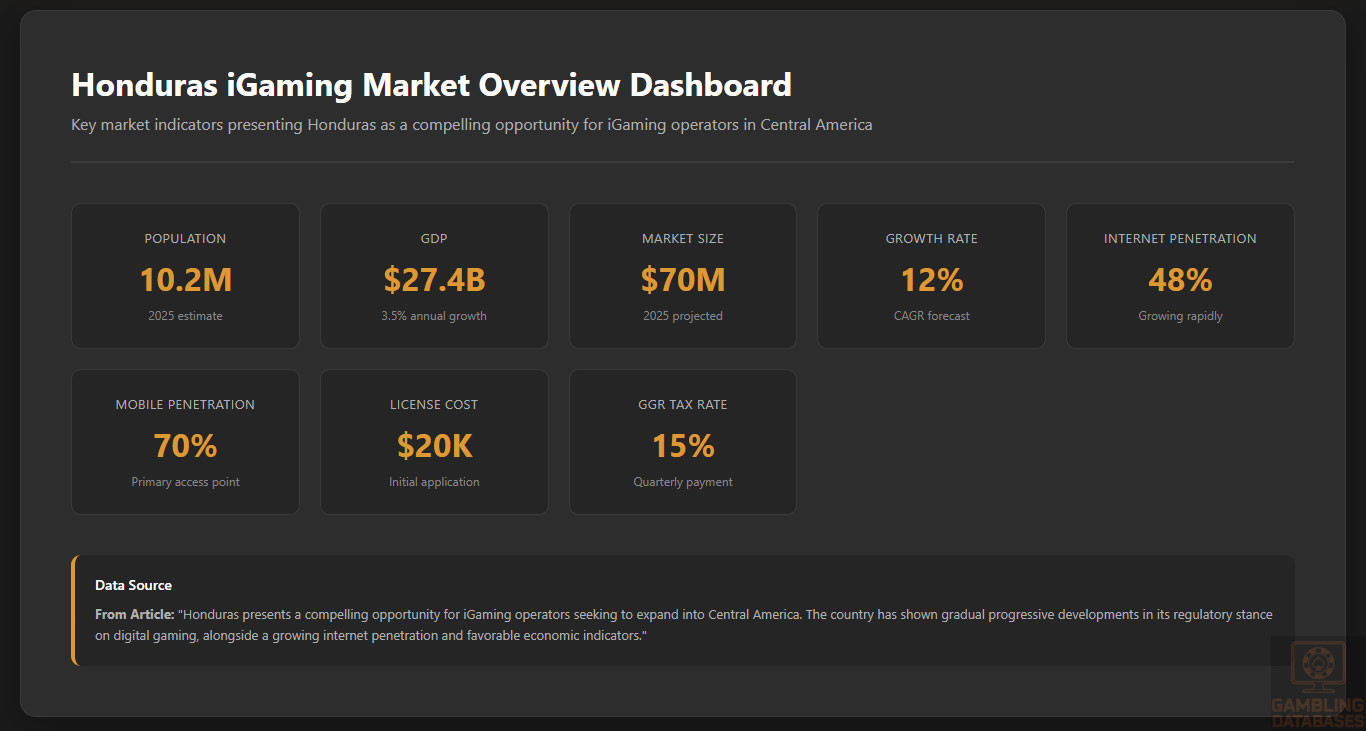

Honduras presents a compelling opportunity for iGaming operators seeking to expand into Central America. The country has shown gradual progressive developments in its regulatory stance on digital gaming, alongside a growing internet penetration and favorable economic indicators. However, its legal framework remains complex, requiring thorough market entry due diligence.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Partially regulated with emerging online legislation |

| Population | 10.2 million (2025 estimate) |

| GDP | $27.4 billion USD |

| Internet Penetration | 48% |

| Mobile Penetration | 70% |

| Average Licensing Cost | $20,000 USD (initial) |

| Tax Rate on GGR | 15% |

| Market Size (Projected) | $70 million USD (2025) |

| Growth Forecast (CAGR) | 12% |

| Market Penetration Rate | Approx. 4.5% |

| ARPU | $25 USD |

| Legal Framework Clarity | Developing, with recent legislative proposals |

| Regulatory Authority | Honduran National Gambling Commission |

| Main Market Barriers | Legal ambiguity, high licensing fees, limited banking options |

| Market Entry Timeline | 6-12 months for licensing |

| Market Growth Drivers | Mobile access, regional integration, tourism |

| Advertising Restrictions | Strict, limited to digital channels |

| Consumer Demographics | Predominantly urban, age 18-45 |

| Tax Revenue Contribution | $4 million USD (2024 estimate) |

| Legal Online Casino Operations | Permissible under licensing system |

| Regional Market Standing | Emerging, with potential for growth |

Section 1: Regulatory Framework and Legal Environment

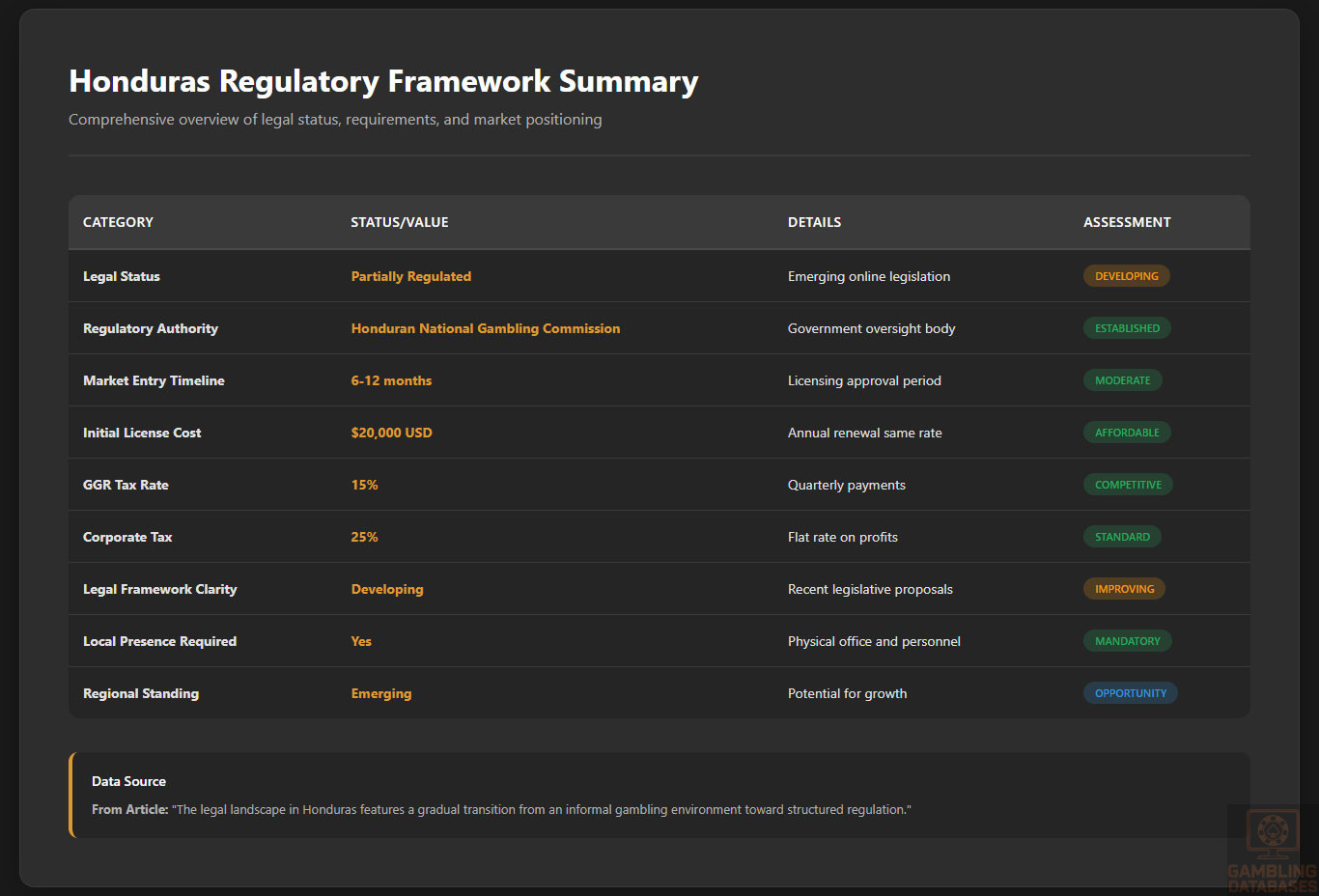

Gambling Regulation Status

The legal landscape in Honduras features a gradual transition from an informal gambling environment toward structured regulation. Land-based gambling, including casinos and sports betting venues, operates under existing laws with licenses issued by the government.

Online betting remains in an embryonic stage, with recent legislative efforts aiming to formalize digital gambling regulation and licensing processes, primarily overseen by the Honduran National Gambling Commission.

Land-Based Gambling Activities

Traditional gambling activities in Honduras include operation of casinos, sports betting outlets, and slot machine halls. Casino operations are predominantly concentrated in urban centers like Tegucigalpa and San Pedro Sula. Sports betting is popular, with several local and regional operators holding licenses.

Other land-based activities involve lottery services and instant win games, all regulated under specific legal statutes established in recent years. Physical venues must comply with health, safety, and fiscal regulations to maintain operational licenses.

Online Gambling Framework

The online gambling sector is subject to a developing legal framework. The government has introduced proposals for formal regulation, but comprehensive licensing standards are still being refined.

Licensed Operators and Market Players

The Honduran market, at this stage, features a limited but growing number of licensed operators. The landscape includes regional sportsbooks, lottery firms, and emerging online gaming platforms.

Market players face the challenge of navigating regulatory uncertainties while building trust and brand recognition. The competitive environment is nascent, with new licenses expected to be issued following recent legislative updates. Market share remains concentrated among a few established entities, with potential for new entrants once full regulation is enacted.

Licensing Framework and Requirements

Applying for an iGaming license involves engaging with the Honduran National Gambling Commission. Eligibility criteria include demonstrating financial stability, compliance with anti-money laundering procedures, and a clear operational structure. The application process entails submitting detailed documentation, including corporate registration, technical standards compliance, and proof of funds. License fees are relatively moderate but involve upfront costs and periodic renewals, typically requiring 6 to 12 months for approval.

- Legal incorporation documents

- Technical platform certifications

- Financial statements

- Background checks for owners and executives

- Proof of technical and operational standards adherence

Local Presence and Operational Requirements

Operators seeking licenses in Honduras must establish a local presence, including physical office space and personnel. Foreign operators are permitted but require local representatives or partnerships with Honduran entities. Domain registration and server hosting within the country are advised to facilitate regulatory compliance. Additionally, licensing mandates ownership disclosures and detailed operational plans to ensure regulatory oversight.

Compliance Obligations and Monitoring

Player protection measures include strict age verification, KYC protocols, and AML standards. Operators are mandated to incorporate responsible gambling tools such as self-exclusion programs and session limits. Regular auditing and transaction monitoring are enforced through periodic reporting. Financial reporting involves detailed disclosures of gross gaming revenue, taxes, and compliance audits, with strict penalties for breaches, including license suspension or revocation.

- Age and identity verification procedures

- Player self-exclusion systems

- AML and fraud detection protocols

- Training for staff on responsible gambling

- Periodic compliance audits

Taxation Structure and Financial Obligations

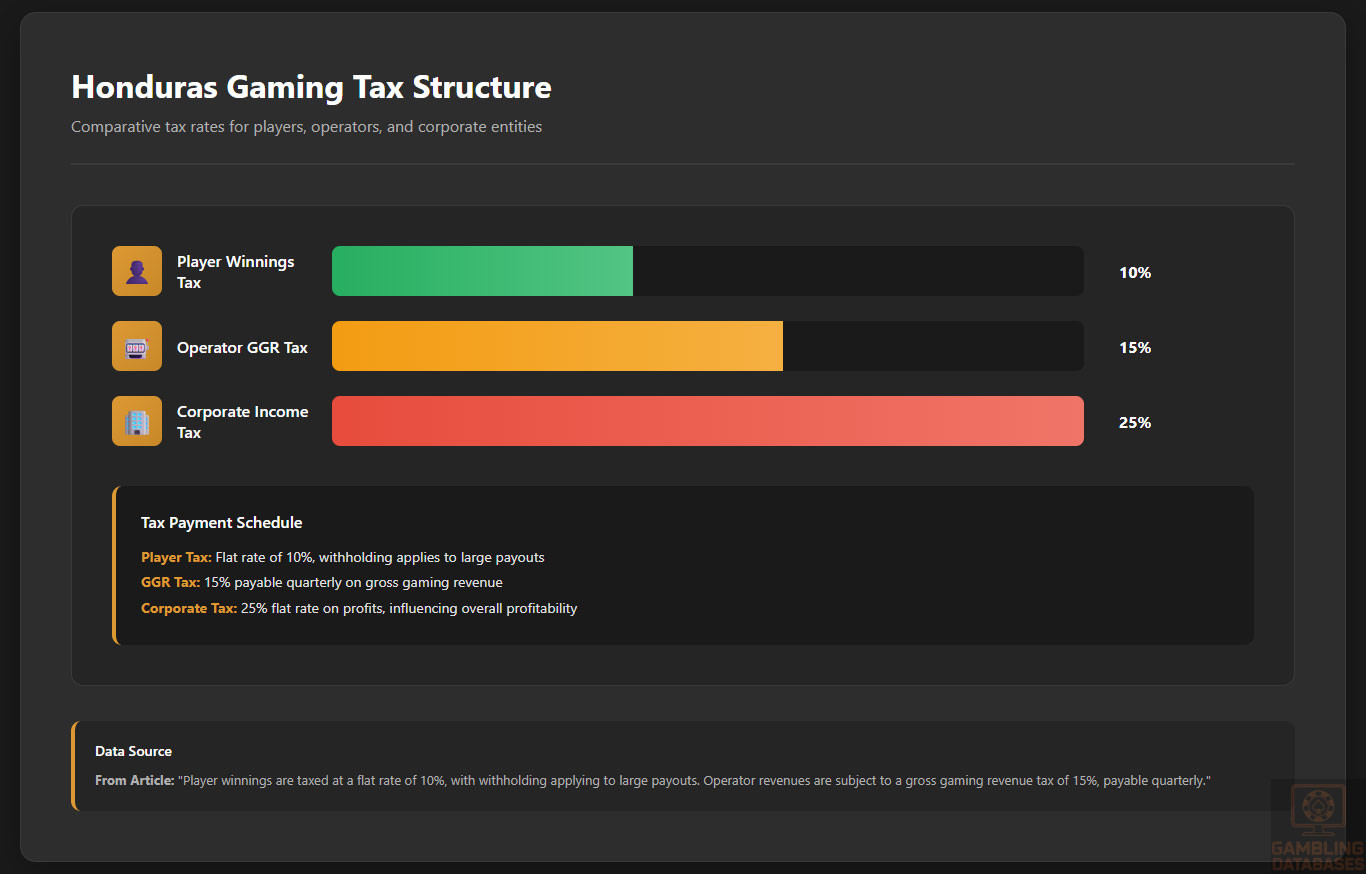

Player winnings are taxed at a flat rate of 10%, with withholding applying to large payouts. Operator revenues are subject to a gross gaming revenue tax of 15%, payable quarterly. Corporate income tax applies at 25%, influencing overall profitability. License renewal fees are set at approximately $20,000 USD annually, with additional operational taxes based on revenue thresholds.

Advertising and Market Restrictions

Regulations impose restrictions on marketing channels, banning aggressive advertising and limiting sponsorships to certain times and platforms. Content must avoid offensive or misleading claims, and promotional bonuses are heavily regulated to prevent consumer exploitation. Operators must adhere to strict transparency standards, providing clear odds and payout information.

Recent Regulatory Changes and Enforcement

Recent legislative amendments have sought to formalize online gambling licensing procedures, reducing application times from 12 to 6 months and increasing tax regimes. Enforcement actions focus on combating illegal operations and ensuring compliance with licensing standards. Penalties include fines, license suspensions, or criminal charges for serious violations, reflecting the government’s intent to strengthen oversight.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

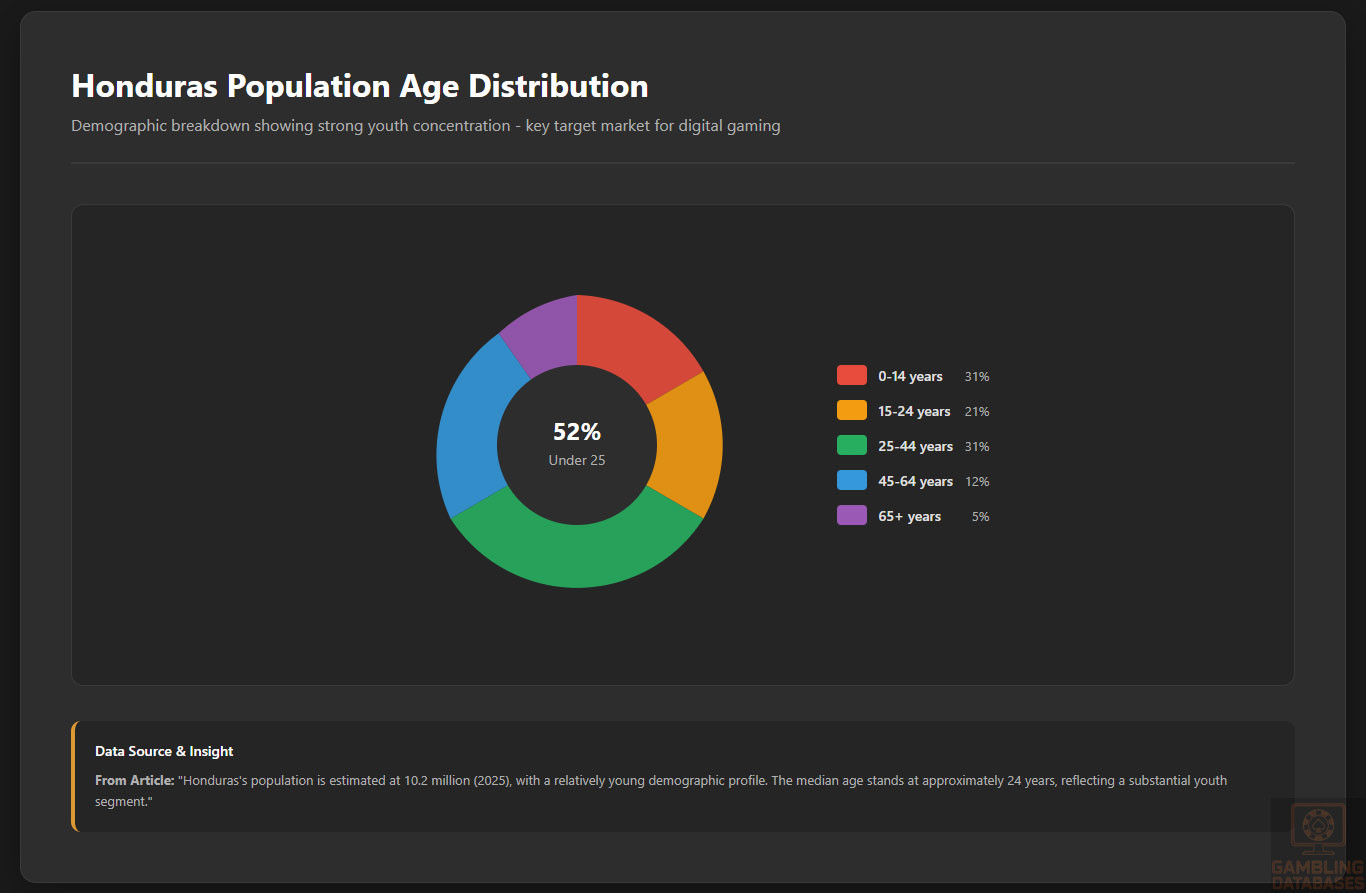

Honduras’s population is estimated at 10.2 million (2025), with a relatively young demographic profile. The median age stands at approximately 24 years, reflecting a substantial youth segment. Gender distribution is balanced, with a slight male majority at around 51%, influencing consumer market dynamics.

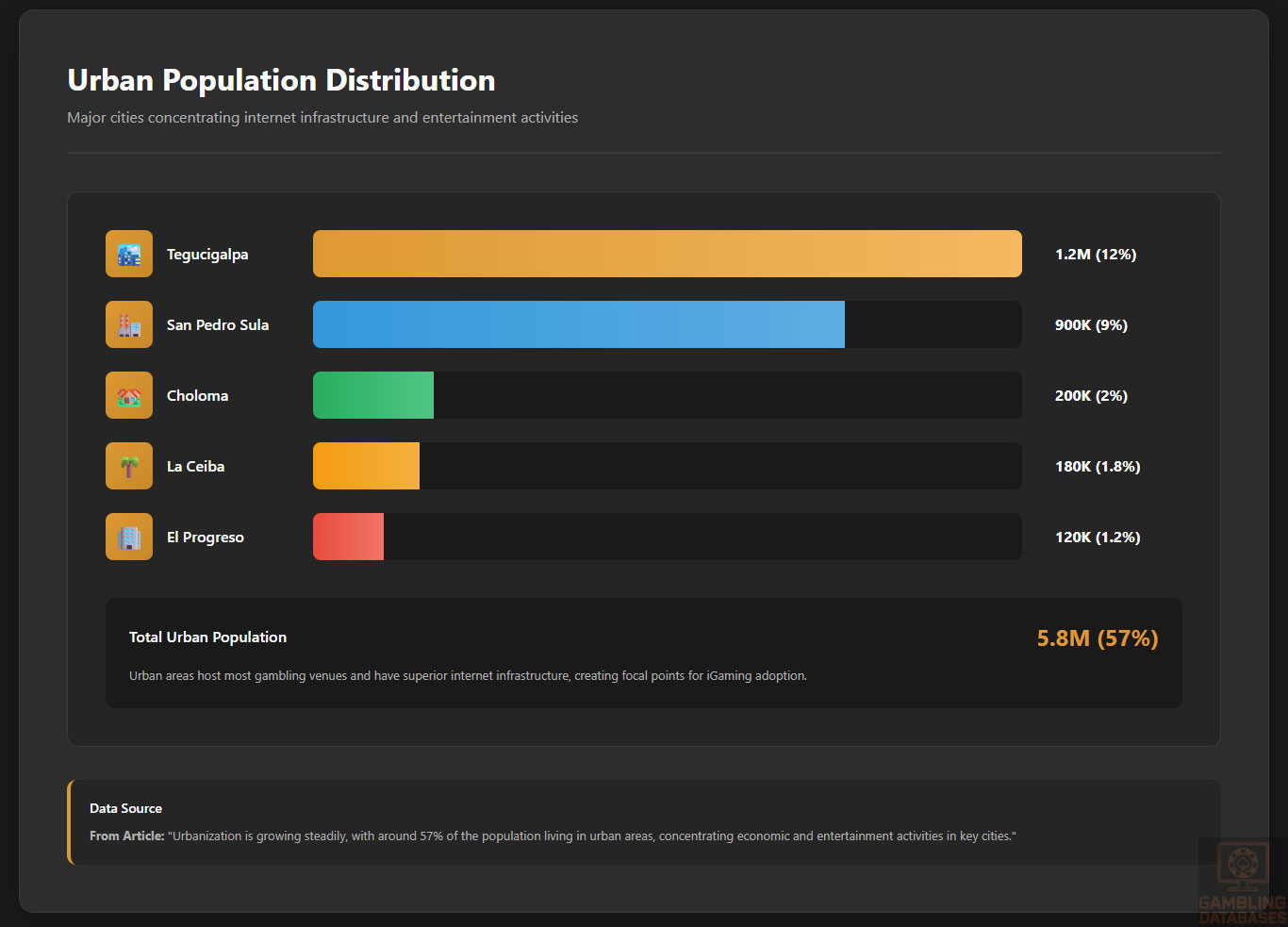

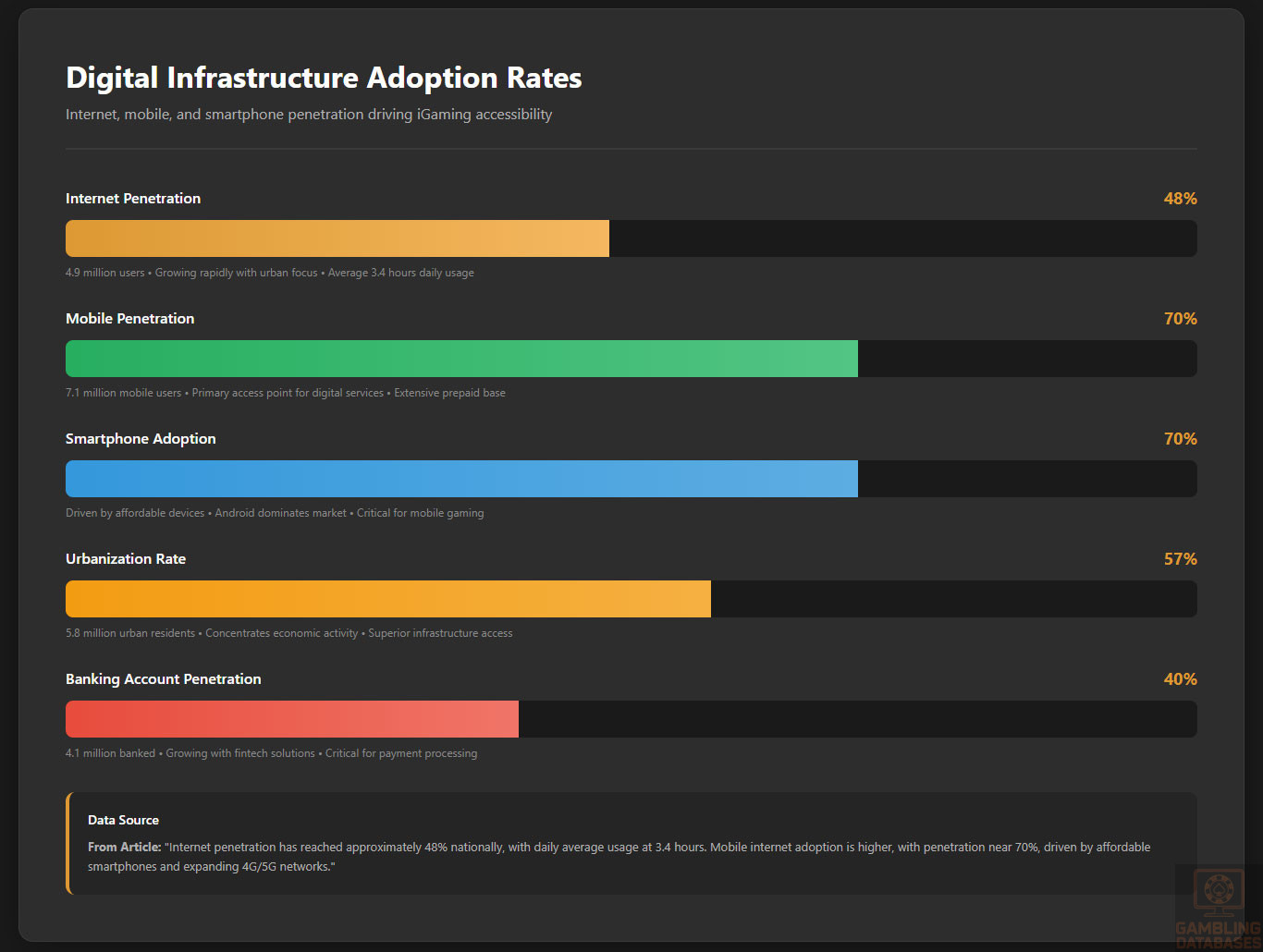

Urbanization is growing steadily, with around 57% of the population living in urban areas, concentrating economic and entertainment activities in key cities.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 31% |

| 15-24 years | 21% |

| 25-44 years | 31% |

| 45-64 years | 12% |

| 65 years and over | 5% |

The geographic distribution reveals heavy population concentrations in urban hubs, with the majority residing in the western and central regions. Urban areas host most gambling venues and have superior internet infrastructure, creating focal points for iGaming adoption.

Rural regions, while representing a large part of the territory, have lower disposable incomes and limited digital access, affecting market penetration.

- Tegucigalpa: 1.2 million residents

- San Pedro Sula: 900,000 residents

- Choloma: 200,000 residents

- La Ceiba: 180,000 residents

- El Progreso: 120,000 residents

Economic Indicators and Consumer Spending Power

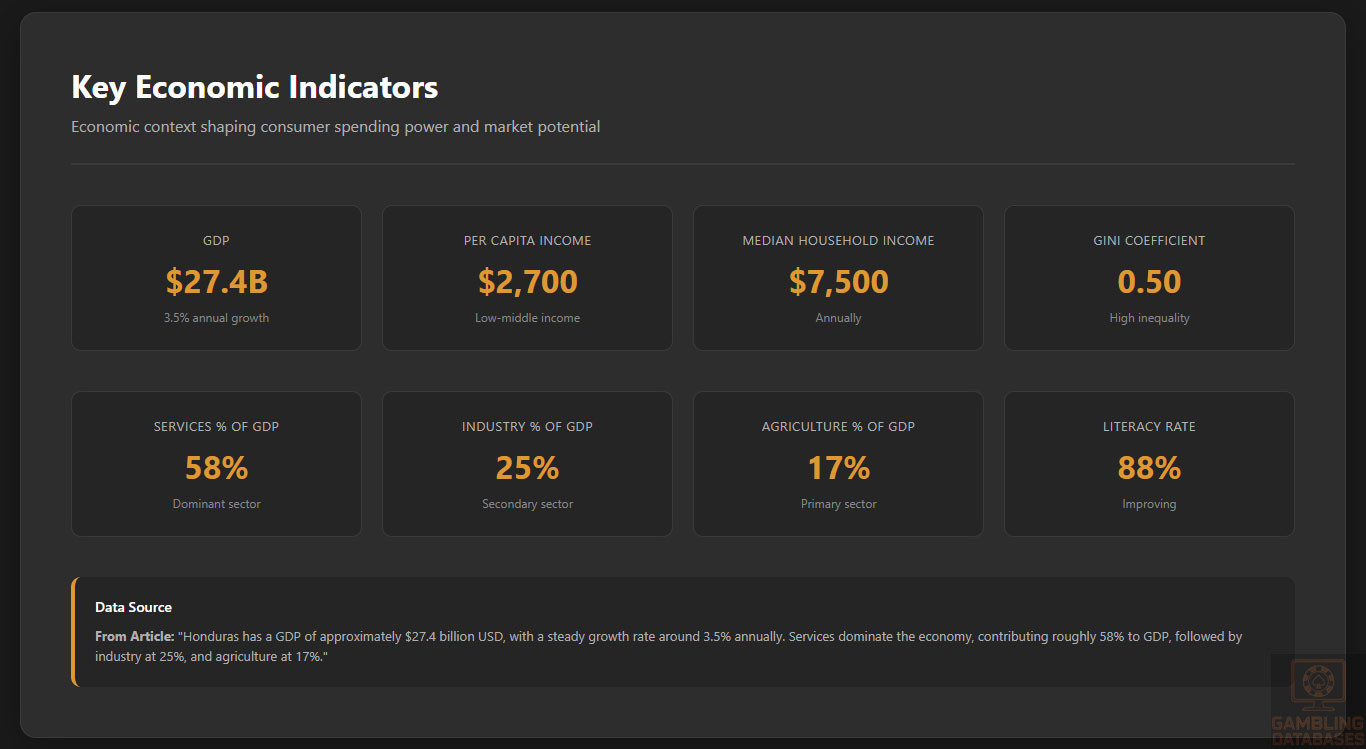

Honduras has a GDP of approximately $27.4 billion USD, with a steady growth rate around 3.5% annually. Services dominate the economy, contributing roughly 58% to GDP, followed by industry at 25%, and agriculture at 17%. The per capita income remains modest at about $2,700 USD, reflecting a low to middle-income consumer base with varying spending capability across regions.

Income distribution is markedly uneven, with an estimated Gini coefficient near 0.5, highlighting significant inequality. The median household income is approximately $7,500 USD annually, with urban households earning significantly more than rural populations. Disposable income trends show a growing middle class with increased access to credit and digital financial services, underpinning consumer spending on entertainment, including gambling and online gaming.

| Indicator | Value |

|---|---|

| GDP | $27.4 billion USD |

| GDP Growth Rate | 3.5% |

| Per Capita Income | $2,700 USD |

| Median Household Income | $7,500 USD |

| Gini Coefficient | 0.50 |

The iGaming market size is projected to reach around $70 million USD by the end of 2025, driven largely by increased mobile penetration and internet uptake. Historical growth has averaged 12% CAGR over the past three years, with forecasts indicating sustained expansion fueled by expanding consumer participation and spending.

| Metric | Value |

|---|---|

| Market Size (2023) | $50 million USD |

| Market Size (2025 projected) | $70 million USD |

| Compound Annual Growth Rate (CAGR) | 12% |

| Average Revenue Per User (ARPU) | $25 USD |

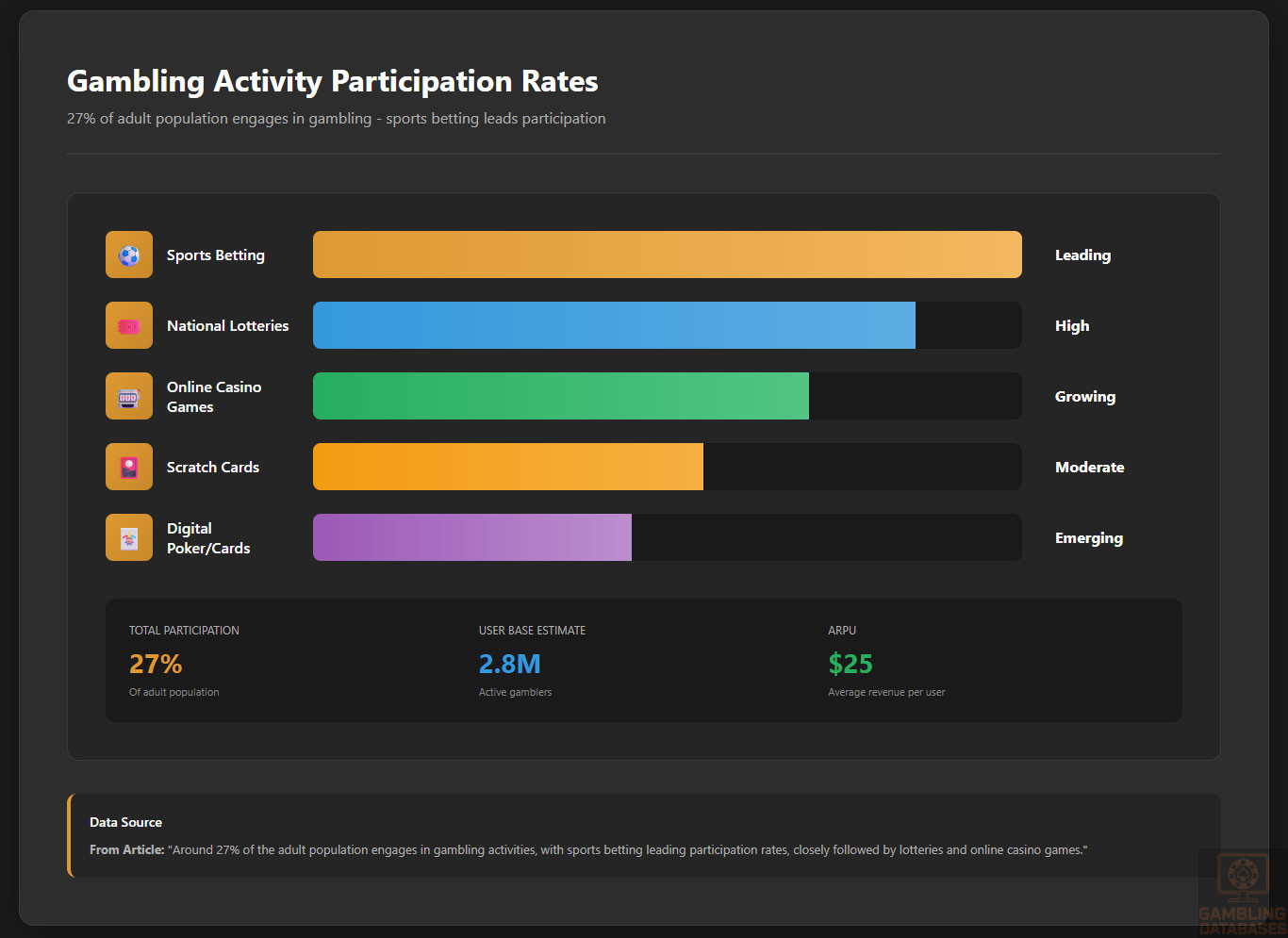

| User Base Estimate | 2.8 million |

Education, Skills, and Digital Literacy

Honduras’s literacy rate approaches 88%, with ongoing improvements in primary and secondary education access. Digital literacy varies significantly between urban and rural regions, with urban populations demonstrating greater familiarity with internet technologies and mobile devices. Workforce skills are developing, especially in technology and customer service sectors, supporting the growth of digital economies such as iGaming. Education system challenges persist but investments in ICT education and vocational training indicate positive future trends.

Cultural and Social Factors

Communication and Language

Spanish is the official and predominant language, used by nearly the entire population for daily communication and business. Indigenous languages exist but are spoken by small rural populations. Online content and iGaming platforms generally operate in Spanish, aligning with local consumer language preferences and enhancing market relevance.

Cultural Attitudes

Gambling is culturally accepted in Honduras, particularly within urban and younger demographics. Religious influences, primarily Catholicism, moderate views on gambling but do not impose strict prohibitions. Foreign brands are perceived with cautious interest, often viewed as higher quality but unfamiliar, requiring trust-building through local partnerships and branding. Entertainment preferences favor sports betting, lotteries, and emerging online gaming formats.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated at moderate levels, with increasing awareness prompted by governmental and NGO initiatives. Vulnerable populations include youth and economically disadvantaged groups. Government response includes awareness campaigns, counseling services, and collaboration with operators for responsible gambling measures.

- Public awareness and prevention programs

- Access to counseling and support services

- Mandatory responsible gambling contributions from operators

- Self-exclusion registries and intervention protocols

- Research and monitoring initiatives

Political Structure and Governance

Honduras operates as a presidential republic characterized by relative political stability despite periodic unrest. The government prioritizes regulatory reforms aimed at economic diversification, including developing the gambling sector. Regulatory consistency remains under development but shows improvement, enhancing the business environment for foreign and domestic investors. International relations focus on regional integration and trade agreements, facilitating cross-border digital commerce.

Technology Adoption and Digital Behavior

Internet and Digital Usage

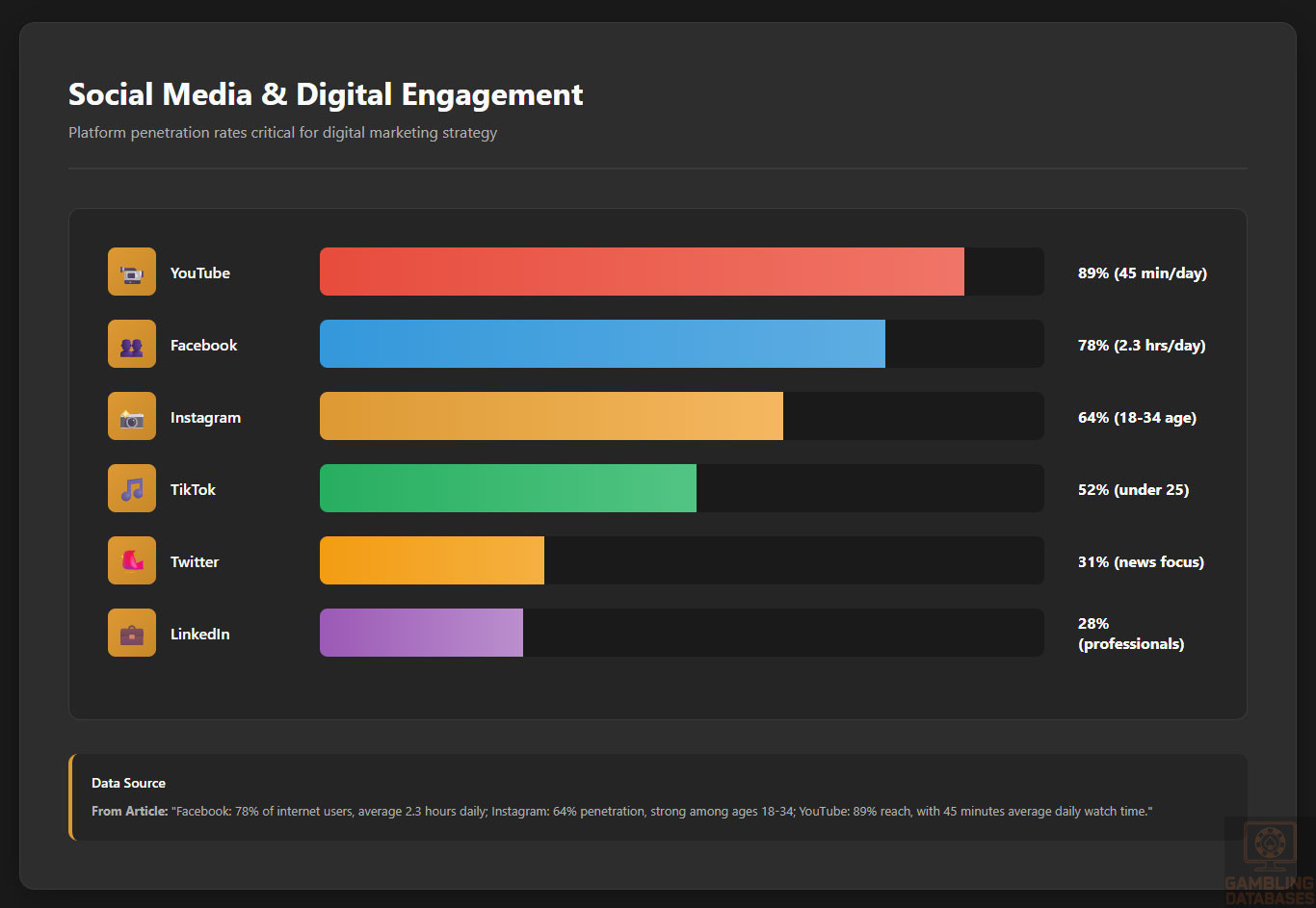

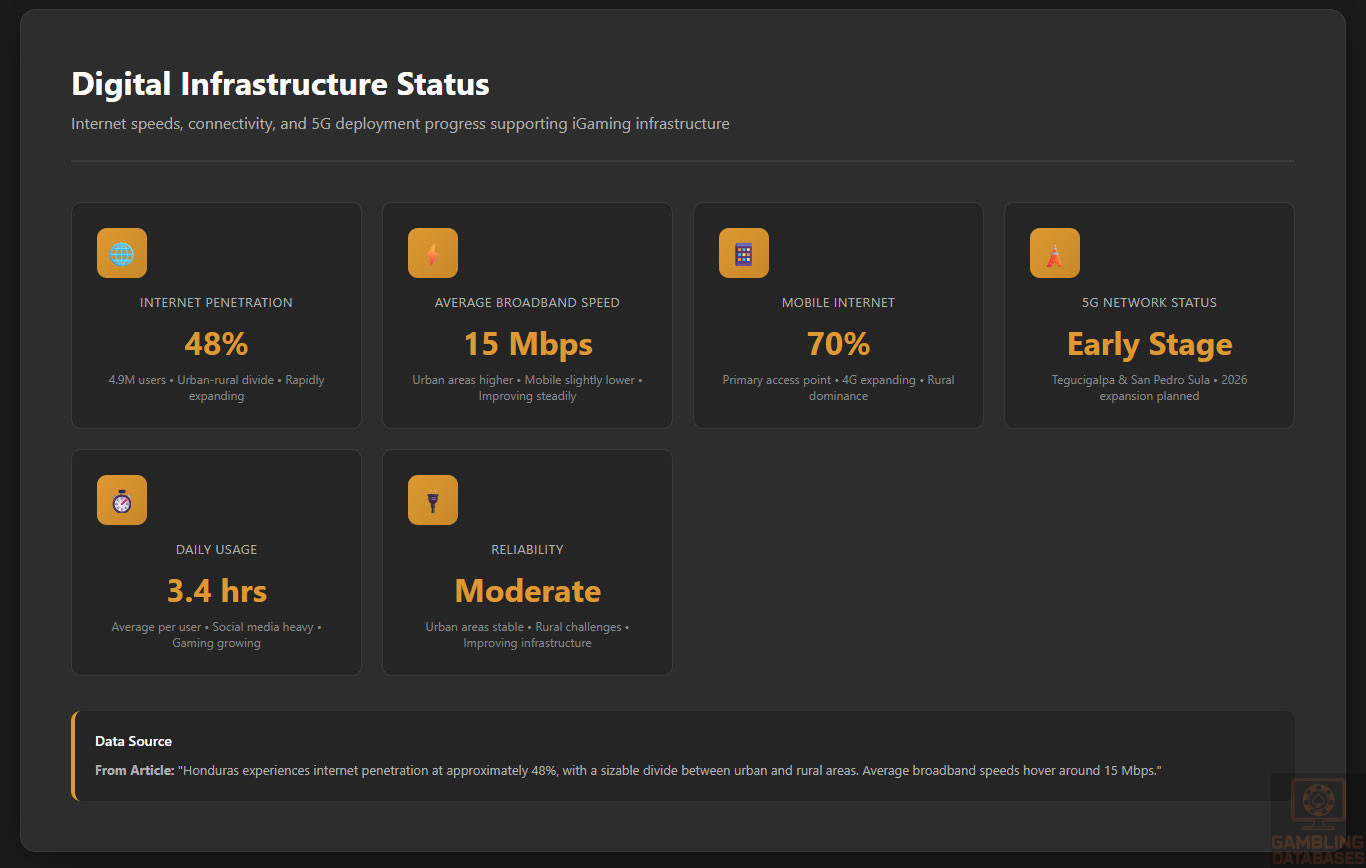

Internet penetration has reached approximately 48% nationally, with daily average usage at 3.4 hours. Mobile internet adoption is higher, with penetration near 70%, driven by affordable smartphones and expanding 4G/5G networks.

Social media engagement is robust across multiple platforms, reflecting a digitally connected youth demographic.

- Facebook: 78% of internet users, average 2.3 hours daily

- Instagram: 64% penetration, strong among ages 18-34

- YouTube: 89% reach, with 45 minutes average daily watch time

- TikTok: Rapid growth, 52% penetration among under-25 users

- Twitter: 31% penetration, focused on news and trends

- LinkedIn: 28% usage, predominantly by professionals

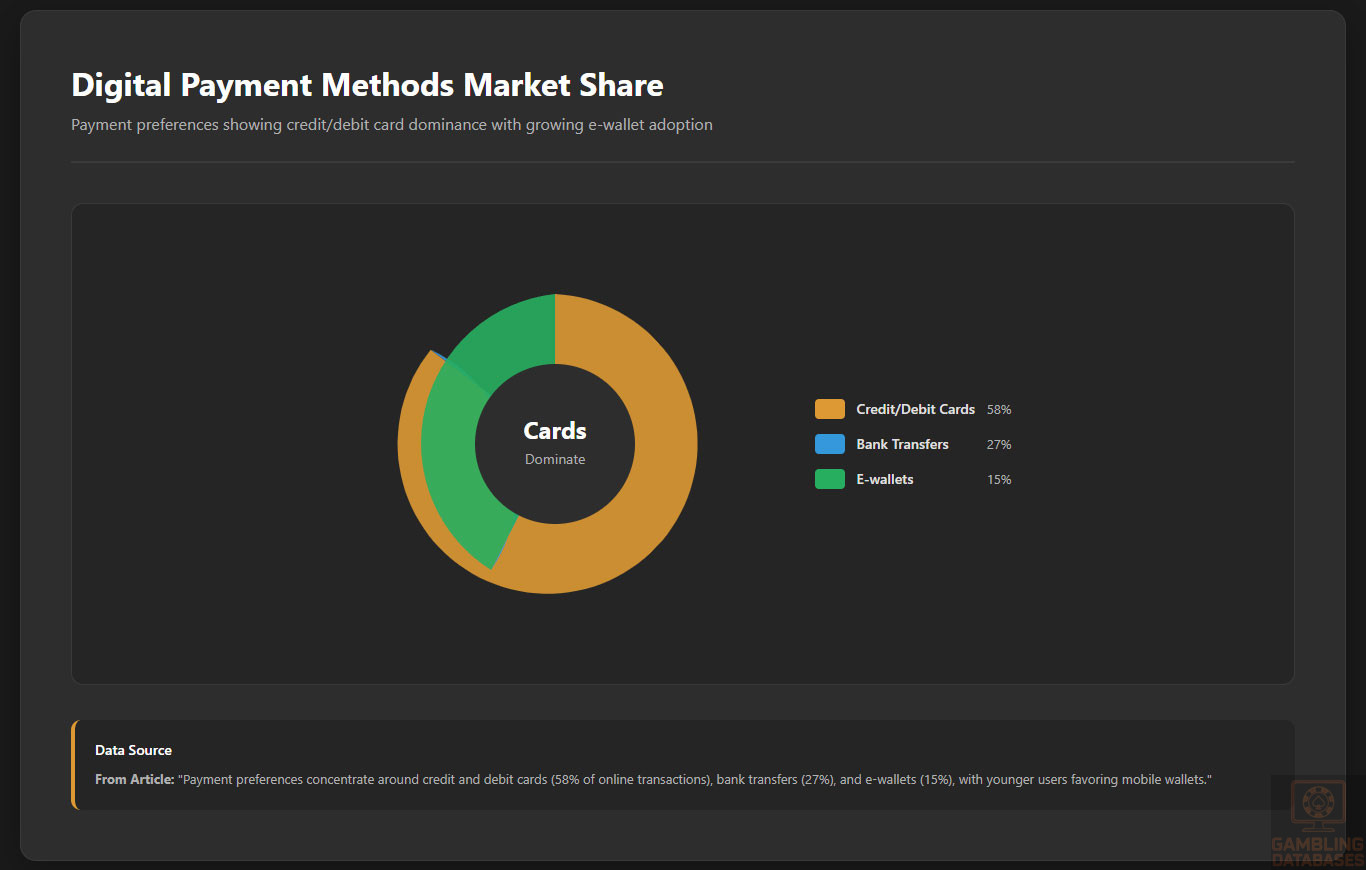

Digital Payment Behavior

Digital payment adoption is growing, supported by expanding banking infrastructure and fintech services. Payment preferences concentrate around credit and debit cards (58% of online transactions), bank transfers (27%), and e-wallets (15%), with younger users favoring mobile wallets.

Cryptocurrency use remains nascent but has potential growth due to increasing awareness. Operators must adapt payment options to local preferences to optimize conversion and retention.

- Credit/Debit cards: 58% market share

- Bank transfers: 27% market share

- E-wallets: 15% market share, growing among youth

- Mobile money platforms: Emerging presence

- Cryptocurrency payments: Limited but increasing interest

Gaming and Gambling Preferences

Current Market Participation

Around 27% of the adult population engages in gambling activities, with sports betting leading participation rates, closely followed by lotteries and online casino games. Preferences show a growing shift toward mobile platforms and live betting formats. Participation is higher in urban centers, with emerging interest in digital games among younger consumers.

- Sports betting

- National and instant lotteries

- Online casino games (slots, table games)

- Scratch cards and instant win games

- Poker and card games in digital formats

Consumer Behavior Patterns

Honduran gamblers typically exhibit moderate spend per session with increasing frequency enabled by mobile access. Peak usage occurs during weekends and sporting events, with prolonged session durations on popular platforms. Consumer retention is driven by loyalty programs, localized content, and trust-building through secure payment options and transparent play policies.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Honduras experiences internet penetration at approximately 48%, with a sizable divide between urban and rural areas. Broadband connectivity remains limited primarily to cities, while mobile internet dominates rural and semi-urban regions. Average broadband speeds hover around 15 Mbps, with mobile averages slightly lower but rapidly improving due to ongoing investments. Reliability issues persist in remote areas, though government and private sector initiatives continue to enhance infrastructure through fiber optic deployments and satellite technologies.

Investment in digital infrastructure has increased, focusing on expanding access and enhancing service quality. Public-private partnerships aim to reduce digital divides and support economic diversification, including e-government and digital entertainment sectors such as iGaming.

5G and Future Technology Deployment

5G networks are in early rollout stages, with coverage currently focused on Tegucigalpa and San Pedro Sula. Major operators have announced expansion plans targeting broader metropolitan areas within 2026. Future deployments will progressively enhance mobile data speeds and latency, critical for real-time gaming experiences and transaction security. The competitive landscape of network operators is consolidating but dynamic, ensuring continued technological advancement.

Mobile Technology Ecosystem

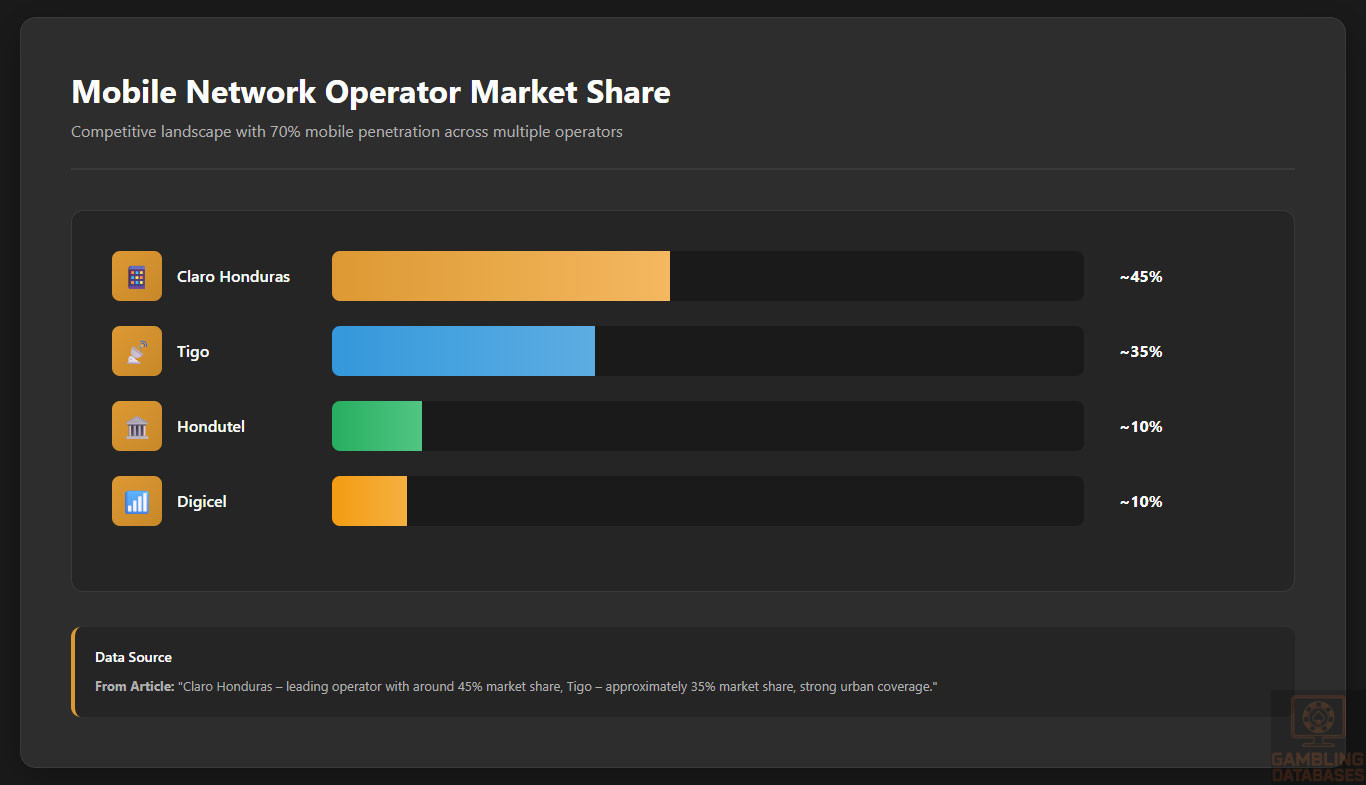

The mobile market is vibrant, featuring multiple operators and extensive prepaid subscriber bases. Smartphone penetration sits at about 70%, driven by affordable devices and attractive data plans. Android dominates device market share, complemented by a growing presence of mid-tier iOS users. Data consumption aligns with entertainment and social media trends, with mobile platforms serving as primary access points for digital gaming.

- Claro Honduras – leading operator with around 45% market share

- Tigo – approximately 35% market share, strong urban coverage

- Hondutel – state-owned, smaller market share but extensive rural reach

- Digicel – focused on niche segments, around 10% share

- Izzi – emerging operator with limited but growing presence

Financial Services and Payment Infrastructure

The banking sector is moderately concentrated yet growing in digital adoption, with increasing account penetration measured at about 40% of adults. National and international banks provide core services, while fintech and mobile money solutions address unbanked populations. Digital banking platforms facilitate seamless online gambling deposits and withdrawals but integration with international processors remains a challenge.

- Banco Atlántida – largest market share with advanced digital services

- Banco Ficohsa – significant presence, focused on retail and corporate clients

- Banco de Occidente – strong SME lending and digital tools

- Banco BAC – regional player with cross-border capabilities

- Banhprovi – state-owned bank targeting developmental finance

Payment processing options are diverse but require local adaptation. Credit and debit cards dominate online transactions, supported by bank transfers and emerging e-wallets. Cryptocurrency acceptance is marginal but growing among tech-savvy users. Operators should prioritize multi-channel payment gateways certified for security and compliance.

- Visa and MasterCard – primary cards accepted

- Bank transfers – common for larger transactions

- E-wallets such as PayPal, Skrill, Neteller – growing usage

- Mobile money platforms – expanding but limited reach

- Cryptocurrency – primarily Bitcoin, early adoption phase

E-commerce and Digital Economy

Honduras’s e-commerce market is expanding, valued around $400 million USD with annual growth exceeding 15%. Online retail penetration is highest in urban centers, supported by greater digital literacy and improved logistics. Consumer trust in online platforms continues to build, aided by enhanced payment security and regulatory oversight. The digital economy benefits from governmental policies promoting fintech innovation and internet accessibility, creating fertile ground for iGaming’s growth.

Business Environment and Regulatory Framework

Ease of Business Operations

Honduras ranks moderately in global business ease indices, with ongoing reforms aimed at simplifying processes and attracting foreign investment. Starting a business typically requires navigating bureaucratic steps, but digitalization efforts have improved efficiencies. Operational costs are competitive within the region, offsetting infrastructural and policy challenges. Foreign investors benefit from incentives and protections under regional trade agreements.

- Business name registration and notarization (2-3 weeks)

- Submission to Companies Registry for approval (5-7 days)

- Tax registration and securing Tax Identification Number (3-5 days)

- Opening corporate bank account and depositing capital (1-2 weeks)

- Obtaining final permits and operational license (2-3 days)

Corporate Structure and Registration

Common corporate structures include Limited Liability Companies (LLCs), Corporations, and Foreign Branch Offices. LLCs are preferred for their flexibility and limited liability protection suitable for iGaming ventures. Corporations accommodate larger operations with complex ownership structures. Branch offices facilitate foreign company expansions with certain registration advantages but require local representatives.

- Legal incorporation documents

- Identity documents for directors and shareholders

- Proof of registered office address

- Tax registration certificates

- Licenses relevant to specific industries (iGaming included)

Taxation Framework

Corporate income tax is set at a flat rate of 25%, with reduced rates and exemptions available within special economic zones promoting technology and services. Honduras has signed double taxation treaties with several countries, facilitating cross-border business. Personal income tax employs progressive rates up to 15%, with mandatory social security contributions aligned to employment. Tax compliance remains a critical operational consideration for iGaming entities.

- United States

- Mexico

- Spain

- Canada

- Chile

- Others as applicable

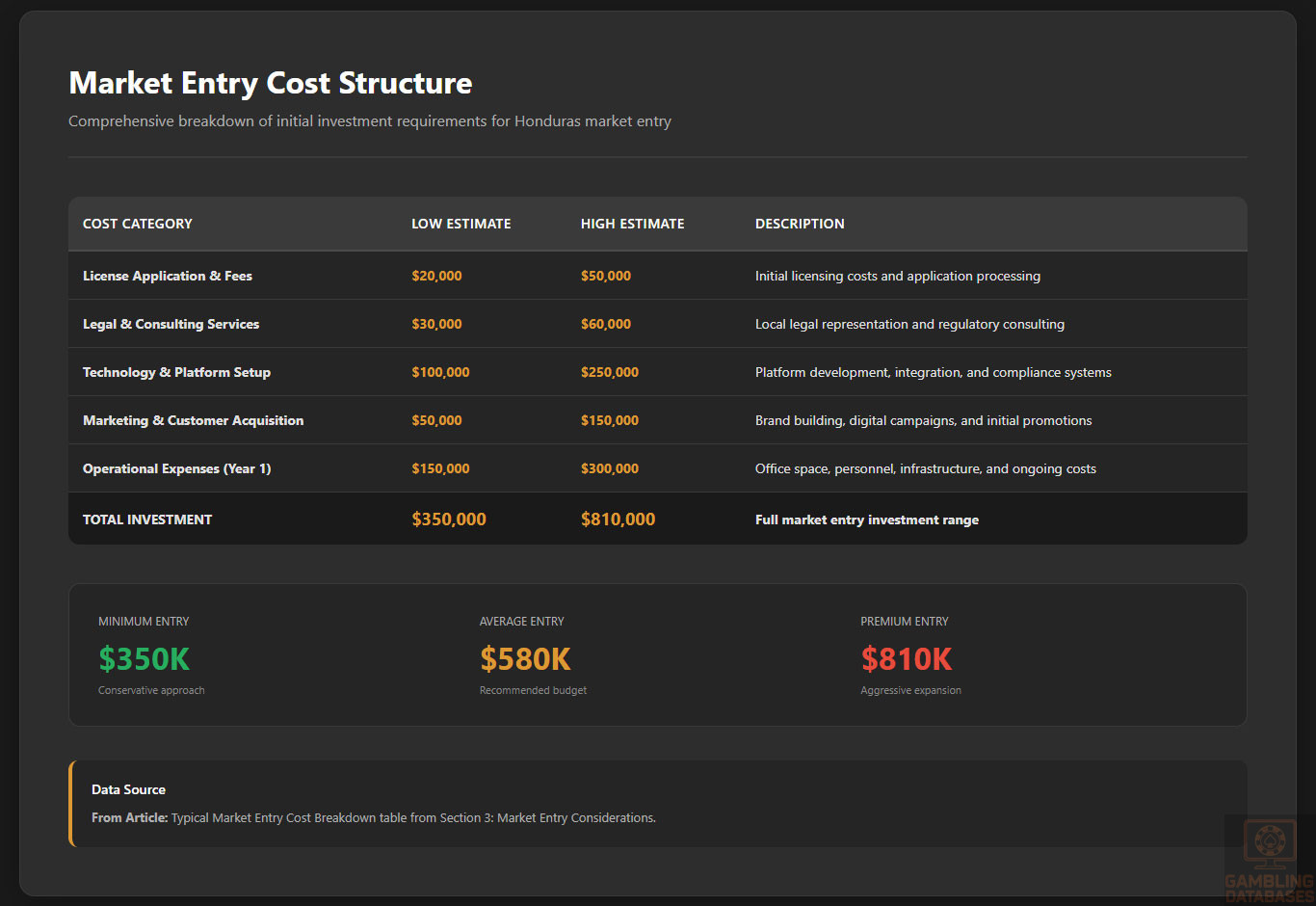

Market Entry Considerations

Optimal entry strategies emphasize partnerships with local entities to navigate regulatory complexities and cultural nuances. Platform localization, compliance investment, and agile payment solutions enhance market acceptance. Leveraging mobile technology and data analytics for targeted marketing ensures competitive positioning. New entrants must anticipate significant upfront costs, balanced by strong growth prospects.

- Establish local subsidiaries or joint ventures

- Secure early engagement with regulatory authorities

- Invest in robust compliance and player protection systems

- Develop mobile-first gaming platforms

- Implement multi-channel payment gateways

| Cost Category | Estimated Amount |

|---|---|

| License application and fees | $20,000 – $50,000 |

| Legal and consulting services | $30,000 – $60,000 |

| Technology and platform setup | $100,000 – $250,000 |

| Marketing and customer acquisition | $50,000 – $150,000 |

| Operational expenses (first 12 months) | $150,000 – $300,000 |

- Engage local legal and financial advisors (Month 1)

- Submit license application and business registration (Month 2-3)

- Platform development and integration (Month 3-6)

- Testing, compliance verification, and soft launch (Month 6-8)

- Full market launch and scaling (Month 9-12)

- Understanding local regulatory nuances

- Strong technical infrastructure and cybersecurity

- Effective localization of products and marketing

- Competitive payment solutions adapting to local needs

- Building trust through responsible gambling practices

- Navigating licensing delays and bureaucratic hurdles

- Building brand recognition in a fragmented market

- Overcoming payment processing limitations

- Ensuring data protection compliance

- Managing fluctuating currency and economic volatility

FAQ: Frequently Asked Questions

1. Is online gambling legal in Honduras?

Online gambling in Honduras is in a transitional legal phase. While land-based gaming is regulated, the online market operates under emerging regulations. The government has begun formalizing laws to regulate, license, and tax digital gaming operators. Currently, licensed operators can legally offer services, but the framework is evolving, and non-compliance risks persist for unlicensed entities.

2. What types of gambling licenses are available and what do they cover?

Honduras offers several license types, mainly covering land-based casinos, sports betting, lotteries, and online gaming services. Online gambling licenses are distinct but integrated within the broader regulatory umbrella. Each license requires specific compliance around operations, technology, and financial reporting. Licensing categories accommodate both local operators and foreign entities partnering with local stakeholders.

3. How much does an iGaming license cost and how long does it take to obtain?

Initial licensing fees range from $20,000 to $50,000, depending on the gaming vertical and scope of operations. The approval process typically takes between 6 to 12 months, influenced by application completeness, regulatory capacity, and compliance verification. Renewal fees apply annually, alongside operational audits and compliance assessments.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain gambling licenses but must comply with local presence requirements. This usually includes establishing a Honduran registered entity or partnering with a local company. Foreign ownership is permitted but subject to regulatory scrutiny regarding transparency, financial stability, and operational oversight.

5. What are the tax obligations for iGaming operators?

Operators pay a gross gaming revenue tax set at 15%, alongside corporate income tax of 25%. There are additional licensing fees and possibly local taxes depending on jurisdictional rules. These fiscal obligations require precise accounting and timely reporting to avoid penalties.

6. Are gambling winnings taxed for players?

Yes, gambling winnings are subject to a flat tax rate of approximately 10%, withheld at source by operators when payouts exceed defined thresholds. This policy applies uniformly across land-based and online winnings, ensuring compliance and revenue collection.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, platform development, legal and compliance services, marketing expenses, payment processing fees, and staffing. Marketing and customer acquisition often represent the largest budget portions, followed by technology maintenance and regulatory compliance.

8. What is the expected ROI timeline for entering this market?

Operators can expect a break-even timeline of 18 to 24 months, factoring in license acquisition, platform launch, and customer base scaling. Market growth rates and demand support attractive returns for well-capitalized and compliant entrants. Ongoing investment in marketing and technology is essential.

9. What are the local presence requirements for operators?

Local presence mandates include registered office space, local staff or representatives, and operational evidence such as server location or customer service provisions. These requirements ensure regulatory oversight and facilitate compliance with legal obligations.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards (Visa, MasterCard), bank transfers, and popular e-wallets such as Skrill and Neteller. Mobile money and emerging cryptocurrency options are gaining traction. Offering multiple payment channels improves customer acquisition and retention.

11. What are the advertising and marketing restrictions?

Advertising is strictly regulated, limiting channels primarily to digital platforms and banning content that is misleading or targets vulnerable populations. Promotional bonuses are capped and must be transparent. Operators are also restricted in sponsorship activities and must observe time-based limitations for gambling adverts.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, player self-exclusion programs, deposit limits, session time tracking, and public awareness materials. Compliance with these measures is monitored through periodic audits and reports to the regulatory authorities.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Honduras is valued at approximately $70 million USD with a consistent 12% CAGR. Growth is propelled by rising internet penetration, mobile adoption, and increasing cultural acceptance of digital gaming. Analysts forecast sustained expansion over the next 5 years, showcasing significant potential for new entrants.

14. Who are the main competitors and what is their market share?

The market features a mix of local and regional operators specializing in sports betting, lotteries, and online casinos. Market share is currently concentrated among a handful of established firms, but regulatory developments are encouraging new entrants, which will diversify competition and increase consumer choice over time.

15. What are the player preferences and typical spending patterns?

Players favor sports betting and lottery games, with growing interest in online slots and table games. Spending is moderate, often concentrated during weekends and major sporting events. Mobile platforms dominate access, emphasizing the importance of responsive and localized gaming offerings.

16. What are the key success factors and main challenges for new entrants?

Critical success factors include regulatory compliance, robust technology infrastructure, effective local partnerships, and tailored marketing strategies. Operational challenges encompass navigating regulatory ambiguities, building brand trust, and developing secure payment integrations. Market cultural adaptation and ongoing player protection adherence are equally important.

Sources and References

- Honduras Gambling Regulatory Authority – Official Website

- National Statistical Office of Honduras – Population and Economic Data 2024

- Central Bank of Honduras – Financial Statistics and Reports

- Ministry of Finance, Honduras – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – Global iGaming Trends 2024

- Honduras Ministry of Economic Development – Digital Economy Initiatives

- Honduras Telecommunications Authority – Network Infrastructure Reports

- International Monetary Fund – Economic Assessments for Central America

- Local Market Research Firms – iGaming Consumer Behavior Analysis 2024

- Central American Digital Payment Associations Annual Report

- Latin America Financial Services Outlook 2024

- Honduran Social Services – Problem Gambling Awareness Publications

- Legal Framework for Gambling in Honduras – Government Gazette 2023

- Regional Casino & Sportsbook Operators – Market Share Reports 2024

- Mobile Technology Adoption in Honduras – ICT Development Reports 2025

- World Economic Forum – Competitiveness Reports 2024

- Honduras Ministry of Education – Literacy and Digital Skills Statistics

- South America and Central America Online Gaming Summit Proceedings 2024

- Honduras Data Protection Authority – Privacy Compliance Guidelines

- International Association of Gaming Regulators – Licensing Best Practices

- Financial Action Task Force – AML Guidelines for Gambling Operators

- Global Digital Payment Trends Report 2024

- Central America Technology Infrastructure Investment Reports

- Consumer Insights – Social Media and Digital Behavior in Honduras 2025

🎯 Gambling Databases Country Rating: Honduras

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 4.8/10 | 🟡 Moderate |

| Player Access Score | 5.5/10 | 🟡 Partially Legal |

| Overall Market Attractiveness | 5.2/10 | 🟡 Emerging market with significant regulatory uncertainty and moderate barriers |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Online casino gaming exists in LEGAL GRAY ZONE – formal licensing standards still being refined, creating significant regulatory uncertainty and risk of sudden rule changes

- Enforcement is INCONSISTENT – operators face unpredictable regulatory oversight with potential for license suspension or revocation without clear precedent

- Legal framework is INCOMPLETE – comprehensive licensing standards are “still being refined,” meaning operators enter at their own risk with no guarantee of regulatory stability

- Banking infrastructure is LIMITED – only 40% adult banking penetration creates severe payment processing challenges and high transaction costs

- High upfront costs ($200,000-$600,000 total) combined with small market size ($70M) makes ROI challenging for most operators

- 6-12 month licensing timeline with no guarantee of approval creates extended uncertainty and capital exposure

- Digital infrastructure is POOR – 48% internet penetration and 15 Mbps average speeds limit market reach and platform performance

- Regulatory ambiguity means operators could face retroactive penalties or licensing requirement changes at any time

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 1.0/3.0 | Started at +1.5 for partial legality (land-based legal, sports betting legal). Online gambling in “embryonic stage” with “gray zone” status (-0.5 for unclear legal status). Casino-style online gaming faces “legal ambiguity” (-0.5 for regulatory uncertainty). Enforcement “inconsistent” but reforms indicate change (-0.25 for instability). Digital gaming operators operate under “provisional oversight” with no clear framework (-0.25 for lack of legal clarity). Final: 1.0/3.0 |

| Licensing Process | 25% | 1.25/2.5 | Limited licensing available, 6-12 month timeline (+1.0 for limited but accessible). License fees $20,000 initial, relatively moderate (+0.5 for under €100k). However, “comprehensive licensing standards still being refined” means no clear process (-0.25 for regulatory uncertainty). Total costs $200k-$600k including legal, consulting, tech setup, and first-year operations (0 points as within €100k-250k range but on high end). Complex documentation requirements and background checks (-0.25 for probity complexity). Mandatory local presence requirement (-0.25 for operational burden). Final: 1.25/2.5 |

| Taxation & Costs | 20% | 1.5/2.0 | 15% GGR tax (+1.5 points for under 15%). 25% corporate income tax is reasonable. 10% withholding on player winnings. However, total effective tax rate 40-50% when combined (-0.25 for multiple tax layers). Operational expenses $150k-$300k first 12 months for small market creates high cost-to-revenue ratio (-0.25 for challenging economics). Limited market size ($70M total) means high customer acquisition costs relative to lifetime value. Final: 1.5/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Started at +0.5 for heavy requirements (significant local presence mandated). Must establish physical office and personnel (-0.25 for local presence burden). Foreign operators require local representatives or partnerships (-0.25 for partnership requirements). Limited banking options severely restrict payment processing (-0.25 for payment limitations affecting only 40% banked population). Domain registration and server hosting within country advised (-0.25 for infrastructure requirements). Poor digital infrastructure (48% internet, 15 Mbps speeds) increases operational complexity. Final: 0.5/1.5 |

| Market Environment | 10% | 0.55/1.0 | Difficult business environment – moderate ranking globally (+0.5 for moderate, 51-100 range implied). Strict advertising restrictions limited to digital channels only (-0.25 for advertising bans). Content must avoid “offensive or misleading claims” with heavy regulation on promotional bonuses (-0.1 for promotional restrictions). Recent regulatory changes indicate instability – amendments reducing timelines but increasing taxes (-0.1 for regulatory uncertainty). Small, fragmented market with limited brand recognition opportunities. Political structure shows “periodic unrest” creating additional risk. Final: 0.55/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 2.0/4.0 | Land-based gambling and sports betting legal (+2.0 for partial legality). Online casino gaming in legal gray zone means players face uncertainty (-1.0 for ambiguous status). No explicit player penalties mentioned, but legal ambiguity creates risk (-0.5 for regulatory uncertainty affecting players). Digital gaming operates under “provisional oversight” with unclear consumer protections (-0.5 for lack of clear legal framework protecting players). Final: 2.0/4.0 |

| Practical Accessibility | 30% | 1.5/3.0 | Started at +2.0 for some payment methods available. Credit/debit cards 58% of transactions, bank transfers 27%, e-wallets only 15%. However, only 40% adult banking penetration severely limits access (-0.5 for payment method limitations). No ISP blocking mentioned, but poor internet infrastructure (48% penetration, 15 Mbps speeds) creates access barriers (-0.5 for connectivity issues). Rural populations have “limited digital access” affecting large portion of country (-0.5 for geographic access inequality). Mobile penetration 70% helps but doesn’t compensate for other limitations. Final: 1.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | No player penalties mentioned in the documentation (+2.0 points). Regulatory focus is on operators, not players. Player protection measures emphasize age verification and responsible gambling rather than punitive enforcement. Final: 2.0/2.0 |

| Market Availability | 10% | 0.0/1.0 | “Limited but growing number of licensed operators” in nascent market (0 points for unclear licensing creating market vacuum). “Market share concentrated among few established entities” indicates limited choice. “New licenses expected following recent legislative updates” means market currently restricted. Offshore access not mentioned as blocked, but gray zone status means uncertain availability (+0.25 for some offshore access). However, poor enforcement and regulatory ambiguity may allow offshore operators (-0.25 for unreliable market access). Final: 0.0/1.0 |

🔍 Key Highlights

Strengths (Limited)

- Relatively low GGR tax at 15% compared to regional standards

- Growing market with 12% CAGR and increasing mobile/internet penetration

- No player penalties or criminalization of gambling activities

- Moderate initial licensing costs ($20,000) compared to developed markets

- Young demographic (31% aged 25-44) with growing middle class and digital adoption

- Regional integration and tourism creating growth opportunities

- No active ISP blocking of gambling sites currently reported

⛔️ CRITICAL RISKS AND CHALLENGES

- Regulatory Uncertainty: Online casino licensing “still being refined” with operators in “gray zone” under “provisional oversight” – NO CLEAR LEGAL FRAMEWORK exists, creating massive risk of rule changes, retroactive penalties, or license denials

- Enforcement Inconsistency: “Inconsistent enforcement” means operators cannot predict regulatory actions, fines, or license suspensions – you’re essentially gambling on the regulator

- Legal Ambiguity for Casino Games: “Casino-style online gaming faces legal ambiguity” – meaning your core product category may be ruled illegal at any time

- Small Market Size: Only $70M total market size projected for 2025 makes it extremely difficult to achieve scale necessary for profitability with $200k-$600k entry costs

- Banking Infrastructure Crisis: Only 40% adult banking penetration means 60% of potential customers cannot easily deposit/withdraw – massive conversion and payment processing challenges

- Digital Infrastructure Inadequacy: 48% internet penetration and 15 Mbps average speeds severely limit addressable market and platform performance quality

- High Entry Costs vs Market Size: $200k-$600k total entry costs for $70M market (0.3-0.9% of entire market needed just to break even on entry) – economics are extremely challenging

- Mandatory Local Presence: Physical office and local partnerships required increase fixed costs and operational complexity significantly

- Limited Payment Options: E-wallets only 15% adoption, cryptocurrency “nascent” and limited – severely restricts modern payment methods

- Strict Advertising Limits: “Limited to digital channels” with “strict” regulations and content restrictions dramatically increase customer acquisition costs in already small market

- Geographic Inequality: Urban concentration (57%) means rural areas with 43% of population are essentially unreachable due to “limited digital access”

- Economic Instability: Per capita income only $2,700 USD with Gini coefficient 0.50 (high inequality) limits spending power and creates volatile revenue base

- Political Risk: “Periodic unrest” and “regulatory consistency under development” create ongoing operational uncertainty

- Long Licensing Timeline: 6-12 months for licensing with no guarantee of approval means extended capital exposure with no revenue generation

Player-Specific Issues

- Online casino games exist in legal gray zone – players uncertain if their activity is legal

- 60% of adults unbanked, severely restricting ability to deposit and withdraw funds

- Rural players (43% of population) face “limited digital access” effectively excluding them from market

- Poor internet speeds (15 Mbps average) create frustrating user experience and disconnections

- Limited operator choice due to nascent licensing regime restricts player options and competition

- Provisional regulatory oversight means unclear consumer protection and dispute resolution mechanisms

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $200,000 – $600,000 USD (licensing $20k-$50k, legal/consulting $30k-$60k, technology $100k-$250k, marketing $50k-$150k, operations $150k-$300k first year)

Monthly Operating Costs: $15,000 – $30,000 USD (local office, staff, compliance, technology, payment processing)

Effective Tax Rate on Revenue: 40-50% (15% GGR tax + 25% corporate income tax + 10% player withholding + operational taxes)

Customer Acquisition Cost: $50-$150 USD (estimated based on strict advertising restrictions, limited digital channels, and need to build brand recognition in nascent market)

Average Revenue Per User: $25 USD (from article)

Total Addressable Market: $70M USD (2025 projection) – but realistically only $30-$40M accessible due to banking/internet penetration limitations

Time to Breakeven: 24-36 months MINIMUM (assuming successful license acquisition, effective market penetration, and no major regulatory changes)

Time to Positive ROI: 36-48 months (assuming everything goes perfectly, which is unlikely given regulatory uncertainty)

Profitability Assessment: Economics are EXTREMELY CHALLENGING and highly risky. To break even on a $400,000 investment at $25 ARPU and 40% effective tax rate, you need approximately 26,667 active players – that’s nearly 1% of the ENTIRE adult population or 3.8% of the entire projected market size. With only 40% banking penetration and 48% internet penetration, your actual addressable market is perhaps 1.9 million people maximum. You’d need to capture 1.4% of the addressable market just to break even – an extremely aggressive target in a nascent, legally ambiguous environment with strict advertising restrictions. Only viable for operators with $1M+ capital willing to accept 3-5 year investment horizons and significant regulatory risk. Most operators should avoid this market entirely.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | HIGH | Operating in legal gray zone with no clear licensing path. Risk of sudden regulatory crackdown, retroactive penalties, or classification as illegal operation. No ISP blocking currently but could be implemented. Inconsistent enforcement creates unpredictable risk. |

| Licensed Operators (if obtainable) | MEDIUM-HIGH | Comprehensive licensing standards “still being refined” means license conditions could change retroactively. Risk of license suspension/revocation under unclear criteria. Provisional oversight provides inadequate legal protection. Regulatory uncertainty makes long-term planning impossible. |

| Affiliates/Advertisers | MEDIUM | Strict advertising restrictions with unclear enforcement. Risk of being caught in regulatory crackdown targeting operators. Content restrictions heavily regulated with “strict penalties for breaches.” Payment processor termination risk if regulatory stance hardens. |

| Payment Processors | MEDIUM | Limited banking infrastructure creates operational challenges. Regulatory ambiguity means processors could face sudden rule changes. Risk of being designated as facilitating illegal activity if online casino status changes. AML requirements strictly enforced. |

| Company Directors/Executives | MEDIUM | Background checks required for licensing expose personal information. Operating in gray zone creates potential personal liability. Local presence requirement means physical presence in country with “periodic political unrest.” Unclear whether directors face personal penalties for regulatory violations. |

🚨 Extradition and International Enforcement

Extradition Treaties: Honduras has extradition agreements with United States, Mexico, Spain, Canada, Chile, and other nations listed in double taxation treaty section. These agreements could theoretically be used for serious financial crimes, though gambling-specific enforcement unclear.

Enforcement History: No specific cases documented of international prosecution for gambling offenses in Honduras. However, regulatory framework is too new to establish clear precedent. The “Honduran National Gambling Commission” has authority to pursue criminal charges for “serious violations” but scope undefined.

Safe Jurisdictions: Not specifically relevant for Honduras market as primary risk is regulatory uncertainty and license revocation rather than criminal prosecution. However, operators should note that extradition agreements exist if activities are later classified as criminal.

Travel Risk: LOW for gambling-related activities currently. However, if operations are later deemed illegal and criminal charges pursued, executives could face arrest when traveling through countries with extradition treaties. Risk increases significantly if operating without attempting proper licensing.

📋 Final Verdict

Honduras receives an Operator Ease Score of 4.8/10 and a Player Access Score of 5.5/10, resulting in an overall market attractiveness rating of 5.2/10.

HONEST ASSESSMENT: Honduras is a HIGH-RISK, MARGINALLY VIABLE market suitable only for specialized operators with significant capital and risk tolerance. The fundamental problem is that you’re being asked to invest $200k-$600k into a regulatory framework that is explicitly “still being refined” with “inconsistent enforcement” and “legal ambiguity” for online casinos.

The economics are punishing: a $70M total market means you need to capture significant market share just to recover entry costs, while 60% of the population can’t easily participate due to banking limitations. For 95% of operators, this is a market to avoid. The remaining 5% who might consider entry must have $1M+ capital, 5-year investment horizons, tolerance for extreme regulatory uncertainty, and willingness to potentially lose their entire investment if regulations change unfavorably.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Established Latin American operator with $1M+ capital willing to absorb total loss

- Operating sports betting ONLY (clearer legal status than casino games)

- Experienced in navigating regulatory uncertainty in emerging markets

- Have 5-7 year investment horizon with no pressure for quick ROI

- Capable of establishing genuine local partnerships and physical presence

- Willing to accept that “comprehensive licensing standards still being refined” means your license conditions could change dramatically

- Prepared for 40-50% effective tax rate and $15k-$30k monthly operating costs

- Have technical infrastructure to handle poor internet speeds and limited connectivity

❌ Definitely Avoid If You Are:

- Casino-focused operator (legal status is explicitly “ambiguous” and in “gray zone”)

- Startup or small operator with less than $1M capital

- Seeking ROI within 24-36 months (nearly impossible given market size and costs)

- Offshore operator without plans to obtain proper licensing (risk too high even without active blocking)

- Unable to establish physical office and local partnerships in Honduras

- Expecting clear, stable regulatory framework (explicitly does not exist)

- Relying on modern payment methods like crypto or advanced e-wallets (limited adoption)

- Planning aggressive marketing campaigns (strict advertising restrictions)

- Risk-averse operator requiring legal certainty before major investment

- Operators focused on rural markets (43% of population essentially unreachable)

- Companies requiring robust banking infrastructure (60% of population unbanked)

- Any operator expecting regulatory clarity and consistent enforcement (explicitly inconsistent)

⚠️ BOTTOM LINE: Honduras is a speculative, high-risk emerging market where the regulatory framework is admittedly incomplete and inconsistent – only operators with deep pockets, long time horizons, and high risk tolerance should even consider entry, and then ONLY for sports betting, not casino gaming.