Iran presents a uniquely challenging but sizable market for the iGaming sector. Despite strict prohibitions under Islamic law, an expansive and predominantly young population with growing internet and mobile adoption fuels substantial underground demand for online gambling.

The complete absence of legal licensing and harsh enforcement characterize the regulatory environment, making market entry complex and high risk. This analysis focuses on Iran’s regulatory framework as the essential foundation for understanding the broader market context.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Population | 87+ million |

| Median Age | 32 years |

| Youth Population Percentage (under 30) | 50%+ |

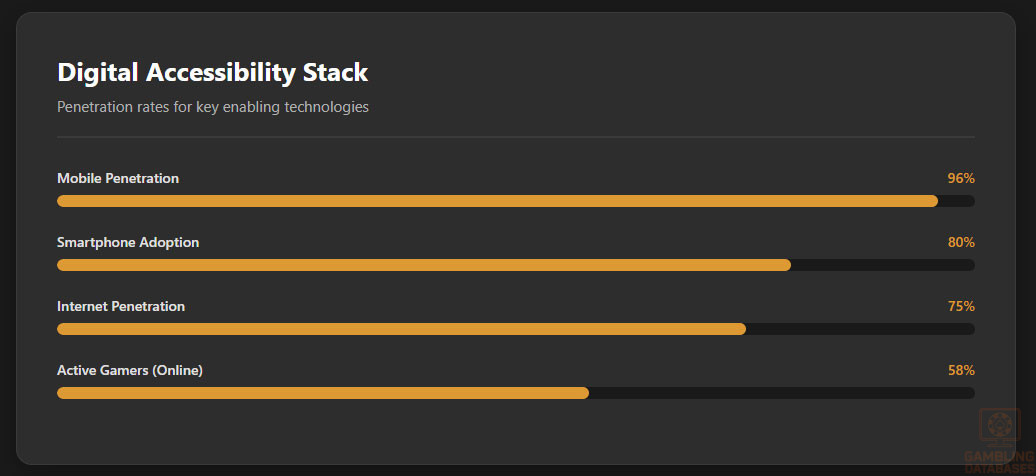

| Internet Penetration Rate | 75%+ |

| Mobile Penetration Rate | 96% |

| Online Gaming Participation | 58% |

| Legal Gambling Status | Strictly prohibited under Islamic Penal Code, Article 705 |

| Gambling Penalties | 1-6 months imprisonment and up to 74 lashes |

| Licensed Operators Allowed | None (No licensing framework exists) |

| Regulatory Authority | None for gambling; AML bodies monitor financial crimes |

| Taxation on Gambling | None (Illicit activity not taxed) |

| Estimated Illegal Market Size (Revenue) | Hundreds of millions USD annually (estimated) |

| Market Growth Rate (Underground) | Positive; increasing despite enforcement |

| Major Enforcement Actions | 2024 shutdown of Nitro Bet network |

| Popular Payment Methods (Illegal) | Cryptocurrencies, VPNs |

| Local Gambling Platforms | None legal; domestic game stores exclude gambling |

| Foreign Operator Market Presence | International offshore brands (888 Casino, Betway) serving Iranians |

| Compliance Focus | Law enforcement, financial transaction monitoring |

| Application Process for License | Not available |

| Operational Physical Presence Required | Not applicable (illegal) |

| Advertising Allowed | None (strictly banned) |

| Reported iGaming Market CAGR (Global comparison) | 8-10% globally; Iran underground market growing |

| Avg. Gamer Age | 25 years |

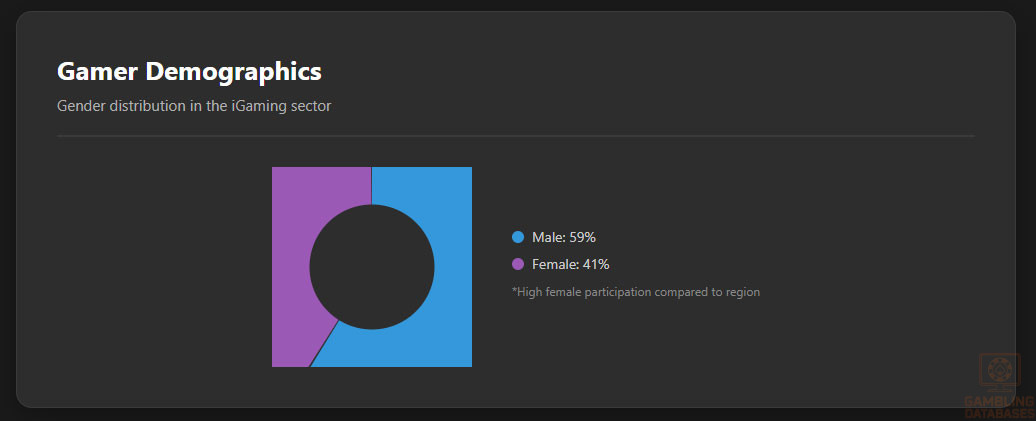

| Female Gamers | 41% |

| Business Environment Ease | Highly restrictive for gambling |

| Anti-Money Laundering Oversight | Present via Financial Intelligence Unit |

| Industry Outlook | Continued crackdown expected; no legalization planned |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling activities in Iran are unequivocally prohibited under the Islamic Penal Code, rooted in Islamic law which deems games of chance haram (forbidden). Article 705 explicitly bans all forms of gambling including land-based casinos, sports betting venues, lotteries, and online gambling platforms. Violators face severe penalties ranging from imprisonment of one to six months, to corporal punishment such as lashes, or both if offenses are public.

Law enforcement agencies actively monitor and intervene against gambling operations. The government employs technical measures including blocking access to gambling websites and restricting financial transactions to combat illegal activities. Although these efforts have dismantled some major gambling networks, underground gambling persists, supported by widespread digital penetration and sophisticated circumvention technologies such as VPNs and cryptocurrencies.

Land-Based Gambling Activities

Due to the stringent prohibitions, no legal land-based gambling venues exist in Iran. This includes the absence of operational casinos, dedicated sports betting shops, slot machine halls, or lottery offices. Any attempt to operate such venues is met with criminal prosecution and state crackdown. The illicit market operates clandestinely with no public visibility or legal recourse for participants.

Online Gambling Framework

The entire online gambling sector in Iran is illegal, with no recognized regulatory authority or licensing framework. Digital gambling platforms face intense opposition from government cyber-policing units. Measures include website blocking, financial transaction monitoring, and criminal prosecution of operators and users.

Licensed Operators and Market Players

No operators hold official licenses since all gambling activities are criminalized. The market consists mainly of offshore international operators providing services remotely to Iranian players using global platforms.

Brands like 888 Casino and Betway tailor offerings with Farsi interfaces and cryptocurrency options to cater to Iranian users. The lack of regulation means operators have no legal protections, but the demand sustains a competitive underground ecosystem.

Licensing Framework and Requirements

Application Process and Eligibility

Iran does not offer any form of legal gambling licensing, as designing, launching, or operating gambling businesses is a criminal offense. No regulatory authority exists to issue licenses or oversee operators. Consequently, there are no application procedures, fees, or financial and technical prerequisites associated with licenses in Iran.

Local Presence and Operational Requirements

Since gambling operations are illegal, there is no requirement or allowance for local physical presence for gambling businesses. Foreign ownership or partnerships relevant to gambling ventures are forbidden. Online operators serving Iranian users function extraterritorially without domain registration or operational offices inside Iran, employing technological circumvention instead of formal regulatory compliance.

Compliance Obligations and Monitoring

Player Protection and Identification

With no formal licensing or regulatory framework, there are no official player protection mechanisms or responsible gambling measures mandated by law. Age verification, KYC (Know Your Customer), and AML (Anti-Money Laundering) protocols are not enforced in the gambling context. However, Iran’s financial intelligence units scrutinize suspicious financial transactions for money laundering risks associated with underground gambling activities.

Financial Monitoring and Reporting

Financial compliance efforts focus on monitoring and restricting transactions linked to illegal gambling. Banks and financial institutions cooperate with authorities to block payments to gambling operators. Law enforcement pursues sequential actions from detection, investigation, account freezing, to prosecution of involved parties. Operators and players have no legal reporting obligations as gambling is illicit.

- Detection of suspicious transactions via banking systems

- Investigation by financial intelligence and police

- Freezing of accounts and financial assets

- Legal prosecution and enforcement actions

Taxation Structure and Financial Obligations

Player Taxation

There is no tax regime for gambling winnings or player profits in Iran due to the illegal status of all gambling activities. Players engaged in underground gambling do so without legal oversight or tax obligations.

Operator Taxation

No taxation framework applies to gambling operators domestically, as no licensed gambling businesses exist. Offshore operators servicing Iranian users are subject to the tax laws of their jurisdictions but face no recognized taxation or fiscal responsibilities within Iran. No license renewal fees, turnover taxes, or gambling-specific corporate tax mechanisms operate in the country.

| Tax Aspect | Status |

|---|---|

| Player Winnings Tax | Not applicable (illegal activity) |

| Operator Gross Gaming Revenue Tax | None |

| Corporate Income Tax (Legal businesses only) | N/A for gambling operators |

| License Fees | None (no licenses issued) |

| Turnover Tax | None |

Gambling Market Financial Performance

Owing to the illicit and underground nature of the gambling sector, no official financial data is available. Independent estimates suggest market revenues run into hundreds of millions USD annually and continue to grow. The market is characterized by steady wagering volumes, high demand for online betting and casino games, and continuous reinvestment in new clandestine platforms.

Advertising and Marketing Restrictions

Advertising of gambling is completely prohibited in Iran. There are no authorized channels for promotional activities, no permitted content types, and no legal sponsorship opportunities for gambling entities. Marketing bans extend across digital platforms, print media, and public spaces, with violations attracting severe penalties.

- All forms of gambling advertising banned

- No social media or online promotion allowed

- No sponsorship of sports or entertainment events

- Strict prohibition on public gambling promotion

- Enforcement includes monitoring of digital ads and social networks

Recent Regulatory Changes and Their Impact

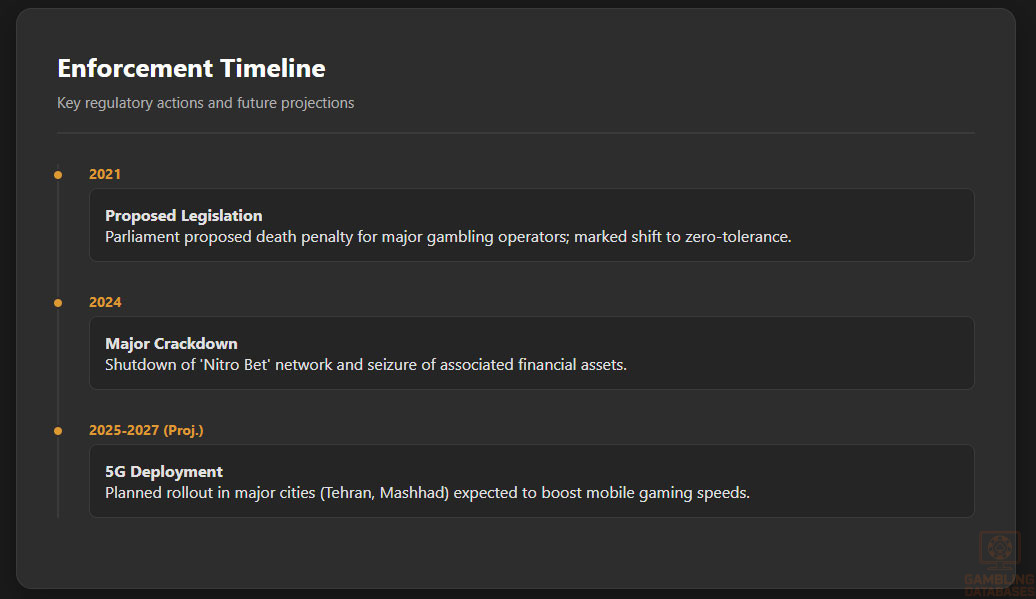

Recent crackdowns illustrate Iran’s firm stance against illegal gambling. The notable 2024 shutdown of the major Nitro Bet online gambling network highlights intensified government action.

Proposed legislation in 2021 suggested even harsher penalties including the death penalty for some operators, although it was not enacted. Enforcement trends indicate a continuous tightening of controls, significantly raising operational risks and costs for underground market players.

Enforcement Mechanisms and Penalties

Penalties for gambling offenses are severe, combining imprisonment, corporal punishment, and hefty fines. Law enforcement agencies employ multiple mechanisms to uphold bans including cyber monitoring, financial transaction blocking, and public prosecutions. These measures collectively serve as a strong deterrent, although illegal activity endures due to socio-economic demand.

- Imprisonment from 1 to 6 months

- Up to 74 lashes for public offenses

- Monetary fines based on case severity

- Blocking and seizure of gambling websites

- Arrest and prosecution of operators and players

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Iran’s total population exceeds 87 million, with demographics dominated by a young and growing cohort. The median age is approximately 32 years, reflecting a youthful population that represents a dynamic consumer base for digital entertainment, including iGaming. Gender distribution is relatively balanced, with a slight male majority at around 51% male to 49% female.

Urbanization is notable, with nearly 75% of the population residing in urban areas, providing concentrated markets with better infrastructure and internet access. Rural regions remain less penetrated by digital technologies but still contribute to burgeoning online consumption trends as connectivity improves.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 24% |

| 15-29 years | 28% |

| 30-44 years | 22% |

| 45-59 years | 16% |

| 60+ years | 10% |

Geographic Distribution

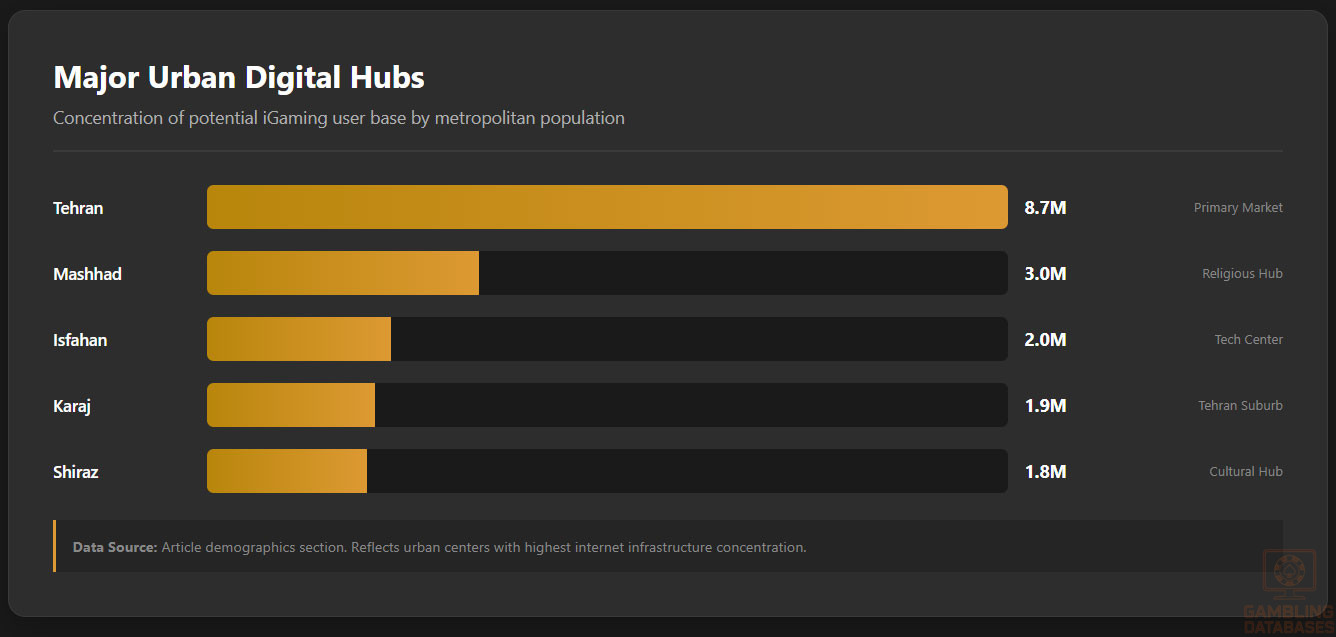

The population is concentrated in several major metropolitan areas that serve as economic and cultural hubs. These cities exhibit higher income levels and more advanced technological infrastructure, encouraging digital entertainment adoption. Internet penetration and mobile connectivity are significantly higher in these regions.

- Tehran – Over 8.7 million residents

- Mashhad – Approximately 3 million residents

- Isfahan – Around 2 million residents

- Karaj – Roughly 1.9 million residents

- Shiraz – Close to 1.8 million residents

- Tabriz – Approximately 1.5 million residents

These urban centers also show the greatest concentration of internet users and digital payment adoption, leading the underground gambling market’s active user base. Regional economic disparities impact disposable income, with urban areas providing more favorable conditions for iGaming participation.

Economic Indicators and Consumer Spending Power

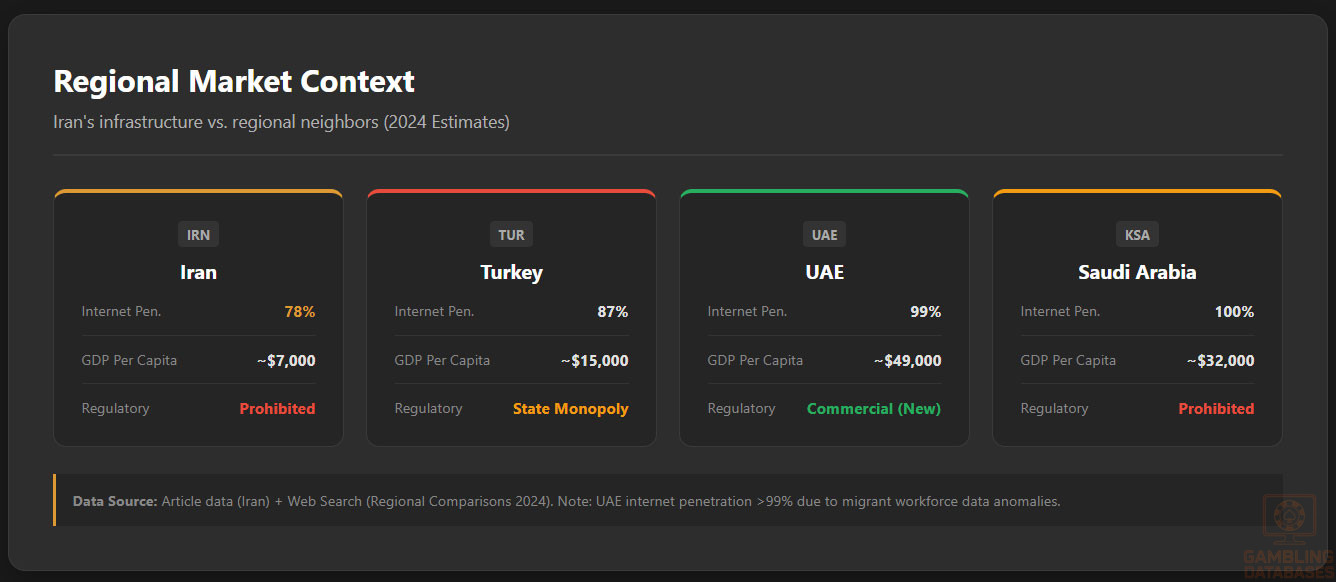

Iran’s economy showed resilience with a GDP exceeding $600 billion in 2024, supported by diverse sectors including services, manufacturing, and natural resources. Despite sanctions impacting growth, economic reforms aim to stabilize and increase per capita income, currently around $7,000, with ongoing inflation challenges.

The service sector dominates at approximately 50% of GDP, driven by telecommunications, retail, and financial services. Industry and agriculture account for roughly 35% and 15%, respectively, highlighting a transitioning economy with expanding urban middle classes.

Disposable income growth remains uneven due to inflation and sanctions, yet consumer spending on digital services and entertainment continues to rise, reflecting changing consumption patterns favoring online engagement.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $610 billion |

| GDP Growth Rate | 2.5% |

| Per Capita Income | $7,050 |

| Inflation Rate | 22% |

| Service Sector Contribution | 50% |

| Industry Sector Contribution | 35% |

| Agriculture Sector Contribution | 15% |

Income and Wealth Distribution

Income distribution in Iran reveals noticeable inequality, with a Gini coefficient around 0.38 indicating moderate disparity. The middle class is expanding but faces pressure from inflation and sanctions. Average household disposable income varies widely between urban and rural areas, with urban households having significantly higher spending power.

Consumer spending is increasingly oriented toward technology and entertainment, particularly among younger demographics. Online services, including mobile gaming and digital streaming, attract rising expenditure despite broader economic constraints.

Market Size and Growth Projections

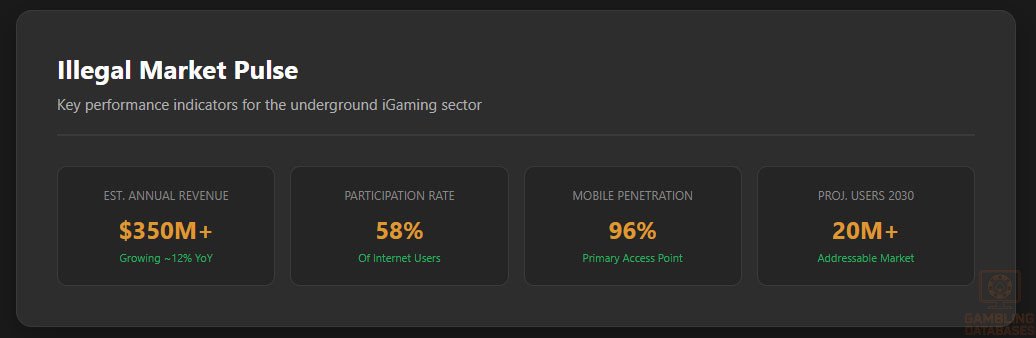

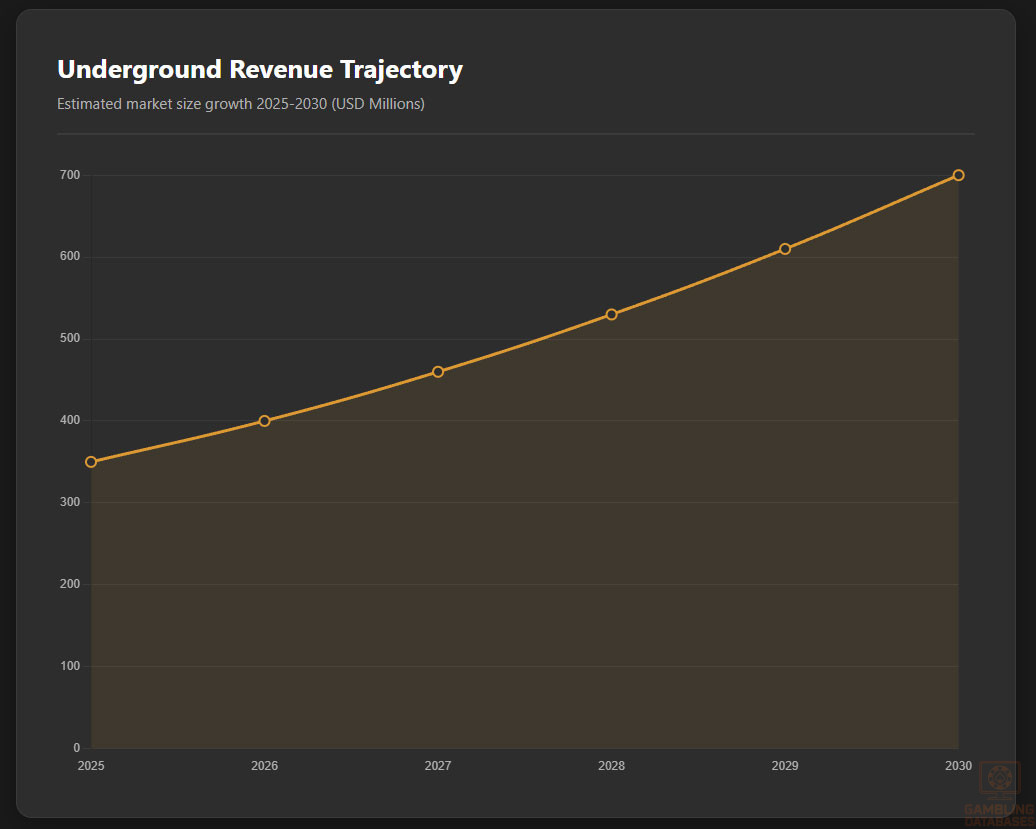

Though illegal, Iran’s underground iGaming market is estimated to generate several hundred million USD annually, buoyed by continuous growth in internet penetration and mobile adoption. Market revenue estimates indicate a CAGR of approximately 12-15% over the next five years, driven by increased smartphone use and digital payment adoption.

Projected user base is expected to exceed 20 million active digital game players by 2030, with Average Revenue Per User (ARPU) increasing as digital wallets and cryptocurrencies ease payment processes. Market expansion is strongly tied to demographic youthfulness and rising digital literacy.

| Metric | Value |

|---|---|

| Estimated Market Revenue 2025 | $350 million |

| Estimated Market Revenue 2030 | $700 million |

| Compound Annual Growth Rate (CAGR) | 12-15% |

| Active iGaming Users 2025 | 12.5 million |

| Projected Users 2030 | 20+ million |

| Average Revenue Per User (ARPU) | $28 – $35 annually |

Education, Skills, and Digital Literacy

Iran exhibits a high literacy rate of over 85%, with widespread enrollment in secondary and tertiary education institutions. Digital literacy is improving rapidly, particularly among urban youth and university graduates, who constitute the majority of online activity participants.

Technical skills in IT and software development are growing, supported by government and private sector initiatives. This environment fosters a digitally savvy population capable of engaging with complex online platforms, including gaming and gambling services despite legal prohibitions.

Cultural and Social Factors

Communication and Language

Persian (Farsi) is the official language, universally spoken and used online. Minority languages include Kurdish, Azeri, Arabic, and Baluchi, but digital content in these is limited. Internet language preference is primarily Persian, with English serving as a secondary language for business and some entertainment sectors.

Cultural Attitudes

Gambling is widely considered socially and religiously unacceptable, heavily influenced by Islamic prohibition. Public opinion largely condemns gambling due to moral and legal factors. However, underground activity and foreign operator presence indicate a disconnect between official attitudes and private consumer behavior.

Foreign brands are viewed with curiosity and some skepticism, but strong interest in international online markets persists, especially for entertainment and economic opportunity. Users favor platforms offering Farsi interfaces and local payment solutions to navigate restrictions.

Problem Gambling and Social Considerations

Data on problem gambling is scarce given the illicit market context, but anecdotal evidence suggests increasing concern among experts. Social stigma limits open discussion and formal support options are minimal. Governmental programs addressing gambling-related harms are essentially nonexistent.

- Limited public awareness campaigns on gambling risks

- No government-supported addiction treatment services focused on gambling

- NGO involvement in mental health and behavioral disorders

- Community awareness programs in urban youth centers

- Online forums providing peer support for compulsive behaviors

Political Structure and Governance

Iran operates under an Islamic Republic political system combining theocratic and democratic elements, leading to stable but highly centralized governance. Regulatory consistency regarding gambling is steadfast, reflecting religious laws integrated into the legal framework. International relations, including sanctions, restrict some business activities but have limited impact on internet-based consumer demand.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at over 75% with daily usage averaging 4.5 hours, spurred by affordable mobile data and smartphone availability. Mobile adoption exceeds 95%, with smartphones as primary access devices. Social media engagement is robust, fostering a digitally connected population engaged in multi-platform content consumption.

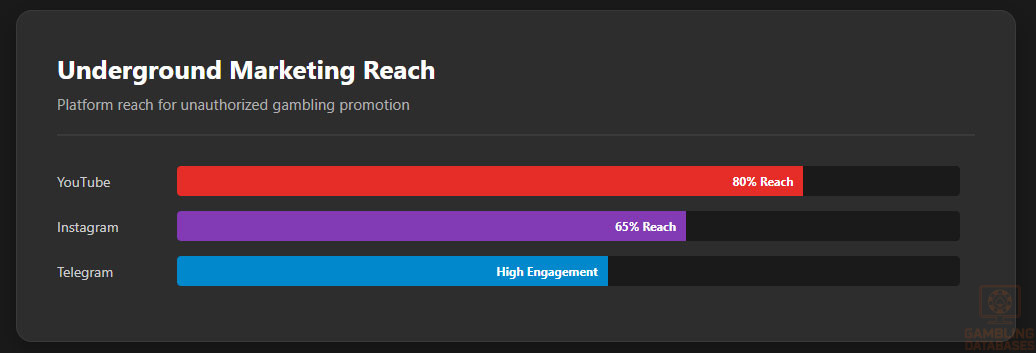

Popular social media platforms include:

- Instagram with 65% penetration focused on visual content

- Telegram widely used for messaging and information sharing

- WhatsApp for private communication

- YouTube for video streaming with 80% reach

- TikTok experiencing rapid growth among younger audiences

- Twitter used primarily for news and public discourse

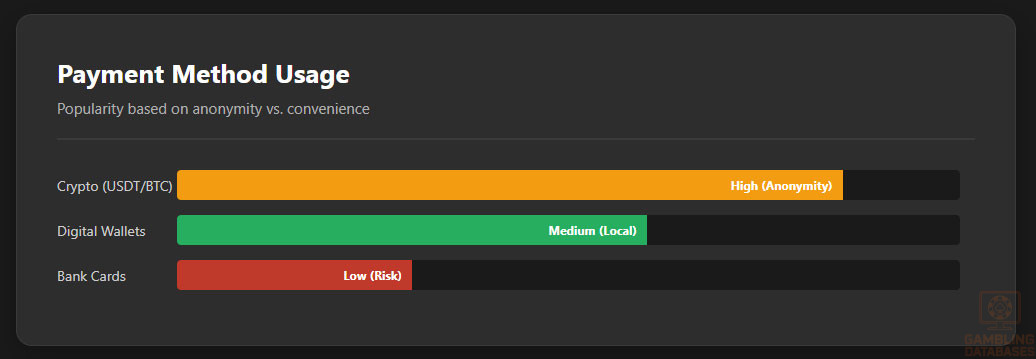

Digital Payment Behavior

Online payment adoption is growing, driven by young, tech-savvy consumers using digital wallets and cryptocurrencies to navigate sanctions and banking restrictions. Traditional bank cards have limited international usability, increasing reliance on alternative methods.

Key digital payment methods include:

- Cryptocurrencies, especially Bitcoin and Tether

- Mobile money wallets such as Zarinpal and Pay.ir

- Prepaid virtual cards for international payments

- Bank transfers domestically for e-commerce

- Cash-based payment services coupled with digital vouchers

Gaming and Gambling Preferences

Current Market Participation

Despite prohibitive laws, over 58% of internet users engage in some form of online gaming, with sports betting, online poker, and casino games as the most popular activities. Betting on football dominates, given the sport’s broad appeal and cultural significance.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting (Football) | 42% |

| 2 | Online Poker | 30% |

| 3 | Casino Slot Games | 25% |

| 4 | Lottery and Number Betting | 15% |

| 5 | Esports Betting | 10% |

Consumer Behavior Patterns

Consumers predominantly favor mobile platforms for accessibility and anonymity. Sessions average 45 to 60 minutes, typically during evening hours after work or study. Spending patterns show moderate bet sizes with frequent small transactions. Retention is driven by localized content and hassle-free payment options adapted to circumvent restrictions.

Players demonstrate high engagement with interactive features such as live betting and multiplayer formats, with growing interest in cryptocurrency-integrated platforms. Privacy and security concerns steer demand toward offshore operators with reputation for discretion.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Iran boasts an internet penetration rate surpassing 75%, with high mobile connectivity facilitating widespread digital engagement. Broadband services are available across major cities, but rural areas still face infrastructure limitations. Average internet speeds are moderate, approximately 20-30 Mbps, with reliability affected by regional sanctions and infrastructure upgrades.

The government continues investing in digital infrastructure, emphasizing increased network coverage and quality. The growth of fiber-optic networks and mobile broadband expansion reflects efforts to modernize communication channels. Despite challenges, Iran’s internet sector remains dynamic, supporting the rapid growth of online activities, including unauthorized gambling platforms.

5G and Future Technology Deployment

Currently, 5G coverage remains limited but is in the pilot phase in select urban centers such as Tehran and Mashhad. The rollout timeline anticipates broader deployment within the next 3-5 years. Iran’s major mobile operators, such as Mobile Iran and MTN Iran, have announced plans to expand 5G infrastructure gradually, prioritizing urban zones.

Future plans focus on improving network capacity, reducing latency, and supporting high-data demand from digital services. However, geopolitical sanctions and economic constraints may delay full-scale deployment. Strategic investments are needed to sustain the growth trajectories anticipated by Iran’s telecom authorities.

Mobile Technology Ecosystem

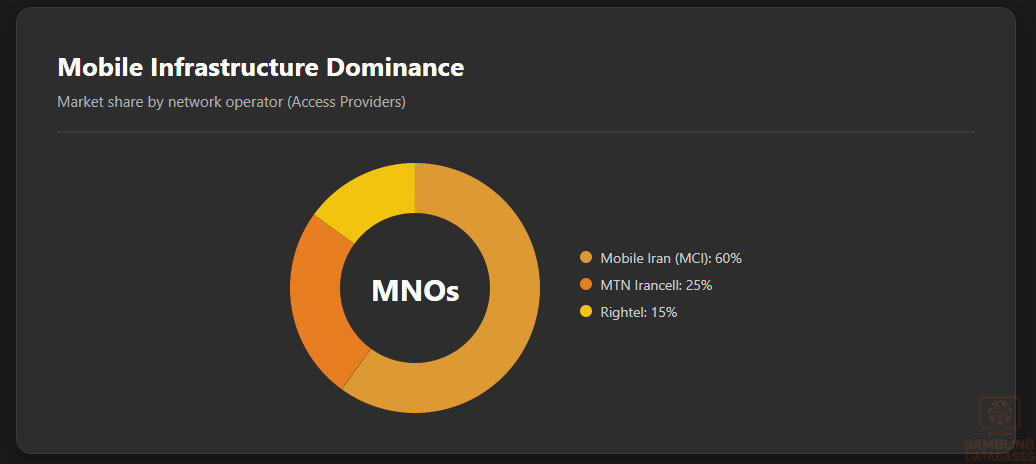

Iran hosts several major mobile network operators, with a market share distribution primarily driven by Mobile Iran (approx. 60%), followed by MTN Iran and Rightel. Coverage is extensive in urban districts, with ongoing efforts to improve rural access. Data costs are relatively low compared to regional standards, supporting high mobile usage rates.

- Mobile Iran: 60% market share

- MTN Iran: 25% market share

- Rightel: 15% market share

- Service quality varies, with urban centers experiencing better speeds

- Data tariffs are affordable, averaging $3-5 per GB for consumers

Device Penetration

Smartphone adoption in Iran is robust, with over 80% of internet users owning a smartphone. Devices are predominantly Android-based, with a growing presence of iOS devices among wealthier segments. Usage patterns reveal high engagement with mobile apps, social media, and digital entertainment, including online gaming.

Consumer preferences lean toward affordable, locally assembled devices, with brands like Samsung and Huawei dominating the market. Usage typically peaks during evening hours, with rapid growth in mobile data consumption linked to social and gaming applications.

Financial Services and Payment Infrastructure

Banking System Structure

Iran’s banking sector comprises several key players, including Bank Melli, Bank Saderat, and Bank Mellat, which collectively dominate the financial landscape. Digital banking is expanding, supported by state initiatives to modernize operations and enhance customer access.

- Bank Melli: Largest state-owned bank with extensive branch network

- Bank Saderat: Major player with broad international ties

- Bank Mellat: Focused on corporate and retail banking

- Private banks are gradually increasing market share

- Digital banking adoption is rising, yet cash remains king in many areas

Payment Processing Options

The Iranian payment ecosystem includes several local and international options, despite sanctions complicating formal channels. Payment methods such as bank cards (Visa/MasterCard), e-wallets like Zarinpal, and cryptocurrencies are widely used. Bank transfers are common for high-value transactions, while mobile payments are gaining popularity among youth.

- Bank debit and credit cards (limited international acceptance)

- E-wallets: Zarinpal, payment gateways supporting local banks

- Cryptocurrencies: Bitcoin, Ethereum for circumventing sanctions

- Bank transfers: Widely used domestically

- Mobile payments: Rapidly expanding segment

E-commerce and Digital Economy

The e-commerce market in Iran continues to grow robustly, with estimates exceeding $6 billion in 2024. Online retail is gaining trust among consumers due to improved digital payment facilities and logistics. Digital services such as streaming, online education, and gaming have surged in popularity, driven by young, connected demographics.

Consumers exhibit high trust in domestic payment gateways, and e-commerce platforms like Digikala have established dominant positions. Digital trust and infrastructure investments are expected to sustain double-digit growth in Iran’s digital economy.

Business Environment and Regulatory Framework

Ease of Business Operations

Iran ranks relatively low on global ease of doing business indexes, primarily due to administrative hurdles, sanction-induced constraints, and regulatory opacity. Company registration can take 4-6 weeks, involving numerous procedural steps and approvals. Despite challenges, the government encourages foreign direct investment in certain sectors through special economic zones and incentives.

- Preparation of legal documents and notarization

- Submission to the Iran Trade Organization

- Tax registration and obtaining a business license

- Establishment of operational accounts

Corporate Structure and Registration

Foreign investors typically establish LLCs or joint-stock companies, with restrictions on full foreign ownership in sensitive sectors. Branch offices are permitted but require government approval. The choice depends on strategic goals, with LLCs preferred due to simpler compliance compared to full subsidiaries.

Registration Requirements

- Initial application form and notarized documents

- Proof of address and identity

- Business plan and financial statements

- Approval from relevant authorities

- Legal representation in Iran

Taxation Framework

Corporate income tax in Iran stands at 25%, with some zones offering tax incentives for specific sectors. Double taxation treaties exist with several countries, including China, India, and Turkey, simplifying cross-border operations. Personal income tax varies from 10% to 35%, based on income brackets, with mandatory social security contributions.

Market Entry Considerations

Entering Iran’s market requires careful adaptation to local regulatory and cultural nuances. Partnerships with local firms are advisable to navigate operational complexities. Leveraging mobile and cryptocurrency platforms, bypassing direct licensing, remains a key strategy for offshore operators.

- Identify local partners or agents

- Invest in digital infrastructure and localized platforms

- Prepare for extended setup timelines due to bureaucratic processes

- Develop trust through localized user interfaces and payment options

Success Factors and Challenges

Success hinges on technological adaptability, local partnership, cultural understanding, anti-fraud measures, and competitive pricing. Major challenges include regulatory ambiguity, sanctions restrictions, banking limitations, cybersecurity threats, and societal attitudes towards gambling. Overcoming these requires innovative, compliant, and customer-centric strategies.

Exit Strategy Planning

Market liquidity is limited, and ownership transfer is legally complex due to the illicit nature of most operations. License transferability is virtually nonexistent in the official context, and valuation multiples depend heavily on underground market perceptions. Strategic liquidation should focus on offshore assets and digital equity.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Iran?

No. All forms of online gambling are strictly prohibited by law, with severe penalties including imprisonment, fines, and lashes. The government actively enforces bans, with limited tolerance for illegal activities.

2. What types of gambling licenses are available and what do they cover?

Currently, no licensed gambling operators exist legally in Iran. The regime does not issue licenses for any gambling activities; all operations are illicit.

3. How much does an iGaming license cost and how long does it take to obtain?

Since licensing is unavailable, costs and timelines do not apply legally. Any licensing process in Iran would be illegal and unrecognized.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot legally obtain licenses in Iran, as the government does not permit any formal licensing or regulation of gambling operations.

5. What are the tax obligations for iGaming operators?

There are no official tax obligations for illegal operators. If any licenses were granted, standard corporate taxes of around 25% and VAT could apply, but presently no legal framework exists.

6. Are gambling winnings taxed for players?

Gambling winnings are not taxed as most gambling activity occurs underground and illegitimately. The government does not officially collect taxes from individual players.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include platform development, hosting, security, marketing, and payment processing, typically totaling hundreds of thousands of dollars annually for underground operators.

8. What is the expected ROI timeline for entering this market?

ROI timelines are highly uncertain due to legal risks; successful underground operations may see breakeven within 12-18 months, but legal entry involves prohibitive costs and risks.

9. What are the local presence requirements for operators?

Legal presence is not required, but establishing local partnerships and legitimate local addresses can help mitigate risks and improve trust among users.

10. What payment methods are available and recommended?

Payment options include cryptocurrencies, local bank transfers, and digital wallets. Cryptocurrencies are most favored for anonymity and circumventing restrictions.

11. What are the advertising and marketing restrictions?

Advertising is illegal across all channels, including social media, digital ads, sponsorships, and public promotions, with strict enforcement and penalties.

12. What responsible gambling measures are mandatory?

Currently, no official responsible gambling measures are mandated for illegal operators, although informal self-exclusion and awareness campaigns are emerging among youth.

13. How large is the iGaming market and what is the growth potential?

The illegal market exceeds hundreds of millions USD annually, driven by a young, digital-native population, with growth driven by mobile and cryptocurrency adoption.

14. Who are the main competitors and what is their market share?

Competitors are mainly international offshore operators such as Betway, 888 Casino, and local informal networks, with no official market share due to illegality.

15. What are the player preferences and typical spending patterns?

Players prefer mobile platforms, mainly betting on football and slots, with average spendings around $100-$150 annually. Peak usage occurs evenings and weekends.

16. What are the key success factors and main challenges for new entrants?

Key success factors include technological innovation, local partnerships, and localized content. Main challenges involve regulatory risks, banking restrictions, societal attitudes, and enforcement crackdown.

SOURCES AND REFERENCES

- IranGambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Iran – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – 2024

- Government legal acts and edicts

- Telecom Infrastructure Reports

- Local banking sector publications

- Digital economy analysis

- Offshore gambling providers data

- E-commerce market studies

- Foreign investment guides

- Mobile network operator reports

🎯 Gambling Databases Country Rating: Iran

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 0.2/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.1/10 | ⛔️ Extremely High Risk (Black Market Only) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- TOTAL PROHIBITION: All forms of gambling (online, land-based, sports betting, casino) are strictly illegal under the Islamic Penal Code, Article 705.

- CORPORAL PUNISHMENT: Violations are not just civil offenses; they are criminal acts punishable by 1 to 6 months imprisonment and up to 74 lashes.

- ACTIVE ENFORCEMENT: The regime actively polices this sector. In 2024, the “Nitro Bet” network was dismantled, leading to arrests. Cyber-police (FATA) aggressively monitor financial flows.

- DEATH PENALTY RISK: While not currently standard, legislators have previously proposed the death penalty for “corruption on earth” charges applied to large-scale gambling operators.

- FINANCIAL BLOCKADE: Due to international sanctions and local laws, no legitimate banking channels exist. Operators must use money mules, crypto, or rent bank accounts, all of which carry high money laundering (AML) prosecution risks.

- INTERNET CENSORSHIP: Iran employs one of the world’s most sophisticated censorship firewalls (“Filternet”). Access requires constant domain rotation and VPNs.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Illegal with enforcement (-1.0). Sports betting prohibited (-1.5 deduction). Online casino prohibited (-1.5 deduction). Active ISP blocking and arrests (-0.5). Score is floored at minimum. |

| Licensing Process | 25% | 0.0/2.5 | No licensing available (0). There is no regulator, no license, and no application process. Operating implies criminal conspiracy. |

| Taxation & Costs | 20% | 0.0/2.0 | N/A (Illegal). While there is no “tax,” the effective cost is the risk of 100% asset seizure. High operational costs for obfuscation/cloaking (-0.5). High risk premium for payments (-0.5). Score set to 0 due to 100% seizure risk. |

| Operational Requirements | 15% | 0.0/1.5 | Excessive Requirements (0). Requires complex illegal infrastructure (rented bank accounts, crypto rails). Credit card ban (Sanctions + Local law) (-0.25). Cryptocurrency banking restrictions (-0.25). |

| Market Environment | 10% | 0.0/1.0 | Difficult Environment (0.25). Advertising strictly banned (-0.5). Active enforcement against operators (-0.25). Political instability/Sanctions (-0.25). Final: 0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal with player penalties (0). Gambling is considered “Haram” and a crime. Major product prohibition (-1.5). Players face criminal prosecution risks (-0.5). |

| Practical Accessibility | 30% | 0.5/3.0 | Severe restrictions (+0.5). Active ISP blocking (-0.5). VPN required for all access (-0.5). No standard credit card processing (-0.5). Reliance on crypto/informal hawala networks. |

| Player Penalties | 20% | 0.0/2.0 | Criminal penalties possible (0). Penalties include fines, imprisonment, and corporal punishment (lashes). |

| Market Availability | 10% | 0.0/1.0 | No access / Effective blocking (0). No licensed operators. Extensive black market only. |

🔍 Key Highlights

Strengths (If Any)

- Demographics: Young population (median age 32) with high mobile penetration (96%) creates immense illegal demand.

- Crypto Adoption: Due to sanctions and inflation, the population is highly literate in cryptocurrencies (Tether/Bitcoin), which facilitates underground deposits.

⛔️ CRITICAL RISKS AND CHALLENGES

- Theocratic Prohibition: Gambling is not just a regulatory violation; it is a religious crime against the state.

- Physical Safety: Local agents, developers, or affiliates residing in Iran face immediate arrest, imprisonment, and physical punishment.

- Financial Sanctions: Iran is cut off from SWIFT. International payment processors (Visa/Mastercard/Skrill/Neteller) generally do not function. You cannot repatriate funds legally.

- Cyber Warfare: The government uses state-level cyber tools to identify VPN traffic and block gambling domains rapidly.

- Asset Seizure: Any funds discovered by the Financial Intelligence Unit are subject to immediate confiscation without due process.

Player-Specific Issues

- Players risk receiving lashes if caught gambling in public or if bank records are subpoenaed.

- High risk of non-payment by fly-by-night underground operators with no recourse.

- Identity theft risks from providing KYC to illegal operators.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: Low ($50k+) technically, but effectively infinite risk.

Monthly Operating Costs: High. Requires constant domain mirroring, purchasing rented bank accounts (mules), and high crypto-exchange fees.

Effective Tax Rate on Revenue: 0% Official / 100% Risk of Seizure.

Customer Acquisition Cost: Low organic demand, but high technical cost to retain access.

Time to Breakeven: Fast (if not arrested).

Profitability Assessment: EXTREMELY HIGH RISK. While the market generates hundreds of millions in black market revenue, it is uninvestable for legitimate businesses. The “profit” comes with the risk of international money laundering charges and the imprisonment of any local staff.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Domain seizure, permanent blacklisting, money laundering charges in home jurisdictions for processing sanctioned funds. |

| Licensed Sports Betting Operators | N/A | Cannot exist. No license available. |

| Affiliates/Advertisers | CRITICAL | If located in Iran: Arrest, torture, prison. If offshore: Loss of all revenue, potential blocking. |

| Payment Processors | CRITICAL | Violating US/EU sanctions against Iran (OFAC risks), leading to global business collapse and imprisonment. |

| Company Directors/Executives | HIGH | Travel restrictions due to Interpol notices if Iran pursues cross-border financial crime charges. |

🚨 Extradition and International Enforcement

Extradition Treaties: Iran has no extradition treaties with the US or EU. However, it has treaties with countries like Russia, China, and regional neighbors.

Enforcement History: Iran utilizes Interpol Red Notices for “financial crimes” and “fraud” to target operators of gambling networks. The 2024 crackdown on Nitro Bet showed domestic capability, and they actively pressure regional neighbors (Turkey, UAE) to deport Iranian nationals running these rings.

Sanctions Risk: The biggest risk for Western operators is not Iranian enforcement, but US/EU Sanctions violations. Processing payments from Iran can result in federal prison time in the US and massive fines from global regulators.

📋 Final Verdict

Iran receives an Operator Ease Score of 0.0/10 and a Player Access Score of 0.2/10, resulting in an overall market attractiveness rating of 0.1/10.

HONEST ASSESSMENT: Iran is a complete no-go zone for any legitimate iGaming business. The combination of strict Islamic prohibition, corporal punishment (lashes), and global economic sanctions makes it one of the most hostile environments on earth for this industry. Any operation here is strictly criminal enterprise, not business.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- NOBODY. There is no legal way to operate here.

❌ Definitely Avoid If You Are:

- A Publicly Listed Company: Sanctions violations will delist you and jail your executives.

- A Licensed Operator: You will lose your Tier-1 licenses (MGA, UKGC) immediately for operating in a sanctioned jurisdiction.

- Risk-Averse: The penalty for failure involves prison and lashes for local staff.

- Dependent on Credit Cards: Global banking is disconnected from Iran.

⚠️ BOTTOM LINE: Avoid Iran entirely. The market is exclusively for criminal syndicates willing to risk imprisonment and navigate complex international sanctions.

Iran’s iGaming market is a powder keg waiting to explode. With 58% online gaming participation, the demand is undeniable. Yet, strict Islamic laws and harsh penalties stifle the industry. I’ve seen operators like 888 Casino and Betway try to tap into this market, but the lack of a licensing framework and regulatory authority makes it a high-risk endeavor.

Regarding the Iranian iGaming market, it’s essential to understand the complexities of the regulatory environment. While there’s a significant demand for online gaming, the government’s stance on gambling is clear. However, this hasn’t stopped international operators from attempting to capitalize on the market. The use of cryptocurrencies and VPNs has become increasingly common, allowing players to access offshore platforms. Nevertheless, the risks associated with operating in this market cannot be overstated.

That’s a great point about the regulatory environment. But what about the role of AML bodies in monitoring financial transactions? How do they impact the underground market?

The Financial Intelligence Unit plays a crucial role in combating money laundering and terrorist financing. While their primary focus isn’t on the iGaming industry, they do monitor suspicious transactions that may be related to illicit activities, including underground gambling. This has led to the shutdown of several major gambling networks in the past.