Italy presents a mature and highly regulated iGaming market offering substantial opportunities due to its large population and high internet penetration. The country enforces a robust regulatory framework ensuring player protection and market integrity. This analysis covers key regulatory aspects and license requirements essential for market entry.

| Metric | Value |

|---|---|

| Gambling Legal Status | Fully regulated with licensed land-based and online gambling |

| Regulatory Authority | Agenzia delle Dogane e dei Monopoli (ADM) |

| Population | ~60 million |

| Median Age | 47 years |

| GDP | ~€2 trillion |

| GDP per Capita | ~€33,000 |

| Internet Penetration | 82% |

| Mobile Penetration | 135% (includes multiple device ownership) |

| Licensed Operators | ~150 online licensed operators |

| License Application Fee | €50,000 |

| License Renewal Fee | €20,000 annually |

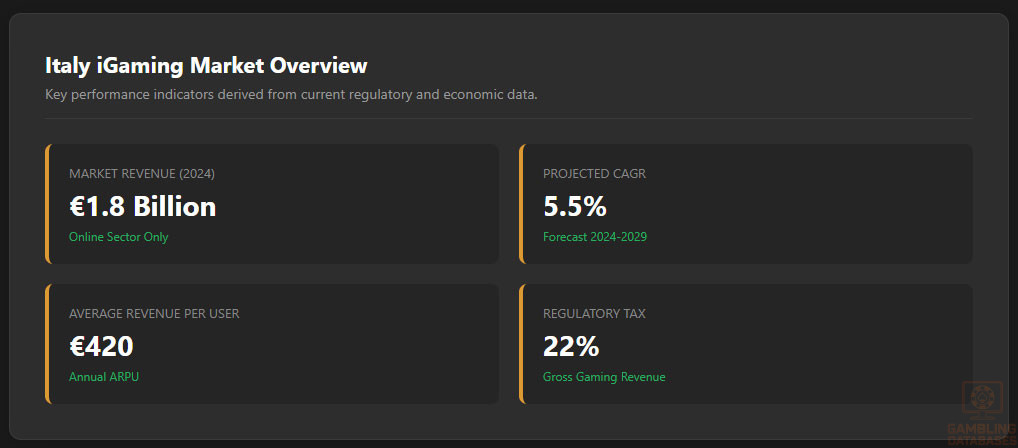

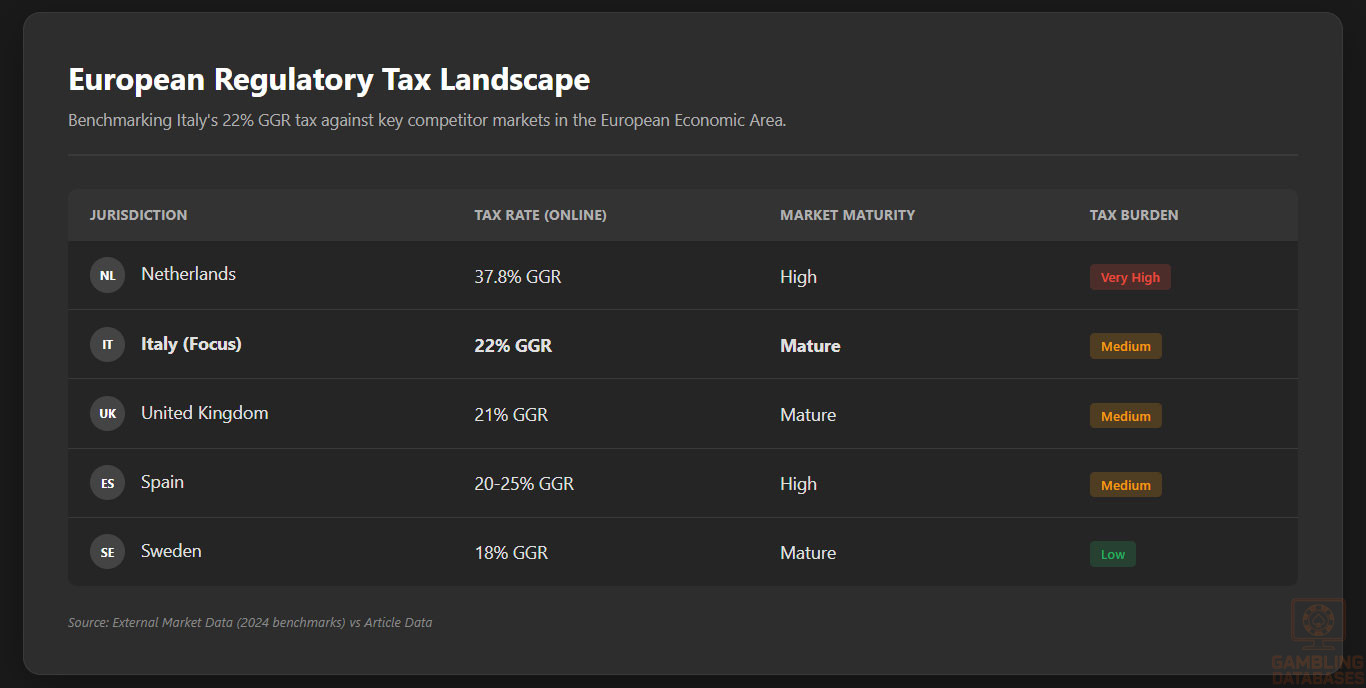

| Gross Gaming Revenue (GGR) Tax Rate | 22% on online gaming |

| Corporate Tax Rate | 24% |

| Market Size (Revenue) | ~€1.8 billion (2024 online gambling) |

| Market Growth (CAGR) | 5.5% (2024-2029 forecast) |

| Average Revenue Per User (ARPU) | €420 |

| Problem Gambling Prevalence | ~1.5% adult population |

| Advertising Restrictions | Strict with content and time limitations |

| KYC/AML Requirements | Comprehensive, including ID and proof of residence |

| Responsible Gambling Measures | Mandatory self-exclusion and deposit limits |

| Payment Methods | Credit cards, e-wallets, bank transfers, prepaid cards, Postepay |

| Market Entry Timeline | 6-12 months |

| Physical Presence Required | No mandatory local office, but Italian payment gateway required |

| Foreign Ownership | Allowed with restrictions |

| Compliance Reporting Frequency | Monthly submissions |

| Enforcement Penalties | Fines, license suspension, criminal sanctions |

| Land-Based Casino Availability | Casino di Venezia, others |

| Sports Betting Popularity | High with licensed operators |

| Slot Machine Regulations | Strict with location and technical controls |

| RNG Certification | Mandatory for all games |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Italy maintains a comprehensive regulatory framework for all gambling categories, including land-based casinos, sports betting, slot machines, lotteries, and online gaming. The primary regulatory authority is Agenzia delle Dogane e dei Monopoli (ADM), responsible for licensing and market supervision. Land-based gambling operations are well-established with strict controls on location, operating hours, and game integrity. Online gambling is fully regulated with specific licensing for operators, mandatory player protection measures, and rigorous compliance monitoring.

The Italian online gambling market is characterized by a structured licensing regime that mandates operators obtain an ADM license to legally offer services. Prohibited activities include unlicensed betting, unauthorized poker games, and unregulated skill games. The framework enforces strong KYC/AML procedures, player deposit limits, and mandatory self-exclusion tools to protect consumers. Regulatory oversight includes frequent audits and an integrated monitoring system to ensure fairness and compliance.

The market includes approximately 150 licensed online operators, ranging from international gaming giants to local operators. Market concentration is moderate with leading operators commanding a significant share, but room remains for niche and innovative market entrants. Competitive dynamics focus on platform quality, game variety, and compliance reliability. Entry strategies often involve partnerships with local payment processors and targeted marketing tailored to Italian player preferences.

Licensing Framework and Requirements

The licensing process is administered by ADM, requiring detailed submissions including corporate documents, financial disclosures, and technical certifications. The application fee is €50,000, with annual renewal fees of €20,000.

Typical processing time ranges from 6 to 12 months depending on completeness and regulatory workload. Operators must meet strict financial solvency criteria and demonstrate robust technical infrastructure meeting ADM standards.

The licensing framework requires submission of multiple documents:

- Corporate registration certificate and articles of incorporation

- Financial statements audited for the past three years

- Detailed business plan and market strategy

- Technical documentation including RNG certification

- Anti-money laundering compliance policies

- Criminal background checks for directors and beneficial owners

- Proof of minimum capital deposit in a licensed Italian bank

- Responsible gaming and player protection protocols

While no mandatory physical office is required in Italy, operators must use Italian payment gateways and maintain local customer service facilities. Foreign ownership is permitted but subject to regulatory scrutiny ensuring transparency and compliance. Operational mandates include maintaining records within Italian jurisdiction and cooperating fully with ADM audits.

Operators must comply with the following operational requirements:

- Use of Italian-based payment processing

- Provision of Italian-language customer support

- Data storage compliant with EU GDPR

- Compliance with responsible gambling regulations

- Regular submission of compliance reports to ADM

Compliance Obligations and Monitoring

Player protection in Italy is enforced through multiple mandatory measures:

- Mandatory age verification (18+)

- Full KYC including ID and residence proof

- Real-time monitoring of suspicious transactions

- Self-exclusion programs

- Deposit limits and loss limits

- Advertising restrictions to protect vulnerable groups

Operators must monitor all financial transactions for AML compliance, reporting suspicious activities to authorities. Monthly financial and operational reports are submitted to ADM including revenue, tax payments, and compliance status. Audits are conducted periodically to ensure adherence to gaming and financial regulations, with penalties for non-compliance.

The sequence of financial reporting is as follows:

- Collection of transactional data

- Analysis for suspicious activities

- Reporting to ADM via official channels

- Internal compliance review and audit preparation

- Implementation of corrective actions if needed

Taxation Structure and Financial Obligations

Players are not taxed directly on gambling winnings as tax obligations are assumed by operators through withholding. Winnings above certain thresholds are subject to automatic reporting to tax authorities. Taxation largely focuses on operators rather than individual gamblers.

| Game Type | Tax Rate on GGR |

|---|---|

| Online Sports Betting | 22% |

| Online Casino Games | 22% |

| Online Poker | 22% |

| Land-Based Casinos | 20% |

| Lotteries | 15% |

Italy’s gambling market shows consistent growth with total wagers exceeding €15 billion annually. Online gambling revenue reached approximately €1.8 billion in 2024, driven by increased mobile device usage and improved payment infrastructures. Tax revenues from gambling represent a significant contribution to public finances, with stable year-over-year growth supported by mature regulatory oversight.

Advertising and Marketing Restrictions

Advertising in the Italian iGaming industry faces strict content and time restrictions:

- Restrictions on TV and radio gambling ads

- No ads targeting minors or vulnerable groups

- Limited promotional offers with clear terms

- Time restrictions on advertising slots

- Mandatory responsible gambling messaging

Recent Regulatory Changes and Their Impact

- 2023: Introduction of unified licensing system reducing application times

- 2023: Increased GGR tax from 15% to 22% for online operators

- 2024: Stricter AML and KYC enforcement

- 2025: Expanded restrictions on gambling advertising

These changes have increased operational costs for operators due to higher licensing fees and tax rates, while improving overall market transparency and consumer protection. Strategies have shifted towards compliance optimization and enhanced player trust initiatives.

Enforcement Mechanisms and Penalties

Enforcement is stringent, involving a range of penalties:

- Fines based on violation severity

- License suspension or revocation

- Criminal prosecution for illegal operators

- Confiscation of illegal proceeds

- Public blacklisting of non-compliant entities

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

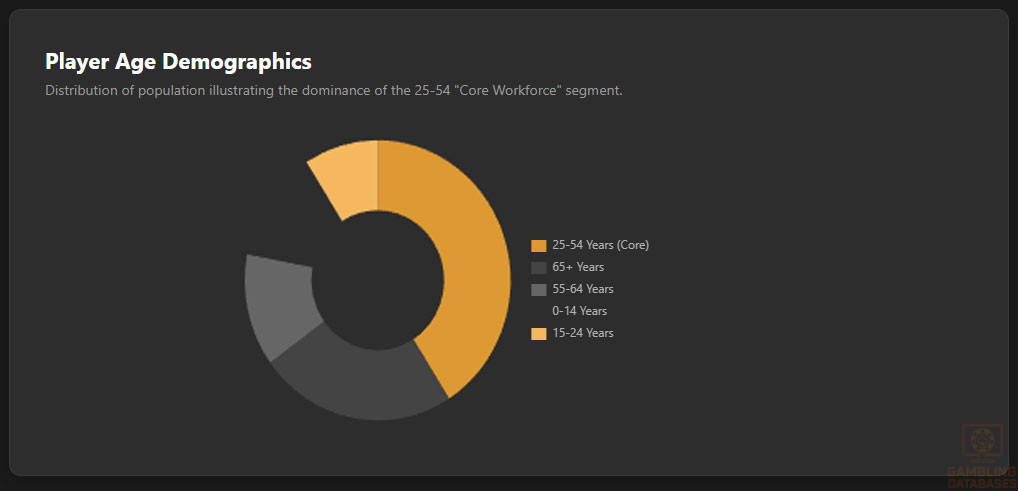

Italy’s population stands at approximately 60 million, with a median age of 47 years, reflecting one of Europe’s older populations. The gender ratio is relatively balanced, with a slight female majority. Age distribution highlights a significant portion of the population aged 25-54, which constitutes the main economic and consumer base.

Urbanization is notable, with about 70% of the population residing in urban areas. Rural regions are characterized by lower population density and limited gambling venue access, while metropolitan hubs display concentrated consumer activity and connectivity.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 13% |

| 15-24 years | 9% |

| 25-54 years | 41% |

| 55-64 years | 13% |

| 65+ years | 24% |

The geographic distribution centers around northern and central Italy’s economic powerhouses, while southern regions exhibit lower GDP per capita but rising digital adoption.

Internet access is highest in urban areas, correlating strongly with the location of both physical gambling venues and online player concentrations.

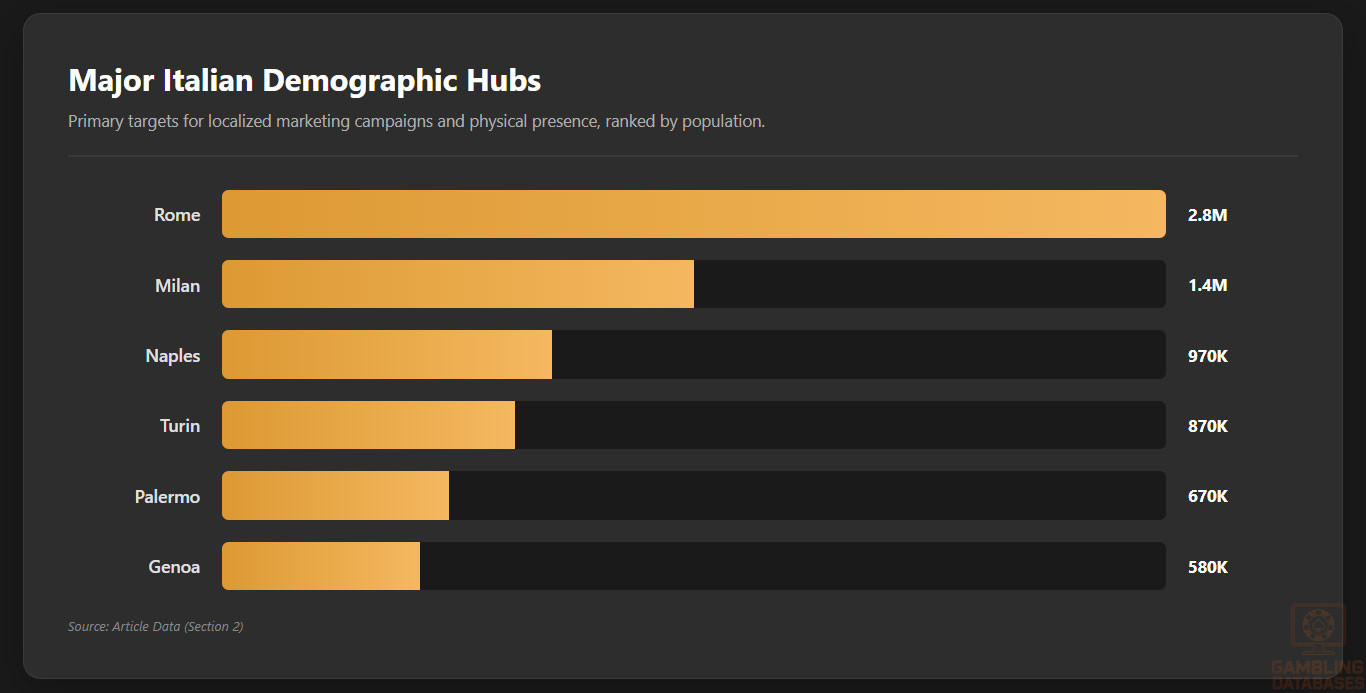

- Rome: population ~2.8 million

- Milan: population ~1.4 million

- Naples: population ~970,000

- Turin: population ~870,000

- Palermo: population ~670,000

- Genoa: population ~580,000

Economic Indicators and Consumer Spending Power

Italy’s GDP is near €2 trillion, experiencing modest growth with a forecasted CAGR of about 1.2% over the next five years. The economy is led by the service sector contributing approximately 64% of GDP, followed by industry at 31% and agriculture at 5%. Consumer spending remains a key economic driver with an increasing shift toward digital and experiential consumption.

Average household income is approximately €32,000, with median income slightly lower due to wealth disparities concentrated in northern regions. Disposable income trends show moderate growth but are offset by high regional taxation and living costs, influencing spending on leisure and gaming entertainment.

| Indicator | Value |

|---|---|

| GDP | €2 trillion |

| GDP Growth Forecast | 1.2% CAGR |

| Service Sector Contribution | 64% |

| Industry Sector Contribution | 31% |

| Agriculture Sector Contribution | 5% |

| Average Household Income | €32,000 |

| Median Income | €27,500 |

| Unemployment Rate | 8.1% |

The iGaming market growth is supported by a user base exhibiting moderate to high disposable income in the 25-44 age bracket.

Market size projections estimate a revenue increase driven by rising internet penetration and the adoption of mobile gambling platforms.

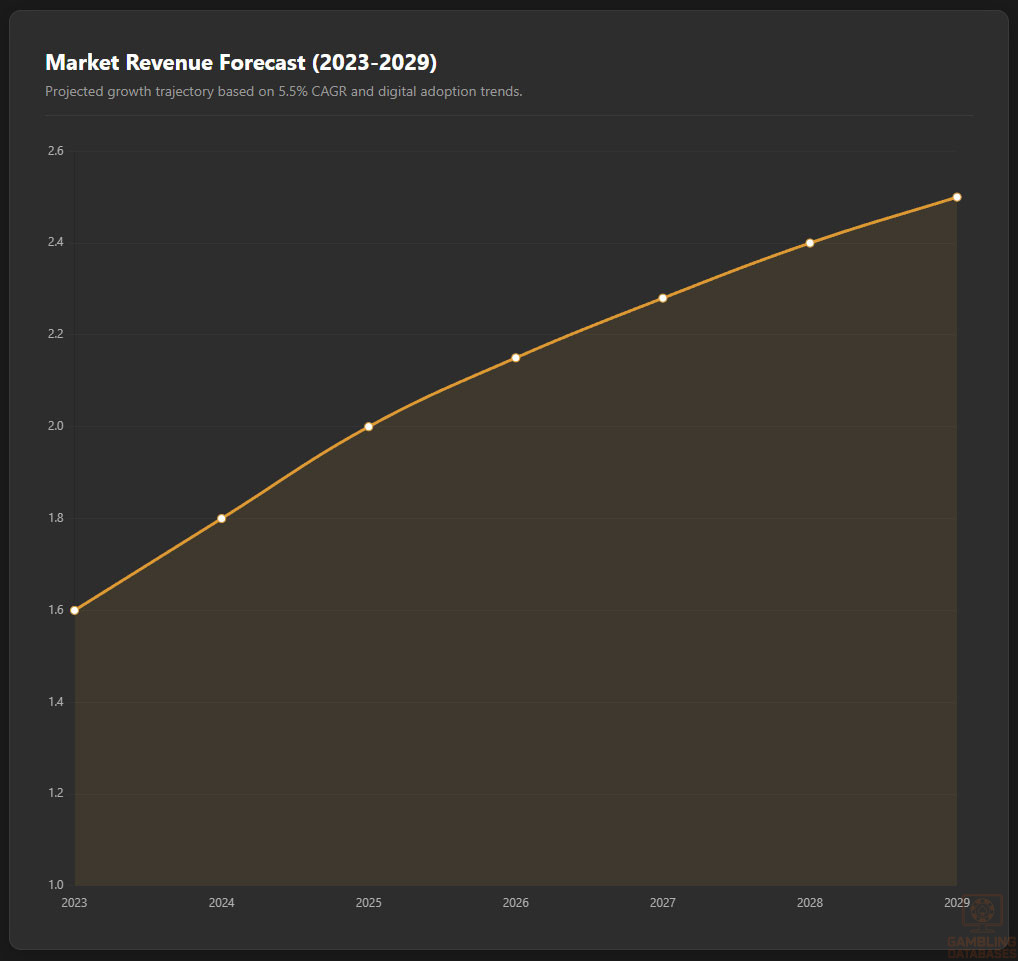

| Year | Revenue (€ billion) | User Base (million) | ARPU (€) |

|---|---|---|---|

| 2023 | 1.6 | 3.6 | 410 |

| 2024 | 1.8 | 3.9 | 420 |

| 2025 (forecast) | 2.0 | 4.2 | 430 |

| 2029 (forecast) | 2.5 | 4.9 | 460 |

Education, Skills, and Digital Literacy

Italy boasts a high literacy rate exceeding 99%, with increasing tertiary education enrollment, particularly in northern and central regions. Digital literacy is advancing rapidly, showing over 80% of adults proficient in internet use and digital tools.

Workforce skills favor service and technology sectors, contributing to growing e-commerce and digital entertainment adoption. Younger populations demonstrate greater comfort with mobile and online platforms, enhancing opportunities for digital gambling engagement.

Cultural and Social Factors

Communication and Language

Italian is the predominant language used across digital platforms and in customer interactions, with regional dialects influencing cultural expressions. English proficiency is moderate, especially among younger and urban populations, facilitating access to international brands.

- Italian (official and dominant language)

- English (widely used in business and younger demographics)

- Neapolitan (regional dialect)

- Sicilian (regional dialect)

- Lombard (regional dialect)

Cultural Attitudes

Gambling is culturally accepted in Italy, seen as a mainstream leisure activity, though often approached with caution due to strong family values and regional religious influences. Foreign gambling brands face moderate resistance related to trust and local market knowledge but gain acceptance through localized offerings and compliance with regulations.

Entertainment preferences lean towards sports betting, online casino games, and lotteries, with social gambling gaining traction among younger demographics. Community and familial aspects influence gambling behavior, often favoring responsible participation.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated at 1.5% of the adult population, with at-risk groups including younger males and lower-income individuals. The government, alongside industry stakeholders, implements comprehensive response measures supporting prevention and rehabilitation.

- State-funded counseling and support services

- Mandatory responsible gambling contributions from operators

- Public awareness campaigns targeting youth

- Self-exclusion programs facilitated by ADM

- Ongoing research and data collection on gambling behavior

Social responsibility frameworks mandate operators to provide transparency, limit incentives for excessive gambling, and support socially responsible marketing.

Political Structure and Governance

Italy operates a parliamentary representative democratic republic system with stable governance frameworks supporting regulatory consistency in sectors including gaming. Political stability fosters a predictable business environment, though bureaucratic processes may extend licensing timelines.

The country maintains active international relations within the EU and global economic institutions, aligning domestic regulations with EU directives and compliance standards enhancing cross-border cooperation in gaming oversight.

Technology Adoption and Digital Behavior

Internet and Digital Usage

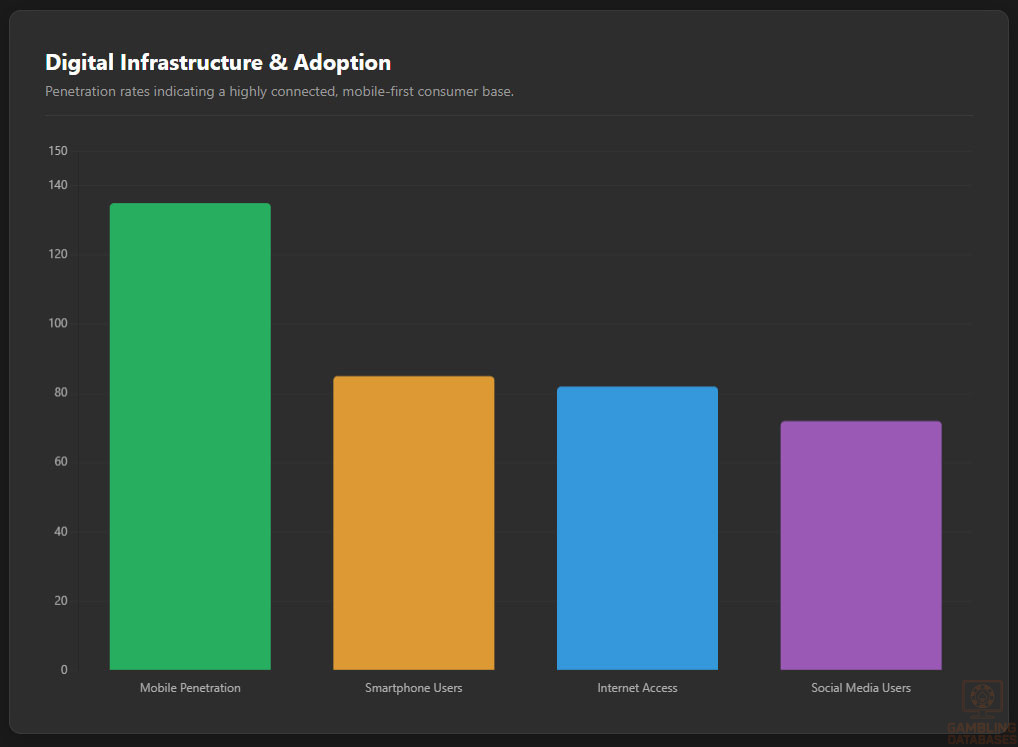

Internet penetration reaches 82% of the population, with daily usage averaging over 6 hours across devices. Mobile adoption exceeds 135%, reflecting multiple device ownership per user.

Social media engagement remains high, with platforms dominating communication and marketing channels.

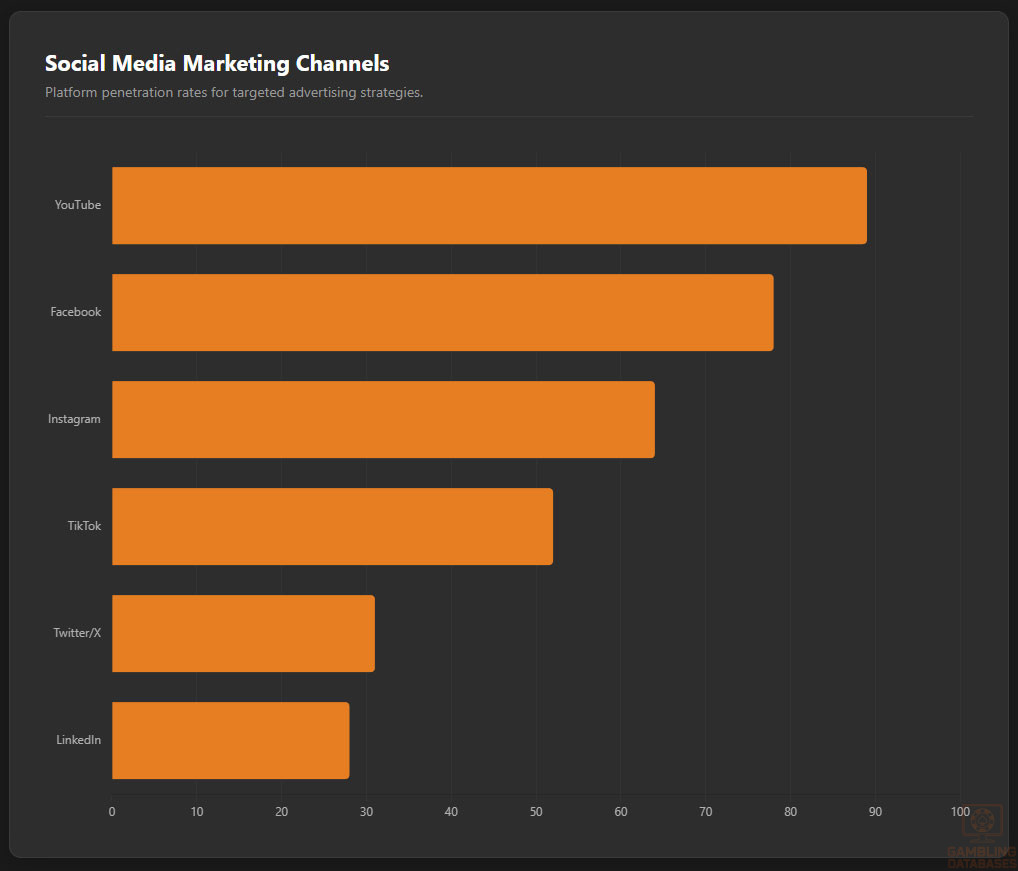

- Facebook: 78% penetration, daily use approximately 2.3 hours

- Instagram: 64% penetration, strong among 18-34 age group

- YouTube: 89% penetration, average watch time 45 minutes daily

- TikTok: 52% penetration, fastest growth among under-25 users

- Twitter: 31% penetration, focused on news and current events

- LinkedIn: 28% penetration, business and professional networking

Digital Payment Behavior

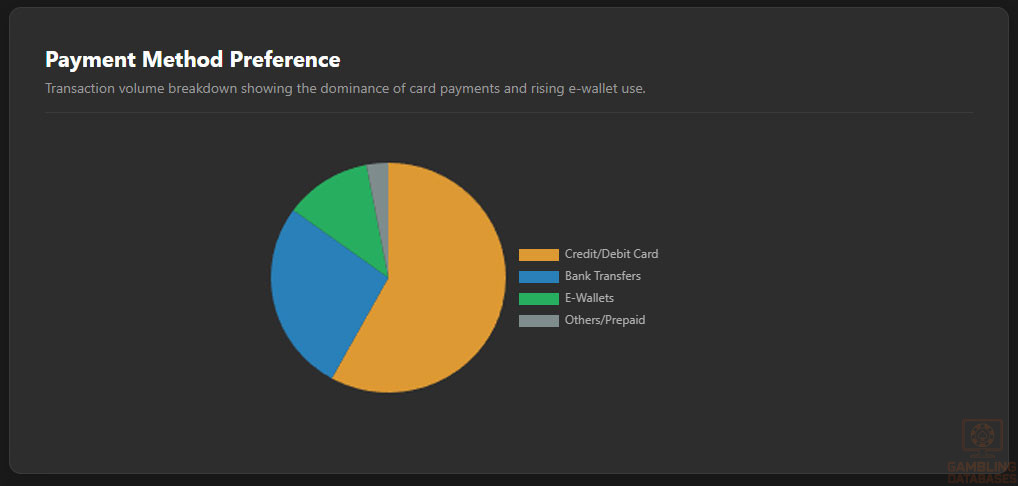

Digital payment adoption is increasingly diversified, led by credit and debit cards, followed by e-wallets and bank transfers. Cryptocurrency use remains marginal but is growing among niche consumer segments. Online transactions in iGaming favor secure, rapid, and regulated payment channels.

- Credit and debit cards: 58% of online transactions

- Bank transfers: 27% of payment volume

- E-wallets (PayPal, Skrill, Neteller): 12% and growing

- Prepaid cards (Postepay): Preferred for security and anonymity

- Cryptocurrency: Niche adoption, under 1% market share

Gaming and Gambling Preferences

Current Market Participation

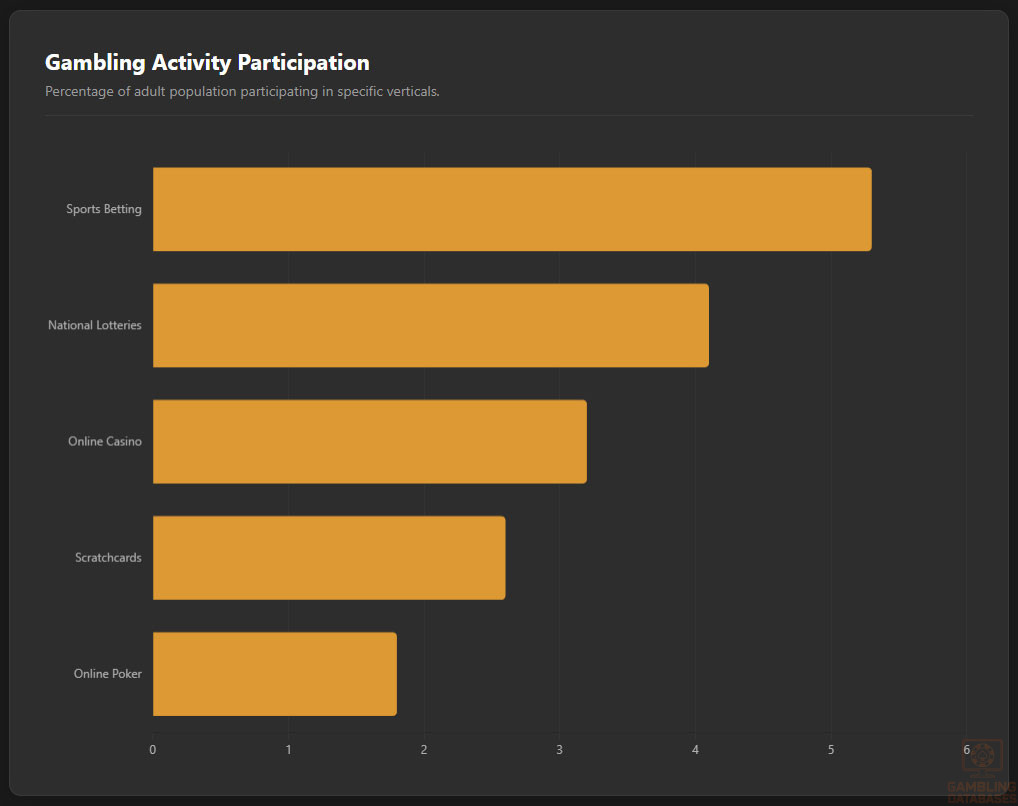

Participation in gambling activities spans approximately 6.5 million adults, representing over 10% of Italy’s adult population. Sports betting dominates popular participation, followed by lotteries and casino gaming, with increasing preference for online mobile platforms.

| Rank | Activity | Participation % |

|---|---|---|

| 1 | Sports Betting | 5.3% |

| 2 | National and Instant Lotteries | 4.1% |

| 3 | Online Casino Games | 3.2% |

| 4 | Scratchcards | 2.6% |

| 5 | Online Poker | 1.8% |

Consumer Behavior Patterns

Italian consumers exhibit preferences for mobile-first gambling, with peak activity occurring during evening hours and major sports events. Average session lengths range from 15 to 45 minutes, favoring quick bets and casino-style play. Retention is driven by bonuses, local promotions, and culturally tailored content.

Spending behavior correlates positively with disposable income and internet accessibility, with urban and northern regions showing higher ARPU and engagement. Multi-channel operators integrating land-based and online offerings enjoy competitive advantages through consumer loyalty and cross-platform promotions.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Italy exhibits strong digital connectivity with internet penetration at approximately 82%, combining both fixed broadband and mobile internet access. Broadband subscriptions are widespread in urban centers, while mobile internet coverage dominates in rural and less accessible areas. Average fixed broadband download speeds exceed 100 Mbps, with upload speeds steadily improving due to fiber optic network investments.

Network reliability is solid, supported by continuous infrastructure enhancements funded by both public initiatives and private sector investments. Broadband infrastructure expansion particularly targets underserved southern regions aiming to bridge the digital divide and enable nationwide e-commerce and online gaming access.

5G and Future Technology Deployment

Italy is advancing rapidly in 5G deployment, with commercial networks covering around 60% of the population as of 2025. Leading mobile operators have accelerated rollout, with complete urban coverage expected by 2027. Planned investments involve expansion into suburban and rural areas to support high-speed mobile data and low latency services essential for enhanced gaming experiences.

The 5G network landscape includes comprehensive spectrum allocation and competition among multiple operators, fostering innovation and affordable data plans. As 5G matures, augmented reality and cloud gaming could emerge as growth drivers within the Italian iGaming ecosystem.

Mobile Technology Ecosystem

The mobile network infrastructure includes several key players competing for market share with reliable nationwide coverage. Data pricing is competitive, incentivizing extensive mobile data use for gaming and streaming services.

- TIM (Telecom Italia) – Largest coverage and market leader

- Vodafone Italy – Strong urban presence and innovation focus

- Wind Tre – High user base concentrated in large cities

- Iliad – Disruptor with low-cost plans and growing coverage

- Fastweb Mobile – Niche player with integrated services

Smartphone adoption exceeds 85%, led by brands like Apple and Samsung. Consumers show strong preference for mid-to-high range devices supporting advanced graphics and secure transactions. Mobile gaming dominates digital engagement patterns, with a preference for Android devices slightly surpassing iOS.

Financial Services and Payment Infrastructure

Italy’s banking sector features both traditional and digital-first institutions, supporting widespread financial inclusion and digital payment adoption. Account penetration is high, with increasing use of online and mobile banking platforms enhancing transaction efficiency and security critical for the gaming industry.

- UniCredit – Italy’s largest bank with comprehensive digital services

- Intesa Sanpaolo – Extensive retail network and innovation in fintech

- Banca Monte dei Paschi di Siena – Historical bank focusing on SME lending

- Banca Nazionale del Lavoro (BNL) – Strong corporate banking presence

- Credito Emiliano (Credem) – Regional player with growing digital portfolio

Payment processing options align with European standards, encompassing card payments, e-wallets, instant bank transfers, and prepaid cards. The regulatory framework emphasizes secure payment gateways certified under EU directives to ensure consumer protection.

- Visa and Mastercard credit/debit cards widely supported

- PayPal, Skrill, Neteller as preferred e-wallets

- Postepay prepaid cards popular among cautious spenders

- SEPA bank transfers for secure and regulated transactions

- Apple Pay and Google Pay as mobile wallet solutions

E-commerce and Digital Economy

Italy’s e-commerce market grew to an estimated €55 billion in 2024, driven by increased consumer trust and mobile-first shopping behaviors. Online retail penetration varies regionally, with northern areas leading in digital purchases. Digital services extend beyond retail, including entertainment, financial services, and digital content consumption, all fostering an ecosystem conducive to online gambling expansion.

Consumer trust in secure payment methods and customer service responsiveness is critical, with established platforms leveraging integrated fraud prevention and data privacy compliance to maintain competitive advantages.

Business Environment and Regulatory Framework

Italy ranks moderately high on the World Bank’s ease of doing business index, benefiting from streamlined company registration processes and robust legal protections. However, bureaucratic delays and complex tax regulations can increase operational burdens.

Foreign investment policies encourage international entrants, though compliance with strict AML and GDPR regulations remains mandatory. Operational costs are influenced by regional differences in labor, rental, and utility expenses, with Milan and Rome representing the highest cost centers.

- Preparation and notarization of legal incorporation documents

- Submission to the Italian Companies Registry (Registro delle Imprese)

- Tax registration with Agenzia delle Entrate to obtain a tax ID number

- Opening bank accounts and depositing required capital

- Notification and registration with social security and labor authorities

Corporate Structure and Registration

Common entity types include the limited liability company (SRL), joint-stock company (SpA), and branch office of a foreign company. The SRL is preferred by small to medium businesses due to flexible capital requirements and simpler governance.

Entity choice impacts operational flexibility, tax obligations, and regulatory compliance. Most iGaming entrants prefer SRL or branch structures for market entry, balancing cost and administrative complexity.

Registration timelines range from 2 to 6 weeks depending on document completeness and procedural backlog. Compliance requires adherence to anti-money laundering policies and data protection regulations.

- Certificate of incorporation and memorandum of association

- Tax identification number application

- Fiscal domicile declaration

- Identification documents of directors and shareholders

- Proof of registered office address in Italy

- Bank statements confirming capital deposit

- Registration with social security and insurance authorities

Taxation Framework

Corporate income tax (IRES) is set at a standard rate of 24%, complemented by a regional production tax (IRAP) averaging 3.9%. Tax holidays and incentives are available in designated special economic zones focusing on innovation and export.

Italy maintains double taxation treaties with numerous countries facilitating cross-border business operations.

- Germany

- France

- United Kingdom

- United States

- Spain

- Netherlands

- Switzerland

Personal income tax employs progressive rates up to 43% with mandatory social security contributions. Tax residency rules require individuals to comply with local tax regulations if residing over 183 days annually.

Market Entry Considerations

Recommended strategies emphasize partnerships with local payment processors, adoption of ADM-compliant platforms, and culturally localized marketing. Leveraging mobile-first technology and broad content portfolios enhances competitiveness in this sophisticated market.

- Joint ventures with existing Italian operators

- Acquisition of smaller local license holders

- White-label agreements with established platform providers

- Direct licensing with ADM supported by local legal counsel

- Investment in responsible gambling and player protection initiatives

Typical initial investments cover licensing fees, technology integration, marketing, and capital reserves, with overall time to market averaging 6 to 12 months depending on regulatory and operational readiness.

- License application and renewal fees

- IT infrastructure deployment and compliance tools

- Marketing and customer acquisition expenses

- Local staffing and customer support setup

- Legal and regulatory consultancy fees

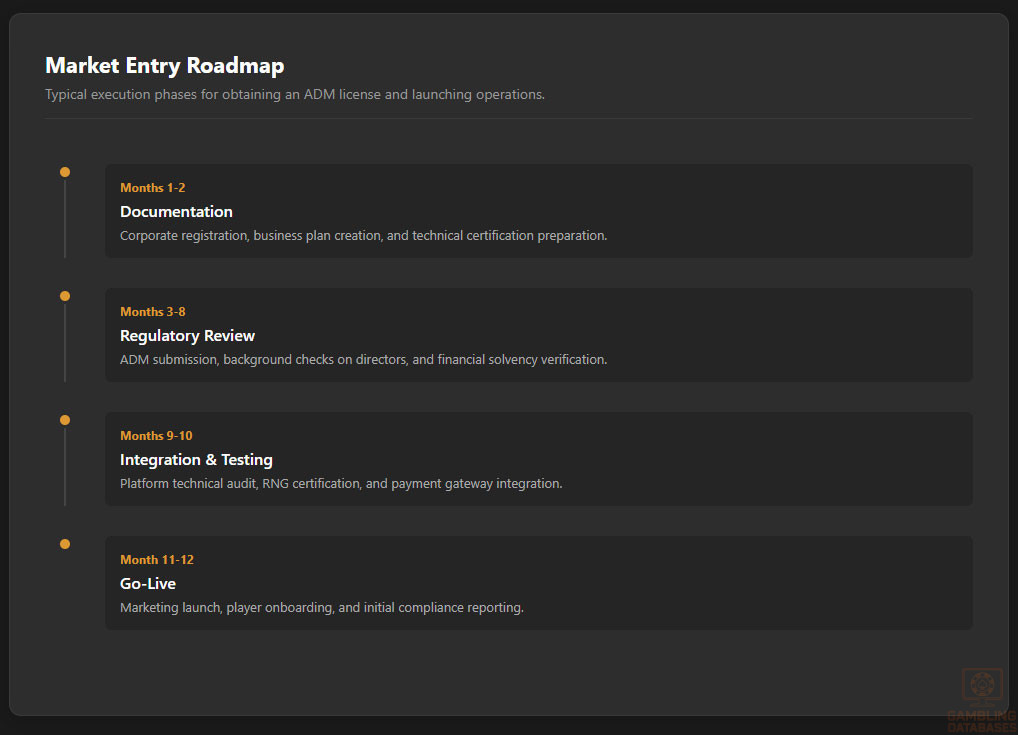

| Phase | Duration |

|---|---|

| Document preparation and submission | 1-2 months |

| Regulatory review and background checks | 3-6 months |

| Platform integration and testing | 1-2 months |

| Marketing launch and customer onboarding | 1 month |

Key success factors include robust compliance culture, technology agility, strong local partnerships, and attentive player experience management. Likewise, operational challenges stem from complex regulatory frameworks, competitive market saturation, and fluctuating tax burdens.

- Adherence to stringent regulatory requirements

- Implementation of leading-edge gaming platforms

- Understanding Italian consumer preferences

- Effective multi-channel marketing strategies

- Efficient risk and compliance management

Exit considerations require careful review of license transferability, market valuation, and regulatory approval processes. Liquidity in the Italian iGaming sector is moderate, reflecting a stable yet competitive market environment.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Italy?

Yes, online gambling is legal and fully regulated in Italy under the supervision of Agenzia delle Dogane e dei Monopoli (ADM). Licensed operators can offer various gambling services including sports betting, casino games, poker, and lotteries. Unlicensed gambling activities are prohibited and subject to enforcement actions.

2. What types of gambling licenses are available and what do they cover?

The primary license categories include licenses for sports betting, online casino gaming, poker, lotteries, and skill games. Operators must obtain specific ADM licenses corresponding to the games offered. Ancillary licenses cover payment processing and marketing activities tied to gaming services.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees stand at approximately €50,000, with an annual renewal fee of €20,000. The approval process generally takes between 6 to 12 months, depending on documentation completeness and regulatory workload.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible to obtain an Italian gambling license but must comply with all ADM regulatory requirements, including transparency, financial solvency, and provision of Italian-language customer support. While foreign ownership is permitted, operators must maintain robust compliance programs and use Italian payment gateways.

5. What are the tax obligations for iGaming operators?

Operators are subject to a gross gaming revenue (GGR) tax of 22% on online betting and casino games. Additional corporate income tax of 24% applies on profits, alongside regional business taxes. Mandatory license fees and reporting obligations supplement the tax structure.

6. Are gambling winnings taxed for players?

Players do not pay direct taxes on gambling winnings as operators withhold and remit applicable taxes. Reporting thresholds exist for large wins, but individual players are generally exempt from filing gambling-related income separately.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational expenses include licensing fees, technology platform licensing or development, marketing and customer acquisition, regulatory compliance, local staffing, and payment processing costs. Infrastructure and compliance-related expenditures constitute significant portions of budgets.

8. What is the expected ROI timeline for entering this market?

Operators typically anticipate break-even and ROI within 18 to 36 months post-launch, influenced by market entry strategy, marketing effectiveness, and operational efficiency. Established partnerships and localized strategies accelerate profitability.

9. What are the local presence requirements for operators?

While physical offices in Italy are not mandatory, operators must host Italian payment gateways and offer customer service in Italian. Compliance reporting and data storage within Italian or EU jurisdiction are required to satisfy regulatory terms.

10. What payment methods are available and recommended?

Recommended methods include credit/debit cards (Visa, Mastercard), widely-used e-wallets (PayPal, Skrill), prepaid cards like Postepay, SEPA bank transfers, and mobile wallets (Apple Pay, Google Pay). Payment reliability and regulatory compliance are critical selection factors.

11. What are the advertising and marketing restrictions?

Advertising is tightly regulated to prevent targeting minors and vulnerable groups. Restrictions include limitations on advertising times (banned during certain hours), mandatory responsible gambling messages, and prohibitions on misleading claims. Sponsors and promotions must comply with ADM guidelines.

12. What responsible gambling measures are mandatory?

Operators must enforce measures including age verification (18+), self-exclusion programs, deposit and loss limits, player activity monitoring, and provision of clear information on gambling risks. ADM requires operators to demonstrate ongoing support for responsible gambling policies.

13. How large is the iGaming market and what is the growth potential?

The Italian iGaming market generated around €1.8 billion in online gambling revenue in 2024, with an expected CAGR of approximately 5.5% through 2029. Mobile gaming and diversified offerings suggest sustained expansion opportunities.

14. Who are the main competitors and what is their market share?

The market is served by a mix of large international operators and established domestic brands. Leading providers capture significant share through diversified product portfolios and strong compliance records, while smaller niche operators find success focusing on market segments like poker or sports betting.

15. What are the player preferences and typical spending patterns?

Players show strong preferences for sports betting and lottery products, followed by online casino and poker games. Spending correlates with disposable income and tends to spike around major sports events. Users favor mobile access and value seamless payment options and localized content.

16. What are the key success factors and main challenges for new entrants?

Success hinges on regulatory compliance, local market knowledge, technology reliability, and targeted marketing. Key challenges include navigating complex licensing processes, sustaining competitive differentiation, and managing operational costs in a tax-intensive environment.

Sources and References

- Italy Gambling Regulatory Authority – Agenzia delle Dogane e dei Monopoli (ADM) Official Website – https://adm.gov.it

- Italian National Institute of Statistics (ISTAT) – Demographic and Economic Data 2024 – https://istat.it

- Bank of Italy – Financial and Payment Systems Reports 2024 – https://bancaditalia.it

- Ministry of Finance Italy – Taxation and Regulatory Updates – https://finanze.gov.it

- World Bank – Doing Business Report 2024 – https://worldbank.org

- International Telecommunication Union – ICT Statistics 2024 – https://itu.int

- Italian Communications Authority – Telecom Reports and 5G Rollout – https://agcom.it

- European Gaming and Betting Association – Market Research 2024

- European Central Bank – Digital Payment Systems Analysis 2024

- Corriere della Sera – Italian Economic Reports 2024

- Gaming Compliance Journal – Italy Market Overview 2024

- Statista – Italy Internet and Mobile Usage Statistics 2025

- Telecom Italia Annual Report 2024

- Vodafone Italy Corporate Reports 2024

- UNCTAD – Investment Policy Review Italy 2024

- OECD – Tax Policy Studies Italy 2024

- Italian Ministry of Economic Development – E-commerce and Digital Services 2024

- European Commission – Consumer Market Reports 2024

- Fitch Ratings – Italy Credit and Business Reports 2025

- PwC Italy – Gambling Industry Compliance and Taxation Report 2024

- Deloitte Italy – Technology Sector Analysis 2025

- EY Italy – Business Environment and Market Entry Guide 2024

- McKinsey & Company – Digital Consumer Behavior Italy 2025

- GfK – Market Research on Italian Lottery and Betting 2024

- Italian Association of Online Gaming Operators (AAMS) Reports 2024

- Academic Studies – University of Rome – Gambling Behavior and Prevention 2024

- Reuters – Italy Gambling Regulatory News Updates 2024-2025

- European Gaming and Betting Supervision Network (EGBA) – Regulatory Cooperation 2024

- Financial Times – Italy Business and Technology Feature 2025

- Local Italian media outlets – Economic and Regulatory Developments 2024-2025

- Google Trends Data – Italy Gaming and Digital Services 2025

- Apple & Samsung Market Share Reports Italy 2025

- Italian Digital Marketing Agencies – User Behavior Studies 2024

🎯 Gambling Databases Country Rating: Italy

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.3/10 | 🟡 Moderate |

| Player Access Score | 9.3/10 | 🟢 Excellent |

| Overall Market Attractiveness | 7.3/10 | 🟡 Mature but Saturated |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Strict Advertising Prohibition (“Decree Dignity”): Since 2019, a near-total ban on gambling advertising (TV, radio, internet, sports sponsorships) makes customer acquisition EXTREMELY difficult and expensive for new entrants.

- Aggressive ISP Blocking: ADM actively maintains a blacklist of unlicensed sites. ISPs are legally mandated to block access to offshore operators within days of detection.

- High Effective Tax Burden: While GGR tax is 22%, the combination of Corporate Tax (24%) and Regional Tax (3.9%) results in a heavy fiscal burden.

- Strict Compliance & Reporting: Operators must connect to ADM’s centralized server for real-time transaction monitoring. Any discrepancy leads to immediate fines or license suspension.

- Criminal Sanctions: Operating without an ADM license is a criminal offense in Italy (Law 401/1989), punishable by imprisonment and asset seizure.

- Payment Blocking: Italian banks and payment processors (PSPs) are prohibited from processing transactions for unlicensed gambling entities.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality (Casino, Sports, Poker, Lotto all legal +3.0). Deductions: Severe advertising restrictions limit commercial viability (-0.5). Final: 2.5/3.0. |

| Licensing Process | 25% | 1.8/2.5 | Accessible process with clear requirements (+2.0). Fees are reasonable (€50k application + €20k/year). Deductions: Lengthy processing time of 6-12 months (-0.25), extensive technical certification and bureaucracy (-0.25), rigid probity checks (-0.20). Final: 1.8/2.5. |

| Taxation & Costs | 20% | 0.5/2.0 | GGR tax is 22% (15-25% bracket +1.5). Deductions: Corporate tax (24%) + Regional Tax (3.9%) pushes effective tax rate near 50% (-1.0). Customer Acquisition Costs are inflated due to ad ban, often exceeding €400-500 (-0.5). Final: 0.5/2.0. |

| Operational Requirements | 15% | 0.5/1.5 | Remote operation possible (+1.5). Deductions: Must use Italian payment gateways/banking (-0.25), mandatory real-time server connection to ADM (SOGEI system) is technically burdensome (-0.5), strict monthly compliance reporting (-0.25). Final: 0.5/1.5. |

| Market Environment | 10% | 0.0/1.0 | Good general business environment (+0.7). Deductions: The “Decree Dignity” advertising ban severely hampers growth (-0.5), market is saturated with 150+ operators (-0.20). Final: 0.0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal and regulated (+4.0). Players can access all verticals (Slots, Live Casino, Sports, Poker) without legal risk on licensed sites. |

| Practical Accessibility | 30% | 2.3/3.0 | Multiple payment methods including PayPal/Postepay (+3.0). Deductions: ISP blocking of offshore sites is effective (-0.5), strict KYC requires ID upload *before* withdrawal or within 30 days (-0.20). Final: 2.3/3.0. |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players using licensed sites (+2.0). Tax is withheld at source, simplifying player experience. |

| Market Availability | 10% | 1.0/1.0 | Over 150 licensed operators available (+1.0). High competition benefits the player with good odds and platforms. |

🔍 Key Highlights

Strengths

- Total Market Legality: Unlike many countries, every major vertical (Casino, Sports, Poker, Bingo) is fully regulated and legal.

- Clear Licensing Path: The ADM provides a transparent, albeit bureaucratic, path to legality. It is not a “closed” monopoly system.

- High ARPU: Italian players are valuable (€420 ARPU) and culturally accustomed to gambling.

⛔️ CRITICAL RISKS AND CHALLENGES

- Advertising Ban (Decree Dignity): You cannot run TV spots, radio ads, or sponsor Serie A teams. Marketing is restricted to SEO, affiliate comparison sites (grey area), and CRM. This cements the dominance of established brands.

- Financial Barriers: 22% GGR Tax + 24% Corporate Tax + 3.9% IRAP means the government takes roughly half your profits.

- Technical Integration: You must integrate with the SOGEI platform. Every bet is authorized in real-time by the state. If the state server goes down, your site cannot take bets.

- Offshore Enforcement: Italy is a pioneer in ISP blocking. Unlicensed domains are blocked rapidly, and payments to known unlicensed processors are often declined by Postepay and Italian banks.

- Market Saturation: With ~150 licensees, the market is crowded. Competing without mass-media advertising requires a massive budget for alternative acquisition channels.

Player-Specific Issues

- KYC Friction: Players must submit a copy of their ID within 30 days of registration, or the account is suspended. This causes drop-off.

- Offshore Access: Accessing non-AAMS/ADM sites usually requires a VPN due to ISP blocking.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €250,000 – €500,000 (License fee is only €50k, but legal, technical compliance, and bank guarantees drive this up significantly).

Monthly Operating Costs: High. Compliance reporting, Italian-speaking support, and server maintenance add up.

Effective Tax Rate on Revenue: ~45-50% (22% GGR + 27.9% tax on profits).

Customer Acquisition Cost: High (€300+) due to the inability to advertise via mass media. Reliability on SEO and affiliates drives up CPA.

Time to Breakeven: 24-36 months.

Profitability Assessment: The economics are challenging for small operators. The high tax wedge and the advertising ban favor large, incumbents who already have a database. Entry is not recommended for startups with less than €3M-€5M in funding. This is a volume game where thin margins only work at scale.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Immediate ISP blocking, payment processing blacklisting, criminal charges under Law 401/1989. |

| Licensed Operators | Medium | Risk of heavy fines for AML failures or advertising violations (fines for ad breaches start at €50k). |

| Affiliates/Advertisers | High | The “Decree Dignity” extends fines to affiliates and media owners promoting gambling. Review sites exist in a grey area but face constant scrutiny. |

| Payment Processors | High | Processing for unlicensed sites is illegal; Italian authorities actively pressure Visa/MC/Banks to block MCC 7995 for unlicensed merchants. |

| Company Directors | Medium | Criminal liability exists for operating without a license; directors of licensed entities face scrutiny for compliance failures. |

🚨 Extradition and International Enforcement

Extradition Treaties: Italy is a key member of the EU and has active extradition treaties with the USA, UK, Canada, Australia, and all EU member states. The European Arrest Warrant (EAW) allows for rapid extradition within Europe.

Enforcement History: Italy actively participates in Interpol and Europol operations (e.g., Operation ‘Gambling’). Authorities frequently target organized crime links in gambling, seizing assets and issuing arrest warrants across borders.

Safe Jurisdictions: Only countries with no extradition treaty and poor diplomatic relations with the EU (e.g., Russia, parts of Asia) offer safety, but operating an Italian-facing site from there is commercially unviable due to payment blocking.

📋 Final Verdict

Italy receives an Operator Ease Score of 5.3/10 and a Player Access Score of 9.3/10, resulting in an overall market attractiveness rating of 7.3/10.

HONEST ASSESSMENT: Italy is a “Pay-to-Play” market designed for giants, not innovators. While legally open and fully regulated, the marketing ban (Decree Dignity) acts as a massive moat protecting incumbents. For a new operator, the inability to advertise, combined with an effective tax rate approaching 50% and strict technical mandates, makes profitability extremely difficult to achieve without a massive database or acquisition budget. Offshore operation is highly risky due to efficient ISP blocking and criminal sanctions.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major multi-national operator with an existing database and significant capital (>€5M).

- Able to sustain low margins (10-15%) for 3+ years while building market share.

- Expert in SEO and CRM retention, as paid media is banned.

❌ Definitely Avoid If You Are:

- A startup looking for quick ROI (under 2 years).

- Heavily reliant on traditional advertising (TV, Social Media Paid Ads) for acquisition.

- An offshore operator hoping to fly under the radar (ADM blocking is automated and effective).

- Under-capitalized (less than €1M won’t even cover the first year of compliance and tech costs).

⚠️ BOTTOM LINE: A stable, high-volume market that is legally safe but commercially punishing. Enter only if you have deep pockets and can survive without advertising.

Looking for sharpest bookies in Italy, anyone know which sites have lowest margins?

Regarding your question about sharpest bookies in Italy, it’s worth noting that the market is highly competitive, with many licensed operators offering competitive odds. Some of the most popular bookmakers in Italy include Bet365, William Hill, and Unibet. However, it’s always important to do your own research and compare odds across different sites to find the best value for your bets. Additionally, be sure to check the terms and conditions of each site, as well as their licensing and regulatory status, to ensure that you’re betting with a reputable and trustworthy operator.

Thanks for the info, do you know if any of these bookies offer decent limits for sharp bettors?

Regarding limits for sharp bettors, it’s worth noting that some bookmakers in Italy do offer higher limits for experienced bettors. However, these limits can vary depending on the operator and the specific market. It’s always a good idea to check with the bookmaker directly to see what their limits are and to discuss your options with their customer service team.

Italy’s iGaming market is fascinating, with a strong focus on player protection and market integrity. The country’s regulatory framework, overseen by the Agenzia delle Dogane e dei Monopoli (ADM), ensures that operators must obtain a license to offer services. This has led to a structured market with approximately 150 licensed online operators. The market size is estimated to be around €1.8 billion, with a growth rate of 5.5% forecasted from 2024 to 2029. In terms of poker, the Italian market is quite competitive, with many operators offering a range of games and tournaments. However, the regulations around online poker are strict, with a focus on ensuring that players are protected and that the games are fair. I’ve been analyzing the market and noticed that the average revenue per user (ARPU) is around €420, which is relatively high compared to other European markets. The problem gambling prevalence is also relatively low, at around 1.5% of the adult population. Overall, Italy’s iGaming market is a complex and highly regulated environment that requires operators to be compliant with strict regulations and to prioritize player protection.

That’s a great analysis of the Italian iGaming market. The focus on player protection and market integrity is indeed a key aspect of the country’s regulatory framework. The use of technology, such as RNG certification, to ensure game fairness is also an important aspect of the market. In terms of poker, the Italian market is indeed competitive, with many operators offering a range of games and tournaments. The strict regulations around online poker are designed to protect players and ensure that the games are fair. The high ARPU and low problem gambling prevalence are also positive indicators of the market’s health. Overall, Italy’s iGaming market is a complex and highly regulated environment that requires operators to be compliant with strict regulations and to prioritize player protection.