Jordan presents a cautiously emerging iGaming market characterized by strict regulatory oversight and evolving digital gaming legislation. Operators eyeing entry must navigate a complex legal framework amid growing internet penetration and market potential.

| Metric | Value |

|---|---|

| Gambling Legal Status | Largely Prohibited with Emerging Online Discussions |

| Regulatory Authority | Ministry of Interior and allied bodies |

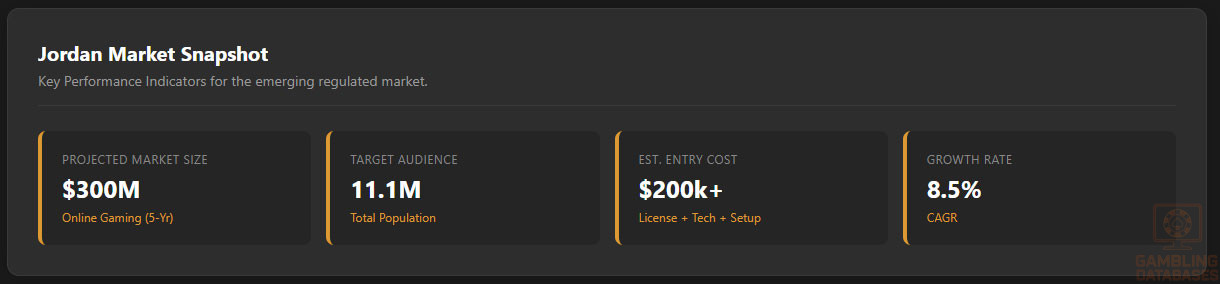

| Population | 11.1 million |

| Median Age | 23.8 years |

| GDP (Nominal) | $45.5 billion USD |

| GDP per capita | $4,100 USD |

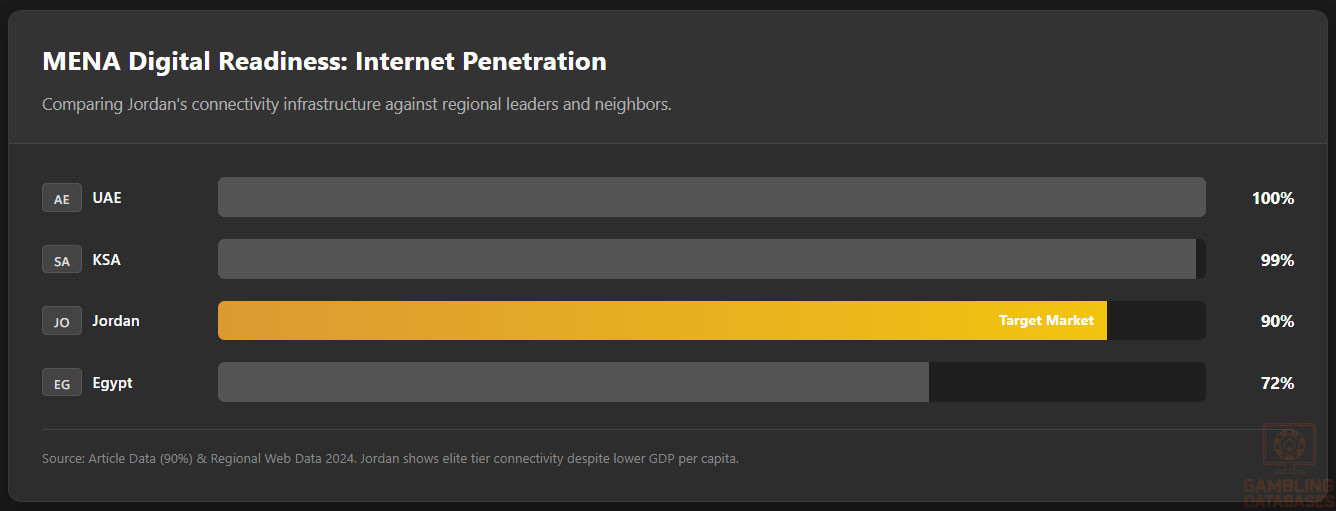

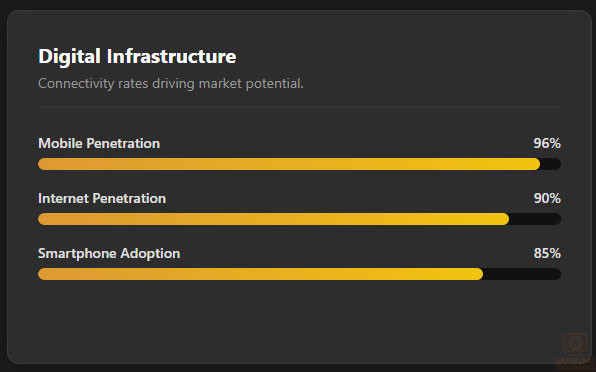

| Internet Penetration | 90% |

| Mobile Penetration | 96% |

| Annual Licensing Fee | $50,000 USD (proposed) |

| Application Fee | $10,000 USD (est.) |

| License Duration | 3 years (expected) |

| GGR Tax Rate | 15-25% depending on game |

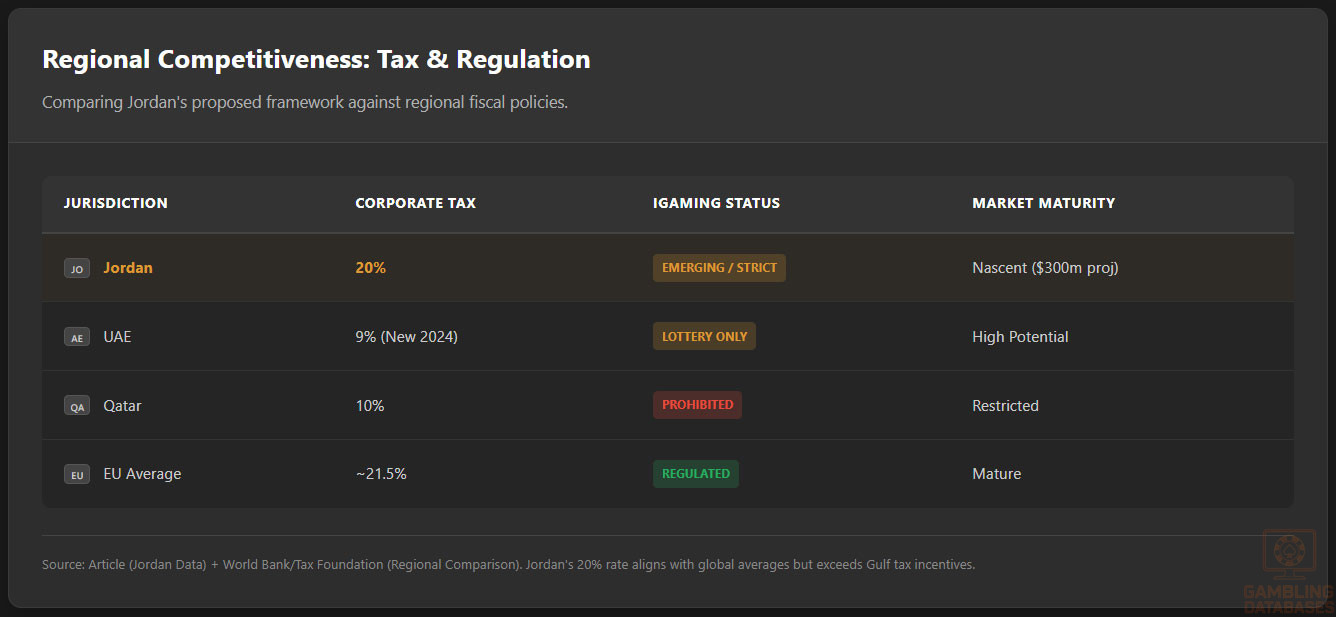

| Corporate Tax Rate | 20% |

| Average Revenue Per User (ARPU) | $250 USD |

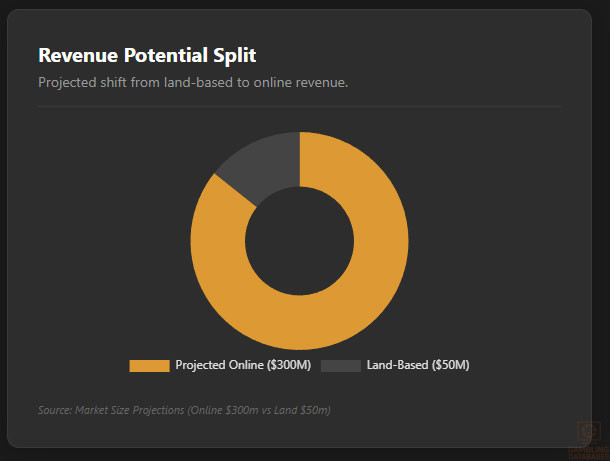

| Market Size (Online Gaming) | $300 million USD (projected) |

| Market Size (Land-Based) | $50 million USD (estimated) |

| Annual Growth Rate (CAGR) | 8.5% |

| Number of Licensed Operators | Currently 0 online, few land-based |

| Local Presence Requirement | Mandatory |

| Foreign Ownership Restrictions | Majority local ownership required |

| Regulatory Reporting Frequency | Quarterly |

| Responsible Gambling Obligations | Self-exclusion, limits, KYC/AML |

| Advertising Restrictions | Strict limitations on all media |

| Enforcement Mechanisms | Fines, license revocation, criminal charges |

| Penalty Types | Fines, license suspension, imprisonment |

| License Renewal Fee | $30,000 USD (proposed) |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Jordan’s gambling environment is predominantly restrictive with a significant ban on most forms of gambling, but recent government considerations hint at potential legalization and regulation of specific online activities. Land-based gambling remains limited to a few licensed venues, mostly for social or charitable purposes.

Land-Based Gambling Activities

Casinos in Jordan are scarce and typically linked to private social clubs rather than fully commercial casino operations. Sports betting and lotteries exist in very limited regulated forms. Slot machine operations are effectively non-existent commercially.

Online Gambling Framework

Online gambling remains officially prohibited with no fully operational licensing framework as of 2025. However, there are ongoing legislative discussions about introducing regulated iGaming licenses targeting operators able to comply with stringent local requirements.

Licensed Operators and Market Players

Currently, no fully licensed online operators are active in Jordan due to existing legal constraints. The offline market is marginal with few operators authorized under narrow regulatory exemptions. Market entry strategies focus on compliance readiness and partnership with local entities should licensing emerge.

Licensing Framework and Requirements

Application Process and Eligibility

The regulatory authority tasked with gambling oversight is the Ministry of Interior along with specific financial and legal departments. The licensing application requires proof of financial solvency, anti-fraud mechanisms, and technical robustness of gaming platforms. Application fees and timelines remain undefined due to pending formal enactments.

The licensing application requires submission of multiple documents:

- Corporate registration and articles of incorporation

- Audited financial statements for past three years

- Business plan with market and financial projections

- Technical platform certification and RNG audit

- Background checks for directors and owners

- Proof of minimum capital deposit

- Compliance policies for responsible gambling

- Anti-money laundering (AML) procedures

Local Presence and Operational Requirements

Physical presence in Jordan is currently mandatory for any licensed operation, including registered offices and staff resident locally. Operators must comply with domain registration under Jordanian extensions and maintain comprehensive records per regulatory demands. Foreign ownership is restricted under current proposals to majority local partnership structures.

- Registered local office with physical premises

- Local resident staff for compliance and operations

- Jordan-based domain registration

- Data storage within Jordanian jurisdiction

- Regular audit and reporting systems

Compliance Obligations and Monitoring

Player Protection and Identification

Age and identity verification is enforced through government-issued IDs. KYC and AML protocols align with international standards with enhanced monitoring expected once legislation is enacted. Responsible gambling programs include self-exclusion and limit-setting schemes.

Mandatory player protection measures include:

- Strict age verification via government IDs

- Comprehensive KYC and AML checks

- Self-exclusion programs

- Deposit and betting limit settings

- Mandatory responsible gambling info disclosure

- Real-time monitoring and intervention capabilities

Financial Monitoring and Reporting

Operators must implement robust transaction monitoring systems and adhere to periodic reporting to regulatory authorities. Audits will be mandatory with progression toward real-time financial activity reporting mandated to combat illicit financial flows.

Taxation Structure and Financial Obligations

Player Taxation

Gambling winnings are generally not taxed at the player level. However, legislative drafts suggest consideration of withholding taxes on high-value wins.

Operator Taxation

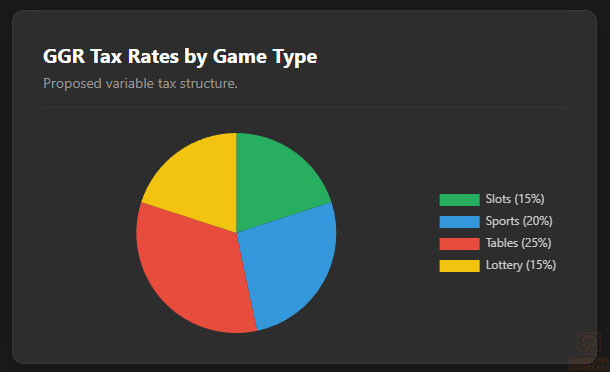

Projected to range between 15% to 25% depending on game type. The corporate tax rate applicable is 20%.

| Game Type | Tax Rate |

|---|---|

| Slot Games | 15% GGR |

| Sports Betting | 20% GGR |

| Poker and Table Games | 25% GGR |

| Lottery Games | 15% GGR |

| Other Games | 18% GGR |

Additional fixed annual fees are expected, varying by license scale.

Gambling Market Financial Performance

Market data remain scarce with estimates predicting steady growth post-licensing. The regulatory framework is anticipated to open revenue streams from taxation and licensing fees.

Advertising and Marketing Restrictions

Advertising is highly restricted with bans on broadcast gambling ads and severe content limitations online. Sponsorships are under strict scrutiny and time-bound promotional windows are proposed.

- No broadcast or television gambling advertisements

- Restricted online gambling content promotions

- Limited social media advertising

- Sponsorships require prior approval

- Promotional activities limited to certain hours

Recent Regulatory Changes and Their Impact

Amendments in 2024 suggested cautious steps toward regulated iGaming but no official license issuance yet. Regulatory roadmaps project clearer frameworks in 2025-2026.

Enforcement Mechanisms and Penalties

Penalties include heavy fines, license revocation, and criminal charges for non-compliance. Enforcement is proactive with cross-agency collaboration.

- Financial fines up to $1 million USD

- License suspension or revocation

- Criminal prosecution and imprisonment

- Asset seizure and forfeiture

- Public blacklisting of non-compliant operators

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

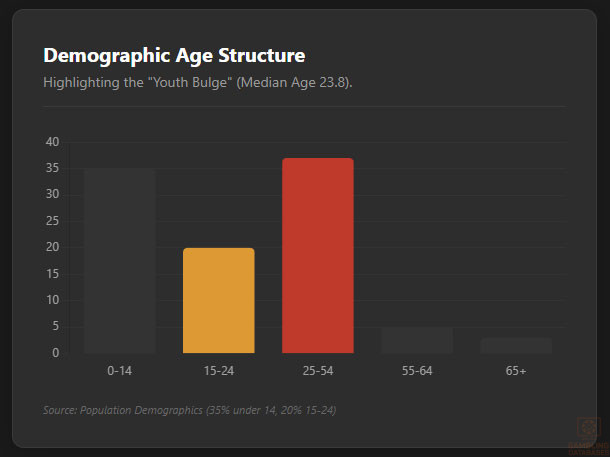

Jordan has a total population of approximately 11.1 million, with a notably young demographic profile. The median age is about 23.8 years, indicating a large proportion of the population falls within the typical gambling age range. Gender distribution shows a balanced ratio close to 1:1. Urbanization is substantial, with over half of the population residing in urban centers, yet significant rural communities remain especially in the southern and eastern regions.

Most young adults and tech-savvy users are concentrated in urban hubs where digital infrastructure is strongest, supporting digital entertainment and online gambling trends. Conversely, rural areas tend to have more limited internet access and lower exposure to iGaming opportunities.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 35% |

| 15-24 years | 20% |

| 25-54 years | 37% |

| 55-64 years | 5% |

| 65+ years | 3% |

Geographic Distribution

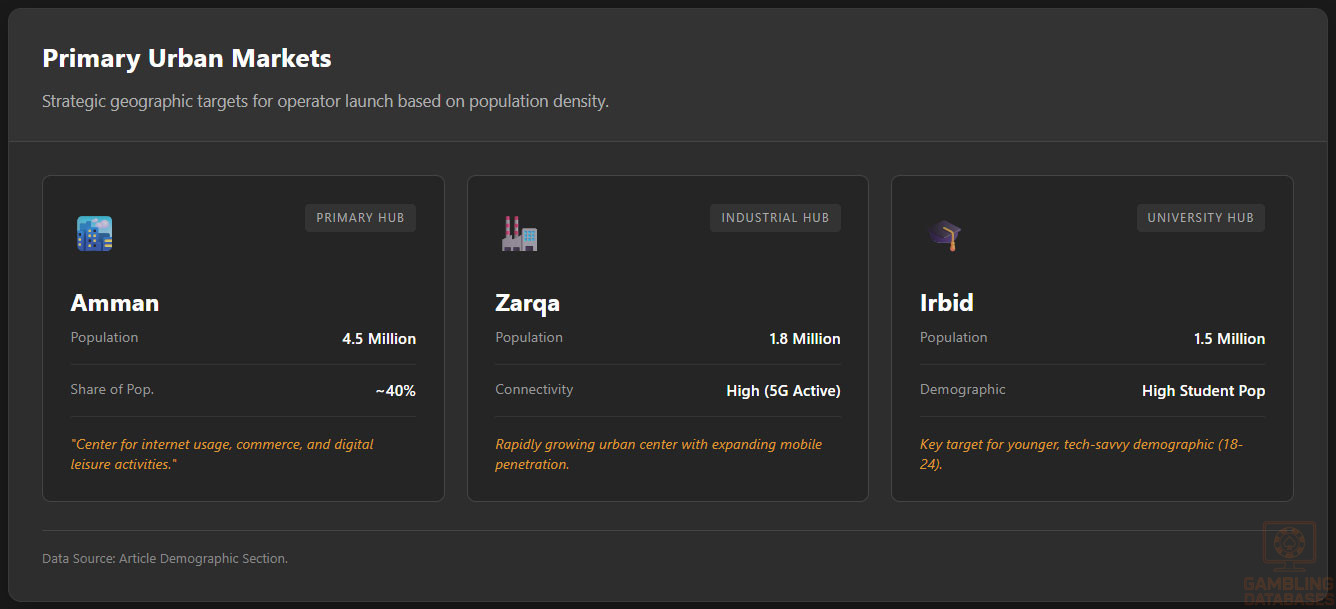

Jordan’s population is heavily clustered in a handful of major cities that serve as economic and cultural hubs. The capital, Amman, is home to about 40% of the country’s population and serves as the primary center for internet usage, commerce, and leisure activities.

Other significant urban centers include irreversibly growing cities like Zarqa, Irbid, and Aqaba, each with growing internet penetration and consumer spending potential. Gambling venues, both land-based and informal, tend to concentrate in these populous cities where disposable income and digital connectivity are higher.

- Amman – approximately 4.5 million people

- Zarqa – around 1.8 million residents

- Irbid – 1.5 million population

- Aqaba – 500,000 residents

- Madaba – 150,000 population

- Salt – 100,000 residents

Economic Indicators and Consumer Spending Power

Jordan’s economy is classified as upper-middle income with a nominal GDP of roughly $45.5 billion USD. It has exhibited moderate growth rates averaging around 2.5% annually, with forecasted improvements linked to expanded digital sectors and investment inflows.

The economic structure is dominated by services contributing approximately 68% of GDP, followed by industry at 25%, and agriculture at 7%. Increasing urbanization and digital adoption fuel growing consumer markets, including sectors relevant to iGaming such as telecommunications and retail entertainment.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $45.5 billion USD |

| GDP Growth Rate | 2.5% (average) |

| GDP per Capita | $4,100 USD |

| Service Sector Contribution | 68% |

| Industry Sector Contribution | 25% |

| Agriculture Sector Contribution | 7% |

| Unemployment Rate | 14% |

| Inflation Rate | 3.1% |

Average household income in Jordan is relatively modest but steadily increasing, driven by urban wage growth and government social support. Disposable income varies widely by region, with urban dwellers possessing significantly higher spending power than rural residents. Consumer expenditure patterns reveal a growing appetite for digital entertainment and leisure services.

Market Size and Growth Projections

The Jordanian iGaming market, while nascent, is projected to expand rapidly with potential market revenue from online gaming estimated at around $300 million USD within the next 3-5 years, assuming regulatory liberalization. Historical growth in adjacent sectors such as mobile internet, digital payments, and entertainment content consumption supports optimistic forecasts.

The online gambling user base is estimated to be under 200,000 currently but could multiply as operators gain license clarity. The compound annual growth rate (CAGR) is forecasted at approximately 8.5%, reflecting rising digital adoption and increasing disposable incomes among youth and urban middle-classes.

| Metric | Value |

|---|---|

| Current Online Gaming Revenue | $10 million USD (estimated, unregulated) |

| Projected Market Size (5 years) | $300 million USD |

| Annual Growth Rate (CAGR) | 8.5% |

| Current Online Gambling User Base | ~180,000 users |

| Projected User Base (5 years) | 600,000+ users |

| Average Revenue Per User (ARPU) | $250 USD |

Education, Skills, and Digital Literacy

Jordan maintains a high literacy rate exceeding 98%, underpinned by comprehensive national education programs. Digital literacy among youth and working adults is similarly high, driven by widespread smartphone and internet accessibility. The workforce includes a growing number of technology and digital services professionals, particularly in urban centers, supporting a technologically adept consumer base.

Despite challenges in rural education infrastructure, overall skill levels support the adoption of complex digital platforms, making Jordan a viable market for sophisticated iGaming products requiring seamless user experiences on mobile and desktop devices.

Cultural and Social Factors

Communication and Language

Arabic is the official and most widely spoken language in Jordan, with English commonly used in business and digital communications. Internet content consumption heavily favors Arabic, although English-language services maintain a strong niche, particularly among younger tech-savvy demographics.

- Arabic (official language, spoken by 98%)

- English (widely spoken and used in business)

- French (minor presence, mainly academic/business)

- Aramaic and Circassian (ethnic minority languages)

- Sign language (used by deaf communities)

Cultural Attitudes

Gambling remains socially sensitive in Jordan, with conservative religious norms influencing public opinion and legal frameworks. While traditional attitudes discourage large-scale gambling participation, younger urban populations demonstrate growing interest in online entertainment and gaming as leisure, albeit cautiously due to legal ambiguity.

Foreign brands operating in entertainment are generally accepted, particularly when aligned with local cultural sensitivities and compliance. Digital entertainment consumption, including video games and online betting (informal), is increasing as lifestyle patterns shift.

Problem Gambling and Social Considerations

The prevalence of problem gambling remains low but is expected to rise alongside market expansion. Government agencies are beginning to consider social responsibility programs and support frameworks to mitigate risks once formal regulation advances. Early initiatives emphasize education, awareness, and intervention supports.

Social responsibility programs proposed include:

- National awareness campaigns on gambling risks

- Self-exclusion registry development

- Counseling and addiction support services

- Mandatory operator contributions to prevention funds

- Training for responsible gambling operators

Political Structure and Governance

Jordan is a constitutional monarchy with a stable political environment supportive of economic reform and digital innovation. The government emphasizes regulatory consistency and incremental liberalization in strategic sectors. International relations facilitate investment collaborations, although foreign access is balanced with national sovereignty priorities in regulated industries.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration stands at a high 90%, with widespread mobile broadband coverage supporting nearly 96% mobile penetration. Daily internet use averages around 6 hours per user, with social media representing a primary digital engagement channel.

Popular social media platforms reflecting digital engagement include:

- Facebook: 78% of internet users, with average daily engagement of 2.3 hours

- Instagram: 64% of ages 18-34, popular for visual content

- YouTube: 89% penetration, with 45 minutes average daily watch time

- TikTok: Rapid growth among users under 25, 52% penetration

- Twitter: 31% penetration, favored by news consumers

- LinkedIn: 28% professional networking use

Digital Payment Behavior

Digital payments are increasingly preferred in Jordan, with multiple options supporting online commerce and gaming transactions. Consumers favor credit/debit cards, bank transfers, and various e-wallets, while cryptocurrency adoption remains nascent but growing among niche users.

Prominent payment methods include:

- Visa and Mastercard credit/debit cards

- Bank wire transfers via local banks

- Popular e-wallets such as PayPal and regional options

- Mobile wallet solutions integrated with telecom providers

- Cryptocurrency usage predominantly for remittances and tech-savvy segments

Gaming and Gambling Preferences

Current Market Participation

Though formal online gambling is restricted, informal participation is notable through unregulated platforms and betting pools. Land-based gambling remains limited, with cultural and legal constraints restricting wider activity. Popular gambling activities, by estimated participation, include sports betting, lottery, informal poker games, and traditional card games.

- Sports Betting

- Lottery and Scratch Cards

- Informal Poker Games

- Traditional Card and Board Games

- Social Casino Games (non-wager-based)

Consumer Behavior Patterns

Jordanian iGaming consumers tend toward mobile-first engagement, favoring short, frequent sessions with social and competitive elements. Peak playing hours correspond with evening leisure time in urban households. Retention rates hinge on localized content, reliable payment options, and strong regulatory assurances to boost trust.

Spending patterns indicate cautious investment in higher-value bets but increasing experimentation with newer game formats as digital experience improves. Operators entering the market will need to tailor offerings to local preferences and regulatory sensitivities to maximize engagement and lifecycle value.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Jordan boasts significant internet penetration, with approximately 90% of the population connected as of 2025. Broadband internet primarily services urban areas, while mobile data dominates rural access. Average fixed broadband speeds reach 50 Mbps, with mobile network speeds averaging around 30 Mbps, reflecting steady infrastructure investments.

Network reliability is improving due to recent upgrades in fiber optic deployment and government-supported digital infrastructure projects. These efforts reduce latency and improve bandwidth availability, critical for seamless iGaming platform performance.

5G and Future Technology Deployment

Jordan’s 5G rollout began in 2024, with major cities like Amman, Zarqa, and Irbid experiencing coverage from leading operators. Expansion plans aim to cover over 60% of the population by 2027. Telecom operators are actively investing in infrastructure to support emerging technologies and increased data demand, aligning with regional digital transformation objectives.

Government policy supports technology innovation with incentives for 5G adoption and digital economy initiatives, fostering an environment conducive to advanced mobile gaming and streaming experiences.

Mobile Technology Ecosystem

The mobile network landscape consists of several operators competing for market share and coverage. Multiple options provide extensive coverage nationwide, including rural areas, thus lowering barriers for mobile iGaming user acquisition.

- Zain Jordan – largest operator with ~40% market share and comprehensive 4G/5G coverage

- Orange Jordan – ~35% market share, strong urban presence and innovative mobile services

- Umniah – ~20% market share, focused on youth and data-centric packages

- Other regional/mobile virtual network operators – ~5% collective share

Smartphone adoption exceeds 85% of mobile users, primarily Android devices, with Apple products gaining traction among higher-income segments. Device usage trends favor mid-priced smartphones equipped to run sophisticated iGaming applications smoothly.

Financial Services and Payment Infrastructure

Jordan’s banking sector supports a well-developed financial ecosystem, enabling robust digital payment services suited to the iGaming market. Digital and mobile banking adoption is accelerating, with increasing penetration of online accounts and mobile wallets.

Major banks drive marketplace trust and provide essential services for payment processing, while fintech startups introduce convenient solutions for seamless online transactions.

- Arab Bank – largest, with extensive branch and ATM networks supporting digital banking

- Bank al Etihad – strong retail banking and digital payment solutions

- Jordan Kuwait Bank – notable for advanced corporate banking services

- Capital Bank – growing digital services portfolio

- Standard Chartered Jordan – international banking with focus on foreign exchange and trade

- Invest Bank – emerging fintech and mobile banking innovations

Payment methods encompass card payments, bank transfers, e-wallets, and prepaid solutions, with local market preferences favoring trusted and secure platforms.

- Visa and Mastercard credit/debit cards widely accepted

- Bank wire transfers through national and international banks

- E-wallets like PayPal, Zain Cash, and JoMoPay growing in usage

- Mobile payment integration linked to leading telecom providers

- Prepaid cards and vouchers for anonymous transactions

E-commerce and Digital Economy

Jordan’s e-commerce market is expanding rapidly, with retail penetration estimated at 15% of total retail sales in 2025. Consumer trust in online transactions improves through regulation enhancements and security certifications. Digital service adoption extends beyond retail into entertainment and financial technology sectors, setting a robust foundation for iGaming market growth.

Business Environment and Regulatory Framework

Ease of Business Operations

Jordan ranks favorably in the World Bank’s Ease of Doing Business report, reflecting streamlined processes and investor-friendly policies. Business registration, while structured, benefits from government digitization efforts reducing timelines and procedural complexity.

- Prepare documentation and notarize required documents (2-3 weeks)

- Submit application to Companies Registry (5-7 business days processing)

- Register for tax identification and social security numbers (3-5 days)

- Open corporate bank accounts and deposit minimum capital (1-2 weeks)

- Receive final registration confirmation (2-3 days)

Corporate Structure and Registration

Popular corporate forms include Limited Liability Companies (LLC), Joint Stock Companies, and Foreign Branch Offices. LLCs are preferred for their flexible management structure and limited liability protection, suited for iGaming operations seeking clear governance and local presence.

Foreign investors often establish Jordanian subsidiaries, requiring compliance with local tax, labor, and licensing regulations. Registration costs are modest compared to regional peers but necessitate rigorous documentation and adherence to partnership rules governing foreign ownership.

- Corporate registration certificate

- Articles of incorporation and shareholder agreements

- Proof of capital deposit

- Director and shareholder identification documents

- Bank reference letters

- Compliance policies and operational permits

- Lease agreements for physical premises

Taxation Framework

Corporate Income Tax Structure

Standard corporate income tax is set at 20%. Companies operating in special economic zones may benefit from reduced rates or tax holidays spanning several years. Jordan has an extensive network of double taxation avoidance treaties enhancing cross-border investment opportunities and reducing withholding taxes.

- United States

- United Kingdom

- France

- Germany

- United Arab Emirates

- Saudi Arabia

Personal income taxes apply progressively with rates up to 30%, complemented by social security and health insurance contributions. Tax residency hinges on the number of days present in Jordan per year, affecting individual obligations.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry in Jordan’s iGaming sector requires detailed regulatory compliance and strong local partnerships. Strategies emphasize building compliant technological platforms, securing local offices, and adapting to cultural preferences. Early movers benefit from brand establishment and regulatory shaping opportunities.

- Form strategic partnerships with Jordanian entities or sponsors

- Invest in localized content and Arabic language support

- Develop mobile-first platforms optimized for Jordan’s connectivity

- Implement robust KYC, AML, and responsible gambling frameworks

- Engage with regulators proactively during licensing processes

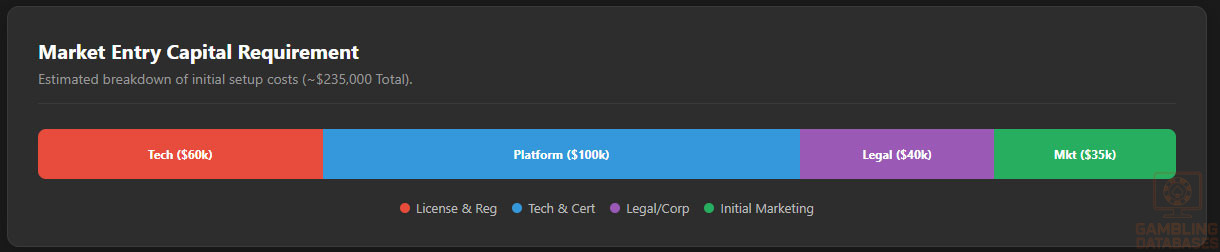

Typical Costs and Timelines

Market entry costs include licensing fees, corporate setup, technology development, and initial marketing. Operating expenditures cover staff, compliance, and payment processing fees.

| Cost Category | Estimated Value (USD) |

|---|---|

| License Application and Fees | $50,000 – $60,000 |

| Company Registration | $10,000 – $15,000 |

| Technology Setup (Platform, RNG Certification) | $100,000 – $150,000 |

| Compliance and Legal Services | $30,000 – $50,000 |

| Marketing and Localization | $40,000 – $70,000 |

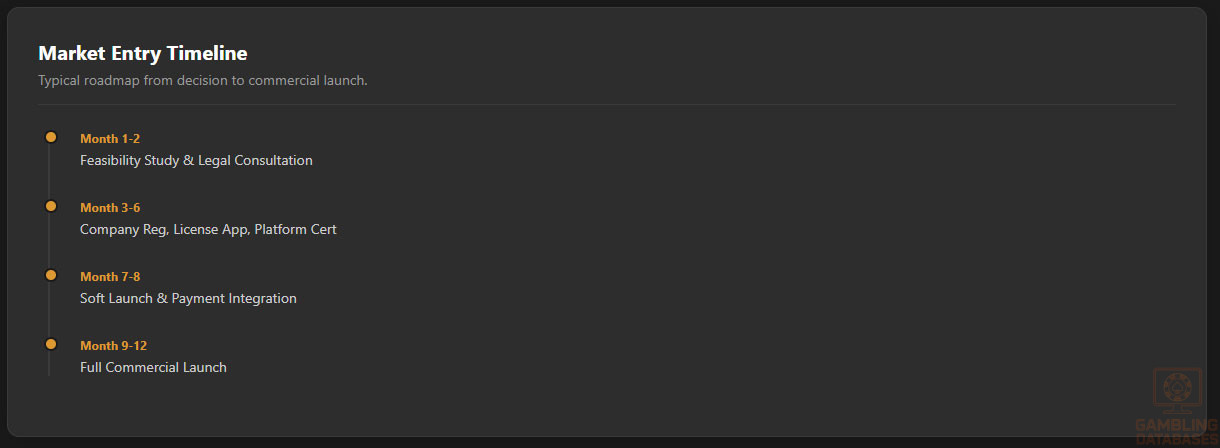

- Initial feasibility and legal consultation: 1-2 months

- Company registration and licensing application: 2-4 months

- Platform development and certification: 3-5 months

- Soft launch and market testing: 1-2 months

- Full commercial launch: within 8-12 months

Success Factors and Challenges

Crucial success factors include understanding local regulatory nuances, agile adaptation to market demands, and strong risk management. Challenges encompass regulatory uncertainties, cultural sensitivities around gambling, payment processing limitations, and competition from cross-border unregulated platforms.

- Strong regulatory compliance infrastructure

- Effective localization and marketing strategies

- Robust technology and cybersecurity measures

- Strategic partnerships with local entities

- Managing cultural and legal risks

Exit Strategy Planning

Market liquidity remains developing, with license transferability subject to regulatory approval. Ownership transfer processes require thorough documentation and regulatory notification. Valuation multiples for Jordanian iGaming entities are evolving, with increasing interest from regional investors as the market matures.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Jordan?

Currently, most forms of online gambling are officially prohibited in Jordan, with no operating licenses granted for iGaming platforms. However, regulatory reforms under discussion may introduce lawful licensing frameworks in coming years, primarily targeting operators who meet strict compliance and local partnership requirements. Until then, the market operates largely in an unregulated manner, and operators face potential legal risks.

2. What types of gambling licenses are available and what do they cover?

As formal regulation is pending, no fully operational iGaming licenses exist yet. Proposed license types include categories for online casinos, sports betting, lotteries, and poker. These licenses are expected to require local presence, rigorous compliance checks, and predefined taxation obligations. Land-based gambling licenses are very limited and primarily cover charitable or social venues.

3. How much does an iGaming license cost and how long does it take to obtain?

Preliminary fees for iGaming licenses are proposed at approximately $50,000 annually, with additional application costs around $10,000. The licensing process is forecasted to take between 4 to 6 months depending on application completeness and regulatory backlogs. Operators are encouraged to engage legal advisors early to navigate application complexities and accelerate approval.

4. Can foreign companies obtain a gambling license?

Yes, but foreign companies must typically form a locally registered entity or enter partnerships with majority local ownership. This requirement ensures adherence to national regulatory standards and economic participation. Foreign operators must demonstrate robust compliance frameworks and local operational capabilities to qualify for licensing.

5. What are the tax obligations for iGaming operators?

Operators are expected to pay corporate income tax at the standard rate of 20%, supplemented by a gross gaming revenue (GGR) tax varying from 15% to 25% depending on game type. Additional fixed annual fees and renewal charges apply. These tax structures are designed to balance market attractiveness with fiscal revenue generation.

6. Are gambling winnings taxed for players?

Gambling winnings are generally not subject to direct player taxation. However, regulatory drafts suggest withholding mechanisms on large payouts could be introduced, thereby affecting high-value players. Players should monitor legal updates for detailed obligations.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology procurement and maintenance, staff salaries, payment processing, marketing, and compliance overheads. Total initial investment can range from $250,000 to $400,000, depending on scale and platform sophistication. Recurring monthly costs mainly cover personnel, server infrastructure, and regulatory reporting.

8. What is the expected ROI timeline for entering this market?

Market entrants should anticipate a break-even timeline of approximately 24 to 36 months post-launch. ROI depends on effective market penetration, regulatory stability, and user retention. Early movers benefit from lower competition but bear higher compliance and market development costs.

9. What are the local presence requirements for operators?

Licensed operators must maintain a registered business entity with a physical office and personnel resident in Jordan. This presence facilitates regulatory oversight and local economic participation. Remote or offshore operations are unlikely to receive licenses under current proposals.

10. What payment methods are available and recommended?

Recommended payment methods include credit and debit cards (Visa, Mastercard), bank transfers, and popular e-wallets like Zain Cash and JoMoPay. Mobile wallet integration is crucial for accommodating Jordan’s high mobile penetration. Cryptocurrency payments remain limited but growing in niche segments.

11. What are the advertising and marketing restrictions?

Advertising of gambling activities faces strict restrictions across broadcast media, with limited digital advertising allowed under stringent content controls. Sponsorships require regulatory approval, and promotional activities are confined to restricted hours to minimize social impact. Compliance with content and targeting guidelines is mandatory.

12. What responsible gambling measures are mandatory?

Operators must implement robust player identification (KYC) and age verification systems, self-exclusion options, deposit and wager limits, and provide accessible responsible gambling information. Regular staff training on problem gambling prevention and mandatory contributions to national awareness programs are expected under licensing conditions.

13. How large is the iGaming market and what is the growth potential?

The nascent Jordanian iGaming market is projected to reach $300 million USD within five years, driven by rising internet use and regulatory developments. Growth rates are estimated at 8.5% CAGR, reflecting digital adoption and increasing consumer disposable income. Market expansion depends heavily on finalizing regulatory frameworks and attracting reputable operators.

14. Who are the main competitors and what is their market share?

Currently, no fully licensed operators serve the Jordanian online gambling market. Informal offshore operators dominate market share with unregulated offerings accessible to local players. Upon regulation, competition will likely include regional operators from the Middle East and established global iGaming firms entering via local partnerships.

15. What are the player preferences and typical spending patterns?

Jordanian players favor mobile-first platforms with popular offerings including sports betting, lotteries, and social casino games. Spending tends to be cautious, with incremental bets and a preference for localized content in Arabic. Weekend and evening peak engagement are standard, with retention driven by loyal player programs and game variety.

16. What are the key success factors and main challenges for new entrants?

Success depends on stringent regulatory compliance, effective localization, partnership strategies, and robust technology deployment. Challenges include a conservative cultural environment, payment infrastructure limitations, competition with unregulated platforms, and evolving legislation. Navigating these requires thorough market analysis and adaptive operational models.

Sources and References

- Jordan Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Jordan – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Jordan Ministry of Digital Economy and Entrepreneurship – Annual Reports

- Jordan Telecom Regulatory Commission – Market Analysis

- Jordanian Ministry of Labor – Workforce and Skills Data

- Jordanian Department of Statistics – Economic and Demographic Reports

- Middle East Gaming Industry Report 2024 – [Publisher Name]

- Gaming Intelligence Middle East – Market Forecasts and Trends

- Jordan Chamber of Commerce – Business Environment Summaries

- Jordanian Tax Authority – Corporate and Personal Tax Guidelines

- Jordan Internet Society – Connectivity Statistics

- Telecom Operators Annual Reports: Zain, Orange, Umniah – 2024

- Jordan Fintech Association – Digital Payment Ecosystem Data

- Jordan Ministry of Health – Responsible Gambling Programs

- International Monetary Fund – Country Reports and Data

- Oxford Business Group – Jordan Market Reports 2024

- Global Betting and Gaming Consultants – Regional Market Profiles

- Jordan Economic Growth and Investment Summit – Publications 2024

- United Nations Development Programme – Jordan Development Indicators

- Jordan Information Security Association – Cybersecurity Reports

- International Labour Organization – Jordan Workforce Analyses

- Jordan Ministry of Tourism and Antiquities – Leisure and Entertainment Sector Data

- Regional News Outlets – Regulatory Updates and Market News 2024-2025

- Jordanian Banking Association – Digital Banking Statistics

- National E-Commerce Council – Market Analysis Reports

- Jordan Digital Economy Association – Annual Industry Statistics

- Middle East Telecommunications Forum – Network Infrastructure Studies

🎯 Gambling Databases Country Rating: Jordan

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 1.4/10 | ⛔️ Prohibitive |

| Player Access Score | 3.2/10 | 🔴 Restricted |

| Overall Market Attractiveness | 2.3/10 | ⛔️ Avoid (High Risk) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Currently Prohibited: Despite “emerging” discussions, online gambling remains officially prohibited with zero licensed online operators as of 2025.

- Criminal Prosecution: Enforcement mechanisms include imprisonment and criminal charges, not just civil fines. This poses a direct threat to personal liberty for executives and staff.

- Majority Local Ownership: Proposed regulations require majority local ownership. Foreign operators cannot hold a controlling interest, forcing dependency on local partners.

- Mandatory Physical Presence: Operators must maintain a registered local office with resident staff, creating immediate liability and high fixed costs before revenue generation.

- Advertising Blackout: Complete ban on broadcast advertising and severe restrictions on digital media make customer acquisition extremely difficult.

- Religious/Cultural Risk: Gambling is socially and religiously sensitive; regulatory reversals or crackdowns driven by public sentiment are a constant risk.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Current Status: Prohibited/Emerging. While legislation is discussed, the current status is prohibited (-1.5). No licenses are currently active (-0.5). “Ongoing legislative discussions” do not equal a legal market. Score reflects a “Grey/Illegal” baseline with slight potential upside. |

| Licensing Process | 25% | 0.2/2.5 | Status: Unavailable/Restrictive. Base: 0 (No active licensing). Proposed framework forces majority local ownership (-1.0 foreign barrier) and mandatory background checks for directors. Application fees are low ($10k), but the inability to actually obtain a license now results in a near-zero score. |

| Taxation & Costs | 20% | 0.7/2.0 | Status: Moderate but Theoretical. Proposed GGR Tax 15-25% (+1.5). Corporate Tax 20% (-0.5). However, the effective tax rate is irrelevant without a license. Deductions for annual fixed fees and proposed withholding taxes on winnings reduce attractiveness. |

| Operational Requirements | 15% | 0.0/1.5 | Status: Excessive. Mandatory physical office (-0.5). Mandatory resident staff (-0.25). Majority local ownership requirement (-0.5). Data storage within Jordan required (-0.25). These requirements destroy operational flexibility. |

| Market Environment | 10% | 0.0/1.0 | Status: Difficult. Strict advertising bans (-0.5). Risk of criminal prosecution (-0.25). Social/Religious hostility toward the industry (-0.25). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.0/4.0 | Status: Grey/Restricted. Technically illegal under general laws, though winnings are not currently taxed. Online activity is officially prohibited (-1.5), creating legal ambiguity and risk for users. |

| Practical Accessibility | 30% | 1.5/3.0 | Status: Limited. VPNs may be required. While banks exist, proactive financial monitoring (-0.5) and potential blocking of gambling codes restrict seamless payments. 90% internet penetration is the only positive factor. |

| Player Penalties | 20% | 0.5/2.0 | Status: Risk of Fines/Social Penalties. While mass arrests of players are rare, the legal framework allows for penalties. Social stigma is high. Strict AML/KYC enforcement could flag players to authorities. |

| Market Availability | 10% | 0.2/1.0 | Status: None. Zero licensed online operators. Players are forced to use unregulated offshore sites, which are targets for blocking. |

🔍 Key Highlights

Strengths (Theoretical Only)

- Young Demographic: Median age of 23.8 years suggests a tech-savvy potential user base.

- High Connectivity: 90% internet penetration and 96% mobile penetration provide strong technical infrastructure.

- Proposed Tax Rates: If enacted, 15-25% GGR is reasonable compared to European standards.

⛔️ CRITICAL RISKS AND CHALLENGES

- Ownership Restrictions: The requirement for majority local ownership (51%+) makes this market uninvestable for major international PLCs who require control.

- Criminal Liability: The threat of imprisonment for non-compliance is a non-starter for most corporate risk frameworks.

- No Active Market: There are currently zero licensed online operators. The “market size” is entirely projected/speculative.

- Advertising Bans: You cannot broadcast ads. Digital ads are severely restricted. How will you acquire customers?

- Cultural Hostility: In a conservative jurisdiction, gambling is often one political decision away from a total crackdown.

- Operational Burden: Requiring local servers, local offices, and local staff for a market of only 11 million people (with low GDP per capita) ruins unit economics.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: High. $150k+ setup, plus physical office leases and local staff salaries before launch.

Monthly Operating Costs: High due to mandatory local office and resident staff requirements.

Effective Tax Rate on Revenue: Est. 40%+ (20% avg GGR + 20% Corporate + Withholding taxes).

Customer Acquisition Cost: Likely High ($200+) due to advertising bans forcing reliance on expensive affiliate/SEO networks.

Profitability Assessment: POOR. The combination of a small population (11.1m), low GDP per capita ($4,100), majority local partner requirement, and high operational overhead makes profitability extremely difficult. This is a “prestige” or “local monopoly” play, not a viable open market.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Criminal prosecution, domain seizure, indefinite blacklisting. |

| Local Partners/Staff | HIGH | Immediate physical liability, imprisonment risk if compliance fails. |

| Affiliates/Advertisers | HIGH | Promotion of illegal services can lead to fines and criminal charges. |

| Payment Processors | HIGH | Processing illicit financial flows (gambling funds) triggers AML penalties. |

| Company Directors | CRITICAL | Personal liability for regulatory breaches, potential travel bans/detention. |

🚨 Extradition and International Enforcement

Extradition Treaties: Jordan maintains extradition treaties with several nations. While not typically aggressive on cross-border gambling extradition, the criminal nature of the law makes this a risk.

Enforcement History: Enforcement is described as “proactive” with “cross-agency collaboration.” This suggests a high likelihood of domestic crackdowns on any physical presence or local assets.

Travel Risk: High. Executives of non-compliant operators should avoid traveling to or transiting through Jordan due to the risk of detention.

📋 Final Verdict

Jordan receives an Operator Ease Score of 1.4/10 and a Player Access Score of 3.2/10, resulting in an overall market attractiveness rating of 2.3/10.

HONEST ASSESSMENT: Jordan is currently a speculative trap. While legislation is being discussed, the current reality is that online gambling is prohibited, criminal penalties include imprisonment, and the proposed framework requires you to surrender majority ownership to a local partner. There is no first-mover advantage here that outweighs the risk of operating in a strict jurisdiction with no active licenses. Do not enter until the first license is actually issued and the ownership rules are clarified.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry ONLY If You Are:

- A local Jordanian conglomerate with strong government ties.

- Willing to accept a minority stake (49%) in a joint venture.

- Able to sustain 2+ years of losses while regulations finalize.

❌ Definitely Avoid If You Are:

- An International PLC: Majority local ownership rules likely violate your governance standards.

- An Online Casino Operator: The legal status of casino games is highly precarious compared to sports betting.

- Risk-Averse: The threat of imprisonment and criminal charges is real.

- Looking for Quick ROI: Small GDP and high setup costs mean a long payback period.

⚠️ BOTTOM LINE: The market is theoretically opening but practically closed. The “Majority Local Ownership” clause alone renders this market unviable for most international operators.

What’s the current commission structure for affiliates in Jordan’s emerging iGaming market?

Regarding commission structures, Jordan’s iGaming market is still evolving, but we can expect a revenue share model similar to other emerging markets, with a potential CPA structure for new player acquisitions. However, specific details will depend on the final regulatory framework and operator agreements.

Thanks for the insight! What about player lifetime value in the Jordanian market? How can affiliates optimize their content strategies for better conversions?

Player lifetime value in Jordan will depend on various factors, including the regulatory environment, market competition, and player preferences. Affiliates can optimize their content by focusing on educational materials, promoting responsible gaming practices, and leveraging social media platforms popular among Jordanian players.

Considering Jordan’s strict regulatory oversight, I’m planning my betting calendar around sports seasons. How do preseason preparations and injury tracking impact the market? Are there any local sports data sources I can leverage for better insights?

For sports betting in Jordan, preseason preparations and injury tracking are crucial. Local data sources might be limited, but leveraging international sports analytics platforms can provide valuable insights. Additionally, considering the cultural and regional preferences of Jordanian bettors can help in predicting market trends.