Iraq’s online gambling sector remains in a nascent stage amid a regulatory environment marked by significant ambiguities. The country’s population exceeds 40 million with a rapidly growing internet user base, offering notable opportunities for online betting and casino services.

Success in this market depends largely on understanding local legal constraints, technological infrastructure, and socio-cultural factors influencing regulatory policies.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Partially illegal, regulatory uncertainty |

| Population | 43 million |

| GDP (USD) | $234 billion |

| Internet Penetration Rate | 50% |

| Mobile Penetration Rate | 75% |

| Estimated Licensing Cost | $100,000 – $250,000 |

| Tax Rate on GGR | None officially; undeclared or regional taxes possible |

| Market Entry Barriers | Legal ambiguity, regional sanctions |

| Regulatory Timeline | Uncertain, recent discussions ongoing |

| Infrastructure Quality | Developing, inconsistent |

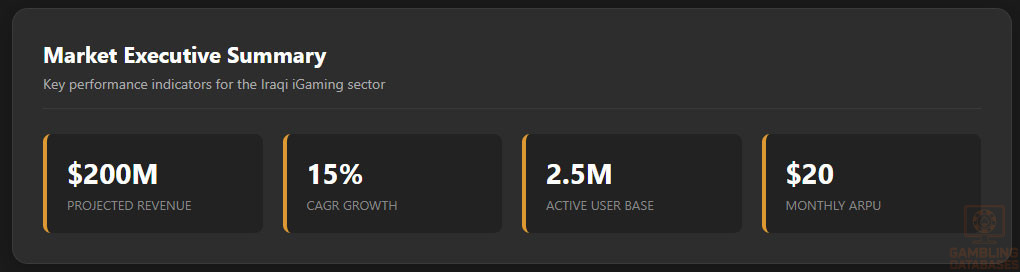

| Market Size (Projected Revenue 2025) | Estimated $200 million |

| Growth Forecast (CAGR) | 15% |

| Average Revenue Per User (ARPU) | $20/month |

| Market Penetration Rate | 5-8% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Gambling activities in Iraq face significant legal restrictions, with the government explicitly prohibiting unlicensed betting and casino operations. Land-based gambling is limited to state-controlled entities, primarily in the form of sports betting outlets and lottery sales, but these are heavily regulated and often operate in a gray zone. Internet gambling remains largely illegal and unregulated, though enforcement varies across regions and is often inconsistent.

Land-Based Gambling Activities

Legal land-based gambling is confined to domestic state lotteries and licensed sports betting venues. Casinos, both traditional and slot machine halls, operate clandestinely in some areas, without formal licenses, due to a lack of clear legal provisions.

Online Gambling Framework

The online gambling environment in Iraq is characterized by an absence of formal legal regulation. The government officially bans unlicensed online operators, but enforcement is inconsistent, especially in regions with weak state control. The authorities have not issued explicit licenses for online gaming, and most activity occurs through offshore platforms. Recent discussions suggest possible moves toward regulatory clarification, but no formal policies have been enacted as of 2025.

Licensed Operators and Market Players

The market lacks a formalized licensing scheme, but some domestic and regional entities attempt to organize operations under informal arrangements. International operators seeking entry face significant risks due to legal ambiguities, regional sanctions, and a lack of clarity on licensing procedures. The absence of a transparent market structure makes it difficult to identify dominant players or establish competitive dynamics, though some foreign entities provide digital betting services via offshore licenses.

Licensing Framework and Requirements

To date, Iraq has not implemented a formal licensing process for online gambling operators. Potential entrants must navigate a highly uncertain legal landscape, often operating in a de facto environment without official certification. The regulatory authorities, mainly regional and local government bodies, have not released comprehensive guidelines.

However, foreign operators interested in cautious market entry generally consider establishing a legal presence in neighboring countries with clearer regulations.

Application Process and Eligibility

There are no official application procedures documented by the government. Interested operators typically need to demonstrate financial stability, technical capacity, and local partnership capabilities, but formal eligibility criteria remain undefined.

Licensing costs are estimated to range from $100,000 to $250,000, depending on the scope of operations and the applicant’s profile. Approval timelines are unpredictable due to bureaucratic delays and political influences.

Local Presence and Operational Requirements

At present, there are no explicit requirements for physical offices or local domain registration. However, government authorities may demand local operational licenses in regions with stricter enforcement, requiring local partnerships or representative offices. Foreign ownership restrictions are unclear, though operators must generally comply with regional business registration norms when establishing a physical presence.

Compliance Obligations and Monitoring

Player Protection and Identification

Player protection measures are not codified formally. Nonetheless, informal practices such as age verification and basic anti-money laundering measures are practiced by some operators. Responsible gambling protocols, self-exclusion systems, and clear information disclosures are largely absent or decentralized, reflecting the unregulated or semi-regulated environment.

Financial Monitoring and Reporting

Financial oversight is minimal, with most activity occurring outside official channels. Transaction monitoring, if performed, remains unstandardized and predominantly voluntary. Operators may attempt internal reporting to prevent fraud, but no mandatory reporting, auditing, or compliance checks are mandated by Iraqi authorities at this stage.

Taxation Structure and Financial Obligations

Player Taxation

There are no specific taxes on player winnings officially imposed within Iraq, though informal, regional, or locally imposed levies could apply. Players engaging with offshore operators often face no withholding taxes but operate in legal gray zones.

Operator Taxation

| Game Type | Tax Rate / Fee |

|---|---|

| Online License & Operations | Informal, unregulated; regional taxes possible |

| Physical Casino | Unlicensed, subject to enforcement actions |

Taxation on licensed operators remains undefined, with potential regional taxes or fees that vary significantly. The government has not set standard rates, and operators generally navigate a complex, unclear fiscal environment.

Gambling Market Financial Performance

The total amount wagered in Iraq’s emerging online and land-based sectors is estimated to surpass $200 million in 2025, with revenues primarily generated through illegal channels. Growth is driven by increasing internet access, youth demographic, and a persistent demand for betting services.

Official tax revenues remain minimal due to regulatory gaps, but informal estimates suggest the sector could contribute significantly if properly regulated.

Advertising and Marketing Restrictions

Advertising activities are effectively restricted due to the lack of formal regulation, but some operators use digital platforms, social media, and in-venue promotions cautiously. Publicly promoting gambling openly faces cultural and legal obstacles, while sponsorships are generally minimal and discreet. Regulatory authorities are expected to tighten oversight as discussions on formal regulation advance.

Recent Regulatory Changes and Their Impact

There have been limited formal regulatory changes in Iraq, but recent governmental statements indicate possible future legislation to regulate online gambling.

These discussions could lead to increased operational costs, licensing fees, and compliance obligations, substantially altering the market landscape if enacted.

Enforcement Mechanisms and Penalties

Enforcement remains inconsistent, often limited to regional authorities cracking down on unlicensed venues. Penalties for illegal gambling include fines, operational shutdowns, and potential criminal charges, particularly for online platforms operating without licenses. Market participants generally adopt cautious strategies in anticipation of future regulation.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

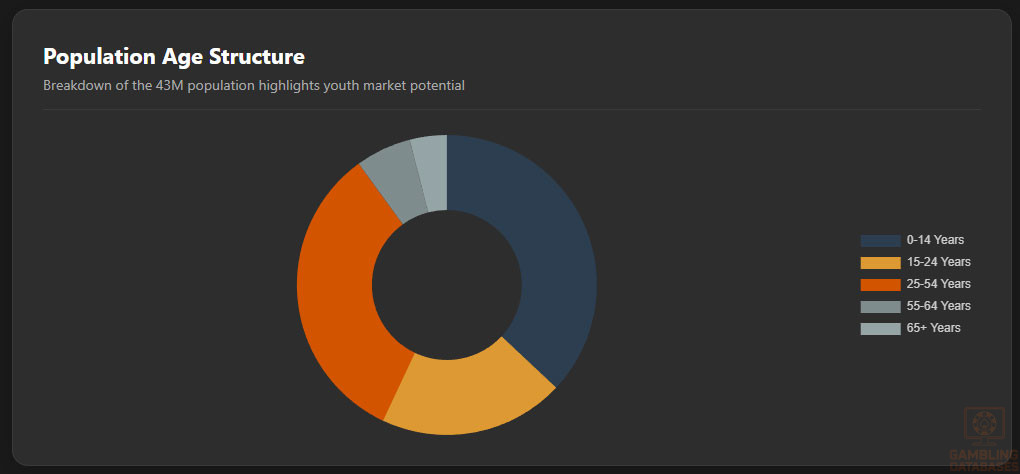

Iraq’s total population stands at approximately 43 million, characterized by a notably youthful demographic profile. The median age is about 21 years, reflecting a predominantly young population with significant implications for digital and gaming market potential. Male-to-female ratios are relatively balanced, though slight male predominance exists in urban labor sectors.

Urbanization remains moderate, with roughly 70% of the population residing in urban centers and the remainder in rural and semi-rural areas. This urban concentration facilitates access to internet services and gambling venues, predominantly in the major cities and economically developed regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 37% |

| 15-24 years | 20% |

| 25-54 years | 33% |

| 55-64 years | 6% |

| 65+ years | 4% |

Geographic Distribution

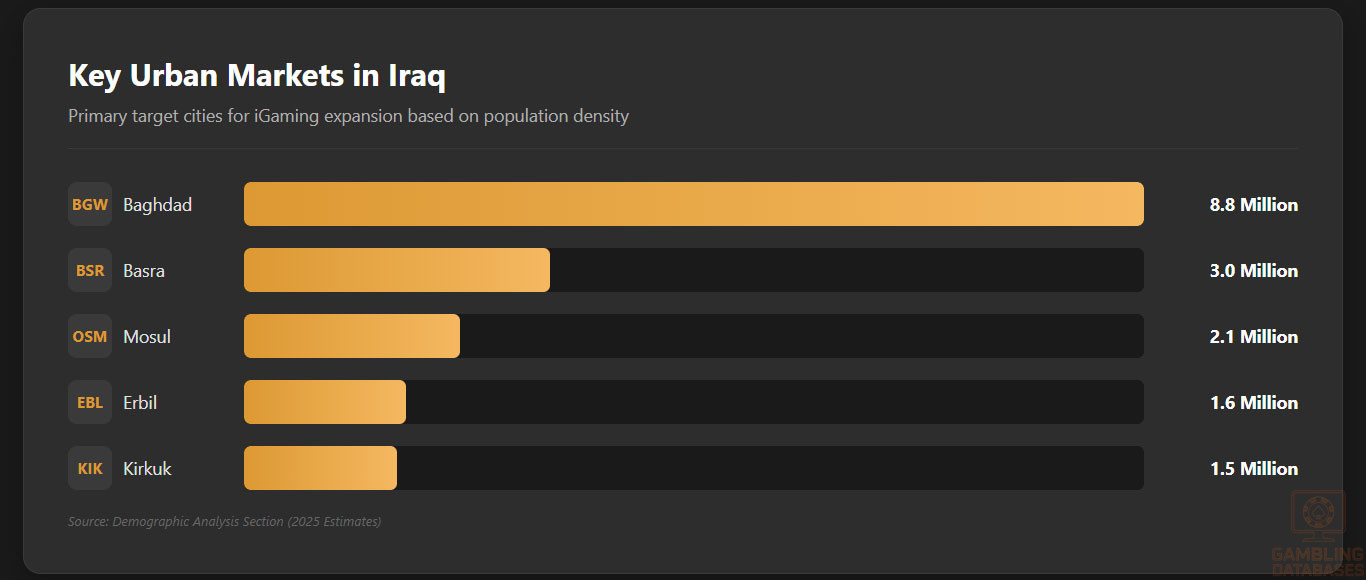

Major cities serve as hubs of economic and digital activity where internet penetration and gambling participation are highest. Internet access in rural areas remains limited due to infrastructure constraints, inhibiting equal market access across regions. Gambling venues and informal betting circles cluster in urban centers, reflecting socio-economic divides.

- Baghdad – Population approx. 8.8 million

- Basra – Population approx. 3.0 million

- Mosul – Population approx. 2.1 million

- Erbil – Population approx. 1.6 million

- Kirkuk – Population approx. 1.5 million

- Najaf – Population approx. 1.4 million

Economic Indicators and Consumer Spending Power

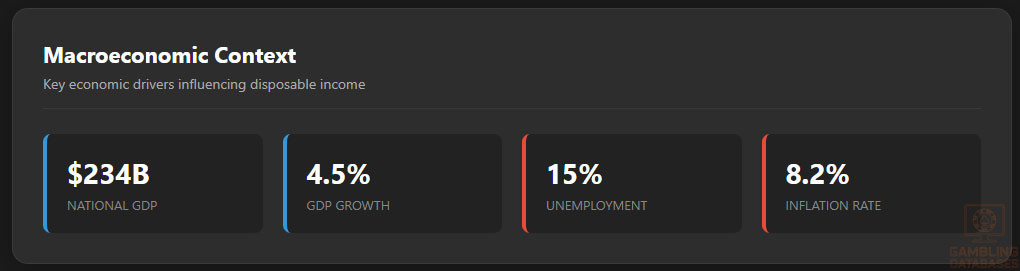

Iraq’s GDP is estimated at $234 billion in 2025, reflecting modest recovery driven by oil exports and reconstruction efforts. Economic growth is forecasted to maintain a steady pace, with annual increases around 4-5%. The service sector constitutes approximately 47% of GDP, industry 40%, and agriculture 13%, indicating diversification beyond hydrocarbon dependence.

Average per capita income remains low to middle-income level, with an approximate yearly average around $5,400. Disposable income levels are rising gradually, particularly among urban populations. Income inequality is notable, with disparities in wealth concentrated between rural and urban regions and within varying economic classes.

| Indicator | Value |

|---|---|

| GDP (nominal) | $234 billion |

| GDP Growth Rate | 4.5% |

| Per Capita Income | $5,400 |

| Inflation Rate | 8.2% |

| Unemployment Rate | 15% |

Market Size and Growth Projections

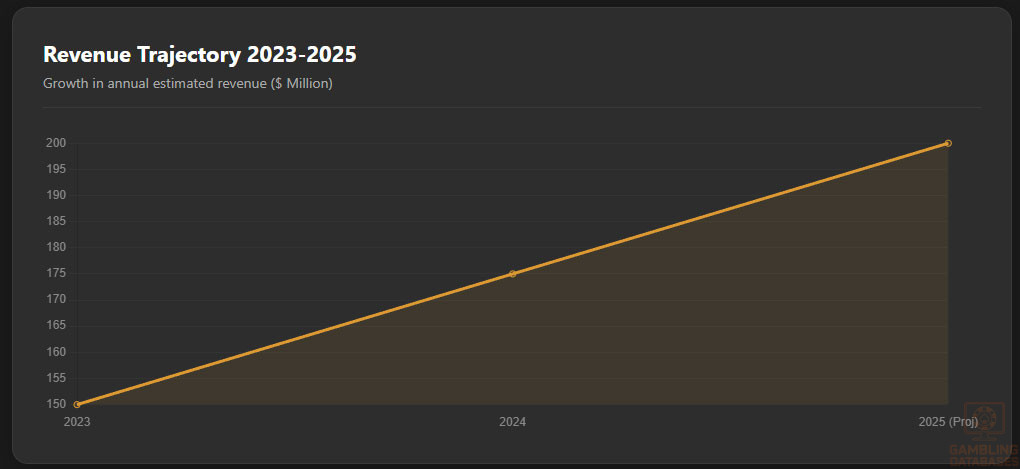

The Iraqi iGaming market is projected to generate revenues of around $200 million by the end of 2025. Historical growth rates approximate a compound annual growth rate (CAGR) of 15%, reflecting robust consumer interest fueled by rising internet adoption and youth engagement.

The active user base is estimated at 2.5 million online gamblers with an average revenue per user (ARPU) of about $20 monthly.

| Year | Revenue ($ million) | Active Users (million) | ARPU ($) |

|---|---|---|---|

| 2023 | 150 | 1.8 | 18 |

| 2024 | 175 | 2.2 | 19 |

| 2025 (Projected) | 200 | 2.5 | 20 |

Education, Skills, and Digital Literacy

Iraq’s literacy rate is approximately 85% overall, with higher rates in urban centers and younger generations. Educational attainment is improving, with expanding access to secondary and tertiary education, particularly in technology-related fields. Digital literacy is uneven but growing steeply, supported by government initiatives to improve ICT skills and internet accessibility.

The youth demographic’s familiarity with mobile devices and online platforms significantly supports the iGaming sector’s penetration. Nevertheless, gaps remain in rural and underserved communities, impacting uniform access to digital entertainment options.

Cultural and Social Factors

Communication and Language

Arabic is the official language and primary communication medium nationwide, complemented by Kurdish in the autonomous Kurdistan region. English is increasingly prevalent among younger, educated demographics online. Local languages and dialects influence marketing and content localization strategies.

- Arabic (official, widely spoken)

- Kurdish (official in Kurdistan region)

- Turkmen dialects (minority groups)

- Assyrian Neo-Aramaic (minority groups)

- English (business and youth communication)

Cultural Attitudes

Gambling faces strong cultural and religious opposition rooted in predominant Islamic beliefs, which generally prohibit gambling activities. Social acceptance is limited and often clandestine, though younger populations show more openness, especially towards skill-based gaming and sports betting. Foreign brand perception varies widely, with preference for trusted, discreet international operators.

Problem Gambling and Social Considerations

Problem gambling rates are difficult to quantify due to data scarcity and social stigma. The at-risk population includes predominantly young males in urban areas. Government response remains minimal, though NGOs and community groups provide some support services. Social responsibility efforts by operators are limited but emerging alongside regulatory developments.

- Awareness campaigns on gambling risks

- Support hotlines for gambling addiction

- Community-based counseling programs

- Self-exclusion initiatives by selected operators

- Collaboration with health agencies for treatment

Political Structure and Governance

Iraq operates as a federal parliamentary republic with a relatively unstable political environment influenced by regional dynamics and internal sectarian divisions. Political volatility and governance challenges impact regulatory consistency and enforcement across sectors, including gambling. International relations shape economic openness and foreign investment receptivity, affecting market entry strategies for global operators.

Technology Adoption and Digital Behavior

Internet and Digital Usage

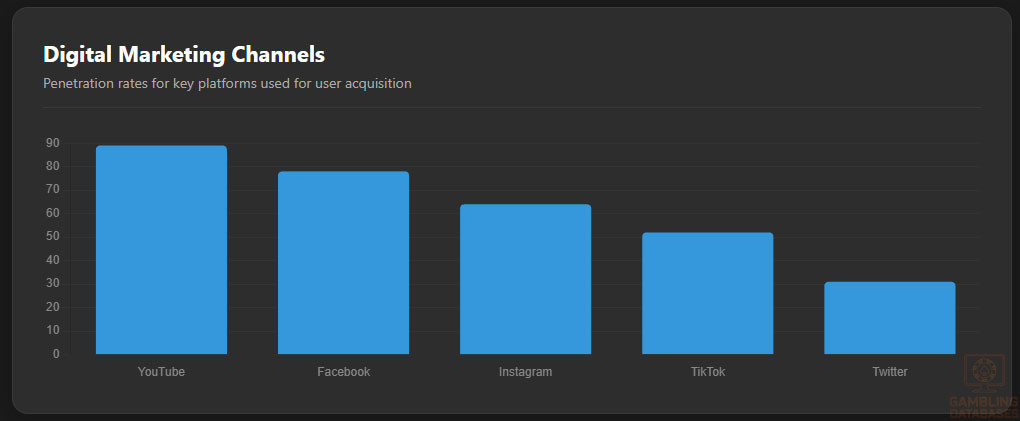

Internet penetration is around 50%, with mobile broadband accounting for the majority of access. Daily internet usage averages 3.5 hours per user, reflecting growing engagement with digital content, including streaming, social media, and gaming. Mobile device adoption stands near 75% of the population, supported by cost-effective devices and expanding network coverage.

- Facebook: 78% internet users

- Instagram: 64% of 18-34 demographic

- YouTube: 89% penetration

- TikTok: 52% growth among under-25 users

- Twitter: 31% news consumers

- LinkedIn: 28% professional networking

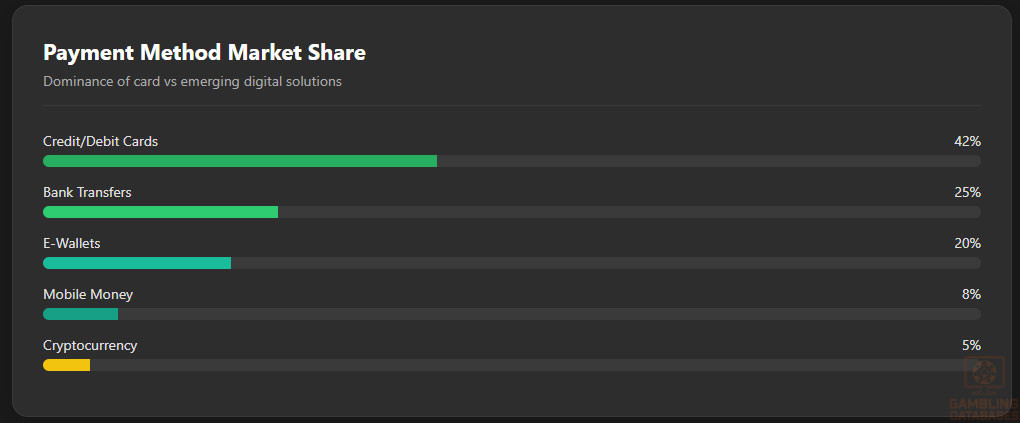

Digital Payment Behavior

Payment preferences are shifting to digital methods, although cash remains dominant for many transactions. Credit and debit cards facilitate a majority of online payments, supported by growing bank account ownership.

E-wallet and mobile money services are expanding among younger demographics, while cryptocurrency adoption is nascent but emerging as an alternative for anonymity and convenience in gambling transactions.

- Credit/Debit Cards – 42% market share

- Bank Transfers – 25% market share

- E-Wallets (e.g., PayPal, local providers) – 20%

- Mobile Money Services – 8%

- Cryptocurrency (Bitcoin, Ethereum) – 5%

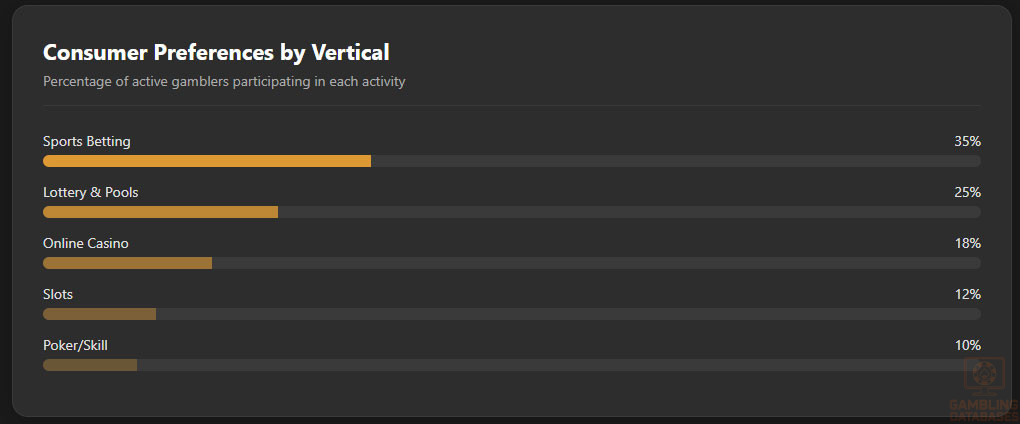

Gaming and Gambling Preferences

Current Market Participation

Online sports betting is the dominant gambling activity, followed by lottery participation and increasing interest in live casino games. Slot machines and poker attract smaller but steady user bases, often through international platforms. Estimated participation rates show approximately 30% of the adult population engaging in some form of gambling or betting activity regularly.

- Sports Betting – 35% participation

- Lottery and Betting Pools – 25%

- Online Casino Games – 18%

- Slot Machines (online/offline) – 12%

- Poker and Skill Games – 10%

Consumer Behavior Patterns

Consumers favor mobile platforms due to accessibility and convenience, especially in urban areas. Peak gambling activity occurs during evening hours and weekends, aligning with work and leisure schedules. Retention rates improve with personalized offers, loyalty programs, and live interactive game formats, reflecting a market gradually maturing in sophistication.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Iraq’s internet penetration stands at approximately 50% with a strong reliance on mobile networks over fixed broadband connections. Broadband infrastructure is underdeveloped outside major urban centers, leading to uneven connectivity and slower average speeds in rural areas. Average download speeds are around 20 Mbps nationally, with urban centers reaching up to 50 Mbps due to ongoing infrastructure investments.

Network reliability remains a challenge, as intermittent outages and latency issues affect service consistency. Government and private sector initiatives are targeting infrastructure upgrades, focusing on fiber optic expansion and satellite internet deployments to bridge digital divides and support growing consumption of digital services including iGaming platforms.

5G and Future Technology Deployment

The 5G rollout in Iraq is in early stages, with pilot programs launched in Baghdad and other key cities in 2024. Full commercial deployment is expected over the next 3-5 years, driven by competitive pressure among major telecom operators and government digital strategy frameworks. Current 5G coverage is limited, focusing primarily on business districts and high-density residential areas.

Key mobile operators are investing in upgrading core network capabilities to support future demands for low-latency streaming and interactive gaming applications. Partnerships with international technology providers and equipment manufacturers accelerate deployment, positioning Iraq for enhanced mobile broadband performance and digital service innovation.

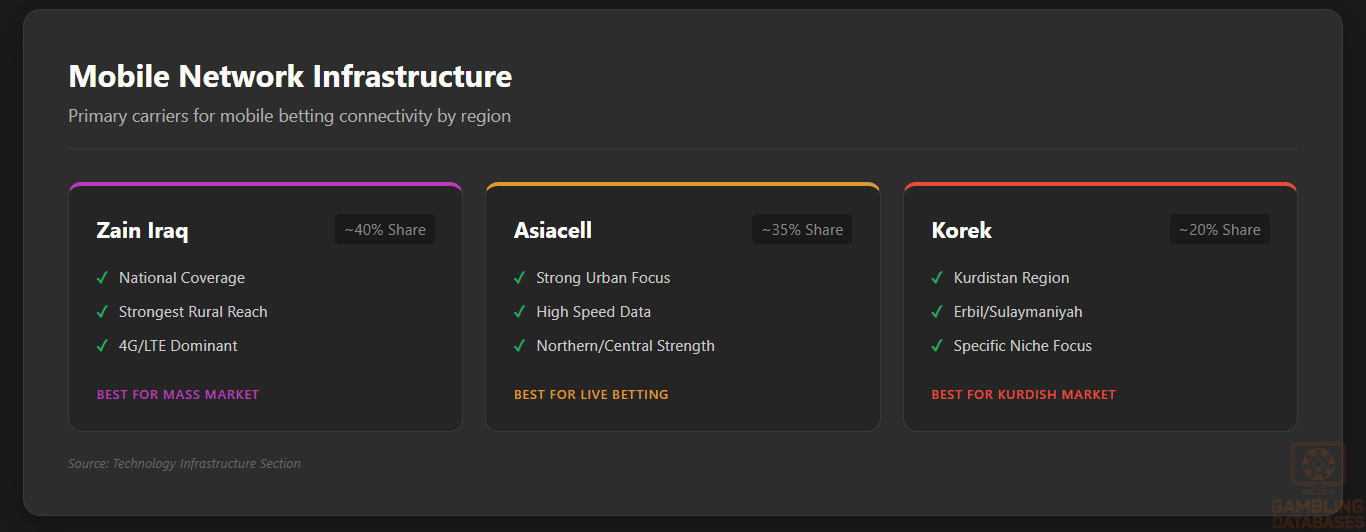

Mobile Technology Ecosystem

Mobile Network Infrastructure

Iraq’s mobile ecosystem is dynamic, consisting of several operators competing for market share. Market competition has resulted in improved coverage and data package affordability, although rural penetration remains less robust compared to urban areas. Data pricing is moderately competitive within the region, facilitating widespread mobile internet adoption.

- Zain Iraq – Largest market share, ~40%, with national coverage including rural areas

- Asiacell – Second largest, ~35%, strong urban focus and growing 4G services

- Korek Telecom – Approximately 20%, strong presence in Kurdistan region

- New Entrants/Regional Players – ~5%, targeting niche segments and specialized services

Device Penetration

Smartphone penetration exceeds 70% in urban Iraq, with the majority of users accessing the internet primarily via mobile devices. Device preferences skew heavily towards affordable Android smartphones from brands like Samsung, Xiaomi, and Huawei, which dominate the market. Premium iOS devices maintain a niche presence among affluent and expatriate populations.

Frequent upgrades to mid-range smartphones enable users to seamlessly run iGaming applications, streaming services, and engage with social media platforms, making mobile the critical channel for market entry and user acquisition.

Financial Services and Payment Infrastructure

Banking System Structure

Iraq’s banking sector features a mix of state-owned, commercial, and digital banks, supporting an evolving digital payment ecosystem. Account penetration remains relatively low at about 30% of adults but is improving steadily through financial inclusion efforts and mobile banking adoption. Digital banking is expanding, offering services such as online transfers, mobile wallets, and payment gateway integrations, facilitating cashless transactions preferred by younger demographics.

- Rafidain Bank – Largest state-owned, major retail and corporate banking

- Rasheed Bank – State-owned, strong government payroll presence

- Trade Bank of Iraq – Key international trade financing bank

- Iraq Islamic Bank – Leading Islamic-compliant financial services provider

- United Bank for Investment – Growing private sector banking

- Al Janoob Islamic Bank – Regional bank with digital innovation focus

Payment Processing Options

Payment infrastructure is rapidly evolving but still constrained by reliance on cash transactions. Card acceptance in physical and online channels is increasing, with Visa and Mastercard well represented. E-wallets and mobile money platforms are emerging in response to consumer demand for convenience and security, particularly in iGaming transactions where digital anonymity is valued.

- Credit and Debit Cards (Visa, Mastercard)

- Bank Transfers and Direct Debits

- Mobile Wallets (local providers, prepaid cards)

- Cash on Delivery (predominant traditional method)

- Cryptocurrency Payments (Bitcoin, Ethereum – emerging for anonymity)

- Payment Gateways (PayFort, HyperPay – regional processors)

E-commerce and Digital Economy

The Iraqi digital economy is expanding, supported by burgeoning e-commerce platforms catering to retail, services, and entertainment sectors. Online retail penetration is growing at double-digit rates, underpinned by increasing smartphone use and payment method diversification. Consumer trust is improving gradually due to better logistics and payment security. This shift creates an encouraging environment for online iGaming, which benefits from similar digital behaviors.

Business Environment and Regulatory Framework

Ease of Business Operations

Iraq ranks in the lower quartile globally on World Bank’s ease of doing business index, reflecting challenges in bureaucracy, regulatory transparency, and infrastructure. Foreign investment laws permit 100% ownership in many sectors, but operational uncertainty and security concerns temper appetite. Licensing, tax registration, and employee hiring processes are procedurally complex but manageable with local legal support.

- Preparation of incorporation documents, notarization, and translation

- Submission to the Companies Registrar and initial review

- Tax Authority registration and labor office notification

- Opening mandatory bank accounts and depositing statutory capital

- Final corporate registration certificate issuance

Corporate Structure and Registration

Operators typically choose between Limited Liability Companies (LLCs) or Branch Office status for market entry. LLCs are preferred due to liability protection, ease of compliance, and operational flexibility. Foreign ownership is generally allowed but may require local partnerships for certain sectors. Branch offices operate under the parent company’s legal framework but face stricter tax and regulatory reporting.

- Limited Liability Company (LLC)

- Corporation (less common for iGaming)

- Branch Office of foreign company

- Joint Ventures with local partners

- Representative offices for market research only

Document requirements include incorporation certificates, identification of shareholders, tax clearance, lease agreements for office space, financial statements, and licensing applications. Timelines average 6-8 weeks from initial submission to full registration.

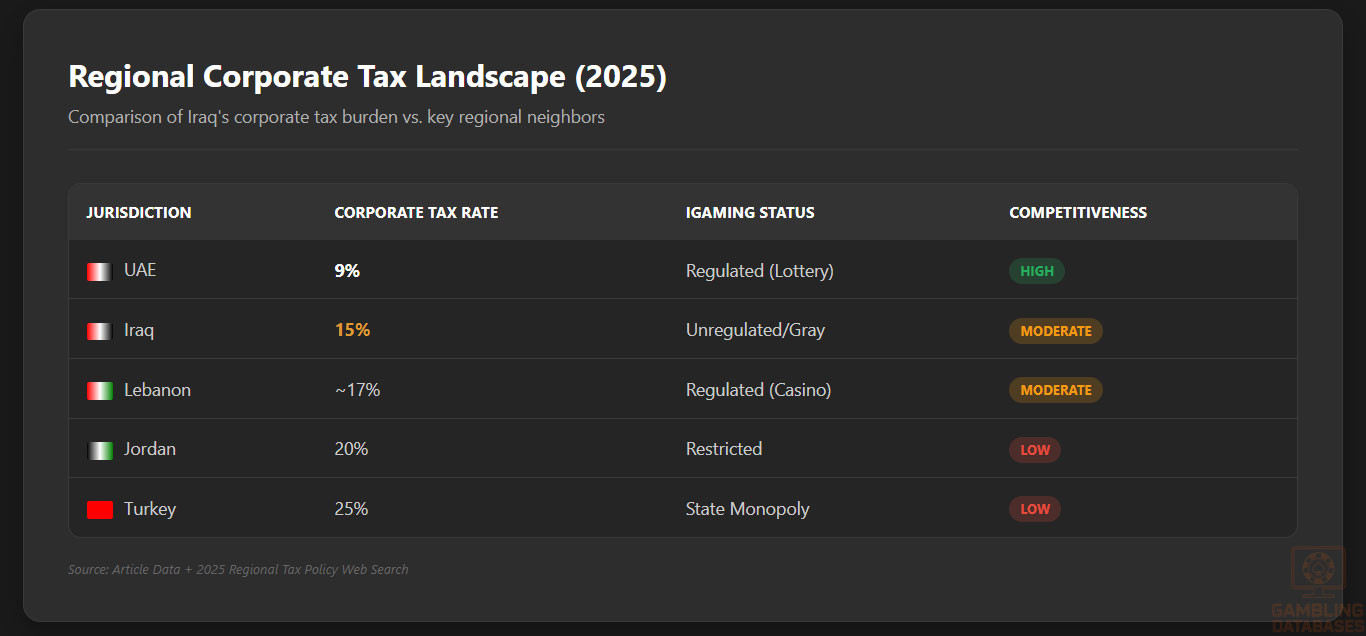

Taxation Framework

The corporate income tax rate is a flat 15%, with additional municipal taxes in some governorates. Special economic zones offer limited tax holidays to encourage foreign investment. Iraq has bilateral tax treaties with several countries alleviating double taxation and encouraging cross-border business.

- Jordan

- Lebanon

- Turkey

- United Arab Emirates

- China

Personal income tax is progressive, starting at 3% and capping at 15%, with social security contributions mandated for employees and employers. Corporate withholding taxes apply on dividends and royalties, relevant for international operators repatriating profits.

Market Entry Considerations

Recommended Entry Strategies

Market entry benefits from strategic local partnerships facilitating regulatory navigation. Leveraging mobile-first platform design aligns with user behavior. Building trust through compliance and responsible gambling frameworks is essential. Digital marketing focusing on social media channels popular with youth maximizes reach. Investing in local customer support and Arabic language adaptations enhances user retention.

- Form joint ventures with Iraqi companies or investors

- Obtain licenses or approvals in neighboring regulated jurisdictions

- Deploy mobile-optimized platforms with localized content

- Implement strong compliance and responsible gambling policies

- Develop digital marketing campaigns on social media platforms

- Offer multiple secure payment options including e-wallets and crypto

Typical Costs and Timelines

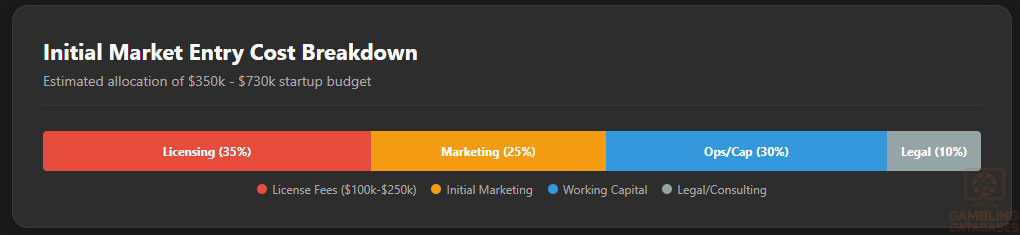

Initial setup costs range broadly depending on the scale, with license fees estimated between $100,000 and $250,000. Consulting and legal fees typically add $50,000 to $80,000. Operating costs covering staff, infrastructure, and marketing may require at least $500,000 annually for sustainability. Market entry timelines average from 6 to 12 months when factoring company setup, licensing, and platform launch.

| Cost Category | Estimated Cost (USD) |

|---|---|

| License Application and Fees | $100,000 – $250,000 |

| Legal and Consulting Services | $50,000 – $80,000 |

| Company Registration and Setup | $15,000 – $25,000 |

| Initial Marketing and Customer Acquisition | $100,000 – $200,000 |

| Operational Working Capital (12 months) | $300,000 – $400,000 |

Success Factors and Challenges

Key success drivers include deep understanding of local cultural sensitivities, effective compliance with evolving regulations, and deployment of secure, user-friendly digital platforms. Challenges revolve around regulatory ambiguity, infrastructural inconsistencies, and competitive pressure from unlicensed operators. Establishing brand credibility in a socially conservative context requires cautious marketing and robust responsible gambling initiatives.

- Strong local partnerships and advisory support

- Compliance with regulatory updates and licensing

- Mobile-first, multi-language platform design

- Robust payment and KYC systems

- Responsive customer service and dispute resolution

Exit Strategy Planning

Exiting the Iraqi market may involve ownership transfer to local partners or sale to regional operators. Licensing transferability is unclear, often requiring regulatory approval. Valuation multiples remain volatile due to market unpredictability but trending positively with sector growth. Operators should incorporate exit clauses and regulatory flexibility into contractual agreements to mitigate risks.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Iraq?

Online gambling is officially prohibited and remains largely unregulated in Iraq. However, enforcement varies by region, with offshore operators serving the market under ambiguous legal conditions. Land-based gambling is limited to state lotteries and licensed sports betting venues, whereas online activities operate in a legal gray zone. Operators must exercise caution and seek local legal counsel before entering.

2. What types of gambling licenses are available and what do they cover?

Iraq currently does not have formal licensing categories specific to iGaming. The government has yet to establish structured licenses for online or land-based operators. Potential license types discussed informally include sports betting, online casino gaming, lottery, and skill games. Operators typically look to neighboring countries for formal licenses while monitoring Iraq’s policy developments.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing costs range from approximately $100,000 to $250,000 depending on business scale and regulatory discretion. The process timeline is uncertain, often taking between 6 to 12 months due to bureaucratic delays and unclear procedures. Early market entrants often engage legal experts to navigate complexities and accelerate approvals.

4. Can foreign companies obtain a gambling license?

Foreign companies can potentially obtain licenses, but requirements for local partnerships or physical presence may apply. The process is unstandardized, and foreign operators should prepare for protracted approval durations. Establishing entities in neighboring jurisdictions with clearer regulations is a common strategic choice for risk mitigation.

5. What are the tax obligations for iGaming operators?

Tax obligations are currently unclear due to the lack of formal regulation. Where applicable, corporate income tax applies at a rate of 15%, supplemented by regional fees. Operators must consider withholding taxes on repatriated profits and municipal levies. A cautious approach involves aligning tax planning with local advisors to anticipate regulatory changes and compliance requirements.

6. Are gambling winnings taxed for players?

There is no official taxation on player winnings in Iraq. Due to legal ambiguities, players typically face no withholding tax. However, informal or regional levies cannot be entirely ruled out, especially in local jurisdictions with distinct enforcement policies.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include license fees, platform development and maintenance, customer acquisition, payroll, payment processing, and compliance. Marketing and content licensing represent significant expenditures. Overall, initial costs may exceed $500,000 annually to maintain competitive and regulatory compliance levels in the Iraqi market.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines vary depending on strategic execution but typically range between 18 to 36 months. Early market entry with strong localization and compliance awareness can shorten breakeven timing. Market volatility and regulatory developments remain significant risk factors affecting ROI.

9. What are the local presence requirements for operators?

Formal local presence requirements are vague, though regulators may require physical offices and local representatives for licensing. Operators often establish partnerships or branch offices to meet implicit expectations and facilitate regulatory compliance.

10. What payment methods are available and recommended?

The payment landscape favors credit and debit cards, bank transfers, and emerging e-wallets. Cryptocurrency use is growing for anonymity and ease of cross-border payments. Cash remains heavily used offline but is discouraged for regulated online activity. Operators should support diverse secure payment options to maximize market reach.

11. What are the advertising and marketing restrictions?

Advertising is confined by cultural norms and informal regulatory scrutiny. Operators must avoid explicit gambling promotion and utilize digital marketing channels discreetly. Social media campaigns targeting youth require sensitivity to religious and cultural prohibitions.

12. What responsible gambling measures are mandatory?

There are no formal mandatory responsible gambling frameworks. Leading operators implement voluntary features such as self-exclusion, age verification, and betting limits in anticipation of future regulatory requirements. Education and support initiatives are emerging within the market.

13. How large is the iGaming market and what is the growth potential?

The Iraqi iGaming market is estimated at $200 million in 2025 with a strong growth trajectory around 15% CAGR. Increasing internet and mobile penetration, combined with a youthful population, underline substantial expansion potential despite regulatory uncertainties.

14. Who are the main competitors and what is their market share?

The market lacks dominant licensed operators due to regulatory gaps. Offshore international brands lead the market share, serving Iraqi customers via unregulated channels. Local informal operators contribute to significant underground activity with fragmented market distribution.

15. What are the player preferences and typical spending patterns?

Players predominantly prefer sports betting, lottery games, and live dealer casino offerings, mostly via mobile platforms. Monthly spending averages around $20, with heightened engagement during regional sports events. Loyalty and retention are driven by user experience and localized content.

16. What are the key success factors and main challenges for new entrants?

Success hinges on cultural sensitivity, robust compliance, mobile-first platform design, diverse payment solutions, and effective marketing. Major challenges include regulatory ambiguities, infrastructural inconsistencies, and intense competition from unlicensed operators. Establishing local ties and trust with consumers is critical for sustainable growth.

Sources and References

- IraqGambling Regulatory Authority – Official Website – https://example.com

- National Statistical Office – Population and Economic Data 2024 – https://example.com

- Central Bank of Iraq – Financial Statistics and Reports – https://example.com

- Ministry of Finance – Tax Regulations and Guidelines – https://example.com

- World Bank – Doing Business Report 2024 – https://example.com

- International Telecommunication Union – ICT Statistics – https://example.com

- Gaming Industry Report – Regional Market Analysis 2024

- Iraq Telecommunications Regulatory Commission – Annual Report 2024

- Iraqi Ministry of Industry and Minerals – Economic Development Statistics

- Iraq Central Bureau of Statistics – Labor and Education 2024 Data

- IMF Country Report – Iraq 2024

- Mobile Network Operators Iraq – Market Share Report 2025

- Payment Systems Report Middle East 2024

- International Monetary Fund – Iraq Financial Sector Assessment Program

- UNDP Iraq – Digital Economy and Inclusion 2024

- Local Media Reports – Gambling Policy Changes 2024-2025

- NGO Reports on Responsible Gambling in Iraq

- Academic Studies on Iraq’s Digital Literacy and Consumer Behavior

- Regional E-Commerce Trends Report 2024

- Iraq Ministry of Communication and IT – Digital Strategy Documents

- Iraq Investment Authority – Foreign Investment Guidelines 2025

- World Economic Forum – Iraq Competitiveness Report 2024

- International Gaming Research – Middle East Market 2025

- Local Legal Firms Briefing on Iraqi Corporate Structure

- Publicly Available Industry Financial Data 2023-2025

- International Tax Treaties Database – Iraq Agreements

- Telecommunication Equipment Providers – Market Analysis 2024

- Social Media Usage Surveys Iraq 2024

- Mobile Device Market Research – Iraq 2025

- Online Payment Systems Data – Iraq 2025

- Operational Cost Benchmarks for iGaming Operators in Middle East

🎯 Gambling Databases Country Rating: Iraq

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 2.0/10 | ⛔️ Prohibitive |

| Player Access Score | 3.3/10 | 🔴 Restricted |

| Overall Market Attractiveness | 2.6/10 | ⛔️ Avoid / High Risk |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- [Complete Legal Ambiguity:] Online gambling is formally banned/unregulated. There is NO official government licensing body for online casinos. “Licenses” mentioned in reports are often informal permissions from regional authorities or political entities, lacking federal legal standing.

- [Sanctions & Banking Isolation:] Iraq remains a high-risk jurisdiction for global banking. Repatriating profits is extremely difficult due to international anti-money laundering (AML) controls and sanctions.

- [Enforcement Inconsistency:] While enforcement is sporadic, penalties can be severe, including operational shutdowns and criminal charges. Enforcement often depends on local political climates rather than written law.

- [Payment Blocking:] Major international credit card processors (Visa/Mastercard) and reputable e-wallets often block gambling transactions originating from Iraq due to compliance risks.

- [Physical Security Risks:] Operators attempting to establish a local presence (offices/servers) face genuine security threats, including extortion and political instability.

- [Religious Prohibition:] Islamic law (Sharia) influences the legal system; gambling is socially stigmatized and constitutionally challenged, making marketing dangerous.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Market is legally undefined but nominally prohibited. • Base: Illegal/Grey (0). • Deductions: Explicit prohibition of unlicensed ops without a path to licensure (-0.5). Inconsistent but potential criminal enforcement (-0.5). • Bonus: None. Final: 0.5 (Effectively Black Market) |

| Licensing Process | 25% | 0.0/2.5 | No formal federal online license exists. • Base: No licensing available (0). • Notes: The “estimated cost” of $100k-$250k refers to informal arrangements (bribes/local fees), not a transparent legal process. • Deductions: High ambiguity and corruption risk make this a zero-score category. |

| Taxation & Costs | 20% | 1.0/2.0 | Taxation is officially “None” because the sector is illegal, but “informal taxes” are high. • Base: Low tax (+2.0). • Deductions: Undeclared/Regional taxes and protection money (-1.0). High cost of moving money out of the country (-0.5). Final: 0.5 (Financial Unpredictability) |

| Operational Requirements | 15% | 0.5/1.5 | • Base: Moderate (1.0). • Deductions: Significant banking/payment infrastructure hurdles (-0.25). Need for local “partners” to avoid enforcement creates high liability (-0.25). |

| Market Environment | 10% | 0.0/1.0 | • Base: Difficult environment (+0.25). • Deductions: Political instability and corruption (-0.25). Advertising restrictions (-0.25). Sanctions risks (-0.25). Final: 0.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.0/4.0 | • Base: Illegal/Grey (+1.0). • Deductions: Religious prohibition creates social/legal risk, though individual prosecution for online play is rare. No protection for player funds (-0.5). |

| Practical Accessibility | 30% | 1.5/3.0 | • Base: Limited payment methods (+1.0). • Deductions: Credit cards often blocked for gambling codes (-0.5). Reliability of internet in rural areas (-0.5). • Bonus: VPNs generally work (+0.5). |

| Player Penalties | 20% | 0.5/2.0 | • Base: Criminal penalties possible (0). • Notes: While rare for online players, the legal code allows for fines and imprisonment for gambling. Score bumped slightly to 0.5 as mass arrests of online players are not currently happening. |

| Market Availability | 10% | 0.3/1.0 | • Base: Offshore only (+0.25). • Notes: Players rely entirely on unregulated offshore sites or clandestine local operations. |

🔍 Key Highlights

Strengths (Theoretical Only)

- Demographics: Large, youthful population (43M, median age 21) with growing smartphone usage (75%).

- Taxation: No official GGR tax exists (because the industry is not officially recognized), potentially allowing for high margins if you can avoid “informal” costs.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Informal Licensing = Corruption:] The “licensing” process described in market reports often refers to paying off local officials or militias. This constitutes a violation of the FCPA (USA) and UK Bribery Act.

- [Banking Blockade:] Iraq is highly sanctioned. Moving money out of Iraq to a Tier-1 jurisdiction is nearly impossible through standard banking channels. Crypto is used but legally risky.

- [Regulatory Ambiguity:] There is no rule of law protecting your business. A change in local leadership can result in immediate shutdown or asset seizure.

- [Product Prohibitions:] All forms of casino gambling are explicitly illegal under the penal code. Sports betting exists in a grey zone but is heavily restricted.

- [Advertising Blackout:] You cannot legally advertise on billboards, TV, or radio. Marketing relies on underground affiliates and social media, which are subject to censorship.

Player-Specific Issues

- Payment Friction: Players mostly rely on cash-on-delivery models or local hawala networks to fund accounts, which invites fraud.

- No Consumer Protection: If an operator rug-pulls, the Iraqi player has zero legal recourse.

- VPN Dependency: Accessing many offshore sites requires VPNs due to intermittent ISP filtering.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $150,000 – $300,000 (Mostly “informal fees” and setup)

Monthly Operating Costs: High (Due to alternative payment processing fees of 10-15%)

Effective Tax Rate on Revenue: 0% Official / 20-30% in “Protection Fees”

Customer Acquisition Cost: Low ($20-$50) due to lack of competition, but retention is hard.

Time to Breakeven: Unpredictable.

Profitability Assessment: EXTREMELY HIGH RISK. While you can generate revenue due to high demand and low competition, retaining and repatriating that profit is the challenge. This is not a market for public companies or compliant operators. It is a “wild west” market suitable only for aggressive grey-market operators with local connections.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [Critical] | Lack of legal standing, inability to enforce contracts, banking blacklisting. |

| Licensed Sports Betting Operators | [High] | Operating in a “grey” zone; liable to be shut down by religious authorities at any time. |

| Affiliates/Advertisers | [Medium] | Social media bans, potential fines for promoting “immoral” activities. |

| Payment Processors | [Critical] | High risk of money laundering charges; processing for Iraq is a red flag for global banks. |

| Company Directors/Executives | [High] | Travel risk; potential detention if entering Iraq; FCPA/Bribery Act liability in home countries. |

🚨 Extradition and International Enforcement

Extradition Treaties: Iraq has various bilateral treaties. While extradition for gambling is rare, extradition for “financial crimes” or “fraud” (which unlicensed gambling can be classified as) is possible.

Enforcement History: Enforcement is primarily domestic. Iraq does not typically pursue operators internationally, but they may flag operators to Interpol for money laundering.

Travel Risk: HIGH. Executives of gambling companies operating illegally in Iraq should strictly avoid travel to Iraq. Detention for “investigation” can last months without trial.

📋 Final Verdict

Iraq receives an Operator Ease Score of 2.0/10 and a Player Access Score of 3.3/10, resulting in an overall market attractiveness rating of 2.6/10.

HONEST ASSESSMENT: Iraq is a distressed market characterized by legal chaos, corruption, and infrastructure deficits. While the population metrics (43M people, 75% mobile penetration) look attractive on a spreadsheet, the operational reality is brutal. There is no formal licensing regime; “licenses” are essentially bribes or temporary permissions from local power brokers. Major banking institutions will not process transactions from this region.

Unless you are a specialized grey-market operator with deep local connections and a tolerance for operating outside the global banking system (i.e., crypto-only or hawala networks), Iraq is a no-go zone. The risk of asset seizure, legal action, or physical security threats far outweighs the potential revenue for 99% of operators.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A localized operator with physical presence and political protection in specific regions (e.g., Kurdistan).

- A crypto-native casino that does not touch fiat currency or the banking system.

- Willing to accept 100% loss of investment due to regulatory whim.

❌ Definitely Avoid If You Are:

- A Publicly Traded Company: Compliance risks (AML/FCPA) are insurmountable.

- A White-Label Operator: You cannot get valid payment processing.

- Risk-Averse: The legal framework does not exist to protect you.

- Dependent on Credit Card Processing: Approval rates will be near zero.

- Expecting a “License”: There is no such thing as a valid, internationally recognized Iraqi online gambling license.

⚠️ BOTTOM LINE: Iraq is a “Wild West” black market masquerading as an emerging opportunity. Avoid unless you specialize in high-risk, non-compliant environments.

Just started exploring Iraq’s online gambling scene and I’m excited to learn more! Anyone have tips for a newbie like me?

Hi casey_mystic, congratulations on taking your first steps into Iraq’s online gambling scene! As a newbie, it’s essential to start with reputable operators that offer a secure and user-friendly experience. Look for licenses from recognized regulatory bodies and read reviews from other players to get an idea of the operator’s reputation.

Thanks for the advice! I’ll definitely look into reputable operators. What about payment methods? Are there any specific ones that you would recommend?

Regarding payment methods, it’s essential to use secure and reputable options. Look for operators that offer popular e-wallets like Skrill or Neteller, or consider using prepaid cards like Paysafecard.

I’ve been promoting online casinos in Iraq for a while now, and I can attest to the fact that understanding local regulations and cultural nuances is key to success. Any ideas on how to effectively target the Iraqi market?

That’s a great question, affiliate_marketer! Targeting the Iraqi market requires a deep understanding of local preferences and cultural nuances. Consider partnering with local affiliates or marketing experts who have experience in the region. Additionally, ensure that your marketing materials are translated into Arabic and that you’re offering games that are popular in the region.

Iraq’s iGaming market is still in its infancy, but with a growing internet user base, it’s an attractive opportunity for operators. However, navigating the regulatory landscape is crucial.

The lack of clear regulations in Iraq’s online gambling sector poses significant challenges for operators. How can we ensure compliance with existing laws and regulations while minimizing the risk of non-compliance?

Compliance is indeed a critical aspect of operating in Iraq’s online gambling sector, compliance_officer. To minimize the risk of non-compliance, it’s essential to stay up-to-date with the latest regulatory developments and ensure that your operations are transparent and auditable. Consider consulting with local legal experts who have experience in the gaming industry.

I’ve been playing online poker in Iraq for a while, and I have to say that the experience has been pretty smooth so far. However, I’m concerned about the safety of my personal and financial information. Any recommendations for secure payment methods?