| Agriculture Sector Employment | 40% |

| Industry Sector Contribution | 24% |

Income and Wealth Distribution

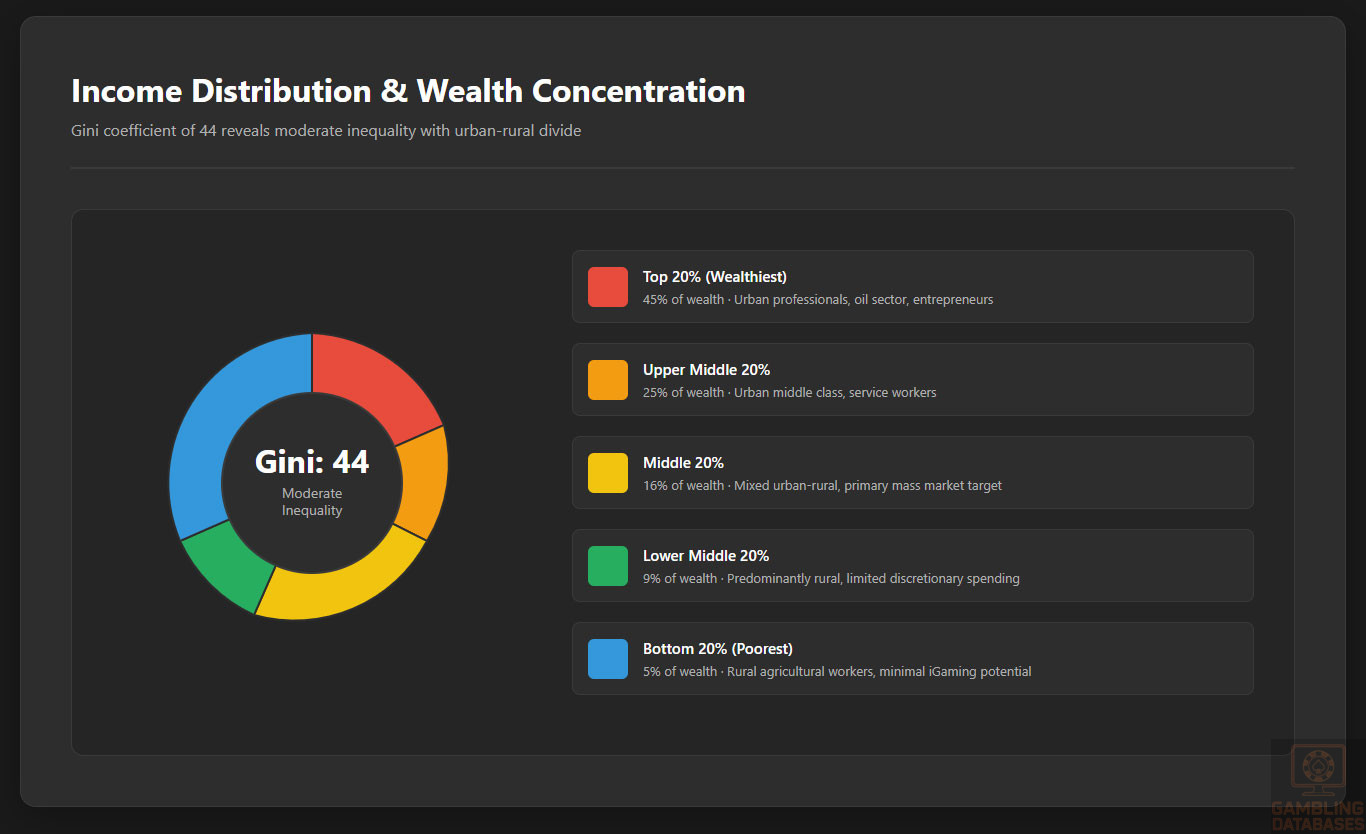

Income distribution in Guyana exhibits moderate inequality, with a Gini coefficient estimated around 44. Average household income varies substantially between urban and rural populations, with urban households reporting roughly 30% higher disposable income.

Median individual income is approximately $6,500 USD annually, with wealth increasingly concentrated among professional and entrepreneurial classes associated with the oil and service industries. Consumer spending leans towards essential goods with discretionary spending on entertainment and digital services showing an upward trajectory among younger demographics.

Market Size and Growth Projections

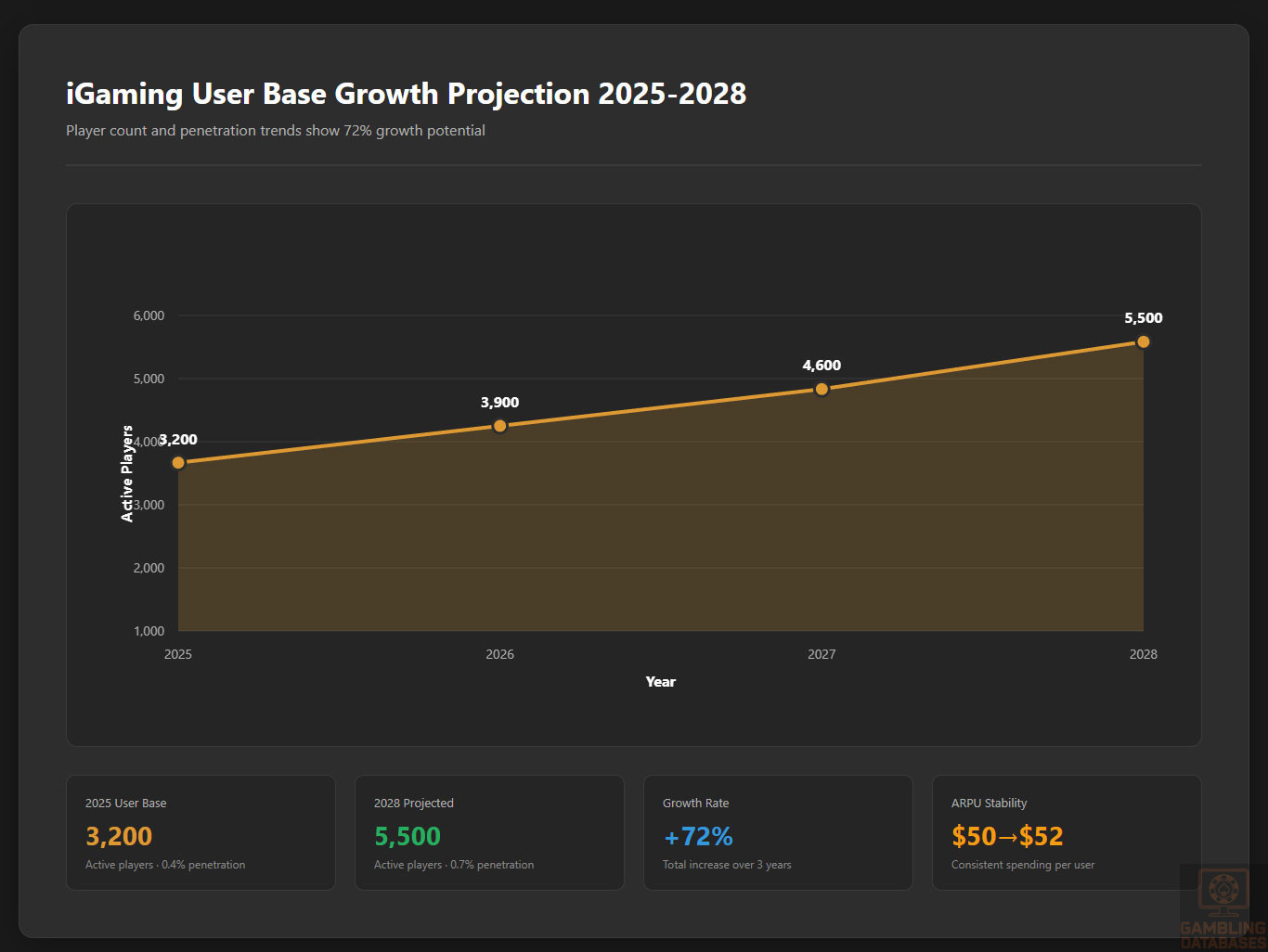

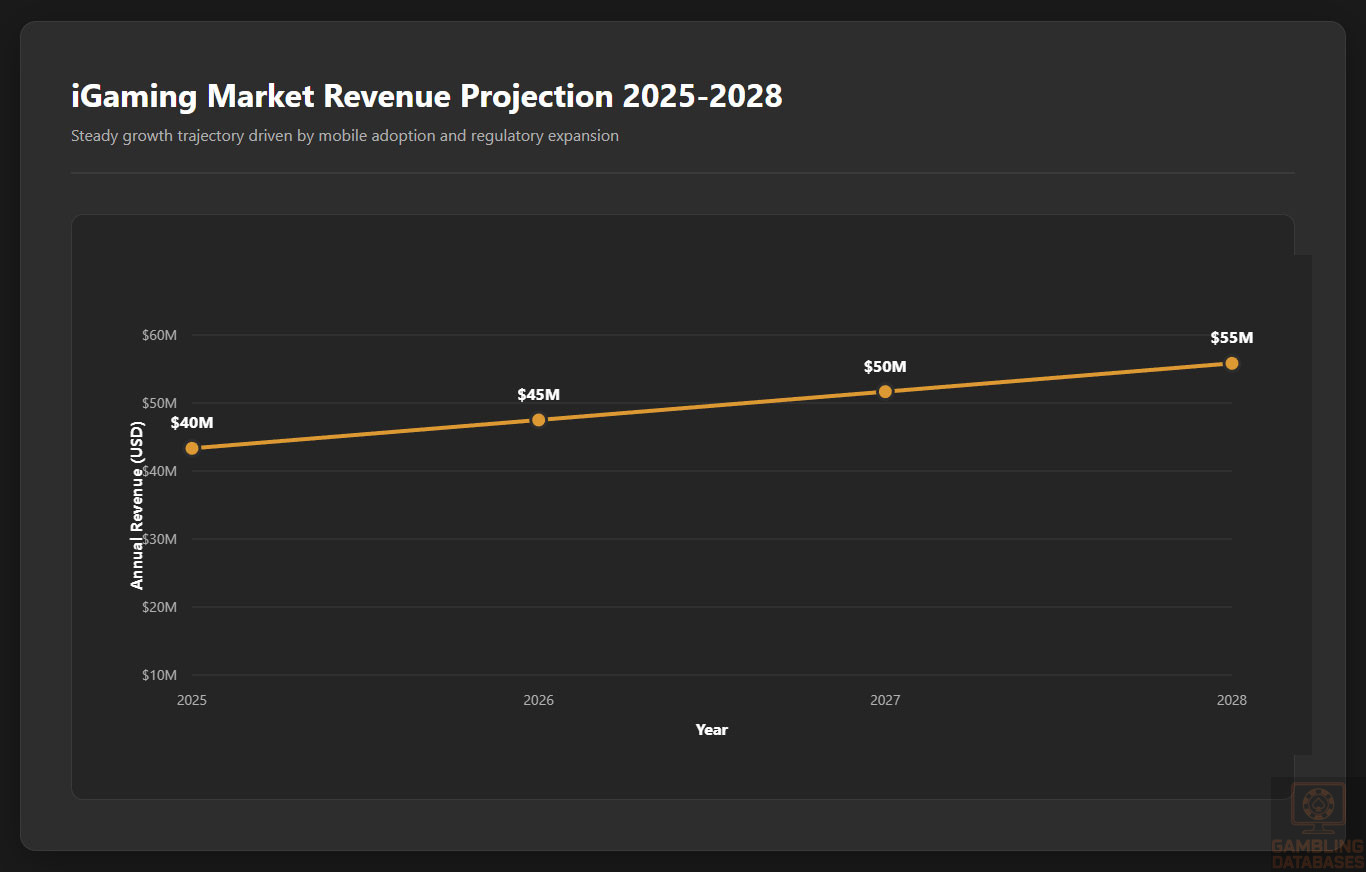

The gaming market in Guyana currently generates roughly $40 million USD in annual revenue, combining land-based and online betting segments. The market has experienced historical growth around 7-9% CAGR, driven largely by sports betting and mobile access improvements.

Forecasts project continued expansion with increased mobile penetration and regulatory reforms expected to broaden legalized online gaming. User base projections estimate penetration rising to 0.7% by 2028, with ARPU standing at about $50 USD, reflecting moderate average spending per player.

| Metric | 2025 | 2028 (Projected) |

|---|---|---|

| Annual Revenue | $40 million | $55 million |

| CAGR | 7-9% | 7-9% |

| Online Betting Penetration | 0.4% | 0.7% |

| Average Revenue Per User | $50 | $52 |

| User Base | ~3,200 (000 players) | ~5,500 (000 players) |

Education, Skills, and Digital Literacy

Guyana has a literacy rate exceeding 88%, with secondary education completion at roughly 60%. Digital literacy is growing steadily due to increased smartphone usage, internet availability, and government initiatives promoting ICT skills. Workforce skills are concentrated in agriculture and natural resource extraction sectors, with a burgeoning service and tech sector fostering a younger, digitally-oriented labor pool.

However, disparities remain between urban and rural areas, with many interior regions lacking access to quality education and modern technology infrastructure. These gaps impact both digital engagement levels and potential for online iGaming uptake.

Cultural and Social Factors

Communication and Language

Guyana’s official language is English, facilitating international business and digital communications. The majority of the population also speaks Guyanese Creole in informal settings. Indigenous and immigrant communities contribute additional dialects present throughout the country.

- English (Official, used in media and education)

- Guyanese Creole (Widely spoken colloquially)

- Hindi and Urdu (Among Indo-Guyanese communities)

- Indigenous Amerindian languages (Including Akawaio, Macushi)

- Portuguese (Among some border populations)

Cultural Attitudes

Gambling is culturally accepted in urban areas, often viewed as entertainment and a social activity, while rural regions exhibit more conservative views due to religious and community norms. Christianity is predominant, and some religious groups discourage gambling participation.

Foreign brands, especially those from North America and Europe, are generally well-received, with younger consumers showing affinity for internationally recognized sports betting platforms and online casino operators. Entertainment preferences include sports, music, and digital interactive content, shaping consumer gaming interests.

Problem Gambling and Social Considerations

Problem gambling prevalence is currently low but expected to rise with expanding access to online platforms. Awareness and support services remain nascent, with limited government-sponsored programs addressing addiction or social harms.

- National awareness campaigns are minimal but slowly increasing

- Peer and community education programs on responsible gambling

- Self-exclusion and voluntary limits promoted by some operators

- Healthcare intervention services for addiction support

- Research initiatives by NGOs focusing on gambling harm

Social responsibility policies are emerging, especially among international operators targeting Guyana, including mandatory funding for treatment programs in some offshore licensing regimes.

Political Structure and Governance

Guyana is a parliamentary democracy with a stable political environment that supports foreign investment and regulatory modernization. The government has demonstrated commitment to reforming gambling laws to increase transparency, tax revenues, and protect consumers, although bureaucratic hurdles persist.

Strong international relations with regional trade blocs and the Commonwealth facilitate cross-border cooperation and potential regulatory alignment within Latin America and the Caribbean.

Technology Adoption and Digital Behavior

Internet and Digital Usage

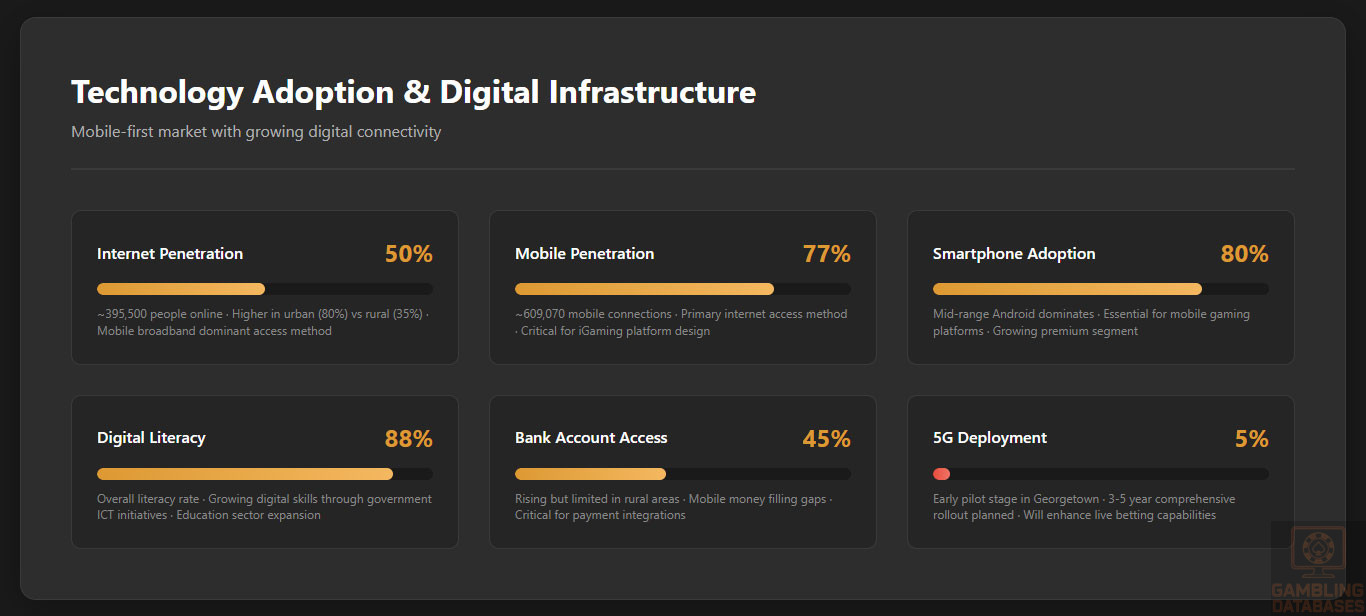

Internet penetration in Guyana is estimated at approximately 50% of the population, with higher rates in urban and coastal areas. Average daily internet usage averages 4 hours, including social media, streaming, and gaming activities. Mobile device adoption is widespread, with smartphone penetration estimated near 80%, making mobile the dominant platform for digital content consumption.

Social media engagement is vibrant, spanning multiple platforms favored by different demographic segments. Connectivity improvements and affordable data plans contribute to sustained growth in digital participation.

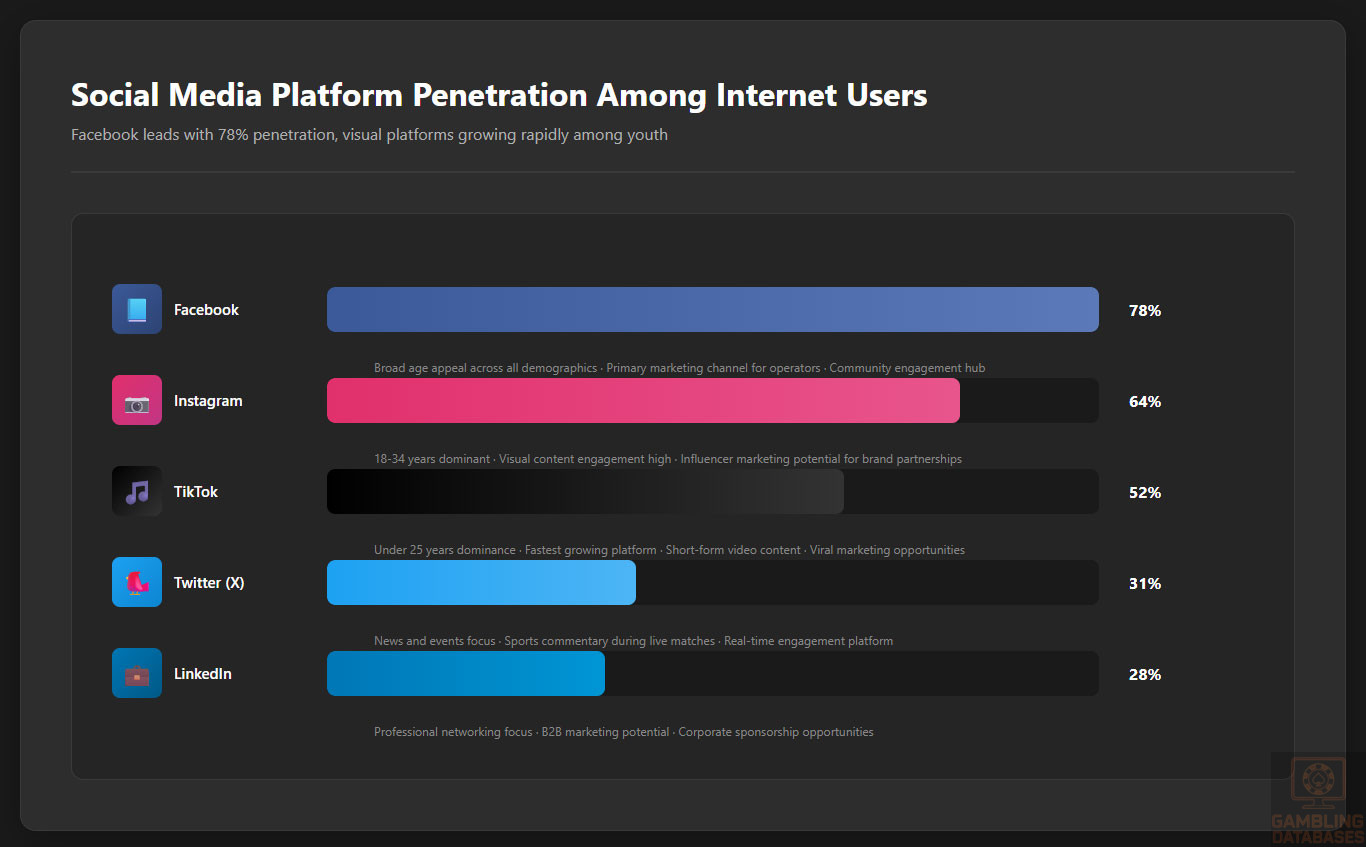

- Facebook: 78% penetration among internet users, favored by broad age groups

- Instagram: 64% among 18-34-year-olds, strong visual content engagement

- YouTube: Most consumed digital video platform with daily watch times averaging 45 minutes

- TikTok: Rapidly growing among users under 25, capturing 52% of this segment

- Twitter: News and event updates preferred by 31% of users

- LinkedIn: Used by 28% of professionals for networking

Digital Payment Behavior

Electronic payments are increasingly common, especially for online services and remittances. Payment behavior trends favor mobile money solutions alongside traditional credit and debit cards. Informal cash-based transactions remain prevalent but are gradually supplemented by digital wallets and fintech platforms.

- Mobile Money (e.g., Digicel Money, GTT Pay)

- Credit and Debit Cards (Visa, Mastercard)

- Bank Transfers (used primarily for higher-value transactions)

- E-wallets (PayPal, Skrill among expatriates)

- Cryptocurrencies (emerging interest but limited adoption)

- Cash-on-Delivery (retail payments)

Gaming and Gambling Preferences

Current Market Participation

Gambling participation is modest but growing, with sports betting as the dominant activity, especially football and cricket wagering. Lottery games are popular, benefiting from government backing and rural accessibility. Casino attendance remains localized to urban centers, constrained by venue availability and income prerequisites.

- Sports Betting

- Government-run Lottery

- Casino Games (Table games, slots)

- Online Betting Platforms (mostly offshore)

- Informal Lottery Pools and Betting Circles

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 12% |

| Lottery | 9% |

| Casino Games (Land-based) | 6% |

| Online Betting (Offshore) | 4% |

| Informal Betting Pools | 3% |

Consumer Behavior Patterns

Users exhibit strong preferences for mobile and social betting platforms with instant access and live betting features. Peak activity aligns with sporting event schedules, with weekend evenings recording the highest session counts. Average session duration ranges between 25 to 40 minutes, reflecting engagement but also the nascent maturity of the digital market.

Retention rates are influenced by localized promotions, community trust in brand reputation, and payment convenience. Younger demographics display higher frequency betting and greater openness to experimenting with new gaming formats, positioning them as a key target segment for operators.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Guyana’s population stands at approximately 791,000 as of 2025, with a relatively young demographic profile. The median age is estimated at 27 years, with about 55% of the population below the age of 35, underscoring a sizable youth segment likely to engage with digital entertainment and mobile gaming.

Gender distribution is fairly balanced with males comprising 51% and females 49%. Urbanization is moderate, with around 35% of the population residing in urban centers while the majority live in rural or semi-rural areas, impacting access to gaming venues and internet connectivity differently across regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 28% |

| 15-24 years | 20% |

| 25-54 years | 39% |

| 55-64 years | 7% |

| 65 years and over | 6% |

Geographic Distribution

Geographically, Guyana is divided into coastal urban hubs and a vast interior of sparsely populated regions. The largest urban center and economic hub is Georgetown, home to approximately 234,000 residents, serving as the primary locus for gambling and entertainment industries.

Other significant towns include Linden, New Amsterdam, and Bartica, which have smaller populations but contribute to regional economic activity. Internet penetration and access to gambling venues are strongly concentrated in coastal and urban areas, while interior regions remain underserved.

- Georgetown (Population ~234,000)

- Linden (~27,000)

- New Amsterdam (~17,000)

- Bartica (~12,500)

- Lethem (~7,200)

Urban areas consistently exhibit higher internet and mobile penetration rates, creating localized hot spots for iGaming adoption compared to rural zones where connectivity and disposable income are lower.

Economic Indicators and Consumer Spending Power

Guyana’s economy is rapidly expanding, buoyed by recent oil discoveries and upgrades in infrastructure. The nominal GDP reached approximately $15 billion USD in 2025, reflecting strong growth of around 8% annually over the past five years.

The economic structure is shifting from agriculture and mining towards services and oil extraction, with agriculture still employing a significant portion of the workforce. GDP per capita is around $19,000 USD, which positions Guyana as a lower-middle-income country within Latin America, showing rising consumer purchasing power and discretionary spending potential relevant to entertainment sectors.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $15 billion USD |

| GDP Growth Rate (5-year CAGR) | 8% |

| GDP per Capita | $19,000 USD |

| Service Sector Contribution | 54% |

| Agriculture Sector Employment | 40% |

| Industry Sector Contribution | 24% |

Income and Wealth Distribution

Income distribution in Guyana exhibits moderate inequality, with a Gini coefficient estimated around 44. Average household income varies substantially between urban and rural populations, with urban households reporting roughly 30% higher disposable income.

Median individual income is approximately $6,500 USD annually, with wealth increasingly concentrated among professional and entrepreneurial classes associated with the oil and service industries. Consumer spending leans towards essential goods with discretionary spending on entertainment and digital services showing an upward trajectory among younger demographics.

Market Size and Growth Projections

The gaming market in Guyana currently generates roughly $40 million USD in annual revenue, combining land-based and online betting segments. The market has experienced historical growth around 7-9% CAGR, driven largely by sports betting and mobile access improvements.

Forecasts project continued expansion with increased mobile penetration and regulatory reforms expected to broaden legalized online gaming. User base projections estimate penetration rising to 0.7% by 2028, with ARPU standing at about $50 USD, reflecting moderate average spending per player.

| Metric | 2025 | 2028 (Projected) |

|---|---|---|

| Annual Revenue | $40 million | $55 million |

| CAGR | 7-9% | 7-9% |

| Online Betting Penetration | 0.4% | 0.7% |

| Average Revenue Per User | $50 | $52 |

| User Base | ~3,200 (000 players) | ~5,500 (000 players) |

Education, Skills, and Digital Literacy

Guyana has a literacy rate exceeding 88%, with secondary education completion at roughly 60%. Digital literacy is growing steadily due to increased smartphone usage, internet availability, and government initiatives promoting ICT skills. Workforce skills are concentrated in agriculture and natural resource extraction sectors, with a burgeoning service and tech sector fostering a younger, digitally-oriented labor pool.

However, disparities remain between urban and rural areas, with many interior regions lacking access to quality education and modern technology infrastructure. These gaps impact both digital engagement levels and potential for online iGaming uptake.

Cultural and Social Factors

Communication and Language

Guyana’s official language is English, facilitating international business and digital communications. The majority of the population also speaks Guyanese Creole in informal settings. Indigenous and immigrant communities contribute additional dialects present throughout the country.

- English (Official, used in media and education)

- Guyanese Creole (Widely spoken colloquially)

- Hindi and Urdu (Among Indo-Guyanese communities)

- Indigenous Amerindian languages (Including Akawaio, Macushi)

- Portuguese (Among some border populations)

Cultural Attitudes

Gambling is culturally accepted in urban areas, often viewed as entertainment and a social activity, while rural regions exhibit more conservative views due to religious and community norms. Christianity is predominant, and some religious groups discourage gambling participation.

Foreign brands, especially those from North America and Europe, are generally well-received, with younger consumers showing affinity for internationally recognized sports betting platforms and online casino operators. Entertainment preferences include sports, music, and digital interactive content, shaping consumer gaming interests.

Problem Gambling and Social Considerations

Problem gambling prevalence is currently low but expected to rise with expanding access to online platforms. Awareness and support services remain nascent, with limited government-sponsored programs addressing addiction or social harms.

- National awareness campaigns are minimal but slowly increasing

- Peer and community education programs on responsible gambling

- Self-exclusion and voluntary limits promoted by some operators

- Healthcare intervention services for addiction support

- Research initiatives by NGOs focusing on gambling harm

Social responsibility policies are emerging, especially among international operators targeting Guyana, including mandatory funding for treatment programs in some offshore licensing regimes.

Political Structure and Governance

Guyana is a parliamentary democracy with a stable political environment that supports foreign investment and regulatory modernization. The government has demonstrated commitment to reforming gambling laws to increase transparency, tax revenues, and protect consumers, although bureaucratic hurdles persist.

Strong international relations with regional trade blocs and the Commonwealth facilitate cross-border cooperation and potential regulatory alignment within Latin America and the Caribbean.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration in Guyana is estimated at approximately 50% of the population, with higher rates in urban and coastal areas. Average daily internet usage averages 4 hours, including social media, streaming, and gaming activities. Mobile device adoption is widespread, with smartphone penetration estimated near 80%, making mobile the dominant platform for digital content consumption.

Social media engagement is vibrant, spanning multiple platforms favored by different demographic segments. Connectivity improvements and affordable data plans contribute to sustained growth in digital participation.

- Facebook: 78% penetration among internet users, favored by broad age groups

- Instagram: 64% among 18-34-year-olds, strong visual content engagement

- YouTube: Most consumed digital video platform with daily watch times averaging 45 minutes

- TikTok: Rapidly growing among users under 25, capturing 52% of this segment

- Twitter: News and event updates preferred by 31% of users

- LinkedIn: Used by 28% of professionals for networking

Digital Payment Behavior

Electronic payments are increasingly common, especially for online services and remittances. Payment behavior trends favor mobile money solutions alongside traditional credit and debit cards. Informal cash-based transactions remain prevalent but are gradually supplemented by digital wallets and fintech platforms.

- Mobile Money (e.g., Digicel Money, GTT Pay)

- Credit and Debit Cards (Visa, Mastercard)

- Bank Transfers (used primarily for higher-value transactions)

- E-wallets (PayPal, Skrill among expatriates)

- Cryptocurrencies (emerging interest but limited adoption)

- Cash-on-Delivery (retail payments)

Gaming and Gambling Preferences

Current Market Participation

Gambling participation is modest but growing, with sports betting as the dominant activity, especially football and cricket wagering. Lottery games are popular, benefiting from government backing and rural accessibility. Casino attendance remains localized to urban centers, constrained by venue availability and income prerequisites.

- Sports Betting

- Government-run Lottery

- Casino Games (Table games, slots)

- Online Betting Platforms (mostly offshore)

- Informal Lottery Pools and Betting Circles

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 12% |

| Lottery | 9% |

| Casino Games (Land-based) | 6% |

| Online Betting (Offshore) | 4% |

| Informal Betting Pools | 3% |

Consumer Behavior Patterns

Users exhibit strong preferences for mobile and social betting platforms with instant access and live betting features. Peak activity aligns with sporting event schedules, with weekend evenings recording the highest session counts. Average session duration ranges between 25 to 40 minutes, reflecting engagement but also the nascent maturity of the digital market.

Retention rates are influenced by localized promotions, community trust in brand reputation, and payment convenience. Younger demographics display higher frequency betting and greater openness to experimenting with new gaming formats, positioning them as a key target segment for operators.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Guyana’s internet penetration stands at approximately 50%, composed predominantly of mobile broadband connections, reflecting the country’s geographic dispersion and infrastructural development stage. Fixed broadband access remains limited and mainly concentrated in urban centers, while the majority of rural areas depend on mobile networks as the primary internet source.

Average mobile internet speeds range between 20 to 40 Mbps in urban zones, sufficient for digital gaming activities. Network reliability varies, with outages more frequent in interior regions, prompting ongoing government and private sector investments in fiber-optic expansion and satellite connectivity projects to improve nationwide coverage.

5G and Future Technology Deployment

As of 2025, 5G deployment in Guyana is in early stages, with pilot projects underway in Georgetown and other urban hubs. Comprehensive 5G coverage rollout is planned over the next 3-5 years, aligning with regional technological upgrades and government digital transformation initiatives.

The key mobile network operators are actively upgrading infrastructure to support 5G capabilities, aiming to enhance gaming, streaming, and fintech services. The regulatory framework is adapting to facilitate spectrum allocation and encourage competition among telecom providers.

Mobile Technology Ecosystem

Guyana’s mobile network is competitive, featuring multiple operators with diverse market shares. The market experiences high smartphone adoption, driven by affordable devices and expanding 4G availability.

- Digicel Guyana: Largest operator with approximately 45% market share and extensive coastal and urban coverage

- GTT (Guyana Telephone & Telegraph): Holding about 40% market share, noted for improved data packages

- Amerindian Telecom Providers: Serve rural and interior areas, limited coverage

- Smaller MVNOs: Focused on niche segments, ~10% market presence

- New Entrants (5G-focused startups): Emerging in urban zones, capturing early adoption

Smartphone penetration is estimated near 80%, spurred by younger demographics and growing urbanization. Device preferences lean towards mid-range Android models providing balance between performance and affordability. Premium device penetration remains under 10%, though increasing due to consumer aspiration for enhanced features.

Financial Services and Payment Infrastructure

Guyana’s banking system comprises several established institutions offering full-spectrum financial services with an increasing shift towards digital banking solutions. Bank account penetration is rising but still limited in rural populations due to accessibility and financial literacy barriers.

- Republic Bank (Guyana) Limited: Leading financial institution with comprehensive digital offerings

- Guyana Bank for Trade and Industry (GBTI): Strong SME client focus and expanding digital channels

- Citibank Caribbean: Specializes in corporate and trade finance

- Bank of Baroda (Guyana Branch): Focuses on remittance and retail banking services

- Demerara Bank Limited: Growing digital banking footprint catering to younger consumers

Payment options are also diversifying with mobile money platforms gaining traction alongside traditional card payments and bank transfers. Cryptocurrency adoption is nascent but noted among tech-savvy segments as an alternative payment method for international transactions.

- Mobile Money (Digicel Money, GTT Pay)

- Credit and Debit Cards (Visa, Mastercard dominant)

- Bank Transfers (Common for higher-value transactions)

- E-wallets (PayPal, Skrill accessible to expatriates)

- Cryptocurrency Payments (Limited but emerging interest)

E-commerce and Digital Economy

Guyana’s e-commerce sector is growing steadily, fueled by increased internet access and improved payment infrastructure. Online retail penetration remains low compared to regional peers but demonstrates strong growth potential, especially in urban centers.

Consumer trust in digital transactions is evolving, bolstered by improved cybersecurity measures and government-led digital literacy campaigns. Digital services, including online entertainment and financial products, comprise a larger share of consumer spending relative to physical goods, reflecting the digital engagement trends relevant to iGaming operators.

Business Environment and Regulatory Framework

Ease of Business Operations

Guyana ranks moderately on World Bank’s Ease of Doing Business index, with strengths in credit access and investor protections offset by bureaucratic delays in registration and permit issuance. The business registration process is straightforward but requires compliance with multiple regulatory bodies and tax authorities.

- Prepare corporate documents and notarize required legal papers with apostille certification if foreign-based

- Register the company at the Guyana Companies Registry (processing time ~5-7 business days)

- Register for tax and obtain a Taxpayer Identification Number (TIN) within 3-5 days

- Open a corporate bank account and deposit the minimum capital (1-2 weeks)

- Apply for sector-specific licenses (gambling, if applicable) and await regulatory approval

Corporate Structure and Registration

Foreign investors commonly establish Limited Liability Companies (LLCs) due to flexible management structures and lower compliance burdens. Branch offices are also permitted but require local representation and regulatory approvals.

Corporations can undertake full operational activities with shareholder liability confined to capital contributions, making them preferable for iGaming ventures where risk mitigation is essential. Registration requires transparency on ownership, beneficial owners, and adherence to anti-money laundering laws.

- Limited Liability Company (LLC)

- Branch Office of Foreign Corporation

- Public Corporation (less common for iGaming entrants)

- Partnerships (restricted usage)

- Sole Proprietorship (not suitable for iGaming due to liability)

Registration Requirements

- Certificate of Incorporation and Articles of Incorporation

- Declaration of Beneficial Owners with identification documents

- Business plan highlighting operational scope and financial projections

- Proof of registered office address in Guyana

- Tax registration and social security registration proofs

- Compliance certifications for specific regulated sectors (e.g., iGaming license application)

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate is 40% on profits, with an alternative minimum tax of 2% on turnover to safeguard government revenues. Special economic zones offer tax holidays and reduced rates for qualifying entities.

Guyana has tax treaties with countries including Canada, Cuba, Suriname, and Trinidad and Tobago, facilitating cross-border investment and reducing double taxation liabilities for multinational operators.

- Canada

- Cuba

- Suriname

- Trinidad and Tobago

- United Kingdom

- United States (in negotiation)

Personal Income Tax

Individuals are taxed progressively with rates from 28% to 40%, while gambling winnings are exempt from taxation. Employers and employees contribute to National Insurance Scheme (social security) at prescribed rates, and tax residency is determined based on duration of stay exceeding 183 days annually.

Market Entry Considerations

Recommended Entry Strategies

Successful entry into the Guyana iGaming market requires a multi-pronged approach leveraging local partnerships, compliance adherence, and technological flexibility to adapt to infrastructure constraints. International operators often establish local subsidiaries or joint ventures to satisfy regulatory expectations and build brand credibility.

- Form strategic partnerships with local enterprises for market insight and operational support

- Secure full compliance with licensing and operational regulations to mitigate risks

- Deploy mobile-optimized platforms catering to prevalent smartphone usage

- Implement diverse payment options including mobile money and local bank integrations

- Develop robust responsible gambling programs to align with emerging regulatory expectations

Typical Costs and Timelines

Market entry costs can be substantial due to licensing, operational setup, and marketing investments. Initial licensing fees range between $10,000 and $20,000 USD, with legal and consultancy services adding $30,000 to $50,000 USD.

Operational cost baselines include technology hosting, staffing, compliance, and payment processing fees, typically requiring at least $500,000 USD working capital to sustain initial 12 months of operations.

| Cost Category | Estimated Amount (USD) |

|---|---|

| License Application & Renewal Fees | $10,000 – $20,000 |

| Legal & Consulting | $30,000 – $50,000 |

| Technology & Platform Setup | $150,000 – $300,000 |

| Marketing & Customer Acquisition | $100,000 – $200,000 |

| Working Capital (12 months) | $200,000 – $400,000 |

- Preliminary market research and due diligence (1-2 months)

- Company formation and registration (1 month)

- License application and regulatory approval (3-6 months)

- Platform integration and local partnerships (2-3 months)

- Go-to-market launch and customer acquisition (ongoing)

Success Factors and Challenges

Key success factors include strong regulatory compliance, localized payment options, aggressive marketing, and mobile platform optimization. Challenges encompass infrastructure reliability, regulatory uncertainties, competition from offshore operators, and financial literacy barriers among consumers.

- Regulatory adherence and transparent licensing

- Effective local partnership and market knowledge

- Adaptation to mobile-first consumer behavior

- Robust anti-fraud and responsible gambling systems

- Addressing rural connectivity and payment barriers

Exit Strategy Planning

Given the evolving regulatory framework, exit strategies should consider liquidity options including license transferability, potential sale of local entities, and valuation based on future market size projections. The regulatory authority allows license transfers subject to approval, facilitating strategic divestments.

Valuation multiples are influenced by market growth outlook, player base size, and profitability metrics, with specialized advisory recommended for market exit preparation.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Guyana?

Online sports betting and government lotteries were legalized in 2021, setting initial legal precedent for digital gambling. However, full-scale online casino gaming remains unregulated at the national level, with offshore operators dominating the digital market. Operators serving Guyanese players typically rely on licenses from foreign jurisdictions. Regulatory reform is ongoing to clarify and expand online gambling legality.

2. What types of gambling licenses are available and what do they cover?

The main licenses include Casino Premises, Casino Operating, and Betting Shop licenses focused on land-based operations. These cover physical casino venues, betting shop establishments, and government lotteries. No formal national license yet exists for online casino or sportsbook operators domestically. License scopes define permitted activities, compliance obligations, and renewal terms.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees typically range from $10,000 to $20,000 USD, with annual renewal obligations. Application processing for land-based licenses can take between 3 to 6 months, factoring due diligence and regulatory reviews. For online licenses, no clear domestic framework exists yet, creating uncertainty on timelines.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible to apply, but they must submit detailed ownership disclosures and comply with local regulations including physical presence requirements for land-based licenses. Joint ventures with local partners are common to facilitate regulatory approval and market integration.

5. What are the tax obligations for iGaming operators?

Operators pay a corporate income tax rate of 40% on profits or 2% of turnover as an alternative minimum tax. License renewal fees and other operational levies apply yearly. There is no designated Gross Gaming Revenue (GGR) tax, but general corporate tax laws govern profit taxation including iGaming entities.

| Tax Type | Rate/Requirement |

|---|---|

| Corporate Income Tax | 40% on profits or 2% turnover (whichever is higher) |

| License Renewal Fee | $10,000 – $20,000 annually |

| Withholding Tax | 20% on foreign branch profits |

| VAT | 16% (applicable where relevant) |

6. Are gambling winnings taxed for players?

No, players are not subject to taxation on winnings in Guyana, making the environment attractive for bettors. This exemption helps maintain consumer interest and encourages gaming participation.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include technology platform hosting, licensing fees, regulatory compliance, payment processing, marketing, and customer service. Typical budgets require substantial working capital, often exceeding $500,000 annually to sustain growth and compliance in this emerging market.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines vary but generally span 2 to 4 years depending on market penetration speed, regulatory developments, and brand establishment. Early movers may realize faster gains due to limited competition but must navigate infrastructural and compliance risks.

9. What are the local presence requirements for operators?

Land-based operators must maintain physical premises and local management fulfilling regulatory mandates. Online operators currently face no formal local presence requirement but may be encouraged or required under future regulatory reforms. Local partnerships improve market access and regulatory acceptance.

10. What payment methods are available and recommended?

Payment methods include mobile money platforms, credit/debit cards, bank transfers, and emerging e-wallets. Mobile money is particularly recommended due to its widespread use and accessibility in Guyana’s mobile-first environment. Cryptocurrency use remains limited but growing in niche segments.

- Mobile Money (Digicel Money, GTT Pay)

- Credit/Debit Cards (Visa, Mastercard)

- Bank Transfers

- E-wallets

- Cryptocurrencies (emerging)

11. What are the advertising and marketing restrictions?

Advertising regulations are minimal with few explicit restrictions, allowing broad promotional activities across traditional and digital channels. Operators typically leverage social media, sponsorships, and targeted promotions without significant time-of-day or content limitations. Emerging legislation may impose stricter controls to protect consumers.

12. What responsible gambling measures are mandatory?

Land-based operators are required to implement age verification, self-exclusion systems, deposit limits, and player education programs. Online platforms follow less rigorous standards locally but often comply with higher international standards from their foreign licensing jurisdictions.

- Age verification (minimum 18 years)

- Self-exclusion options

- Deposit and bet limits

- Responsible gambling information disclosure

- Monitoring player behavior for problem gambling indicators

13. How large is the iGaming market and what is the growth potential?

The iGaming market currently generates an estimated $40 million USD annually, with projected growth rates of 7-9% CAGR through 2028. Increasing mobile adoption and regulatory reforms are key drivers expanding betting participation and revenue potential particularly in sports betting and digital lottery segments.

14. Who are the main competitors and what is their market share?

Local land-based operators hold a smaller market share, with offshore international sportsbooks like Bet365, 1xBet, and Betway dominating online betting. These operators leverage established brands and regulatory licenses from other jurisdictions to capture over 70% of online sports betting volume.

15. What are the player preferences and typical spending patterns?

Players favor sports betting, especially football and cricket, followed by government lotteries and casino games in urban areas. Average Revenue Per User (ARPU) is around $50, with peak gaming activity during weekend evenings and major sporting events. Younger players show higher frequency and openness to new gaming types.

16. What are the key success factors and main challenges for new entrants?

Success depends on strong regulatory compliance, effective local partnerships, mobile-optimized platforms, payment flexibility, and responsible gambling initiatives. Challenges include infrastructural variability, evolving regulations, competition from offshore operators, and consumer education gaps.

- Regulatory transparency and adherence

- Localized payment integration

- Robust mobile-first user experience

- Strong marketing and brand trust

- Addressing digital literacy and social responsibility

Sources and References

- Guyana Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2025

- Central Bank of Guyana – Financial Statistics and Reports 2025

- Ministry of Finance Guyana – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics 2025

- Guyana Telecommunications Authority – Annual Reports 2025

- Gaming Industry Report Latin America 2024

- Guyana National Bureau of Standards – Internet Infrastructure Reports

- Guyana Ministry of Business – Corporate Registration Guidelines

- Guyana Revenue Authority – Taxation Framework Publications 2025

- Financial Services Commission of Guyana – Banking Sector Analysis 2025

- Digicel Guyana – Market Share and Services Overview

- GTT Guyana – Network Upgrade Plans and Market Data

- Guyana Digital Economy Report 2024

- Latin American Gaming Counsel – Guyana Market Update 2025

- Caribbean Network Providers Report 2025

- Guyana Ministry of ICT – National Digital Policy 2025

- International Monetary Fund – Guyana Economic Outlook 2025

- Guyana Social Services – Responsible Gambling Initiatives

- Global Betting and Gaming Consultants – Compliance Reports 2025

- New Dawn Guyana News – Gambling Regulatory Updates

- Guyana Legal Firm Publications – Corporate and Gaming Law 2025

- PwC Caribbean – Market Entry Advisory for Digital Gaming 2025

- LATAM iGaming Association – Market Reports 2024-2025

- USAID Guyana Digital Inclusion Report 2025

- Guyana Chamber of Commerce – Business Climate Overview 2025

- EY – Taxation and Investment Guide Guyana 2025

- Caribbean Development Bank – ICT Investment Analysis 2024

- Guyana Lottery Commission – Annual Performance Review 2025

- Guyana Ministry of Culture and Tourism – Entertainment Trends 2025

🎯 Gambling Databases Country Rating: Guyana

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.8/10 | 🟡 Moderate |

| Player Access Score | 5.5/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 5.1/10 | Emerging market with significant regulatory uncertainty – proceed with extreme caution |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ONLINE CASINO GAMING COMPLETELY UNREGULATED: No licensing framework exists for online casinos, poker, or most digital gambling products. Only sports betting and government lotteries are expressly legal online.

- NO LOCAL LICENSING AVAILABLE: There is currently NO way to obtain a local Guyana iGaming operator license. The regulatory framework does not exist as of 2025.

- REGULATORY VACUUM = LEGAL LIMBO: Operating as an offshore casino serving Guyana players puts you in a grey zone with ZERO legal protection and potential future prosecution when regulations are enacted.

- PENDING LEGISLATION THREAT: Government is actively developing comprehensive online gambling regulations. Your offshore operation today could become explicitly illegal tomorrow.

- EXTREMELY SMALL MARKET: With only 791,000 total population and 0.4% online penetration, you’re targeting approximately 3,200 active players generating USD $40M total market revenue. This is a TINY market.

- INFRASTRUCTURE CHALLENGES: Only 50% internet penetration, frequent rural outages, limited payment infrastructure. Expect high technical support costs and payment processing failures.

- HIGH ENTRY COSTS FOR TINY RETURNS: Minimum USD $500,000 working capital required to operate for 12 months in a market generating only $40M total annual revenue across ALL operators.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Started at 0.5 for grey area status. Online sports betting legal (+1.5). ONLINE CASINO COMPLETELY UNREGULATED – no legal framework exists (-1.5). Government lotteries online legal but irrelevant to commercial operators (+0). Regulatory framework described as “nascent and evolving” creating massive uncertainty (-0). Final: 0.5/3.0. This is essentially a legal black hole for online casino operators. |

| Licensing Process | 25% | 0.0/2.5 | NO LICENSING FRAMEWORK EXISTS for online operators (0 points). Land-based casino licensing requires hotel/resort with 150+ rooms – completely irrelevant for iGaming operators (-0). Application timeline “uncertain for online entry” per article. Foreign ownership allowed (+0.5). BUT application costs USD $10,000-$20,000 PLUS legal/consulting USD $30,000-$50,000 for a license that DOESN’T EXIST (-0.5). Total setup costs over USD $250,000 (-0.25). Final: 0.0/2.5. You literally CANNOT get licensed here. |

| Taxation & Costs | 20% | 1.0/2.0 | No established GGR or turnover tax for online gambling (+0, but this is because regulations don’t exist, not because it’s favorable). Corporate income tax at BRUTAL 40% standard rate with 2% minimum on turnover (-1.0 point). Total working capital requirement USD $500,000 for 12 months in a $40M total market (-0.5). Market entry costs USD $290,000-$620,000 excluding working capital (-0.5). Customer acquisition costs likely high due to tiny market and limited payment options (-0). No player winnings tax (+0.5, minor benefit). Final: 1.0/2.0. Economics are TERRIBLE. |

| Operational Requirements | 15% | 1.0/1.5 | No explicit local presence requirements for online operators (+1.5) – BUT this is because there are NO requirements at all since licensing doesn’t exist. Land-based casinos require physical presence in 150+ room hotels (irrelevant for online, -0). Limited payment infrastructure forces high payment processing costs (-0.25). Only 50% internet penetration and frequent rural outages increase technical support costs (-0.25). Foreign ownership permitted (+0, already counted). Final: 1.0/1.5. Minimal requirements exist only because regulations don’t exist. |

| Market Environment | 10% | 0.3/1.0 | Guyana ranks moderately on Ease of Doing Business with “bureaucratic delays” (+0.5). Advertising regulations “largely undefined online” creating legal uncertainty (-0.25). “Pending legislation for comprehensive online regulation” means rules could change dramatically overnight (-0.25). Market dominated 70%+ by international offshore operators – massive existing competition (-0.25). Enforcement mechanisms include “fines exceeding one million Guyanese dollars and imprisonment from six months to two years” for unlicensed operations (-0.5, though currently focused on land-based). Infrastructure quality “improving” but still poor in rural areas (-0). Final: 0.3/1.0. |

OPERATOR EASE TOTAL: 4.8/10

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Partially legal status: sports betting explicitly legal (+1.5), government lotteries online legal (+0.5). ONLINE CASINOS AND POKER HAVE NO LEGAL FRAMEWORK – exist in grey zone, not explicitly legal (-1.5). Players currently face no penalties for using offshore sites (+0.5). Article states online gambling “holds a legally ambiguous position due to outdated legislation.” Final: 2.0/4.0. Players can access sports betting legally but everything else is legal limbo. |

| Practical Accessibility | 30% | 1.5/3.0 | Multiple payment methods available including cards, mobile money, growing crypto acceptance (+2.0). However, only 50% internet penetration severely limits accessibility (-0.5). Rural areas have “frequent outages” impacting reliability (-0.25). No evidence of ISP blocking currently (+0), but “pending legislation” could change this. “Limited” payment infrastructure compared to developed markets (-0.25). Mobile penetration 77% helps (+0.5). Final: 1.5/3.0. Technical accessibility exists but infrastructure is weak. |

| Player Penalties | 20% | 2.0/2.0 | No tax on player winnings (+1.0). Article explicitly states “There is no tax imposed on players’ gambling winnings in Guyana” and no evidence of any penalties for players using offshore sites (+1.0). Final: 2.0/2.0. This is the ONE bright spot – players face zero penalties currently. |

| Market Availability | 10% | 0.25/1.0 | ZERO licensed online casino operators – no local licensing framework exists (0 points). Three land-based casino premises max per region (irrelevant for online). Market “dominated by international operators licensed offshore” at 70%+ market share (+0.25 for offshore availability). Only 3,200 active online players estimated in entire country. Final: 0.25/1.0. Offshore only, zero local operators. |

PLAYER ACCESS TOTAL: 5.5/10

🔍 Key Highlights

Strengths (If Any)

- No player taxation: Gambling winnings are completely tax-free for players, which theoretically improves player retention

- English language: Official language is English, eliminating localization barriers for international operators

- Foreign ownership permitted: No restrictions on foreign investors owning gambling businesses

- No ISP blocking currently: Unlike many jurisdictions, there is no active blocking of offshore gambling sites (yet)

- Young demographic: 55% of population under 35 years old represents digitally-oriented potential player base

- Economic growth: 8% annual GDP growth and oil discoveries indicate rising consumer purchasing power over time

⛔️ CRITICAL RISKS AND CHALLENGES

- [Product Prohibitions:] ONLINE CASINOS, POKER, AND MOST DIGITAL GAMBLING HAVE NO LEGAL FRAMEWORK. Only sports betting and government lotteries are expressly legal online. This eliminates 60-70% of typical iGaming revenue streams and makes your business model potentially illegal when regulations are enacted.

- [No Licensing Available:] THERE IS NO WAY TO OBTAIN A LOCAL ONLINE GAMBLING LICENSE. The article explicitly states “no local framework for iGaming operators” and “no formal licensing regime for other online games.” You cannot operate legally even if you wanted to. Timeline for licensing framework creation is completely uncertain – could be years.

- [Pending Regulatory Changes:] Article warns of “pending legislation for comprehensive online regulation.” Your offshore operation today could become explicitly illegal tomorrow. Government is “actively developing” new regulations with unknown enforcement provisions, penalties, and retroactive application.

- [Catastrophically Small Market:] Total population 791,000. Only 0.4% online gambling penetration = approximately 3,200 active players. Total market revenue USD $40M annually across ALL operators. Market penetration forecast to reach only 0.7% by 2028 (5,500 players). Average revenue per user only USD $50. This market is TOO SMALL to justify USD $500,000+ entry costs.

- [Prohibitive Entry Economics:] Minimum total investment USD $790,000-$1,120,000 including: licensing/legal USD $40,000-$70,000, technology USD $150,000-$300,000, marketing USD $100,000-$200,000, working capital USD $500,000. In a market generating only USD $40M total annual revenue, achieving ROI is nearly impossible for new entrants.

- [Brutal Tax Structure:] 40% corporate income tax with 2% minimum on turnover creates effective tax rates over 40% even before GGR taxes are established. When online gambling tax regulations are enacted, expect GGR taxes stacked on top of this 40% corporate rate for total effective rates potentially exceeding 50-60%.

- [Infrastructure Limitations:] Only 50% internet penetration, frequent outages in rural areas, “improving broadband” indicates current quality is poor. Mobile internet speeds only 20-40 Mbps in urban areas. Limited payment infrastructure forces reliance on costly international payment processors. Technical support costs will be extremely high relative to player value.

- [Offshore Competition:] International sportsbook operators with global licenses “collectively hold over 70% of the digital betting market share.” You’re competing against established, well-funded operators like Bet365, 1xBet, etc. who already have brand recognition and player trust. Market share gain will be expensive and slow.

- [Payment Processing Challenges:] Article mentions “growing crypto acceptance” suggesting current payment options are limited. Bank account penetration is “rising but still limited in rural populations.” Credit card penetration likely low. Payment failures and high processing costs expected.

- [Future Enforcement Risk:] Current grey zone status offers NO legal protection. Enforcement mechanisms already include “fines exceeding one million Guyanese dollars and imprisonment from six months to two years” for unlicensed operations. When online regulations are enacted, these penalties could apply retroactively or create prosecution risk for current operators.

- [Market Concentration:] 70%+ market share held by international offshore operators means severe competition for the remaining 30%. Three land-based casino licenses maximum per region shows government favors market concentration, not competitive markets.

- [Consumer Protection Void:] “Digital gambling platforms currently lack standardized consumer protection mandates” means no regulatory requirements for responsible gambling, KYC, AML. BUT when regulations are enacted, compliance costs will spike dramatically and retroactive compliance may be required.

Player-Specific Issues

- Product Access Limitations: Players can ONLY legally access sports betting and government lotteries online. Casino games, poker, and other products exist in legal grey zone with zero consumer protection.

- Infrastructure Challenges: 50% of population has NO internet access. Rural players face frequent outages and poor connectivity limiting play sessions.

- Limited Payment Options: “Limited payment infrastructure” means players struggle with deposits/withdrawals. International payment processors may reject transactions. Cryptocurrency “limited adoption” despite “emerging interest.”

- No Regulatory Protection: Players using offshore sites have zero recourse for disputes, no responsible gambling protections, no deposit insurance, and no regulatory authority to file complaints with.

- Low Income Levels: Median individual income USD $6,500 annually with “moderate inequality” means most players have very limited disposable income for gambling. ARPU of only USD $50 reflects this constraint.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD $790,000 – $1,120,000 (legal/licensing $40k-$70k + technology $150k-$300k + marketing $100k-$200k + 12-month working capital $500k-$550k)

Monthly Operating Costs: USD $50,000 – $80,000 (technology hosting, payment processing, customer support, compliance monitoring, marketing)

Total Addressable Market: 791,000 total population × 0.4% online penetration = 3,200 active players generating USD $40M annually across ALL operators

Realistic Market Share Target: 5-10% for new entrant = USD $2M – $4M annual revenue (if you’re lucky and spend heavily on marketing)

Effective Tax Rate on Revenue: Currently 40% corporate income tax + 2% minimum turnover tax. When GGR taxes are enacted, expect 15-25% GGR tax + 40% corporate = 50-60% total effective rate.

Customer Acquisition Cost: Not specified in article but likely USD $200-$400+ given small market, high competition from 70% offshore market share holders, limited payment options, and poor infrastructure. Marketing to 791,000 people with 50% internet penetration in scattered urban/rural areas is expensive per acquisition.

Time to Breakeven: 36-60+ months IF you achieve 5-10% market share AND no new regulations increase costs. More likely NEVER break even.

Time to Positive ROI: 48-72+ months IF best-case scenario. Realistically, most operators will NEVER achieve positive ROI in this market.

Profitability Assessment: THE ECONOMICS ARE COMPLETELY UNVIABLE FOR NEW ENTRANTS. You need to invest USD $800,000-$1,100,000 to compete for a share of a USD $40M market where 70% is already controlled by international operators with established brands. Even capturing 10% market share (USD $4M annually) at 40% tax rate and USD $50k-$80k monthly costs leaves minimal profit margin – completely insufficient to recoup USD $800k-$1.1M investment in any reasonable timeframe.

The market is simply TOO SMALL and TOO COMPETITIVE to justify entry costs. Only existing operators with sunk platform costs should consider this market as a marginal add-on territory, not a primary target.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | HIGH | Operating in complete legal grey zone with zero licensing framework. Pending legislation could criminalize current operations retroactively. Enforcement mechanisms already exist: fines over GYD $1M + 6 months to 2 years imprisonment for unlicensed operations. Current lack of enforcement does NOT equal legality – regulatory vacuum could close suddenly with prosecution of existing operators. No ISP blocking currently but pending regulations likely to include blocking provisions. |

| Licensed Sports Betting Operators | MEDIUM | Sports betting expressly legal but no local licensing framework exists yet – must operate offshore. When licensing is introduced, expect product restrictions (sports only, no casino), heavy taxation likely 15-25% GGR + 40% corporate = 50-60% effective rate, strict regulatory compliance burdens, and mandatory responsible gambling funding. Market size USD $40M makes licensing costs disproportionately high relative to revenue potential. |

| Affiliates/Advertisers | MEDIUM | Advertising regulations “largely undefined online” creates uncertainty. Land-based advertising has “moderate restrictions” suggesting future online restrictions likely when regulations are enacted. Promoting offshore casinos (currently in legal grey zone) could become explicitly illegal. No current evidence of affiliate prosecution but regulatory framework development likely to include affiliate compliance requirements. Payment processors may terminate accounts promoting unregulated gambling. |

| Payment Processors | MEDIUM | “Limited payment infrastructure” and pending regulations create compliance uncertainty. When online gambling regulations are enacted, expect strict KYC/AML requirements, transaction monitoring mandates, and potential restrictions on processing for unregulated operators. International payment processors (Visa, Mastercard) may preemptively restrict Guyana gambling transactions to avoid future regulatory issues. |

| Company Directors/Executives | MEDIUM-HIGH | Operating unlicensed gambling business carries penalties of “fines exceeding one million Guyanese dollars and imprisonment from six months to two years.” Directors face personal liability under “fit and proper” criteria being developed. Extradition risk MODERATE – Guyana has “strong international relations with regional trade blocs and the Commonwealth” suggesting extradition treaties likely with UK, Canada, Caribbean nations. Travel through Commonwealth countries could expose directors to arrest if regulations are enacted and violations charged. |

🚨 Extradition and International Enforcement

Extradition Treaties: As a Commonwealth member with “strong international relations with regional trade blocs and the Commonwealth,” Guyana likely has extradition agreements with: United Kingdom, Canada, Caribbean Community (CARICOM) member states, potentially other Commonwealth nations. Specific treaty details not provided in article but Commonwealth membership suggests broad extradition cooperation.

Enforcement History: No specific cases of international gambling prosecution or extradition mentioned in article. However, enforcement mechanisms for unlicensed gambling already exist with severe penalties (fines over GYD $1M + 6 months to 2 years imprisonment), indicating government willingness to prosecute gambling violations.

Safe Jurisdictions: Not specified in article. Typical non-extradition jurisdictions for Commonwealth member states include: Russia, China, UAE, some CIS countries. However, “pending legislation” could expand Guyana’s enforcement cooperation internationally.

Travel Risk: MODERATE risk when traveling through Commonwealth countries IF regulations are enacted and you are charged with unlicensed gambling operations. Current regulatory vacuum provides some protection but offers zero legal certainty. Directors of offshore operators serving Guyana should avoid travel through UK, Canada, Caribbean nations if regulations are enacted and violations charged.

📋 Final Verdict

Guyana receives an Operator Ease Score of 4.8/10 and a Player Access Score of 5.5/10, resulting in an overall market attractiveness rating of 5.1/10.

HONEST ASSESSMENT: Guyana is a REGULATORY BLACK HOLE masquerading as an opportunity. While articles promote it as an “emerging market,” the brutal reality is there is NO legal way to obtain an online gambling license, the entire online casino sector exists in legal limbo, and pending regulations could criminalize current operations overnight. Even worse, the total market size of USD $40M with only 3,200 active players makes the economics completely unviable – you need to invest USD $800,000-$1,100,000 to compete for scraps in a market dominated 70% by international operators.

The combination of regulatory uncertainty, catastrophically small market size, brutal 40% corporate tax rates (with GGR taxes coming), poor infrastructure, and zero licensing pathway creates one of the worst risk-reward ratios in global iGaming. This is a market to AVOID unless you are an existing operator adding it as a marginal territory with zero additional platform costs.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Existing international operator with established platform: Already operating in 20+ markets and can add Guyana with near-zero marginal cost for incremental USD $2M-$4M annual revenue

- Sports betting specialist willing to wait: Can operate offshore serving sports betting demand while monitoring regulatory development for eventual licensing opportunity (if/when it arrives)

- Patient investor with 5+ year horizon: Willing to accept losses for 3-5 years while market matures, regulations are enacted, internet penetration rises, and GDP per capita increases from current USD $19,000

- Willing to target only urban Georgetown: Focus exclusively on the 234,000 residents in Georgetown where internet penetration and payment infrastructure are adequate, ignoring 70% of country in rural areas

❌ Definitely Avoid If You Are:

- Casino-focused operator: Online casinos have NO legal framework and exist in complete legal limbo with zero path to licensing

- Startup or small operator: USD $800,000-$1,100,000 entry cost for a USD $40M total market (targeting 3,200 players) makes ROI mathematically impossible

- Seeking licensed, legal operation: There is literally NO online gambling licensing framework – you CANNOT get licensed even if you want to comply with local law

- Risk-averse operator: Pending legislation could criminalize your operation overnight, regulations could apply retroactively, enforcement includes imprisonment for directors

- Seeking quick ROI within 3 years: Breakeven 36-60+ months, positive ROI 48-72+ months IF best case – most will never break even

- Operators without existing Caribbean/LatAm presence: Payment processing, customer support, and marketing costs are prohibitively high without regional infrastructure already in place

- Primary market seekers: This can ONLY be a marginal add-on market, never a primary target or revenue driver given tiny size and massive competition

- Companies prioritizing legal certainty: The regulatory vacuum and “pending legislation” create maximum legal uncertainty – you’re operating blindfolded hoping regulators don’t criminalize you tomorrow

⚠️ BOTTOM LINE: Guyana is a market for EXISTING operators only as a marginal add-on with near-zero incremental cost. New entrants face catastrophic economics (USD $800k-$1.1M investment for USD $2M-$4M revenue potential in a 3,200-player market) combined with maximum legal uncertainty (no licensing framework + pending criminalization risk). The “emerging market opportunity” narrative is marketing fiction – the reality is a regulatory black hole with prohibitive entry costs targeting one of the world’s smallest gambling markets. AVOID COMPLETELY unless you meet very specific criteria above.