Hungary presents a compelling opportunity for iGaming operators amid ongoing regulatory modernization and market liberalization. The evolving legal framework is transitioning from state monopoly dominance to a more open, competitive market, especially in online sports betting and casinos.

With increasing digital adoption and a tech-savvy population, Hungary’s iGaming sector offers growth prospects enhanced by planned regulatory reforms improving licensing and player protection measures.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal with regulatory licensing |

| Regulatory Authority | Supervisory Authority for Regulatory Affairs (SZTFH) |

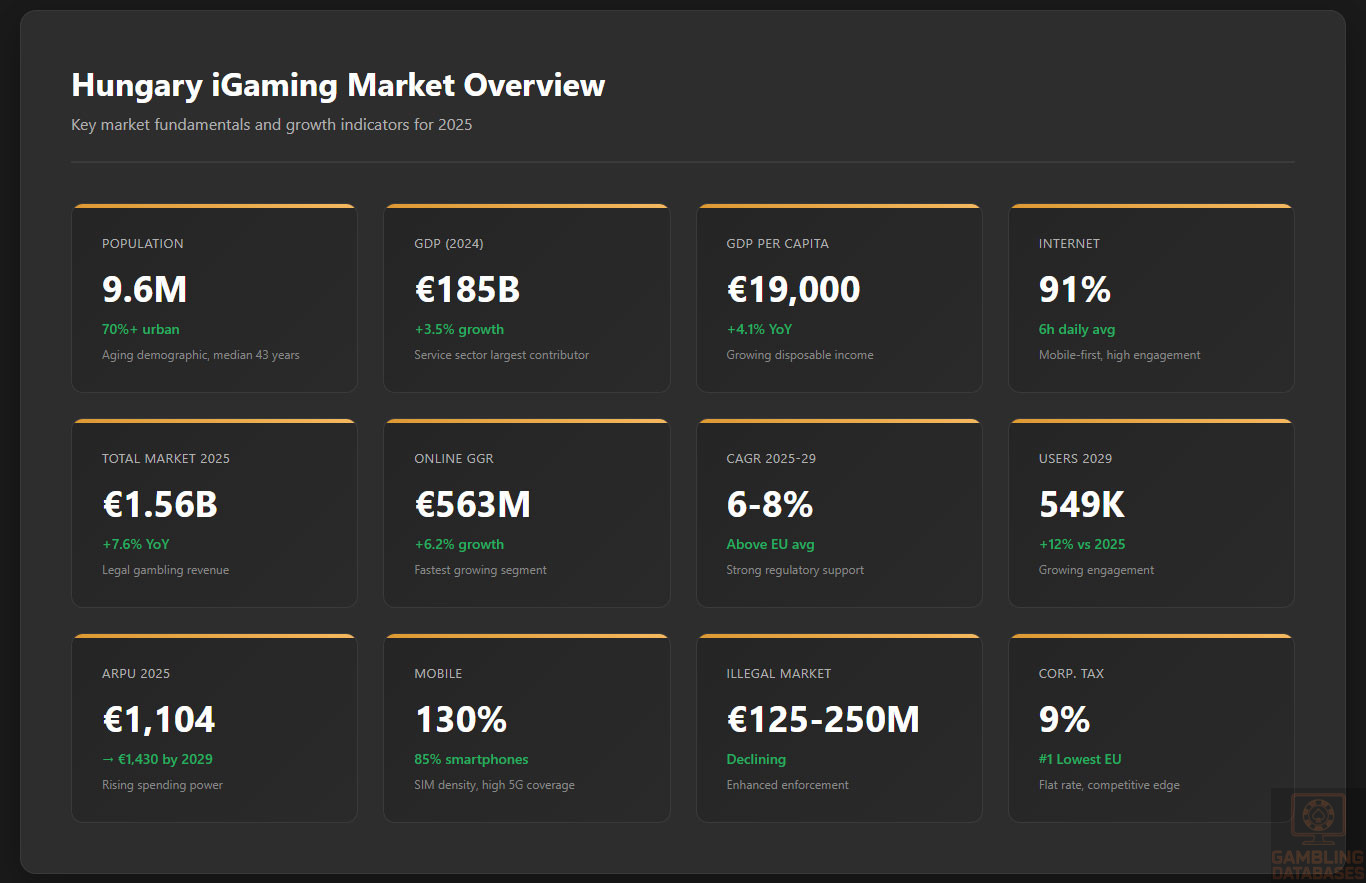

| Population | 9.6 million |

| GDP (Nominal) 2024 | Approx. €185 billion |

| GDP per Capita | ~€19,000 |

| Internet Penetration | 91% |

| Mobile Penetration | 130% (SIM density) |

| Online Gambling Revenue (2024) | €563 million |

| Land-Based Gambling Revenue (2025) | ~€1.0 billion |

| Total Gambling Market Revenue (2025) | €1.56 billion |

| Expected Market CAGR (2025-2029) | 6-8% |

| Estimated Online Users (2029) | 549,000 |

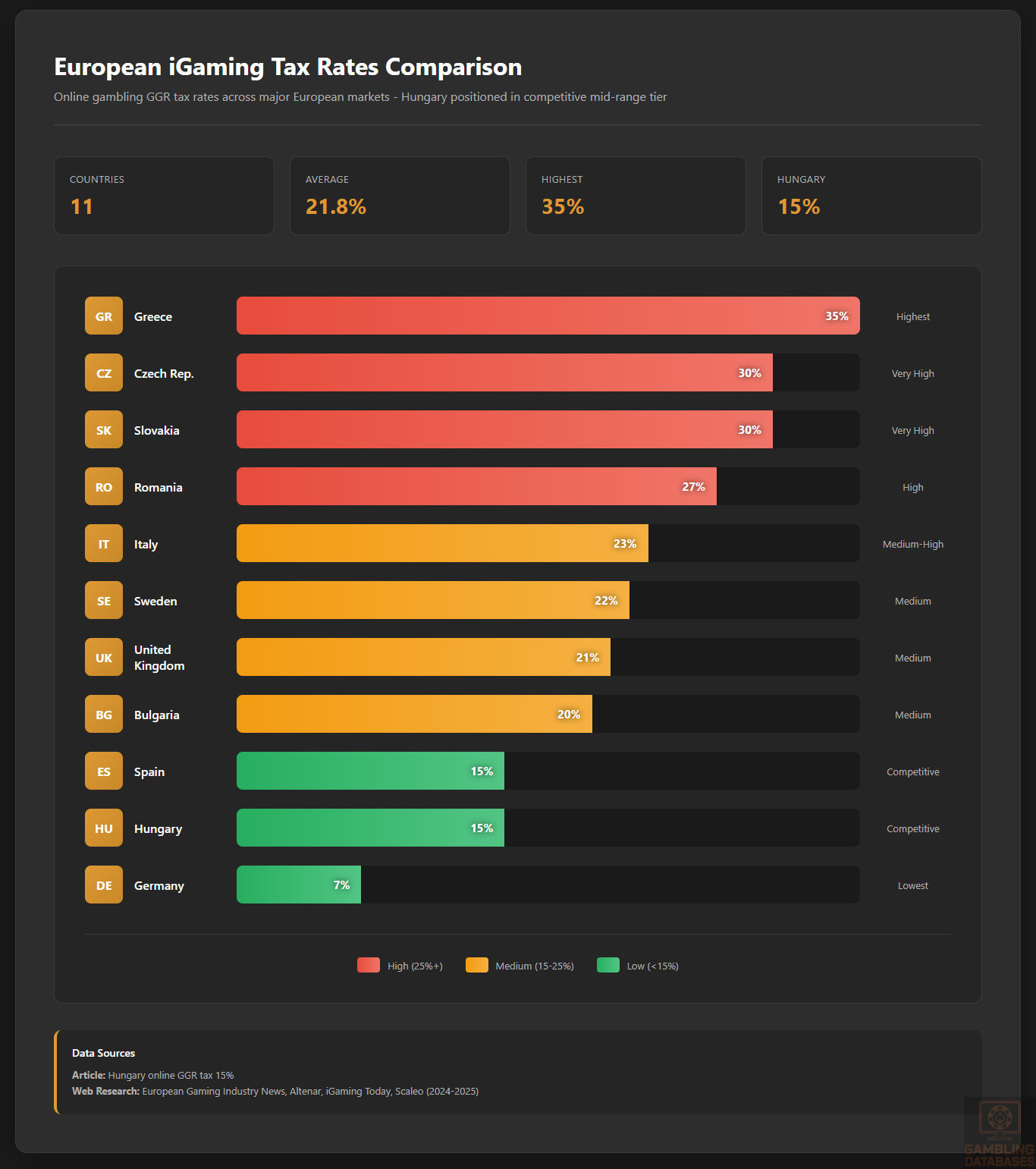

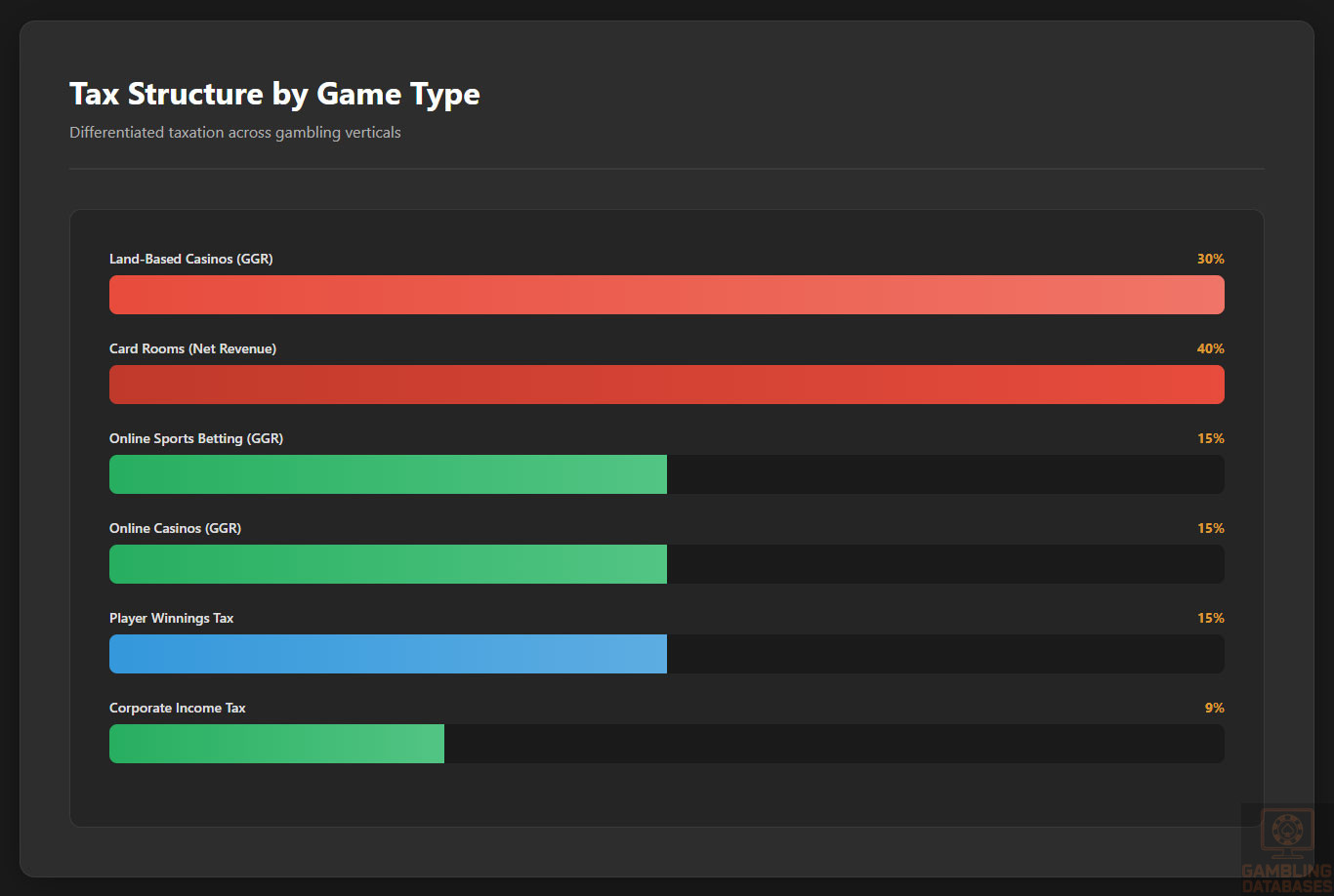

| Online Casino GGR Tax Rate | 15% |

| Land-Based Casino GGR Tax Rate | 30% |

| Sports Betting GGR Tax Rate | 15% |

| Corporate Income Tax Rate | 9% flat |

| Slot Machine Monthly Tax | HUF 500,000 per machine |

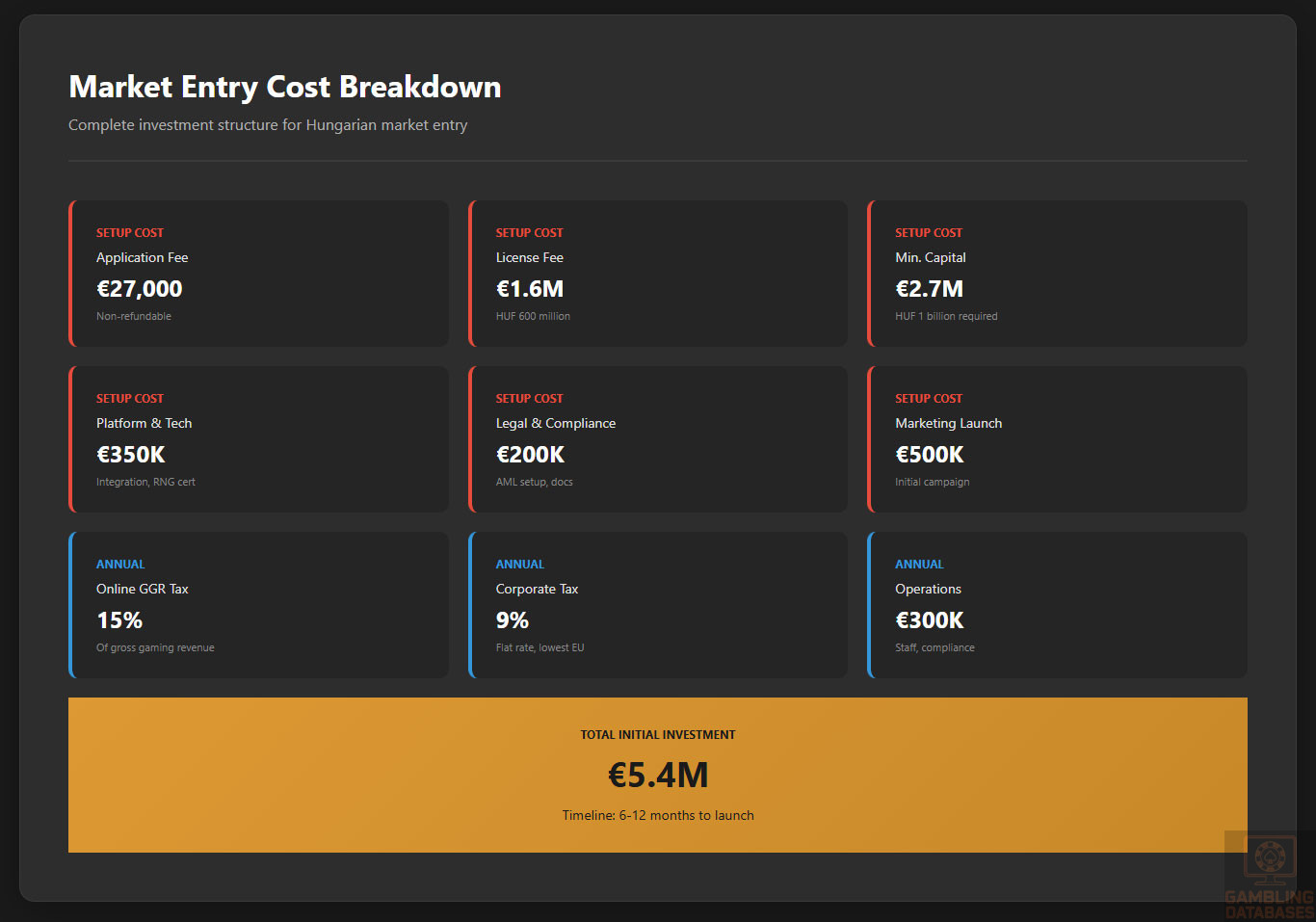

| Licensing Fee | HUF 600 million (~€1.6 million) |

| Application Fee | HUF 10 million (~€27,000) |

| Minimum Capital Requirement | HUF 1 billion (~€2.7 million) |

| Local Presence Requirement | Company registration and servers in Hungary required |

| License Validity | Multiples years (subject to renewal) |

| Player Age Limit | 18 years |

| Responsible Gambling Measures | Mandatory |

| Illegal Gambling Market Size | €125-250 million estimated |

| Unified Licensing Introduction | Expected 2025 for multiple gambling verticals |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Hungary maintains a well-defined regulatory framework governing all gambling activities, including land-based and online sectors. The regime is overseen by the Supervisory Authority for Regulatory Affairs (SZTFH), which operates under the Ministry of Finance.

The national Gambling Act, initially adopted in 1991 and substantially amended over the years, provides the backbone for regulatory control. Key reforms have aimed at transitioning Hungary from a state monopoly in online gambling towards a more open competitive environment while ensuring player protection and market integrity.

Land-Based Gambling Activities

Land-based gambling in Hungary covers casinos, sports betting outlets, slot machine halls, and card rooms. Casino operations are tightly regulated, with licensing conditioned on high capital requirements and operational standards. Sports betting is available both online and in physical venues, with a clear licensing and tax regime.

Slot machines outside casinos are taxed by a fixed monthly fee per device, which incentivizes regulatory compliance and revenue collection. The government actively enforces regulation to combat illegal gambling venues and operators.

Online Gambling Framework

The online gambling market is regulated separately, with distinct licensing and operational requirements. Historically dominated by a state monopoly for online casinos, recent regulatory changes have opened the market to private and foreign operators, specifically in online sports betting since 2023.

Hungary’s online gambling framework enforces strict technical, financial, and compliance standards. Operators must obtain a license from SZTFH, implement robust AML and KYC procedures, and provide player protection tools including responsible gambling measures. Prohibited activities include unlicensed operations and gambling services offered without local authorization.

Licensed Operators and Market Players

The market features a mix of state-owned entities alongside licensed private operators specializing in sports betting and emerging online casino offerings. The 2023 regulatory reforms enabled foreign operators to apply for licenses, although uptake has been gradual due to stringent requirements on local presence and financial strength.

Competitive dynamics are evolving with the introduction of a unified licensing system expected in 2025. This will streamline operator access to multiple gambling verticals under a single license, facilitating market entry and expansion strategies for reputable operators.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing process is rigorous, designed to ensure only credible operators enter the market. Applicants must demonstrate at least five years of licensed gambling experience within the European Economic Area, possess minimum share capital of HUF 1 billion, and pay non-refundable application and licensing fees.

Commonly required documents include corporate registration, audited financial statements, technical platform certifications, proof of local server location, and background checks for key personnel.

Local Presence and Operational Requirements

Hungary mandates strict local presence obligations for licensed operators. They must have company registration and infrastructure within the country, including hosting gambling servers locally to ensure regulatory oversight and data protection compliance.

Personnel requirements include employment of compliance officers and dedicated local representatives to liaise with authorities. Foreign ownership is permitted but closely scrutinized to ensure operational transparency and national security considerations.

Compliance Obligations and Monitoring

Player Protection and Identification

- Strict age verification to ensure players are 18 or older

- Comprehensive KYC and AML compliance aligned with EU directives

- Implementation of deposit and loss limits to mitigate gambling harm

- Availability of self-exclusion mechanisms for voluntary player exclusion

- Promotion of responsible gambling via mandatory support tools and awareness campaigns

- Regular reporting of suspicious activity to regulators

Operators are required to maintain transparent player data management and privacy standards compliant with GDPR. The regulatory framework emphasizes safeguarding vulnerable players and ensuring transparent, fair game outcomes through certified Random Number Generators (RNG).

Financial Monitoring and Reporting

Financial compliance involves continuous transaction monitoring, submission of periodic financial and operational reports to the regulator, and undergoing independent audits. Operators must submit monthly reports covering gross gaming revenue, tax payments, and suspicious transaction investigations.

- Monthly submission of revenue and tax declarations

- Quarterly AML compliance and financial control reports

- Annual external audits verifying operational compliance

- Immediate reporting of regulatory breaches or suspicious activities

- Cooperation with regulator on inspection and enforcement actions

Taxation Structure and Financial Obligations

Player Taxation

Players’ gambling winnings are taxable at a flat rate of 15%, which operators withhold and remit to tax authorities. There are no exemptions based on amount thresholds, making compliance straightforward from a player perspective.

Operator Taxation

| Gambling Type | Tax Base | Tax Rate |

|---|---|---|

| Land-Based Casinos | Gross Gaming Revenue (GGR) | 30% (tiered above HUF 10 billion) |

| Online Sports Betting | Gross Gaming Revenue (GGR) | 15% |

| Online Casinos (State Monopoly Applies) | Gross Gaming Revenue (GGR) | 15% |

| Lottery | Turnover | Varies by game type (fixed percentages) |

| Slot Machines (outside casinos) | Per device monthly | HUF 500,000 per machine |

| Card Rooms | Net Gaming Revenue | 40% |

| Corporate Income Tax | Profits | 9% flat rate |

Operators pay fixed and variable taxes depending on game categories, along with corporate income tax on profits. License renewal fees and turnover taxes also apply, influencing operator cost structures significantly.

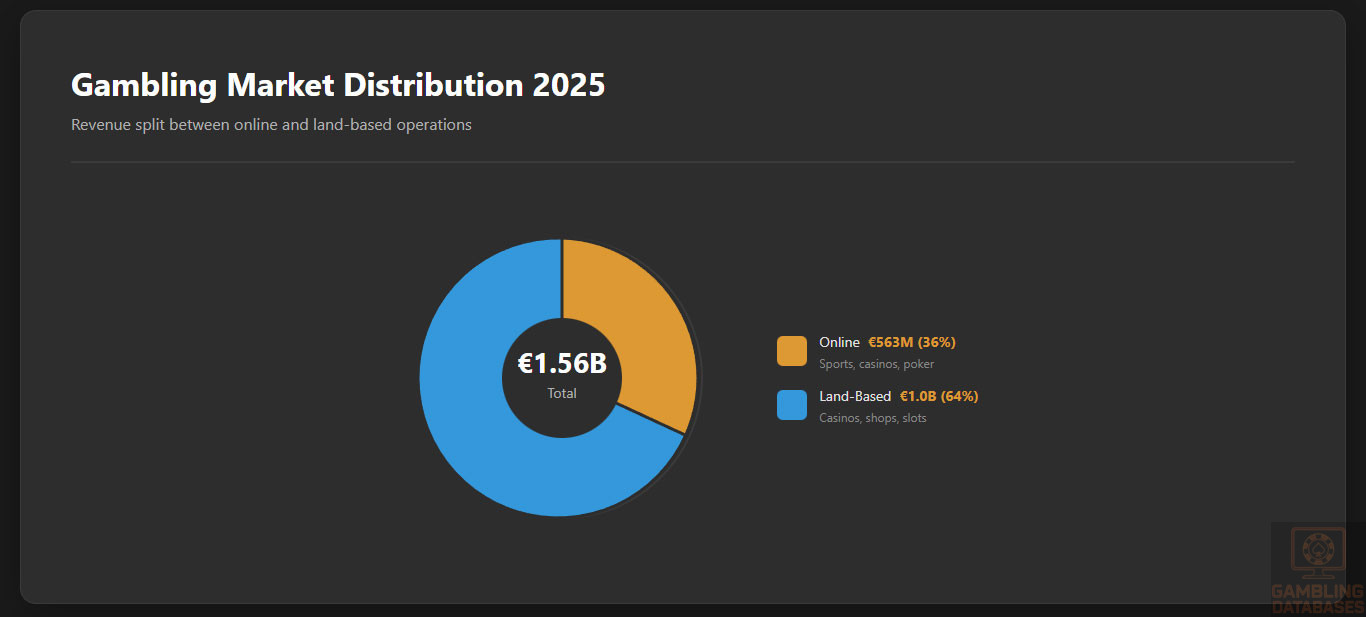

Gambling Market Financial Performance

The total legal gambling market turnover is estimated at €1.56 billion for 2025, split between land-based and online segments. Revenue trends indicate sustained growth with an expected CAGR of 6-8% driven by increasing online adoption and regulatory clarity.

The black market still accounts for an estimated €125–250 million, but enhanced enforcement and blocking measures of unlicensed sites have contributed to a strong legal market traffic increase.

Advertising and Marketing Restrictions

- Advertising restricted to authorized channels only

- Mandatory inclusion of responsible gambling messaging

- Limits on promotional bonuses and advertising timing

- Prohibition of targeting minors or vulnerable groups

- Restrictions on sponsorship visibility in certain media

Marketing activities are closely monitored to ensure compliance with consumer protection objectives. Operators must report advertising content and adhere to audit requirements.

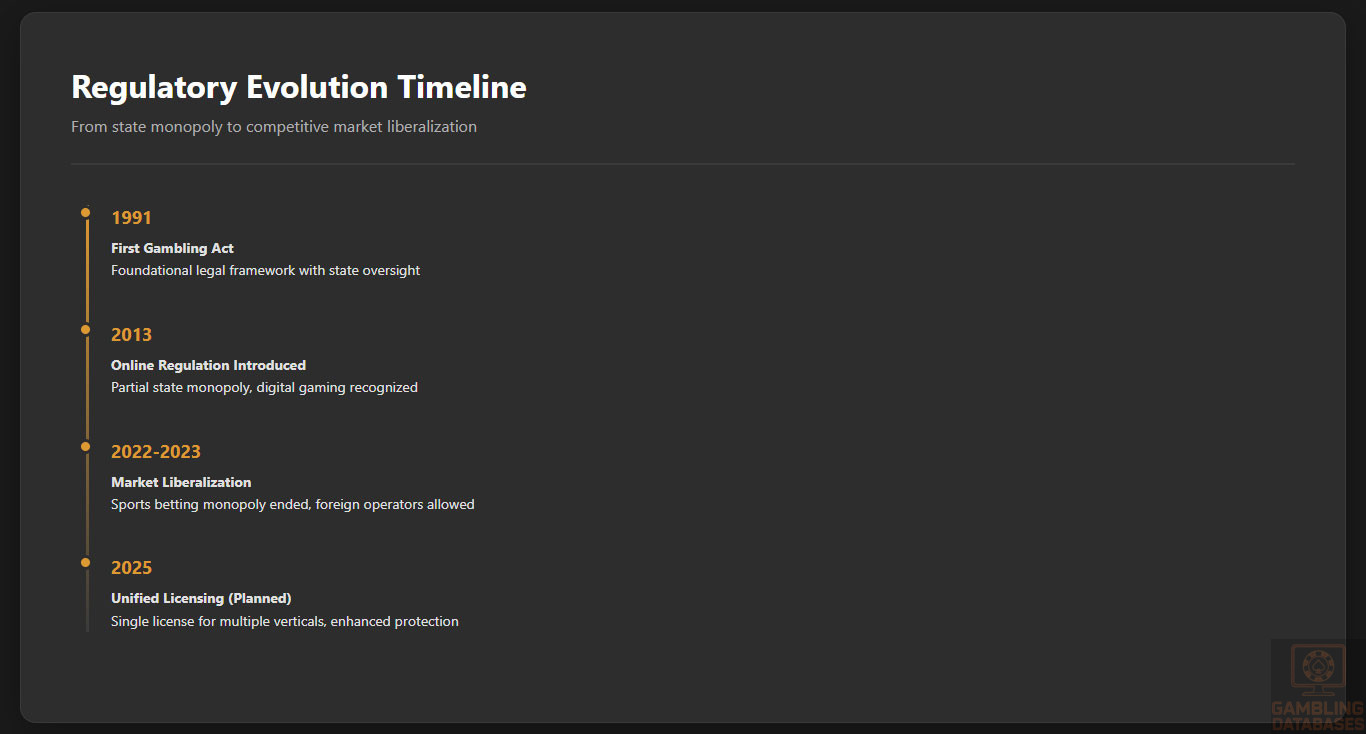

Recent Regulatory Changes and Their Impact

- 1991: First Gambling Act establishing foundational legal framework

- 2013: Introduction of online gambling regulation with partial state monopoly

- 2022-2023: End of online sports betting monopoly, entry allowed for foreign operators

- 2025 (planned): Introduction of unified licensing and modernized player protection measures

Recent reforms have reduced regulatory barriers but increased compliance costs through stricter safeguards, ensuring a balanced market favorable to reputable operators.

Enforcement Mechanisms and Penalties

- Fines for operating without license

- Revocation and suspension of licenses for non-compliance

- Criminal penalties for fraudulent activities

- Blocking of illegal gambling websites

- Ongoing monitoring and mystery shopping by regulators

The regulatory regime employs proactive enforcement to maintain market integrity and consumer confidence, deterring illicit operators effectively through both administrative and criminal sanctions.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

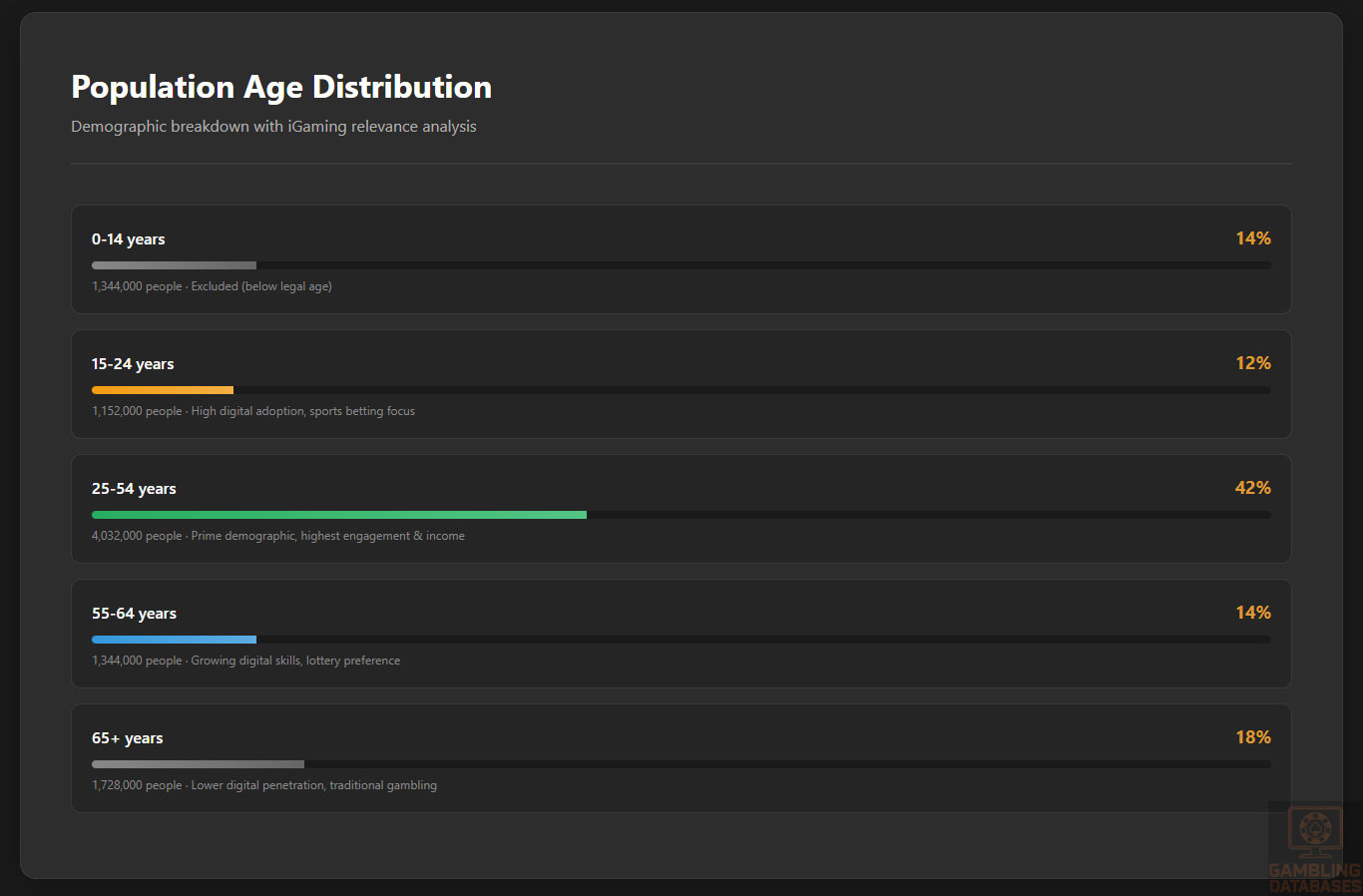

Hungary has a population of approximately 9.6 million people, characterized by an aging demographic with a median age of about 43 years. The population exhibits a slightly higher female ratio, with women making up roughly 52%, reflecting typical European demographic trends. Urbanization is significant, with more than 70% of the population residing in urban areas, influencing gambling venue distribution and online betting participation.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 14% |

| 15-24 years | 12% |

| 25-54 years | 42% |

| 55-64 years | 14% |

| 65+ years | 18% |

Geographically, the population is concentrated in key urban centers primarily in the central and western regions. This urban concentration corresponds with higher internet and mobile network penetration, facilitating access to regulated gambling platforms.

Geographic Distribution

Major cities dominate economic activity and gambling infrastructure, with Budapest as the clear epicenter for market demand and gambling venues. The western region exhibits higher GDP per capita, supporting elevated consumer spending patterns. Rural areas, while less densely populated, have increasing access to mobile internet, supporting gradual growth in online gambling participation.

- Budapest: Population approx. 1.7 million, primary center for gambling and entertainment

- Debrecen: 200,000+, significant regional economic hub

- Szeged: 160,000+, growing urban market with expanding digital access

- Miskolc: 150,000+, industrial region with emerging gambling interest

- Pécs: 140,000+, cultural center influencing consumer behaviors

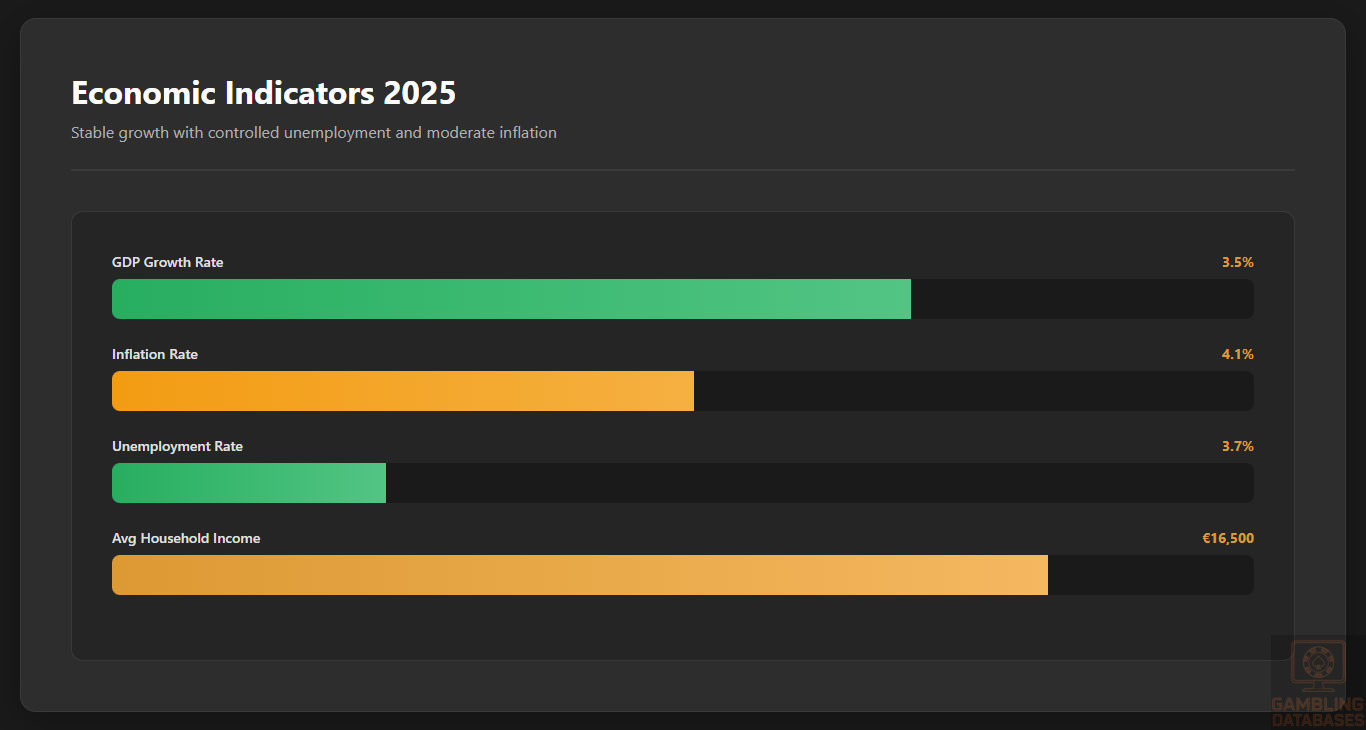

Economic Indicators and Consumer Spending Power

Hungary’s economy shows steady growth with a nominal GDP of approximately €185 billion. The economy is diverse, driven by manufacturing, services, and agriculture, with the service sector representing the largest contribution. Recent forecasts anticipate continued GDP growth of around 3-4% annually.

Per capita GDP hovers near €19,000, with median household income increasing in line with inflation and economic reforms. Disposable incomes have grown notably in urban areas, where consumer spending on entertainment and digital services, including gambling, reflects upward trends.

| Indicator | Value |

|---|---|

| GDP (Nominal) | €185 billion |

| GDP Growth Rate | Approx. 3.5% |

| GDP per Capita | €19,000 |

| Unemployment Rate | 3.7% |

| Inflation Rate | 4.1% |

| Average Household Income | €16,500 |

Consumer spending in Hungary is increasingly digital-focused, with a notable shift towards online transactions and subscription services, making the market fertile for online gambling operators targeting tech-savvy consumers.

Market Size and Growth Projections

Hungary’s gambling market is projected to expand significantly over the next five years. The current legal market size is approximately €1.56 billion, with online segments growing faster due to increasing digital penetration and regulatory liberalization.

Market forecasts show a compound annual growth rate (CAGR) of around 6-8% through 2029, propelled by expanding access to online sports betting and casino platforms. Average revenue per user (ARPU) is projected to rise steadily, supported by broader demographic engagement and innovative product offerings.

| Year | Total Market Size (€ Billion) | Online Market Size (€ Million) | Estimated Users (Thousands) | ARPU (€) |

|---|---|---|---|---|

| 2024 | 1.45 | 530 | 490 | 1082 |

| 2025 | 1.56 | 563 | 510 | 1104 |

| 2027 | 1.88 | 670 | 540 | 1240 |

| 2029 (Forecast) | 2.15 | 785 | 549 | 1430 |

Education, Skills, and Digital Literacy

Hungary boasts a literacy rate exceeding 99%, with a strong emphasis on secondary and higher education fostering a skilled workforce. The country maintains solid digital literacy, especially among younger and urban populations, facilitating rapid adoption of online services, including gaming platforms.

University education and technical training enhance digital proficiency, with widespread usage of computers, smartphones, and internet technologies. This skill base underpins a fertile environment for iGaming operators looking to engage well-informed consumers who value innovative and secure online experiences.

Cultural and Social Factors

Communication and Language

Hungarian is the official and dominant language, used extensively in media, business, and online content. While English proficiency is growing, particularly among younger and urban demographics, online gambling operators typically localize content predominantly in Hungarian for broader market reach.

Minority language groups exist but are small; the market is linguistically homogeneous, which simplifies marketing and communications. Consumer engagement platforms and customer support overwhelmingly utilize Hungarian.

Cultural Attitudes

The public in Hungary generally holds a pragmatic attitude toward gambling, viewing it as a popular form of entertainment with moderate social acceptance. Although some conservative segments express concerns about gambling-related harm, overall gambling participation is culturally normalized, especially for sports betting and lottery products.

Religious influences, particularly from dominant Christian denominations, shape some regional attitudes but do not strongly impede market participation. Foreign gambling brands are regarded with interest, especially when offering reputable, regulated services aligned with local expectations and compliance standards.

Problem Gambling and Social Considerations

The prevalence of problem gambling is estimated at roughly 2-3% of the adult population, consistent with European averages. At-risk groups include young adults, lower-income communities, and heavy sports bettors. The government promotes socially responsible gambling through mandated contributions from operators and public education campaigns.

- National problem gambling prevention programs

- Gambling addiction treatment centers

- Self-exclusion registries and tools

- Public awareness and education initiatives

- Mandatory operator contributions to responsible gambling funds

Political Structure and Governance

Hungary is a parliamentary republic with a stable political environment. Its regulatory framework benefits from consistent policies supporting transparency and investor protections, conducive to foreign business operations. The government’s pro-European economic stance while maintaining national regulatory control ensures a balanced approach to gambling market governance and cross-border cooperation.

Technology Adoption and Digital Behavior

Internet and Digital Usage

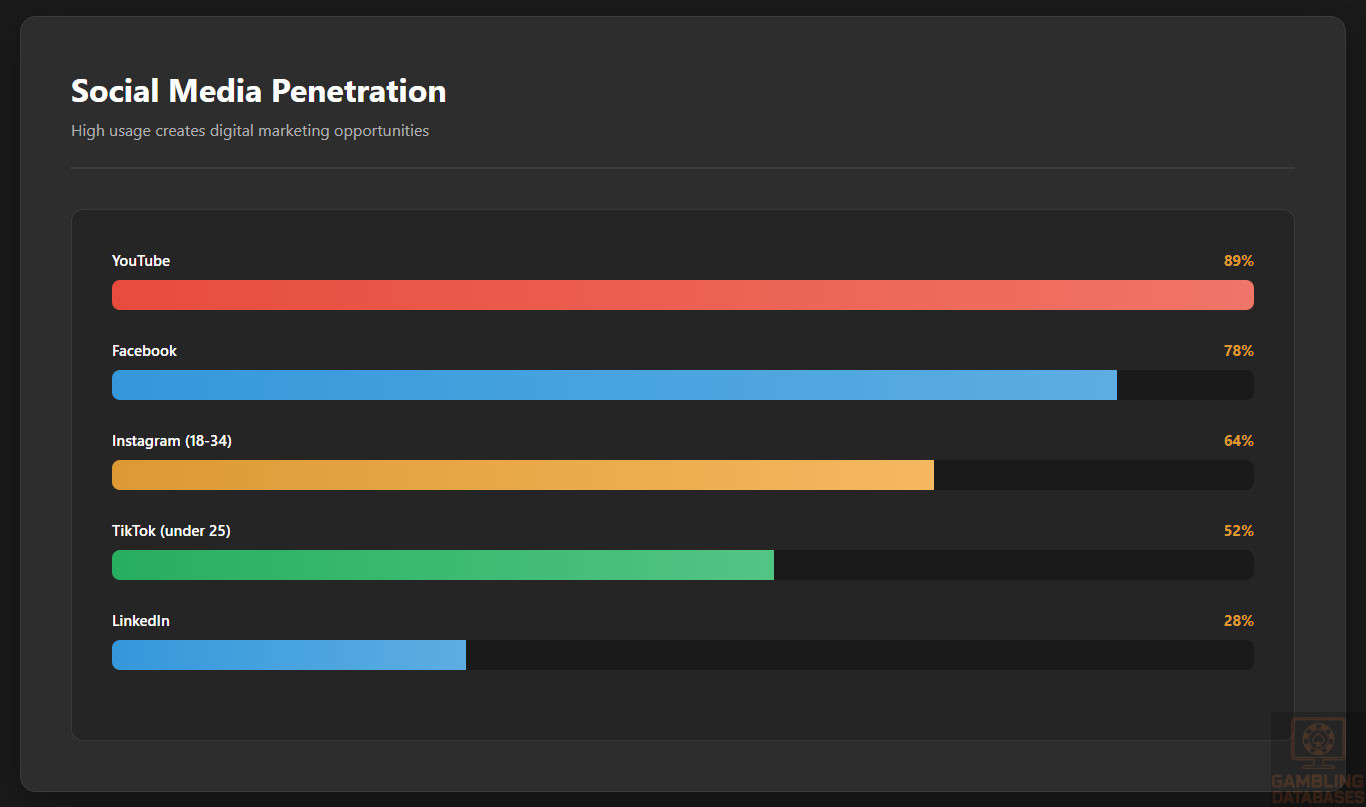

Internet penetration exceeds 90%, with average daily usage around six hours. Mobile internet access is prevalent, with smartphone adoption surpassing 85%. Social media engagement is robust, particularly among younger cohorts, driving extensive digital interaction.

- Facebook: 78% of internet users, daily engagement 2.3 hours

- YouTube: 89% penetration, average watch time 45 minutes daily

- Instagram: 64% among ages 18-34, visual content preferred

- TikTok: Rapid growth with 52% penetration under 25 years

- LinkedIn: 28% usage for professional networking

Digital Payment Behavior

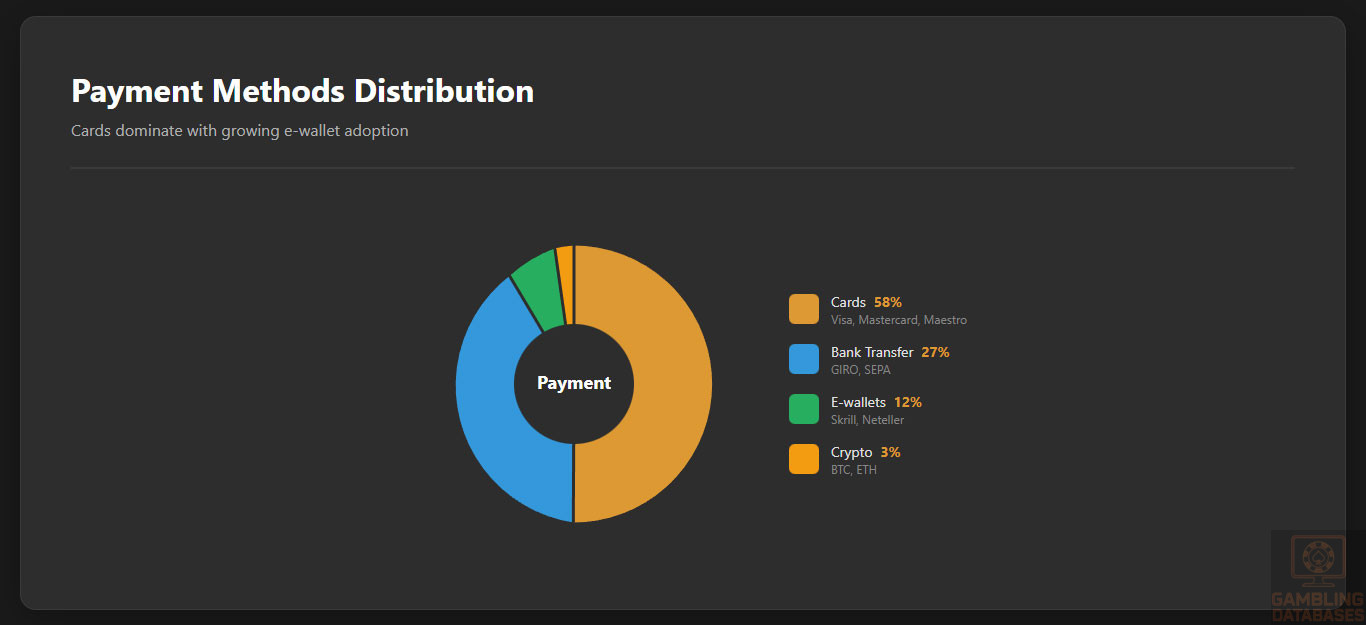

Hungarian consumers demonstrate a preference for convenient, secure payment methods in online environments. Credit and debit cards dominate online transactions, supported by rapid growth in e-wallet use and bank transfers. Cryptocurrency adoption remains niche but is growing among younger consumer segments.

- Credit and debit cards: 58% of online gambling payments

- Bank transfers: 27% of payment volume

- E-wallets (e.g., Skrill, Neteller): 12% and rising

- Mobile payment solutions (Apple Pay, Google Pay): Increasing adoption

- Cryptocurrency: Emerging but less than 5% of transactions

Gaming and Gambling Preferences

Current Market Participation

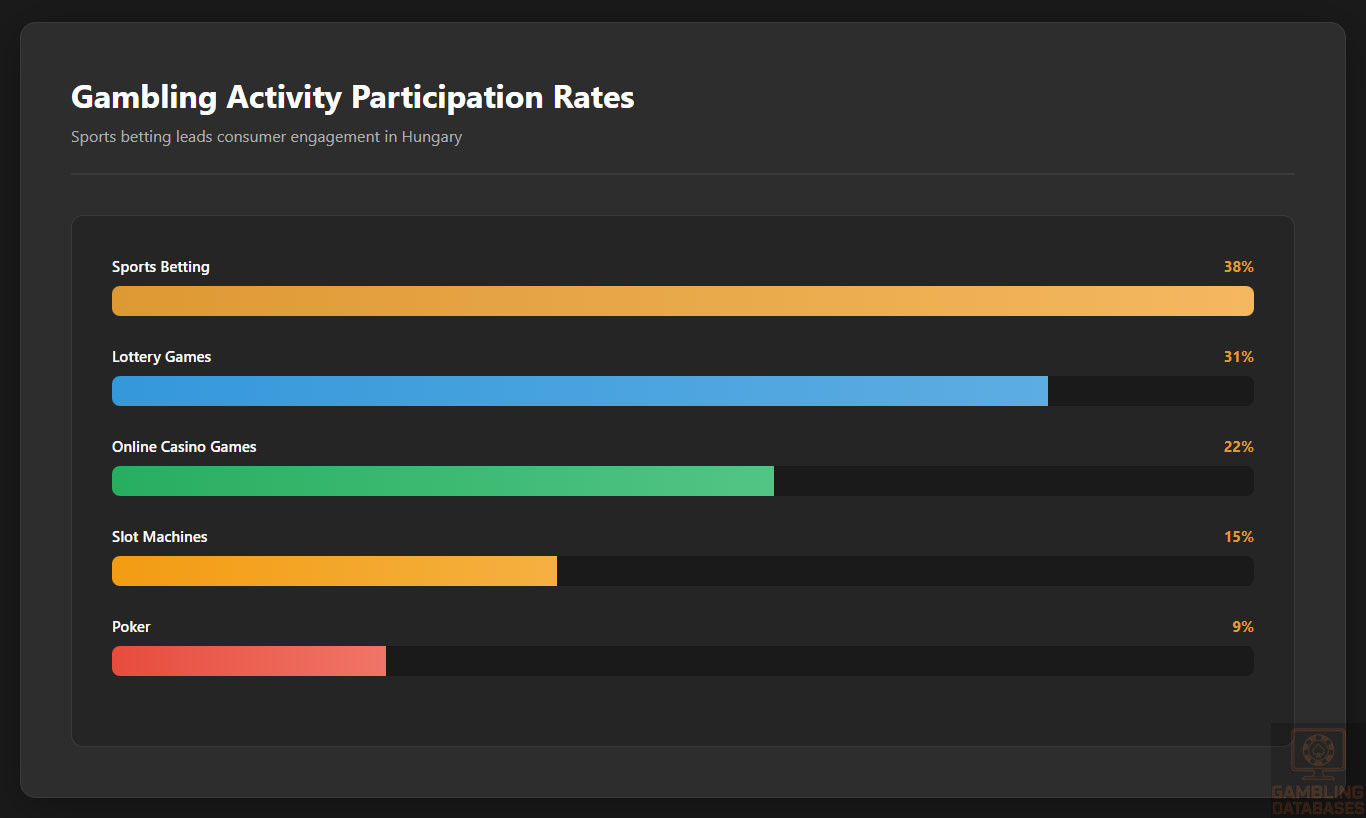

Gambling participation in Hungary is widespread with diverse consumer preferences. Sports betting leads in popularity followed by lotteries, followed by online casino games spreading rapidly due to internet accessibility.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 38% |

| 2 | Lottery Games | 31% |

| 3 | Online Casino Games | 22% |

| 4 | Slot Machines | 15% |

| 5 | Poker | 9% |

Consumer Behavior Patterns

Hungarian gamblers typically favor platforms offering localized content, ease of payment, and strong mobile functionality. Peak gambling activity occurs during evening hours and weekends, reflecting work and leisure cycles. User retention is driven by loyalty programs and availability of multiple product verticals within one platform.

Spending patterns reveal moderate average session lengths but high frequency among dedicated bettors, especially in sports markets correlated with European football leagues and major tournaments.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

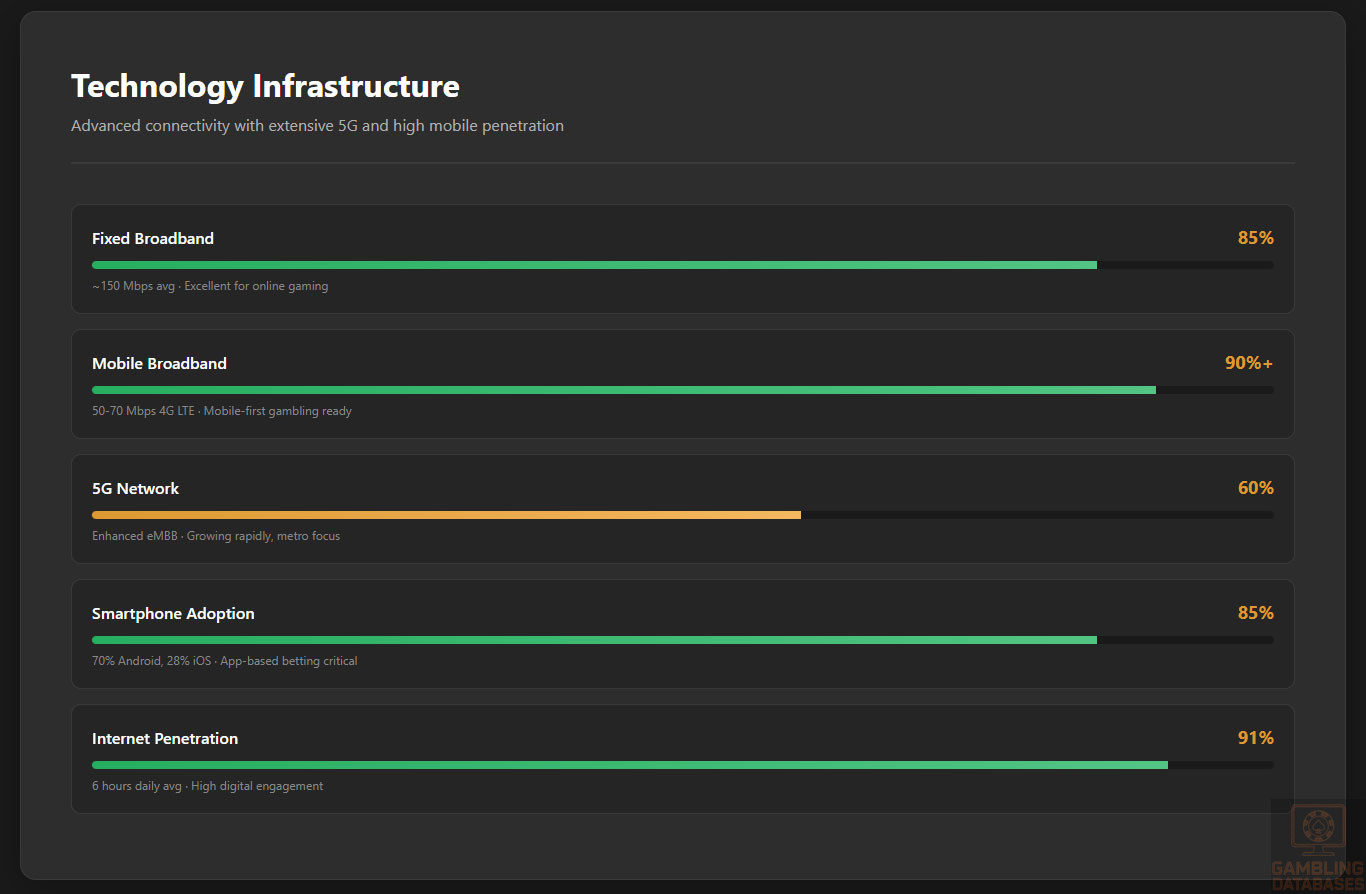

Hungary benefits from extensive internet coverage with broadband and mobile network access highly developed across urban and rural regions. Fixed broadband penetration stands at approximately 85% of households, while mobile broadband usage surpasses 90%.

Average fixed broadband speeds reach around 150 Mbps, supporting data-intensive applications, with mobile networks offering consistent 4G LTE speeds averaging 50-70 Mbps. Significant investments in fiber-optic networks and backbone infrastructure have enhanced reliability and reduced latency, key for latency-sensitive iGaming operations.

5G and Future Technology Deployment

Hungary has aggressively deployed 5G networks, with coverage currently exceeding 60% of the population, focusing primarily on metropolitan and industrial centers. The rollout includes urban hubs like Budapest, Debrecen, and Szeged, with ongoing expansion planned to reach national saturation by 2027.

Leading mobile network operators (MNOs) compete aggressively, deploying infrastructure that supports enhanced mobile broadband (eMBB) and low latency critical for real-time betting and immersive gaming experiences.

Mobile Technology Ecosystem

The mobile ecosystem is characterized by high smartphone penetration, which reached around 85% in 2025. Consumers favor mid to high-end Android devices, comprising roughly 70% of the market, with iOS representing 28%, supporting extensive app-based gambling usage.

- Magyar Telekom (T-Mobile) – Largest market share approx. 40%

- Telenor Hungary – Around 25% market share

- Vodafone Hungary – 22% market share

- UPC Magyarország – Integrated telecom services including mobile

- Yettel Hungary – Newer brand consolidating various operators

Quality of mobile data networks is high, with average data costs moderately competitive compared to EU averages. Mobile device usage patterns favor apps integrating seamless payment and gaming functionalities.

Financial Services and Payment Infrastructure

Hungary’s banking sector is mature and competitive, offering full digital banking services. Major banks provide broad account penetration, digital wallets, and instant payment capabilities, essential for supporting real-time gambling transactions.

- OTP Bank – Hungary’s largest bank with extensive retail and corporate services

- K&H Bank – Strong digital banking presence and SME focus

- Raiffeisen Bank – Regional European bank offering advanced e-payment solutions

- Erste Bank Hungary – Leading in online and mobile banking adoption

- UniCredit Bank Hungary – Specialized in corporate and investment banking

Payment methods cover standard cards, e-wallets, bank transfers, and emerging contactless and mobile wallet payments. Cryptocurrency remains niche but is gradually growing in acceptance in digital entertainment sectors.

- Credit and Debit Cards (Visa, MasterCard, Maestro)

- E-wallets (Skrill, Neteller, PayPal)

- Bank Transfer and Instant Payment systems (GIRO, SEPA)

- Mobile Payment Systems (Apple Pay, Google Pay)

- Cryptocurrency (Bitcoin, Ethereum) increasingly accepted by select operators

E-commerce and Digital Economy

The Hungarian e-commerce market continues to expand explosively, with turnover estimated to exceed €5 billion in 2025. High digital trust, coupled with widespread internet access, drives consumer adoption of online retail, streaming, and subscription services.

This digital economy growth directly benefits iGaming operators by providing digitally native consumers accustomed to online payments and mobile interfaces, facilitating rapid scaling and market penetration.

Business Environment and Regulatory Framework

Hungary ranks favorably in the World Bank’s Ease of Doing Business report, with simplified company registration and transparent legal systems. Strategic location within the EU and proactive foreign investment policies offer solid foundations for market entry.

The business registration process follows a standardized pathway starting with document preparation, submission to the Company Registry, tax registration, bank account opening, and final certification. Each phase is digitally integrated to reduce processing times.

- Prepare and notarize incorporation documents (2-3 weeks)

- Submit to Company Registry (5-7 business days)

- Tax Authority registration and obtain tax ID (3-5 days)

- Open corporate bank account and deposit minimum capital (1-2 weeks)

- Receive final registration confirmation and certificate (2-3 days)

Operators commonly choose between limited liability companies (LLCs), corporations, or branch offices. LLCs dominate due to flexibility and limited shareholder liability, while branches are used for existing foreign companies expanding locally.

- LLC: Limited liability, standalone legal entity preferred for iGaming

- Corporation: Suitable for larger-scale operations with complex ownership

- Branch Office: Extension of foreign parent company, subject to stricter control

Registration requires a set of essential documents:

- Articles of incorporation and company statutes

- Shareholder and director identification documents

- Proof of registered office address in Hungary

- Bank account confirmation and capital deposit evidence

- Tax or social security registration filings

- Compliance and AML policies where applicable

Taxation Framework

Corporate income tax is levied at a flat 9%, one of the lowest in the EU, fostering investment attractiveness. Several special economic zones provide tax incentives and holiday periods encouraging business expansion.

Hungary maintains bilateral tax treaties with numerous countries, fostering avoidance of double taxation and facilitating cross-border business.

- Austria

- Germany

- Slovakia

- Poland

- United Kingdom

- France

- Italy

- Czech Republic

- Romania

- China

Personal income tax is a flat rate of 15% with social security contributions paid separately. Tax residency rules require individuals spending more than 183 days in Hungary annually to declare global income.

Market Entry Considerations

Successful market entry involves careful regulatory alignment, establishing local presence, and partnerships with established providers for payments and marketing. Leveraging technology platforms with multilingual and customer support capabilities is crucial.

- Form strategic alliances with local partners and payment providers

- Invest in certified gaming platforms meeting regulatory standards

- Implement comprehensive player protection and compliance systems

- Develop localized marketing strategies aligned with cultural preferences

- Plan for scalable operations to navigate future regulatory changes

Typical operational costs include regulatory fees, technology investments, marketing budgets, staffing, and compliance expenditures. The average timeline from market entry preparations to full launch spans 6-12 months.

| Cost Category | Estimated Cost (€) |

|---|---|

| License Application and Fees | 1,600,000 |

| Platform Integration and Certification | 350,000 |

| Marketing and Customer Acquisition | 500,000 |

| Compliance and Legal Services | 200,000 |

| Staffing and Local Operations | 300,000 annually |

Regulatory complexity and competitive intensity require diligent compliance management and user experience optimization. Exit strategies typically involve license transfer or asset sales, subject to regulator approval and market conditions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Hungary?

Online gambling is legal but strictly regulated by the Supervisory Authority for Regulatory Affairs. Licensed operators must comply with local registration, technical, and financial requirements, including hosting servers domestically and adhering to player protection mandates. Unlicensed operations are prohibited and actively blocked.

2. What types of gambling licenses are available and what do they cover?

Hungary offers licenses covering land-based casinos, online sports betting, online casino games, lotteries, and slot machine operation. A unified licensing system was introduced recently to simplify access across verticals. Each license type has distinct tax rates, operational conditions, and compliance requirements tailored to the activity.

3. How much does an iGaming license cost and how long does it take to obtain?

The licensing fee is approximately €1.6 million with a non-refundable application fee of around €27,000. The process, including document preparation, audits, and approvals, takes 6 to 12 months depending on compliance readiness and completeness of applications.

4. Can foreign companies obtain a gambling license?

Yes, but foreign companies must establish a locally registered entity and infrastructure within Hungary. Operators are subject to stringent checks on ownership, financial soundness, and operational capabilities, ensuring transparency and local accountability.

5. What are the tax obligations for iGaming operators?

Operators pay Gross Gaming Revenue taxes, varying by segment: 15% for online casinos and sports betting, and up to 30% for land-based casinos. Corporate income tax is a flat 9%. Operators also incur fixed device taxes and license renewal fees depending on activity and scale.

6. Are gambling winnings taxed for players?

Players’ gambling winnings are taxed at a flat 15% rate, withheld by operators at the source. This applies regardless of winning size, simplifying player tax compliance.

7. What are the typical operational costs for running an online casino/sportsbook?

Costs include licensing fees, technology and platform integration, customer acquisition, compliance staffing, payment processing charges, and marketing. Technology and regulatory compliance combined typically account for 30-40% of total operational expenses.

8. What is the expected ROI timeline for entering this market?

Return on investment typically occurs within 2 to 4 years, depending on market penetration, operational efficiency, and marketing effectiveness. Initial heavy investment in licensing and customer acquisition is required.

9. What are the local presence requirements for operators?

Operators must have a locally registered company and host gambling servers within Hungary. Additionally, compliance officers resident in the country are required to liaise with authorities and manage ongoing regulatory obligations.

10. What payment methods are available and recommended?

Recommended payment methods include credit/debit cards, e-wallets like Skrill and Neteller, bank transfers, and mobile payments such as Apple Pay and Google Pay. Cryptocurrency use is emerging but still not widespread.

11. What are the advertising and marketing restrictions?

Advertising is permitted only on licensed channels with mandatory responsible gambling messaging. Promotions must avoid targeting minors and vulnerable persons. Restrictions apply on timing, content, and bonus offerings to limit excessive gambling inducement.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion tools, deposit and loss limits, and provide access to support resources. Regular reporting to regulators on player protection activities is required to ensure compliance and social responsibility.

13. How large is the iGaming market and what is the growth potential?

The Hungarian iGaming market size currently exceeds €560 million in annual online revenue, with total gambling revenues reaching €1.56 billion. Projected CAGR of 6-8% reflects strong growth potential driven by market liberalization and digital adoption.

14. Who are the main competitors and what is their market share?

Key players include legacy state operators transitioning alongside licensed private companies specializing in sports betting and casino games. Market share distribution remains dynamic due to recent regulatory changes fostering increased competition and foreign entry.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-optimized platforms offering diverse gaming verticals, including sports betting, casino slots, and lottery products. Spending tends to peak on weekends and during major sports events, with moderate session lengths and high retention driven by loyalty incentives.

16. What are the key success factors and main challenges for new entrants?

Success depends on local regulatory compliance, strong customer acquisition strategies, quality platform technology, comprehensive responsible gambling policies, and cultural adaptation. Key challenges include navigating licensing complexity, competition from established players, and managing evolving regulatory scrutiny.

Sources and References

- Hungary Gambling Regulatory Authority – Official Website – https://sztfh.gov.hu

- National Statistical Office of Hungary – Population and Demographic Data 2024 – https://ksh.hu

- Central Bank of Hungary – Financial and Payment Systems Reports – https://mnb.hu

- Hungarian Ministry of Finance – Tax and Licensing Regulations – https://pm.gov.hu

- World Bank – Doing Business Report Hungary 2024 – https://worldbank.org

- International Telecommunication Union – Hungary ICT Statistics 2024 – https://itu.int

- Global Gaming Industry Report 2024 – European Gaming & Betting Association

- Hungarian Tax Authority Publications – 2025 Guidelines

- European Commission – Digital Economy and Society Index (DESI) 2024

- Magyar Telekom Annual Infrastructure Report 2024

- Mobile Network Operator Market Share Reports Hungary 2025

- Hungarian Data Protection Authority – GDPR Compliance Guidelines

- Hungarian Ministry of Human Capacities – Education & Workforce Data 2025

- Hungarian Gambling Market Research Report 2025 – iGaming Today

- Legal Guides: Gambling Laws in Hungary, CMS Expert Guide 2024

- Media Reports on Hungary Gambling Regulation Changes 2023-2025

- Hungarian E-commerce Association – Market Statistics 2025

- European Lotteries Association Reports 2024

- Hungarian Financial Supervisory Authority – Licensing and Compliance Updates

- Industry Whitepapers on iGaming Market Entry – Accace 2025

- Hungarian Social Services – Problem Gambling Programs

- Telco Operator Annual Reports 2024 (Magyar Telekom, Vodafone, Telenor)

- International Monetary Fund – Hungary Economic Outlook 2025

- OECD – Economic Surveys: Hungary 2024

- Hungarian Tax Treaties Database – Ministry of Foreign Affairs

- Hungary Digital Payment Trends – Consulting Reports 2025

- Consumer Market Research Hungary – Digital Behavior 2024

- Gaming Platform Providers Regional Market Data 2025

- International Legal Reviews on iGaming Licensing – 2025

- Hungarian Data Privacy and Cybersecurity Frameworks

- EU Reports on Cross-Border Gambling Operations and Compliance

🎯 Gambling Databases Country Rating: Hungary

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | 🟡 Moderate – Accessible but expensive with significant barriers |

| Player Access Score | 7.5/10 | 🟡 Partially Legal – Sports betting fully legal, online casinos transitioning from monopoly |

| Overall Market Attractiveness | 6.7/10 | 🟡 Moderately Attractive – Small market with high entry costs but improving regulatory framework |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- EXTREMELY HIGH ENTRY COSTS: Licensing fee of HUF 600 million (~€1.6 million) plus HUF 10 million application fee (~€27,000) creates one of Europe’s most expensive licensing regimes

- MASSIVE CAPITAL REQUIREMENT: HUF 1 billion (~€2.7 million) minimum share capital must be maintained, effectively requiring €4.3+ million just to apply

- ONLINE CASINO HISTORICALLY MONOPOLIZED: Until recently, online casinos operated under state monopoly. While liberalization is ongoing (unified licensing expected 2025), market remains dominated by established state-connected players

- MANDATORY LOCAL INFRASTRUCTURE: Company registration AND gambling servers must be physically located in Hungary, eliminating remote operation possibilities and adding significant operational costs

- SMALL MARKET SIZE: With only 9.6 million population and €563 million online gambling revenue (2024), market is too small for multiple operators to achieve profitability at these entry costs

- 5-YEAR EU EXPERIENCE REQUIREMENT: Operators must demonstrate minimum five years of licensed gambling operation within EEA, eliminating newer operators and non-European companies

- BLACK MARKET REMAINS SIGNIFICANT: Estimated €125-250 million illegal gambling market indicates enforcement challenges and competition from unlicensed operators

- REGULATORY TRANSITION UNCERTAINTY: Unified licensing system “expected” in 2025 but not yet implemented, creating regulatory uncertainty for new entrants

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.0/3.0 | Starting: 3.0 points (full legality framework exists) Sports betting fully legal and open to foreign operators since 2023 (+1.5 base) Online casinos transitioning from state monopoly, liberalization ongoing (+1.0 partial credit) DEDUCTIONS: -0.5: Historical state monopoly on online casinos creates entrenched competition disadvantage -0.5: Unified licensing system still “expected” for 2025, not yet implemented – regulatory uncertainty Black market €125-250M indicates incomplete enforcement (noted but not deducted as enforcement exists) FINAL: 2.0/3.0 |

| Licensing Process | 25% | 0.75/2.5 | Starting: 2.0 points (licensing available, defined process) CRITICAL DEDUCTIONS: -0.5: Application + licensing fees total €1.627 million (HUF 610M) – among highest in Europe -0.25: HUF 1 billion (~€2.7M) minimum capital requirement – excessive barrier to entry -0.25: Mandatory 5-year EEA licensed experience eliminates newer operators -0.25: Complex technical audits, financial reviews, background checks extend timeline significantly Process takes several months with extensive documentation requirements Foreign ownership permitted but heavily scrutinized adds delays FINAL: 0.75/2.5 |

| Taxation & Costs | 20% | 1.25/2.0 | Starting: 2.0 points (15% GGR baseline) Online casino GGR tax: 15% (+1.5 base good rate) Sports betting GGR tax: 15% (+1.5 base good rate) Corporate income tax: 9% flat (one of EU’s lowest, +0.5 bonus) DEDUCTIONS: -0.5: Combined effective tax rate 15% GGR + 9% corporate on profits = ~23-24% total burden -0.25: Slot machine monthly tax HUF 500,000 per device if operating land-based alongside online -0.25: License renewal fees and annual compliance costs add ongoing expenses Total estimated market entry costs €2.95 million (licensing + platform + initial marketing + compliance) High operational costs due to mandatory local presence and staffing FINAL: 1.25/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Starting: 1.5 points (baseline) CRITICAL DEDUCTIONS: -0.5: MANDATORY company registration in Hungary – no remote operation possible -0.25: MANDATORY server hosting within Hungary – significant infrastructure costs and technical complexity -0.25: Dedicated local compliance officers and representatives required – ongoing staff costs Comprehensive KYC/AML systems aligned with EU directives required Age verification, self-exclusion, deposit limits mandatory Monthly financial reporting, quarterly AML reports, annual external audits required GDPR compliance adds additional data management requirements No credit card or cryptocurrency bans (positive, no additional deduction) FINAL: 0.5/1.5 |

| Market Environment | 10% | 0.75/1.0 | Starting: 1.0 point (baseline) Hungary ranks favorably in World Bank Ease of Doing Business – stable regulatory environment (+0.7 base) DEDUCTIONS: -0.25: Small market (9.6M population, €563M online revenue) limits scaling opportunities -0.25: Recent transition from monopoly creates competitive disadvantage for new entrants vs established players Advertising restricted to authorized channels with mandatory responsible gambling messaging Market expected 6-8% CAGR through 2029 (positive growth but from small base) Black market €125-250M indicates incomplete market capture FINAL: 0.75/1.0 |

| TOTAL OPERATOR EASE SCORE | 100% | 5.8/10 | Sum: (2.0×0.30) + (0.75×0.25) + (1.25×0.20) + (0.5×0.15) + (0.75×0.10) = 0.60 + 0.19 + 0.25 + 0.08 + 0.08 = 5.8/10 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.0/4.0 | Starting: 4.0 points (full legality) Sports betting fully legal and accessible since 2023 (+2.0) Online casinos legal but historically monopolized, liberalization ongoing (+1.5) Lottery and land-based gambling fully legal (+0.5) DEDUCTIONS: -0.5: Online casino market dominated by state-connected operators limits true player choice -0.5: Historical monopoly period means limited licensed casino options currently available Players face 15% tax on winnings (withheld by operators) – transparent but reduces net returns No penalties for using licensed operators FINAL: 3.0/4.0 |

| Practical Accessibility | 30% | 2.5/3.0 | Starting: 3.0 points (baseline full access) Multiple payment methods available: credit/debit cards (58%), bank transfers (27%), e-wallets (12%) Mobile payment solutions (Apple Pay, Google Pay) increasingly adopted Internet penetration 91%, mobile penetration 130% DEDUCTIONS: -0.25: Limited licensed online casino operators due to recent monopoly transition reduces practical choices -0.25: Cryptocurrency adoption under 5% and still emerging, not fully mainstream payment option Active website blocking of unlicensed operators protects legal market but limits offshore alternatives No VPN required for licensed sites Strong payment infrastructure supports transactions FINAL: 2.5/3.0 |

| Player Penalties | 20% | 2.0/2.0 | Starting: 2.0 points (no player penalties) Players face NO penalties for using licensed operators No criminal liability for gambling on regulated platforms 15% withholding tax on winnings is administrative, not punitive Players using unlicensed offshore sites face access blocking (ISP level) but no personal fines or prosecution Strong player protection measures including self-exclusion, deposit limits NO DEDUCTIONS FINAL: 2.0/2.0 |

| Market Availability | 10% | 0.5/1.0 | Starting: 1.0 point (baseline) DEDUCTIONS: -0.5: Limited number of licensed online casino operators due to recent liberalization from state monopoly Sports betting has multiple licensed operators since 2023 reforms (+0.3 partial credit) Land-based casinos, sports betting outlets widely available Market transitioning toward unified licensing (expected 2025) should increase operator availability Current licensed operator count unclear but historically concentrated FINAL: 0.5/1.0 |

| TOTAL PLAYER ACCESS SCORE | 100% | 7.5/10 | Sum: (3.0×0.40) + (2.5×0.30) + (2.0×0.20) + (0.5×0.10) = 1.20 + 0.75 + 0.40 + 0.05 = 7.5/10 |

🔍 Key Highlights

Strengths

- Genuine Regulatory Liberalization: Hungary actively transitioning from state monopoly to competitive market, with sports betting already open since 2023 and unified licensing expected 2025

- EU-Aligned Framework: Comprehensive player protection, KYC/AML standards, GDPR compliance creates professional, trustworthy regulatory environment

- Low Corporate Tax: 9% flat corporate income tax among lowest in EU, improving net profitability for successful operators

- Reasonable GGR Tax: 15% GGR tax for online sports betting and casinos competitive compared to Western European markets (UK 21%, Germany 5.3% + other taxes)

- High Digital Penetration: 91% internet penetration, 85% smartphone adoption, 130% mobile SIM density creates digitally native consumer base ready for online gambling

- Stable Political Environment: Parliamentary republic with consistent pro-business policies and transparent legal framework

- Growing Market: 6-8% CAGR projected through 2029, ARPU increasing from €1,104 (2025) to €1,430 (2029)

- No Player Penalties: Players face no prosecution or fines for using licensed operators, encouraging legal market participation

⛔️ CRITICAL RISKS AND CHALLENGES

- [Prohibitive Entry Costs]: €1.627M licensing fees + €2.7M minimum capital = €4.3+ million required BEFORE operations begin. Among Europe’s highest barriers. Only viable for well-capitalized operators with €5-10M+ budgets.

- [Market Size Economics]: Total online gambling market only €563M (2024) across 9.6M population. With 6-8 operators sharing market, individual operator revenues likely €50-100M maximum. At these entry costs, ROI timeline extends to 3-5+ years minimum.

- [Monopoly Legacy Competition]: State-connected operators dominated online casinos until recently, maintaining brand recognition, customer databases, and infrastructure advantages. New entrants face entrenched competition with established market share.

- [Mandatory Local Infrastructure]: Company registration AND server hosting in Hungary eliminates cost-efficient remote operations. Requires physical office, local staff, data center presence – adding €300-500K+ annual operational costs.

- [5-Year EEA Experience Barrier]: Requirement for minimum five years licensed operation within European Economic Area eliminates startups, non-European operators, and newer companies regardless of capital or expertise.

- [Regulatory Transition Uncertainty]: Unified licensing system “expected” 2025 but not yet implemented. Timeline, exact requirements, and fees remain uncertain. Early entrants face risk of changing rules mid-application.

- [Black Market Competition]: €125-250M illegal gambling market (18-44% of legal online market) indicates significant unlicensed competition and incomplete enforcement, potentially undercutting licensed operator revenues.

- [Limited Scaling Potential]: Small domestic market (9.6M vs Poland 38M, Germany 84M) means no economy of scale benefits. Operators cannot leverage Hungary license for broader regional expansion.

- [Customer Acquisition Costs]: While not explicitly stated, typical CEE markets show €150-400 CAC. In small, concentrated market with entrenched competitors, expect upper range €300-500+ CAC.

- [Timeline to Launch]: 6-12 months from application to operations, during which capital remains locked and market conditions may shift.

Player-Specific Issues

- Limited Licensed Casino Choices: Recent transition from state monopoly means few licensed online casino operators currently available, restricting player options

- 15% Withholding Tax: All gambling winnings taxed at 15% (operator-withheld), reducing net player returns vs. zero-tax jurisdictions

- Historic Monopoly Period: Players accustomed to single state operator may show loyalty inertia toward new entrants

- Payment Method Limitations: Cryptocurrency adoption under 5%, limiting options for crypto-preferring players

- ISP Blocking of Offshore Sites: While protecting legal market, reduces access to international operators with potentially better bonuses or game variety

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €4.3-5.0 million (€1.627M licensing + €2.7M minimum capital + €350K platform + €200K compliance + €300K initial staffing)

Monthly Operating Costs: €150,000-250,000 (local staff, server hosting, compliance, marketing, payment processing, customer support)

Effective Tax Rate on Revenue: ~23-24% total (15% GGR tax + 9% corporate tax on remaining profits = combined ~23-24% of gross revenue depending on profit margins)

Customer Acquisition Cost: €300-500 estimated (not explicitly stated in article, but typical for competitive CEE markets with entrenched players)

Realistic Revenue Potential: €50-100 million annually IF capturing 10-15% market share (optimistic scenario)

Time to Breakeven: 36-48 months minimum assuming successful market penetration and 10%+ market share achievement

Time to Positive ROI: 48-60 months realistically, potentially longer if market share targets not met

Profitability Assessment: MARGINAL TO CHALLENGING. Hungary presents a “catch-22” scenario: Entry costs are extremely high (€4.3-5M) while market size is small (€563M online total). Simple math reveals the problem: Even capturing an optimistic 15% market share yields only €84M annual revenue. After 15% GGR tax (€12.6M), operating costs (€2-3M annually), and customer acquisition (€1-2M annually for growth), net profit before corporate tax would be €66-69M – €14.6M = €51-54M, or roughly €4.2-4.5M monthly. Corporate tax takes another 9%, leaving ~€47-49M annual net profit. At this rate, recovering the initial €4.3-5M investment takes approximately 1-1.5 years IF you immediately capture 15% market share, which is unrealistic. More realistic 5-8% initial market share extends breakeven to 3-5+ years.

VIABLE ONLY for operators with: (1) €10M+ total capital budget allowing patient market development, (2) Existing European operations to amortize platform costs, (3) 5+ year investment horizon, (4) Ability to capture 10%+ market share within 24 months. AVOID if you’re a startup, have limited capital, need quick ROI, or cannot demonstrate track record.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators (Unlicensed) | HIGH | Active ISP blocking of unlicensed gambling websites, payment processor restrictions, potential regulatory fines, exclusion from Hungarian payment systems. No evidence of criminal prosecution but regulatory environment hostile to unlicensed operators. Black market persists (€125-250M) indicating incomplete enforcement, but risk increasing as regulatory framework strengthens. |

| Licensed Sports Betting/Casino Operators | MEDIUM | High entry costs (€4.3M+) create financial risk if market share targets not met. Regulatory compliance burden significant with monthly reporting, quarterly audits, annual external reviews. Local presence requirements add operational complexity. Risk of license suspension/revocation for compliance failures. Emerging regulatory framework may shift requirements during operations. |

| Affiliates/Advertisers | LOW-MEDIUM | Advertising restricted to authorized channels with mandatory responsible gambling messaging. Promotional content must be pre-approved by operators. No evidence of direct affiliate prosecution, but advertising violations could result in operator penalties cascading to affiliates. Must ensure partners are fully licensed. Promoting unlicensed operators carries reputational and potential regulatory risk. |

| Payment Processors | LOW-MEDIUM | Must verify operator licensing status before processing gambling transactions. Risk of regulatory action if processing for unlicensed operators. Strong financial compliance requirements including AML monitoring, suspicious transaction reporting. Hungarian banking sector well-regulated with EU standards. No evidence of major payment processor enforcement actions but regulatory scrutiny exists. |

| Company Directors/Executives | LOW-MEDIUM | Background checks required for key personnel during licensing. Must maintain clean criminal record and financial standing. Directors of licensed operators personally responsible for regulatory compliance. Potential liability for serious compliance failures or fraudulent activities. Hungary has strong rule of law and transparent legal system. No evidence of personal prosecution for directors of properly licensed operators, but criminal penalties exist for fraudulent gambling activities. |

🚨 Extradition and International Enforcement

Extradition Treaties: As EU member state, Hungary maintains extradition agreements with all EU countries (27 members), plus United Kingdom, United States, Canada, Australia, Switzerland, Norway. European Arrest Warrant (EAW) system enables rapid extradition within EU for serious crimes including major fraud or organized gambling crimes.

Enforcement History: No documented cases of international extradition specifically for gambling offenses from Hungary. Regulatory enforcement focused on administrative measures (ISP blocking, fines, license revocations) rather than criminal prosecution. Hungarian authorities prioritize domestic enforcement against unlicensed land-based venues over offshore operator prosecution.

Safe Jurisdictions: Countries WITHOUT extradition agreements with Hungary include: Russia, China, Belarus, some CIS countries (Armenia, Azerbaijan, Kazakhstan, Uzbekistan), some Middle Eastern nations. However, practical travel restrictions exist as these operators would be unable to visit EU/US/UK/Australia without arrest risk if serious charges filed.

Travel Risk: LOW for properly licensed operators complying with regulations. MEDIUM for unlicensed offshore operators – while no documented gambling-specific extraditions exist, travelers with outstanding regulatory violations or fraud charges could face arrest in EU countries or those with extradition treaties. RECOMMENDATION: Licensed operators face minimal travel risk; unlicensed operators should consult legal counsel before travel to EU/US/UK.

📋 Final Verdict

Hungary receives an Operator Ease Score of 5.8/10 and a Player Access Score of 7.5/10, resulting in an overall market attractiveness rating of 6.7/10.

HONEST ASSESSMENT: Hungary represents a moderately attractive but financially challenging market suitable only for well-capitalized, experienced European operators with patient capital. The combination of extremely high entry costs (€4.3-5M) and small market size (€563M online, 9.6M population) creates marginal economics requiring 3-5 year investment horizons. While the regulatory framework is genuinely liberalizing with professional EU-aligned standards, the legacy of state monopoly creates entrenched competition, and the €1.6M licensing fee plus €2.7M capital requirement effectively limit market entry to established international operators. The 15% GGR tax and 9% corporate tax are competitive, but mandatory local infrastructure eliminates remote operation cost efficiencies. This is NOT a market for startups, undercapitalized operators, or those seeking quick returns.

For the right operator – established European brand, €10M+ capital, 5-year horizon, multi-market strategy – Hungary offers genuine opportunity. For everyone else, look elsewhere.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major European operator with minimum €10M available capital and existing operations in 2+ EU markets to amortize platform costs

- Established brand with 5+ years licensed EEA gambling experience (mandatory requirement)

- Patient investor accepting 3-5 year timeline to profitability and positive ROI

- Multi-vertical operator planning to offer sports betting, online casino, and potentially land-based products under unified licensing (expected 2025)

- Realistic about market share: Understanding that 10-15% share is optimistic target requiring €2-3M annual marketing spend

- Prepared for local presence: Willing to establish Hungarian subsidiary, hire local staff, host servers in-country, and maintain physical office

- Looking for EU expansion foothold: Using Hungary as one piece of broader CEE regional strategy (Poland, Czech Republic, Romania)

❌ Definitely Avoid If You Are:

- Startup or newer operator: 5-year EEA licensing experience requirement eliminates new entrants regardless of capital

- Undercapitalized operator: Less than €5-7M available capital makes entry financially irresponsible given costs and breakeven timeline

- Seeking quick ROI: If you need profitability within 18-24 months, economics don’t work in Hungary’s small market

- Remote operation focused: Mandatory local company registration, server hosting, and physical presence eliminate remote operation models

- Non-European operator: Without EEA licensing history, you’re automatically disqualified from application

- Casino-only operator: While casinos are legal and liberalizing, sports betting drives major revenue. Single-vertical operators face disadvantage vs. multi-product competitors

- Offshore operator without local license: ISP blocking active, payment restrictions exist, black market tolerated at €125-250M indicates some unlicensed activity, but regulatory environment increasingly hostile with enforcement tightening

- Expecting low-competition environment: State monopoly legacy means entrenched players with brand recognition, customer databases, and operational advantages

⚠️ BOTTOM LINE: Hungary is a professional, regulated market with high barriers designed to keep out undercapitalized operators. The €4.3M entry cost in a €563M market means only 8-12 operators can realistically achieve profitability. If you’re well-capitalized, experienced, patient, and have broader European ambitions, Hungary offers legitimate opportunity. If you’re seeking easy entry, quick profits, or low-cost market testing, this market will destroy your capital. The math is brutal: spend €4-5M, wait 3-5 years, compete against entrenched state-connected operators, and hope to capture 10%+ share. Only the largest, most patient operators should apply.