Haiti presents a unique iGaming opportunity characterized by a largely unregulated online gambling landscape contrasted with limited, traditional land-based casino operations. While formal gambling exists through licensed casinos and an extensive lottery market, the absence of clear online gambling laws creates significant challenges and opportunities for operators willing to navigate a developing regulatory framework.

The country’s gaming market is small yet showing steady growth, primarily fueled by informal lottery (“borlette”) popularity and emerging digital payment adoption. Strategic entry requires understanding Haiti’s fragmented regulatory environment, tax structures, and compliance expectations, all set against a backdrop of economic and infrastructural constraints.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Land-based casinos and lottery legal; online gambling unregulated |

| Regulatory Authority | Lottery of the Haitian State (LISA/LEH) |

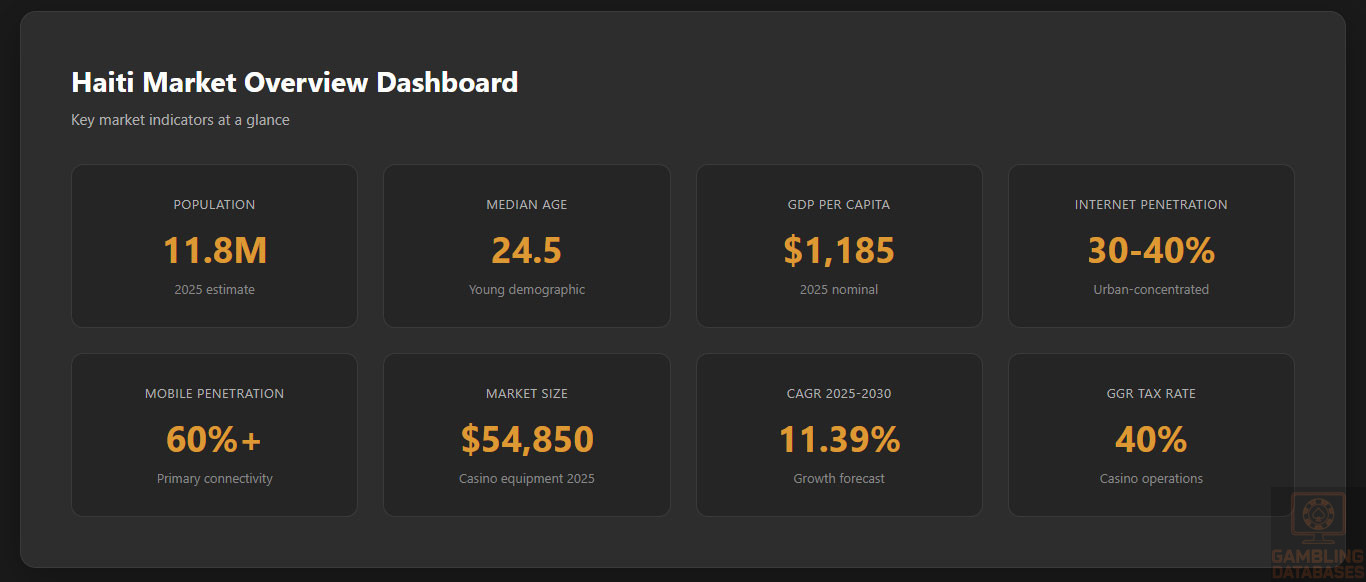

| Population | 11.8 million (2025 estimate) |

| Median Age | 24.5 years |

| GDP (Nominal) | Approx. $14 billion USD (2025) |

| GDP Per Capita | Approx. $1,185 USD |

| Internet Penetration | Approx. 30-40% |

| Mobile Penetration | Over 60% |

| Casino License Fee | $1,000 per annum |

| Gross Gaming Revenue (GGR) Tax Rate | 40% on casinos |

| Withholding Tax on Player Winnings | 5% (withheld from operator, not player) |

| License Types | Casino, Gaming House, Lottery Operator |

| Minimum Licensed Casino Requirement | Hotels with 200+ rooms |

| Allowed Casino Games | Slots, table games (blackjack, roulette, craps) |

| Licensed Casinos | El Rancho Hotel and Casino (largest) |

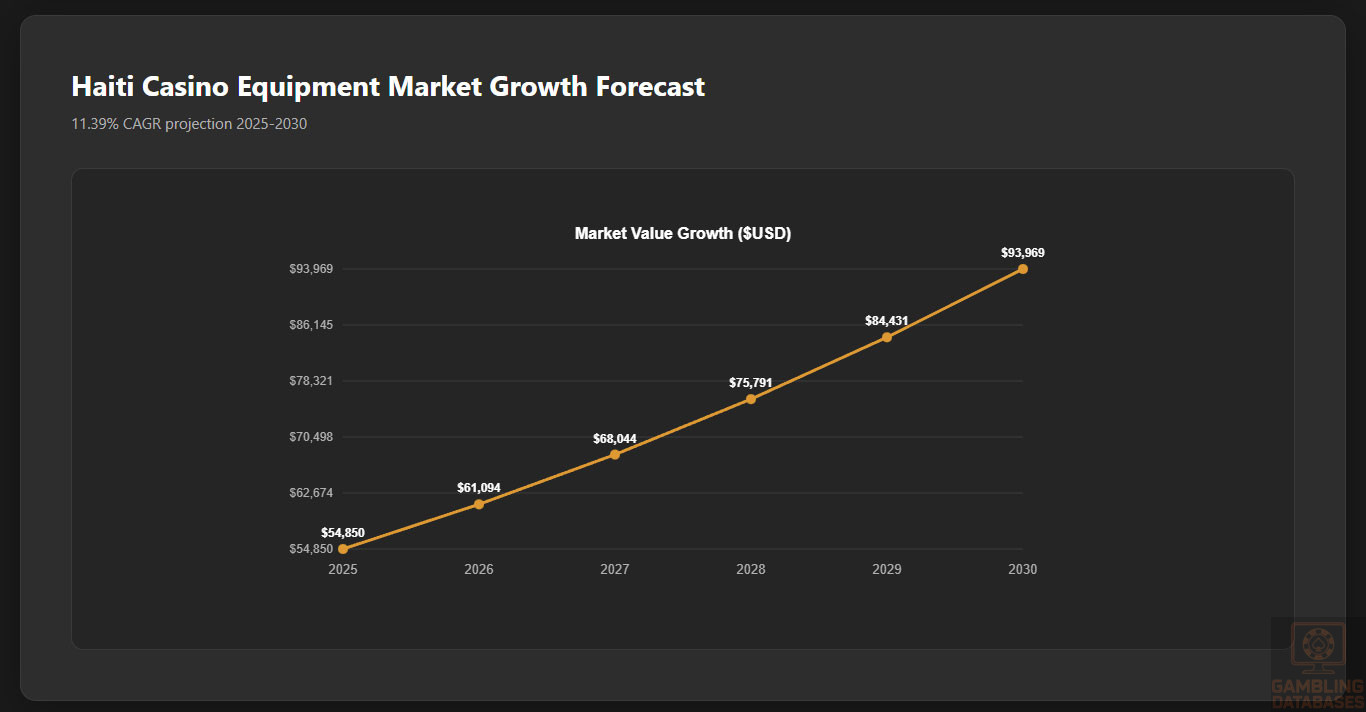

| Market Size (Casino Equipment) | $54,850 USD (2025 forecast) |

| Market Growth (Casino Equipment) | 11.39% CAGR (2025-2030 forecast) |

| Informal Lottery Market | Dominant gambling segment (Borlette) |

| Online Gambling Licensing | No licensing structure; offshore operators accessible |

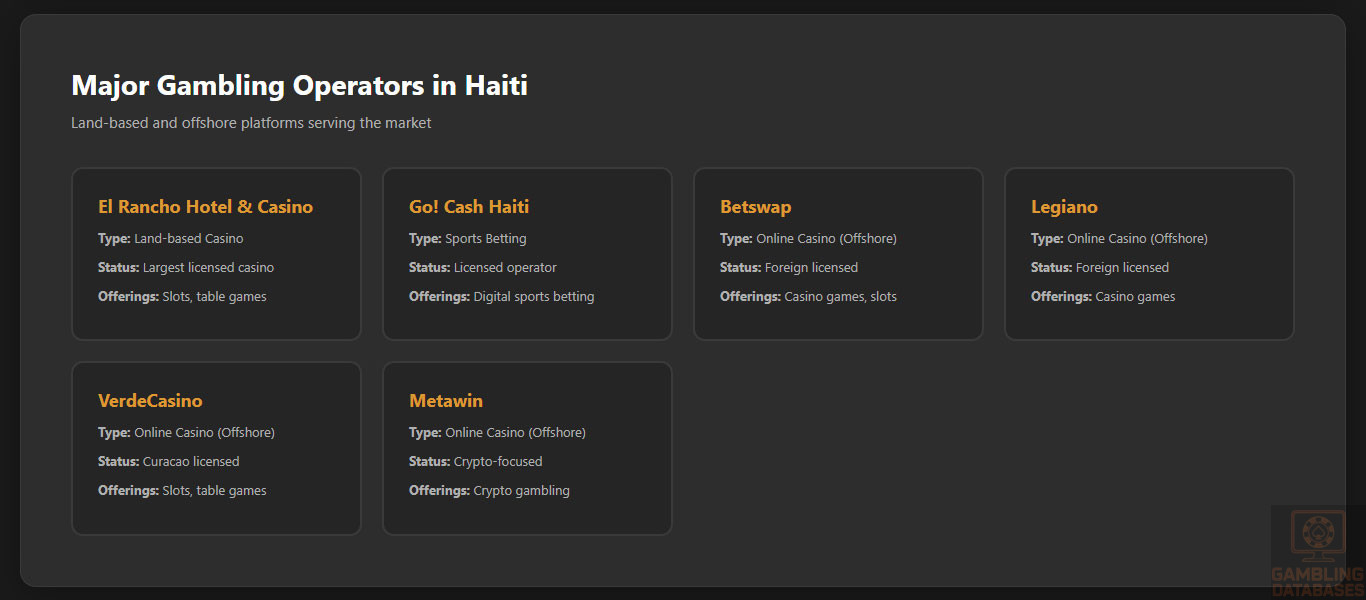

| Key Online Operators Serving Haiti | Betswap, Legiano, VerdeCasino, Metawin |

| Entry Barriers | Regulatory uncertainty, infrastructure challenges |

| Business Environment | Low transparency; informal market prevalent |

| Compliance Risks | Weak AML controls, lack of responsible gambling laws |

| Advertising Restrictions | Subject to LISA guidelines; restrictions on misleading ads |

| Tax Compliance Monitoring | Limited, mostly focused on land-based operators |

| Player Protection Measures | Minimal; no mandated responsible gambling programs |

| Market Outlook | Moderate growth potential amid regulatory evolution |

| Average Revenue Per User (ARPU) | Data not reported; informal market dominant |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling in Haiti is regulated primarily through land-based casino operations and lottery activities. The regulatory authority responsible is the Lottery of the Haitian State (LISA), sometimes referenced as LEH. The legal framework is antiquated and offers limited formal structure, mainly governing physical casinos and lottery operators.

Online gambling exists in a legal gray area. No specific online gambling laws or licensing systems exist within Haiti. Consequently, no operators are licensed to offer online gambling from within the country. Haitian players commonly access international offshore operators that serve the region without Haitian regulatory oversight. This absence of online regulation results in minimal consumer protection and an uncoordinated approach to compliance and taxation.

Land-Based Gambling Activities

The land-based gambling sector consists mainly of:

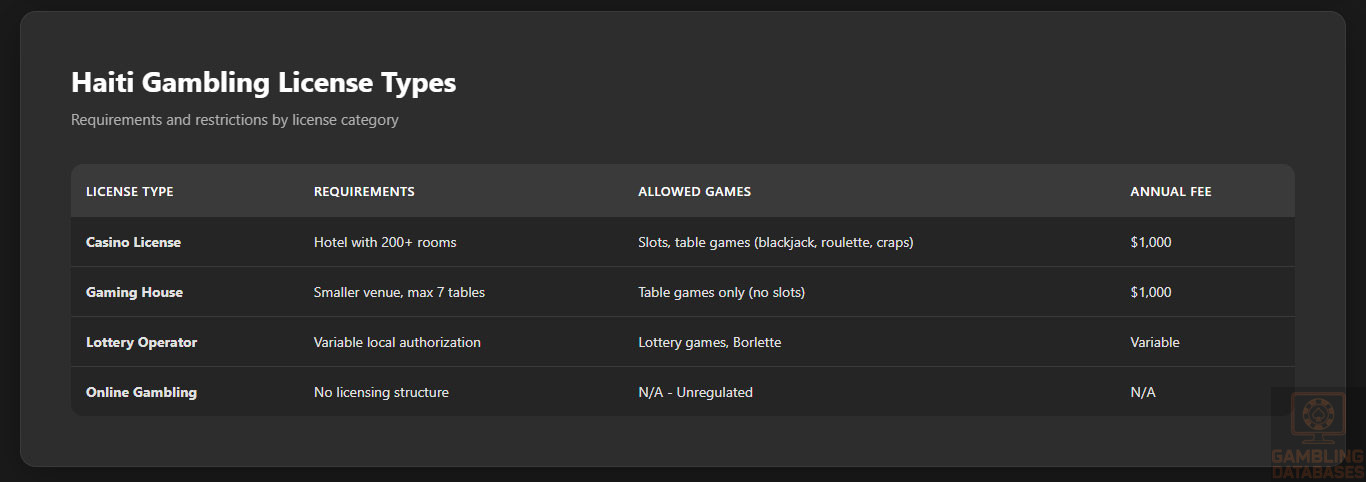

- Licensed casinos in large hotels, featuring slot machines and table games such as blackjack, roulette, and craps

- Gaming houses, which are smaller venues limited to a maximum of seven table games and no slots

- Widespread lottery agencies (“borlette” booths) operating informally across urban and rural areas

- Sports betting conducted through licensed operators and informal channels

The largest and most recognized land-based casino is the El Rancho Hotel and Casino, which provides a variety of slot machines and table games. Sports betting operators like Go! Cash Haiti have also gained market share, particularly in the digital space.

Online Gambling Framework

Haiti’s online gambling regulation is effectively nonexistent. There is no formal legalization, licensing, or regulatory oversight for online casinos, online poker, or sports betting platforms operating within the country. The regulatory gap means that Haitian players are reliant on offshore online gambling sites that accept residents from Haiti without local licensing obligations.

This unregulated environment poses significant risks such as lack of consumer protection, possible fraud exposure, and limited enforcement of anti-money laundering (AML) policies. Payment access is a known challenge; some banks restrict gambling-related transactions, prompting users to adopt alternative payment methods like e-wallets and cryptocurrencies. Operators targeting Haiti must therefore consider crypto-friendly and mobile-compatible platforms to maximize accessibility.

Licensed Operators and Market Players

The competitive structure of Haiti’s formal gambling market is narrowly concentrated, with a few known licensed operators dominating land-based gambling. The El Rancho Hotel and Casino is the flagship licensed casino, while several smaller gaming houses operate under restricted licenses.

In the lottery segment, countless informal “borlette” agents provide access to popular lottery games, which hold the largest player base and transaction volume by far. On the online front, international offshore platforms such as Betswap, Legiano, VerdeCasino, and Metawin serve Haitian players, operating remotely with licenses from foreign jurisdictions like Curacao.

The absence of domestic online licenses and consumer protections means offshore operators dominate the online landscape, whereas local operators focus on land-based venues and lottery operations under LISA supervision. Market share data for online operators is limited, but these platforms are heavily used by younger, urban demographics.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing authority in Haiti lies with LISA, which issues licenses primarily to hotels for casino operations and to smaller venues for gaming houses. The application process is opaque, with limited publicly available guidance on procedural steps or approval times.

Licenses require compliance with several financial and technical standards, including:

- Hotel size minimum of 200 rooms for casino licenses

- Specification and approval of the gaming floor and permitted games

- Submission of financial statements and criminal background checks for owners and directors

- Adherence to approved game types and operational standards

- Payment of a $1,000 annual license fee

Gaming houses face restrictions on the number and types of games— a maximum of seven table games without slot machines—and must adhere to similar licensing fees and approval standards. Lottery operators engage in variable local authorization processes, often informal and aligned with state lottery oversight.

Local Presence and Operational Requirements

Operators seeking licensing in Haiti must maintain a physical presence, especially land-based casinos situated within qualifying hotels. Registered business entities and premises subject to inspection are part of the licensing prerequisites.

There are no specific domain requirements because online gambling licensing is nonexistent. Foreign ownership is permitted, but operators must coordinate with local authorities and meet standard corporate registration and taxation obligations under general Haitian business law.

Operational requirements include maintaining records for audits, facilitating regulatory inspections, and complying with financial reporting. Licensing is annual and renewable, contingent upon ongoing compliance and payment of fees.

Compliance Obligations and Monitoring

Player Protection and Identification

Haiti lacks comprehensive responsible gambling regulations and player protection frameworks. There are no mandated self-exclusion programs or formal policies governing advertising and consumer information supported by law.

Age and identity verification processes are basic, mostly delegated to operators’ policies and minimal regulatory oversight. Anti-money laundering initiatives exist but are undeveloped by international standards, with the country identified as having weak AML controls.

- Age verification to restrict underage gambling

- Basic Know Your Customer (KYC) requirements during player registration

- Responsible gambling messaging encouraged but not legally required

- No formal self-exclusion or problem gambling programs mandated

- Operator obligation to monitor suspicious financial transactions

Financial Monitoring and Reporting

Licensed operators are subject to periodic audits and financial reporting requirements enforced by LISA, focusing on the accuracy of gross gaming revenue and tax remittances. Financial transaction monitoring aims to meet minimal AML standards but lacks rigorous enforcement mechanisms.

Operators must submit regular reports detailing revenue, taxes paid, and transaction volumes. These are critical to maintaining licenses and preventing penalties. However, weak institutional capacity often limits effectiveness.

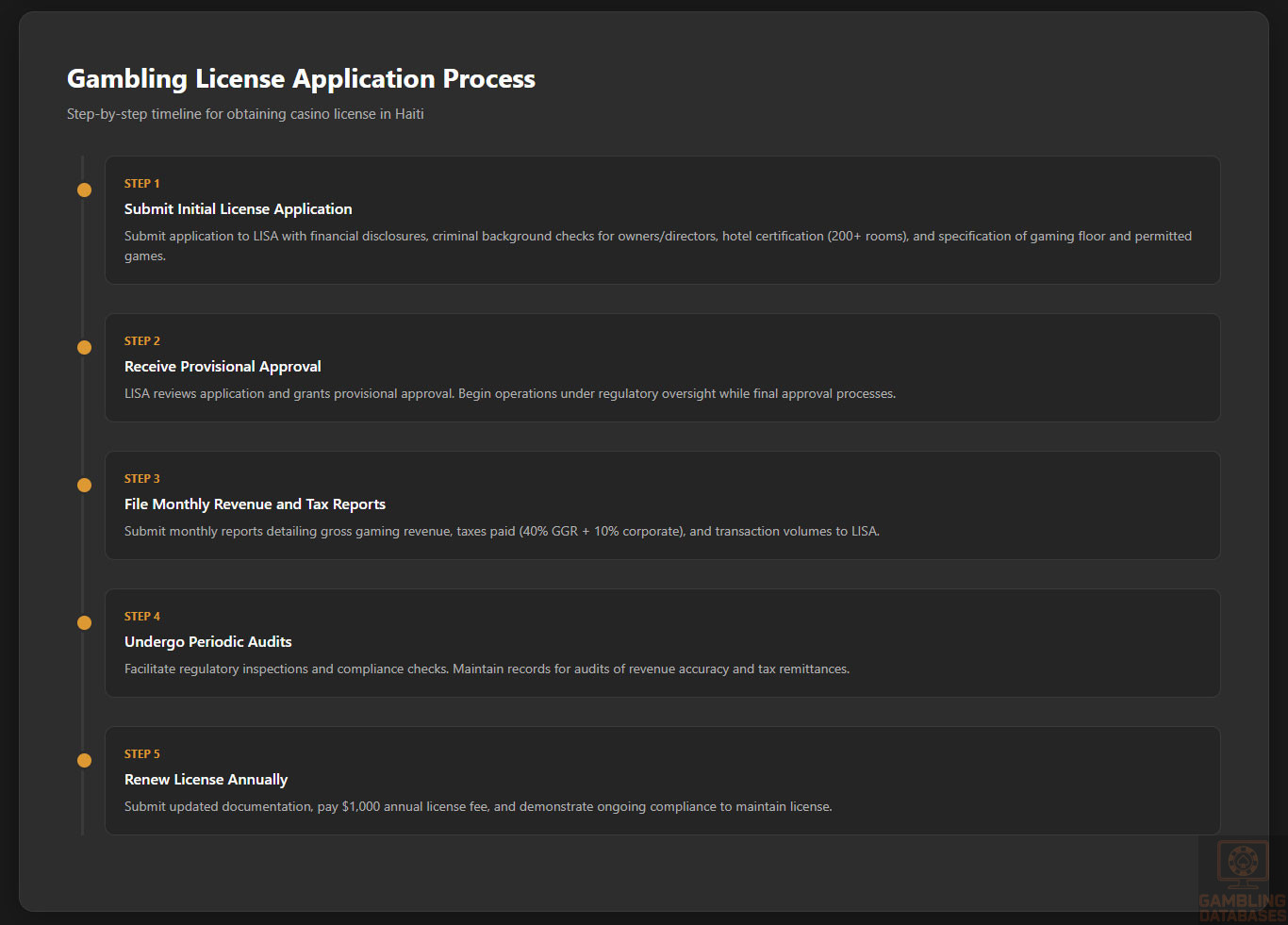

- Submit initial license application with financial disclosures

- Receive provisional approval and begin operations under oversight

- File monthly revenue and tax reports to LISA

- Undergo periodic audits and compliance checks

- Renew license annually with updated documentation and fees

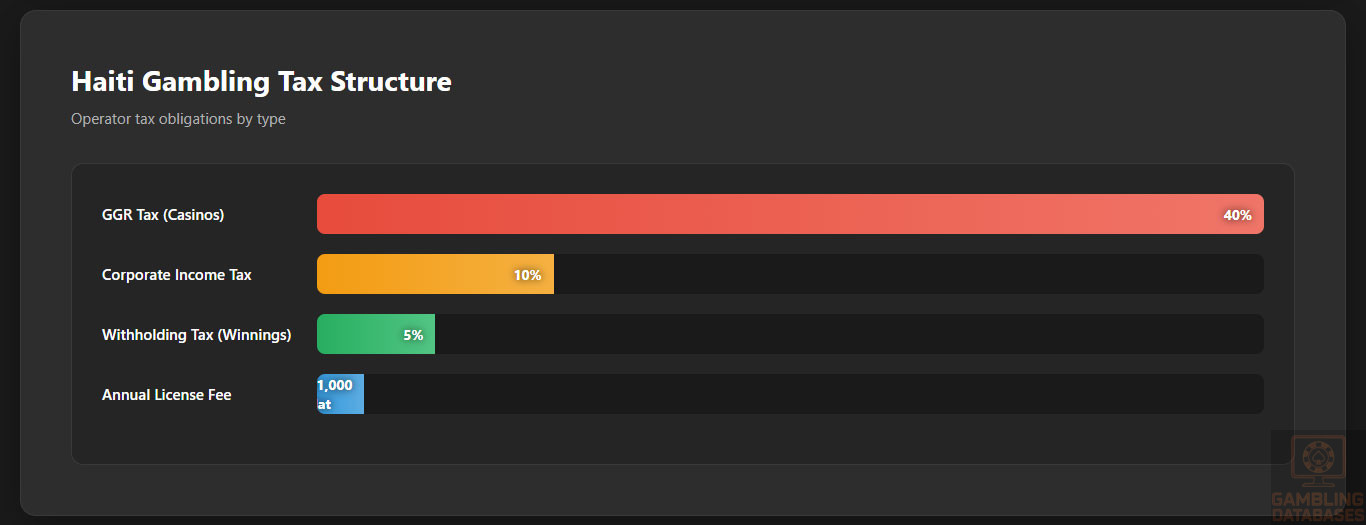

Taxation Structure and Financial Obligations

Player Taxation

In Haiti, players are not directly taxed on gambling winnings. Instead, a 5% withholding tax is applied to winnings by operators when payouts occur, which is deducted from the operator’s amounts rather than the player’s gross winnings. This structure simplifies player obligations but places compliance responsibility on operators.

Operator Taxation

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue (GGR) Tax on Casinos | 40% |

| Annual License Fee | $1,000 USD flat fee |

| Withholding Tax on Player Winnings | 5% withheld by operator |

| Corporate Income Tax | Flat 10% on operations |

| Gaming Houses Tax | Similar to casinos (details less documented) |

Operators must also pay corporate income tax on net profits at a flat rate of 10%, consistent with general Haitian tax law. These obligations combine to create a relatively heavy tax burden on gaming operators, particularly at 40% GGR tax, which is among the higher rates globally.

Gambling Market Financial Performance

The dominant financial contributor within Haiti’s gambling ecosystem is the informal lottery market, which accounts for the majority of player participation and transaction value. Formal casinos and gaming houses contribute a smaller, more measurable revenue share.

The market for gaming equipment, which reflects investment in physical casino assets and technology, is forecasted to grow at an 11.39% CAGR through 2030, albeit from a low base. Tax revenues from the gaming sector remain limited due to widespread informal operations and the lack of regulated online gambling.

Advertising and Marketing Restrictions

Advertising of gambling services in Haiti must comply with LISA guidelines to avoid misleading or harmful promotions. Restrictions include limiting deceptive claims and prohibiting targeting of minors.

Permitted advertising channels include authorized physical venues, local media outlets, and increasingly, digital platforms adhering to responsible marketing principles. However, clear statutory regulations are minimal, and enforcement inconsistent.

- Advertising content must not mislead or exploit vulnerable consumers

- Prohibition of marketing targeting persons under legal gambling age

- Restrictions on time frames and locations for gambling advertisements

- Sponsorship of events requires regulatory approval

- Online or digital marketing is largely unregulated but self-monitored by operators

Recent Regulatory Changes and Their Impact

While Haiti has not introduced recent major legislative reforms specific to gambling, incremental administrative adjustments by LISA have aimed to improve licensing transparency and tax compliance enforcement. No significant changes affecting online gambling legalization or player protection have been enacted.

The lack of new regulations maintains operational uncertainty for online market entrants, while land-based operators continue to shoulder the bulk of tax and compliance costs. This status quo encourages offshore operators to serve the Haitian online audience without local licensing.

Enforcement Mechanisms and Penalties

Enforcement of gambling regulation rests with LISA and local law enforcement. Penalties for unlicensed operations include fines, business closure, and possible imprisonment.

- Fines proportional to the scale of illegal operation

- Revocation of licenses upon non-compliance

- Seizure of gaming equipment used illegally

- Criminal charges and imprisonment for repeat offenders

- Restrictions on advertising for non-licensed entities

Enforcement remains challenging due to Haiti’s economic and infrastructural constraints, contributing to a persistent informal gambling sector beyond regulatory reach.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

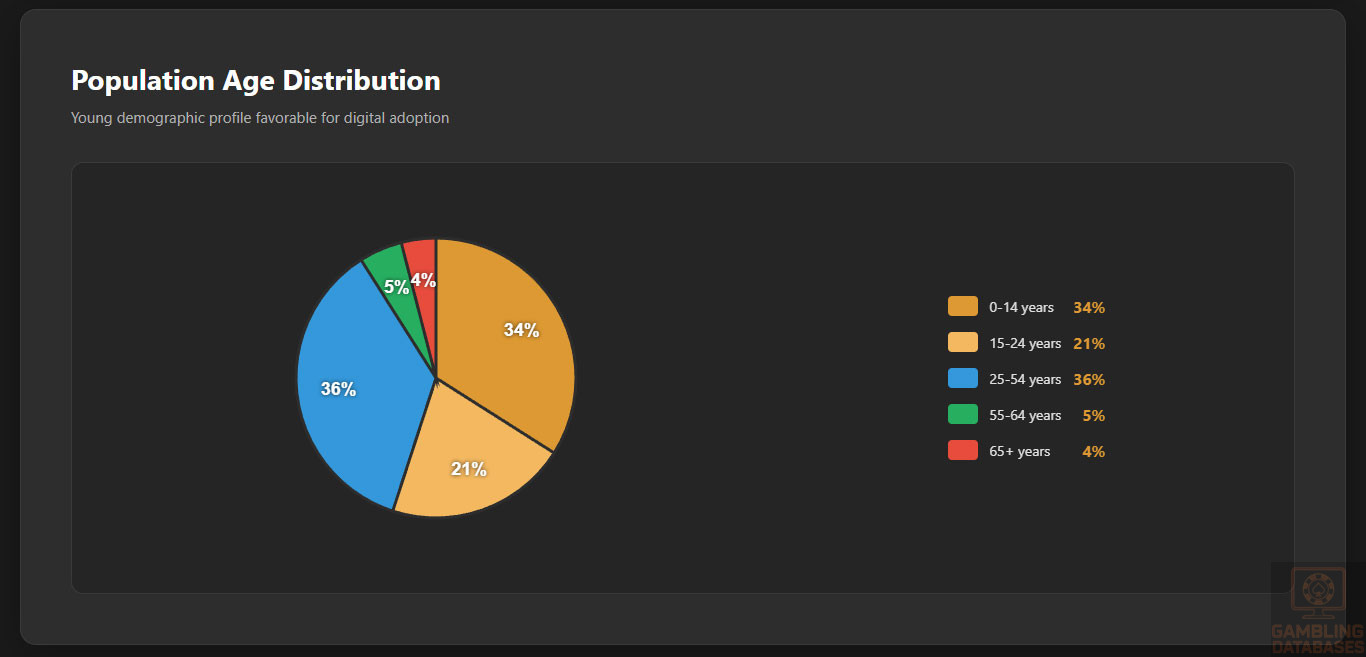

Haiti’s total population is estimated at 11.8 million in 2025, characterized by a youthful demographic structure with a median age of approximately 24.5 years. The population is almost evenly split between genders, with a slight female majority of about 51%. The majority of Haitians are under 30 years old, reflecting a young and potentially tech-savvy consumer base.

Urbanization is moderate, with roughly 60% of the population residing in urban areas, primarily concentrated around the capital and major cities. Rural regions retain a large share of the population, where access to digital infrastructure and gambling venues is limited compared to urban centers.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 34% |

| 15-24 years | 21% |

| 25-54 years | 36% |

| 55-64 years | 5% |

| 65 years and over | 4% |

Geographic Distribution

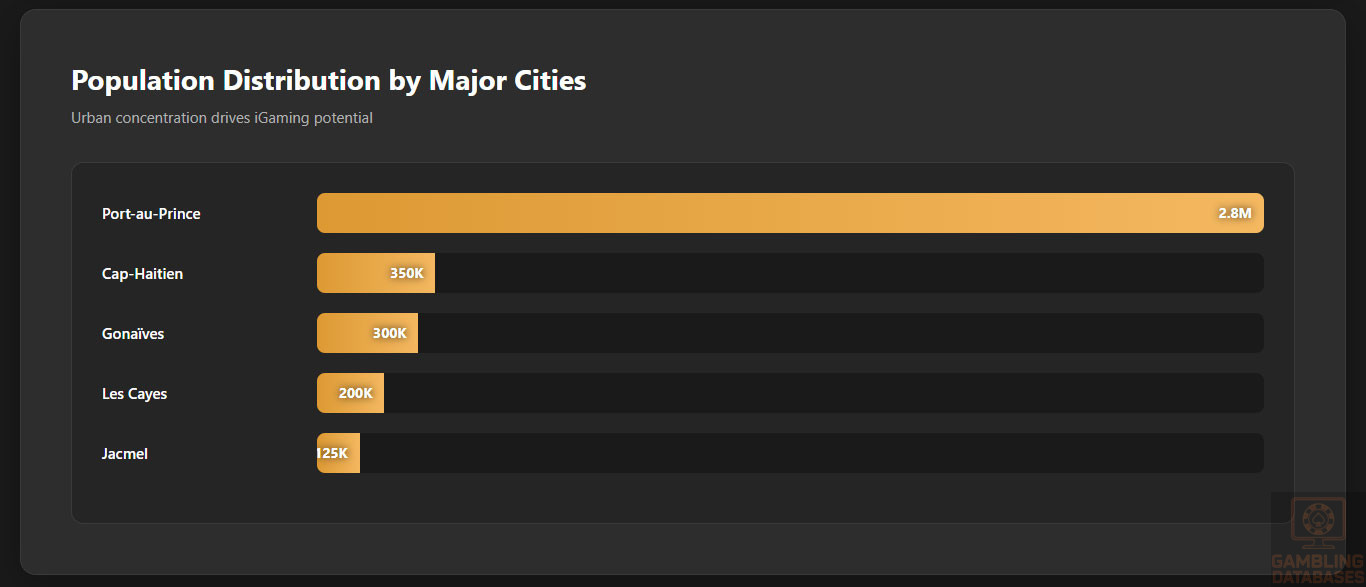

The population is heavily centered in and around Port-au-Prince, the capital and economic hub, which accounts for over 2.8 million residents. Other significant urban centers distributed across the country include Cap-Haitien, Gonaïves, Les Cayes, and Jacmel, which serve as regional commercial and cultural centers.

- Port-au-Prince: Approx. 2.8 million inhabitants

- Cap-Haitien: Approx. 350,000 inhabitants

- Gonaïves: Approx. 300,000 inhabitants

- Les Cayes: Approx. 200,000 inhabitants

- Jacmel: Approx. 125,000 inhabitants

Internet access and gambling venue density are highest in Port-au-Prince and these major cities, where infrastructure and economic activity are concentrated. Rural areas generally lag in internet penetration and digital engagement, posing challenges for nationwide iGaming adoption.

Economic Indicators and Consumer Spending Power

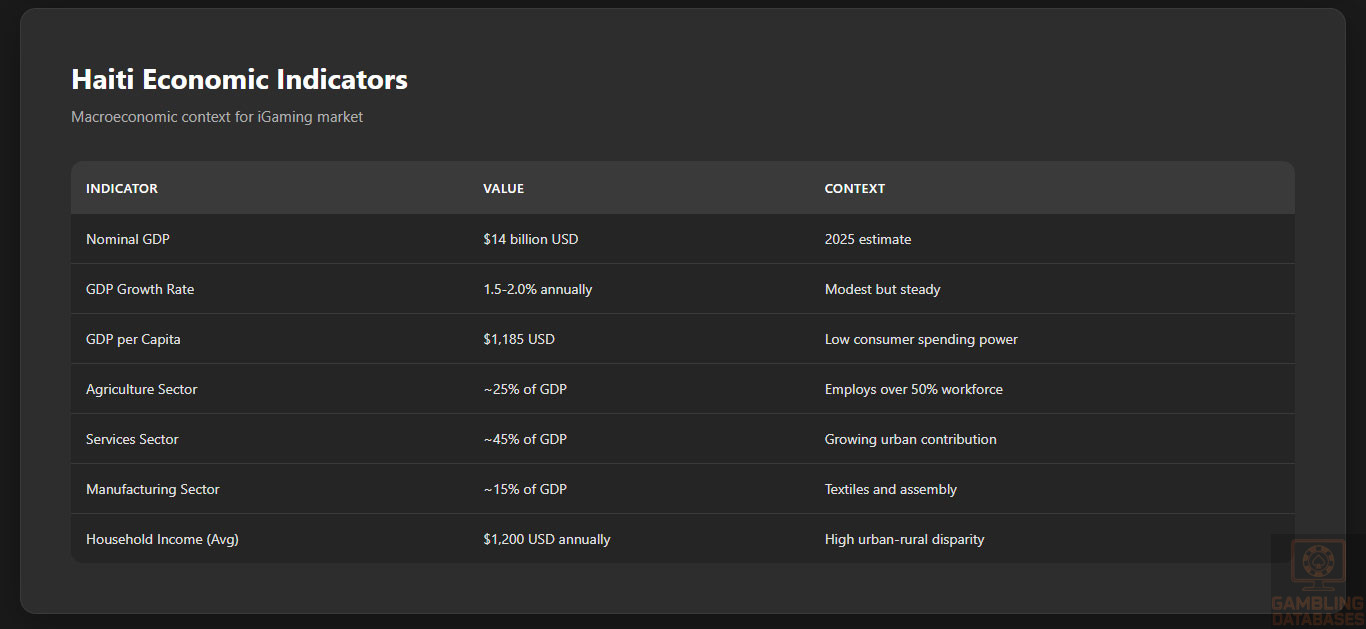

Haiti’s economy is developing slowly, with a nominal GDP close to $14 billion USD in 2025. The country’s GDP growth rate is modest but steady, averaging around 1.5-2% annually. Per capita income remains low at roughly $1,185 USD, reflecting widespread poverty and limited consumer spending capability.

The economic structure is dominated by the agricultural sector, which employs over half of the workforce, followed by textiles/manufacturing and services. Informal economic activities constitute a substantial portion of total economic output, complicating formal market assessments and consumer financial data.

| Indicator | Value |

|---|---|

| Nominal GDP | $14 billion USD |

| GDP Growth Rate | 1.5-2.0% annually |

| GDP per Capita | $1,185 USD |

| Agriculture Sector Contribution | Approximately 25% |

| Services Sector Contribution | Approximately 45% |

| Manufacturing Sector Contribution | Approximately 15% |

Consumer spending is constrained but growing, especially in urban centers. Disposable income levels are low for most, limiting average gambling expenditure, yet informal lottery participation and remittance-driven disposable income help sustain localized gambling activity.

Income and Wealth Distribution

Haiti ranks as one of the most unequal economies globally, with the wealth gap heavily skewed toward the upper urban middle class, which constitutes a small minority. The majority live under challenging financial conditions, with limited access to formal banking and credit systems.

Household income averages approximately $1,200 USD annually, but significant disparities exist between urban and rural areas, with urban households exhibiting better access to services and some discretionary spending power. Consumer spending patterns show a preference for low-cost, accessible gambling products like lotteries, rather than high-stake casino games.

Market Size and Growth Projections

The formal gambling market in Haiti is nascent but growing, driven mainly by land-based casinos and an expanding informal lottery sector. Current revenue streams from licensed operators are modest, with casino equipment market size projected at an estimated $54,850 USD in 2025, forecasted to grow at an 11.39% CAGR through 2030.

Online gambling remains unregulated, but offshore operators tapping Haitian players report steady user base growth aligned with mobile internet adoption. While exact Average Revenue Per User (ARPU) figures are unavailable, the youth demographic and rising smartphone penetration present potential for significant digital market expansion.

| Metric | Value |

|---|---|

| Casino Equipment Market Revenue | $54,850 USD (2025 forecast) |

| Projected CAGR (2025-2030) | 11.39% |

| Informal Lottery Market Share | Dominant, >70% of total gambling volume |

| Online Gambling Revenue | Unreported, growing offshore activity |

| Projected User Base Growth | 7-9% annually (mobile-driven) |

Education, Skills, and Digital Literacy

Haiti struggles with moderate literacy rates estimated at about 61% nationwide, with higher rates in urban areas. School attendance varies widely, and tertiary education enrollment remains low. Digital literacy is emerging but limited, particularly outside major cities.

The workforce generally has basic skills suitable for entry-level service sectors but lacks widespread technical proficiency required for advanced IT or digital industries. Internet and smartphone adoption foster growing familiarity with digital platforms, creating a foundation for increased engagement in online iGaming if regulatory clarity emerges.

Cultural and Social Factors

Communication and Language

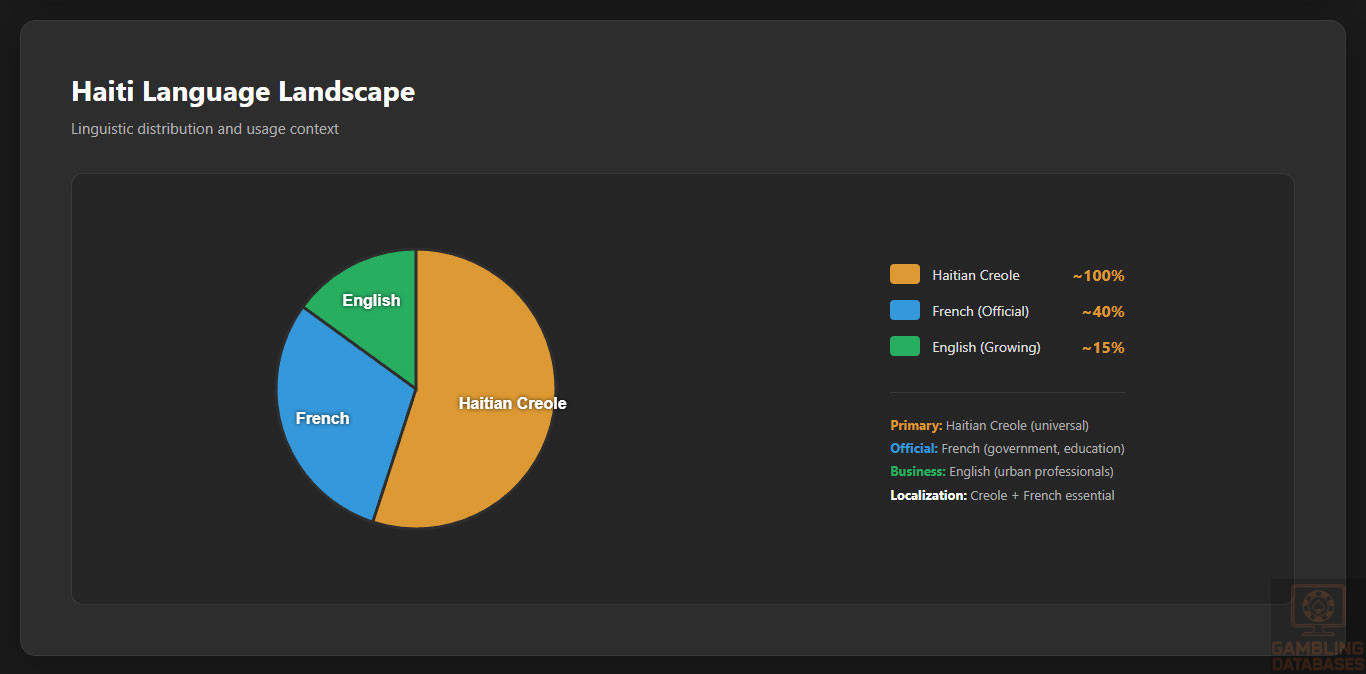

Haiti’s linguistic landscape is bilingual, dominated by Haitian Creole and French as the official languages. French is used in government, education, and formal commerce, while Haitian Creole is universally spoken.

- Haitian Creole: Primary language for majority

- French: Official language, used in formal contexts

- English: Growing among younger urban professionals

- Spanish: Spoken in border regions and some business sectors

- Portuguese: Limited usage among migrant workers

Internet content consumption tends to favor Haitian Creole and French, requiring localization for digital and marketing strategies targeting Haitian audiences.

Cultural Attitudes

Gambling holds an ambiguous cultural status in Haiti. Lotteries and “borlette” games enjoy widespread social acceptance as traditional forms of entertainment and informal income generation.

Religious influences, particularly from the Catholic Church and Protestant denominations, often position gambling as morally questionable, contributing to societal ambivalence toward the sector. Foreign gambling brands face cautious reception, with a preference for localized or culturally sensitive marketing approaches.

Problem Gambling and Social Considerations

Data on problem gambling prevalence is limited, but anecdotal evidence suggests relatively low awareness and support infrastructure for gambling addiction. The informal nature of much gambling activity complicates reliable measurement.

- Minimal government-sponsored problem gambling awareness programs

- Limited availability of counseling and addiction support services

- Low regulatory emphasis on responsible gambling initiatives

- Community and religious groups offer informal support mechanisms

- Emerging NGO interest in social impact related to gambling

Mandatory social responsibility contributions by operators are not established, reflecting the embryonic state of regulatory oversight. This presents risks and opportunities for responsible operators seeking market leadership through consumer trust.

Political Structure and Governance

Haiti operates as a semi-presidential republic with a history of political volatility and governance challenges. Regulatory consistency is affected by periodic governmental transitions and institutional weaknesses.

Despite instability, there is ongoing effort to improve investment climate transparency and regulatory frameworks, supported by international partnerships. These dynamics influence confidence levels for potential iGaming market entrants.

Technology Adoption and Digital Behavior

Internet and Digital Usage

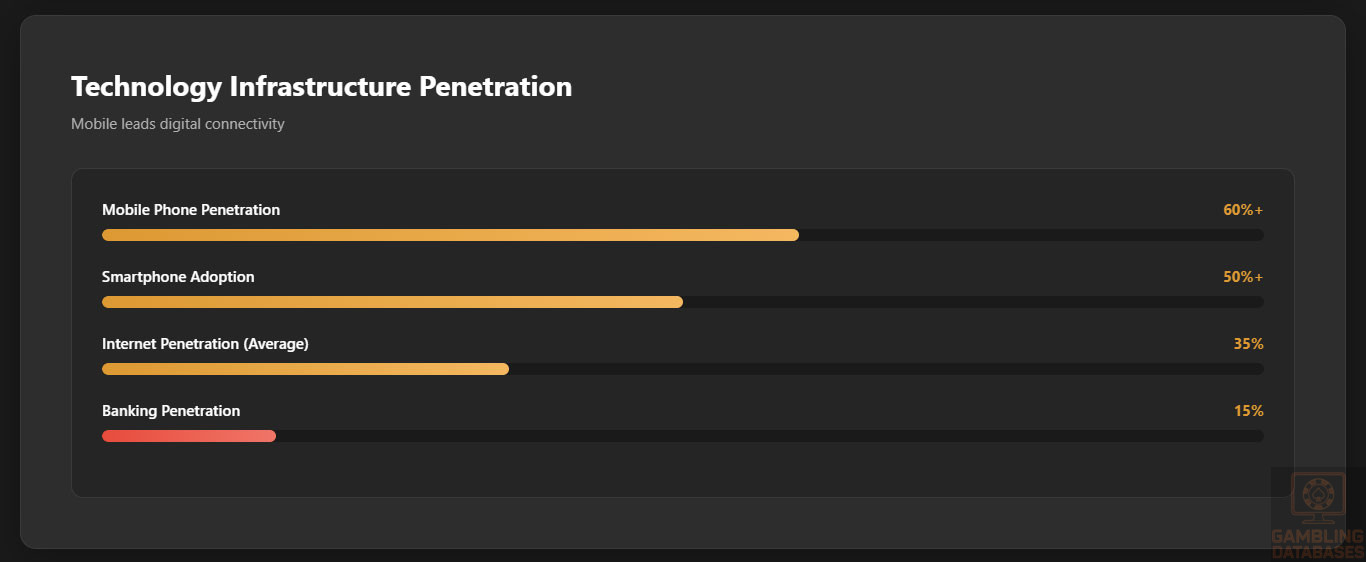

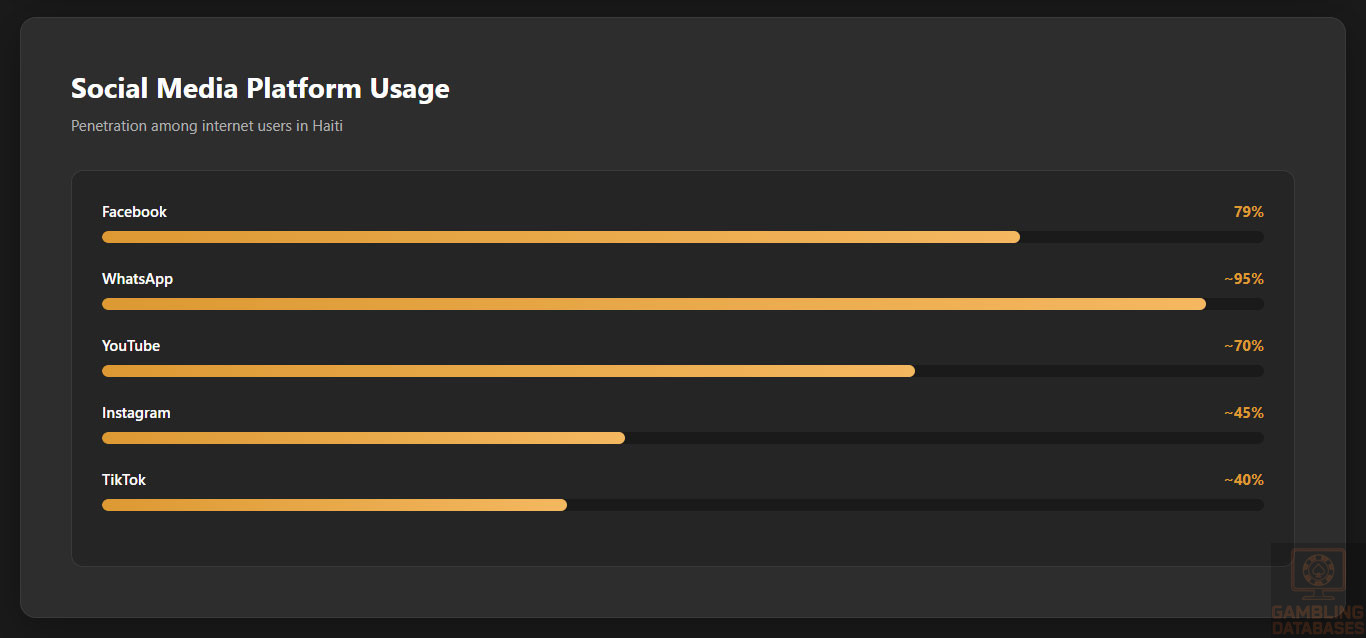

Internet penetration in Haiti is estimated between 30-40%, unevenly distributed, skewed heavily toward urban populations. Mobile phone penetration exceeds 60%, with smartphones increasingly driving connectivity, particularly among younger demographics.

Daily internet usage averages 3-4 hours, heavily dominated by social media, messaging apps, and digital media consumption. Mobile data affordability and network reliability remain significant barriers in rural zones.

- Facebook: 79% penetration among internet users, dominant social network

- YouTube: Widely used for entertainment and information

- WhatsApp: Primary messaging platform with near-universal use

- Instagram: Popular among urban youth and influencers

- TikTok: Rapidly growing user base in under-25 demographic

- Twitter: Used mainly for news and public discourse

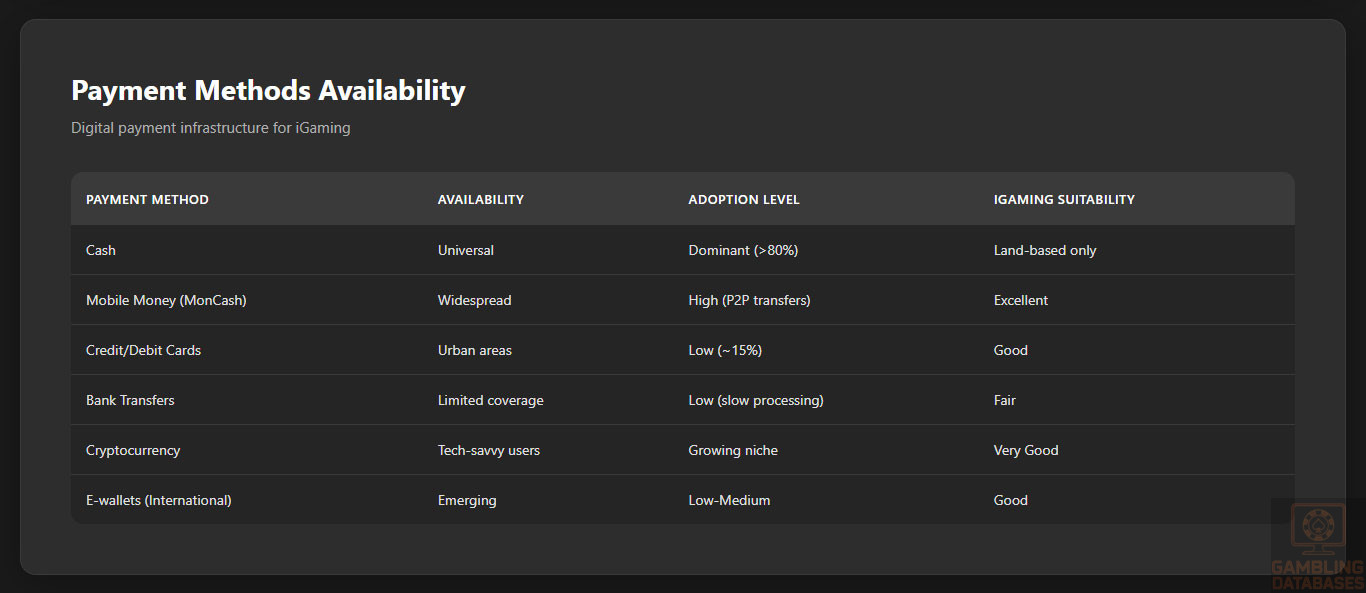

Digital Payment Behavior

Digital payments are growing but still limited by infrastructural and trust issues. Cash remains dominant, but electronic wallets and mobile money solutions gain traction, favored for convenience and accessibility.

- Mobile money platforms (e.g., MonCash) widely used for P2P transfers

- Credit/debit cards accepted primarily in urban retail environments

- Digital wallets growing in e-commerce and gambling transactions

- Bank transfers limited by coverage and speed

- Cryptocurrency adoption rising among tech-savvy users

Gaming and Gambling Preferences

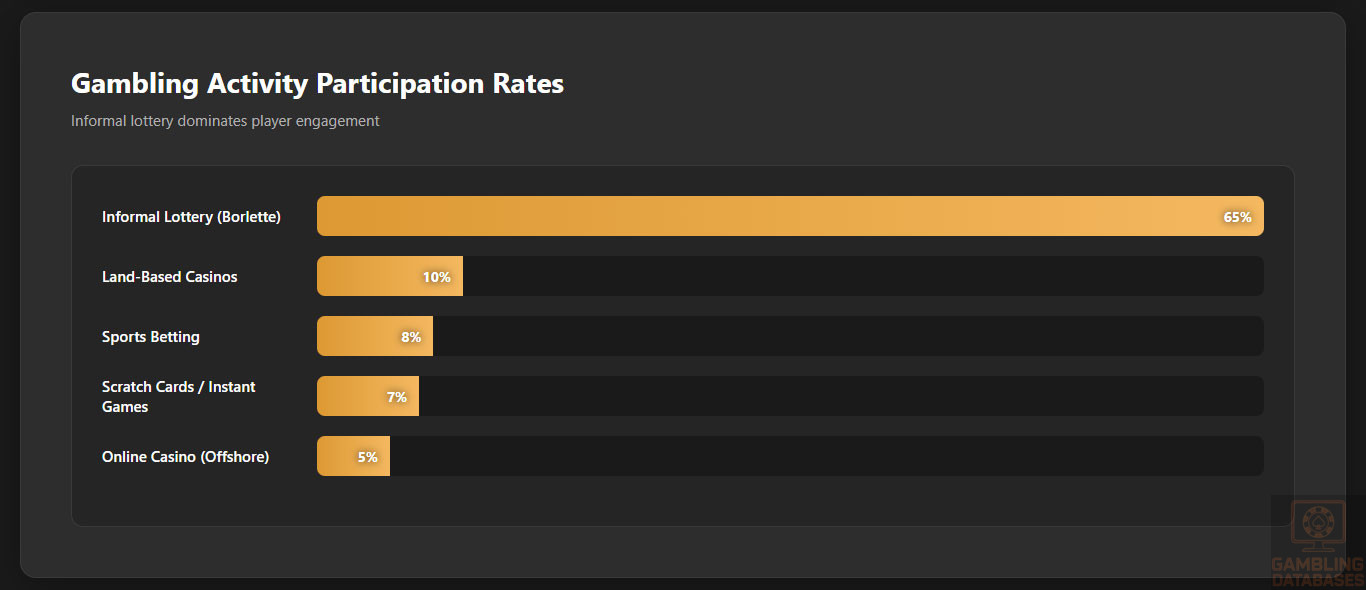

Current Market Participation

Gambling participation is widespread but heavily concentrated in low-entry lottery games popular in both urban and rural areas. Land-based casino attendance remains modest due to limited venue availability and consumer income constraints.

| Rank | Activity | Estimated Participation (%) |

|---|---|---|

| 1 | Informal Lottery (“Borlette”) | 65% |

| 2 | Land-Based Casinos | 10% |

| 3 | Sports Betting (Informal & Online) | 8% |

| 4 | Scratch Cards and Instant Games | 7% |

| 5 | Online Casino Games (Offshore) | 5% |

Consumer Behavior Patterns

Haitian consumers display cautious spending on gambling, focusing on low-cost, frequent betting opportunities like lotteries. Online players accessing offshore platforms tend to prefer mobile-friendly slots and soccer betting, with session durations averaging 20-30 minutes.

Peak gambling times align with evening hours and weekends. Retention rates vary, with strong loyalty to informal local operators but weaker brand attachment to offshore iGaming sites due to limited promotional engagement and support.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Haiti’s internet penetration remains limited, estimated between 30-40%, with broadband access accounting for a small share relative to mobile internet usage. Fixed broadband infrastructure is sparse and concentrated in urban centers, while mobile broadband dominates connectivity in most regions due to lower costs and easier deployment.

Average internet speeds are modest, averaging around 10-12 Mbps download in urban areas, but frequently dropping below 5 Mbps in rural zones. Network reliability is hindered by infrastructural challenges, frequent power outages, and economic constraints affecting investment in high-speed networks.

Telecommunications operators and government initiatives have increased fiber optic coverage in main cities, driving modest improvements in fixed-line broadband availability. However, national broadband development plans face delays due to funding and logistical issues.

5G and Future Technology Deployment

5G deployment in Haiti is in preliminary stages, with no significant commercial coverage as of 2025. Major mobile network operators are evaluating pilot projects but widespread rollouts are unlikely before 2027 due to infrastructure deficits and investment limitations.

The three main mobile operators have signaled intentions to upgrade existing 3G and 4G networks to LTE-Advanced to extend coverage and improve speeds. International partnerships and government encouragement seek to accelerate technology adoption, but adoption remains gradual.

Mobile Technology Ecosystem

Haiti’s mobile network ecosystem comprises several operators competing for market share, with mobile data and voice services forming the backbone of digital communication. Market penetration is approximately 60%, driven by increasing smartphone affordability and mobile money usage.

- Digicel Haiti: Market leader with over 40% share, extensive urban and rural coverage

- Natcom Haiti: Second largest, focusing on urban LTE expansion with 30% market share

- Haiti Telecom: Smaller footprint, with 15% share primarily in metropolitan areas

- Comcel Haiti: Regional operator with localized coverage and 10% share

- Other MVNOs and emerging players: Minor market segments

Smartphone adoption is increasing steadily, now estimated above 50% of mobile users, with Android devices overwhelmingly dominating due to price competitiveness. Device usage favors social media, video streaming, and increasingly mobile gaming applications, laying a foundation supportive of iGaming growth.

Financial Services and Payment Infrastructure

Haiti’s banking sector comprises a mix of domestic and international banks, but overall banking penetration remains low, necessitating reliance on cash and alternative payment systems.

- Capital Bank: Largest market share with expanding digital services

- Unibank: Strong commercial banking presence, growing mobile banking

- Sogebank: Focused on retail banking and SME credit lines

- Banque de l’Union Haitienne (BUH): Regional coverage and retail services

- Haitian American Bank: Niche corporate and remittance banking

Digital payment options are growing with mobile money services such as MonCash widely used for peer-to-peer transfers and bill payments. Card penetration remains low but urban consumers increasingly use credit/debit cards for online and retail transactions.

- Mobile money wallets (MonCash, local alternatives)

- Credit and debit card processing (Visa, Mastercard)

- Bank wire transfers and ACH payments

- Third-party payment gateways supporting e-commerce and iGaming

- Cryptocurrency adoption among tech-savvy demographics

E-commerce and Digital Economy

Haiti’s e-commerce market is nascent but growing, especially in urban centers where digital literacy and payment options are more accessible. Online retail penetration remains below 5%, constrained by infrastructure, trust issues, and limited logistics networks.

Digital services such as mobile financial services, telecommunications, and entertainment are expanding rapidly, contributing to the emergence of a broader digital economy supportive of online gambling platforms.

Business Environment and Regulatory Framework

Haiti ranks low in global ease of doing business indicators, challenged by bureaucratic complexity, regulatory opacity, and infrastructural constraints. Opening a business can be time-consuming due to administrative delays and inconsistent enforcement.

- Prepare corporate documents and approvals including notarization and apostille where applicable

- Register with the Haitian Companies Registry (Registre du Commerce et du Crédit Mobilier)

- Obtain tax identification number and register with the General Directorate of Taxes

- Open a corporate bank account to deposit minimum capital and facilitate transactions

- Secure operational permits and any industry-specific licenses

- Register with social security and labor authorities for employee compliance

Corporate Structure and Registration

Incorporation options include Limited Liability Companies (LLC), Corporations (Société Anonyme), and Branch Offices of foreign companies. LLCs are popular for smaller ventures due to simpler governance, while Corporations suit larger or more complex operations requiring equity sharing.

Foreign investors face no explicit restrictions on ownership, but practical hurdles include navigating local legal frameworks and compliance with tax and labor regulations. Registration timelines average 4-6 weeks, assuming no significant delays.

- Articles of Incorporation and company bylaws notarized and translated if needed

- Proof of registered office address in Haiti

- Passport or national ID copies of directors and shareholders

- Bank reference letters or proof of capital deposit

- Tax registration and social security documentation

Taxation Framework

The corporate income tax rate in Haiti is a flat 10%, with no specific tax holidays for gaming operators. Certain special economic zones provide tax incentives, but these are limited and not gaming-sector focused.

Personal income tax is progressive by brackets, with withholding obligations on salaries and bonuses, alongside mandatory social security contributions. Tax residency rules depend on physical presence and domicile status for individual players and employees.

Market Entry Considerations

Successful entry into Haiti’s iGaming market requires navigating regulatory uncertainty, infrastructural limitations, and cultural nuances. Operators are advised to form local partnerships to mitigate operational challenges and improve market penetration.

- Establish strategic alliances with hotel operators or local gaming venues

- Utilize offshore licensing while preparing for future domestic regulatory developments

- Leverage mobile-first platform design targeting younger demographics

- Incorporate multilingual support focusing on Haitian Creole and French

- Adapt payment processing to include mobile money and cryptocurrency options

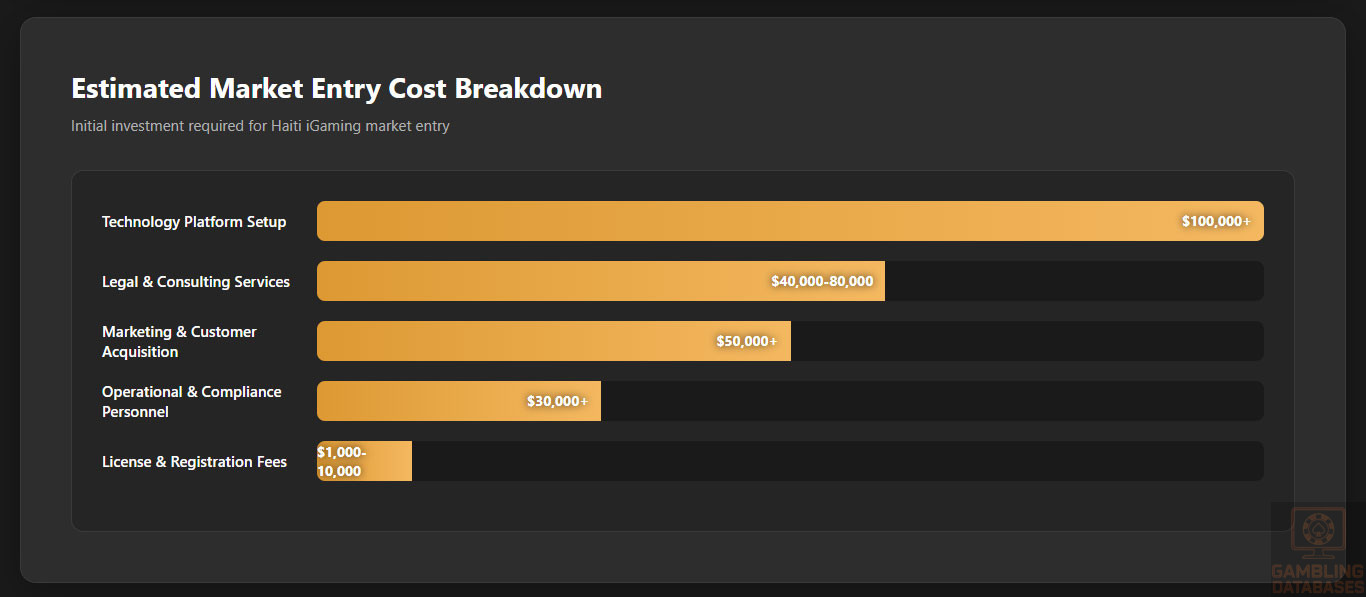

Typical market entry costs include licensing fees, local legal consulting, technology deployment, marketing, and compliance expenditures. Initial set-up investments start around $250,000 USD, but operational expenses and marketing budgets can drive total entry costs higher depending on scale and strategy.

| Cost Category | Estimated Cost (USD) |

|---|---|

| License and Registration Fees | $1,000 – $10,000 |

| Legal and Consulting Services | $40,000 – $80,000 |

| Technology Platform Setup | $100,000+ |

| Marketing and Customer Acquisition | $50,000+ |

| Operational and Compliance Personnel | $30,000+ |

Entry timelines typically span 4-9 months, factoring licensing processing, partner onboarding, platform localization, and marketing launch phases. Exit strategies require understanding of license transferability (limited) and valuation based on market traction and reputational assets.

Success Factors and Challenges

- Strong local partnerships ensuring cultural competency and market access

- Mobile-optimized platforms compensating for internet limitations

- Regulatory agility to adapt to evolving Haitian compliance requirements

- Robust AML and KYC systems to foster trust and regulatory acceptance

- Effective marketing tailored to young, bilingual audiences

- Infrastructure challenges including power reliability and payment limitations

- Political and economic volatility impacting operational stability

- Informal market competition and limited consumer protection frameworks

FAQ: Frequently Asked Questions

1. Is online gambling legal in Haiti?

Online gambling in Haiti currently remains unregulated with no specific licensing or legal framework governing its operation. This means it is neither explicitly legal nor illegal, creating a grey market environment. Haitian players commonly access international offshore gaming platforms that accept residents without domestic licensing, posing risks in terms of consumer protection, payment access, and regulatory compliance.

2. What types of gambling licenses are available and what do they cover?

Haiti offers a limited range of gambling licenses focusing on land-based operations. These include casino licenses for hotels with a minimum of 200 rooms, gaming house licenses for smaller venues restricted to table games, and lottery operator licenses. There are currently no formal licenses for online gambling or remote gaming platforms. Licensing covers operational approval, taxation compliance, and adherence to permitted game types.

3. How much does an iGaming license cost and how long does it take to obtain?

For land-based casino operators, licensing fees are relatively modest, typically around $1,000 annually. However, application processing timelines are opaque and can range from several weeks to a few months, subject to regulatory discretion and completeness of documentation. Online gaming licenses are not available, necessitating offshore licensing for online operators targeting Haitian players.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain land-based gambling licenses in Haiti, provided they adhere to local regulatory requirements including corporate registration, physical presence establishment, and tax obligations. No specific restrictions block foreign ownership; however, navigating local legal frameworks and sustaining compliance is challenging. Formal partnerships with Haitian entities can facilitate market entry and operational success.

5. What are the tax obligations for iGaming operators?

Operators pay a gross gaming revenue tax of 40% on land-based casinos and a flat 10% corporate income tax on net profits. Additionally, operators are responsible for withholding a 5% tax on player winnings paid out. There are annual licensing fees and compliance-related tax obligations, contributing to a significant overall tax burden relative to market size.

| Tax Type | Rate |

|---|---|

| GGR Tax (Casinos) | 40% |

| Corporate Income Tax | 10% |

| Withholding Tax on Player Winnings | 5% |

| Annual License Fee | $1,000 |

6. Are gambling winnings taxed for players?

Players themselves do not pay direct taxes on gambling winnings. The tax obligation is applied at source by operators who withhold a 5% tax on winnings at payout. This ensures simplified compliance for players but increases operational responsibilities of licensed businesses.

7. What are the typical operational costs for running an online casino/sportsbook?

Typical costs include technology platform licensing or development, payment processing fees, marketing and customer acquisition, license and regulatory compliance expenses, and staffing including customer support and compliance personnel. Additional costs arise from localization, legal advisory, and contingency reserves for regulatory risks.

- Technology platform fees and software licensing

- Marketing and customer acquisition

- Payment processing and fraud management

- Legal and regulatory compliance

- Operational staffing and administrative overhead

8. What is the expected ROI timeline for entering this market?

Given the emerging nature and regulatory uncertainty of the Haitian iGaming market, ROI timelines vary widely. A conservative estimate anticipates 18-36 months to break even, depending on scale, market penetration, and operational efficiency. Successful operators often leverage niche targeting and cost-conscious strategies to accelerate returns.

9. What are the local presence requirements for operators?

For land-based operations, a physical presence is mandatory, typically within licensed hotel premises or approved gaming houses. For online operators, no formal domestic license exists, so local presence requirements do not apply; however, establishing local partnerships and contact points can enhance market access and regulatory relations.

10. What payment methods are available and recommended?

Recommended payment methods for Haitian players include mobile money platforms like MonCash, credit and debit cards where accepted, bank transfers mainly in urban hubs, e-wallet services supporting local currency, and increasing adoption of cryptocurrencies. Diversifying payment options is key to overcoming infrastructural and banking limitations.

- Mobile money (MonCash)

- Credit/debit cards (Visa, Mastercard)

- Bank wire transfers

- E-wallets and third-party processors

- Cryptocurrency wallets

11. What are the advertising and marketing restrictions?

Advertising gambling in Haiti must avoid deceptive and misleading content, prohibit targeting minors, and observe any content restrictions outlined by the Lottery regulatory authority. Enforcement is uneven, with self-regulation common among operators. Digital advertising remains largely unregulated but exposed to scrutiny for compliance with general advertising standards.

12. What responsible gambling measures are mandatory?

Currently, Haiti lacks formal mandatory responsible gambling frameworks. Operators are encouraged to implement age verification, basic KYC, and voluntary self-exclusion options, but no legally binding requirements or formal support programs exist. This regulatory gap places emphasis on operator-led social responsibility initiatives.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Haiti is embryonic, with formal revenue limited to land-based casinos generating modest turnover. The informal lottery market dominates player participation. Growth potential is solid given increasing mobile internet access, youth demographics, and expanding digital payments, but hampered by regulatory absence and infrastructure challenges.

14. Who are the main competitors and what is their market share?

The market is dominated in the land-based segment by licensed casinos such as the El Rancho Hotel and Casino. Online, no domestic licensed competitors exist; international offshore operators serve Haitian players. Popular offshore brands include Betswap, Legiano, VerdeCasino, and Metawin, with market shares undefined due to lack of local regulation.

15. What are the player preferences and typical spending patterns?

Players favor informal lottery products and low-stake games accessible with minimal disposable income. Online players prefer mobile-optimized slots and sports betting, especially soccer. Spend per session is moderate, with peak participation during evenings and weekends, reflecting leisure-time gambling culture.

16. What are the key success factors and main challenges for new entrants?

Key success factors encompass forming reliable local partnerships, adapting to multilingual audience needs, leveraging mobile-first technologies, and implementing robust compliance systems. Major challenges include infrastructural deficits, regulatory unpredictability, informal market dominance, and political-economic instability affecting business continuity.

- Strong local relationships and in-market expertise

- Mobile network and platform optimization

- Agile compliance frameworks anticipating regulatory shifts

- Comprehensive payment method integration

- Understanding and respecting cultural sensitivities

- Infrastructure and service quality limitations

- Competition from informal and offshore operators

- Political and regulatory uncertainty

Sources and References

- Haiti Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2025

- Central Bank of Haiti – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines Haiti 2025

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics 2025

- Gaming Industry Report – Global Market Analysis 2024-2025

- iGaming Today – Haiti Gambling Regulation Overview 2025

- Haiti Investment Climate Statement 2025 – U.S. State Department

- SlotEgrator – Gambling Legality and Market Reports 2025

- Betpack – Best Online Casinos Serving Haiti 2025

- Lawzana – Legal Professionals Directory Port-au-Prince 2025

- Advennt – Licensing and Regulation Market Analysis 2024

- Research and Markets – Gambling Market Report 2025

- Statista – Haiti Game Consoles and Digital Forecasts 2025

- Vixio Insights – Gambling Taxation Trends Globally 2025

- Funduaunoir.ca – Tax Rates for Gambling Earnings Guide 2025

- IGaming Express – Global Gambling Regulatory Changes 2025

- LCB.org – Online Casino Laws and Restrictions Haiti 2021-2025

- Bookiessite – Betting Sites Overview in Haiti 2024

- Central American and Caribbean Telecom Reports 2024-2025

- Mobile Network Operators Market Share Reports Haiti 2025

- Local Haitian Banking Institutions Annual Reports 2024-2025

- Global Payment Systems Market in Emerging Economies 2025

- Academic Studies on Haitian Digital Literacy and Economy 2024

- News Articles on Haiti Infrastructure Developments 2024-2025

- Official Tax Authority Publications Haiti 2024-2025

- World Bank Digital Economy Report Haiti 2025

- Country Profile – Haiti – International Monetary Fund 2024

- Reports on Haiti Political Stability and Governance 2024-2025

- Industry Whitepapers on iGaming Market Entry Strategies 2025

🎯 Gambling Databases Country Rating: Haiti

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 3.2/10 | 🔴 Difficult |

| Player Access Score | 4.8/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 4.0/10 | Poor market with severe operational challenges and minimal regulatory framework |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ZERO ONLINE GAMBLING REGULATION: Haiti has NO licensing framework, NO regulatory oversight, and NO consumer protection for online gambling – you’re operating in a complete legal void

- EXTREME TAXATION: 40% GGR tax on casinos + 10% corporate tax + 5% withholding tax creates 50%+ effective tax burden on land-based operations

- INFRASTRUCTURE DISASTER: Only 30-40% internet penetration, frequent power outages, 5-12 Mbps average speeds – your platform will be inaccessible to 60-70% of population

- EXTREME POVERTY: $1,185 USD GDP per capita means your target market has essentially ZERO disposable income for gambling

- POLITICAL INSTABILITY: History of governance challenges and institutional weakness creates unpredictable regulatory environment

- WEAK AML CONTROLS: Country identified as having substandard anti-money laundering frameworks – reputation risk for international operators

- PAYMENT NIGHTMARE: Limited banking penetration, some banks restrict gambling transactions, forcing reliance on cash and informal systems

- INFORMAL MARKET DOMINANCE: 70%+ of gambling activity is informal “borlette” lottery – impossible to compete with untaxed, unregulated local operations

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Land-based casinos legal with basic framework (+1.5). Online gambling COMPLETELY UNREGULATED – no laws, no licenses, no framework (-1.0 for creating legal void and compliance uncertainty). Weak AML controls identified internationally (-0.5). Minimal consumer protection (-0.5). Total: 0.5/3.0 |

| Licensing Process | 25% | 0.75/2.5 | Land-based casino licensing exists but opaque process (+0.5). NO ONLINE GAMBLING LICENSING AVAILABLE – operators must operate without any legal framework (0 points for online). $1,000 annual fee is low (+0.25). However: process lacks transparency (-0.25), requires 200+ room hotel for casino license (-0.25), application process poorly documented (-0.25), 4-6 week registration timeline reasonable (+0.25). Total: 0.75/2.5 |

| Taxation & Costs | 20% | 0.5/2.0 | Started at 0.5 for 40% GGR tax (extreme rate, should be 0 points). Additional 10% corporate tax creates layered taxation (-0.5). 5% withholding tax adds complexity (-0.25). Total effective rate exceeds 50% (-1.0 additional deduction). High entry costs $250k+ (-0.25). Infrastructure costs elevated due to power/internet issues (-0.25). Small market size ($54,850 casino equipment market) makes revenue potential minimal (-0.25). Total: 0.5/2.0 |

| Operational Requirements | 15% | 0.75/1.5 | Physical presence required for land-based (+0.5 for clarity). 200+ room hotel requirement extremely restrictive (-0.25). Payment infrastructure severely limited – banks restrict gambling transactions (-0.25). Power outages disrupt operations (-0.25). Weak institutional capacity for compliance monitoring (-0.25). Must navigate informal market competition (-0.25). Foreign ownership permitted (+0.25). Total: 0.75/1.5 |

| Market Environment | 10% | 0.7/1.0 | Poor business environment – low global ease of doing business ranking (+0.25 for difficult category). Political instability and governance challenges (-0.25). Regulatory opacity and bureaucratic delays (-0.25). Informal economy dominates, creating unfair competition (-0.25). Limited enforcement capacity (-0.1). No advertising restrictions provide some flexibility (+0.3). Total: 0.7/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Land-based casinos and lottery fully legal (+2.0). Online gambling exists in legal gray area – not explicitly legal but not criminally prohibited (+1.0). However: ZERO consumer protection for online players (-0.5). No regulatory oversight means no recourse for disputes (-0.5). Total: 2.0/4.0 |

| Practical Accessibility | 30% | 1.5/3.0 | Some payment methods available – mobile money (MonCash) widely used (+1.0). Some banks restrict gambling transactions (-0.5). Limited credit/debit card penetration (-0.5). Cryptocurrency adoption emerging but limited (+0.25). NO ISP blocking of offshore sites (+0.5). Internet penetration only 30-40% means 60-70% of population cannot access online gambling (-0.75). Infrastructure limitations severely impact accessibility (-0.5). Total: 1.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players using gambling services (+2.0). No enforcement against individual players. Informal lottery participation socially accepted. Total: 2.0/2.0 |

| Market Availability | 10% | 0.3/1.0 | Only ONE major licensed casino (El Rancho) (+0.25). Several offshore operators serve Haiti (Betswap, Legiano, VerdeCasino, Metawin) (+0.25). However: No locally licensed online operators available (0 points for online). Informal lottery dominates 70%+ of market but unregulated (-0.2). Total: 0.3/1.0 |

🔍 Key Highlights

Strengths (Very Limited)

- No ISP Blocking: Unlike many jurisdictions, Haiti does not actively block offshore gambling sites, allowing players theoretical access

- No Player Penalties: Individual players face no legal consequences for gambling activities

- Young Demographics: Median age 24.5 years with 21% aged 15-24 suggests potential tech-savvy audience if infrastructure improves

- Mobile Penetration Over 60%: Higher mobile than internet penetration creates mobile-first opportunity

- Low License Fees: $1,000 annual fee for land-based operations is minimal (though operational barriers remain extreme)

⛔️ CRITICAL RISKS AND CHALLENGES

- [Regulatory Void:] ZERO online gambling regulation means no legal framework, no licensing path, no compliance standards – operators fly completely blind with no legal protection

- [Prohibitive Economics:] 40% GGR tax + 10% corporate tax + 5% withholding = 50%+ effective tax rate makes profitability nearly impossible. Tiny $54,850 casino equipment market demonstrates microscopic formal sector

- [Infrastructure Catastrophe:] 30-40% internet penetration eliminates 60-70% of potential market. Average 5-12 Mbps speeds inadequate for modern gaming. Frequent power outages disrupt operations constantly

- [Extreme Poverty:] $1,185 GDP per capita means target demographic has virtually NO disposable income. This isn’t a “developing market opportunity” – it’s extreme poverty that makes gambling spend unrealistic

- [Payment Chaos:] Limited banking penetration, some banks actively restrict gambling transactions, forcing reliance on cash-based informal systems and emerging mobile money with limited scale

- [Informal Market Dominance:] 70%+ of gambling activity through unregulated “borlette” lottery operations – impossible to compete with untaxed, unlicensed local operations with community trust

- [AML Reputation Risk:] Country identified internationally as having weak anti-money laundering controls – operating here creates compliance and reputation risks for international operators

- [Political Instability:] History of governance challenges and institutional weakness means regulatory environment could change unpredictably or enforcement could suddenly intensify

- [Operational Barriers for Land-Based:] 200+ room hotel requirement for casino license is exceptionally restrictive – eliminates 99% of potential operators

- [Zero Consumer Protection:] No responsible gambling programs, no self-exclusion, no dispute resolution – when things go wrong, players have ZERO recourse

Player-Specific Issues

- No Regulatory Protection: Online gambling unregulated means zero consumer protection, no dispute resolution, no recourse for fraud

- Infrastructure Access: 60-70% of population lacks internet access entirely – online gambling physically inaccessible

- Payment Limitations: Banking restrictions and limited card penetration severely restrict deposit/withdrawal options

- Poverty Constraints: $1,185 annual per capita income means most Haitians cannot afford recreational gambling

- Limited Operator Choices: Only one major licensed land-based casino; online options limited to offshore operators with no local oversight

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $250,000+ USD minimum (legal consulting $40k-80k, technology platform $100k+, marketing $50k+, operational setup $30k+, licenses $1k-10k)

Monthly Operating Costs: $50,000-100,000+ USD (infrastructure workarounds for power/internet, payment processing costs elevated, compliance personnel, customer support, local partnerships)

Effective Tax Rate on Revenue: 50-55% (40% GGR tax + 10% corporate tax on remaining profits + 5% withholding tax obligations)

Customer Acquisition Cost: Estimated $100-300+ USD (high relative to market income levels; informal lottery competition makes conversion extremely difficult)

Accessible Market Size: Potentially only 3-5 million people with internet access, of which perhaps 500,000-1,000,000 have disposable income for gambling

Time to Breakeven: 3-5+ years IF successful (realistically may never break even given market constraints)

Time to Positive ROI: 5-7+ years minimum, assuming survival and scale achievement

Profitability Assessment: Economics are PROHIBITIVE for virtually all operators. The combination of 50%+ effective taxation, $1,185 per capita income (meaning zero spending power), 60-70% of population without internet access, infrastructure failures, dominant informal untaxed competition, and complete regulatory uncertainty makes profitable operation essentially impossible. The formal casino equipment market is projected at only $54,850 USD for 2025 – this microscopic figure demonstrates there is NO real formal market here. Even with perfect execution, you’re competing for scraps in an impoverished market where informal operators dominate.

AVOID UNLESS YOU VIEW THIS AS A LONG-TERM STRATEGIC LOSS LEADER FOR BROADER CARIBBEAN EXPANSION – AND EVEN THEN, QUESTION WHY YOU’RE STARTING HERE.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Online Casino Operators | Medium-High | No legal framework creates uncertainty; no ISP blocking currently but this could change; regulatory void means no legal protection if government decides to act; AML reputation risk from operating in jurisdiction with weak controls |

| Licensed Land-Based Operators | High | 50%+ effective tax rate; restrictive 200+ room hotel requirement; infrastructure failures disrupt operations; political instability could change rules unpredictably; competition from untaxed informal sector |

| Affiliates/Advertisers | Low-Medium | No current enforcement against affiliates; however, regulatory void means situation could change; reputation risk from promoting in unregulated market; payment processing challenges |

| Payment Processors | Medium | Some banks already restrict gambling transactions; weak AML framework creates compliance concerns; informal economy dominates reducing formal payment volumes |

| Company Directors/Executives | Medium | Political instability creates unpredictable environment; weak AML controls could create reputation/compliance issues internationally; no clear legal framework means future enforcement unpredictable |

🚨 Extradition and International Enforcement

Extradition Treaties: Haiti has extradition agreements with the United States and maintains cooperative relationships with international law enforcement. However, gambling-related extradition is not currently a documented enforcement priority.

Enforcement History: No documented cases of international prosecution or extradition specifically related to online gambling operations targeting Haiti. The regulatory void means enforcement precedents don’t exist.

Cross-Border Risk Assessment: Low current risk but unpredictable. The lack of online gambling laws means there’s nothing to violate currently, but this legal void could be filled at any time with retroactive implications unclear.

Travel Risk: Low for gambling-related activities specifically, but Haiti’s political instability creates general operational and safety concerns for international business executives.

📋 Final Verdict

Haiti receives an Operator Ease Score of 3.2/10 and a Player Access Score of 4.8/10, resulting in an overall market attractiveness rating of 4.0/10.

HONEST ASSESSMENT:

Haiti represents one of the LEAST attractive iGaming markets globally. The complete absence of online gambling regulation isn’t an “opportunity” – it’s a legal void that provides zero protection or framework for operators. Combined with extreme poverty ($1,185 GDP per capita), catastrophic infrastructure (only 30-40% internet penetration, frequent power outages, 5-12 Mbps speeds), punitive 50%+ effective taxation, and dominance by untaxed informal lottery operations controlling 70%+ of the market, this market is essentially a guaranteed money-losing proposition.

The formal casino equipment market is projected at a microscopic $54,850 USD for 2025 – this tells you everything about the “opportunity” here. Unless you’re a major international operator viewing Haiti as a strategic loss leader for broader Caribbean presence, or you have a specific corporate social responsibility agenda, there is NO rational business case for market entry.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major Caribbean operator with existing regional infrastructure seeking comprehensive coverage and willing to operate Haiti as a strategic loss leader

- NGO or social enterprise focused on responsible gambling education and harm reduction with philanthropic rather than profit objectives

- Remittance or fintech company exploring gambling as ancillary service to existing payment infrastructure for diaspora community

- Prepared to invest $5M+ over 5-7 years with no expectation of profitability, treating this as market development/brand building

- Willing to operate land-based with 200+ room hotel property and accept 50%+ effective taxation while competing with informal untaxed operators

❌ Definitely Avoid If You Are:

- Any operator seeking profitability within 5 years (economics make this essentially impossible)

- Online-only operator expecting regulatory clarity (there is ZERO framework and unlikely to develop soon)

- Startup or mid-sized operator with capital under $5M (you’ll burn through funds before achieving any scale)

- Operator requiring modern infrastructure (60-70% of population lacks internet access; power outages constant)

- Premium or high-roller focused ($1,185 per capita income means virtually zero high-value players exist)

- Compliance-focused international brand (weak AML controls create reputation risk; regulatory void provides no framework)

- Seeking quick market entry (infrastructure and partnership requirements make rapid deployment impossible)

- Unprepared for informal competition (70%+ of gambling is untaxed local “borlette” – you cannot compete with untaxed operations)

- Risk-averse operator (political instability, regulatory uncertainty, and infrastructure failures create constant operational disruption)

⚠️ BOTTOM LINE: Haiti is a AVOID market for 99% of operators. The combination of extreme poverty, infrastructure catastrophe, regulatory void, punitive taxation, and informal market dominance creates a perfect storm of unprofitability. Unless you have very specific strategic reasons unrelated to profit (regional coverage, CSR agenda, loss leader strategy), your capital is better deployed literally anywhere else in the Caribbean or Latin America.