Indonesia represents a highly challenging market for iGaming entry in 2025 due to its strict prohibition and regulatory crackdown on all forms of gambling, including online platforms. Despite legal barriers, the nation exhibits strong demand fueled by rapid internet penetration and a growing base of online bettors. This report analyzes the regulatory framework, market dynamics, and compliance environment crucial for any market player considering Indonesia.

| Metric | Value |

|---|---|

| Gambling Legal Status | Illegal and banned outright nationwide |

| Regulatory Authority | No dedicated gambling regulator; enforcement by multiple government agencies |

| Prohibited Activities | All forms of land-based and online gambling including casino, sports betting, slots, poker |

| Population | ~280 million (2025) |

| Active Online Bettors (Estimate) | 3 million |

| Internet Penetration Rate | ~77% |

| Mobile Penetration Rate | ~92% |

| GDP (Nominal) | Approx. $1.5 trillion |

| Average Income Level | GDP per capita approx. $5,400 |

| Online Gambling Market Size (Est.) | Rp 400 trillion (~$25.79 billion) total transactions (2024) |

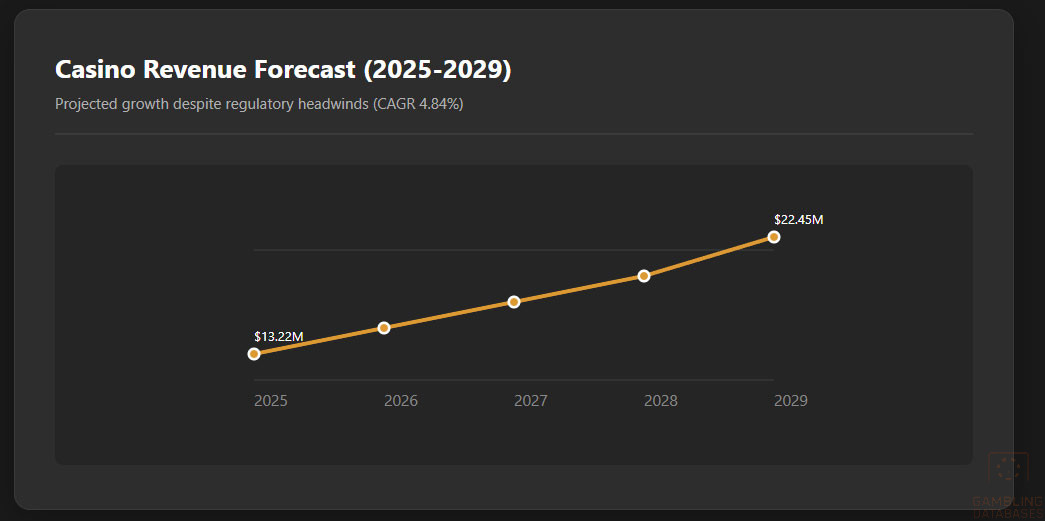

| Casino Games Revenue (Est.) | $13.22 million (2025) |

| Projected Casino Revenue (2029) | $22.45 million (CAGR 4.84%) |

| Number of Licensed iGaming Operators | None legally licensed in Indonesia |

| License Application Fee | Not applicable (prohibition) |

| Tax on Operators | Not applicable; operators illegal |

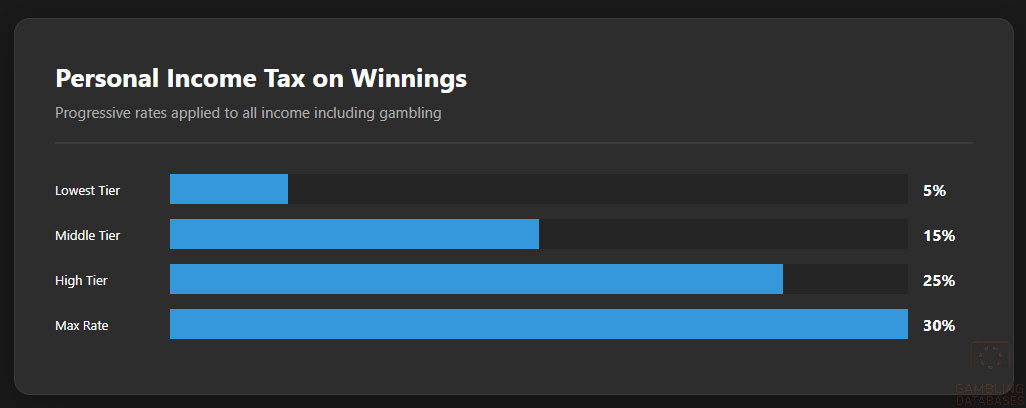

| Personal Income Tax on Gambling Winnings | Applies under general personal income tax; rates from 5%-30% |

| Compliance Monitoring Agencies | Ministry of Communication & Information Technology, National Police, Bank Indonesia, Financial Services Authority (OJK) |

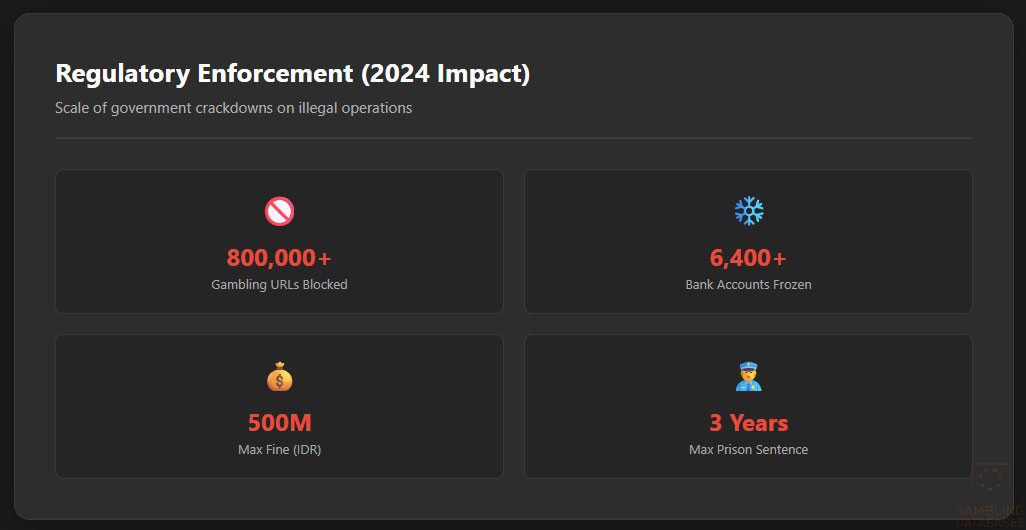

| Online Gambling Website Blocks | 800,000+ URLs blocked (2024) |

| Enforcement Penalties | Fines up to IDR 500 million, imprisonment up to 3 years for habitual offenders |

| Advertising Restrictions | All gambling advertising prohibited |

| Typical Enforcement Actions | Website takedowns, bank account freezes (6,400+ accounts in 2024), raids, arrests |

| Local Presence Requirement | Not applicable (no legal operation) |

| Operational Requirements | Illegal operation risks criminal prosecution |

| Average Revenue Per User (ARPU) | Data unavailable due to illegality |

| Market Penetration Rate | Limited by access restrictions but significant illegal participation |

| Growth Forecast (Online Gambling) | Continued growth in illegal participation despite enforcement (3+ million players) |

| Recent Regulatory Developments | Stricter government regulations on ISPs, fintech firms, enhanced sanctions (2025) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Indonesia enforces a strict prohibition on all forms of gambling under national law, reflecting strong cultural and religious opposition. Both land-based and online gambling activities are banned outright, with no legal licensing frameworks for operators in the country. This ban extends to casino games, sports betting, poker, slots, and lotteries without exception.

The government maintains a multi-agency enforcement system including the Ministry of Communication and Information Technology (Kominfo), National Police, Bank Indonesia, and the Financial Services Authority (OJK). These agencies collaborate to monitor, block, and dismantle gambling operations and associated financial transactions.

Land-Based Gambling Activities

There are no legal land-based casinos or commercial gambling venues in Indonesia. The law prohibits casino halls, sports betting shops, slot machine arcades, and any form of commercial betting shops. Traditional games such as cockfighting and community raffles exist culturally in some regions but operate in a legal gray area without formal regulation or protection.

Online Gambling Framework

Online gambling is categorically illegal with no legal regulatory authority for its oversight. The law criminalizes not only the operators but also the participants, intermediaries, and facilitators of gambling activities. Comprehensive website blocking is enforced by Kominfo, which has blocked over 800,000 gambling-related URLs as of 2024. Financial institutions partner with regulatory bodies to freeze accounts linked to illegal operators.

Recent government initiatives in 2025 involve stricter regulations targeting internet service providers and fintech companies, mandating risk mitigation mechanisms and ongoing monitoring to curb access to illegal gambling platforms. The regulatory framework increasingly emphasizes the protection of minors due to widespread underage gambling on unregulated digital platforms.

Licensed Operators and Market Players

Indonesia currently does not license any domestic or international iGaming operators. The market is dominated entirely by unlicensed offshore operators accessible via VPN and other circumvention tools. Competition exists in the illegal segment among offshore platforms targeting Indonesian bettors, who constitute a sizeable underground market despite enforcement efforts.

Licensing Framework and Requirements

Since online and land-based gambling are illegal, Indonesia does not offer formal licensing for gambling operators. There is no official gambling regulator to issue licenses or regulate operators. Instead, regulatory efforts are focused on prohibition enforcement.

The licensing application processes, fees, or eligibility criteria do not exist domestically. Foreign operators servicing Indonesian consumers do so without legal permission and face increasing risk of website blocking and financial sanctions.

Local Presence and Operational Requirements

There are no legal requirements for local presence or establishment related to gambling operations since gambling is banned. Foreign ownership restrictions apply by default as no legal gambling business may operate within Indonesia’s jurisdiction, and any local partnership would inherently risk criminal liability.

Compliance Obligations and Monitoring

Player Protection and Identification

Given the illegal status, regulated player protection frameworks such as age verification, KYC, and responsible gambling measures are not implemented within Indonesia for gambling. However, emerging regulations seek to curtail underage access by enforcing stricter controls on digital platforms and service providers.

- Mandatory website blocking of gambling content by internet providers

- Financial transaction monitoring and blocking by banks and payment processors

- Law enforcement raids and investigations of illegal gambling networks

- Public awareness campaigns targeting youth and vulnerable populations

- Self-exclusion and complaint mechanisms are not established due to illegality

Financial Monitoring and Reporting

Financial institutions cooperate with regulatory authorities to monitor suspicious transactions linked to gambling activity. Banks and fintech companies are required to flag and block payments to and from illegal gambling operators. Financial reporting and audits target criminal money flows rather than commercial tax compliance.

- Detection of suspicious gambling-related transactions by financial institutions

- Reporting of identified transactions to regulatory authorities

- Freezing or blocking of funds in gambling-linked accounts

- Investigation and prosecution by law enforcement agencies

Taxation Structure and Financial Obligations

Player Taxation

The taxation of gambling winnings falls under general personal income tax laws as no specific gambling tax framework exists. Indonesian residents are required to report all income sources, including gambling winnings, with tax rates ranging from 5% to 30% depending on total income.

Operator Taxation

No legal gambling operators exist within Indonesia, so operator-specific gaming taxes or licensing fees are not applicable. Corporate income tax for entities operating within Indonesia is set at 22%, but illegal gambling operators do not officially comply or pay these taxes.

| Tax Type | Rate / Details |

|---|---|

| Personal Income Tax (Gambling Winnings) | 5% – 30% progressive rate |

| Corporate Income Tax | 22% standard rate (no legal gambling operators) |

| Withholding Tax by Foreign Platforms | No alignment with Indonesian tax laws, operates independently |

| License Fees for Gambling Operators | Not applicable (illegal market) |

| Turnover or GGR Tax | None legally enforced |

Gambling Market Financial Performance

The illegal gambling market in Indonesia is large, with total online gambling transactions estimated at approximately Rp 400 trillion (~$25.79 billion) in 2024. Casino game revenue is projected at $13.22 million in 2025 with growth forecasts expecting $22.45 million by 2029 at a CAGR of 4.84%.

Enforcement efforts result in freezing bank accounts (6,400+ frozen in 2024), website blocks, and arrests, significantly impacting market operations.

Advertising and Marketing Restrictions

All forms of gambling advertising and promotion are banned nationwide. The government prohibits gambling ads across television, internet, social media, and physical venues. Social media platforms face government pressure to remove gambling content proactively. Sponsorship and promotional activities related to gambling are not permitted, and enforcement includes content removal and penalties for infractions.

- Prohibition of gambling advertisements on broadcast and digital media

- Removal of gambling content on social networks and platforms without government order

- Ban on sponsorships and promotional events related to gambling

- Enforcement against influencers and content creators promoting gambling

- Time and place restrictions on potential gambling-related marketing

Recent Regulatory Changes and Their Impact

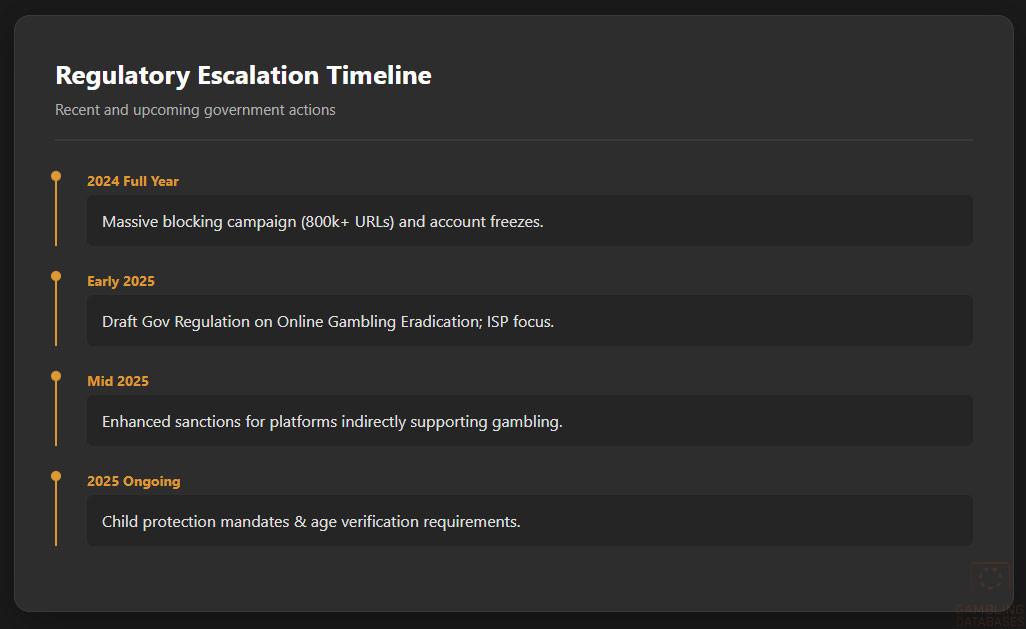

- 2024: Expansion of URL blocking covering 800,000+ gambling-related websites and domains.

- 2025 early: Draft Government Regulation on Online Gambling Eradication emphasizing stricter ISP and fintech compliance.

- 2025 mid: Enhanced sanctions for digital platforms indirectly supporting gambling operations introduced.

- 2025 ongoing: New child protection provisions requiring digital service providers to implement age verification and risk mitigation.

These changes increased operational risks for illicit providers and raised the costs of compliance for digital intermediaries. They also contributed to higher penalties and enforcement actions against violators, reinforcing Indonesia’s zero-tolerance stance.

Enforcement Mechanisms and Penalties

Enforcement involves collaborative operations by multiple agencies including police raids, judicial prosecutions, and financial sanctions. Penalties escalate from fines to imprisonment based on the severity and recurrence of offenses. The government also enforces bank account freezes and website takedown orders as core tools.

- Fines up to IDR 500 million for simple gambling offenses

- Prison sentences up to 3 years for habitual or large-scale offenders

- Confiscation of gambling proceeds and assets

- Bank account freezing and financial transaction blocking

- Website and domain blocking, including mirror and proxy sites

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

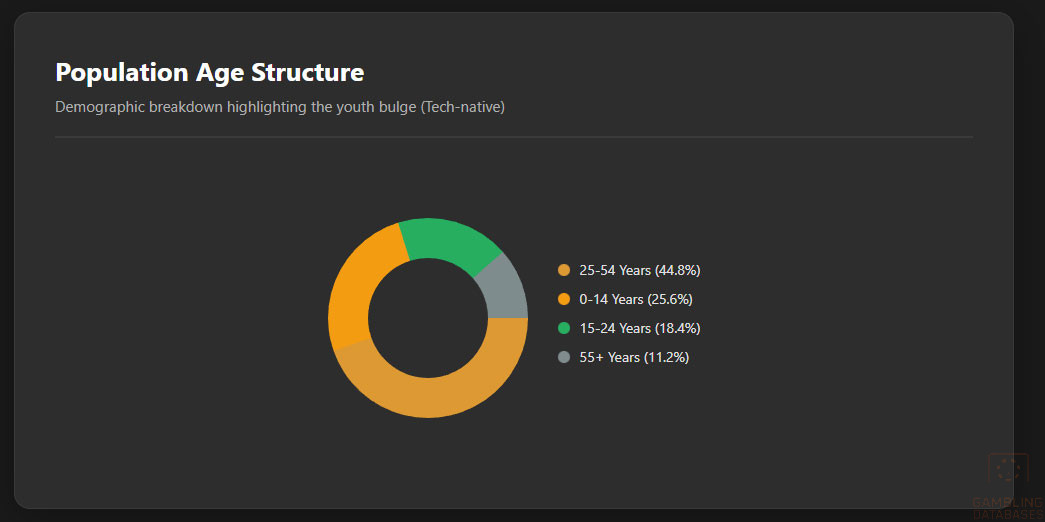

Indonesia is the world’s fourth most populous country with an estimated population of 280 million in 2025. The population is notably young, with a median age of approximately 30.2 years reflecting a significant proportion of working-age adults and youth. Gender distribution is fairly balanced, with males making up around 50.4% and females 49.6% of the population.

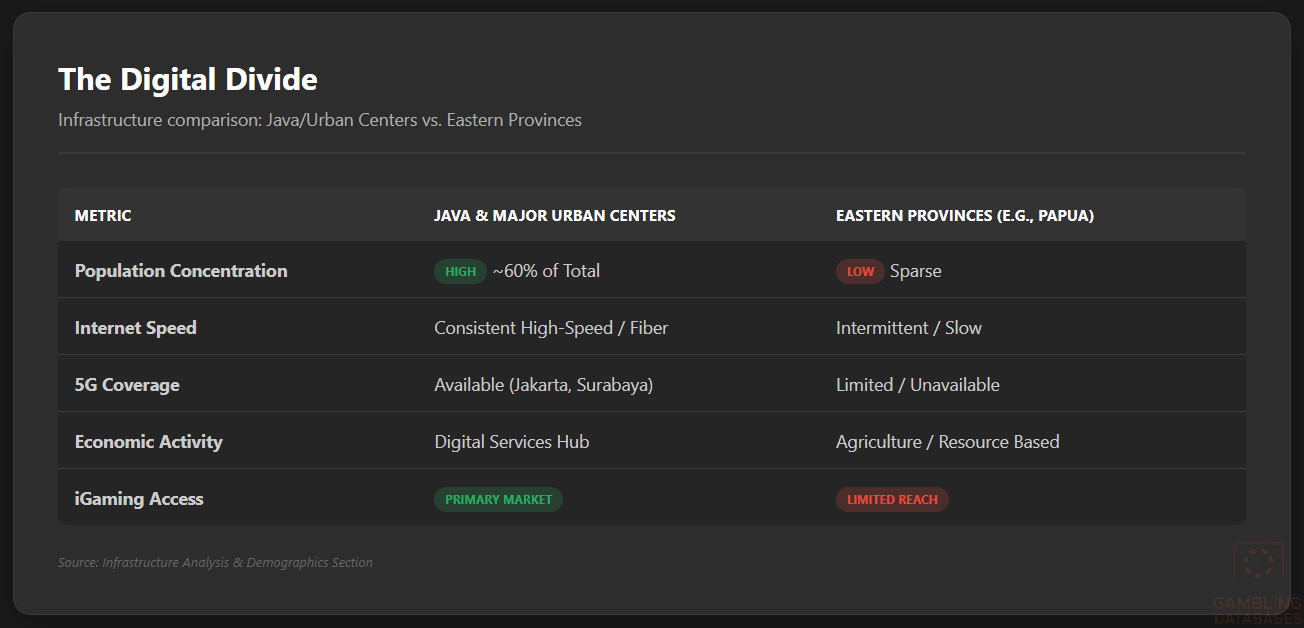

The age distribution illustrates a large youth segment, vital for shaping market demand in emerging sectors such as online gaming. Urbanization trends remain strong, with over 58% of the population residing in urban areas, predominantly on the island of Java. The rural population, while decreasing, still constitutes a substantial demographic with limited digital access in some regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 25.6% |

| 15-24 years | 18.4% |

| 25-54 years | 44.8% |

| 55-64 years | 6.7% |

| 65 years and older | 4.5% |

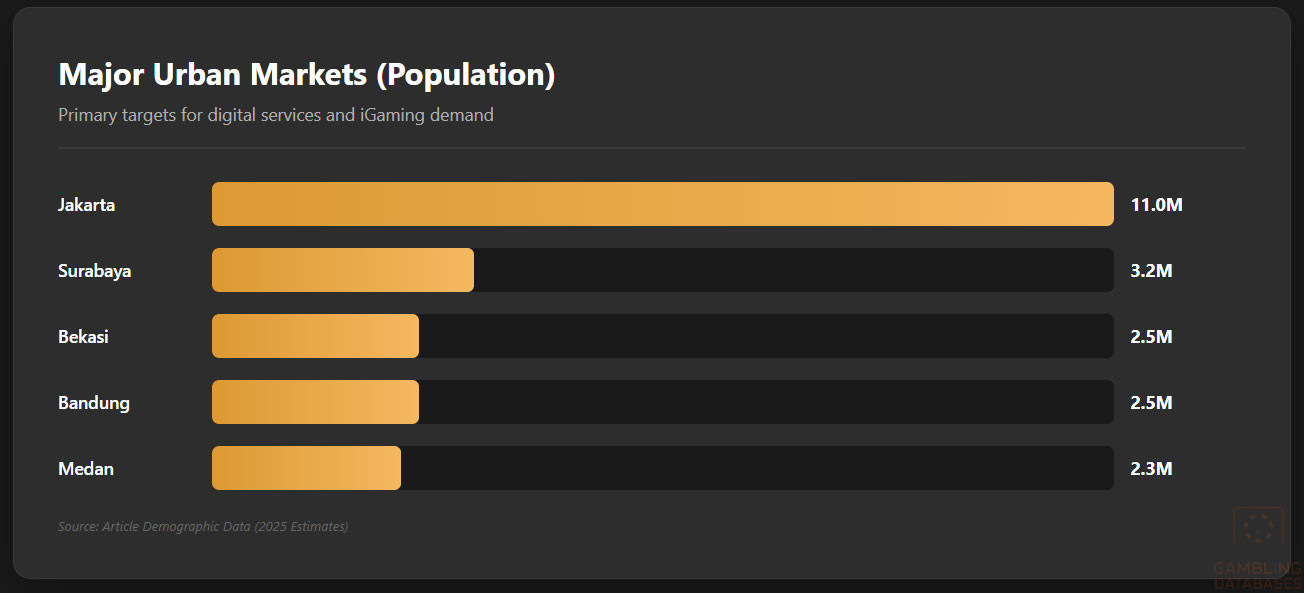

Geographically, Indonesia is an archipelago of over 17,000 islands, with economic and demographic activity concentrated in key urban centers. Java, the world’s most populous island, holds nearly 60% of the national population, making it the principal market for digital services and iGaming demand.

- Jakarta: Capital city and economic hub with over 11 million residents in metropolitan area

- Surabaya: Second largest city, key commercial center, population ~3.2 million

- Bandung: Industrial and educational hub with ~2.5 million residents

- Medan: Largest city on Sumatra island, population ~2.3 million

- Bekasi: Rapidly growing satellite city near Jakarta with ~2.5 million residents

Internet infrastructure and access are most developed in these urban areas, where the majority of the online gambling activity is concentrated despite its illegal status. Conversely, sparsely populated eastern provinces such as Papua lag behind in digital penetration and consumer market development.

Economic Indicators and Consumer Spending Power

Indonesia’s economy is the largest in Southeast Asia, with a nominal GDP estimated above $1.5 trillion in 2025 and a steady growth forecast averaging 5.1% annually over the next five years. The economy is diversified, with key contributions from services (around 44%), industry (39%), and agriculture (17%).

GDP per capita stands near $5,400, marking a rising middle-income status and growing consumer purchasing power. Inflation has been controlled moderately, preserving disposable income gains despite global economic turbulence.

Household income distribution shows significant disparities, with urban centers enjoying higher average earnings than rural areas. The average monthly household income in Jakarta, for example, is roughly three times higher than in less developed provinces. Disposable income continues to increase, fueled by expanding consumer credit and digital payment adoption.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $1.5 trillion |

| GDP Growth Forecast (2026-2030 CAGR) | ~5.1% |

| GDP per Capita | $5,400 |

| Inflation Rate | 3.8% |

| Unemployment Rate | 5.1% |

The consumer spending pattern is increasingly directed toward digital goods and services. E-commerce and mobile-based platforms have surged, associated with growing smartphone penetration and internet usage. This trend is a key driver for the illegal but robust iGaming demand, with large segments of the population willing to spend on online betting and casino games despite the regulatory restrictions.

Market Size and Growth Projections

Indonesia’s illegal online gambling market is significant, with estimates suggesting over 3 million active players involved in various digital betting activities. Total wagering transaction volumes exceed Rp 400 trillion (~$25.79 billion) annually, positioning Indonesia as one of the largest untapped markets in Southeast Asia for iGaming operators willing to navigate risk.

The casino games segment alone is projected to generate around $13.22 million in revenue in 2025, with a compound annual growth rate (CAGR) of approximately 4.84% expected through 2029, reaching an estimated $22.45 million. Market growth is driven by increasing smartphone usage and undisrupted digital access via VPN bypasses.

| Metric | 2025 | 2029 Projection | CAGR |

|---|---|---|---|

| Active Online Players (Millions) | 3.0 | 3.7 | 5.4% |

| Total Gambling Transactions (Rp Trillion) | 400 | 510 | 6.2% |

| Casino Games Revenue ($ Million) | 13.22 | 22.45 | 4.84% |

| Average Revenue Per User (ARPU) ($) | 4.41 | 5.80 | 6.3% |

Education, Skills, and Digital Literacy

Indonesia has achieved significant progress in literacy rates, with over 96% of the adult population able to read and write. Education levels are improving, with increasing enrollment in secondary and tertiary education, particularly in urban centers. Digital literacy also shows rapid growth, supported by government initiatives and expanding access to smartphones and affordable internet.

Workforce skills are improving in technology and services sectors, although gaps remain in rural and less developed regions. The younger generation is highly proficient in digital tools, social media, and mobile applications, which correlates strongly with their significant participation in online gaming activities.

Cultural and Social Factors

Communication and Language

Indonesia’s official language is Bahasa Indonesia, which serves as the lingua franca across its numerous islands. Local languages and dialects are widely spoken, with over 700 recognized languages in use nationally. Internet content consumption predominantly occurs in Bahasa Indonesia followed by English and localized regional languages.

- Bahasa Indonesia (official and dominant)

- Javanese (largest ethnic group primary language)

- Sundanese (West Java regional language)

- Madurese (East Java and Madura Island)

- Minangkabau (West Sumatra region)

Cultural Attitudes

Islam is the predominant religion, influencing conservative social norms and strong opposition to gambling activities, perceived as morally and socially harmful. Despite religious proscriptions, gambling persists underground, reflecting a complex cultural landscape where economic motivations often override religious restrictions.

Foreign brands face skepticism but also fascination in Indonesia, especially in urban youth markets. Entertainment preferences skew toward mobile and digital media, creating latent demand for iGaming if regulatory barriers could be moderated.

Problem Gambling and Social Considerations

Problem gambling is a growing social concern, especially among youth and low-income groups who have easy access to illegal online platforms. Government awareness programs and NGOs have started addressing addiction and financial harm resulting from unregulated gambling.

- Public education campaigns on gambling risks

- Counseling and rehabilitation services for compulsive gamblers

- Legal restrictions aimed at protecting minors and vulnerable groups

- Financial literacy initiatives to reduce gambling-induced debt

- Collaboration with digital platforms to reduce gambling content exposure

Political Structure and Governance

Indonesia operates as a presidential republic with stable democratic governance and consistent policymaking. Its regulatory environment shows strong state control over gambling due to social, religious, and political pressures. International relations favor trade and technology cooperation but maintain a cautious stance on gambling and digital vice industries.

Technology Adoption and Digital Behavior

Internet and Digital Usage

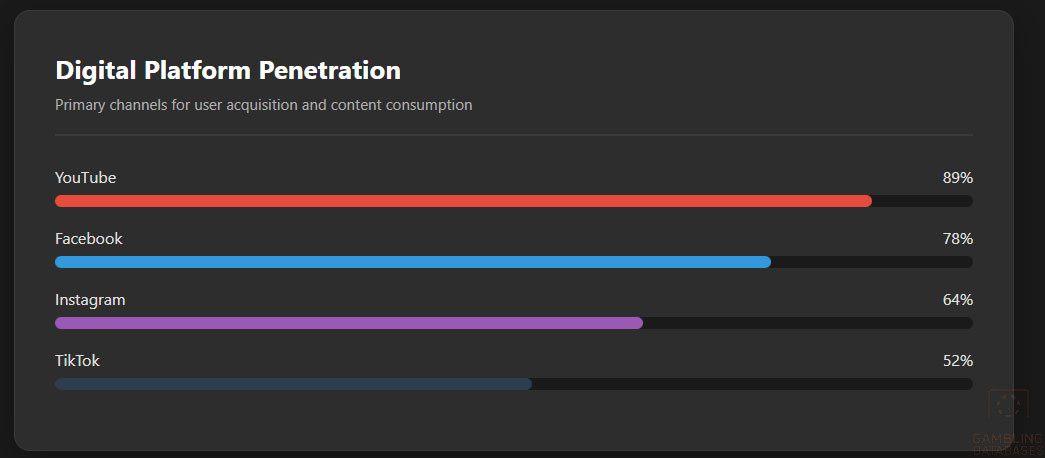

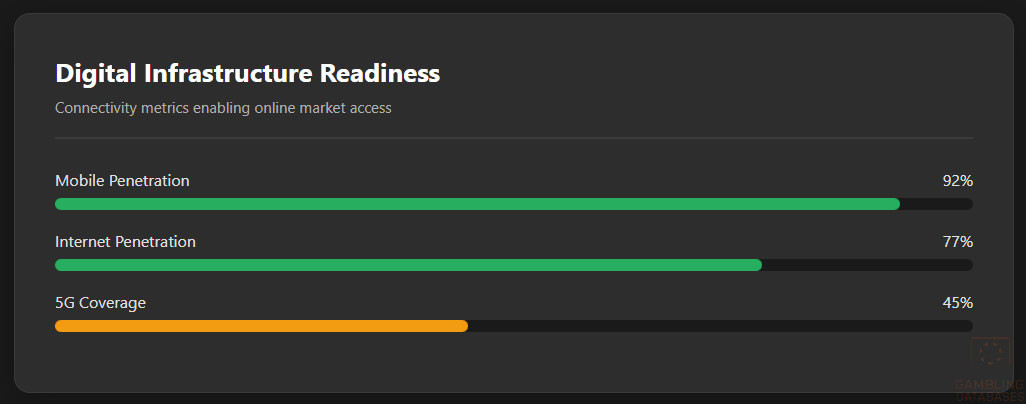

Internet penetration reaches approximately 77%, with mobile adoption substantially higher at about 92%. Indonesians spend an average of 6.7 hours daily on digital media, including social networks, streaming, and interactive content. The youth demographic drives much of the online activity, fueling demand for mobile gaming and betting platforms.

- YouTube: 89% penetration, leading platform for entertainment and influencers

- Facebook: 78% penetration with strong engagement among adults

- Instagram: 64% penetration, popular with urban youth and lifestyle content

- TikTok: Rapid growth at 52%, dominant among under-25 users

- WhatsApp: Ubiquitous messaging platform used for social and informal gambling communities

- Twitter: 31% penetration, primarily for news and trends

Digital Payment Behavior

Payment methods have diversified, with e-wallets rapidly gaining market share alongside traditional bank transfers and card payments. Digital transactions dominate urban centers, facilitated by widespread smartphone use and fintech innovation. Cryptocurrency use remains niche but growing as an alternative transaction medium within illicit gambling circles.

- GoPay: Leading e-wallet with over 70 million active users

- OVO: Strong urban wallet growing among millennials

- DANA: Popular for small online transactions and remittances

- Bank Transfers: Widely used for larger payments and payroll

- Credit/Debit Cards: Increasing in online retail but less in gambling due to restrictions

- Cryptocurrencies: Emerging for privacy-focused gambling transactions

Gaming and Gambling Preferences

Current Market Participation

Despite legal prohibitions, an estimated 3 million Indonesians actively participate in online gambling. The most popular activities include slot games, online poker, sportsbook betting, lottery, and casino table games, reflecting typical market trends across Asia.

- Slot games – highest participation due to ease of access and variety

- Online poker – popular for skill-based gaming and community engagement

- Sports betting – increasing interest, especially in football and badminton

- Lottery games – traditional and digital formats widely played

- Casino table games (blackjack, roulette) – niche but stable segment

Consumer Behavior Patterns

Players typically engage in short, frequent gaming sessions with peak activity during evenings and weekends. Mobile platforms dominate access, with preferences for user-friendly, fast-loading apps optimized for low-bandwidth conditions. Retention depends on promotional offers, social interactivity, and game variety, though regulatory risks create frequent disruptions.

Spending is unevenly distributed, with a small percentage of high-value players contributing disproportionately to market revenues. Despite risks, consumers demonstrate loyalty to offshore operators providing local language content and convenient payment options, underscoring potential if regulation evolves.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Indonesia’s internet penetration hits approximately 77%, heavily supported by mobile broadband connectivity which accounts for over 85% of total internet usage. Fixed broadband remains limited, concentrated in urban areas where fiber optic infrastructure and public Wi-Fi hotspots are expanding steadily. Average mobile network speeds range from 20 to 35 Mbps, with fixed broadband capable of exceeding 50 Mbps in major cities.

5G and Future Technology Deployment

Rolling out since early 2024, Indonesia’s 5G network covers more than 45% of populated areas, primarily in Jakarta, Surabaya, and Bali. The government targets nationwide 5G availability by 2027, with network operators actively expanding coverage and infrastructure investment. The competitive landscape comprises several dominant operators pushing aggressive 5G adoption plans that are integral to improving digital services, including emerging technologies relevant for gaming and streaming.

Mobile Technology Ecosystem

Indonesia’s mobile market is highly developed with smartphone adoption surpassing 70% of the population, driven by affordable mid-range Android devices. Device preferences show dominance by brands like Samsung, Xiaomi, Oppo, and Vivo, favored for their price-performance balance. Mobile device use significantly influences internet consumption patterns, gaming preferences, and payment behavior given its accessibility and efficiency.

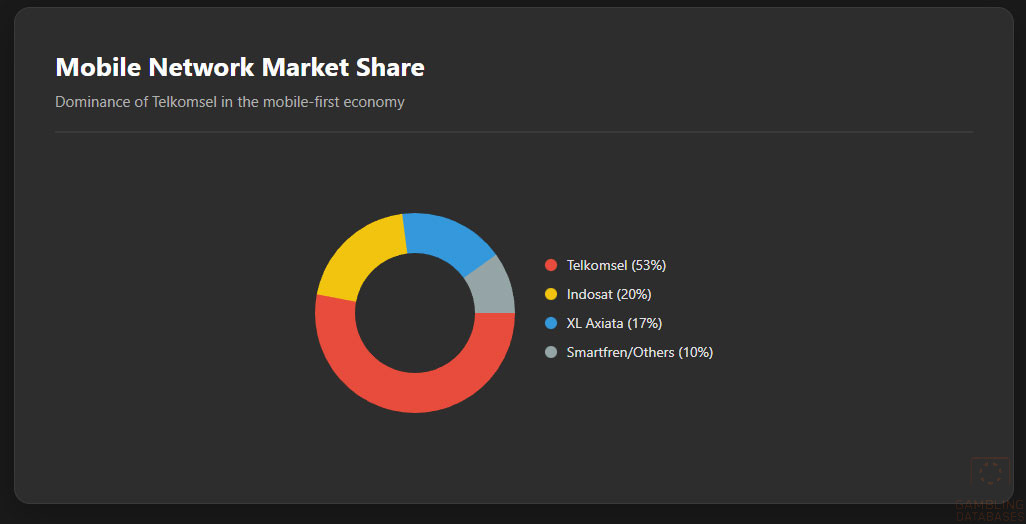

- Telkomsel: Market leader with 53% share, strong prepaid customer base

- Indosat Ooredoo: Holds 20% market share, focusing on urban youth segments

- XL Axiata: Represents 17% share, known for data-centric packages

- Smartfren: Smaller operator with 8% share, innovating on 4G and 5G

- By.U: Digital-first operator targeting millennials and Gen Z

Financial Services and Payment Infrastructure

Indonesia’s banking sector underpins a growing digital economy with over 70% of adults holding bank accounts and increasing adoption of mobile banking. Major banks have embraced digital transformation allowing seamless services, crucial for e-commerce and online betting payment flows.

- Bank Mandiri: Largest bank with extensive digital banking platform and nationwide reach

- Bank Central Asia (BCA): Market leader in digital transactions and retail banking

- Bank Rakyat Indonesia (BRI): Focused on microfinance and rural accessibility

- Bank Negara Indonesia (BNI): Strong corporate banking presence with digital services

- Permata Bank: Innovator in digital-only account services and investment platforms

Payment processing showcases diverse methods with credit/debit card penetration rising but constrained by limited issuer networks. E-wallets dominate digital payments with platforms like GoPay, OVO, and DANA facilitating instant, mobile-centric transactions. Bank transfers remain integral for larger transactions, while fintech innovations enhance financial inclusion.

- GoPay: Largest e-wallet with extensive ecosystem integration

- OVO: Strong presence in e-commerce and transport sectors

- DANA: Popular for remittances and bill payments

- Credit/Debit Cards: Mainly Visa and Mastercard networks, growing online

- Bank Transfers: Trusted for high-value and B2B payments

- Cryptocurrency: Limited but growing adoption in niche markets

E-commerce and Digital Economy

Indonesia’s e-commerce market surpassed a valuation of $50 billion in 2024, with an annual growth rate exceeding 15%. Online retail adoption benefits from broad smartphone penetration and improving logistics, with platforms such as Tokopedia, Shopee, and Bukalapak dominating market share.

Consumer trust in digital transaction security and service reliability continues to improve, enhancing opportunities for ancillary sectors such as digital gaming and betting.

Business Environment and Regulatory Framework

Indonesia ranks 73rd in the World Bank’s Ease of Doing Business Index, reflecting moderate challenges in regulatory efficiency and bureaucracy. Business registrations have been streamlined via the Online Single Submission (OSS) system, reducing processing times and enhancing transparency. Foreign investment policies encourage participation but impose strict restrictions in high-risk sectors like gambling.

- Preparation and notarization of founding documents (2-3 weeks)

- Company registration via government online portal (5-7 business days)

- Tax and social security registrations (3-5 days)

- Opening of corporate bank accounts (1-2 weeks)

- Business licensing and operational permits (varies by sector)

Foreign entities can establish limited liability companies (PT PMA) or representative branch offices. The preferred structure for iGaming-related activities is the PT PMA, due to full foreign ownership possibilities and operational flexibility. However, gambling-related licenses are unavailable due to prohibitions, limiting legal incorporation for operators serving local markets directly.

- Limited Liability Company (PT PMA): Full foreign ownership, suitable for tech and service ventures

- Representative Office: Limited activity scope, no revenue generation

- Foreign Branch Office: Requires parent company accountability, regulated by foreign investment law

Company registration demands multiple documents including Articles of Association, domiciliary letter, taxpayer ID, and information about shareholders and directors. Compliance with foreign ownership reporting and capital requirements is mandatory.

- Articles of Association notarized by Indonesian notary

- Domicile Certificate from local government

- Taxpayer Identification Number (NPWP)

- Identity details of shareholders and directors

- Statement of capital investment and business plan

- Company Seal and official stamps

Taxation Framework

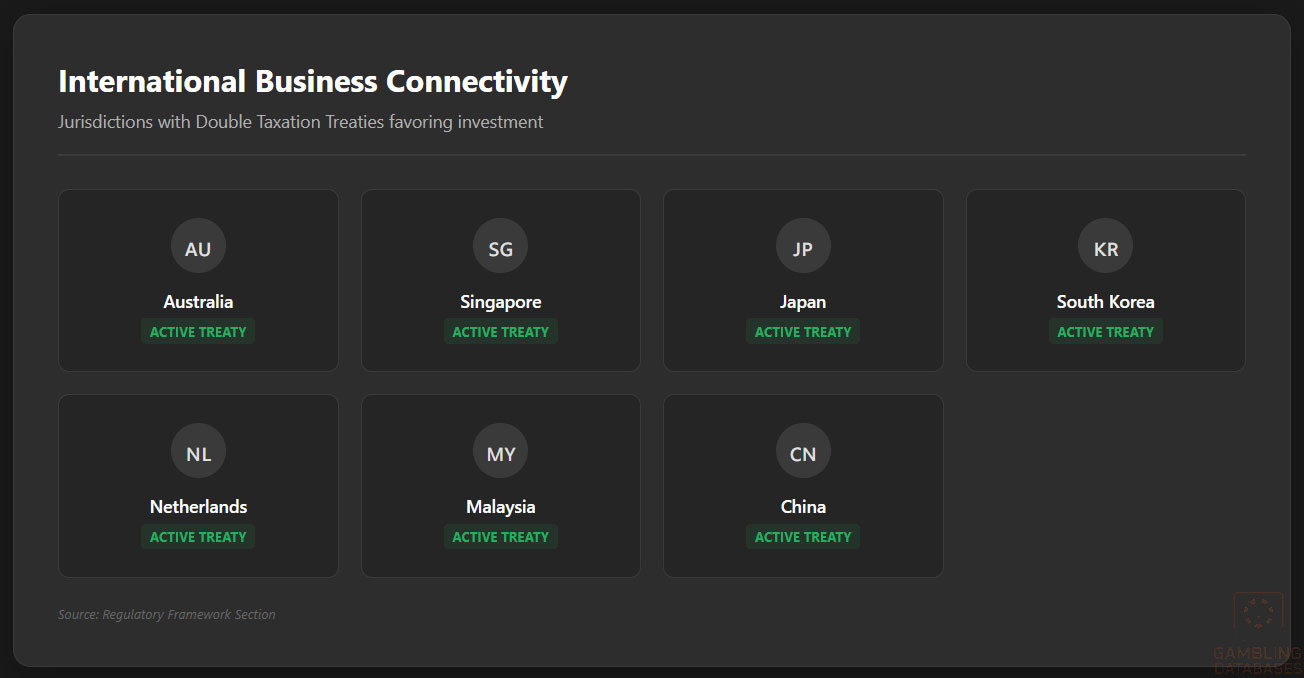

Corporate income tax is set at a standard rate of 22%. Special economic zones offer benefits such as tax holidays and reduced rates to encourage investments in targeted industries, excluding gambling. Indonesia holds double taxation treaties with several countries facilitating international business.

- Australia

- Singapore

- Japan

- South Korea

- Netherlands

- Malaysia

- China

Personal income tax ranges from 5% to 30% progressive rates. Withholding taxes apply on dividends and royalties. Social security contributions are compulsory for all employees. Tax residency rules depend on the 183-day physical presence threshold in a calendar year.

Market Entry Considerations

Entry into Indonesia’s iGaming sector requires careful navigation of the outright prohibition on gambling. Operators often explore indirect strategies such as technology provision, payment processing solutions, or regional partnerships outside of direct gambling operations to access market potential legally.

- Joint ventures with local tech firms to provide ancillary services

- Technology licensing agreements without direct market-facing operations

- Establishing server operations outside Indonesia with regional outreach

- Leveraging digital payment platforms for compatible services

- Engagement in socially responsible promotion and compliance advocacy

Initial setup costs vary widely but demand considerable investment in legal, compliance, and technological adaptation. Typical operational timelines for market entry extend from 4 to 9 months depending on scope and regulatory interactions. Maintaining flexibility in strategic planning allows adaptation to evolving regulations.

- Legal and consulting services: $75,000 – $120,000

- Company registration and licensing setup: $15,000 – $30,000

- Technology and platform integration: $200,000 – $350,000

- Marketing and compliance expenditures: $50,000 – $100,000

- Initial working capital for 6-12 months: $500,000+

| Phase | Duration |

|---|---|

| Document preparation and legal consultation | 1-2 months |

| Company registration and regulatory setup | 1-2 months |

| Technology platform development and testing | 2-3 months |

| Marketing and partnership establishment | 1-2 months |

| Operational launch and compliance monitoring | Ongoing |

Key success factors include navigating complex regulatory frameworks, establishing robust technological infrastructure, and building consumer trust through secure, locally adapted services. The main challenges stem from legal prohibitions, enforcement risk, and fragmented market penetration due to digital restrictions and cultural barriers.

- Strong legal and regulatory expertise to mitigate risks

- Local partnerships to facilitate market knowledge acquisition

- High-quality digital infrastructure for seamless user experience

- Effective digital marketing tailored to local preferences

- Robust compliance and responsible gaming frameworks

- Strict government enforcement and unpredictable regulation

- Limited access to legal banking and payment channels

- Cultural resistance and religious opposition to gambling

- High competition from unlicensed offshore operators

- Infrastructure disparities limiting rural market access

Exit strategies should consider market liquidity and regulatory implications for ownership transfer or divestiture. Since formal licenses are unavailable, asset valuation focuses on technology, user base, and regional operations beyond Indonesian jurisdiction.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Indonesia?

Online gambling is strictly illegal across all categories. The government enforces a comprehensive ban including website blocking, financial transaction monitoring, and criminal penalties. No licensing system exists, and operators or players risk fines and imprisonment. The ban extends to all digital gambling formats such as casino games, poker, and sports betting.

2. What types of gambling licenses are available and what do they cover?

Indonesia does not issue any gambling licenses as all forms of gambling are prohibited. There is no legal framework for regulating operators or issuing licenses. Any provider servicing Indonesian consumers operates without formal approval and faces enforcement risks including site blocking and legal actions.

3. How much does an iGaming license cost and how long does it take to obtain?

Since no gambling licenses are issued legally, there are no associated costs or official timelines for licensing in Indonesia. Operators must consider illegality and enforcement dynamics rather than licensing expenses. Costs typically arise from risk mitigation and circumventing regulatory controls rather than formal license fees.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot obtain a gambling license in Indonesia due to the nationwide prohibition. While foreign investors can establish entities for technology or ancillary services, engaging in actual gambling operations is illegal and exposes companies to criminal and financial penalties under Indonesian law.

5. What are the tax obligations for iGaming operators?

Legally compliant iGaming operators do not exist domestically, so no formal operator tax regime applies. Corporate taxation at 22% applies to registered companies, but illegal operators do not comply. Personal income tax and withholding may apply to winnings. Enforcement focuses mainly on prohibiting and penalizing illicit activities rather than tax collection.

6. Are gambling winnings taxed for players?

Gambling winnings are taxed under general personal income tax regulations, with progressive rates from 5% to 30%. Players are obligated to report all income, including gambling receipts. However, enforcement is limited due to the underground nature of gambling activities, though legal risks remain for unreported income.

7. What are the typical operational costs for running an online casino/sportsbook?

Typical operational costs for market entry include legal consulting ($75,000 – $120,000), company setup ($15,000 – $30,000), technology development ($200,000 – $350,000), marketing expenditures ($50,000 – $100,000), and working capital reserves exceeding $500,000 for stability. Costs vary based on scale, compliance needs, and market penetration strategy.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines generally span 18 to 36 months due to operational complexities, regulatory risks, and competitive pressures. High expenditures on compliance, tech development, and risk management delay profitability. Successful operators require adaptive business models and localized approaches to achieve sustainable returns.

9. What are the local presence requirements for operators?

There are no legal provisions for gambling operators to establish local presence due to the ban. Foreign companies engaging indirectly through technology provision or partnerships must establish locally registered entities, but direct gambling operations remain prohibited with substantial enforcement risks.

10. What payment methods are available and recommended?

Recommended payment methods include e-wallets like GoPay, OVO, and DANA, which offer fast mobile payments suitable for the digital-first population. Bank transfers and card payments are used primarily for larger transactions or regulated online commerce. Cryptocurrency remains niche but offers privacy advantages in illicit gambling segments.

11. What are the advertising and marketing restrictions?

All advertising and promotion of gambling are banned. This includes online, broadcast, social media, and outdoor channels. The government enforces content removal aggressively and penalizes violators including influencers promoting gambling content. Sponsorships and direct promotions are strictly prohibited.

12. What responsible gambling measures are mandatory?

Due to gambling’s illegal status, mandated responsible gambling frameworks are not formally implemented. However, government digital policies focus on youth protection, public awareness campaigns, and restricting access to minimize harm in illicit markets. Operators may voluntarily adopt responsible gaming tools to build consumer trust if legally feasible.

13. How large is the iGaming market and what is the growth potential?

The estimated illegal iGaming market features over 3 million active players with transaction volumes exceeding $25 billion. Despite risks, the market shows projected growth at 5-6% CAGR owing to increasing mobile internet use and digital payment adoption. Regulatory tightening may limit growth but latent demand remains strong.

14. Who are the main competitors and what is their market share?

The market lacks legally licensed operators. Instead, offshore platforms dominate, targeting Indonesian users via VPN and proxies. Key operators include major Asian and global betting brands offering localized language content and payment integration. Competitive advantage relies on technology agility and regulatory risk tolerance.

15. What are the player preferences and typical spending patterns?

Players prefer slot games, followed by poker, sports betting, lottery, and table games. Sessions are usually short but frequent, peaking during evenings and weekends. Spending is uneven, with a small percentage of high rollers contributing most revenue. Mobile platforms and local-language offerings dominate user preference.

16. What are the key success factors and main challenges for new entrants?

Key success depends on compliance expertise, strong local partnerships, technological innovation, and effective marketing adapted to local culture. Challenges include regulatory prohibitions, payment restrictions, cultural resistance, and market fragmentation. Operators must balance risk with extensive due diligence and adaptive strategies for long-term viability.

Sources and References

- Indonesia Ministry of Communication and Information Technology – https://kominfo.go.id

- National Statistics Bureau of Indonesia (BPS) – Population and Economic Data 2025 – https://bps.go.id

- Bank Indonesia – Financial and Banking Reports 2024-2025 – https://bi.go.id

- Ministry of Finance Indonesia – Taxation Guidelines – https://www.djponline.pajak.go.id

- World Bank – Ease of Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union – Indonesia ICT Statistics – https://www.itu.int

- Telkomsel Investor Reports 2025 – https://telkomsel.com

- Indonesia Financial Services Authority (OJK) – Oversight Documents – https://ojk.go.id

- IGN Asia – Indonesian iGaming Market Update 2025

- European Gaming & Betting Association – Market Reports 2025

- Statista – Indonesia Digital and Mobile Usage Data 2025

- Palapa Ring Project – National Infrastructure Development – https://palaparingsat.com

- Indonesia Internet Service Providers Association – Market Data 2025

- Ministry of Trade Indonesia – E-commerce Market Reports 2024

- Indonesian Ministry of Social Affairs – Public Health and Gambling Awareness Programs 2025

- Asian Development Bank – Regional Telecommunication Data 2024

- GamblingInsider – Indonesia Regulatory Developments 2025

- RichAds – Online Gambling Legal Landscape Indonesia 2025

- IGaming Today – Southeast Asia Market Analysis 2024-2025

- LawRange – Gambling Licensing Procedures in Asia

- World Economic Forum – Digital Economy Rankings 2024

- GoPay, OVO, and DANA Annual Reports 2025

- Indonesia Ministry of Youth and Sports – Sports Betting Trends Report 2025

- Statista – Mobile Network Operator Market Shares Indonesia 2025

- Shopee and Tokopedia Financials 2024-2025

- Indonesian Ministry of Religious Affairs – Cultural and Social Guidance Reports

- Academic Research on Gambling Behavior Indonesia – Journal of Southeast Asian Studies 2024

- Central Bureau of Statistics Indonesia – Education and Literacy Surveys 2025

- Digital Economy Indonesia Report – GSMA Intelligence 2025

- Indonesia Cybersecurity Bureau Annual Threat Report 2024

🎯 Gambling Databases Country Rating: Indonesia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 0.5/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.2/10 | Black Market / Radioactive |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE PROHIBITION: All forms of gambling (online and land-based) are completely illegal under Article 303 of the Criminal Code (KUHP) and Law No. 11 of 2008 on Electronic Information and Transactions.

- CRIMINAL PENALTIES: Operators and habitual offenders face imprisonment of up to 10 years (general law) or specific statutes citing up to 6 years prison and fines up to IDR 1 billion ($65,000+).

- AGGRESSIVE ENFORCEMENT: The Ministry of Communication (Kominfo) has blocked over 800,000 gambling URLs and domains as of 2024.

- FINANCIAL FREEZING: Authorities froze over 6,400 bank accounts linked to gambling in 2024 alone. Financial institutions are legally mandated to report and block these transactions.

- ADVERTISING BAN: A total ban on all gambling advertising exists. Influencers and social media figures promoting gambling sites are actively arrested and prosecuted.

- RELIGIOUS OPPOSITION: As the world’s largest Muslim-majority nation, gambling is strictly forbidden (haram), leading to high social vigilance and reporting of operators by the public.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Illegal with enforcement (-1.0). Online casino prohibited (-1.5). Active ISP blocking (-0.5). Affiliate prosecution (-0.5). Score is effectively negative, floored at 0. |

| Licensing Process | 25% | 0.0/2.5 | No licensing available (0). There is no mechanism to apply for a license; any operation is a criminal offense. |

| Taxation & Costs | 20% | 0.0/2.0 | While there is no “tax,” the cost of business includes asset seizure, bank account freezing, and criminal defense. High operational costs to evade blocking (-0.5). Extreme CAC due to ad bans (-0.5). Final: 0.0/2.0. |

| Operational Requirements | 15% | 0.0/1.5 | Excessive requirements (0). To operate, one must use mirror sites, cloak payments, and hide ownership to avoid arrest. Crypto and credit cards are actively monitored/blocked (-0.5). |

| Market Environment | 10% | 0.0/1.0 | Difficult environment (+0.25). Advertising completely banned (-0.5). Active enforcement against offshore operators (-0.25). Enforcement against affiliates (-0.25). Final: 0.0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal with player penalties (0). Players are subject to arrest and imprisonment under Article 303. Major product bans (-1.5). |

| Practical Accessibility | 30% | 0.5/3.0 | Severe restrictions (+0.5). VPN required (-0.5). Active ISP blocking of 800k+ sites (-0.5). Banks freeze accounts (-0.5). Access is technically possible but highly difficult/risky. |

| Player Penalties | 20% | 0.0/2.0 | Criminal penalties possible (0). Players can face jail time and fines. Raids on internet cafes and personal devices occur. |

| Market Availability | 10% | 0.0/1.0 | No licensed operators (0). All access is via illegal offshore entities that are constantly hunted by Kominfo. |

🔍 Key Highlights

Strengths (Theoretical Only)

- Population Size: 280 million people, 4th largest in the world.

- Mobile Penetration: 92% mobile penetration creates a massive, albeit illegal, addressable market.

- Market Value: Estimated $25.79 billion (Rp 400 trillion) in illegal transaction volume shows high demand despite bans.

⛔️ CRITICAL RISKS AND CHALLENGES

- Zero-Tolerance Policy: The government treats gambling eradication as a priority similar to drug enforcement.

- Financial Stranglehold: The OJK (Financial Services Authority) orders banks to block accounts. Payment processing is the single biggest failure point; finding reliable payment rails is nearly impossible long-term.

- ISP Filtering: “TrustPositif” internet filtering system is aggressive, blocking gambling domains and IP addresses automatically.

- Social Vigilance: Public reporting hotlines exist for citizens to report gambling sites and neighbors who gamble.

- Affiliate Crackdown: Police actively target “endorsers” and influencers on Instagram/TikTok who promote gambling sites, resulting in public arrests.

Player-Specific Issues

- Criminal Liability: Unlike many grey markets, the player is criminalized in Indonesia.

- Asset Forfeiture: Winnings found in bank accounts can be seized as proceeds of crime.

- Scam Risk: Due to illegality, players have no recourse if an offshore operator refuses to pay.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $500,000+ (Mostly for cloaking tech, mirror domains, and disposable payment accounts).

Monthly Operating Costs: High. You will burn through payment processors and domains weekly.

Effective Tax Rate on Revenue: N/A (Illegal). However, expect 20-30% of revenue to be lost to payment friction and account freezes.

Customer Acquisition Cost: Extreme. You cannot advertise. You must rely on SEO (which is fought by Kominfo) or high-risk SMS/WhatsApp spam.

Time to Breakeven: Unknown. One police raid or bank freeze can wipe out 100% of working capital instantly.

Profitability Assessment: Prohibitive. While the transaction volume is high ($25B), this revenue is captured by criminal syndicates willing to risk imprisonment. For a legitimate business or standard offshore operator, the risk-to-reward ratio is mathematically broken.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | Website blocking, bank account seizure, international arrest warrants via Interpol. |

| Licensed Sports Betting Operators | Critical | There is no distinction between sports betting and casino. All are banned equally. |

| Affiliates/Advertisers | Critical | High priority targets for local police. Arrests of influencers are common and public. |

| Payment Processors | Critical | Risk of losing banking license, money laundering charges, and asset seizure. |

| Company Directors/Executives | High | Do not travel to Indonesia. Risk of detention if identified. |

🚨 Extradition and International Enforcement

Extradition Treaties: Indonesia has extradition treaties with Australia, Malaysia, Philippines, Singapore, Thailand, China, and South Korea. They cooperate closely with ASEAN police forces (ASEANAPOL).

Enforcement History: Indonesia frequently coordinates with Cambodian, Philippine, and Malaysian police to raid call centers targeting Indonesian players and deport suspects back to Jakarta for trial.

Safe Jurisdictions: Few. Even without a treaty, Indonesia uses diplomatic pressure to deport gambling operators from neighboring Asian countries.

Travel Risk: EXTREME. If you are a director of an operator targeting Indonesia, entering the country puts you at immediate risk of arrest.

📋 Final Verdict

Indonesia receives an Operator Ease Score of 0.0/10 and a Player Access Score of 0.5/10, resulting in an overall market attractiveness rating of 0.2/10.

HONEST ASSESSMENT: Indonesia is a hostile, no-go zone for any legitimate iGaming business. The government utilizes a “total war” approach involving internet censorship, financial sector blacklisting, and criminal prosecution of both operators and players. While the demand is massive, it is exclusively serviced by black-market syndicates willing to face prison time; there is absolutely no pathway for grey-market or white-label entry.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NO ONE. There are no legal pathways for entry.

❌ Definitely Avoid If You Are:

- A Publicly Traded Company: Operating here is a compliance violation that will de-list you.

- A Licensed Offshore Operator: You will risk your Tier-1 licenses (MGA, UKGC) by operating in a criminally prohibited black market.

- Dependent on Stable Payments: Payment channels are shut down constantly.

- Concerned about Staff Safety: Marketing staff and affiliates within Indonesia face real prison time.

⚠️ BOTTOM LINE: This is a criminal market, not a business opportunity. Stay away entirely.