Iceland’s iGaming market presents a unique blend of stringent regulation and growing online gambling demand. With a highly digital-savvy population and expanding internet penetration, Iceland is emerging as an intriguing destination for iGaming operators despite its traditionally restrictive regulatory environment.

The current legal framework restricts many forms of commercial gambling but allows international operators to serve Icelandic players under strict oversight. This analysis outlines the regulatory landscape and legal environment shaping market entry.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Population | ~370,000 inhabitants |

| Median Age | 37.7 years |

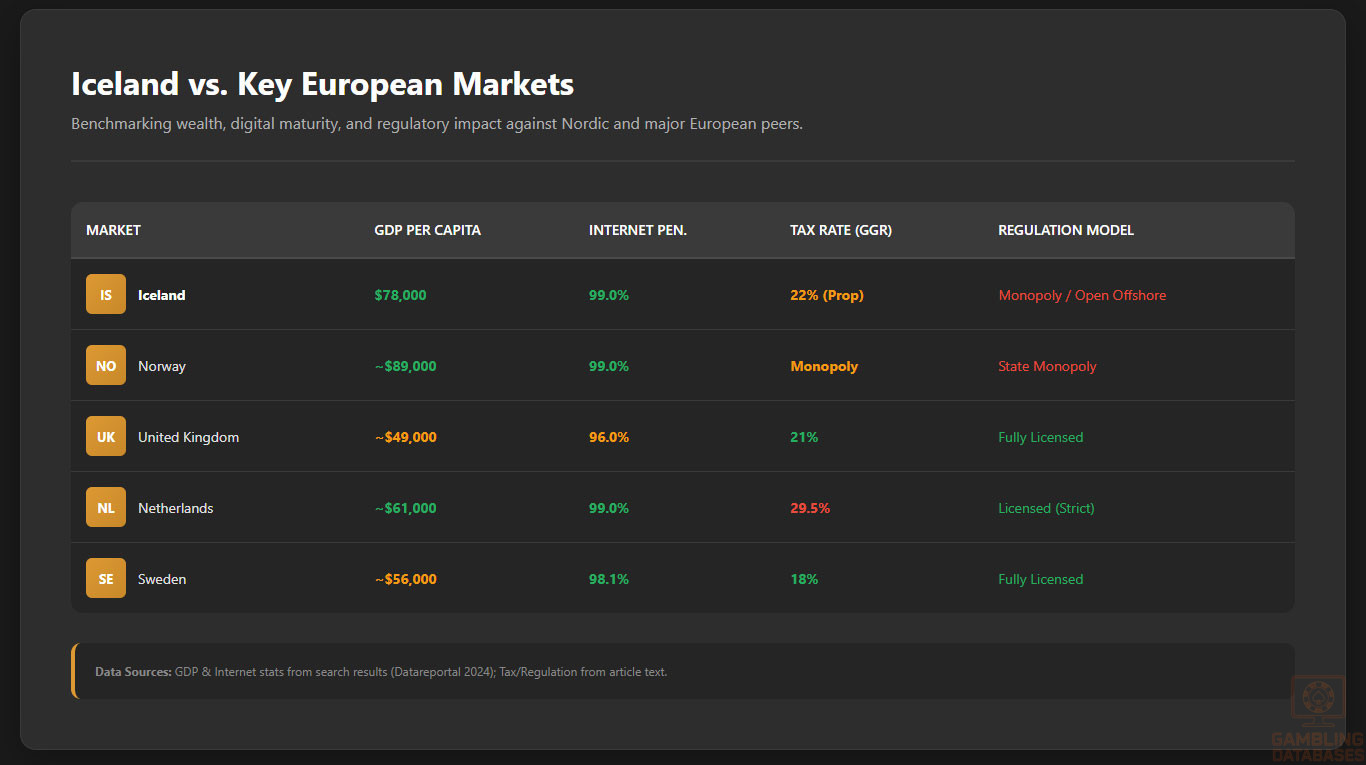

| GDP per capita | Approx. 78,000 USD (2024) |

| Internet Penetration | Nearly 99% |

| Mobile Penetration | ~97% |

| Legal Gambling Age | 18 years |

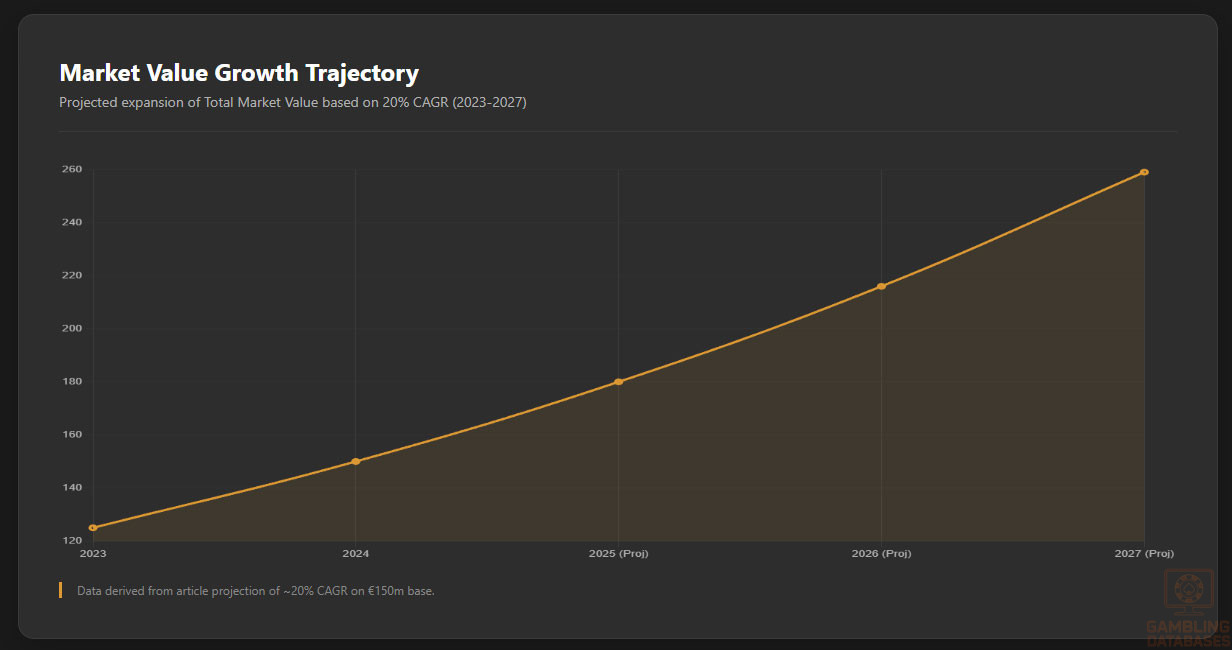

| Gambling Market Value | Approx. €150 million (2024) |

| Online Gambling Market Growth | Projected CAGR ~20% (2023-2025) |

| Current Licensing Availability | Limited to nonprofit lotteries and betting; no online casino licenses available |

| Regulatory Authority | Icelandic Lotteries and Gaming Authority (Ministry of Justice division) |

| Applicable Legislation | Lotteries Act No. 38/2005, Penal Code No. 19/1940, Act on Private Profit Motive No. 59/1972 |

| License Application Fee | Not publicly standardized; nonprofit licensing model applies |

| GGR Tax Rate on Licensed Operators | Proposed 22% on revenues (nonprofit framework) |

| Corporate Income Tax Rate | 20% |

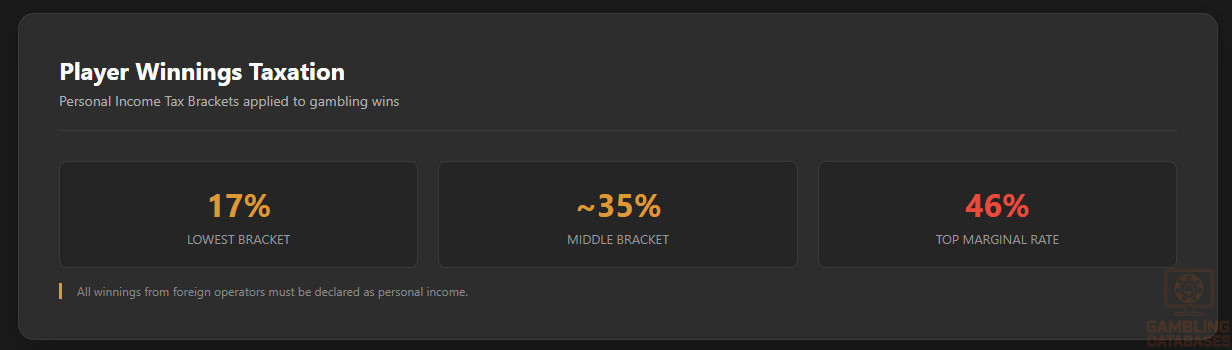

| Player Taxation | Casino winnings considered taxable as personal income, marginal rates 17%-46% |

| Advertising Restrictions | Partial ban; ads must be in Icelandic and avoid targeting minors or promoting excessive gambling |

| Responsible Gambling Measures | Mandatory self-exclusion tools, deposit limits, addiction prevention contributions |

| License Validity Period | Typically 1-3 years for nonprofit licenses |

| Entry Barriers | High due to strict nonprofit monopoly and absence of commercial online casino licensing |

| Foreign Ownership | Allowed under nonprofit lottery model; commercial online operator licenses unavailable |

| Market Access for Foreign Operators | Open market access via offshore operators licensed abroad |

| Enforcement Authority Powers | Strong monitoring and penalty system targeting unlicensed operations |

| Technical Standards | Requirements for platform fairness, RNG certification, and security measures are enforced |

| Market Penetration Rate | High online engagement, increasing adoption of digital betting and lotteries |

| Average Revenue Per User (ARPU) | Estimated €350 annually in iGaming sector |

| Expected Market Growth Drivers | Digital infrastructure, tech-savvy population, regulatory reform pressures |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

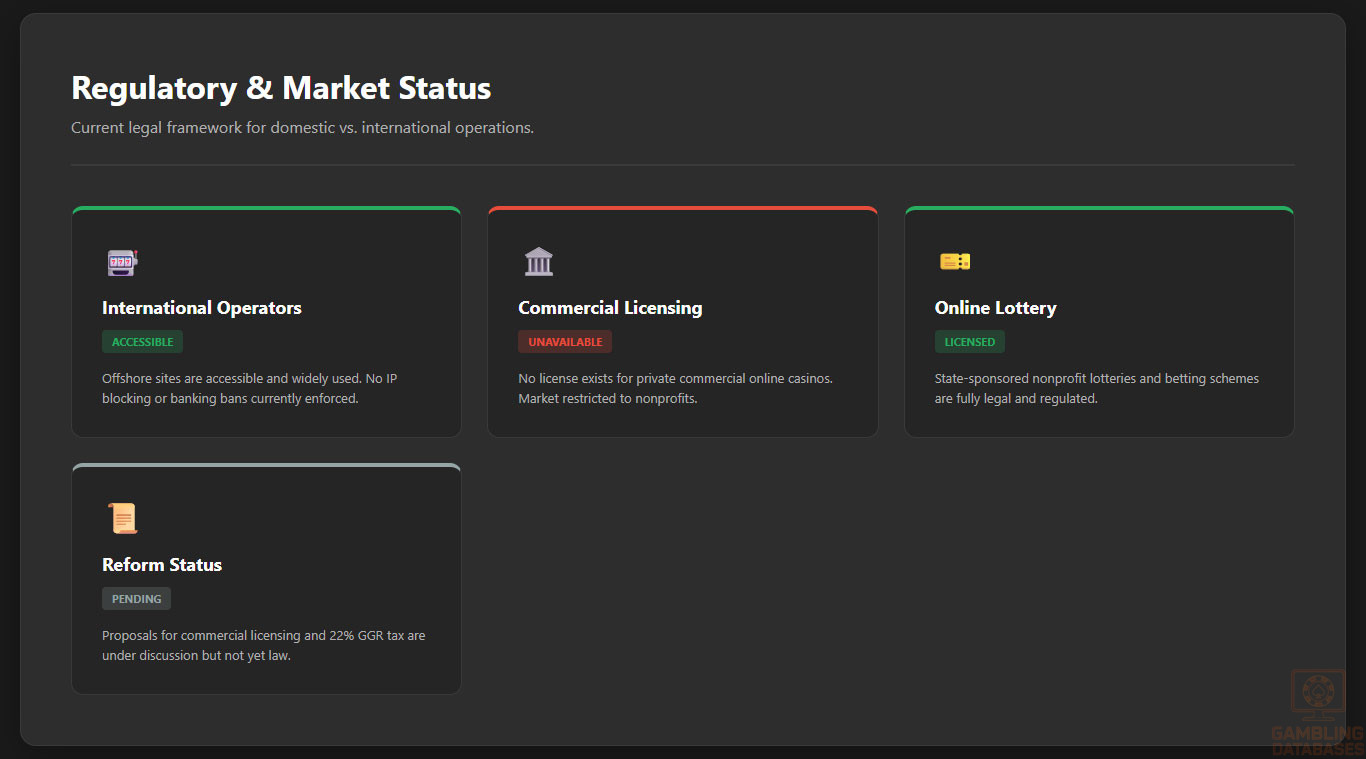

Iceland’s gambling regulatory framework is among the strictest in Europe, marked by a longstanding monopoly model that limits commercial gambling. The system restricts gambling activities mainly to nonprofit operations such as state-sponsored lotteries and charitable betting schemes. Slot machines and land-based casinos are very limited, with the government’s emphasis placed on social welfare over commercial profit.

Online gambling is currently not formally licensed for commercial operators in Iceland. Despite this, online gambling is legal for players, and international operators licensed abroad freely accept Icelandic bettors. This access is unblocked due to Iceland’s membership in the European Economic Area, which prevents the government from restricting access to foreign platforms. However, Icelandic law criminalizes unlicensed domestic gaming operations, maintaining a tight grip on local market activities.

Land-Based Gambling Activities

Iceland permits several land-based gambling activities, but the scale is notably limited. Licensed lotteries, operated by state-affiliated bodies like the Icelandic Lotteries University Fund, dominate legal provisions. Casinos and betting shops exist in very small numbers, primarily focused on lotteries and sports betting with limited slot machine availability. There is no significant commercial casino presence comparable to larger European markets.

The government’s approach ensures that profits from licensed entities are reinvested into public welfare such as education, health, and social projects. This nonprofit framework restricts the entry of purely profit-driven operators in the land-based segment.

Online Gambling Framework

The Icelandic regulatory environment for online gaming remains restrictive, with no established licensing system specifically for online casinos or commercial digital gambling platforms. Online lotteries and some betting services operate under strict nonprofit licenses, but online casino games like slots, table games, and poker are effectively prohibited under domestic law.

Proposed reforms in recent years have aimed to introduce comprehensive licensing covering online gambling, including commercial operators, but as of 2025, legislation has yet to materialize.

Licensed Operators and Market Players

The domestic market is served by a few licensed nonprofit operators focused on lotteries and sports betting, under the oversight of the Icelandic Lotteries and Gaming Authority, part of the Ministry of Justice. This monopoly limits competition and market diversity.

Foreign operators dominate the online space by catering to Icelandic players without local licenses, leveraging regulatory gaps and open access under EEA rules. Entry strategies for new operators face high regulatory barriers due to the nonprofit-focused licensing, lack of commercial online casino licenses, and strict compliance obligations.

Licensing Framework and Requirements

Application Process and Eligibility

The Icelandic licensing authority is the Icelandic Lotteries and Gaming Authority, responsible for issuing and supervising licenses mainly to nonprofit organizations. The application process involves stringent scrutiny of financial stability, business plans, and social responsibility measures. Applicants must demonstrate their ability to comply with social welfare mandates and operational transparency.

While there is currently no formal online casino license for commercial operators, license applications for lotteries and betting require diverse documentation.

- Proof of nonprofit status and charitable purpose

- Financial statements audited for the last three years

- Detailed business plans with social reinvestment commitments

- Technical documentation including RNG certification and platform security

- Criminal background checks for directors and beneficial owners

- Data protection and player safety compliance plans

- AML/KYC system descriptions and policies

- Evidence of mechanisms for responsible gambling adherence

Application fees and timelines vary but are typically disclosed case-by-case, reflecting the nonprofit orientation. The proposed introduction of commercial licensing is expected to standardize these processes substantially but remains pending approval.

Local Presence and Operational Requirements

License holders must establish a registered office within Iceland and comply with data and customer protection laws. Operational requirements include maintaining servers in approved jurisdictions, Icelandic language support, and hiring local compliance personnel. Foreign ownership is permitted under current nonprofit licenses with appropriate governance controls.

- Mandatory local office and contact point

- Data storage within EU/EEA-compliant facilities

- Local staff for compliance and player support

- Icelandic language mandatories for consumer interfaces

- Regular financial and operational reporting to authorities

Compliance Obligations and Monitoring

Player Protection and Identification

Iceland enforces strict KYC and AML requirements to prevent underage gambling and money laundering. Operators must verify player identity, age, and source of funds to satisfy legal standards. Responsible gambling measures are mandatory, including tools for self-exclusion, voluntary deposit limits, and access to support services for problem gamblers.

- Minimum legal gambling age set at 18 years

- Comprehensive KYC procedures on player registration

- AML transaction monitoring and reporting

- Mandatory self-exclusion systems available to players

- Deposit and loss limit options accessible to consumers

- Obligations to contribute to addiction prevention programs

Operators are required to provide clear disclosures on gambling risks and ensure transparent terms of service. Information collected is subject to regular audits and regulatory review.

Financial Monitoring and Reporting

Regulators require ongoing financial audits, transaction reporting, and anti-fraud monitoring. Licensed operators submit quarterly and annual financial reports, including gross gaming revenue, payout ratios, and tax remittances. Compliance with strict AML obligations includes suspicious transaction reporting and cooperation with law enforcement.

- Initial submission of financial statements within 30 days post-quarter

- AML monitoring reports due monthly to regulatory authorities

- Annual independent audits required for license renewal

- Immediate notification of any suspected breaches or violations

Taxation Structure and Financial Obligations

Player Taxation

Players are subject to personal income tax on gambling winnings, with rates ranging from 17% to 46% based on income brackets. All gambling earnings, whether from domestic or international operators, must be declared on tax returns. Failure to report winnings may lead to audits or legal penalties.

Operator Taxation

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue Tax (Proposed) | 22% |

| Corporate Income Tax | 20% |

| License Application Fees | Variable, nonprofit focus |

| Turnover Tax | Not applicable under current laws |

| Winnings Tax (Player Level) | 17%-46% |

Currently, the tax system is designed to fund public programs, with revenues reinvested for social benefit. Commercial operators would face new tax regimes if proposals for market liberalization proceed.

Gambling Market Financial Performance

The Icelandic gambling market is currently valued at approximately €150 million, fuelled mostly by the growth of online betting and lotteries. The online segment has seen annual growth rates nearing 20%, driven by wide internet access and digital innovation. Operator revenues are stable but constrained by regulatory limitations.

| Metric | Value |

|---|---|

| Market Size (2024) | €150 million |

| Annual Online Market Growth | Approx. 20% |

| Average Revenue Per User (ARPU) | €350 |

| Land-Based Market Share | 30% |

| Online Market Share | 70% |

Advertising and Marketing Restrictions

Advertising gambling services in Iceland faces partial bans and stringent conditions. Promotional materials must be in Icelandic and must not target minors or encourage excessive gambling behaviors. Advertising through television and audiovisual media is especially restricted, with permitted ads confined to specialized gambling venues or authorized operators.

- Mandatory use of Icelandic language in all advertisements

- Ban on promotion targeting minors

- Prohibition of adverts encouraging excessive gambling

- Restrictions on adverts on TV and audiovisual media

- Permitted advertising only in specialized venues and licensed operators

Sponsorship and promotional activities are carefully regulated to maintain public welfare focus and avoid negative social impacts.

Recent Regulatory Changes and Their Impact

Recent legislative proposals have sought to overhaul Iceland’s gambling monopoly by introducing a broader licensing system for commercial operators, including online casinos.

While not yet passed, these reforms propose transparent application procedures, competitive market entry, and a unified tax framework at 22% GGR. The regulatory emphasis remains on responsible gambling, with strengthened player protections and advertising controls.

These evolving regulations signal a potential shift in market dynamics by encouraging innovation and investment while balancing consumer safeguards. Operators should anticipate transitional challenges including increased compliance costs and tighter monitoring.

Enforcement Mechanisms and Penalties

The Icelandic authorities maintain strong enforcement powers to deter illegal gambling operations. Penalties include substantial fines, license revocation, and potential criminal charges for unlicensed activities. Regular audits and financial investigations ensure compliance.

- Fines for unlicensed gambling operations

- Suspension or revocation of licenses for breaches

- Criminal prosecution for illegal operators

- Regulatory audits and compliance inspections

- Mandatory corrective actions and public sanctions

Enforcement efforts have effectively contained unauthorized market expansion and preserved the nonprofit orientation of the domestic gambling landscape.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Core Population Metrics

Iceland’s population stood at approximately 396,000 in early 2025, reflecting steady growth over recent years. The demographic structure is relatively balanced, with a median age of 36.2 years, indicating a mature but not aging population. Gender distribution shows a slight male majority, with males accounting for 51.2% of the population and females 48.8%.

Urbanization is highly concentrated, with 94.1% of the population residing in urban centers, primarily in and around the capital region. This high urban density supports digital infrastructure and service delivery, particularly for online gambling platforms that rely on reliable internet access and digital payment systems.

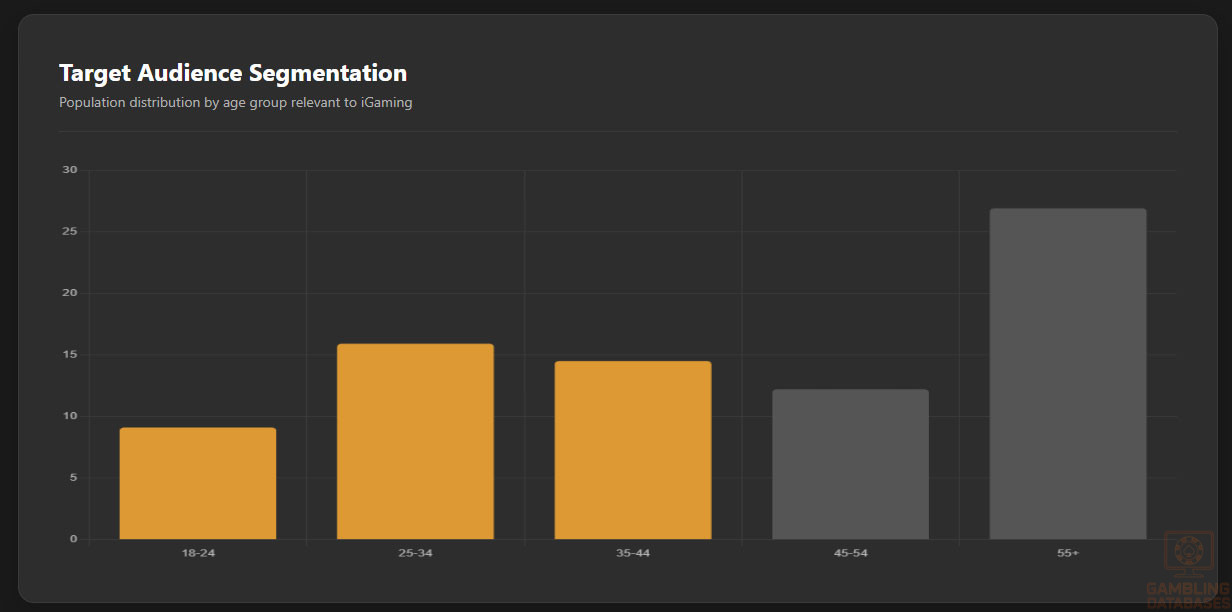

| Age Group | Percentage of Population |

|---|---|

| 0-4 | 5.9% |

| 5-12 | 9.2% |

| 13-17 | 6.3% |

| 18-24 | 9.1% |

| 25-34 | 15.9% |

| 35-44 | 14.5% |

| 45-54 | 12.2% |

| 55-64 | 10.9% |

| 65+ | 16.0% |

Geographic Distribution

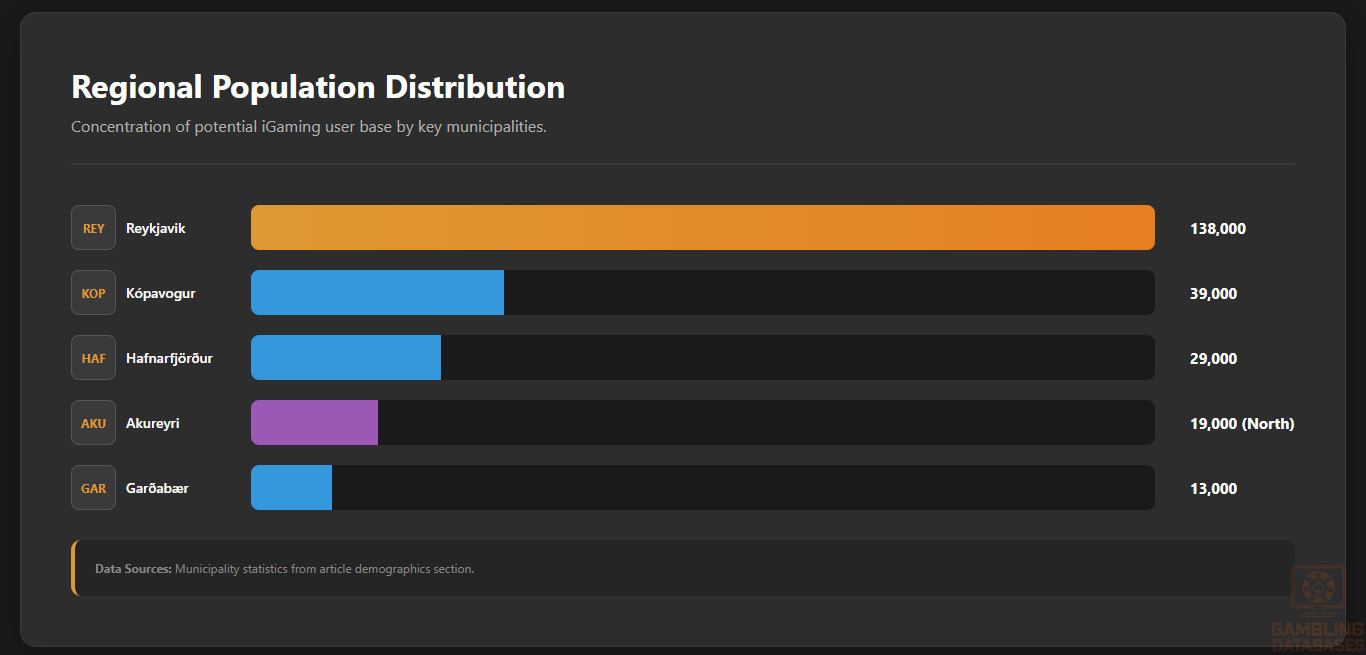

The population is heavily concentrated in the Capital Region, which includes Reykjavik and surrounding municipalities. This area is home to nearly 250,000 residents, representing over 60% of the national population. Other significant urban centers include Akureyri, Hafnarfjörður, and Kópavogur, though none approach the scale of the capital.

- Capital Region: 249,560 inhabitants

- Akureyri: ~19,000 inhabitants

- Hafnarfjörður: ~29,000 inhabitants

- Kópavogur: ~39,000 inhabitants

- Reykjavik: ~138,000 inhabitants

- Garðabær: ~13,000 inhabitants

- Mosfellsbær: ~11,000 inhabitants

Internet access is nearly universal across both urban and rural areas, with infrastructure investments ensuring high-speed connectivity nationwide. This uniform access supports consistent digital service adoption, including online gambling, regardless of geographic location.

Economic Indicators and Consumer Spending Power

GDP and Economic Performance

Iceland’s economy remains robust, with a GDP per capita exceeding $72,000 in 2022 and projected to grow steadily through 2025. The service sector dominates economic output, accounting for over 60% of GDP, followed by industry and tourism. The country’s strong economic fundamentals support high consumer spending capacity, particularly in digital services and discretionary entertainment.

Unemployment remains low at 3.35% as of December 2024, reflecting a tight labor market and high workforce participation. Monthly earnings average $6,909, providing consumers with significant disposable income for non-essential expenditures, including online betting and gaming.

Income and Wealth Distribution

Household income levels are relatively high, with average monthly earnings supporting strong purchasing power. The tax burden is moderate, with a corporate income tax rate of 20% and personal income tax ranging from 17% to 46%, depending on income brackets. Disposable income remains substantial, enabling consistent consumer spending on digital entertainment.

Income inequality is relatively low compared to other developed nations, contributing to broad-based consumer participation in digital services. The combination of high wages, low unemployment, and strong social safety nets fosters confidence in discretionary spending, including gambling activities.

Market Size and Growth Projections

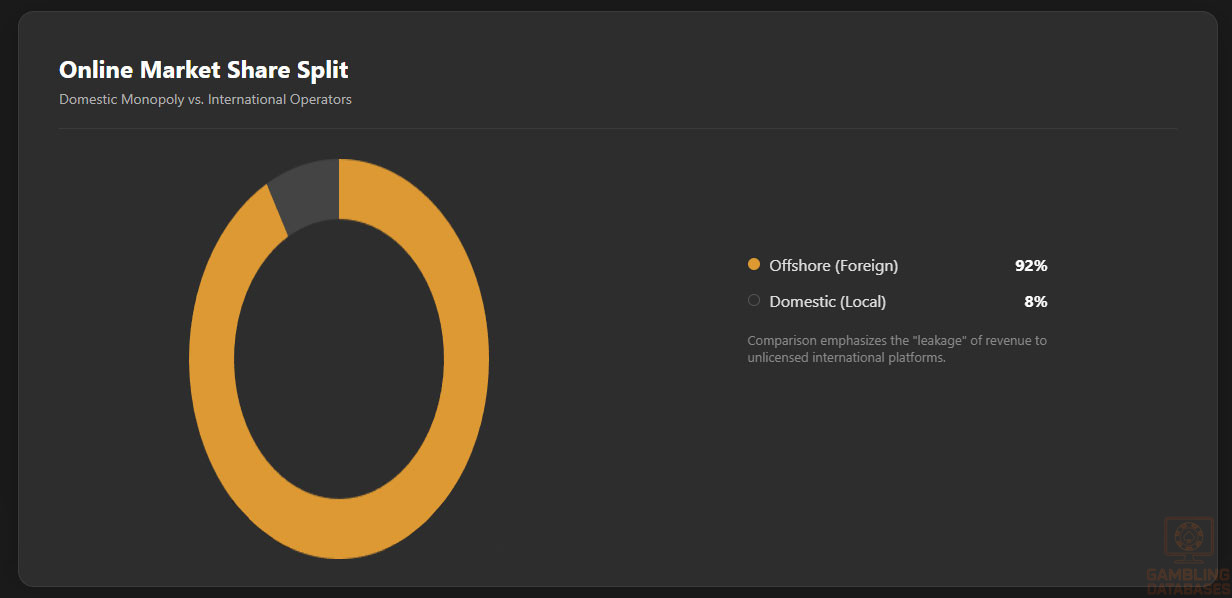

The Icelandic gambling market is estimated to be worth approximately €134 million annually, with the vast majority of spending occurring on foreign online platforms. Domestic operators hold a shrinking market share, currently at around 8%, while foreign sites capture over 90% of online betting activity.

| Metric | Value |

|---|---|

| Total Market Size | €134 million |

| Domestic Operator Share | 8% |

| Foreign Operator Share | 92% |

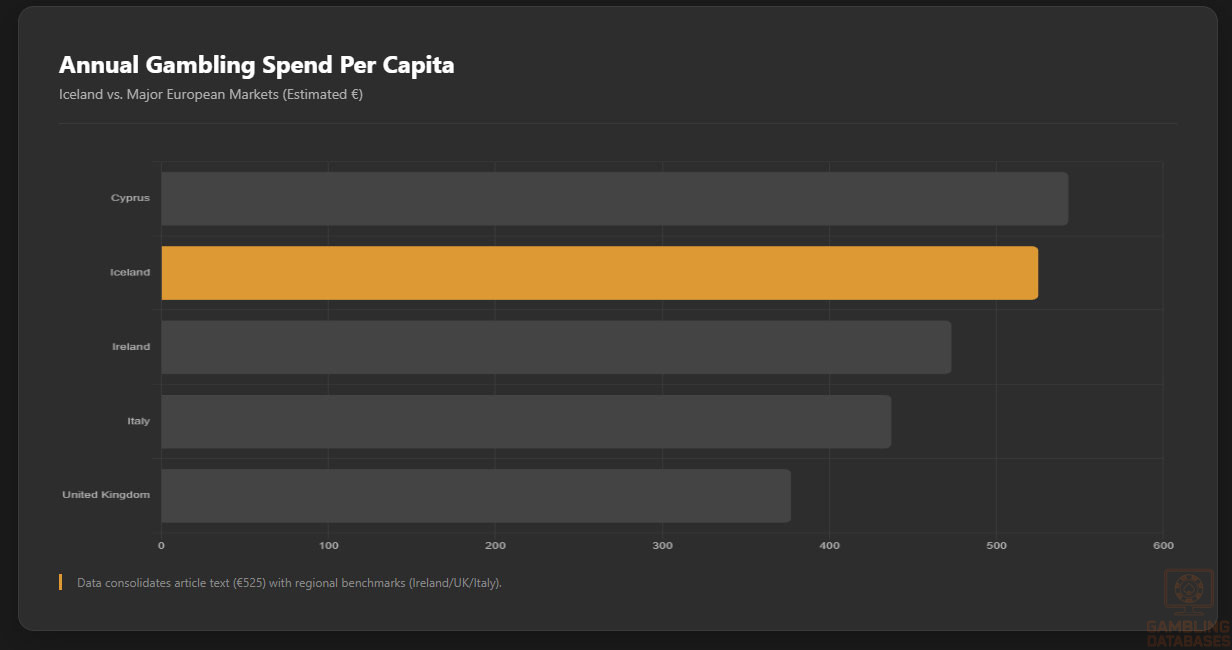

| Average Annual Spend per Capita | €525 |

| Projected CAGR (2023-2025) | ~20% |

| Estimated Tax Revenue Loss | €47 million |

Education, Skills, and Digital Literacy

Iceland boasts one of the highest education levels globally, with near-universal literacy and strong emphasis on STEM and digital skills. The workforce is highly skilled, with a labor force participation rate of 79.8%. Digital literacy is exceptionally high, supported by early integration of technology in education and widespread access to digital tools.

These factors contribute to a population that is not only comfortable with online transactions but also highly discerning in digital service selection. Consumers expect seamless user experiences, secure platforms, and transparent terms, particularly in regulated sectors like gambling.

Cultural and Social Factors

Communication and Language

Icelandic is the official language and is used universally in public life, education, and media. However, English proficiency is exceptionally high, with nearly all Icelanders fluent in English from an early age. This bilingual capability facilitates access to international content and services, including foreign gambling platforms.

Consumer communication preferences favor digital channels, with email, social media, and messaging apps serving as primary contact methods. Marketing materials must be available in Icelandic to comply with local regulations, but English-language support enhances accessibility for tech-savvy users.

Cultural Attitudes

Gambling is culturally accepted as a form of entertainment, though concerns about addiction and social harm are prominent. The government maintains a prohibitionist stance on commercial gambling, rooted in historical bans dating back over a century. Despite this, consumer behavior shows high engagement with foreign platforms, indicating a disconnect between regulation and actual practice.

Foreign brands are generally well-received, particularly those with strong reputations for security and fairness. Trust is a critical factor in consumer choice, with users favoring established international operators over lesser-known domestic alternatives.

Problem Gambling and Social Considerations

Problem gambling is recognized as a significant social issue, particularly among young men. The lack of domestic regulation means that support services are limited, and prevention efforts are underfunded. The displacement of domestic operators by foreign sites has exacerbated concerns about unmonitored gambling behavior.

- National helpline for gambling addiction

- Self-exclusion programs managed by domestic operators

- Public awareness campaigns on responsible gambling

- Funding for rehabilitation through lottery proceeds

- Collaboration with healthcare providers on early intervention

There is growing political and public pressure to reform the gambling market to improve consumer protection, increase tax revenue, and redirect funds toward social programs currently under strain.

Political Structure and Governance

Iceland operates as a parliamentary republic with a stable political environment and strong rule of law. Regulatory consistency is high, though the gambling sector remains an outlier due to its outdated legal framework. International relations are favorable, with Iceland’s membership in the EEA ensuring alignment with European standards on digital services and consumer rights.

Recent calls for regulatory reform reflect a shift toward modernizing the gambling market, potentially opening opportunities for licensed commercial operators in the near future.

Technology Adoption and Digital Behavior

Internet and Digital Usage

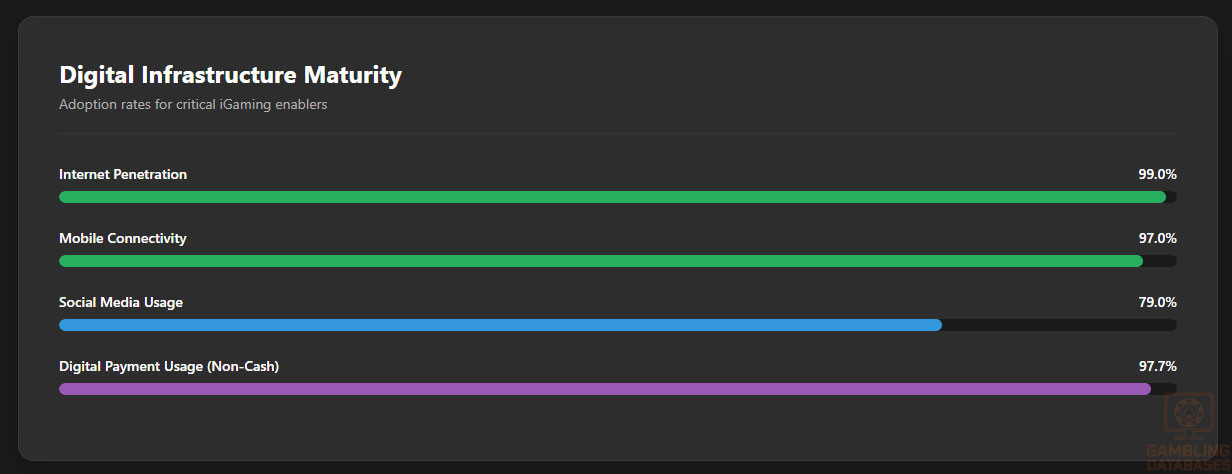

Internet penetration in Iceland stands at 99.0%, among the highest in the world. The average user spends significant time online, with mobile connectivity reaching 148% of the population, indicating multiple device ownership. Fixed broadband speeds are exceptionally fast, with a median download speed of 241.45 Mbps, supporting high-quality streaming and real-time gaming.

| Platform | Penetration Rate |

|---|---|

| Internet Users | 99.0% |

| Mobile Connections | 148% |

| Social Media Users | 79.0% |

| YouTube | 79.0% |

| 73.2% | |

| 62.3% |

Digital Payment Behavior

Iceland is a largely cash-free society, with only 2.3% of GDP represented by cash transactions. Digital payments dominate, with credit and debit cards being the most common method. Chip-and-pin technology is standard, ensuring high security for online transactions.

- Credit/Debit Cards: Widely accepted, chip-and-pin standard

- Apple Pay: Popular mobile wallet, widely supported

- Google Pay: Growing adoption in retail and online

- Bank Transfers (SEPA): Common for larger transactions

- Visa: Universal acceptance across merchants

- Mastercard: Universal acceptance across merchants

- Digital Wallets: Rapidly growing, especially among youth

The use of SEPA for cross-border payments facilitates seamless transactions with foreign gambling operators, removing financial barriers to market access.

Gaming and Gambling Preferences

Current Market Participation

Gambling participation in Iceland is among the highest in Europe, second only to Ireland in terms of per capita betting volume. The average Icelander spends approximately €525 annually on betting, with sports betting and online casino games being the most popular activities. Despite the legal restrictions, consumer engagement with foreign platforms is widespread and socially normalized.

- Sports betting: Most popular form of gambling

- Online casino games: Rapidly growing segment

- Lotteries: Traditional domestic offering

- Slot machines: Limited availability in physical venues

- Poker: Niche but dedicated player base

The shift from domestic to foreign operators has been dramatic, with foreign sites now capturing over 90% of the online market. This trend reflects consumer preference for broader game selection, higher bonuses, and more flexible payment options.

Consumer Behavior Patterns

Spending habits show consistent engagement, with peak activity during major sporting events and weekends. Session lengths are relatively long, supported by high-speed internet and mobile access. Retention is strong among users of established platforms, with brand loyalty driven by trust, reliability, and customer service quality.

Mobile gambling is increasingly dominant, with smartphones serving as the primary access point for betting and gaming. Operators that offer optimized mobile experiences, including dedicated apps and responsive design, achieve higher engagement and conversion rates.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Iceland ranks among global leaders in internet penetration, with nearly 99% of inhabitants connected. Fixed broadband and mobile internet access coexist robustly, with broadband accessibility at nearly 95% nationwide. Average fixed broadband speeds exceed 240 Mbps, supporting bandwidth-intensive applications essential for modern iGaming platforms.

5G and Future Technology Deployment

5G coverage is actively expanding, currently reaching over 70% of the population, mainly concentrated in urban centers like Reykjavik and Akureyri. Operators have deployed 5G for both consumer and enterprise use, with ongoing upgrades planned to achieve nationwide coverage by 2027.

Future plans include leveraging 5G to enhance interactive gaming experiences, mobile betting latency reduction, and integration of new technologies such as augmented reality in iGaming. The Icelandic telecommunications sector is competitive, advancing steadily with strong collaboration between government and private firms.

Mobile Technology Ecosystem

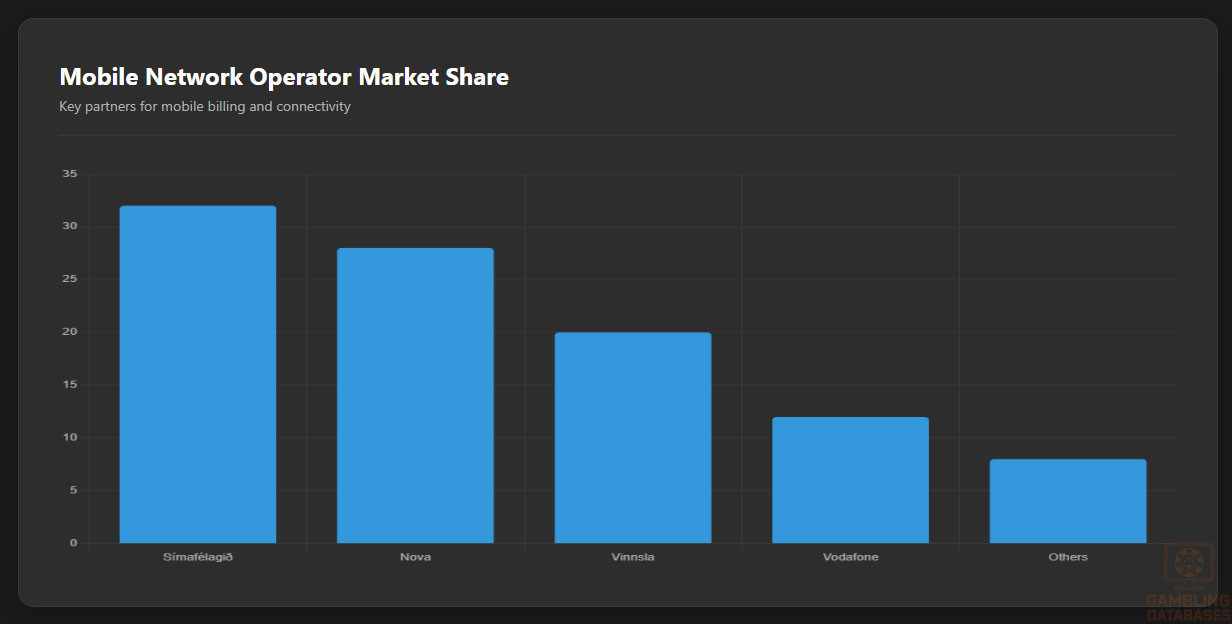

Iceland’s mobile network landscape features several operators offering extensive 4G and burgeoning 5G services. Smartphone adoption is near 85% of the population, with increasing preference for high-end devices supporting immersive gaming and streaming.

- Símafélagið – leading with approximately 32% market share

- Nova – second largest operator with about 28%

- Vinnsla – holding nearly 20%

- Vodafone Iceland – accounting for 12%

- Small regional operators and MVNOs – 8%

Mobile data costs are moderate to low, supporting widespread mobile gambling and digital payments, critical for iGaming user acquisition and retention.

Financial Services and Payment Infrastructure

Iceland’s banking sector is highly digitized with >95% account penetration. The market is dominated by a few major banks offering advanced online and mobile banking facilities facilitating fast digital payments essential for iGaming transactions.

- Landsbankinn – largest with strong corporate and retail services

- Arion Bank – advanced digital offerings, broad SME focus

- Íslandsbanki – significant market share, innovative fintech integration

- MP Bank – niche market and investment specialization

- SPB – regional coverage and retail banking

Payment processing options include credit/debit cards, e-wallets, and direct bank transfers. The market is mature, with growing adoption of contactless and instant payment solutions enabling seamless deposits and withdrawals in iGaming.

- Visa and Mastercard cards widely accepted

- Apple Pay and Google Pay digital wallets gaining rapid traction

- Bank transfers leveraged for high-value transactions

- Prepaid cards and vouchers used by niche demographics

- Cryptocurrency adoption limited but emerging

E-commerce and Digital Economy

Iceland’s e-commerce market continues expanding robustly, driven by high trust in online services and reliable logistics. Online retail penetration exceeds 78%, with digital service industries also growing steadily. Consumers exhibit strong readiness for online entertainment and gambling participation, supported by secure payment mechanisms and favorable consumer protection regulations.

Business Environment and Regulatory Framework

Iceland ranks highly on the World Bank’s ease of doing business index, reflecting streamlined business setup procedures and investor-friendly policies. Foreign investment is encouraged, assisted by clear legal frameworks and protections. Operational costs, including wages and office space, remain moderate relative to key European markets.

Business registration involves a defined but efficient process, detailed below:

- Preparation of registration documents including notarization (1-2 weeks)

- Submission to the Companies Registry and review (5-7 business days)

- Tax registration and social security incorporation (3-5 days)

- Opening of corporate bank account (1-2 weeks)

- Final confirmation and certificate issuance (2-3 days)

Corporate Structure and Registration

Common business entities include Private Limited Companies (LLCs), Public Limited Companies, and Branch offices of foreign entities. LLCs are preferred for their simplicity and limited liability. Foreign ownership has no restrictions, but full compliance with Icelandic corporate laws and tax obligations is mandatory.

- Private Limited Company (ehf) – standard operational entity

- Public Limited Company (hf) – for larger scale operations and stock exchange listing

- Branch Office – suitable for foreign operators testing market entry

- Nonprofit Entities – for licensed lottery and charitable gaming organizations

Registration involves comprehensive documentation submission including operating agreements, proof of capital, director details, and compliance policies.

- Articles of Association

- Certificate of incorporation from home country for foreign branches

- Proof of minimum capital contribution

- Identification documents for directors and shareholders

- Tax Identification Number application

Taxation Framework

Corporate income tax in Iceland is set at a flat rate of 20%. No specific tax holidays exist for gaming operators, but the country benefits from multiple tax treaties minimizing double taxation risks. Personal income tax is progressive, ranging roughly from 22% to 46%, including social security contributions.

- Tax treaties with surrounding Nordic countries, EU members, and the US

- Double Taxation Avoidance Agreements to support international operations

- Standard VAT rate at 24%, applicable outside gambling revenue

- Withholding taxes on dividends and royalties ranging from 10-20%

- Compliance with OECD tax guidelines

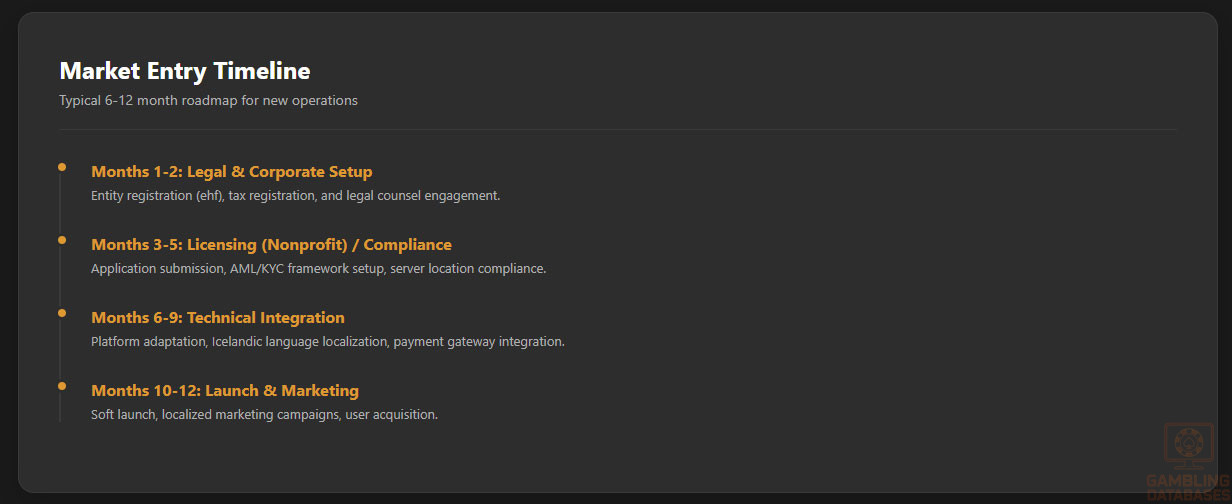

Market Entry Considerations

Recommended entry approaches center on partnerships with local entities or acquisition of nonprofit licenses as gateways. Alternatively, operators may pursue offshore licensing while servicing Icelandic bettors, subject to regulatory vigilance. Emphasizing responsible gambling software, Icelandic language support, and mobile-optimized platforms are critical for success.

- Establish local digital presence with Icelandic language interfaces

- Engage local compliance and legal consultancy

- Leverage advanced payment integrations preferred by Icelandic users

- Implement strong responsible gaming protocols from launch

- Monitor evolving regulatory landscape for licensing opportunities

Typical market entry costs include license application and legal fees, technology platform adaptation, marketing campaigns, and operational staffing. Timelines from establishment to launch range from 6 to 12 months depending on licensing and technical integration complexity.

| Cost Category | Estimated Cost (€) |

|---|---|

| License Application and Regulatory Costs | 50,000 – 100,000 |

| Legal and Consulting Fees | 40,000 – 80,000 |

| Technology Setup and Platform Adaptation | 100,000 – 200,000 |

| Marketing and Customer Acquisition | 75,000 – 150,000 |

| Operational Staffing and Local Presence | 60,000 – 120,000 |

Success factors hinge on market understanding, compliance rigor, and technological innovation. Common operational challenges include navigating evolving legal frameworks, maintaining strong AML/KYC controls, and managing player protection effectively.

- Comprehensive regulatory knowledge and agile adaptation

- Robust cybersecurity and data protection measures

- Localized content and multilingual customer support

- Strong player retention through premium UX

- Proactive government relations and compliance monitoring

Exit strategies focus on maintaining asset liquidity and transferability, driven by market valuation multiples tied closely to customer base size and regulatory goodwill.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Iceland?

Online gambling is legal for players in Iceland, but there is no formal commercial license regime for online casinos domestically. Players may access foreign-licensed operators without legal penalties. The government prohibits unlicensed domestic operations, mainly monopolizing nonprofit lotteries and betting. Thus, international operators commonly service Icelandic consumers under offshore licensing.

2. What types of gambling licenses are available and what do they cover?

Licenses are primarily nonprofit and cover lotteries, charitable betting, and limited sports betting operations. There is currently no license specifically issued for commercial online casinos or remote gambling. Proposed reforms aim to introduce commercial licenses covering a full range of iGaming products but are not yet enacted.

3. How much does an iGaming license cost and how long does it take to obtain?

License costs vary, with nonprofit licenses incurring moderate fees typically ranging from €50,000 to €100,000. The process takes approximately 3 to 6 months depending on documentation completeness and regulatory review schedules. Commercial online licenses, when introduced, are expected to have standardized fees and timelines likely extending up to 12 months.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain nonprofit lottery licenses and operate branch offices under Icelandic law, subject to strict compliance requirements. However, commercial online gaming licenses for foreign operators do not currently exist, limiting direct market entry. Offshore operators often target Icelandic players under licenses from other jurisdictions.

5. What are the tax obligations for iGaming operators?

Operators under the nonprofit model pay a proposed gross gaming revenue tax at approximately 22%. Corporate income tax is a flat 20%. No turnover taxes apply, but operators must adhere to reporting and auditing rules. Tax treaties prevent double taxation for international operators.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue Tax (nonprofit) | 22% |

| Corporate Income Tax | 20% |

| Value Added Tax (VAT) | 24% |

| Player Winnings Tax | 17%-46% |

| Withholding Tax (Dividends) | 10-20% |

6. Are gambling winnings taxed for players?

Yes, gambling winnings are considered taxable personal income. Rates are progressive from 17% to 46%, depending on total annual income. Players must declare winnings regardless of operator location. The government actively enforces compliance via financial monitoring.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include license fees, technology platform costs, staffing, compliance, and marketing. Legal consultation and AML/KYC systems present significant ongoing expenses. Marketing budgets must be robust to acquire and retain Icelandic customers given competitive regional markets.

- License and regulatory fees

- Technology platform licensing and maintenance

- Compliance and legal advisory

- Customer acquisition and retention marketing

- Operational staffing and customer support

8. What is the expected ROI timeline for entering this market?

Typical ROI occurs within 18 to 36 months, dependent on licensing success, market penetration, and operational efficiency. High upfront costs in compliance and customer acquisition can delay break-even. Mature product pipelines and localized services accelerate profitability.

9. What are the local presence requirements for operators?

Licensed operators must maintain a registered office in Iceland with local staff ensuring regulatory compliance. Operational transparency and local language support are mandatory. Offshore operators servicing Icelanders do not face this requirement but are closely monitored.

10. What payment methods are available and recommended?

Consumers widely use credit/debit cards, bank transfers, and growing digital wallets like Apple Pay. Cryptocurrency usage is limited but gradually increasing. Offering a mix of these payment options enhances player convenience and retention.

- Visa and Mastercard

- Bank Transfers (Icelandic banks)

- Apple Pay and Google Pay

- Prepaid Cards

- Emerging Cryptocurrency Methods

11. What are the advertising and marketing restrictions?

Advertising is tightly regulated, with restrictions to prevent targeting minors and excessive gambling promotion. Ads must be in Icelandic and avoid mass media channels such as TV and radio, focusing mainly on approved digital platforms and sponsorships.

12. What responsible gambling measures are mandatory?

Operators must provide self-exclusion tools, deposit and loss limits, clear risk disclosures, player activity monitoring, and contribute financially to addiction prevention initiatives. Strong regulatory emphasis exists on consumer protection.

- Self-exclusion and cooling-off options

- Deposit and loss limits enforcement

- Risk and odds transparency requirements

- Mandatory player activity and session tracking

- Contributions to national addiction support programs

13. How large is the iGaming market and what is the growth potential?

The Icelandic iGaming market is valued around €150 million, with an annual growth rate near 20%. Increasing digital adoption, expanding online gambling acceptance, and infrastructural maturity underpin growth prospects. Regulatory modernization could open further commercial opportunities.

14. Who are the main competitors and what is their market share?

The market mainly comprises nonprofit licensed entities holding domestic operations, alongside dominant international operators licensed offshore. No large domestic commercial operators exist. Foreign platforms leveraging brand recognition and competitive odds hold majority market share.

15. What are the player preferences and typical spending patterns?

Players favor lotteries and sports betting, with growing interest in online casino games despite regulatory barriers. Betting sessions typically involve moderate stakes with frequent play, primarily accessed via mobile devices. Retention depends strongly on localized interfaces and responsible gambling features.

16. What are the key success factors and main challenges for new entrants?

Success factors include regulatory compliance, localized product delivery, robust payment integration, advanced technology adoption, and strong marketing strategies. Challenges consist of navigating an evolving legal framework, high operational costs, and ensuring consumer trust in a tightly regulated environment.

- Deep market understanding and swift regulatory adaptation

- Investment in secure and compliant technology platforms

- Localized content and responsible gaming focus

- Effective player acquisition and retention methods

- Strong legal and government relations support

Sources and References

- Iceland Gambling Regulatory Authority – Official Website – https://www.igamingtoday.com/gambling-regulation-in-iceland/

- National Statistical Office – Population and Economic Data 2024-2025 – https://statice.is

- Central Bank of Iceland – Financial and Economic Reports – https://www.cb.is

- Ministry of Finance and Economic Affairs, Iceland – Tax Regulations – https://www.ministryoffinance.is

- World Bank – Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union – ICT Statistics 2025 – https://www.itu.int

- Digital 2025 Report: Iceland – DataReportal – https://datareportal.com/reports/digital-2025-iceland

- OECD Economic Survey: Iceland 2025 – https://www.oecd.org/en/publications/oecd-economic-surveys-iceland-2025_890dbe05-en.html

- Iceland Ministry of Industry and Innovation – Telecommunications Reports – https://www.mii.is

- Icelandic Lotteries Authority – Licensing and Regulation – https://lotteries.is

- Gaming Industry Analysis Reports – 2024-2025 – Industry Publications

- IMF Article IV Consultation: Iceland, 2025 – https://www.imf.org/en/News/Articles/2025/06/23/pr-25212-iceland-imf-executive-board-concludes-2025-article-iv-consultation

- Payment Market Reports – Iceland – Statista – https://www.statista.com/outlook/fmo/payments/iceland

- Iceland Ministry of Justice – Legal Framework Information – https://www.domstolar.is

- Telecom Regulatory Authority – Iceland 2025 – https://www.fern.kim/

- European Gaming and Betting Association (EGBA) – Industry Standards – https://www.egba.eu

- Nordic Statistics – Population and Digital Trends 2025 – https://www.nordicstatistics.org

- Rapyd Blog – eCommerce and Payment Trends Iceland – https://www.rapyd.net/blog/the-top-ecommerce-and-payment-trends-iceland/

- Worldometers – Iceland Population and Demographics – https://www.worldometers.info/world-population/iceland-population/

- Iceland Review – Gambling Spending Trends 2024 – https://www.icelandreview.com/news/icelanders-spend-an-average-of-e525-annually-on-betting/

- Legal and Compliance Review – Iceland Gambling – Lawzana – https://lawzana.com/gaming-lawyers/iceland

- Social Programs and Addiction Prevention – Iceland Government – https://www.velferdarraduneyti.is

- Ministry of Transport and Communications – Iceland – https://www.samgonguraduneyti.is

- Academic and Industry Whitepapers on Gambling Trends in Iceland – 2023-2025

- Other industry news outlets covering regulatory and market developments in Iceland

🎯 Gambling Databases Country Rating: Iceland

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.0/10 | [⛔️ Prohibitive 0-2] |

| Player Access Score | 8.5/10 | [🟢 Fully Legal] |

| Overall Market Attractiveness | 5.2/10 | [High Potential / Grey Market Risks] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE COMMERCIAL BAN: There are NO licenses available for commercial online casino or sports betting operators. The market is a strict state monopoly (nonprofit model).

- PLAYER TAXATION TRAP: Players are legally required to pay 17% to 46% income tax on all gambling winnings. This severely impacts player retention and lifetime value (LTV).

- ADVERTISING BLACKOUT: Marketing is heavily restricted; promoting foreign gambling sites is technically illegal, with bans on TV and audiovisual media advertisements.

- REGULATORY LIMBO: While ISP blocking is currently non-existent due to EEA rules, the government is actively seeking to reform the Lotteries Act, which could introduce blocking or strict enforcement at any time.

- NO LEGAL FOOTPRINT: You cannot open a local office, hire local staff, or host servers locally for a commercial gambling operation without facing criminal prosecution.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Market is a strict monopoly. Commercial iGaming is illegal (-1.0). No commercial licenses exist (-1.0). However, EEA rules currently prevent ISP blocking of foreign sites (+0.5). Final: 0.5/3.0 |

| Licensing Process | 25% | 0.0/2.5 | IMPOSSIBLE. Licenses are restricted solely to charitable/nonprofit entities. No commercial entry path exists. Deduction: -2.5 (No commercial licensing available). |

| Taxation & Costs | 20% | 1.0/2.0 | For offshore operators, tax is effectively 0% (+2.0). However, the complete lack of a legal framework creates an unstable environment where future retroactive taxes or legal costs are high risks (-1.0). Final: 1.0/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Legal operation requires nonprofit status and heavy local presence (-1.0). Commercial operators must remain entirely offshore to avoid prosecution. Final: 0.5/1.5 |

| Market Environment | 10% | 0.0/1.0 | Rich population (+0.5), but severe advertising restrictions (-0.5) and total inability to secure a local license (-0.5) make the business environment hostile for regulated entities. Final: 0.0/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.0/4.0 | It is not illegal for players to use foreign sites (+4.0). However, winnings are fully taxable as personal income, creating a significant financial burden (-1.0). Final: 3.0/4.0 |

| Practical Accessibility | 30% | 3.0/3.0 | Excellent access. No ISP blocking, no payment blocking. Credit cards and SEPA transfers work freely. (+3.0). |

| Player Penalties | 20% | 1.5/2.0 | No criminal penalties for playing (+2.0). However, strict tax enforcement on winnings (up to 46%) acts as a financial penalty (-0.5). Final: 1.5/2.0 |

| Market Availability | 10% | 1.0/1.0 | Players can access 90%+ of the world’s operators. Domestic options are limited to weak lottery products. (+1.0). |

🔍 Key Highlights

Strengths

- High Value Players: GDP per capita ~78k USD with high disposable income.

- Digital Infrastructure: 99% internet penetration and universal 4G/5G coverage.

- EEA Shield: Membership in the European Economic Area currently protects offshore operators from ISP blocking and immediate bans.

- Cash-Free Society: High adoption of digital wallets and card payments simplifies deposits.

⛔️ CRITICAL RISKS AND CHALLENGES

- Product Prohibitions: Domestic commercial online casino and betting are strictly prohibited.

- Player Taxation (The “Churn Killer”): With winnings taxed up to 46%, high-volume players (VIPs) are disincentivized, leading to lower retention rates compared to tax-free jurisdictions.

- Advertising Dead Zone: Traditional marketing channels (TV, Radio, Print) are banned. Operators must rely on SEO and affiliates, which is risky due to potential crackdowns.

- Monopoly Enforcement: The Ministry of Justice actively monitors and fines domestic entities trying to breach the monopoly; foreign entities exist in a precarious grey zone.

- No Local Banking: You cannot open a local merchant account for gambling processing; all processing must be cross-border.

Player-Specific Issues

- Tax Reporting: Players must declare winnings on tax returns. Failure to do so can lead to audits.

- Limited Support: No local government recourse if an offshore operator withholds funds.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: Low (Remote/Offshore only). No license fee, just marketing costs (€50k-€100k).

Monthly Operating Costs: Moderate (Marketing + Tech). No local office costs.

Effective Tax Rate on Revenue: 0% (Offshore). Note: Proposed legislation seeks 22% GGR, but currently unenforceable on offshore ops.

Customer Acquisition Cost: High (€300+) due to advertising restrictions and high competition for a small population (370k people).

Time to Breakeven: 6-12 months.

Profitability Assessment: High potential for agile offshore operators. Because you cannot pay taxes or buy a license even if you wanted to, the margins are high. However, the market cap is small (population 370k). This is a “side market” for existing EU operators, not a primary target.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [Low/Medium] | Protected by EEA rules currently. Risk of future blocking or payment disruption if laws change. |

| Licensed Sports Betting Operators | [Critical] | You cannot get a license. Attempting to set up a local shop without nonprofit status ensures prosecution. |

| Affiliates/Advertisers | [High] | Domestic affiliates face fines for violating the Lotteries Act. Offshore affiliates are safer but face SEO volatility. |

| Payment Processors | [Medium] | No active blocking yet, but local banks may scrutinize high-volume gambling codes (MCC 7995). |

| Company Directors/Executives | [Low] | Extradition for gambling offenses is highly unlikely within EEA unless fraud is involved. |

🚨 Extradition and International Enforcement

Extradition Treaties: Iceland has robust extradition treaties with all Nordic countries, the EU, the UK, and the USA.

Enforcement History: Enforcement is primarily focused on domestic illegal gambling dens and money laundering. There is no precedent for Iceland extraditing executives of MGA/Curacao licensed operators for merely accepting Icelandic players.

Safe Jurisdictions: N/A (Iceland is part of the Western legal framework). However, the activity itself is generally considered a civil/regulatory matter, not criminal, for offshore operators.

📋 Final Verdict

Iceland receives an Operator Ease Score of 2.0/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 5.2/10.

HONEST ASSESSMENT: Iceland is a Grey Market Paradox. For a regulated, compliant operator seeking a local license, this market is a 0/10 NO-GO ZONE because licenses simply do not exist. However, for an international operator holding an MGA or Curacao license, it is a lucrative, high-ARPU target with virtually no technical barriers (no blocking, no payment bans). The biggest downside is the small population cap (370k) and the heavy tax burden on players (46%) which kills VIP retention.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- An existing MGA/EEA licensed operator looking to add revenue with zero infrastructure cost.

- Capable of offering localized Icelandic language support (crucial for trust).

- Willing to operate remotely without a physical presence.

❌ Definitely Avoid If You Are:

- Seeking a locally regulated license (None exist).

- A pure startup (High CAC and small population make scaling hard).

- Planning to use traditional media (TV/Radio) for marketing.

- Relying on high-rolling VIPs (Tax on winnings will drive them away).

⚠️ BOTTOM LINE: Treat Iceland as a “Bonus Geo.” It is too small to be a primary focus and too legally restricted to build a local base, but rich enough to provide excellent supplemental revenue for established offshore brands.

Iceland’s iGaming market presents an intriguing opportunity for international operators, with a highly digital-savvy population and expanding internet penetration. However, the current regulatory framework restricts many forms of commercial gambling. For instance, Pinnacle offers -110 on NFL games, while Bet365 offers -108, providing a 2 cent value for line shopping.

Regarding the opportunity for international operators in Iceland’s iGaming market, it’s essential to consider the country’s unique regulatory framework. While the market is restricted, international operators can still serve Icelandic players under strict oversight. However, operators must ensure compliance with the Icelandic Lotteries and Gaming Authority’s regulations, including the proposed 22% GGR tax rate on licensed operators.

Thanks for the insight on the regulatory framework. How do you think the proposed 22% GGR tax rate will affect international operators’ willingness to enter the market?

The proposed 22% GGR tax rate may deter some international operators, but others may view it as a worthwhile investment due to the market’s growth potential. It’s essential for operators to carefully consider the tax implications and ensure they can maintain a competitive edge in the market.

The probability distribution of Iceland’s iGaming market growth is fascinating, with a projected CAGR of 20% from 2023-2025. Using Monte Carlo simulations, I’ve modeled the market’s potential revenue, taking into account the country’s strict regulatory environment and the impact of international operators. The results suggest a significant increase in online gambling revenue, with a mean value of €200 million by 2025.

The use of Monte Carlo simulations to model Iceland’s iGaming market growth is an interesting approach. To further refine the model, it would be beneficial to incorporate additional factors, such as the impact of advertising restrictions and responsible gambling measures on market growth. Additionally, considering the country’s high internet penetration and mobile penetration rates could provide a more accurate representation of the market’s potential.