Israel presents a challenging iGaming market dominated by restrictive regulations and limited gambling exemptions. Despite strict prohibitions, growing interest in regulated sports betting and ongoing discussions about live betting legalization offer niche entry opportunities.

Understanding Israel’s conservative legal framework, licensing requirements, and taxation structure is crucial for any operator considering market entry or expansion in this unique environment.

| Metric | Value |

|---|---|

| Gambling Legal Status | Highly Restrictive; Mostly Prohibited |

| Regulatory Framework | State Monopoly on Sports Betting & National Lottery |

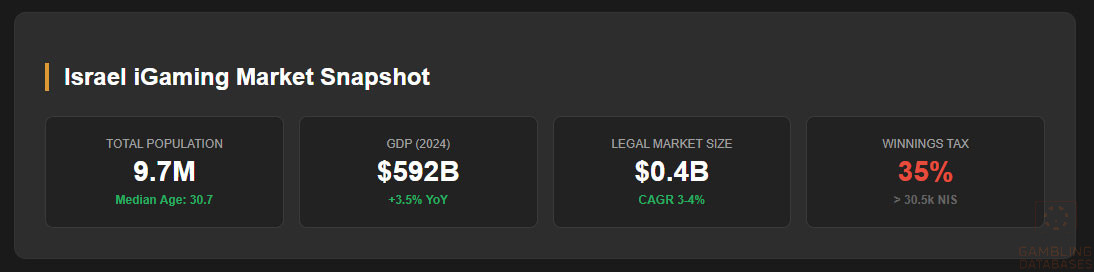

| Population | 9.7 million (2025 est.) |

| GDP | ~USD 592 billion (2024) |

| Per Capita Income | Approx. USD 61,000 (2024) |

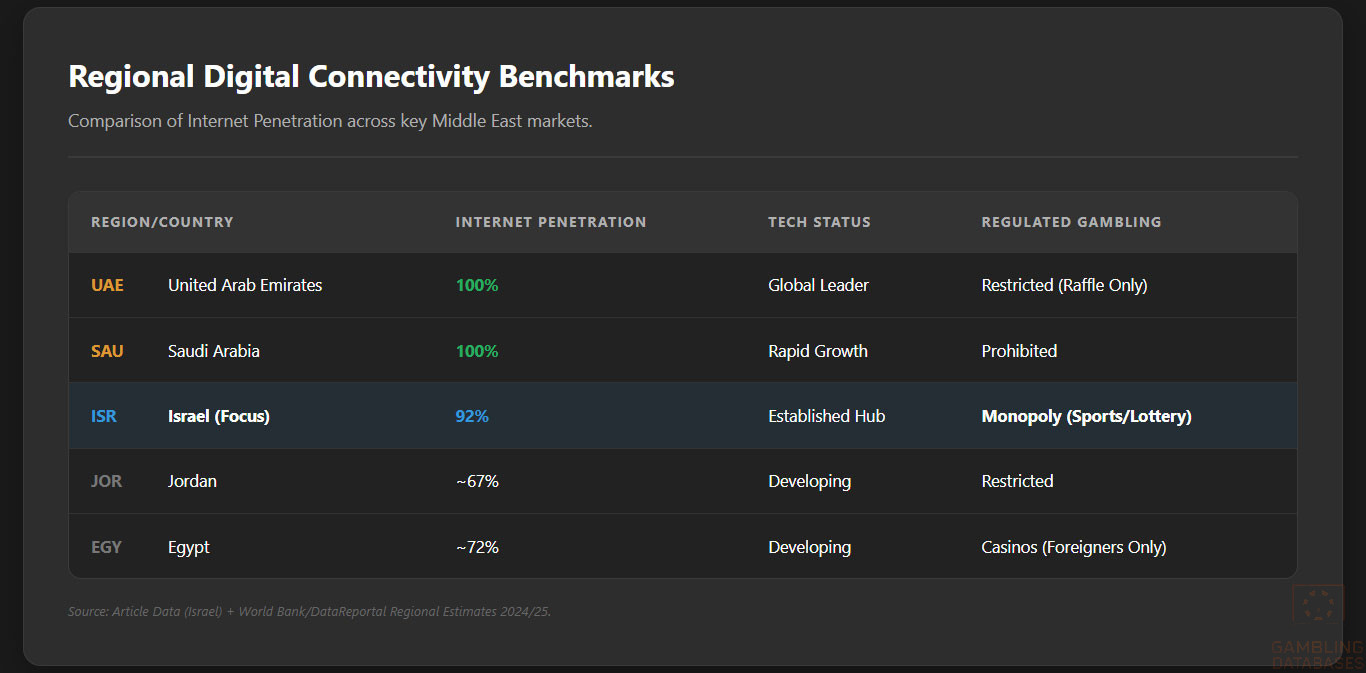

| Internet Penetration | 92% of population |

| Mobile Penetration | 142% (multi-SIM inclusion) |

| Licensed iGaming Operators | 1 Monopoly Licensee (ISBB) for Sports Betting |

| License Application Fee | Not publicly available; licensing limited to state bodies |

| Gross Gaming Revenue (GGR) Tax | Not applicable to private operators; state monopoly model |

| Player Tax on Winnings | 35% above NIS 30,500 threshold (~USD 8,200) |

| Online Gambling Legality | Illegal except ISBB and National Lottery services |

| Average Revenue Per User (ARPU) | Not publicly disclosed; constrained by limited market |

| Market Size (Estimated Revenue) | USD 0.4 billion (strictly legal segment) |

| Market Growth Forecast (CAGR) | Low-to-Moderate; 3-4% within legal framework |

| Online Gambling Enforcement | Active; ISP blocking, financial transaction blocks |

| License Application Process | Restricted to government entities; no private licensing |

| Local Presence Requirement | Mandatory for licensed monopoly entities |

| Regulatory Authority | Ministry of Finance & Israeli Sports Betting Board (ISBB) |

| Compliance Monitoring Entities | Israel Police, Anti-Money Laundering Authority, Tax Authority |

| Payment Processing Restrictions | Bank of Israel bans gambling-related transactions |

| Advertising Restrictions | Strict limits; no public advertising for unlicensed gambling |

| Responsible Gambling Measures | Self-exclusion promoted by ISBB; limited industry requirements |

| License Renewal | Annual review by Ministry of Finance |

| Recent Regulatory Developments | Ongoing debate on live sports betting legalization |

| Enforcement Penalties | Fines, ISP blocking, equipment seizure, criminal charges |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Israel’s gambling laws are among the most restrictive globally. The Israeli Penal Law broadly prohibits gambling activities including lotteries, betting, and games of chance, limiting them to a narrow state-controlled spectrum. The National Lottery and the Israel Sports Betting Board (ISBB) hold exclusive licenses for legally permissible activities.

The legal framework differentiates gambling activities by their nature: those governed by predetermined rules versus those based on agreements between parties. This legal design creates a wide-ranging ban on both land-based and online gambling outside approved exceptions.

Land-Based Gambling Activities

Land-based gambling in Israel is highly limited. The National Lottery offers traditional lottery games, while the ISBB operates limited sports betting venues. Casinos and slot machine halls are illegal, and no private or commercial casinos function legally.

Other forms of betting or gambling halls do not have legal status. The government strictly prohibits establishments facilitating games of chance, maintaining a near-total ban on commercial gambling venues.

Online Gambling Framework

Online gambling is generally prohibited throughout Israel. Only ISBB is authorized to provide online sports betting and horse racing wagering under a government monopoly structure. All other online gambling operators, both domestic and foreign, are considered illegal.

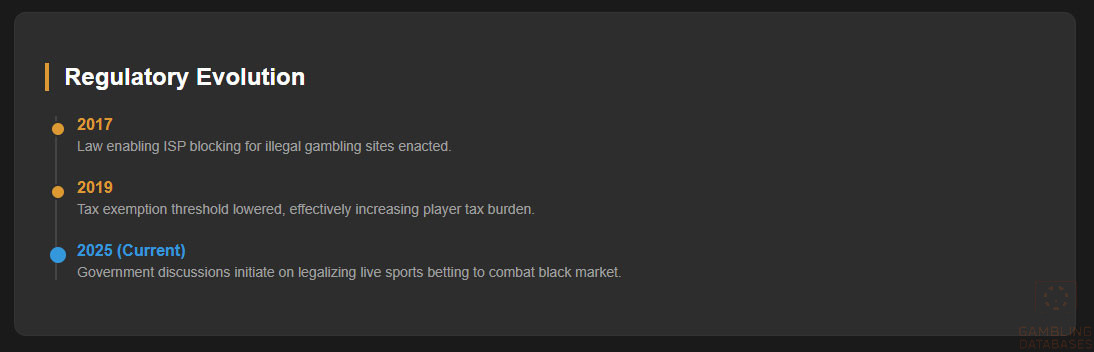

As of early 2025, internal governmental discussions have begun on possibly legalizing live betting on Israeli sports, primarily to combat illegal markets. However, no legislative changes have yet been enacted.

Licensed Operators and Market Players

The Israel Sports Betting Board (ISBB) is the sole licensed operator authorized to offer sports betting, including limited online services. The National Lottery is the other legal gambling entity, operating lottery games under Ministry of Finance oversight.

No private operators have legal licenses to provide any gambling services in Israel. Market entry for private companies is currently blocked by statutory prohibitions.

Market dynamics are shaped by the state monopoly, highly aggressive enforcement of illegal operators, and a small but stable regulated segment mainly focused on sports betting and lottery products.

Licensing Framework and Requirements

Application Process and Eligibility

The licensing framework is exclusively state-controlled. Licenses for gambling operations can only be granted to state entities such as ISBB and authorized National Lottery operators. No licensing pathway exists for private or foreign companies to offer gambling services.

Licensing is governed by the Ministry of Finance, alongside the Israeli Penal Law Chapter 12 and the Law for the Regulation of Sports Betting (1967). Application fees and formal procedures are not publicly defined for private entities due to the exclusive state monopoly.

The regulatory framework requires strict adherence to technical standards, financial stability, and operational transparency for licensed state entities.

Local Presence and Operational Requirements

Licensed entities must maintain a physical presence in Israel. Operational permits are contingent on compliance with local laws, including obligations to cooperate with enforcement authorities and reporting requirements.

Foreign operators face outright prohibitions on offering any gambling services, even from offshore locations. Partnership with licensed state bodies is currently the only viable path to legal market involvement.

Compliance Obligations and Monitoring

Player Protection and Identification

Israel mandates strict age verification to ensure no underage gambling occurs. Robust Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures are enforced by regulatory authorities.

The ISBB promotes responsible gambling measures including voluntary self-exclusion systems and information disclosure to players. While industry-wide responsible gambling standards are limited due to the market’s restricted nature, player protection remains state-prioritized.

- Mandatory age verification at registration and betting

- KYC checks aligned with AML laws

- Self-exclusion options for problem gamblers

- Regular reporting of suspicious transactions

- Limits on maximum betting amounts in certain products

Financial Monitoring and Reporting

Licensed operators are subject to detailed auditing and transaction monitoring, with an emphasis on transparency and anti-fraud controls. Financial institutions cooperate with authorities to report irregular payment flows or suspicious activity.

- Monthly financial reporting to Ministry of Finance and tax authorities

- Submission of audit reports validating compliance

- Real-time transaction monitoring for fraud/AML violations

- Investor and operational disclosures on an annual basis

Taxation Structure and Financial Obligations

Player Taxation

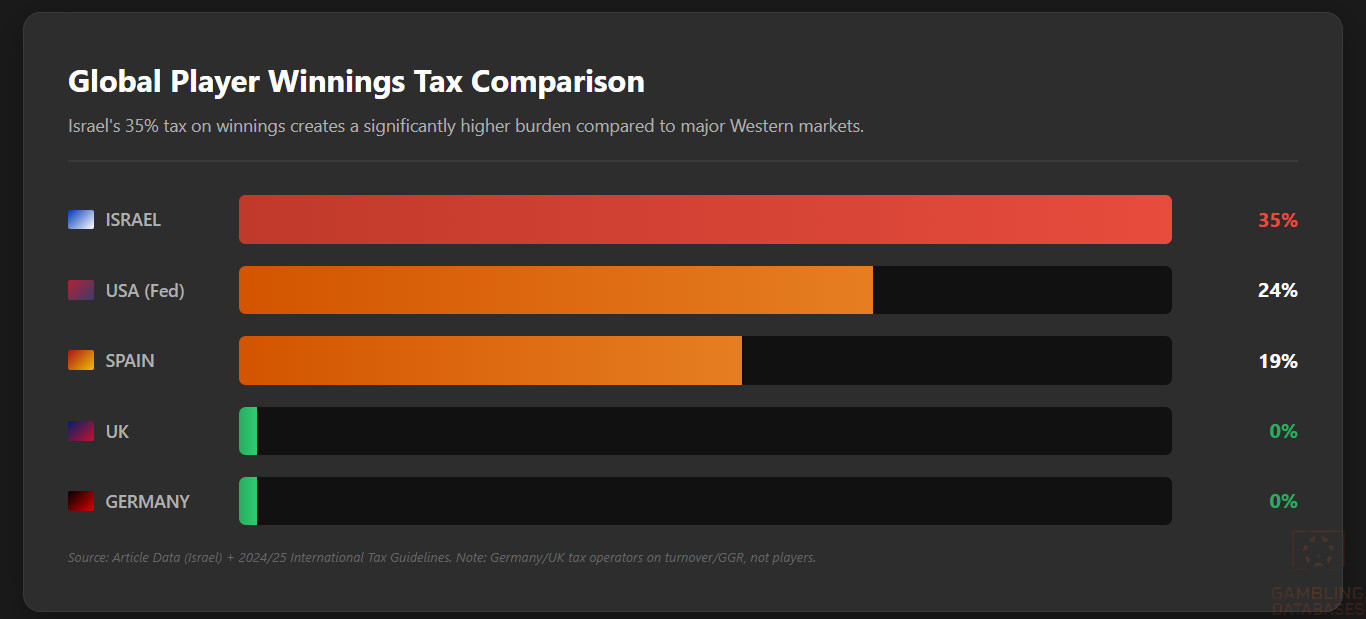

Players are legally obligated to pay taxes on gambling winnings exceeding the threshold of approximately NIS 30,500 (around USD 8,200). This tax is levied at a rate of 35% on amounts exceeding the threshold.

Professional gamblers may be subject to higher progressive tax rates based on classification as income from business or profession, reaching up to 50% depending on income brackets.

Operator Taxation

| Game Type | Tax Rate | Notes |

|---|---|---|

| Sports Betting (ISBB Monopoly) | State revenue-based; no conventional GGR tax | Operated under state authority |

| Online Casinos | Not licensed; no official tax | Illegal for private operators |

| Lottery | State-run revenues only | Ministry of Finance oversight |

| Other Gambling | Prohibited | No taxation regime |

Licenses issued to state operators require annual renewal and may incur administrative fees, though these are not publicly detailed due to the monopoly structure.

Gambling Market Financial Performance

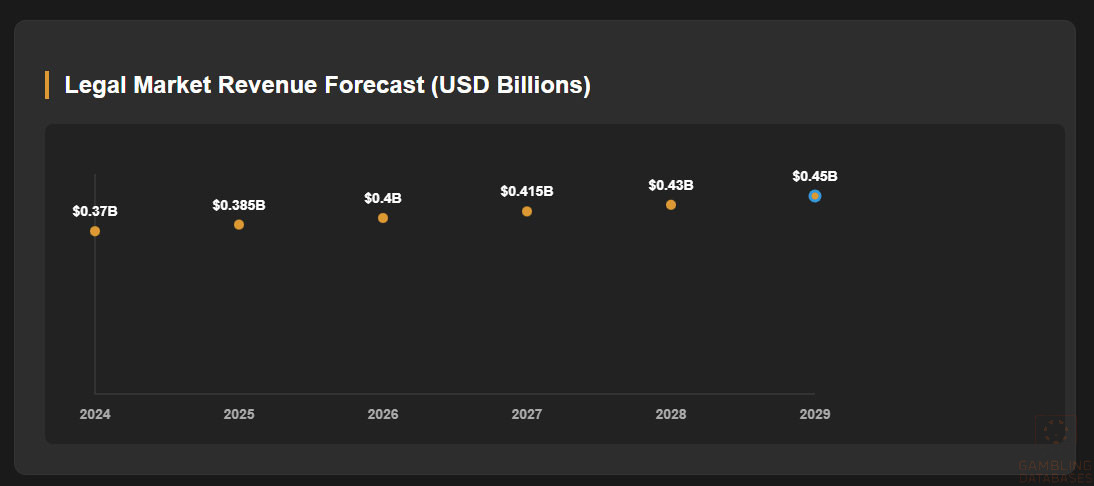

The legal betting and lottery market generates an estimated USD 0.4 billion annually in revenue under the state monopoly. Despite the small scale relative to regional peers, steady revenue growth of 3-4% is projected, largely driven by sports betting interest.

Illegal gambling continues to pose a sizeable challenge, motivating government initiatives to consider legalization of live sports betting as a risk mitigation strategy.

Advertising and Marketing Restrictions

Advertising of gambling services is strictly controlled. Only state-licensed operators may promote offerings, primarily the National Lottery and ISBB sports betting. Public advertising of unlicensed gambling is banned, with severe restrictions on content and timing for approved advertising.

- Bans on advertising unlicensed gambling websites

- Restrictions on promotional content targeting minors

- Prohibition of aggressive marketing tactics

- Limitations on advertising during certain hours

- Sponsorship restrictions in sports and media

Recent Regulatory Changes and Their Impact

- 2017: Law enabling ISP blocking for illegal gambling websites

- 2018: Implementation of ISP blocking to restrict illegal sites

- 2019: Lowering of tax exemption threshold on winnings

- 2025: Initial governmental discussions on legalizing live sports betting

These regulatory steps have increased enforcement costs for illegal operators and strengthened the monopoly’s market position. Potential legalization of live betting could reshape market dynamics in coming years.

Enforcement Mechanisms and Penalties

Enforcement is robust, with authorities empowered to impose fines, block websites via ISP orders, seize equipment, and pursue criminal charges against illegal operators and facilitators.

- Fines for unauthorized gambling provision

- ISP blocking of illegal gambling websites

- Seizure of gambling equipment and funds

- Criminal prosecution and imprisonment

- Financial restrictions imposed by Bank of Israel on payment processors

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

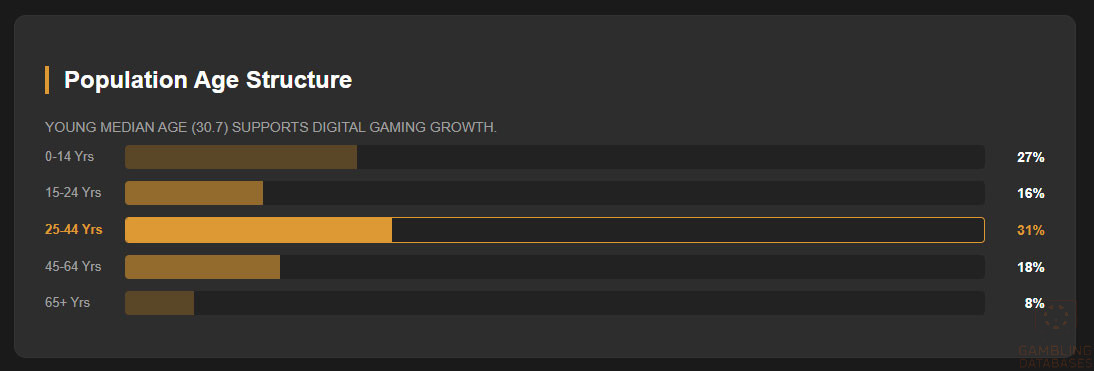

Israel’s population stands at approximately 9.7 million as of 2025, characterized by a relatively young demographic structure and a median age of 30.7 years. The gender ratio is close to parity with a slight male majority, reflecting stable demographic trends supported by steady birth rates and immigration inflows.

Urbanization is high, with over 92% of the population residing in urban areas. This concentration shapes demand for digital entertainment and iGaming opportunities primarily in metropolitan centers, where internet access and disposable incomes are concentrated.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 27% |

| 15-24 years | 16% |

| 25-44 years | 31% |

| 45-64 years | 18% |

| 65+ years | 8% |

The youthful population base supports potential growth in IT-savvy consumers with interest in digital leisure activities, including gaming. Rural areas remain largely underdeveloped regarding digital infrastructure and gambling access.

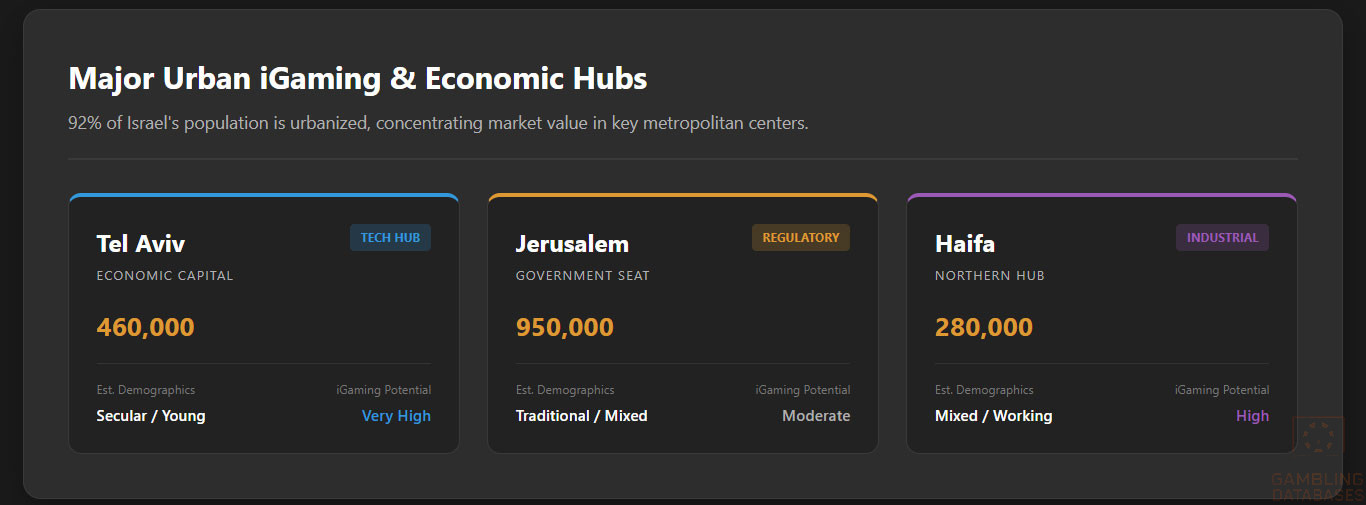

Geographically, population density is highest around the Tel Aviv metropolitan area, Jerusalem, Haifa, and southern coastal cities. These economic hubs dominate in household income levels and digital connectivity, forming the core consumer base for iGaming products.

- Tel Aviv – approximately 460,000 inhabitants

- Jerusalem – approximately 950,000 inhabitants

- Haifa – approximately 280,000 inhabitants

- Rishon LeZion – approximately 260,000 inhabitants

- Petah Tikva – approximately 250,000 inhabitants

- Beersheba – approximately 210,000 inhabitants

Major gambling venues and licensed betting outlets are almost exclusively found in these urban centers, driven by regulatory licensing concentration and consumer demand.

Economic Indicators and Consumer Spending Power

Israel’s economy registered a GDP of approximately USD 592 billion in 2024, growing steadily at an annual rate of 3.5%. The economy’s composition reveals a dominant services sector representing about 70% of GDP, with information technology, finance, and retail leading growth sectors.

Per capita income stands near USD 61,000, among the highest in the region, enabling a relatively affluent consumer base with discretionary spending capabilities suitable for entertainment and gaming services.

Despite wealth concentration in urban centers, income inequality remains moderate, with the Gini coefficient around 0.38. This reflects diverse purchasing powers, with a large middle class driving consumer market dynamics.

| Indicator | Value |

|---|---|

| GDP (USD) | 592 billion |

| GDP Growth Rate | 3.5% |

| Per Capita Income (USD) | 61,000 |

| Unemployment Rate | 3.8% |

| Inflation Rate | 2.1% |

Consumer spending reflects robust retail sales growth, supported by strong credit availability. Entertainment and digital services continue to gain share, especially among younger demographics with rising disposable incomes and mobile connectivity.

Current market size projections for iGaming are modest due to regulatory constraints but show potential growth aligned with gradual digital adoption and evolving social attitudes. Projections estimate growth at a compound annual growth rate (CAGR) of 3-4% in the legal betting segment over the next five years.

| Metric | 2024 | 2029 (Projected) | CAGR |

|---|---|---|---|

| Market Revenue (USD billion) | 0.37 | 0.45 | 3.9% |

| Active Users (Thousands) | 350 | 420 | 3.7% |

| Average Revenue Per User (ARPU) (USD) | 1,050 | 1,080 | 0.6% |

Education, Skills, and Digital Literacy

Israel boasts one of the world’s highest education levels, with literacy rates exceeding 97% and widespread secondary and tertiary education participation. The country’s technological workforce ranks highly in innovation indices, supporting a strong foundation for digital and iGaming industry development.

Digital literacy is advanced, particularly in urban regions, where over 90% of adults have internet proficiency and access to personal computing devices. Technology adoption is driven by a vibrant startup ecosystem and government emphasis on ICT skills training.

These factors contribute to a consumer base comfortable with complex online platforms and digital payment systems, enabling a favorable environment for iGaming user engagement and product innovation.

Cultural and Social Factors

Communication and Language

- Hebrew: Official and dominant language nationally

- Arabic: Official minority language with significant speakers

- English: Widely spoken as a second language, especially among youth and business professionals

- Russian: Spoken by a substantial immigrant population (~20%)

- Amharic and French: Present among minority and immigrant communities

Internet usage and online interaction often occur in Hebrew and English, with bilingual content favored by platforms targeting mass audiences.

Culturally, gambling faces significant social and religious resistance, particularly from Orthodox Jewish communities, who influence public policy and social attitudes. Despite this, secular segments display increasing openness to online gaming activities for entertainment. Foreign brand recognition is positive among younger urban populations, who seek international-style digital gaming experiences.

Problem gambling awareness remains limited but growing. Government and NGOs have implemented support initiatives focused on crisis counseling and prevention programs targeting youth and vulnerable groups. Social responsibility regulations remain modest but are evolving to encourage better player protection practices.

- National helpline for gambling addiction

- Self-exclusion registration support

- Public awareness campaigns on gambling risks

- Collaboration with healthcare providers for addiction treatment

- Research funding for problem gambling studies

Israel’s government operates a parliamentary democracy with stable political institutions. Regulatory consistency is moderate, influenced by coalition politics and conservative social forces. International trade relations and technology partnerships continue to expand, offering strategic advantages for digital service industries.

Technology Adoption and Digital Behavior

Internet penetration in Israel exceeds 92% with average daily usage surpassing 7 hours per user. Mobile adoption is widespread, with smartphone penetration above 95%, supporting high engagement with mobile-first platforms including gaming and betting apps.

- Facebook: Engaging 80% of internet users

- Instagram: Popular among 68% of users aged 18-34

- YouTube: Reaches 90% with high video content consumption

- WhatsApp: Primary messaging app used by 75% of internet users

- LinkedIn: Key professional networking tool with 40% penetration

- TikTok: Rapid growth, especially under age 25 demographic

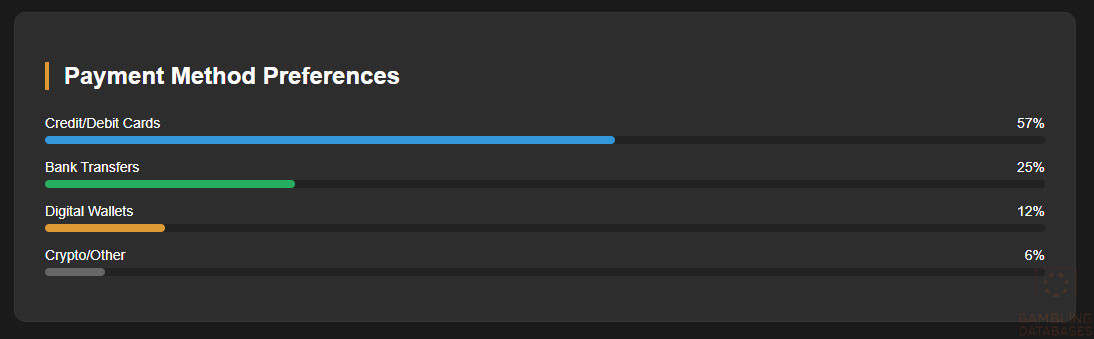

Digital payment behaviors favor credit/debit cards, bank transfers, and increasingly digital wallets. Cryptocurrency use remains niche but is growing due to fintech advancements and regulatory openness to blockchain technologies.

- Credit/Debit cards holding 57% of online transaction volume

- Bank transfers representing 25% of consumer payments

- Digital wallets like PayBox and Pepper Pay gaining market share

- Mobile payments via Apple Pay and Google Pay increasing in popularity

- Cryptocurrency adoption rising within tech-savvy consumer segments

Gaming and Gambling Preferences

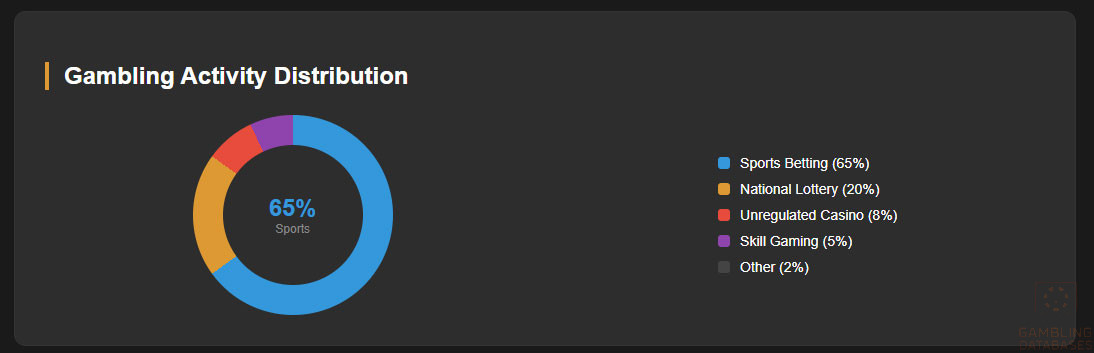

Among the legal market segment, sports betting dominates participation rates, reflecting a strong cultural affinity for football and basketball. Lottery products maintain steady engagement, mainly through offline channels.

- Sports betting (football, basketball, tennis) – 65% participation

- National lottery – 20% participation

- Private unregulated casino gaming – estimated 8% participation

- Online skill-based gaming – 5% participation

- Other betting forms (horses, greyhounds) – 2%

Consumer behavior trends show growing adoption of mobile platforms, with peak gaming activity during evenings and weekends. Session lengths average 30-45 minutes, with retention enhanced by social features and localized content. Consumer spending tends to skew towards mid-level stakes reflecting risk-averse attitudes constrained by legal limits.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Israel exhibits a high level of internet penetration, with over 92% of the population accessing the internet regularly in 2025. The broadband infrastructure is well developed in urban centers, with extensive fiber-optic networks supporting high-speed connections up to 1 Gbps in many areas.

Mobile internet accounts for a significant portion of online access, with mobile broadband subscriptions outnumbering fixed broadband in several demographic groups. Average fixed broadband speeds reach approximately 250 Mbps, while mobile speeds average 120 Mbps, reflecting Israel’s technology-driven telecommunications investments.

The digital infrastructure reliability rates are high, with uptime exceeding 99.8%, supporting gaming platforms demanding low latency and stable connectivity.

5G and Future Technology Deployment

Israel’s 5G rollout began in 2021 and now covers approximately 80% of the population. The deployment is led by the main cellular operators focusing on metro areas and major highways. National plans target full nationwide 5G coverage by 2027, with progressive enhancements in network capacity and latency reduction to serve future digital economy needs.

Operators are investing heavily in newer technologies such as edge computing and IoT frameworks to support advanced gaming experiences, including augmented and virtual reality applications within iGaming.

Mobile Technology Ecosystem

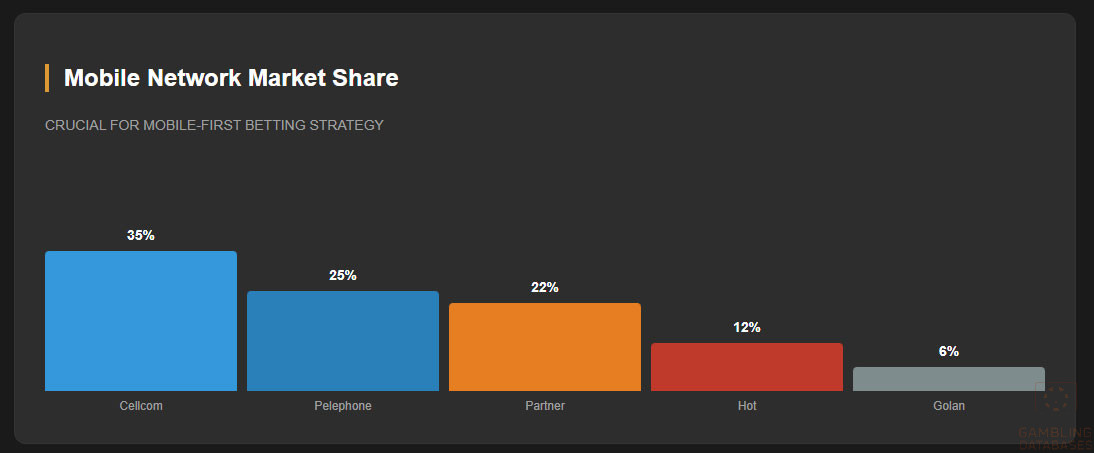

The mobile network infrastructure is highly competitive, comprising several key operators with diverse market shares and comprehensive coverage.

- Cellcom – Largest market share, about 35%

- Pelephone – Holding approximately 25%, strong urban presence

- Partner Communications – Roughly 22%, expanding 5G footprint

- Hot Mobile – 12%, focused on price-sensitive segments

- Golan Telecom – 6%, niche and challenger brand

Mobile data costs are competitive, with average monthly spending on data plans around USD 20-30. This affordability encourages widespread smartphone adoption, with nearly 95% of adults owning a smartphone by 2025.

Device preferences skew towards mid-to-high range Android models, with Apple iPhones capturing significant market share (approximately 40%) among affluent urban users.

Financial Services and Payment Infrastructure

Israel’s banking sector is mature and technologically advanced, featuring widespread acceptance of digital banking services and high account penetration exceeding 90% of adults. Major banks provide robust online platforms compatible with iGaming operator requirements for transactions and compliance.

- Bank Hapoalim – Largest by assets and market penetration

- Bank Leumi – Strong retail and corporate banking operations

- Israel Discount Bank – Significant focus on SME banking

- Mizrahi Tefahot Bank – Leader in mortgage lending and digital innovation

- First International Bank of Israel – Diversified banking services

- Union Bank of Israel – Niche investment and specialized banking

The payment ecosystem includes widespread card usage, bank transfers via the Shekel Clearing House, and a growing range of digital wallets. Financial regulators endorse secure, transparent payment systems compliant with AML and KYC standards critical to the gambling industry.

- Credit/debit cards (Visa, MasterCard)

- Digital wallets (PayBox, Pepper Pay, Apple/Google Pay)

- Bank transfers including instant payments

- Prepaid cards and vouchers

- Emerging cryptocurrency payment gateways (regulated and compliant)

E-commerce and Digital Economy

Israel’s e-commerce market is expanding, now representing an estimated 15% of total retail sales. Consumer confidence in digital transactions is high, supported by secure payment infrastructure and widespread adoption of contactless payments.

The digital service economy thrives on strong consumer trust, regulatory oversight, and technological innovation, positioning Israel as a promising market for digital entertainment verticals such as iGaming.

Business Environment and Regulatory Framework

Israel ranks favorably in the World Bank’s Ease of Doing Business index, marked by streamlined company registration, investor protections, and moderate operational costs. Foreign investment policies encourage innovation, though gaming industry entrants face strict regulatory hurdles.

Market entry requires several sequential registration steps to formalize operations and regulatory compliance.

- Company name reservation and document preparation (2-3 weeks)

- Registration with the Companies Registrar (5-7 business days)

- Tax authority registration and obtaining VAT number (3-5 days)

- Bank account opening and capital deposit (1-2 weeks)

- Licensing or operational approvals for regulated sectors (variable timelines)

Corporate Structure and Registration

Key entity types include Limited Liability Companies, Corporations, and Branch Offices of foreign firms. Limited Liability Companies are the most common for iGaming ventures due to liability protection and operational flexibility.

Foreign ownership is permitted without restrictions in most sectors, though gaming is an exception due to state monopolies. Compliance with anti-money laundering and tax reporting is mandatory.

- Certificate of Incorporation

- Articles of Association

- Proof of Registered Office

- Shareholder and Director identification documents

- Tax registration certificates

Taxation Framework

Corporate income tax stands at a standard rate of 23%, with certain technology companies eligible for benefits under special economic zones. Israel maintains tax treaties with numerous countries, facilitating cross-border business efficiency.

- United States

- United Kingdom

- Germany

- France

- Canada

Personal income tax is progressive, reaching a marginal rate of 50%. Operators must withhold taxes on employee wages and applicable distributions. Social security contributions are mandatory.

Market Entry Considerations

Recommended entry strategies emphasize partnerships with existing licensed entities or digital platform providers. Leveraging advanced technology stacks for localization and regulatory compliance is critical.

- Joint ventures with National Lottery or ISBB franchisees

- White-label partnerships leveraging licensed platforms

- Localized payment gateway integration

- Comprehensive compliance and AML frameworks

- Agile marketing adapting to advertising restrictions

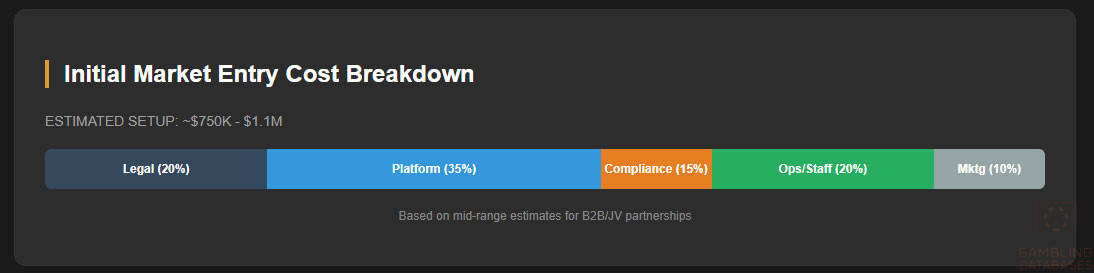

Initial setup costs vary by scale but typically include licensing advisory fees, platform deployment, local staffing, and regulatory compliance investments.

| Cost Category | Estimated Cost |

|---|---|

| Legal and Licensing Advisory | 150-250 |

| Platform Development & Integration | 250-400 |

| Compliance & AML Systems | 100-150 |

| Marketing & Localization | 75-125 |

| Operational Staffing & Offices | 150-200 |

Market entry timelines typically span 6-12 months from initial investment to operational launch, contingent on regulatory approval processes and technology readiness.

- Feasibility and strategic planning (1-2 months)

- Company formation and licensing consultation (2-3 months)

- Platform development and localization (3-4 months)

- Regulatory compliance and testing (1-2 months)

- Market launch and scaling (ongoing)

Success factors include deep understanding of regulatory nuances, advanced technological infrastructure, strong local partnerships, and culturally sensitive marketing. Challenges focus on legal restrictions, high compliance costs, and payment system limitations.

- Robust compliance management

- Effective KYC/AML integration

- Strong digital marketing aligned with legal constraints

- Scalable technology platforms

- Strategic alliances with local stakeholders

Exit strategies require careful planning within legal frameworks, with license transferability limited. Valuations incorporate market niche, compliance standings, and technology assets.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Israel?

Online gambling in Israel is illegal for private operators. Only the Israel Sports Betting Board (ISBB) and the National Lottery hold government-issued monopolies to operate sports betting and lottery services online. All other forms of online gaming are prohibited, with strict enforcement through ISP blocking and financial transaction restrictions. The state is currently reviewing live betting legalization, but no regulatory changes have been implemented.

2. What types of gambling licenses are available and what do they cover?

Currently, gambling licenses in Israel are exclusively issued to state-controlled entities. There are no private license categories for online casinos, sportsbooks, or other gaming activities. Licensed categories include the National Lottery and the ISBB’s sports betting. No commercial or offshore private licenses exist, reflecting the monopoly market structure.

3. How much does an iGaming license cost and how long does it take to obtain?

For private companies, obtaining an iGaming license in Israel is not feasible as licenses are held exclusively by state bodies. Thus, no public fees or application timelines exist for private operators. For state-authorized entities, regulatory fees and review periods are managed internally without publicly disclosed costs.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot independently obtain gambling licenses in Israel. Market entry requires partnership or joint ventures with authorized entities such as ISBB or the National Lottery. Direct foreign online gambling services are prohibited, and foreign operators face blocking and penalties if operating without authorization.

5. What are the tax obligations for iGaming operators?

Due to the monopoly structure, private operators face no legal taxation frameworks, as they cannot legally operate. State operators generate tax revenue under government oversight. Corporate tax rates for general businesses are 23%, applicable to legal entities. Operators must comply with financial reporting and tax obligations applicable to their jurisdiction.

6. Are gambling winnings taxed for players?

Yes, players in Israel pay a 35% tax on gambling winnings exceeding NIS 30,500 (~USD 8,200). Professional gamblers may face higher progressive tax rates. Tax withholding applies at the source for state-authorized games.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing advisory, platform development, compliance systems, marketing, and staffing. Costs vary widely, typically ranging from USD 700,000 to over USD 1 million for initial setup and the first year of operations in regulated jurisdictions. Israeli-specific costs are influenced by limitations on market access and compliance.

8. What is the expected ROI timeline for entering this market?

Due to Israel’s regulated monopoly, private operators face barriers to entry. ROI timelines in comparative regulated markets often range from 18-36 months. Success depends on efficient compliance, market penetration, and product localization.

9. What are the local presence requirements for operators?

Licensed entities must maintain a physical office in Israel, comply with local laws, and cooperate with enforcement authorities. Foreign operators without presence cannot legally offer services.

10. What payment methods are available and recommended?

Credit and debit cards dominate, supported by popular digital wallets and bank transfers. Cryptocurrency use remains developing but offers future potential. Recommended methods emphasize compliance with regulatory AML/KYC standards.

11. What are the advertising and marketing restrictions?

Advertising is highly restricted to licensed entities only, with bans on unlicensed gambling promotions. Restrictions include limited advertising hours, prohibitions on targeting minors, and cautious promotional content.

12. What responsible gambling measures are mandatory?

Mandatory responsible gambling measures include age verification, self-exclusion programs, KYC/AML compliance, and player information disclosure. The ISBB implements voluntary self-exclusion systems, with growing government emphasis on public awareness and problem gambling support.

13. How large is the iGaming market and what is the growth potential?

The legal iGaming market in Israel is small but stable, generating an estimated USD 0.4 billion annually with a projected CAGR of 3-4%. Growth potential exists primarily in legalized sports betting and lottery expansion, pending regulatory reforms.

14. Who are the main competitors and what is their market share?

The competitive landscape is dominated by the Israel Sports Betting Board and the National Lottery holding exclusive licenses. No significant private competitors operate legally. Illegal operators exist but face enforcement risks.

15. What are the player preferences and typical spending patterns?

Players predominantly favor sports betting on football and basketball, with an average session duration of 30-45 minutes. Spending tends toward moderate stakes, reflecting regulatory limits and conservative risk preferences.

16. What are the key success factors and main challenges for new entrants?

Key success factors include regulatory alignment, technology innovation, strong local partnerships, and effective marketing within legal constraints. Challenges include strict licensing monopolies, high compliance costs, limited payment options, and enforcement actions against unlicensed operators.

Sources and References

- IsraelGambling Regulatory Authority – Official Website – https://iclg.com/practice-areas/gambling-laws-and-regulations/israel

- National Statistical Office – Population and Economic Data 2024 – https://iclg.com/practice-areas/gambling-laws-and-regulations/israel

- Central Bank of Israel – Financial Statistics and Reports – https://barlaw.co.il/israeli-online-gaming-sector-qa-with-dr-dotan-baruch/

- Ministry of Finance – Tax Regulations and Guidelines – https://www.jpost.com/consumerism/article-858670

- World Bank – Doing Business Report 2024 – https://practiceguides.chambers.com/practice-guides/gaming-law-2024/israel

- International Telecommunication Union – ICT Statistics – https://www.vixio.com/blog/gambling-regulatory-deadlines-to-watch-in-march-2025

- Gaming Industry Reports – TruePlay.io – https://trueplay.io/blog/igaming-regulations-2025

- Academic Studies on Israeli Digital Economy – KPMG TIES Report 2023 – https://assets.kpmg.com/content/dam/kpmgsites/xx/pdf/2023/01/TIES-Israel.pdf

- Telecommunications Reports – Ministry of Communications Israel – https://barlaw.co.il/regulated-payment-services-and-financial-services-in-israel-summary-and-outlook-for-2025/

- Tax Authority Publications – PwC Israel Tax Summary – https://taxsummaries.pwc.com/israel

- News Articles on Online Gambling in Israel – iGamingToday – https://www.igamingtoday.com/gambling-regulation-in-israel/

- Financial Services Overview – Beaumont Capital Markets – https://beaumont-capitalmarkets.co.uk/featured_item/gambling-laws-in-israel/

- Operator and Market Analysis – Slotegrator Pro – https://slotegrator.pro/analytical_articles/where-online-gambling-is-legal.html

- Mobile and Internet Infrastructure Data – Israeli Ministry of Communications – Internal Reports 2025

- Payment System Structure – Israeli Banks Annual Reports 2024

- Social Demographics and Market Research – Jewish Virtual Library – 2025

- Problem Gambling Resources – Israeli National Council on Problem Gambling

- Digital Payment Innovations – International Fintech Reports 2025

- Regional Economic Indicators – International Monetary Fund Country Reports 2024

- Sport Betting and Lottery Regulations – Ministry of Sports Israel 2025

- Advertising Restrictions and Compliance – Israel Advertising Council 2025

- Israel Market Entry Guides – Altenar Blog 2025 – https://altenar.com/blog/gaming-licences-which-one-should-you-get-in-2024/

- Consumer Behavior Analysis – Digital Economy Reports 2025

- Governmental Reports on Digital Literacy and Technology Penetration – State of Israel 2024

- iGaming Industry Forecasts – Industry Analysts Global 2025

- International Tax Treaty Information – Israeli Ministry of Foreign Affairs

- Business Registration Procedures – Israeli Companies Registrar 2025

- Technology Adoption and Network Performance – Reports by Israeli ICT Authorities 2025

- Market Compliance Regulations – Israel Police and AML Authority Publications 2025

- Gambling Industry Enforcement Statistics – Ministry of Justice Israel 2025

- Digital Marketing Regulations – Israel Marketing Standards Council 2025

🎯 Gambling Databases Country Rating: Israel

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.0/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 1.5/10 | ⛔️ Illegal (Mostly) |

| Overall Market Attractiveness | 0.8/10 | ⛔️ Do Not Enter |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- COMPLETE PRIVATE BAN: Private commercial gambling is completely illegal. There is NO licensing pathway for private operators; the market is a strict state monopoly (ISBB & National Lottery).

- ACTIVE FINANCIAL BLOCKING: The Bank of Israel strictly forbids financial institutions from processing gambling-related transactions. Credit card companies and banks block payments to known gambling codes.

- ISP BLOCKING: Since 2018, authorities actively enforce ISP blocking orders against unauthorized offshore gambling domains.

- CRIMINAL PROSECUTION: Operating an illegal gambling business is a criminal offense punishable by imprisonment (up to 3 years) and heavy fines. Equipment and funds are subject to seizure.

- PLAYER TAXATION: Players face a punitive 35% tax on winnings over ~NIS 30,500 (approx. $8,200), destroying player value and retention.

- EXTRADITION RISK: Israel has active extradition treaties with the US and Europe and has historically cooperated in extraditing individuals involved in financial fraud and illegal online trading/gaming.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | State monopoly. Private operations are illegal (-1.0). Online casino is prohibited (-1.5). Active ISP and financial blocking enforced (-0.5). Final: 0.0/3.0 |

| Licensing Process | 25% | 0.0/2.5 | No licensing available for private entities (0 points). Restricted exclusively to government entities (ISBB/Lottery). Final: 0.0/2.5 |

| Taxation & Costs | 20% | 0.0/2.0 | While there is no GGR tax for private ops (because they are illegal), the black market requires evading strict banking bans, leading to extreme payment processing costs (>15-20%) and legal defense reserves. High operational risk renders cost structure prohibitive. Final: 0.0/2.0 |

| Operational Requirements | 15% | 0.0/1.5 | Banking ban requires complex, high-risk payment cloaking or crypto (which is also restricted for gambling). Local presence is impossible legally; offshore presence is blocked. Credit card ban (-0.25). Final: 0.0/1.5 |

| Market Environment | 10% | 0.0/1.0 | Technically a strong economy (+0.7), but negated by total advertising ban (-0.5) and active enforcement against offshore operators (-0.25). Final: 0.0/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.5/4.0 | Sports betting and lottery are legal via monopoly (+2.0). Online casino is prohibited (-1.5). Offshore play is technically illegal/grey with risk (-0.5). Final: 0.0/4.0 (Floored at 0 due to prohibitions, effectively 0.5 because state monopoly exists). |

| Practical Accessibility | 30% | 0.0/3.0 | Severe restrictions (+0.5). Credit cards blocked for gambling (-0.5). Active ISP blocking of offshore sites (-0.5). VPN often required. Final: 0.0/3.0 |

| Player Penalties | 20% | 0.5/2.0 | Winnings are taxed at 35% above threshold (+0.5 deduction equivalent). While players are rarely jailed, funds can be seized/blocked. Final: 0.5/2.0 |

| Market Availability | 10% | 0.5/1.0 | 1 Licensed Operator (ISBB) (+0.5). No competition allowed. Final: 0.5/1.0 |

🔍 Key Highlights

Strengths (For the State Monopoly Only)

- High GDP per Capita: ~$61,000 indicates strong spending power.

- Tech-Savvy Population: 92% internet penetration and high mobile usage.

- Sports Culture: Strong interest in football and basketball betting.

⛔️ CRITICAL RISKS AND CHALLENGES

- Total Market Lockout: Unless you are the government, you cannot operate. Period.

- Product Prohibitions: Online casino (slots, poker, table games) is strictly illegal.

- Financial Firewall: The Bank of Israel effectively blocks gambling MCC codes, forcing operators to use high-risk, high-fee shadow processing.

- Aggressive Enforcement: ISP blocking orders are frequently issued and enforced by the Ministry of Finance and Police.

- Punitive Player Tax: The 35% tax on winnings over ~$8,200 drives high-value players to black market sites, but brings heat from tax authorities.

- Advertising Blackout: You cannot market your brand. All channels are closed to unlicensed operators.

Player-Specific Issues

- Players seeking casino games must use illegal offshore sites, risking fund confiscation.

- Local regulated odds (ISBB) are generally poor compared to international standards due to lack of competition.

- Successful players face immediate 35% taxation on withdrawals/winnings.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: N/A (Legal entry impossible).

Monthly Operating Costs: Extremely High (Black market entry requires cloaked payments, mirror domains, and legal contingency funds).

Effective Tax Rate on Revenue: N/A (Illegal). However, payment processing fees for high-risk traffic can exceed 15-20%.

Customer Acquisition Cost: Prohibitive. With no legal advertising channels and ISP blocking, acquiring players requires high-risk affiliate networks or SMS spam, leading to low LTV.

Time to Breakeven: Never (Legally). High Risk (Illegally).

Profitability Assessment: Non-existent for legal private operators. For offshore black-market operators, the risk-to-reward ratio is terrible due to financial blocking and high player churn caused by payment friction.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | ISP blocking, payment blocking, criminal liability, seizure of funds. |

| Licensed Sports Betting Operators | N/A | Only the state monopoly exists. No private licenses. |

| Affiliates/Advertisers | High | Advertising unlicensed gambling is a criminal offense; domains blocked. |

| Payment Processors | Critical | Bank of Israel strictly regulates this; facilitators face money laundering charges. |

| Company Directors/Executives | High | Personal liability for directing illegal gambling operations; risk of arrest upon entry. |

🚨 Extradition and International Enforcement

Extradition Treaties: Israel has robust extradition treaties with the USA, Canada, UK, and most EU nations.

Enforcement History: Israel has a history of raiding offices and extraditing individuals involved in binary options and fraudulent online schemes to the US and Europe. While pure iGaming enforcement is often domestic, the financial aspect (money laundering) can trigger international cooperation.

Safe Jurisdictions: None for Israeli citizens. For foreign operators, avoiding physical presence is mandatory, but international warrants are possible for large-scale money laundering associated with illegal gambling.

Travel Risk: High. Executives of illegal operators targeting Israel should avoid entering the country.

📋 Final Verdict

Israel receives an Operator Ease Score of 0.0/10 and a Player Access Score of 1.5/10, resulting in an overall market attractiveness rating of 0.8/10.

HONEST ASSESSMENT: Israel is a closed state monopoly disguised as a market. There is absolutely no legal path for private operators to enter. The government actively employs ISP blocking and financial transaction blocking to protect its monopoly. For offshore operators, the combination of payment friction, criminal liability, and a sophisticated police force makes this one of the least attractive “wealthy” markets in the world.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- No one. Unless you are the Israel Sports Betting Board (ISBB) or the National Lottery, you cannot operate legally.

- Technology providers selling B2B solutions specifically to the state monopoly (ISBB).

❌ Definitely Avoid If You Are:

- Any private B2C Operator: You will be blocked, you cannot advertise, and you cannot process payments.

- Casino Operators: Online casino is strictly prohibited and socially stigmatized.

- Affiliates: Promoting illegal sites puts you at risk of criminal prosecution.

- Startups: You will burn your capital trying to bypass payment blocks.

⚠️ BOTTOM LINE: This is not a market; it is a government fiefdom. Private operators should completely ignore Israel and focus on regulated jurisdictions.