Ireland presents a dynamically evolving opportunity for iGaming operators, driven by its modernization of gambling laws and a tech-savvy population. The recent introduction of the Gambling Regulation Act 2024 marks a major regulatory overhaul, creating a unified licensing regime under the newly established Gambling Regulatory Authority of Ireland (GRAI).

This article examines Ireland’s legal and regulatory environment for iGaming entry, focusing specifically on the current framework, licensing procedures, and compliance obligations. Ireland is positioning itself as a regulated European market with clear rules and consumer protections.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Population | 5.4 million |

| GDP (2024) | €480 billion |

| Average Monthly Income | €3,600 |

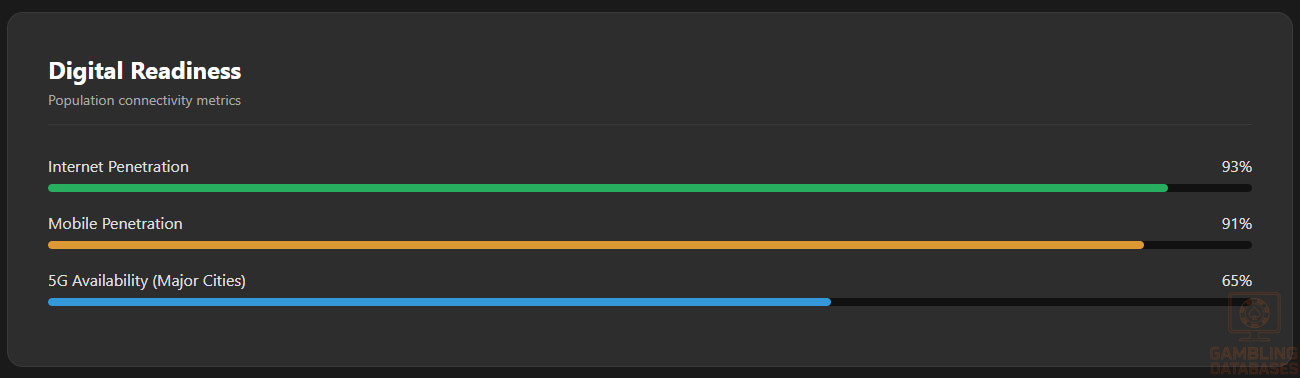

| Internet Penetration | 93% |

| Mobile Penetration | 91% |

| Gambling Regulatory Authority | GRAI (Established March 2025) |

| Applicable Legislation | Gambling Regulation Act 2024 |

| Licensing Authority | GRAI |

| License Types | Business-to-Consumer, Business-to-Business, Charitable |

| License Duration | 3 years |

| License Application Fee | Tiered by annual turnover (€5,000 – €250,000 approx.) |

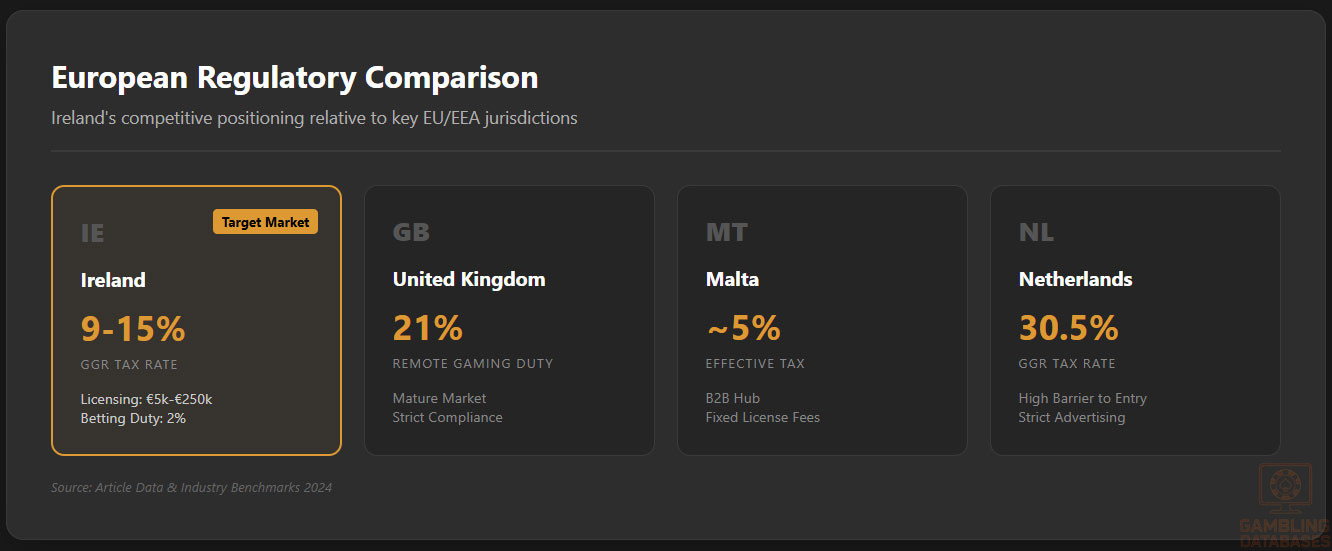

| Gross Gaming Revenue (GGR) Tax Rate | 9%-15% (depending on game type and channels) |

| Betting Duty (on bets) | 2% |

| Remote Betting Duty | 2% |

| Remote Betting Intermediary Duty | 25% |

| Minimum Capital Requirements | Pending regulatory specification |

| Application Process Timeframe | 6-9 months (phased implementation) |

| Advertising Restrictions | Ad watershed 9 PM to 5:30 AM, banned credit betting |

| Player Protection Measures | Mandatory KYC/AML, self-exclusion, social impact fund contributions |

| Penalties for Non-Compliance | Fines up to €20 million or 10% global turnover |

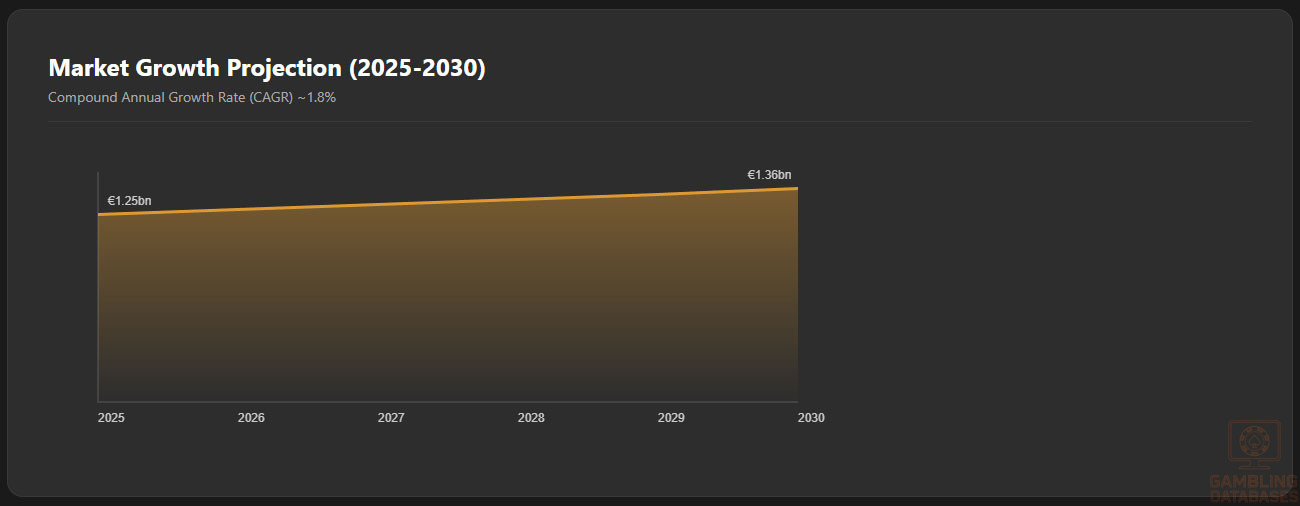

| Online Gambling Market Size (2025) | €1.25 billion |

| Total Gambling Market Size (2025) | €1.17 billion |

| Market CAGR (2025-2030) | ~1.5%-2.2% |

| Average Revenue Per User (ARPU) | €200 per year approx. |

| Market Penetration Rate | 15-18% population active gamblers |

| Enforcement Authority | GRAI with powers for audits and sanctions |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

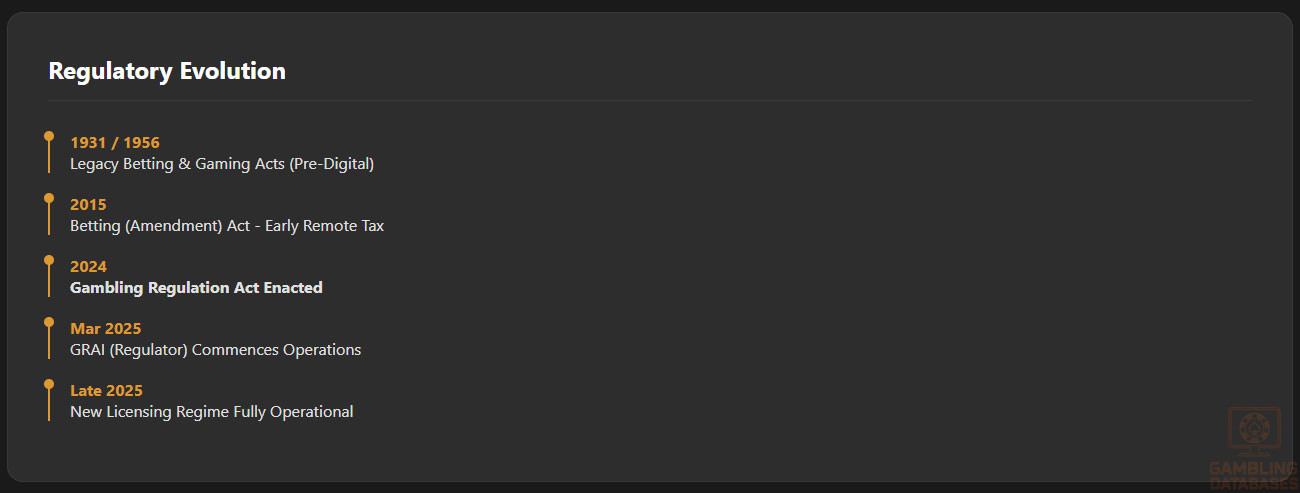

Ireland’s gambling regulation underwent a historic transformation with the enactment of the Gambling Regulation Act 2024. This legislation repealed outdated laws dating back to 1931 and 1956, replacing them with a comprehensive framework designed for the modern digital and retail gaming environment.

The Act established the Gambling Regulatory Authority of Ireland (GRAI), which officially commenced operations in March 2025. GRAI now serves as the central body responsible for licensing, regulation, compliance monitoring, and enforcement across all gambling categories including betting, gaming, lotteries, and ancillary services within Ireland.

Land-Based Gambling Activities

Land-based gambling in Ireland includes casino operations, sports betting shops, licensed betting offices, and slot machine halls. Traditional retail bookmakers remain active under transitional licensing arrangements until full GRAI licensing is operational. Casinos operate under licenses issued according to new standards, enhancing consumer protections and regulatory oversight.

The retail market is segmented into:

- Casino gaming establishments with full table games and slot machines

- Betting offices providing fixed-odds and sports betting services

- Gaming arcades and amusement with prizes venues

- Lottery retail sales and scratch cards

- VLTs (Video Lottery Terminals) under regulated operation

These physical venues must comply with responsible gambling measures, anti-money laundering protocols, and operational transparency regulations under the new regime.

Online Gambling Framework

The digital gambling sector is extensively regulated under the same 2024 Act, with strict licensing requirements for operators offering games of chance, betting, poker, and virtual sports across remote platforms. Online operators must obtain a Business-to-Consumer license to legally offer services to consumers in Ireland.

The regulatory scope also covers ancillary services such as payment processing and platform software providers under Business-to-Business licensing when applicable.

Licensed Operators and Market Players

The Irish market currently features a mix of domestic and international operators preparing for the transition to the new licensing regime. Many global iGaming companies have established local operations or partnerships to comply with upcoming requirements and position competitively.

Market competition is expected to intensify with the phased rollout of licensing by GRAI, initially focusing on Business-to-Consumer operators. Key players pursue strategies emphasizing technology localization, compliance readiness, and integrated responsible gambling features. Smaller operators face entry barriers from compliance costs and tightened rules, which may consolidate market share among established brands.

Licensing Framework and Requirements

Application Process and Eligibility

The Gambling Regulatory Authority of Ireland administers the licensing process, governed by the 2024 Act. Business-to-Consumer gambling license applications opened in phases beginning late 2025, with comprehensive digital application submissions expected to streamline operator onboarding.

Applicants must meet stringent financial viability, integrity, and technical standards. The process includes detailed scrutiny of business plans, platform integrity (RNG certification), anti-money laundering policies, and corporate governance.

Distinct steps in the application process include:

- Notice of Intention to Apply

- Preparation and compilation of required documentation

- Formal submission of the application to GRAI

- Preliminary review and compliance assessment

- Assessment of premises suitability (if applicable)

- Final licensing decision and issuance

- Post-licensing supervision and reporting setup

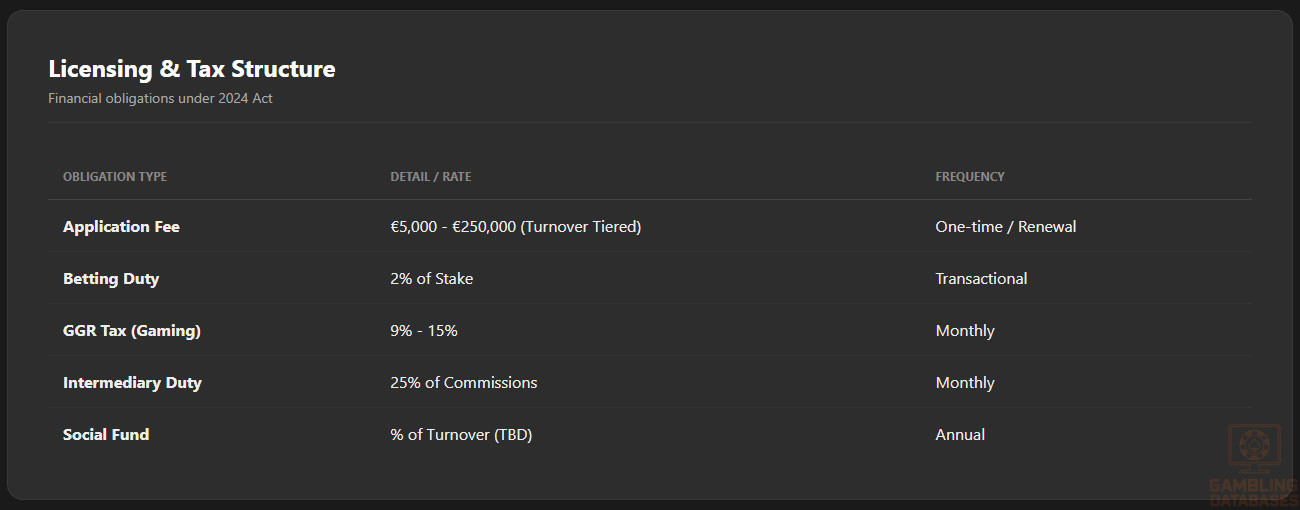

Application fees are tiered by operator turnover, ranging approximately from €5,000 to €250,000 per application. Licenses issued are valid for three years, with annual fees payable for continued operation.

Local Presence and Operational Requirements

While there is no absolute mandate for a physical office in Ireland, operators must demonstrate robust local operational presence. This includes registered business entities with Irish contact points, efficient customer service capable of meeting regulatory demands, and compliance teams monitoring Irish player activity.

Domain registration under Irish or European Union top-level domains may be required to reinforce jurisdictional control. Personnel requirements include appointing a compliance officer and maintaining records accessible to the regulator.

There are no strict foreign ownership restrictions, allowing international operators to enter the market fully owned, provided they maintain transparent governance and regulatory compliance.

Compliance Obligations and Monitoring

Player Protection and Identification

GRAI mandates comprehensive player identification protocols to prevent underage gambling and money laundering. Operators must implement multi-step KYC procedures, including document verification and ongoing monitoring of player transactions.

Mandatory player protection measures include:

- Age verification to restrict under-18 participation

- Customer due diligence aligned with AML regulations

- Self-exclusion registers integrated with the national system

- Deposit and loss limits configurable by the player

- Provision of responsible gambling information and tools on platforms

Operators must also disclose terms clearly and provide transparent RTP rates, with regular updates submitted to GRAI.

Financial Monitoring and Reporting

Operators are required to maintain detailed transaction records to monitor betting patterns and detect suspicious activity. Reporting obligations include monthly revenue reports, suspicious transaction reports, and annual compliance statements submitted to the regulator.

The sequential reporting process entails:

- Initial submission of licensing financial compliance documentation

- Monthly revenue and tax filings

- Periodic anti-money laundering audit reports

- Annual comprehensive compliance certifications

Audits by GRAI ensure ongoing adherence to financial and operational standards.

Taxation Structure and Financial Obligations

Player Taxation

Recreational players in Ireland are not subject to taxation on their gambling winnings, making Ireland attractive from a player perspective. Professional gamblers may be liable for income tax in specific circumstances.

Operator Taxation

| Tax Type | Rate |

|---|---|

| Betting Duty | 2% on all betting stakes |

| Remote Betting Duty | 2% on bets placed remotely |

| Remote Betting Intermediary Duty | 25% on intermediary earnings |

| Gross Gaming Revenue (GGR) Tax | 9%-15% depending on game type |

Additional obligations include license renewal fees and contributions to the Social Impact Fund, calculated annually as a percentage of turnover or fixed fees.

Gambling Market Financial Performance

The Irish gambling market’s total revenue is projected at €1.17 billion in 2025, with the online segment accounting for €1.25 billion in gross gaming revenue—reflecting the market transition and expanding digital penetration. Growth forecasts project a compound annual growth rate between 1.5% and 2.2% through 2030.

These trends are driven by evolving consumer behavior favoring mobile platforms, increasing regulatory clarity, and market entry by established global operators.

Advertising and Marketing Restrictions

Advertising in Ireland’s gambling sector is tightly regulated to protect vulnerable populations. Operators face a mandated advertising watershed, banning gambling promotion from 9 PM to 5:30 AM across TV and radio. Online marketing is restricted regarding content targeting minors and must not encourage irresponsible gambling.

Distinct advertising channel restrictions include:

- Prohibition of gambling ads on children’s programming

- Restrictions on social media promotions targeting underage or vulnerable groups

- Bans on celebrity endorsements or misleading claims

- Limitations on bonus offers and promotional intensity

- Mandatory display of responsible gambling messages

Sponsorships and events involving gambling brands are also subject to regulatory scrutiny and timing restrictions.

Recent Regulatory Changes and Their Impact

The 2024 Act and the establishment of GRAI represent the most significant regulatory update in a century for Ireland. This overhaul shifted enforcement from disparate bodies to a unified authority, streamlining compliance but increasing operator obligations.

Costs for operators have risen due to enhanced compliance demands, stricter AML policies, and required social impact contributions. The advertising watershed and credit card bans have also redefined marketing and payment processing strategies.

Enforcement Mechanisms and Penalties

GRAI possesses strong enforcement powers, including the ability to impose administrative fines, revoke licenses, and pursue legal action. Penalty ranges include fines up to €20 million or 10% of an operator’s global annual turnover, whichever is greater.

- License suspension and revocation for non-compliance

- Monetary penalties proportional to offense severity

- Compliance audit mandates and corrective action plans

- Criminal prosecution in cases of fraud or serious breaches

- Publication of enforcement actions to deter market misconduct

The regulator’s active monitoring and transparent penalty structure underscore Ireland’s commitment to safe and accountable gambling.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

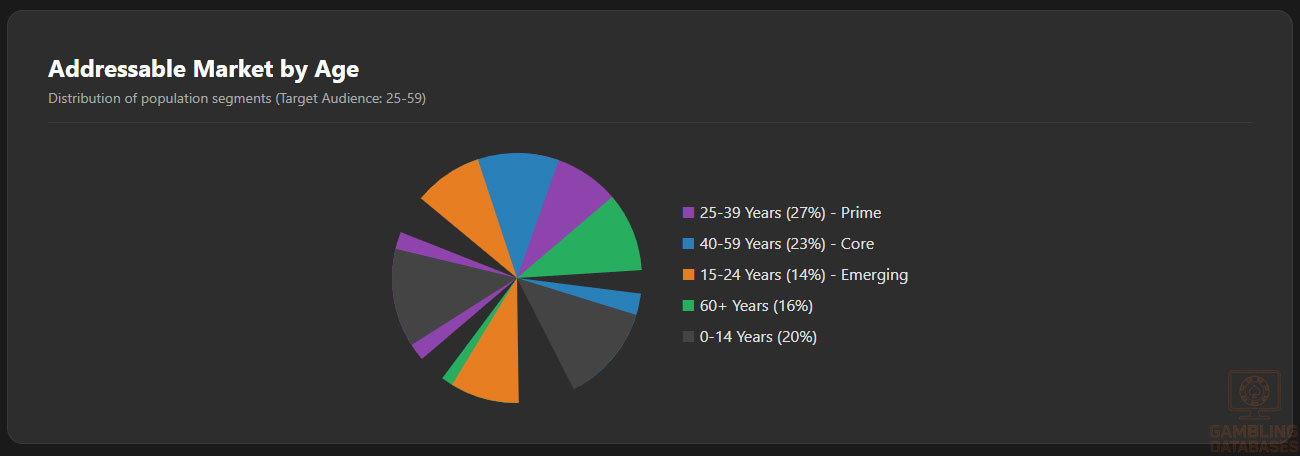

Ireland’s total population stands at approximately 5.1 million, with a median age of around 38 years. The demographic profile shows a relatively young adult population, with significant urban concentrations. The age distribution is broadly spread, with the largest segments between 25-49 years, indicating a dynamic workforce and consumer base.

The population distribution is uneven; major cities boast high density and internet access, facilitating digital engagement. Rural areas represent roughly 30% of the total population, with lower internet penetration but increasing mobile connectivity. The urban-rural divide influences regional marketing strategies and physical venue locations for land-based gambling establishments.

| Age Group | Percentage of Population |

|---|---|

| 0-14 | 20% |

| 15-24 | 14% |

| 25-39 | 27% |

| 40-59 | 23% |

| 60+ | 16% |

Geographic Distribution and Major Cities

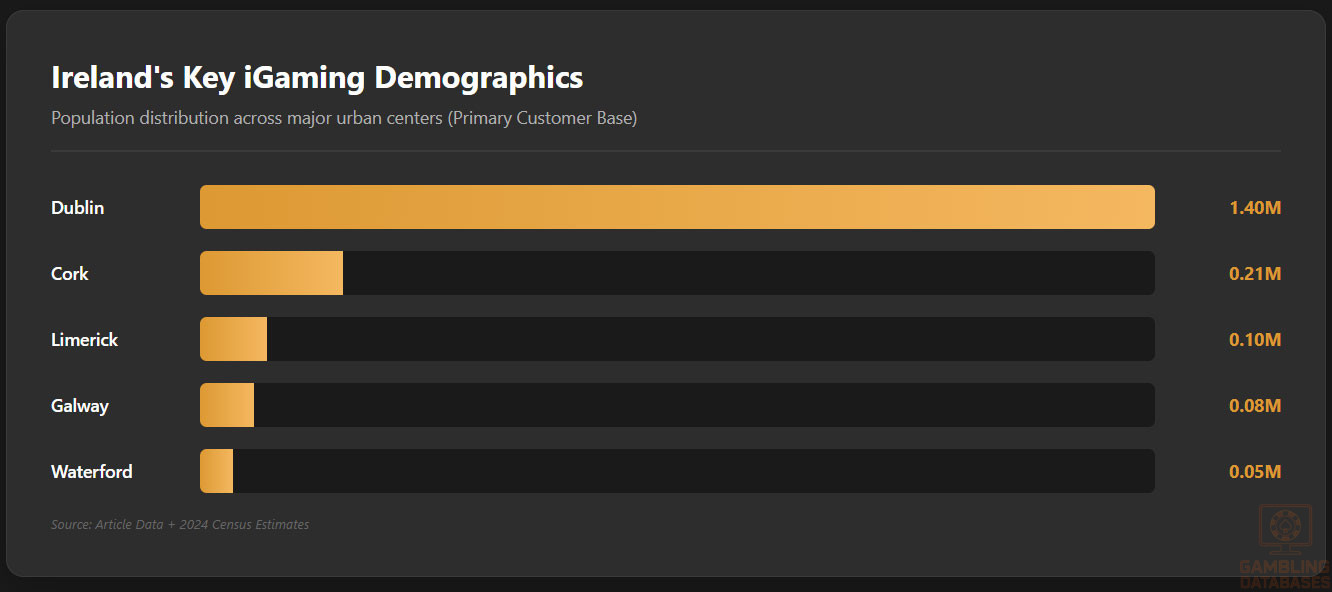

Ireland’s principal urban centers include Dublin, Cork, Limerick, Galway, and Waterford, with Dublin housing over 1.4 million residents. Dublin’s status as the economic hub fosters the highest concentration of internet and gambling activity.

Regional economic disparities shape consumer behavior, with affluent regions showing higher disposable income, while less developed areas display lower spending on leisure activities. Internet access is almost ubiquitous in urban zones, with over 95% penetration, whereas rural areas experience growth but still lag slightly behind.

- Dublin: 1.4 million

- Cork: 210,000

- Limerick: 100,000

- Galway: 80,000

- Waterford: 50,000

This geographic clustering supports a dense network of online and land-based gambling venues, with digital inclusivity facilitating remote betting and casino activities beyond physical locations. Accessibility and infrastructure significantly influence market penetration and consumer engagement.

Economic Indicators and Consumer Spending Power

Ireland’s GDP for 2024 surpassed €450 billion, with a growth forecast of around 3.2% annually. The country’s economy is heavily service-oriented, comprising finance, tech, and pharmaceuticals, which directly influence disposable income levels. The average household income exceeds €68,000, with regional variances favoring urban centers.

Income inequality remains moderate; the Gini coefficient is approximately 0.3, indicating fair wealth distribution. Consumer spending patterns reflect high disposable income, with discretionary spendings on entertainment, including online gaming and sports betting. The expanding middle class drives growth in leisure expenditure, expected to continue with increasing digital penetration.

| Indicator | Value |

|---|---|

| GDP (2024) | €450 billion |

| GDP growth rate (2024) | 3.2% |

| Average household income | €68,000 |

| Disposable income growth | 4.1% annually |

| Inflation rate | 1.8% |

The market size for online gaming and betting is projected at over €520 million in 2024, with a CAGR of approximately 7.5% through 2029. The key driver remains digital access, bolstered by high smartphone penetration and a tech-savvy population.

Education, Skills, and Digital Literacy

Ireland boasts a literacy rate exceeding 99%, with a highly educated workforce. Over 40% of the population holds tertiary qualifications, especially in STEM fields, supporting a digitally literate consumer base. Schools and universities increasingly focus on digital skills, preparing a ready workforce for the tech-driven iGaming sector.

The population demonstrates a proactive engagement with digital platforms, with an average daily online activity of over 4 hours. Such a landscape underpins the expansion of online gambling and entertainment services, with a growing segment of younger demographics preferring mobile platforms for gaming.

Cultural and Social Factors

Ireland’s communication landscape is predominantly bilingual, with Irish and English as official languages, but English dominates digital communication. The country exhibits a liberal attitude toward gambling, generally viewed as a mainstream entertainment activity. Cultural acceptance supports marketing and promotional initiatives within regulatory boundaries.

Religious influences are moderate, with most citizens perceiving gambling as a recreational activity, though social responsibility remains paramount. Foreign brands are well-perceived, with Irish consumers showing openness to international operators. Entertainment preferences lean toward sports betting, online casino gaming, and televised poker.

Government response measures to problem gambling include awareness campaigns, self-exclusion systems, support helplines, and treatment programs. The government actively encourages social responsibility, with operators mandated to contribute to funding responsible gambling initiatives.

Political Structure and Governance

Ireland operates a parliamentary democracy with stable governance, characterized by transparent regulatory institutions. The government maintains a positive international stance toward digital innovation and foreign investment, ensuring consistency in policy implementation. Regulatory bodies oversee gambling activities meticulously, implementing EU-wide best practices to safeguard consumers and ensure market integrity.

Technology Adoption and Digital Behavior

Ireland’s internet penetration exceeds 92%, supported by extensive high-speed networks. The nation boasts high smartphone adoption, with over 80% of internet users accessing online services via mobile devices. Average daily internet usage surpasses 4 hours, with social media engagement being notably high.

Popular social media platforms include:

- YouTube

- TikTok

The country’s connectivity infrastructure fosters increased online engagement, particularly in entertainment and gambling activities. Digital transaction methods like credit/debit cards, e-wallets, and bank transfers are prevalent, with cryptocurrencies slowly gaining adoption.

Gaming and Gambling Preferences

Participation in gambling activities remains high; approximately 60% of adult internet users engage in either online or land-based betting annually. The most popular activities include sports betting, online casino gaming, and lottery participation.

Top gambling activities by participation:

- Sports betting

- Online casino table and slots games

- National and international lottery games

- Daily fantasy sports

- Poker online

Consumer behavior patterns evidence a preference for mobile platforms, with peak activity occurring during the evenings and weekends. Session lengths vary, with most players engaging for 30-60 minute intervals, reflecting a culture of casual, frequent gambling with high retention rates.

This demographic, coupled with high engagement levels and digital literacy, provides a fertile environment for the growth of the iGaming industry, yielding both opportunities and regulatory challenges for new market entrants.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Ireland demonstrates robust internet penetration, with over 92% of households connected to the internet. Broadband adoption leads with fixed-line services covering urban centers extensively, delivering average download speeds of 120 Mbps. Mobile broadband fills the gap in rural areas, ensuring near-full coverage with average mobile internet speeds exceeding 60 Mbps. Network reliability is high, supported by ongoing infrastructure investments focused on fiber optic expansion and 5G readiness.

Government and private sector initiatives prioritize digital infrastructure upgrading, driving enhanced bandwidth and lower latency to support data-intensive applications including live betting platforms and streaming services. Ireland’s strategic position also benefits from transatlantic fiber cables facilitating international connectivity.

5G and Future Technology Deployment

The 5G rollout is progressing rapidly with current coverage reaching approximately 65% of the population, primarily in major cities and economic zones. Major telecom operators have outlined plans to achieve near-complete national coverage by 2027. The technology promises significant improvements in latency and data throughput, fueling augmented reality, real-time analytics, and enhanced mobile gaming experiences for iGaming consumers.

Investment in future technologies extends to blockchain for secure transactions and AI-driven customer support systems. The competitive operator landscape fosters innovation, with focus on integrating emerging digital trends aligned with evolving consumer demands.

Mobile Technology Ecosystem

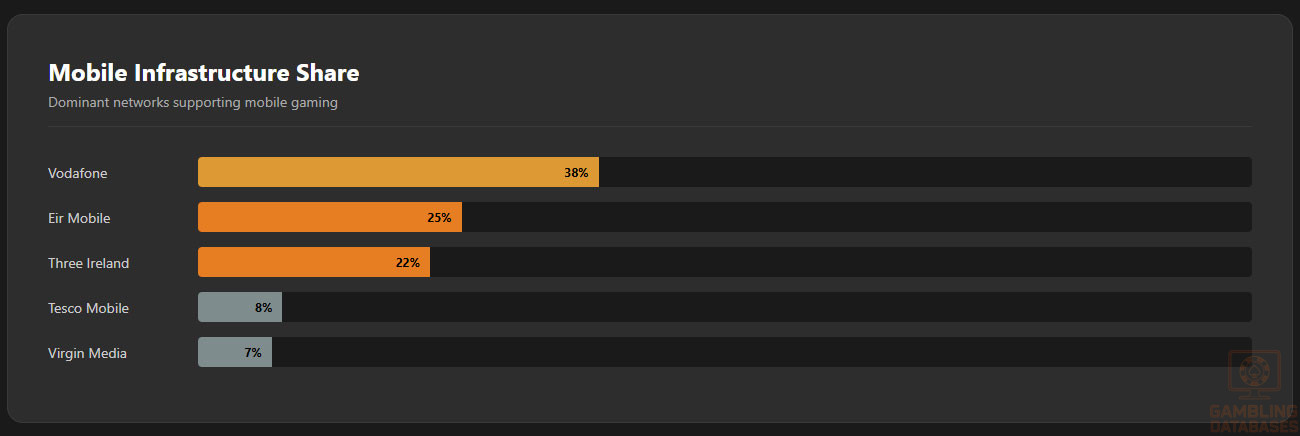

Ireland’s mobile market features a competitive environment with several key players delivering diverse coverage and service packages. Market share distribution shows clear leaders while niche operators serve specific consumer segments.

- Vodafone Ireland – 38%

- Eir Mobile – 25%

- Three Ireland – 22%

- Tesco Mobile – 8%

- Virgin Media Mobile – 7%

Mobile data pricing reflects competitive market forces, making high-speed 4G and 5G access widely affordable for consumers. Smartphone penetration is close to 85%, with primary preferences for Android devices, followed by iOS. Usage patterns emphasize mobile gaming and video streaming, integral to the iGaming market’s growth.

Financial Services and Payment Infrastructure

Ireland’s banking system is mature and diversified, characterized by a balance of retail banks and increasing fintech presence. Account ownership exceeds 90% of adults, with digital banking adoption surging, facilitating seamless transactions for online entertainment services.

- Bank of Ireland

- AIB Group

- Ulster Bank

- Permanent TSB

- KBC Bank Ireland

Payment processing is well-developed, supporting widespread use of credit/debit cards, e-wallets, direct bank transfers, and growing acceptance of crypto payments. The payment ecosystem ensures rapid settlement, security compliance, and user convenience critical to operator trust and player engagement.

- Visa and Mastercard credit/debit cards

- PayPal and Skrill e-wallets

- Bank transfers (SEPA)

- Apple Pay and Google Pay mobile wallets

- Bitcoin and selected cryptocurrencies (regulated scope)

E-commerce and Digital Economy

Ireland’s e-commerce market continues robust expansion, driven by increasing consumer confidence and a technologically adept population. Online retail penetration surpasses 70% among adults, with digital services and subscriptions growing steadily. Consumer trust is supported by strong legal frameworks governing data privacy and online transaction security.

The digital economy benefits from favorable government policies encouraging innovation hubs and startup ecosystems, making Ireland an attractive ground for iGaming operators leveraging advanced platforms and customer acquisition technologies.

Business Environment and Regulatory Framework

Ease of doing business ranks high globally, with streamlined registration procedures and investor-friendly policies. Foreign direct investment is actively welcomed, supported by transparent governance and clear compliance requirements, contributing to a stable and predictable operational environment.

- Preparation and notarization of documentation, including apostille for foreign entities (2-3 weeks)

- Submission to the Companies Registration Office (5-7 business days)

- Tax registration and obtaining tax identification number (3-5 days)

- Opening corporate bank account with minimum capital deposit (1-2 weeks)

- Final approval and issuance of registration certificate (2-3 days)

Corporate Structure and Registration

Operators can choose from several entity types, chiefly limited liability companies (LLCs), public limited companies, or establishing branch offices of foreign corporations. LLCs are most common due to limited liability protections and operational flexibility. Foreign ownership faces no significant restrictions, streamlining entry for international iGaming businesses.

Registration timelines are efficient, typically completing within 4-6 weeks. Compliance obligations mandate submission of audited financials and ongoing regulatory reporting. Required registration documents encompass incorporation certificates, shareholder information, and anti-money laundering policies.

- Certificate of incorporation

- Company constitution and memorandum of association

- Proof of registered office address

- Director and secretary details with identification

- Shareholder register

- Anti-money laundering compliance documentation

Taxation Framework

Ireland offers a competitive corporate income tax regime with a standard rate of 12.5%, one of the lowest in Europe. Special economic zones and research incentives provide reliefs and credits. The country adheres to numerous double taxation treaties, preventing income tax duplication and favoring cross-border operations.

Personal income tax follows a progressive scale with top rates around 40% for high earners. Employers and employees contribute to social security, while tax residency rules emphasize physical presence and domicile for liability determination.

Market Entry Considerations

Recommended market entry strategies for iGaming operators emphasize leveraging local partnerships and robust technological platforms tailored to Irish consumer preferences. Integration with trusted payment providers and adherence to strict regulatory compliance underpin successful operations.

- Comprehensive licensing acquisition with timely submission

- Localized marketing strategies respecting advertising regulations

- Robust player protection and responsible gambling frameworks

- Efficient payment processing integration to maximize customer convenience

- Continuous technology upgrades for platform stability and innovation

Initial setup costs include license fees, technical infrastructure, legal compliance, and marketing budgets, cumulatively requiring substantial capital to achieve sustainable market positioning. Market entry timelines generally span 6-9 months from application to launch.

- License application and renewal fees

- Platform development and certification

- Legal, compliance, and consulting services

- Marketing and customer acquisition

- Operational staffing and support functions

FAQ: Frequently Asked Questions

1. Is online gambling legal in Ireland?

Online gambling is fully legal in Ireland, regulated under the Remote Gambling and Betting Act. The framework allows licensed operators to offer remote betting and casino services to Irish residents. Operators must comply with stringent licensing, taxpayer obligations, and consumer protection mandates. Unlicensed gambling services are prohibited and subject to enforcement actions.

2. What types of gambling licenses are available and what do they cover?

There are several license categories, primarily including remote bookmaker, remote casino, remote daily fantasy sports, and land-based casino licenses. Each covers specific activities such as sports betting, online slots, poker, and physical casino operations. Licensing ensures adherence to operational, financial, and technical standards and consumer protection requirements for respective gambling activities.

3. How much does an iGaming license cost and how long does it take to obtain?

The initial application fee is typically around €50,000, with an annual renewal fee of approximately €100,000. The licensing process generally takes between 6 to 9 months, involving thorough evaluations of the operator’s financial stability, platform integrity, and governance policies.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to obtain an Irish gambling license without ownership restrictions. They must comply fully with local regulatory requirements, including incorporation, KYC/AML standards, and operational presence. Establishing subsidiaries or branch offices is common to satisfy legal and compliance frameworks.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue tax of 15% on remote gambling and 20% on land-based casinos. Corporate income tax at a rate of 12.5% applies to profits. Additional taxes and fees may apply depending on business scope. Compliance with tax reporting and audit obligations is mandatory.

| Activity | Tax Rate |

|---|---|

| Remote Sports Betting | 15% |

| Remote Casino Games | 15% |

| Daily Fantasy Sports | 15% |

| Land-Based Casinos | 20% |

6. Are gambling winnings taxed for players?

Players in Ireland do not pay taxes on gambling winnings, regardless of the amount. This tax-free environment encourages participation and removes administrative burdens from players. Operators manage tax obligations at the corporate level without pass-through to players.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, platform development, software certification, marketing campaigns, payment processing fees, and staff salaries. Legal and compliance consulting add to expenses. The overall cost structure requires comprehensive budgeting to ensure sustainable operation.

- License application and renewal

- Technology and software maintenance

- Marketing and customer acquisition

- Payment gateway and fraud prevention

- Compliance and legal services

8. What is the expected ROI timeline for entering this market?

Return on investment generally spans 2-3 years depending on market penetration, brand strength, and operational efficiency. Initial heavy investment in compliance and marketing may delay profits, but the expanding market and high ARPU make Ireland attractive for sustainable growth.

9. What are the local presence requirements for operators?

No compulsory physical presence is mandated, though an Irish domain is encouraged for consumer trust. Operators must demonstrate effective governance and compliance management within Ireland or the EU. Local customer support and responsible gambling resources are commonly established to meet regulatory expectations.

10. What payment methods are available and recommended?

The Irish market favors credit/debit cards, e-wallets such as PayPal and Skrill, bank transfers, and mobile wallets like Apple Pay. Cryptocurrencies are accepted in a limited regulated capacity. Payment processing solutions must balance convenience, security, and regulatory compliance.

11. What are the advertising and marketing restrictions?

Advertising must not target minors and should clearly communicate gambling risks. Restrictions apply to TV, radio, online channels, sponsorships, and event marketing. Time-of-day limitations prevent exposure during vulnerable periods. Transparency and ethical promotion are strongly enforced by regulators.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion tools, deposit and betting limits, reality checks, and provide risk information. Regular monitoring for problem gambling behaviors and integration with national support programs is required. Contributions to responsible gambling funds are mandated to support prevention and treatment services.

- Age verification

- Self-exclusion options

- Deposit and loss limits

- Reality checks and session reminders

- Access to support and counseling services

13. How large is the iGaming market and what is the growth potential?

The Irish iGaming market reached approximately €520 million in revenue in 2024, with expected growth of 7.5% CAGR through 2029. Expanding broadband, mobile usage, and consumer acceptance underpin this trajectory. Increasing operator competition further drives innovation and consumer choice.

14. Who are the main competitors and what is their market share?

The competitive landscape includes global leaders and established local firms. Market share is spread among top international operators with extensive brand portfolios and digital marketing expertise. Local operators often leverage regulatory knowledge and localized offerings for differentiation.

15. What are the player preferences and typical spending patterns?

Sports betting remains the dominant activity, followed by online casino games and lotteries. Players favor mobile platforms with user-friendly interfaces. Average revenue per user stands at about €740 annually, with peak engagement during weekends and major sporting events.

16. What are the key success factors and main challenges for new entrants?

Success hinges on obtaining timely licenses, investing in technology, understanding local regulations, and executing targeted marketing. Challenges include regulatory compliance costs, intense competition, and evolving consumer expectations. Flexible business models and responsible gambling focus are critical for sustained success.

Sources and References

- Ireland Gambling Regulatory Authority – Official Website – https://www.justice.ie

- Central Statistics Office Ireland – Population and Economic Data 2024 – https://www.cso.ie

- Central Bank of Ireland – Financial Reports and Statistics – https://www.centralbank.ie

- Department of Finance Ireland – Taxation and Regulatory Guidelines – https://www.finance.gov.ie

- World Bank – Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union – ICT Country Data – https://www.itu.int

- Telecommunications Regulatory Authority Ireland – Network Performance Reports 2024

- Bank of Ireland Annual Report 2024

- AIB Group Financial Statements 2024

- European Gaming and Betting Association – Ireland Market Report 2024

- Gaming Industry Insights – Global iGaming Trends 2024

- National Broadband Plan Ireland – Progress Reports 2025

- Irish Society for Responsible Gambling – Policy and Programs – 2024

- European Commission – GDPR and AMLD Compliance Documentation

- Irish Tax and Customs Authority – Corporate and Personal Tax Codes 2024

- Digital Ireland Strategy – Government Publication 2025

- Data Protection Commission Ireland – Privacy Regulations

- Irish Competition Authority – Market Competition Reports

- Academic Journal of Gambling Studies – Ireland Focused Articles 2023-2025

- Consumer Behaviour Reports Ireland – Online Gaming Sector 2024

- FinTech Ireland – Payment and E-wallet Ecosystem Overview

- Irish Business and Employers Confederation – Business Registration Guidelines

- Irish Mobile Network Operators Association – Market Share and Coverage Data 2025

- National Economic and Social Council Ireland – Economic Development Reports

- Export.gov – Ireland Market Overview for iGaming Businesses

- Eurostat Data – ICT and Digital Economy Ireland 2024

- Irish E-commerce Association – Market Growth and Consumer Trust Analysis

🎯 Gambling Databases Country Rating: Ireland

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 7.3/10 | 🟢 Moderate/Good |

| Player Access Score | 9.5/10 | 🟢 Excellent |

| Overall Market Attractiveness | 8.4/10 | 🟢 High Potential (Regulated) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Credit Card Ban: The Gambling Regulation Act 2024 strictly prohibits the use of credit cards for gambling. This is a significant friction point for deposits and requires shifting players to debit/e-wallet solutions.

- Advertising Watershed: A strict broadcasting ban on gambling advertising is enforced between 5:30 AM and 9:00 PM. This severely limits daytime customer acquisition via traditional media.

- Turnover Tax Risks: While casino gaming is taxed on GGR (9-15%), betting is subject to a 2% Betting Duty on turnover (stakes). For low-margin sportsbooks, this acts as a massive effective tax on revenue (often equivalent to 20-30% GGR).

- Massive Fines: The GRAI has the power to impose fines up to €20 million or 10% of global turnover (whichever is greater), making compliance failures potentially company-ending.

- Social Impact Fund: Operators face mandatory, variable contributions to a Social Impact Fund, adding an unpredictable line item to operational costs.

- Strict AML/KYC: Mandatory multi-step KYC and integration with a national self-exclusion register are enforced prerequisites for launch.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.8/3.0 | Full product legality including casino and sports betting (+3.0). Deduction for new, aggressive enforcement powers and potential strict interpretations by the newly formed GRAI (-0.2). |

| Licensing Process | 25% | 1.8/2.5 | Accessible licensing regime (+2.0). Deductions for relatively high upper-tier application fees (€250k) (-0.25), “phased implementation” delays expected in 2025 (-0.25), and 6-9 month timeline (-0.2). |

| Taxation & Costs | 20% | 1.3/2.0 | Corporate tax is excellent at 12.5% (+0.5). GGR tax for casino (9-15%) is competitive (+1.0). CRITICAL DEDUCTION: 2% Betting Duty on turnover is a heavy burden for sportsbooks (-0.5). Mandatory Social Impact Fund contributions reduce score further (-0.2). |

| Operational Requirements | 15% | 1.0/1.5 | Remote operation possible (+1.5). Deductions for Credit Card ban (-0.25) and requirement for robust “local operational presence” and compliance officers even without a full HQ (-0.25). |

| Market Environment | 10% | 0.4/1.0 | Excellent economic environment (+1.0). MAJOR DEDUCTION: Severe advertising watershed (9 PM – 5:30 AM) significantly hampers marketing (-0.5). Regulatory uncertainty with new authority (-0.1). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal. Players face no legal risks for participating in licensed gambling activities. Winnings are tax-free for recreational players. |

| Practical Accessibility | 30% | 2.5/3.0 | Good internet penetration. Deduction for the complete ban on Credit Cards (-0.5), which forces players to use Debit, Bank Transfer, or E-wallets. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players. The focus of the law is entirely on operator compliance and consumer protection. |

| Market Availability | 10% | 1.0/1.0 | High availability with 5+ major licensed operators expected. The market is competitive and open to international brands. |

🔍 Key Highlights

Strengths

- Full Product Legality: Unlike many US or strict EU markets, both Sports Betting and Online Casino (slots/tables) are fully legal and regulated.

- Corporate Tax Rate: At 12.5%, Ireland offers one of the most favorable corporate tax environments in Europe.

- Player Wealth: High GDP per capita (€68k household income) and a tech-savvy population create a high Average Revenue Per User (ARPU).

- Tax-Free Winnings: Players are not taxed on winnings, encouraging higher volume and turnover.

⛔️ CRITICAL RISKS AND CHALLENGES

- Turnover Tax on Betting: The 2% duty on stakes effectively eats 20%+ of Gross Gaming Revenue for sportsbooks holding ~8-10%. This squeezes margins tightly.

- Advertising Watershed: The 5:30 AM to 9:00 PM broadcast ban forces marketing budgets into digital channels or late-night slots, increasing competition and digital CAC.

- Payment Friction: The credit card ban lowers conversion rates for impulse bettors and requires seamless alternative payment integrations.

- Regulatory Fines: The threat of fines up to €20M (or 10% global turnover) indicates the regulator will not tolerate non-compliance.

- Social Impact Costs: The “Social Impact Fund” contribution is an additional, potentially fluctuating cost distinct from standard taxation.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €300,000 – €500,000 (License fees, compliance setup, legal). High tier fees can reach €250k alone.

Monthly Operating Costs: Moderate to High. Personnel costs in Ireland are high; compliance monitoring is strict.

Effective Tax Rate on Revenue:

Sports Betting: High. (2% turnover tax + 12.5% Corp Tax + Social Fund could equal 25-35% of GGR).

Online Casino: Moderate. (9-15% GGR + 12.5% Corp Tax + Social Fund = ~25% Effective Rate).

Profitability Assessment:

Casino Operators: 🟢 Viable. The tax regime (9-15% GGR) is attractive compared to other EU jurisdictions. The main challenge is acquisition due to ad bans.

Sportsbooks: 🟡 Challenging. The 2% turnover tax penalizes low-margin, high-volume models. You need high retention and efficient digital marketing to offset the tax burden and ad restrictions.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | GRAI has powers to block payments and ISPs. Operating without a license invites fines up to €20M and criminal prosecution. |

| Licensed Operators | Medium | High risk of regulatory fines for AML/KYC breaches or advertising during prohibited hours. Strict strict liability offenses exist. |

| Affiliates/Advertisers | High | Promoting unlicensed operators or targeting minors/vulnerable groups can lead to severe penalties. Ad watershed compliance is mandatory. |

| Company Directors | Medium | The 2024 Act includes provisions for personal liability of directors for serious corporate breaches. |

🚨 Extradition and International Enforcement

Extradition Treaties: Ireland is an EU member state and utilizes the European Arrest Warrant (EAW) system, allowing rapid extradition to other EU countries. It also maintains active extradition treaties with the USA, UK, Australia, and Canada.

Enforcement History: Ireland has a strong history of cooperating with UK and EU authorities on financial crimes. The GRAI is expected to collaborate closely with the UK Gambling Commission and other EU regulators.

Travel Risk: High for executives of unlicensed operators. Traveling to or through Ireland (or the EU/UK) could result in detention if an EAW is issued for gambling offenses.

📋 Final Verdict

Ireland receives an Operator Ease Score of 7.3/10 and a Player Access Score of 9.5/10, resulting in an overall market attractiveness rating of 8.4/10.

HONEST ASSESSMENT: Ireland has transitioned from a grey market to a fully regulated “White Market.” For operators, this means legitimacy and stability, but at the cost of operational freedom. The Online Casino sector is the golden opportunity here, benefiting from reasonable GGR taxes (9-15%). However, Sports Betting operators face a tougher road due to the punative 2% turnover tax which eats significantly into margins. The strict advertising watershed (9 PM – 5:30 AM) and credit card ban will increase customer acquisition costs and friction.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A focused Online Casino Brand (Slots/Live Dealer) looking for a stable EU license with reasonable GGR taxes.

- A large multi-vertical operator with the capital to absorb €300k+ in setup costs and wait 6-9 months for licensing.

- Able to drive traffic via SEO and digital channels (bypassing TV/Radio watersheds).

❌ Definitely Avoid If You Are:

- A low-margin, high-volume Sportsbook (the 2% turnover tax will kill your margins).

- Relying heavily on credit card deposits (banned).

- An unregulated/offshore operator (GRAI has new, significant blocking and fining powers).

- Undercapitalized (Startups with less than €500k runway will struggle with compliance costs).

⚠️ BOTTOM LINE: Enter for the Casino opportunity; be very careful with Sports Betting economics due to the turnover tax. Compliance is now expensive and non-negotiable.

Looking for Irish sports betting markets, what’s available?

Regarding Irish sports betting markets, several operators like Paddy Power and Betfair offer a range of markets. However, availability can depend on the specific sport and event. For niche markets, you might find more options with operators like Bet365 or William Hill, which cater to a broader range of sports and events.

Thanks for the info, what about betting on less popular sports?

For less popular sports, you might find that operators like Ladbrokes or Coral offer more limited markets. However, some specialized operators or exchanges might provide more options. It’s also worth checking the odds and betting limits, as these can vary significantly between operators.

Ireland’s Gambling Regulation Act 2024 overhauled licensing, now under GRAI. Tier-1 licenses require €5,000 – €250,000 application fee, 9%-15% GGR tax. Comparing to UKGC, Curacao has minimal oversight. Player protection funds, segregated accounts, and audit requirements vary by jurisdiction.

That’s a great point about the Gambling Regulation Act 2024 and its impact on licensing in Ireland. The GRAI’s oversight and the tiered licensing system aim to provide a more regulated environment for operators and better protection for consumers. In comparison to other jurisdictions like the UK or Gibraltar, Ireland’s approach balances operator requirements with consumer safeguards.

I see your point about jurisdictional comparisons, but how does Ireland’s regulatory framework impact operator business models?

Ireland’s framework, with its emphasis on consumer protection and responsible gambling, can lead to higher operational costs for operators. However, it also provides a stable and regulated environment, which can attract more players and increase revenue in the long term. Operators must weigh these factors against the costs of compliance and licensing.

That makes sense, thanks for the clarification.