India’s iGaming market presents a compelling opportunity fueled by a vast population, rapid digital adoption, and evolving regulations. The landmark Promotion and Regulation of Online Gaming Act, 2025, has established a national regulatory regime balancing industry growth with consumer protection. This analysis provides a comprehensive review of India’s regulatory framework and legal environment for iGaming operators seeking market entry.

| Metric | Value |

|---|---|

| Population | 1.42 billion |

| GDP (Nominal) | USD 3.7 trillion |

| GDP per Capita | Approx. USD 2,600 |

| Internet Penetration | 70.3% |

| Mobile Penetration | 83.5% |

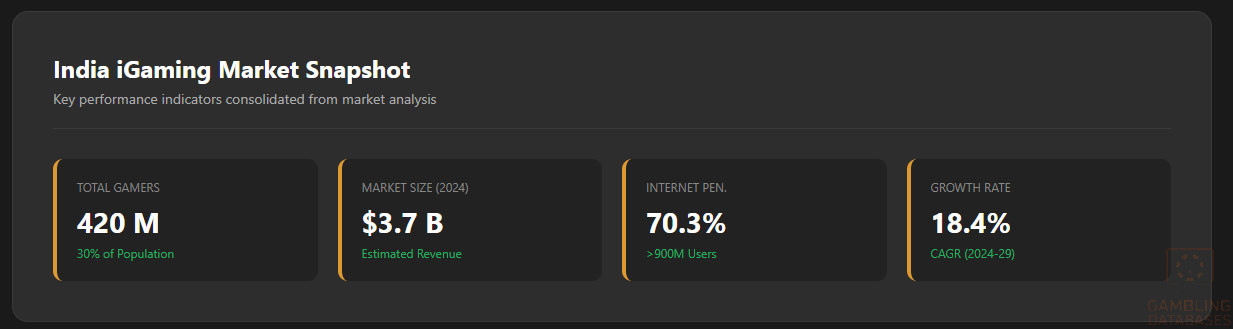

| Online Gamers | 420 million |

| iGaming Market Size (2024 est.) | USD 3.7 billion |

| Market Growth Forecast (CAGR 2024-29) | 18.4% |

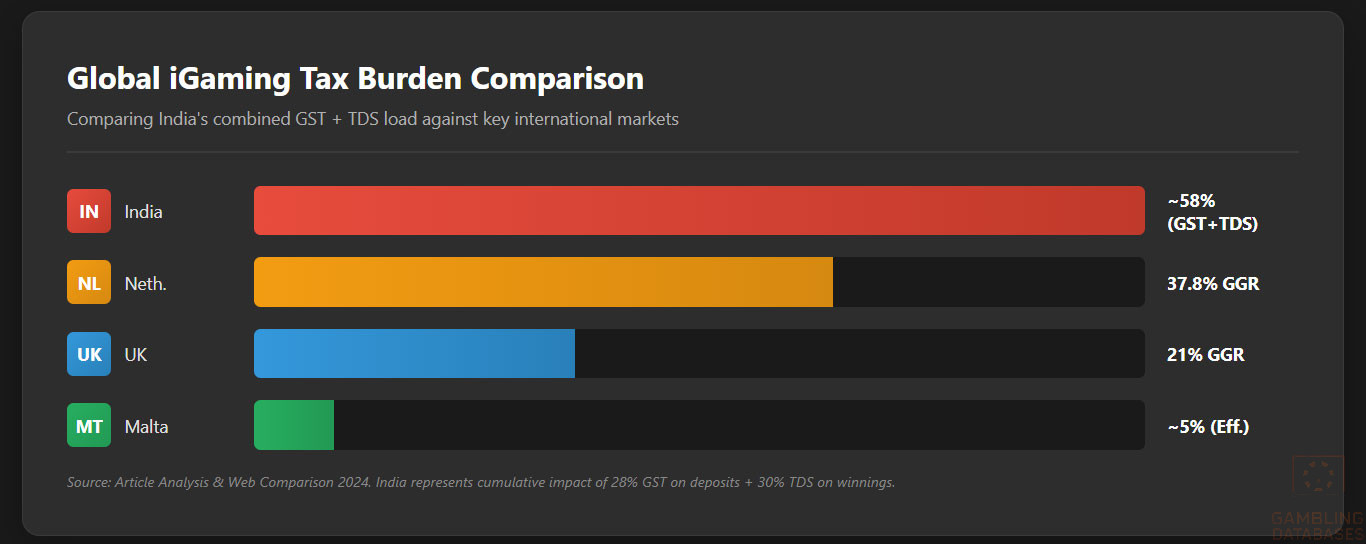

| Gross Gaming Revenue (GGR) Tax Rate | 28% (pre-Aug 2025), banned post-August 2025 for money gaming |

| Goods and Services Tax (GST) Rate | 28% on deposits/bets (until 21 Aug 2025) |

| Tax on Player Winnings | 30% flat on net winnings |

| License Application Fee | Varies by state, INR 50,000+ typical |

| Licensing Authority | National Online Gaming Commission (NOGC) + State-level regulators |

| Market Entry Barriers | Ban on online money gaming, complex licensing, fragmented state laws |

| Regulatory Change Timeline | Act passed Aug 2025, effective Oct 2025 |

| Operator Restrictions | Only licensed skill-based and esports platforms permitted |

| Advertising Restrictions | Responsible advertising, no targeting minors |

| Local Presence Requirements | Mandatory Indian entity and management presence |

| Operational Compliance | KYC, AML, self-exclusion, deposit limits mandatory |

| Technical Standards | RNG certification and platform approval required |

| Player Protection Measures | Age verification, grievance redressal, data security enforceable |

| Online Gaming Act Highlights | Ban on online money games; promotion of esports & skill games |

| Financial Reporting | Regular audits and transaction reporting mandated |

| Market Penetration | 18% of population active gamers |

| Average Revenue Per User (ARPU) | USD 8.85 (approx.) |

| Technology Infrastructure | Fast-growing broadband and mobile network expansions |

| Government Incentives | Support for esports and digital entertainment sector growth |

| Enforcement | Penalties for unlicensed operations include fines & imprisonment |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

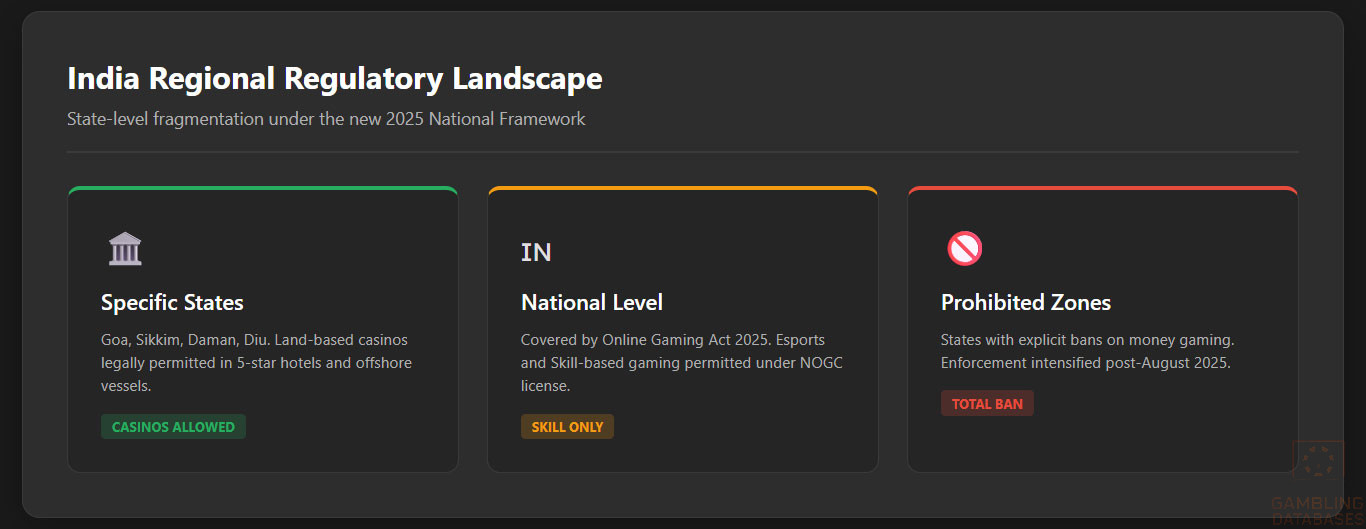

India’s gambling regulation is highly complex and historically fragmented across states, with only a few jurisdictions legally permitting gambling activities. The recent enactment of the Promotion and Regulation of Online Gaming Act, 2025, introduces a unified national legal framework to govern online gaming, addressing consumer protection, operator licensing, and criminalizing online money gaming.

This legislation marks a significant shift from state-specific rules to a federally coordinated regime, promoting esports and skill-based games while banning wager-based money games conducted online nationwide.

Land-Based Gambling Activities

Land-based gambling in India is limited and regulated by individual states. Key activities include casino operations confined primarily to Goa, Sikkim, Daman, and Diu, where casinos operate in designated venues such as five-star hotels and offshore ships. Sports betting is legal only in few states and under strict licensing conditions, focusing mostly on horse racing and limited state lotteries. Slot machine halls and other land-based electronic gaming venues are largely prohibited across most states.

Casino operators must adhere to local laws specifying location, operational hours, and patron eligibility. Licensing requirements for land-based casinos involve detailed scrutiny of physical premises, management credentials, and financial standards, often with high barriers to entry. Sports betting is regulated under separate gaming acts in select states, mandating licensed operators to maintain transparent betting pools and abide by anti-fraud measures.

Online Gambling Framework

The Promotion and Regulation of Online Gaming Act, 2025, creates a national oversight mechanism via the National Online Gaming Commission (NOGC), which licenses and regulates all online gaming operators. The Act classifies games into permissible online games of skill, including esports and fantasy sports, and prohibits online money games or gambling involving bets with financial stakes. Hybrid games containing elements of both skill and chance are subject to classification and potential restriction by the NOGC.

Financial transactions are strictly monitored to prevent money laundering, fraudulent activities, and to ensure user fund segregation and refundability. The Act also provides for an Online Gaming Appellate Tribunal to resolve disputes involving players, platforms, and regulators.

Licensed Operators and Market Players

The Indian iGaming market’s landscape is currently evolving due to the recent regulatory changes. Leading operators have shifted focus from real-money games to esports, social gaming, and skill-based competitions to comply with the new laws. The market is dominated by platforms that have preemptively acquired licenses and established Indian legal entities with compliant management teams.

Key competitive dynamics include strategic partnerships with esports bodies, investments in technological infrastructure compliant with national standards, and aggressive user protection measures. Foreign operators face significant challenges related to local incorporation demands, regulatory oversight, and adapting game offerings to skill-only formats.

Market entry strategies typically involve collaboration with state regulators and investment in brand reputation focused on compliance and consumer trust.

Licensing Framework and Requirements

Application Process and Eligibility

The primary regulatory authority for online gaming licensing is the National Online Gaming Commission (NOGC), supported by state-level regulators where applicable. Applicants must demonstrate financial solvency, technology compliance, and operational integrity. Licensing fees vary by state and gaming vertical but generally start around INR 50,000 for initial application. Licenses are subject to renewal with ongoing compliance requirements.

Applicants must submit extensive documentation to evidence capability and suitability to operate legally, including corporate registration certificates, audited financials, detailed business plans, technical platform evaluations, and criminal background checks for key personnel. Technical standards include certified random number generator (RNG) usage and adherence to secure payment processing protocols. Licence approval timelines range from three to six months depending on application robustness and regulatory workload.

Local Presence and Operational Requirements

Operators must maintain a physical presence in India, including Indian-resident management and local data hosting. Websites and platforms must be registered under Indian law and operate dedicated Indian domains. This allows regulators effective jurisdiction and facilitates compliance monitoring.

Foreign ownership is permitted but requires transparent disclosure and adherence to Indian regulatory provisions on investment and operational control. Partnership with local companies or subsidiaries is a common approach to meet these mandates.

Operational mandates extend to real-time reporting of suspicious transactions, availability of grievance redressal mechanisms, and implementation of responsible gaming tools such as self-exclusion and deposit limits. Platforms must also comply with data privacy laws to protect user information and secure online interactions.

Compliance Obligations and Monitoring

Player Protection and Identification

- Mandatory age verification to prevent underage gambling

- Comprehensive KYC and AML compliance for all users

- Implementation of self-exclusion programs for problem gamblers

- Deposit and wager limits to control betting exposure

- Grievance redressal procedures, including complaint handling and dispute resolution

- User data protection under national privacy regulations

- Mandatory display of responsible gaming warnings on all interfaces

- Advertising restrictions to avoid targeting minors or vulnerable groups

Financial Monitoring and Reporting

Operators must maintain segregated accounts for player funds ensuring their safety separate from operational capital. Transaction monitoring systems are required to detect money laundering and fraudulent activities, with suspicious activities promptly reported to regulatory authorities.

Audits must be conducted regularly to verify financial integrity and compliance with tax obligations. Platforms provide periodic reports to the NOGC and relevant tax authorities detailing gross gaming revenue, payouts, taxes withheld, and operational expenses.

- Submission of quarterly financial and operational reports to regulators

- Independent third-party audits annually to verify compliance

- Reporting of suspicious transactions within 48 hours

- Provision of user transaction histories upon regulator request

Taxation Structure and Financial Obligations

Player Taxation

A flat 30% income tax is levied on all net player winnings regardless of total income or tax slab. This is imposed at source via mandatory tax deduction at payment by licensed operators. There is no minimum threshold for this withholding, ensuring broad revenue capture. Players are responsible for declaring these amounts in their annual tax filings.

Operator Taxation

| Gaming Category | Applicable Tax Rate |

|---|---|

| Online Money Gaming (pre-ban) | 28% GST on full bet value |

| Skill and Esports Games | 18% GST applicable |

| Gross Gaming Revenue (GGR) | 28% (repealed post August 2025 for money games) |

| Corporate Income Tax | 25-30%, depending on turnover |

| License Fees | INR 50,000 and upwards, varies by jurisdiction |

License renewal fees and additional turnover-based taxes may apply in some states. The recent ban on online money gaming has nullified GST on real-money betting since August 22, 2025, shifting operator focus to skill and esports segments with lower GST rates. Despite elevated tax burdens previously, operators benefit from increased legal certainty under the new framework.

Gambling Market Financial Performance

India’s gambling market professionally generated estimated revenues of USD 3.7 billion in 2024, with a projected CAGR of 18.4% through 2029. Total wagered amounts led primarily by fantasy sports and esports have grown rapidly, supported by strong mobile internet penetration.

Despite the ban on online real-money gaming, the sector’s financial health is sustained by fast-expanding esports and social gaming ecosystems. Tax revenue contributions from this segment are stable, though revenue sources have diversified away from direct money betting.

Advertising and Marketing Restrictions

- Advertising must include responsible gaming disclaimers

- Prohibition on targeting minors or vulnerable populations

- Restricted advertising time slots for gaming promotions

- No false or misleading claims regarding winnings

- Sponsorships in esports and non-money game platforms allowed under compliance

These restrictions aim to balance industry growth with consumer safeguards. Operators must ensure all marketing materials comply with legal guidelines and are transparent in their representation, particularly emphasizing the skill-based nature of permitted games.

Recent Regulatory Changes and Their Impact

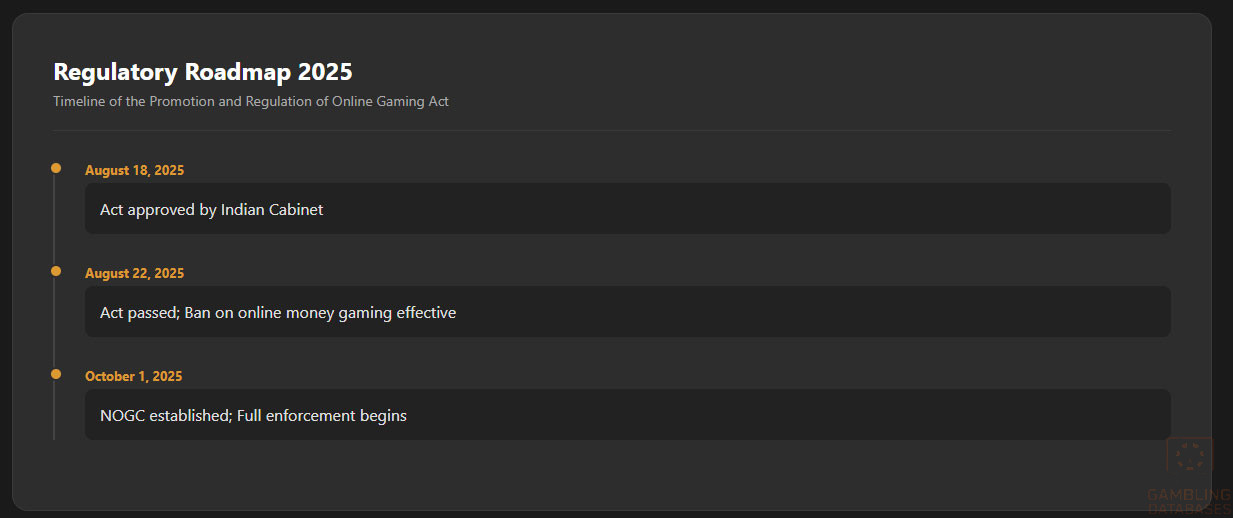

- August 18, 2025: Online Gaming Act approved by Indian Cabinet

- August 21-22, 2025: Act passed by Parliament and received Presidential assent

- August 22, 2025: Ban on online money gaming takes effect nationwide

- October 1, 2025: Act enforcement and establishment of National Online Gaming Commission

The implementation of these milestones drastically reshaped India’s iGaming market, moving from fragmented state laws to centralized oversight, and phasing out unregulated money games. Operators have had to adjust business models rapidly, invest in licensing compliance, and pivot to esports and skill games.

Enforcement Mechanisms and Penalties

- Fines for unlicensed operation starting at INR 500,000

- Imprisonment up to three years for facilitating illegal online money gaming

- Suspension or cancellation of licenses for non-compliance

- Penalties for misleading advertising and consumer rights violations

- Seizure of assets derived from illegal gaming activities

Enforcement is robust, with frequent monitoring by the NOGC and anti-fraud agencies. Compliance trends indicate strong government commitment to regulated market integrity and consumer protection.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

India is home to over 1.42 billion people, making it the world’s most populous country. Its demographic profile is characterized by a youthful population with a median age of approximately 28.4 years. Males account for around 51.9% of the population, while females comprise 48.1%, reflecting a slightly skewed gender ratio.

Urbanization is steadily increasing, with about 35.5% of the population residing in urban areas. Rural zones, however, still dominate, encompassing approximately 64.5% of inhabitants. This urban-rural divide profoundly influences internet access patterns, consumption behavior, and gambling venue availability, with major population centers driving market demand.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 26.7% |

| 15-24 years | 18.1% |

| 25-54 years | 41.7% |

| 55-64 years | 6.1% |

| 65+ years | 7.4% |

Geographic Distribution

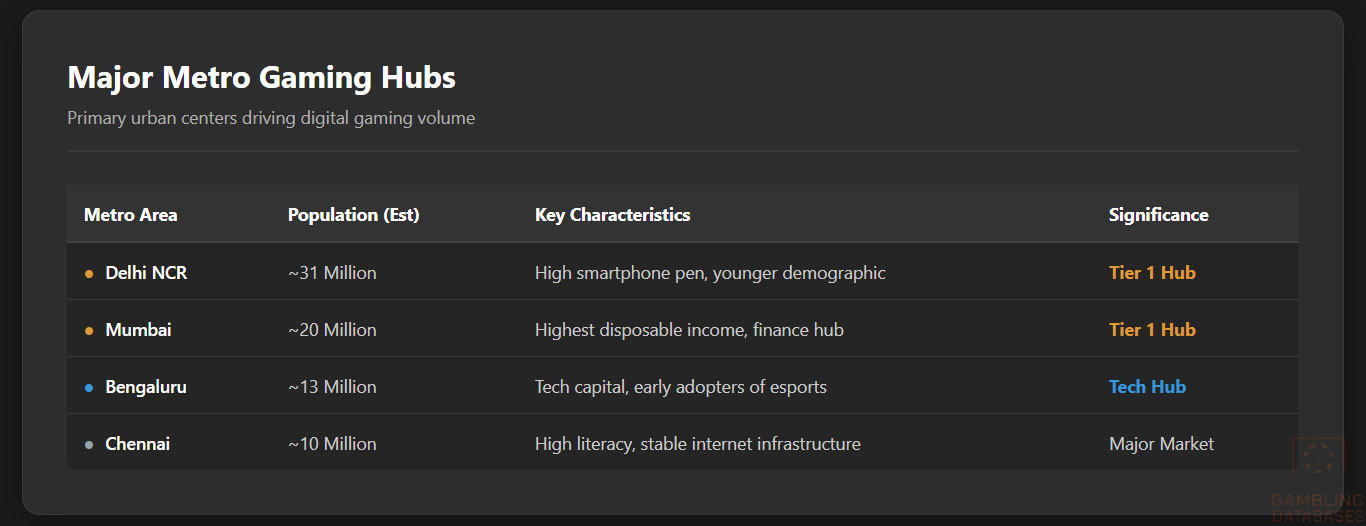

India’s economic and population density is highly concentrated in specific metropolitan hubs and regions. The internet and iGaming activity are largely centered in these urban areas due to superior infrastructure and higher disposable incomes.

- Mumbai: Approx. 20 million

- Delhi: Approx. 31 million (including NCR)

- Bengaluru: Approx. 13 million

- Chennai: Approx. 10 million

- Kolkata: Approx. 14 million

- Hyderabad: Approx. 10 million

- Pune: Approx. 7 million

These cities serve as focal points for digital entertainment, hosting most licensed land-based gaming venues and concentrating online users. Southern and western states such as Maharashtra, Karnataka, and Tamil Nadu rank among the highest for internet penetration and iGaming participation, while northern and eastern rural regions lag in infrastructure deployment.

Economic Indicators and Consumer Spending Power

India’s nominal GDP crosses USD 3.7 trillion as of 2025, maintaining an annual growth rate near 6.8%. The economy’s structure is service-oriented, with approximately 55% of GDP derived from services, 26% from industry, and 19% from agriculture. This composition drives a diversified consumer base with increasing urban middle-class consumption.

Per capita GDP remains moderate at roughly USD 2,600, but is accompanied by rapidly rising disposable income, especially in expanding urban markets. Income inequality is significant, with a Gini coefficient around 35.7, concentrating wealth generation primarily among a middle and upper-middle class that drives discretionary spending in entertainment and gaming.

| Indicator | Value |

|---|---|

| Nominal GDP | USD 3.7 trillion |

| GDP Growth Rate (Annual) | 6.8% |

| Per Capita GDP | USD 2,600 |

| Gini Coefficient | 35.7 |

| Service Sector Contribution to GDP | 55% |

| Industry Sector Contribution to GDP | 26% |

| Agriculture Sector Contribution to GDP | 19% |

Income and Wealth Distribution

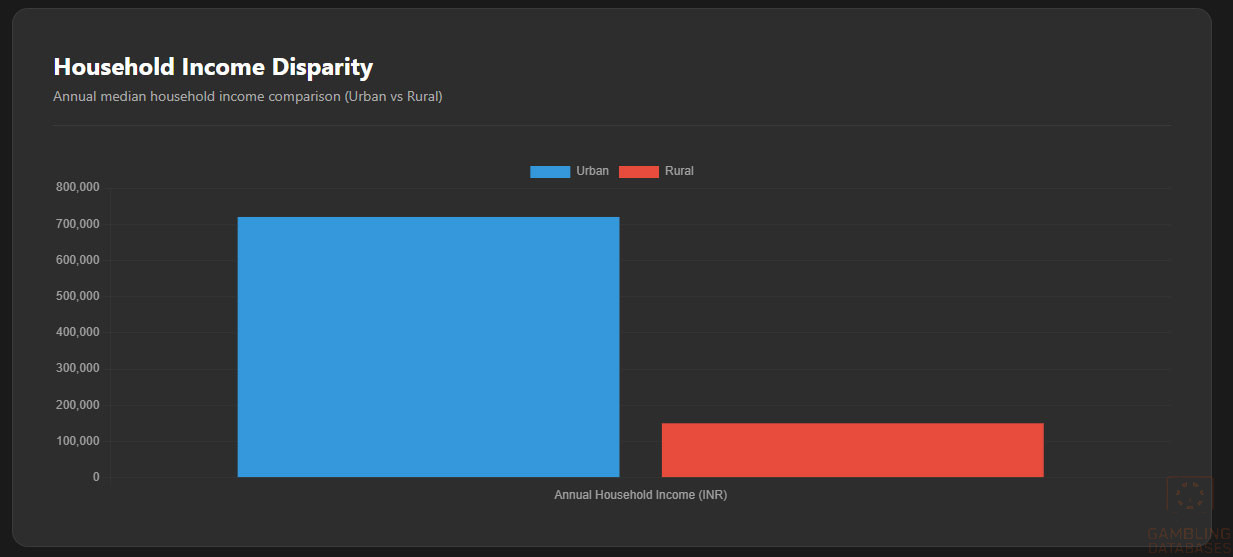

Average household income varies widely by region, with urban centers exhibiting substantially higher earnings than rural areas. The median urban household income is close to INR 720,000 annually, whereas rural households average near INR 150,000. Disposable income is expanding due to wage growth and rising employment in formal sectors.

Consumer spending increasingly favors digital goods, entertainment, and leisure, creating fertile ground for iGaming uptake. Despite income disparities, growing smartphone penetration broadens the available market to lower-income urban and peri-urban populations. Income bracket segmentation reveals a growing affluent class with high propensity to spend on digital gaming services.

Market Size and Growth Projections

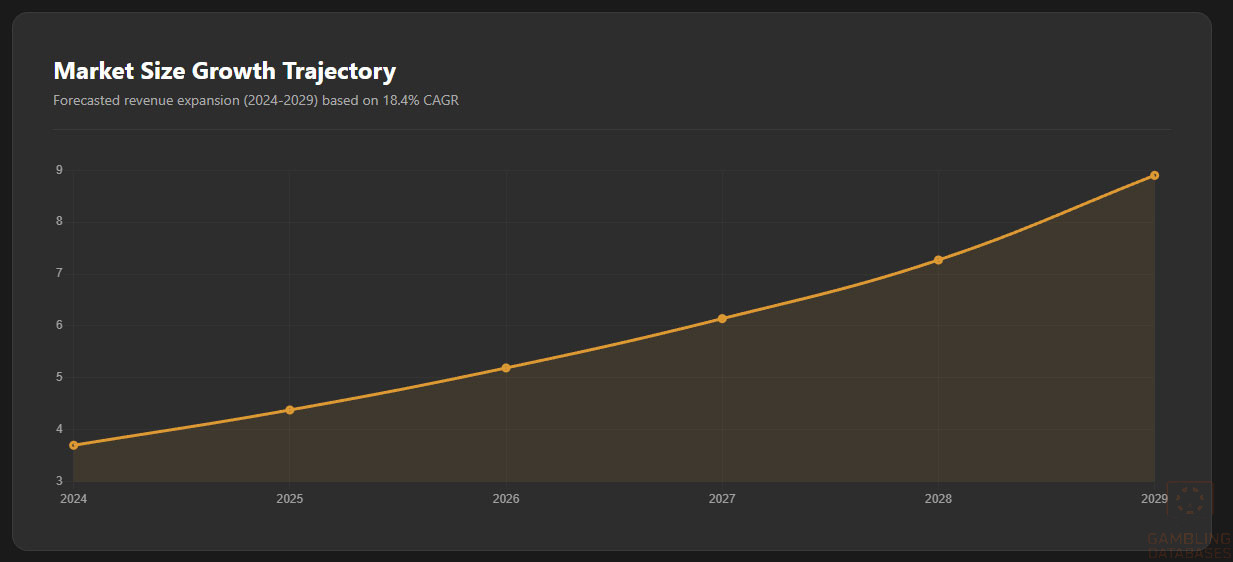

The Indian iGaming market was valued at approximately USD 3.7 billion in 2024, with annual revenues projected to rise sharply due to favorable demographics and digital adoption. The market is expected to grow at a compound annual growth rate (CAGR) of around 18.4% between 2024 and 2029, propelled by esports and skill-based gaming segments.

Projected user base expansion targets over 500 million online gamers by 2029, with average revenue per user (ARPU) increasing modestly by approximately 6% annually as premiumization of offerings continues. Shifts away from online money gaming to licensed skill and esports formats are reshaping revenue distribution across the market.

| Metric | Value |

|---|---|

| Market Size (2024) | USD 3.7 billion |

| Projected Market Size (2029) | USD 8.9 billion |

| Projected CAGR (2024-29) | 18.4% |

| Active Online Gamers (2024) | 420 million |

| Projected Online Gamers (2029) | 520 million |

| Current ARPU | USD 8.85 |

| Projected ARPU (2029) | USD 11.5 |

Education, Skills, and Digital Literacy

India boasts a literacy rate near 77.7% nationally, with marked improvements in primary and secondary education access. Digital literacy is expanding rapidly, with government initiatives targeting skill development in rural and urban areas alike. The workforce is increasingly equipped with technology skills essential for engaging in digital economies, including online gaming.

Higher education, particularly in engineering, computer science, and business, supports the creation of tech-savvy consumer segments and potential workforce talent for the iGaming industry. Continued investments in digital infrastructure and educational programs are helping bridge the digital divide nationally.

Cultural and Social Factors

Communication and Language

India’s linguistic landscape is extremely diverse, with hundreds of languages spoken across regions. The most widely spoken languages include Hindi, Bengali, Telugu, Marathi, Tamil, Urdu, Gujarati, Kannada, Odia, and Malayalam. Internet content and gaming platforms predominantly utilize English and Hindi, with regional language expansions growing steadily to capture broader demographics.

- Hindi

- Bengali

- Telugu

- Marathi

- Tamil

- Urdu

- Gujarati

- Kannada

- Odia

- Malayalam

Cultural Attitudes

Gambling perception in India is shaped by cultural, religious, and legal factors. While gambling traditionally faces social stigma and religious opposition in many communities, modern attitudes have shifted somewhat in urban and youth segments, especially regarding skill-based gaming and esports. Foreign gaming brands are perceived with cautious interest but must navigate sensitivities around gambling morality and regulatory compliance.

Entertainment consumption favors cricket and esports, with digital platforms serving as primary access points. Social gaming and fantasy sports formats enjoy substantial popularity, reflecting a preference for skill and strategy over pure chance betting.

Problem Gambling and Social Considerations

Prevalence of problem gambling in India remains relatively low but is increasing with expanded digital access. Studies estimate that approximately 2-3% of active gamers may exhibit problematic gambling behaviors, with vulnerable groups including young adults and socio-economically disadvantaged populations.

- Government-funded awareness programs targeting youth and families

- Mandatory responsible gaming training for operators and retailers

- Self-exclusion registries and helpline support services

- Collaboration with NGOs for addiction counseling and rehabilitation

- Research funding for social impact studies on gambling behavior

These measures emphasize early intervention, consumer education, and industry accountability, forming an integral part of India’s evolving regulatory framework for iGaming.

Political Structure and Governance

India is a federal parliamentary democratic republic with a stable political environment that supports regulatory reforms aimed at balancing innovation with consumer protection. The central government’s involvement in digital regulation and cooperation with state authorities promotes consistent regulatory implementation. International relations focused on trade and technology partnerships bolster foreign investment confidence in the gaming and entertainment sectors.

Technology Adoption and Digital Behavior

Internet and Digital Usage

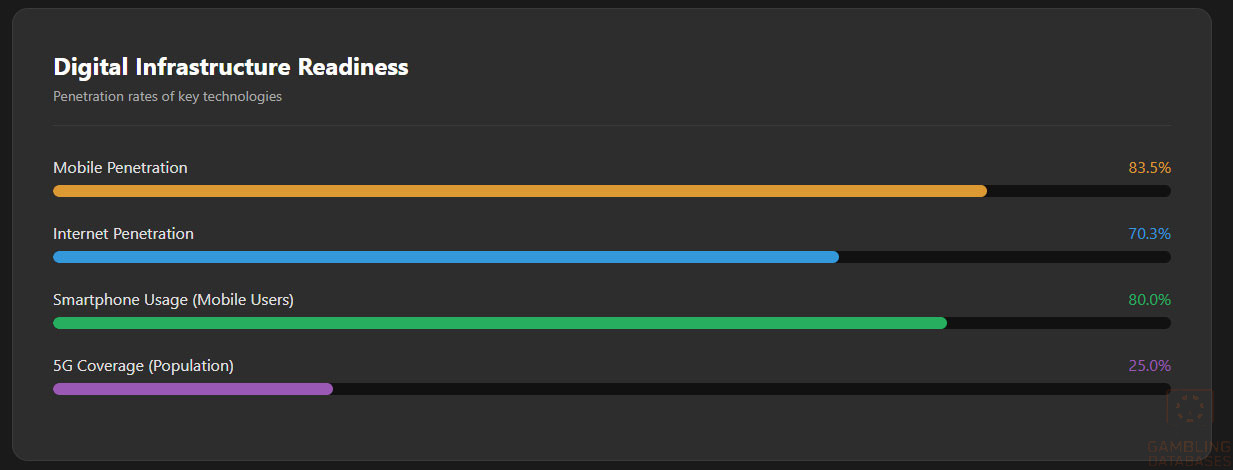

India’s internet penetration stands at approximately 70.3%, with over 900 million active internet users. Average daily internet usage reaches around 7.5 hours, driven by mobile devices. Mobile penetration is even higher at about 83.5%, supported by vast affordable smartphone availability and expanding 4G/5G network coverage.

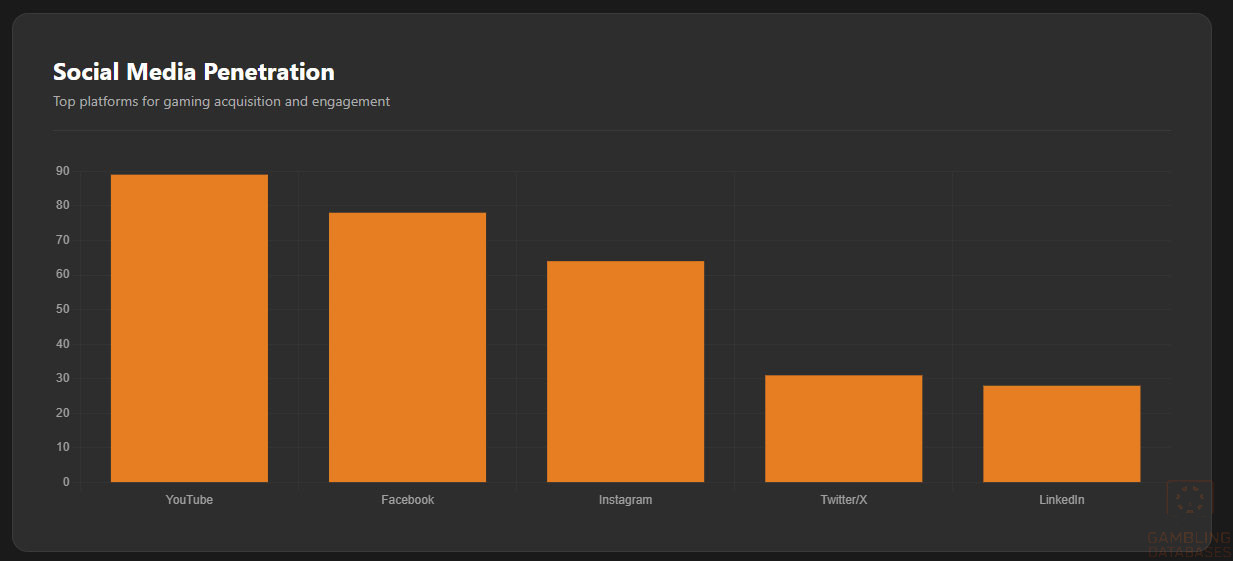

Social media engagement is highly robust, contributing to digital content consumption trends pivotal for iGaming operators targeting youth and urban consumers.

- Facebook: 78% of internet users

- Instagram: 64% penetration in 18-34 age group

- YouTube: 89% overall penetration

- TikTok (or alternatives): Rapid growth among under-25 users

- Twitter: 31% among news and entertainment consumers

- LinkedIn: 28% for professional networking

Digital Payment Behavior

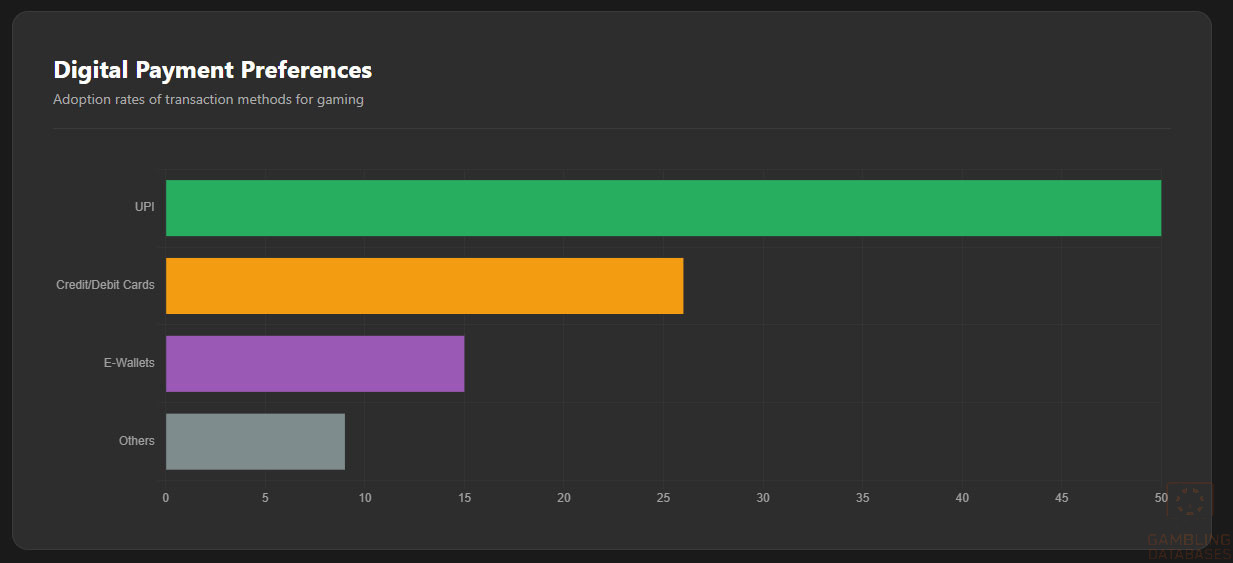

Digital payment adoption is widespread, facilitating seamless in-game transactions and deposits. Popular methods include credit/debit cards, Unified Payments Interface (UPI), net banking, e-wallets, and prepaid cards. Cryptocurrency usage is emerging but remains niche and unregulated officially.

- UPI: Dominates with over 50% transaction volume

- Credit and debit cards: 26% of online payments

- Mobile wallets: 15% market share, popular among youth

- Net banking: Preferred for higher-value transactions

- Prepaid cards and vouchers: Supplementary payment method

Gaming and Gambling Preferences

Current Market Participation

Online gaming engages approximately 30% of the total population, with a higher concentration in urban centers. Participation in gambling-related activities is predominantly skill-based, with fantasy sports, online card games, esports betting, and social gaming leading in popularity. Pure chance-based betting on real money has been largely curtailed due to the legal ban.

- Fantasy Sports (e.g., cricket, football)

- Online Card Games (rummy, poker skill variants)

- Esports Betting and Tournaments

- Social Casino Games (non-money based)

- Casual Mobile Games with Reward Systems

Consumer Behavior Patterns

India’s iGaming consumers prefer mobile-first platforms offering fast, intuitive user experiences. Peak gaming periods align with evening hours post-work and weekends, with average session lengths ranging between 25 and 45 minutes. Retention rates are maximized by offering frequent tournaments, leaderboards, and gamification elements.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

India’s internet connectivity has undergone rapid expansion, reaching over 70.3% penetration as of 2025. The internet user base exceeds 900 million, fueled largely by mobile connectivity. Fixed broadband access remains limited with coverage concentrated in metropolitan areas, while mobile broadband dominates across rural and urban landscapes alike.

Average broadband speeds have reached approximately 55 Mbps, while 4G delivers widespread fast mobile broadband. Despite improvements, rural connectivity still lags, prompting continued government and private investments in fiber optic and satellite technologies. Internet reliability has markedly improved, supporting bandwidth-heavy activities including online gaming and streaming.

5G and Future Technology Deployment

5G rollout is underway with coverage in all major metros and expanding into tier 2 and 3 cities. Leading mobile operators have launched commercial 5G services, covering approximately 25% of the population with plans to reach 50% by 2026. The government fosters 5G expansion through spectrum allocations and infrastructure incentives, aiming to support high-data-demand sectors like iGaming.

The operator landscape is competitive and rapidly evolving, with innovation focused on latency reduction and network slice customization catering to gaming and esports platforms. Future deployments aim to enhance mobile cloud gaming experiences, virtual reality integration, and real-time multiplayer interactions across the country.

Mobile Technology Ecosystem

Mobile Network Infrastructure

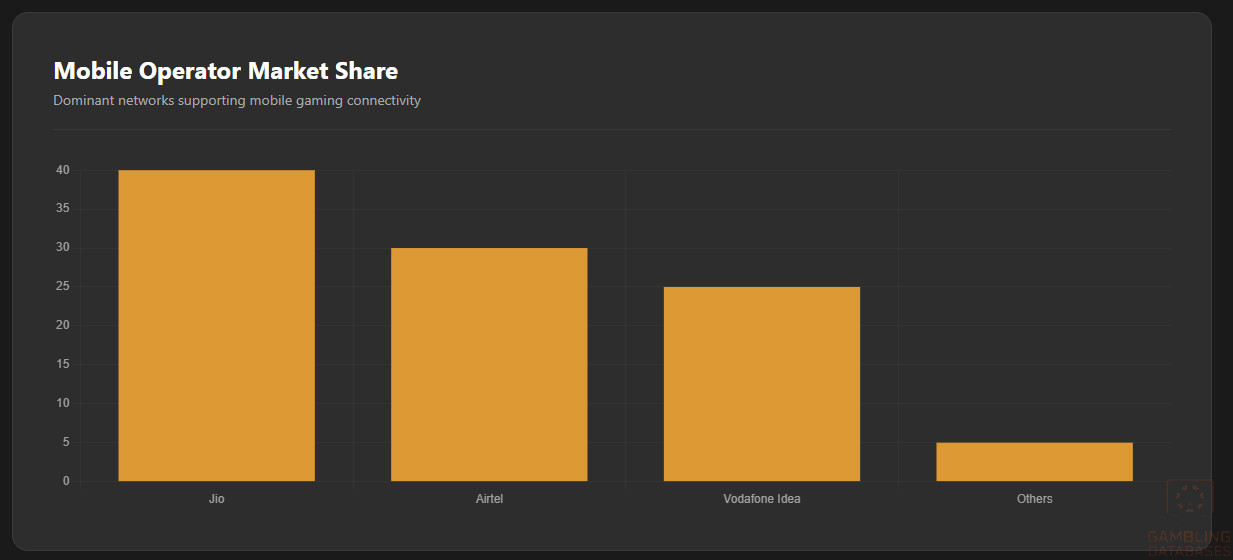

India’s mobile network ecosystem consists of several major players competing vigorously on coverage, pricing, and technology advancement. Market leadership is concentrated in a few key telecom operators that dominate with large subscriber bases and extensive regional footprints. Cost-effective data plans and improved 4G/5G speeds have made mobile internet ubiquitous.

- Jio: Largest market share with over 40% nationwide

- Airtel: Second largest with ~30%, strong 4G and growing 5G footprint

- Vodafone Idea: About 25%, focusing on rural and semi-urban expansions

- BSNL: State-owned operator covering select rural areas

- MTNL: Smaller footprint in metropolitan areas like Delhi and Mumbai

- Reliance Communication: Limited legacy presence

Device Penetration

Smartphone adoption is high and growing, with approximately 80% of mobile users owning smartphones. Android dominates the device market due to cost affordability and broader app ecosystem. Premium devices are gaining traction among urban youth and middle class. Device usage trends favor mobile-first consumption of entertainment and gaming content, with multi-screen interaction common.

Financial Services and Payment Infrastructure

Banking System Structure

The Indian banking sector is diverse, encompassing public sector banks, private banks, and digital-first challengers. Digital banking adoption is bolstered by interoperable payment systems like UPI and increasing smartphone penetration. Account ownership rates remain below 80%, with continued efforts to promote financial inclusion driving growth.

- State Bank of India: Largest with extensive rural and urban branches

- HDFC Bank: Leading private sector bank focused on retail banking

- ICICI Bank: Strong corporate and retail digital offerings

- Axis Bank: Growing digital footprint

- Punjab National Bank: Public sector presence with national coverage

- Kotak Mahindra Bank: Digital innovation leader

Payment Processing Options

India’s payment ecosystem is vibrant, supporting multiple transaction methods suitable for iGaming platforms. The government-backed UPI drives instant payments with broad adoption. Credit/debit card usage is widespread, while e-wallet adoption accelerates rapidly. Bank transfers remain relevant for high-value transactions, and prepaid instruments facilitate user flexibility. Cryptocurrency remains limited but receives increasing attention.

- Unified Payments Interface (UPI) – Most popular digital payment system

- Credit & Debit Cards – Visa, Mastercard, RuPay widely accepted

- E-wallets – Paytm, PhonePe, Google Pay, and others dominate wallet payments

- Net Banking – Integrated with many banks for secure transactions

- Prepaid Cards and Vouchers – Used for casual gamer deposits

- Cryptocurrency – Emerging, unregulated segment

E-commerce and Digital Economy

India’s e-commerce market is valued at over USD 100 billion in 2025, with annual growth rates exceeding 20%. Online retail penetration is driven by rising smartphone usage, improving logistics, and growing consumer trust in digital payments. This environment is highly conducive to iGaming businesses leveraging e-commerce practices for user acquisition, merchandising, and integrated payment processing.

Consumer preferences favor mobile applications, secure payment gateways, and localized content. Digital services like streaming, cloud gaming, and virtual events further fuel the digital economy’s vibrancy, positioning India as a leading emerging market for tech-driven entertainment sectors.

Business Environment and Regulatory Framework

Ease of Business Operations

India ranks 68th globally on the World Bank’s Doing Business Index 2024, reflecting improvements in business registration, permits, and taxation but challenges remain in enforcement and contract resolution. Regulatory reforms continue to simplify entry and operational processes, though bureaucratic complexities and regional variability pose considerations for investors.

- Document preparation and notarization (2-3 weeks)

- Company registration with Ministry of Corporate Affairs (5-7 days)

- Tax registration and PAN application (3-5 days)

- Bank account opening and initial funding (1-2 weeks)

- Local licenses and trade approvals (variable by state)

Corporate Structure and Registration

Foreign operators typically establish private limited companies or subsidiaries to comply with Indian law. Branch offices are allowed with restrictions. Limited Liability Companies (LLCs) are favored for liability protection and ease of governance. Registration requires detailed documentation and compliance with foreign ownership disclosures, with ownership up to 100% permitted in most sectors, including digital gaming.

- Certificate of Incorporation from Registrar of Companies

- Memorandum and Articles of Association

- Digital Signature Certificate for directors

- PAN and TAN tax registrations

- Goods and Services Tax (GST) Registration

- Local municipal and state trade licenses

Taxation Framework

Corporate Income Tax Structure

Corporate tax rates range from 25% to 30% based on turnover, with certain benefits in Special Economic Zones (SEZs) and incentives for IT and digital sectors. India maintains multiple Double Taxation Avoidance Agreements (DTAA), easing repatriation and cross-border business operations.

- United States

- United Kingdom

- Singapore

- United Arab Emirates

- Germany

- Australia

Personal Income Tax

Personal income tax rates are progressive, ranging up to 30%, with standard withholding on winnings and dividends. Operators must withhold taxes on payments to players, ensuring compliance with tax residency and reporting standards. Social security contributions are minimal for digital workers but contribute to broader employment regulations.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry requires a holistic approach considering regulatory compliance, local partnerships, technology adaptation, and consumer engagement. International operators often partner with domestic companies, develop indigenous content, and emphasize strong consumer protection policies. Robust technological infrastructure integration and localization enhance market penetration.

- Form joint ventures or subsidiaries with Indian stakeholders

- Obtain necessary licenses and comply with local regulations

- Invest in skill-based game development and esports platforms

- Leverage mobile-first gaming and digital payment ecosystems

- Implement responsible gaming and data privacy frameworks

- Engage in targeted marketing respecting cultural nuances

Typical Costs and Timelines

Initial market entry costs vary with scale of operations. Licensing fees start at INR 50,000, though consulting and legal fees often exceed INR 2 million due to complexity. Operating expenses include compliance, technology infrastructure, marketing, and staff, leading to initial capital requirements ranging from USD 500,000 to over 1 million. Time-to-market spans 6 to 9 months including license approvals and platform localization.

| Cost Category | Estimated Amount |

|---|---|

| License Application & Fees | 10,000 – 30,000 |

| Legal & Consultancy | 20,000 – 50,000 |

| Technology Setup | 100,000 – 300,000 |

| Marketing & Promotions | 50,000 – 150,000 |

| Operational Expenses (Year 1) | 200,000 – 500,000 |

Success Factors and Challenges

- Adaptation to stringent regulatory environment

- High mobile and digital payment adoption

- Strong focus on responsible gambling

- Growing esports and skill game market

- Localization of content to regional languages

Key challenges include fragmented state regulations, ban on online real-money gaming, infrastructure disparities, and cultural sensitivities around gambling. Strategic compliance, technological innovation, and local market knowledge are critical for new entrants.

Exit Strategy Planning

Market liquidity is growing with secondary market interest in gaming licenses and assets. License transferability is regulated but possible with regulatory approval. Valuation multiples reflect growth potential tempered by regulatory risk. Planning supports flexible exit options, including sale to domestic operators or consolidation through mergers and acquisitions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in India?

Online gambling legality in India is complex. While many forms of traditional gambling remain state-regulated, the Promotion and Regulation of Online Gaming Act, 2025, establishes clear federal rules. The Act permits skill-based games and esports, but prohibits online money gaming involving bets or stakes with real money. This means platforms offering fantasy sports, esports competitions, and skill games can legally operate following licensing, while pure chance-based money gambling is banned.

2. What types of gambling licenses are available and what do they cover?

Licensing is structured primarily around online skill gaming and esports platforms. Licenses cover:

- Skill-Based Online Gaming License

- Esports and Tournament Operator License

- Fantasy Sports Operator License

- Land-Based Casino License (state-specific)

- Sports Betting License (limited states, mostly horse racing)

Each license requires compliance with operational, technical, and financial standards aligned with consumer protection mandates under the 2025 Act.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees start from INR 50,000, though overall costs including legal, technical audits, and compliance may exceed INR 2 million. The application and approval process generally takes between 3 and 6 months, dependent on document completeness, due diligence, and regulatory workload.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies can obtain licenses but must establish a registered Indian entity with local regulatory compliance. Full foreign ownership is permitted, but operators must comply with local management presence, transparency, and financial reporting requirements. Partnerships with Indian firms can facilitate smoother market entry and compliance navigation.

5. What are the tax obligations for iGaming operators?

Operators face multiple tax layers, including GST on deposits and bets, corporate income tax of 25-30%, and license fees. Online money gaming GST was 28% until banned in August 2025; skill games attract 18% GST. Operators must also handle tax withholding for player winnings and comply with turnover-based levies in some states.

6. Are gambling winnings taxed for players?

Player winnings from gambling are subject to a flat 30% income tax withheld at source by operators for licensed activities. This ensures tax compliance regardless of the player’s overall income. Players must declare these winnings in annual tax returns, and no exemption thresholds apply.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational expenses include license fees, platform development, payment processing, marketing, compliance and auditing, staffing, and customer support. These can range broadly but initial and operating budgets typically require USD 500,000 to 1 million annually depending on scale, marketing intensity, and technological sophistication.

8. What is the expected ROI timeline for entering this market?

Return on investment depends on entry strategy and market conditions. Most operators anticipate break-even within 18 to 36 months, with esport and skill gaming segments offering scalable growth paths. Regulatory compliance costs and marketing investments extend ROI horizons but provide long-term stability.

9. What are the local presence requirements for operators?

Operators must register Indian legal entities with resident management and local data hosting. This facilitates regulatory oversight and consumer protection enforcement. Foreign companies typically set up subsidiaries or joint ventures with Indian partners adhering to mandatory disclosures and operational norms.

10. What payment methods are available and recommended?

Preferred payment methods include UPI, credit/debit cards, mobile wallets (Paytm, PhonePe), net banking, and prepaid cards. These methods ensure broad user accessibility and secure, instant transactions vital for online gaming.

11. What are the advertising and marketing restrictions?

Advertising must be responsible, avoiding targeting minors or vulnerable groups. Promotions require transparency regarding skill-based game nature and cannot mislead about winnings. Sponsorship in esports is permitted under compliance, and advertising time and content are regulated.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification, self-exclusion tools, deposit limits, user education on risks, and grievance redressal systems. Operators must implement AML/KYC procedures and regularly report to regulators to uphold market integrity and consumer protection.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in India stood at approx. USD 3.7 billion in 2024 with a projected CAGR of 18.4% through 2029, fueled by increasing internet access, favorable demographics, and expanding esports adoption. The user base is expected to surpass 500 million by 2029.

14. Who are the main competitors and what is their market share?

The competitive landscape is fragmented yet dominated by a handful of licensed skill gaming platforms and esports operators who pivoted from online betting pre-2025. Foreign operators with strong compliance frameworks and local partnerships are gaining ground rapidly, while traditional unlicensed operators recede due to enforcement.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-first, skill-based games and esports tournaments, with peak gaming during evenings and weekends. Spending is concentrated on micro-transactions, skill upgrades, and premium access rather than high-stakes bets. Retention is driven by interactive features and localized content.

16. What are the key success factors and main challenges for new entrants?

Key success factors include regulatory compliance, technological innovation, localized offerings, strong payment integrations, and robust responsible gaming policies. Challenges involve navigating regulatory complexity, regional disparities, cultural sensitivities, and transitioning from banned money gaming models.

Sources and References

- Promotion and Regulation of Online Gaming Act, 2025 – Government of India Website

- National Statistical Office – Population and Demographic Data 2025

- Ministry of Electronics and Information Technology – Digital India Reports 2025

- Reserve Bank of India – Financial and Payment System Reports 2025

- Department of Telecommunications – Telecom Regulatory Authority Reports 2025

- World Bank – Doing Business 2024 Report

- International Telecommunication Union – Global ICT Data 2025

- Indian Ministry of Finance – Taxation Guidelines 2025

- Gaming Industry Expert Reports – Asia-Pacific 2024-25

- Economic Times – Articles on Gaming Regulation India 2025

- Legal 500 – Analysis of India Gaming Laws 2025

- IGaming Today – Market Updates India 2025

- Indian Express – Technology and Telecom Coverage 2025

- Statista – India Internet and Mobile User Data 2025

- Society for Responsible Gambling India – Annual Report 2025

- Ministry of Corporate Affairs – Business Registration Procedures 2025

- National Payments Corporation of India – UPI Reports 2025

- Frost & Sullivan – Digital Payments and Fintech India 2025

- IBEF India Brand Equity Foundation – Market Insights 2025

- Esports Federation of India – Growth Statistics 2024-25

- KPMG India – Technology and Business Environment Review 2025

- PWC India – Taxation and Investment Climate Report 2025

- NITI Aayog – Digital Economy and Infrastructure Roadmap 2025

- Reuters – News Coverage on India’s Online Gambling Ban 2025

- TOI – Consumer Behavior and Digital Adoption Reports 2025

- Local Government Gazettes – State Gambling Laws and Licenses 2025

- Central Bureau of Communication – Internet Literacy and Usage Survey 2025

- McKinsey India Digital Report 2025

- GLOBAL DATA – iGaming Market Forecast India 2024-2029

- Accenture – Gaming and Entertainment Industry Insights 2025

🎯 Gambling Databases Country Rating: India

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.7/10 | ⛔️ Prohibitive |

| Player Access Score | 3.7/10 | 🔴 Restricted |

| Overall Market Attractiveness | 3.2/10 | ⛔️ High Risk / Skill-Gaming Only |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE BAN ON ONLINE MONEY GAMING: The Promotion and Regulation of Online Gaming Act, 2025 explicitly bans “online money games” (games of chance/wager-based gambling). Traditional online casinos and slots are ILLEGAL.

- CRIMINAL LIABILITY: Facilitating illegal online money gaming carries penalties of imprisonment up to three years and heavy fines.

- MANDATORY LOCAL PRESENCE: Operators must have a physical Indian entity, resident management, and local data hosting. This creates immediate legal liability for directors within Indian jurisdiction.

- AGGRESSIVE TAX DEDUCTION AT SOURCE (TDS): A flat 30% tax on all net winnings is deducted at source. This extremely high friction point severely impacts player retention and liquidity.

- ASSET SEIZURE: The government is empowered to seize assets and funds derived from illegal gaming activities.

- ADVERTISING RESTRICTIONS: Strict prohibitions on targeting minors and aggressive marketing; violations attract penal consequences.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Partial Legality (Esports/Skill +1.5). CRITICAL DEDUCTION: Online Casino/Money Gaming Prohibited (-1.5). Active enforcement and imprisonment clauses (-0.5). Only skill-based formats are viable. |

| Licensing Process | 25% | 1.0/2.5 | Limited Licensing (+1.0). Low application fees (+0.5). DEDUCTIONS: Complex probity and bureaucratic hurdles (-0.25). Mandatory local entity requirement complicates structure (-0.25). |

| Taxation & Costs | 20% | 1.0/2.0 | Skill games taxed at 18% GST (+1.5). DEDUCTIONS: Corporate tax 25-30% and mandatory 30% Player Winnings Tax creates high operational friction (-0.5). Effective tax burden on ecosystem is high. |

| Operational Requirements | 15% | 0.0/1.5 | Heavy Requirements (+0.5). CRITICAL DEDUCTIONS: Mandatory resident management exposes staff to arrest (-0.25). Local data hosting required (-0.25). Strict KYC/AML and grievance redressal mandates (-0.25). |

| Market Environment | 10% | 0.2/1.0 | Good growth potential (+0.7). DEDUCTIONS: Recent drastic regulatory change (Ban on RMG) (-0.25). Advertising restrictions (-0.25). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.5/4.0 | Partial Legality (+2.0). CRITICAL DEDUCTION: Major product categories (Slots/Casino) prohibited (-1.5). Accessing money games is legally risky (-0.5). |

| Practical Accessibility | 30% | 1.5/3.0 | UPI and digital payments widely available (+2.0). DEDUCTIONS: Active blocking of unauthorized offshore sites (-0.5). Payment blocking for gambling codes (-0.5). |

| Player Penalties | 20% | 1.0/2.0 | Fines possible for participation in illegal gambling (+1.0). Strict tax enforcement on winnings via TDS reduces net gain visibility (+0.5). |

| Market Availability | 10% | 0.7/1.0 | High availability of permitted skill games (+0.7). Traditional casino options are offshore only and blocked. |

🔍 Key Highlights

Strengths (For Skill-Gaming Only)

- Massive population (1.42 billion) with high mobile penetration (83.5%).

- Rapidly growing Esports and Fantasy Sports sector (18.4% CAGR).

- Low license application fees (INR 50,000 range) compared to Europe/US.

- Advanced digital payment infrastructure (UPI) for seamless low-value transactions.

⛔️ CRITICAL RISKS AND CHALLENGES

- Product Prohibitions: “Online Money Gaming” (Chance/Casino) is BANNED. You cannot legally operate a luck-based casino.

- Director Liability: Requirement for Indian resident management puts your leadership team within physical reach of Indian law enforcement.

- Taxation Structure: The 30% tax on player winnings is deducted at source. This kills the “recycling” of winnings and lowers player lifetime value (LTV).

- Enforcement: The National Online Gaming Commission (NOGC) has powers to block sites, seize assets, and recommend criminal prosecution.

- Distinction Ambiguity: The line between “Skill” and “Chance” is legally volatile. A game classified as skill today could be reclassified and banned tomorrow.

Player-Specific Issues

- 30% Flat Tax: Players lose 30% of net winnings immediately; no threshold exemption.

- Access Barriers: Traditional casino players must use VPNs and face payment blocking.

- KYC Fatigue: Mandatory strict KYC for all users creates friction in onboarding.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD 500,000 – 1,000,000 (Setup, Entity formation, Tech compliance).

Monthly Operating Costs: High (Must maintain local office and staff, plus compliance audits).

Effective Tax Rate: High friction. While GST is 18% on platform fees (for skill games), the 30% player tax acts as a massive dampener on liquidity and turnover.

Customer Acquisition Cost: Moderate to High. Competition is fierce among established fantasy/skill giants (Dream11, etc.), and advertising channels are restricted.

Profitability Assessment: Prohibitive for Traditional Casino. If you are a Slot/Roulette operator, this market is closed. For Skill/Esports operators, it is a volume game with thin margins due to tax friction. Only viable for operators with massive scale and technology to manage micro-transactions.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | ISP blocking, payment freezing, criminal charges for “money gaming,” asset seizure. |

| Skill/Esports Operators | MEDIUM | Reclassification risk (Skill vs Chance), tax compliance audits, strict data localization laws. |

| Affiliates/Advertisers | HIGH | Prosecution for promoting “money gaming,” ban on targeting minors, strict content codes. |

| Company Directors | CRITICAL | Imprisonment risk (up to 3 years) if the platform is deemed to offer “money games.” |

| Payment Processors | HIGH | RBI penalties for processing unregulated gaming transactions, loss of banking license. |

🚨 Extradition and International Enforcement

Extradition Treaties: India has active extradition treaties with 48 countries, including the USA, UK, UAE, France, Germany, and Canada.

Enforcement History: India is increasingly aggressive in pursuing economic offenders globally. The government actively issues Red Corner Notices through Interpol for financial crimes and illegal gambling operations.

Travel Risk: Directors of non-compliant operators run a significant risk of detention if entering India or transiting through treaty countries if charges are filed.

📋 Final Verdict

India receives an Operator Ease Score of 2.7/10 and a Player Access Score of 3.7/10, resulting in an overall market attractiveness rating of 3.2/10.

HONEST ASSESSMENT: The “Gold Rush” narrative for India is misleading for traditional iGaming. With the 2025 Act strictly banning online money gaming (chance) and imposing jail terms, India is a NO-GO zone for traditional online casinos. The market is only open to licensed “Skill” and “Esports” platforms. Even for permitted operators, the mandatory local presence, 30% player tax, and intense regulatory scrutiny make this a low-margin, high-compliance volume game suitable only for specialized, locally-entrenched entities.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A dedicated Fantasy Sports or Esports platform (Not gambling).

- Willing to establish a full Indian subsidiary with local directors.

- Prepared for a high-volume, low-margin business model based on platform fees.

- Able to invest $1M+ in compliance, local tech, and legal retainers.

❌ Definitely Avoid If You Are:

- A Traditional Online Casino (Slots, Roulette, Blackjack are effectively BANNED).

- A Sportsbook relying on pure wagering (Must be framed as fantasy/skill).

- An offshore operator unwilling to set up a local office (You will be blocked).

- Unwilling to expose your directors to Indian legal jurisdiction and potential arrest.

- Looking for a low-tax jurisdiction (30% player tax kills liquidity).

⚠️ BOTTOM LINE: If your business model relies on “House Edge” games of chance, stay away. India is now a regulated “Skill Gaming” market, not a gambling market.