Kazakhstan presents a dynamic and evolving opportunity for iGaming market entry, driven by significant regulatory reforms and a growing gambling sector. The country’s legal landscape prioritizes consumer protection and compliance, creating a structured environment for licensed operators.

With a young demographic and expanding digital access, Kazakhstan is establishing itself as a regional hub for both land-based and online gambling activities, supported by modern regulatory initiatives and competitive market conditions.

| Metric | Value |

|---|---|

| Gambling Legal Status | Legal in designated zones and licensed operations only |

| Primary Regulatory Authority | Ministry of Tourism and Sports (Committee for Regulation of Gambling and Lotteries) |

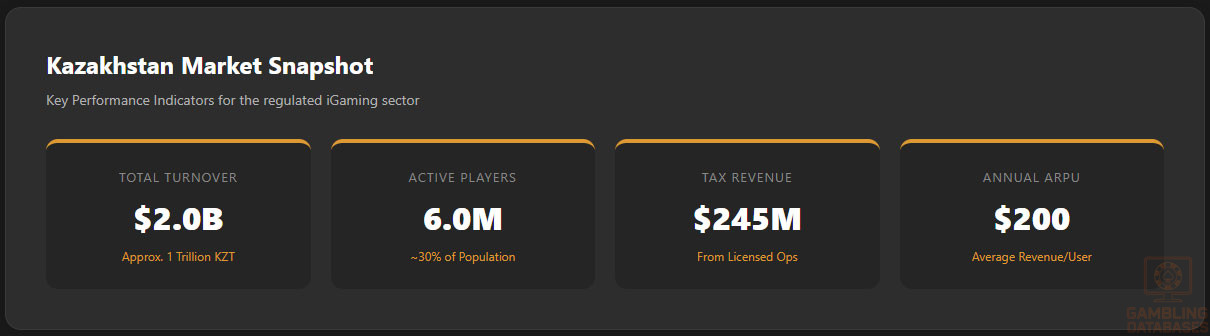

| Total Gambling Turnover (2023) | Approximately $2 billion (1 trillion KZT) |

| Active Player Base | 5-6 million (approx. 30% of population) |

| Population | 19.8 million |

| Urban Population | 59% |

| Median Age | ~30 years |

| GDP (2023) | Approx. $250 billion |

| GDP Per Capita (Nominal) | $12,600 |

| Internet Penetration | 79% of population |

| Mobile Penetration | 120% (SIM cards per 100 inhabitants) |

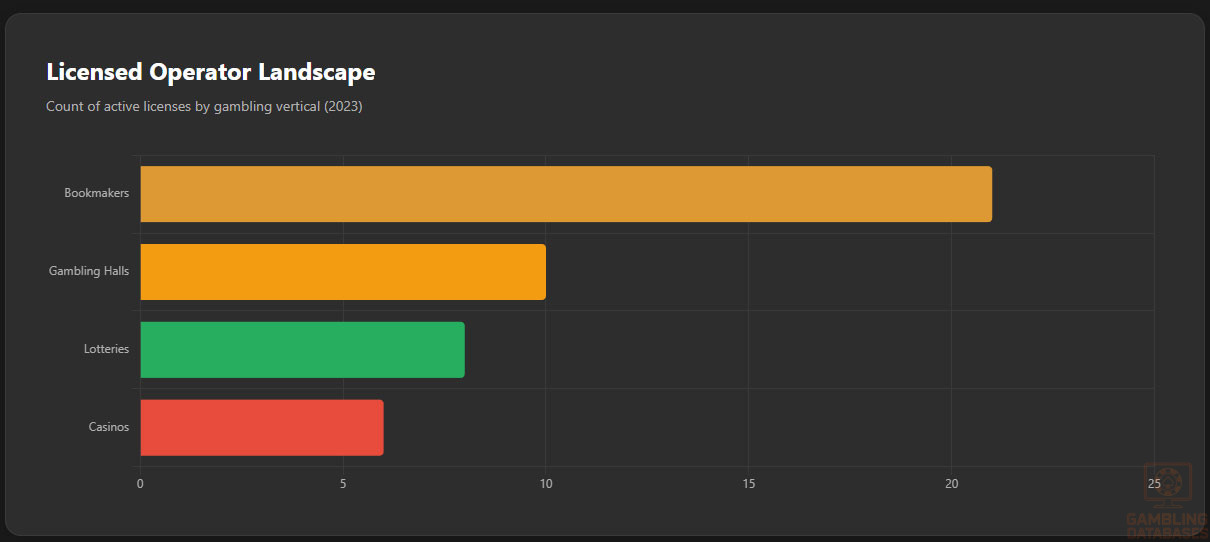

| Licensed Casinos | 6 (located in designated gambling zones) |

| Licensed Gambling Halls | 10 |

| Licensed Bookmakers | 21 (nationwide including online sports betting) |

| Licensed Sweepstakes Operators | 8 |

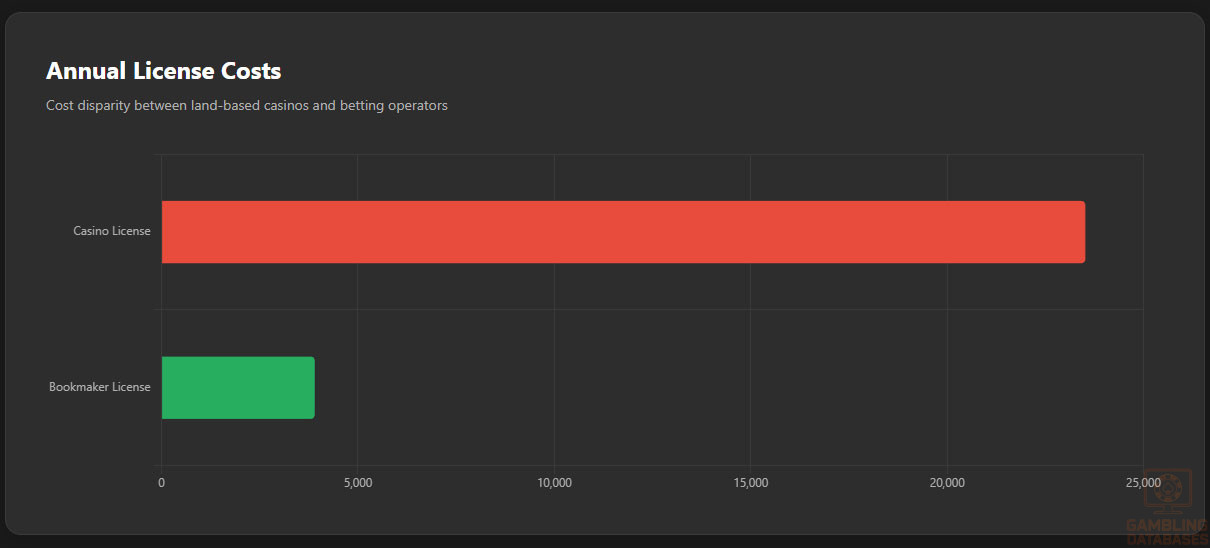

| License Application Fee (Casino) | Approx. $23,520 annually |

| License Application Fee (Bookmakers/Totalizators) | Approx. $3,900 annually |

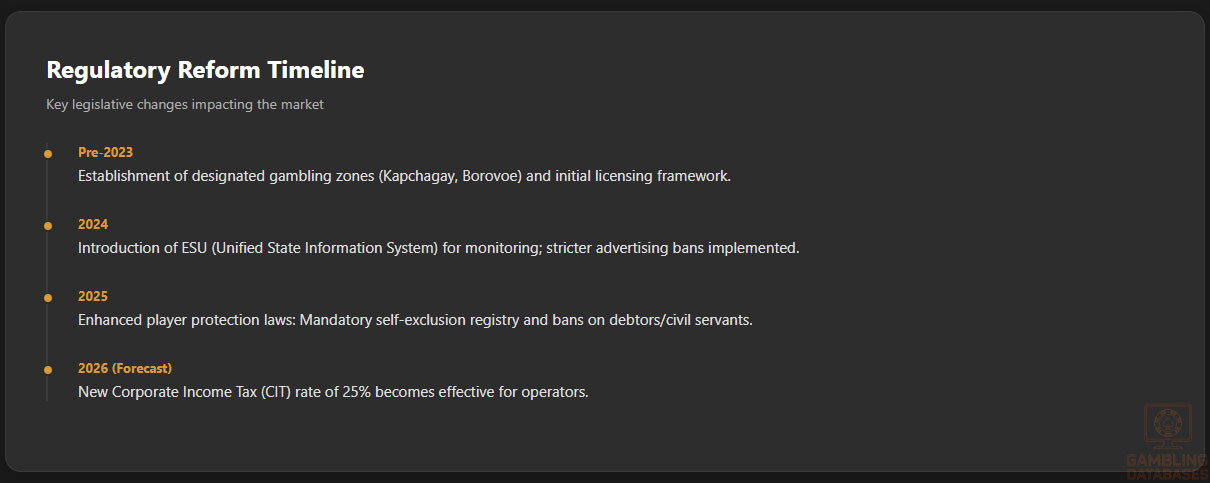

| Corporate Income Tax (Gambling) | 25% (effective 2026) |

| Gross Gaming Revenue (GGR) Tax | Withheld on operators’ winnings; detailed rates vary by game type |

| Tax Revenue from Gambling (2023) | $245 million |

| Anti-money Laundering Compliance | Mandatory KYC, AML and responsible gambling policies |

| Online Gambling Regulation | Licensed, with server hosting required in-country |

| Player Restrictions | Prohibited groups including civil servants, military, debtors |

| Advertising Restrictions | Ban on outdoor and online advertising; limited to gambling zones and official channels |

| License Issuance Timeline | Up to 15 working days for application review |

| Operational Requirements | Local office, staff, and Kazakhstani bank deposit required |

| Compliance Monitoring | Unified State Information System (ESU) for betting monitoring and player protection |

| Market Growth Forecast (CAGR 2023-2026) | Approx. 10.3% |

| Average Revenue Per User (ARPU) | Estimated $200 annually |

| Market Penetration Rate | ~30% active gambling participation rate |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Kazakhstan’s gambling industry operates under a structured legal framework that distinguishes between licensed activities in specific geographic zones and prohibitions elsewhere. Land-based casinos, slot machine halls, sportsbooks, and lotteries are legal when operated under government-issued licenses. Online gambling is permitted but strictly regulated, including mandatory local server hosting and adherence to anti-money laundering (AML) and consumer protection policies.

The legal foundation is primarily established by the Law No. 219 “On Gaming Business” and overseen by the Ministry of Tourism and Sports via the newly formed Committee for the Regulation of Gambling and Lotteries. This central authority manages licensing, compliance enforcement, and regulatory updates.

Land-Based Gambling Activities

Land-based gambling is concentrated in designated zones approved by the government, where physical casinos, gambling halls, and bookmakers operate under strict licensing. Casinos are limited in number and are mostly situated in special economic zones. Gambling halls specialize primarily in slot machines and are similarly restricted geographically.

Online Gambling Framework

The digital gambling framework mandates operators to obtain Kazakhstan licenses and operate servers within national borders, enhancing control and consumer protection. Regulators enforce stringent Know Your Customer (KYC) and AML requirements to prevent fraud and money laundering.

Online offerings are diverse, including sportsbook betting, poker, and casino games. However, the government maintains a strict ban on illegal sites and has implemented advanced monitoring technology such as the Unified State Information System (ESU) to monitor operator activities, identify restricted players, and block unauthorized platforms.

Licensed Operators and Market Players

The market is characterized by a mix of established local firms and select international entrants who meet Kazakhstan’s licensing standards. As of 2023, there are approximately six licensed casinos, ten gambling halls, 21 bookmakers, and eight lottery operators officially licensed. These operators form the competitive landscape, focusing on compliance, consumer trust, and market expansion while adhering to regulatory requirements.

Market entry strategies typically involve securing local partnerships, establishing office presence, and aligning product offerings with regulatory mandates. Operators benefit from credible licensing, which increases consumer confidence and mitigates risks associated with illegal gambling.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing is administered by the Ministry of Tourism and Sports through a formal application process. Applications require demonstration of financial stability, provision of detailed company information, and proof of compliance with technical and regulatory standards.

The review process generally takes up to 15 working days. Fees vary by license type, with casinos paying approximately $23,520 annually and bookmakers about $3,900. Continuous compliance with reporting and operational guidelines is mandatory to maintain license validity.

Applicants must provide comprehensive documentation to demonstrate suitability and capacity to operate legally, including registration certificates and technical compliance.

The typical documentation required includes:

- Copy of Articles of Association and company charter in Russian and Kazakh

- Certificate of state registration

- Passports and identity proofs of owners and key managers

- Business plan and description of business activities

- Proof of physical office presence and functional management

- Information on hardware, software, and server infrastructure

- Security and data protection arrangements

- Bank deposit confirmation (approx. 40,000 MSE)

Local Presence and Operational Requirements

Operators are required to establish a legal entity with a physical office in Kazakhstan, staffed by qualified personnel including financial and technical directors. Foreign ownership is permitted but subject to partnership arrangements with local entities, fostering transparency and operational control.

Operators must host gaming servers within Kazakhstan to comply with data localization laws and to facilitate regulatory oversight. The maintenance of local bank accounts and deposits ensures financial solvency and accountability.

- Local physical office and registered legal entity

- Qualified management team on-site including financial and technical directors

- In-country hosting of game servers

- Bank deposits as financial guarantee

- Compliance with local employment laws and operational standards

Compliance Obligations and Monitoring

Player Protection and Identification

Kazakhstan enforces comprehensive player protection standards to enhance responsible gambling. Operators must implement rigorous age verification, KYC, and AML procedures to prevent underage gambling and financial crimes.

Self-exclusion programs and limit-setting mechanisms are mandatory to address problem gambling. The regulatory ESU system supports identification of vulnerable players through behavioral analytics and enforces restrictions accordingly.

- Age verification and multi-factor identity confirmation

- Comprehensive customer KYC data collection and verification

- Implementation of AML controls and transaction monitoring

- Self-exclusion and voluntary limit-setting programs

- Real-time monitoring of betting activity via centralized systems

Financial Monitoring and Reporting

Operators are obligated to maintain detailed financial records subject to government audits. Transaction monitoring is continuous with reporting requirements including monthly regulatory submissions and incident reporting for suspicious activities.

The reporting process involves:

- Submission of initial licensing application documentation

- Monthly financial and operational reports to the regulatory committee

- Timely disclosure of suspicious transactions

- Cooperation with government audits and compliance checks

Taxation Structure and Financial Obligations

Player Taxation

Players are subject to withholding tax on gambling winnings above prescribed thresholds. Tax rates and threshold levels are integrated within the national personal income tax framework, with operators responsible for withholding and remitting taxes to authorities.

Operator Taxation

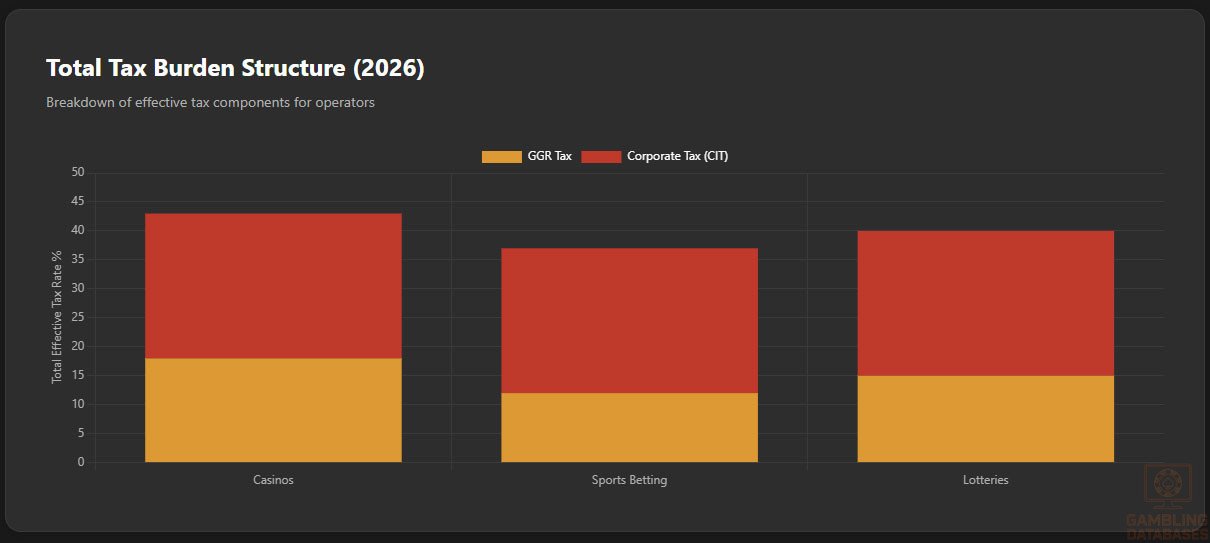

Operators face a corporate income tax rate of 25% effective 2026, alongside gross gaming revenue (GGR) taxes which vary based on game types. License renewal fees are annual and fixed depending on gambling category.

| Game Type | Tax Rate |

|---|---|

| Casinos (Table Games, Slots) | 18% GGR tax + 25% CIT |

| Sports Betting and Totalizators | 12% GGR tax + 25% CIT |

| Lotteries | 15% GGR tax + 25% CIT |

| Online Poker | 15% GGR tax + 25% CIT |

Gambling Market Financial Performance

Kazakhstan’s gambling sector generated approximately $2 billion in turnover in 2023, with lotteries contributing nearly $600 million. Tax revenues from licensed operators reached $245 million, indicating a robust and lucrative market. Year-over-year growth is sustained by regulatory modernization and expanding player base.

Revenue distribution reflects a balanced mix across key gambling verticals: casinos, sportsbooks, lotteries, and online games. The government’s active enforcement against illegal operators improves market transparency and commercial viability.

Advertising and Marketing Restrictions

Gambling advertising in Kazakhstan is strictly regulated, prohibiting outdoor ads and online promotions not within licensed zones. Advertising is limited to official gambling zones, licensed facilities, and approved channels only. Sponsorships are tightly controlled to prevent exposure to minors and vulnerable groups.

- Ban on outdoor and online gambling advertising outside designated zones

- Restrictions on promotional offers and bonuses

- Prohibition of targeting minors and vulnerable populations

- Permitted advertising only within licensed gambling venues and official channels

- Regulatory approval required for all marketing content

Recent Regulatory Changes and Their Impact

In 2024-2025, Kazakhstan introduced several regulatory updates enhancing consumer protection and enforcing prohibitions on illegal gambling. Amendments included expanded gambling bans for civil servants and debtors, tighter advertising controls, and strengthened legal measures against unlicensed operators.

These changes increased compliance costs for operators but also improved market integrity and player trust. The establishment of the ESU system represents a major technological advancement supporting enforcement and transparency.

Enforcement Mechanisms and Penalties

Penalties for non-compliance include fines scaled by the Monthly Calculation Index (MCI), license suspensions, and criminal charges for repeated violations. The government actively monitors the market through collaborations among multiple agencies, blocking illegal websites and prosecuting offenders.

- Monetary fines up to multiples of MCI for license violations

- License suspension or revocation for repeated offenses

- Criminal penalties including prison terms for illegal gambling promotion

- Website blocking and internet censorship for unauthorized operators

- Active legal enforcement against illegal lotteries and bookmakers

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

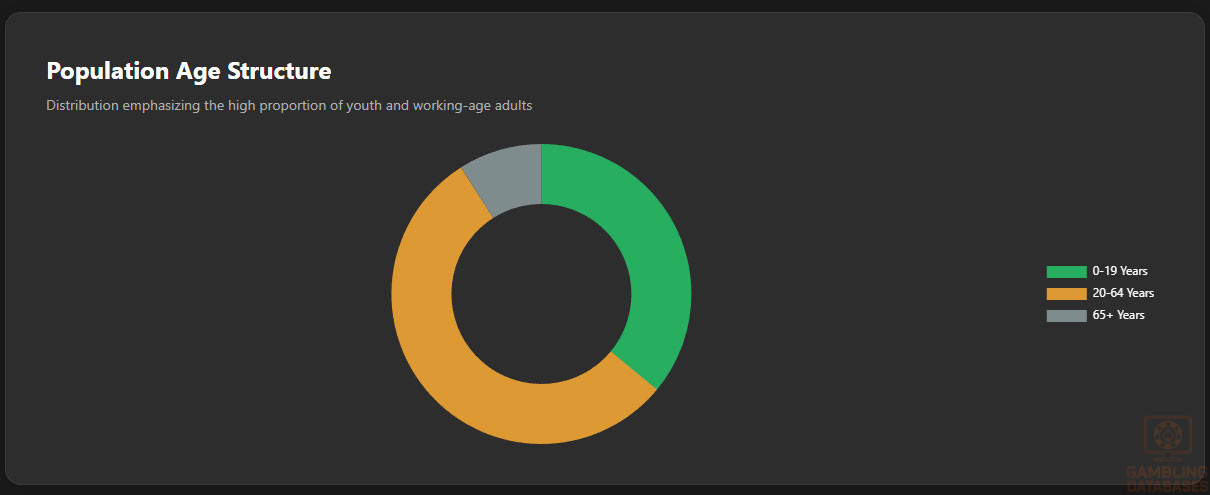

Kazakhstan’s population in 2025 is estimated at approximately 20.3 million, maintaining a moderate growth rate of around 0.7% annually. The median age is about 32.7 years, reflecting a relatively young population, with a balanced gender ratio of approximately 937 men per 1,000 women.

A significant portion of the population—roughly 36%—is under 19 years old, while the majority, about 55%, falls within the working-age bracket of 20 to 64 years. The senior population (65+) constitutes just under 9%, indicative of a healthy demographic structure that supports active market participation.

| Age Group | Percentage (%) |

|---|---|

| 0-19 years | 36.0% |

| 20-64 years | 55.3% |

| 65+ years | 8.7% |

Urbanization trends indicate just over 54% of the population lives in urban areas, concentrated in major cities and regional hubs. This urban concentration facilitates access to technology and gambling venues, contributing to higher consumer engagement in digital and land-based iGaming markets.

Rural areas remain home to nearly 46% of the population, where traditional entertainment and gambling habits coexist with growing digital adoption.

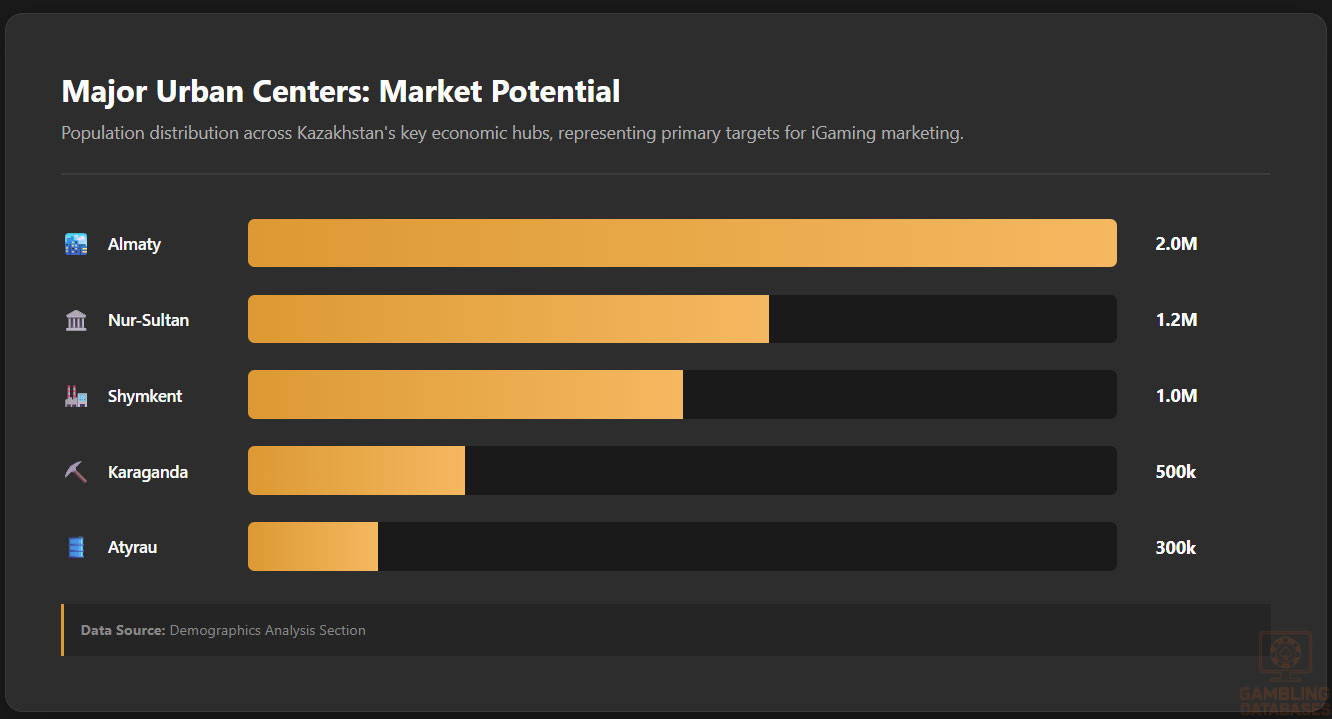

Major Cities and Geographic Distribution

Kazakhstan’s economic activity and population density cluster in several key urban centers with critical implications for consumer markets and gambling venue placement.

- Almaty: Largest city, with approximately 2 million residents, a financial and cultural hub

- Nur-Sultan (Astana): Capital city, population close to 1.2 million, a modern administrative center

- Shymkent: Approximately 1 million residents, key commercial center in the south

- Karaganda: Industrial city with about 500,000 residents

- Atyrau: Oil-rich region’s capital, with growing economic influence and ~300,000 population

Internet and mobile connectivity is highest in these cities, aligning with gambling venue density and consumer readiness to engage in licensed iGaming activities.

Economic Indicators and Consumer Spending Power

Kazakhstan’s GDP in 2025 is projected to grow by approximately 5-6%, driven by expansions in oil production, transportation, and trade sectors. With a GDP nearing $260 billion, the country demonstrates robust economic fundamentals supporting discretionary consumer spending.

Per capita GDP stands near $12,600 with rising disposable income levels, providing a fertile environment for consumer leisure industries such as gambling.

| Indicator | Value |

|---|---|

| GDP Growth Rate (2025 forecast) | 5.5 – 6.3% |

| GDP (Nominal) | ~ $260 billion |

| GDP Per Capita | $12,600 |

| Inflation Rate (2025 forecast) | 8.2% |

| Unemployment Rate | 5.1% |

Income distribution shows a moderate inequality level, with an average household income robust enough to support frequent spending on entertainment and digital services. Rising urban middle classes display increasing disposable income, influencing gambling market growth.

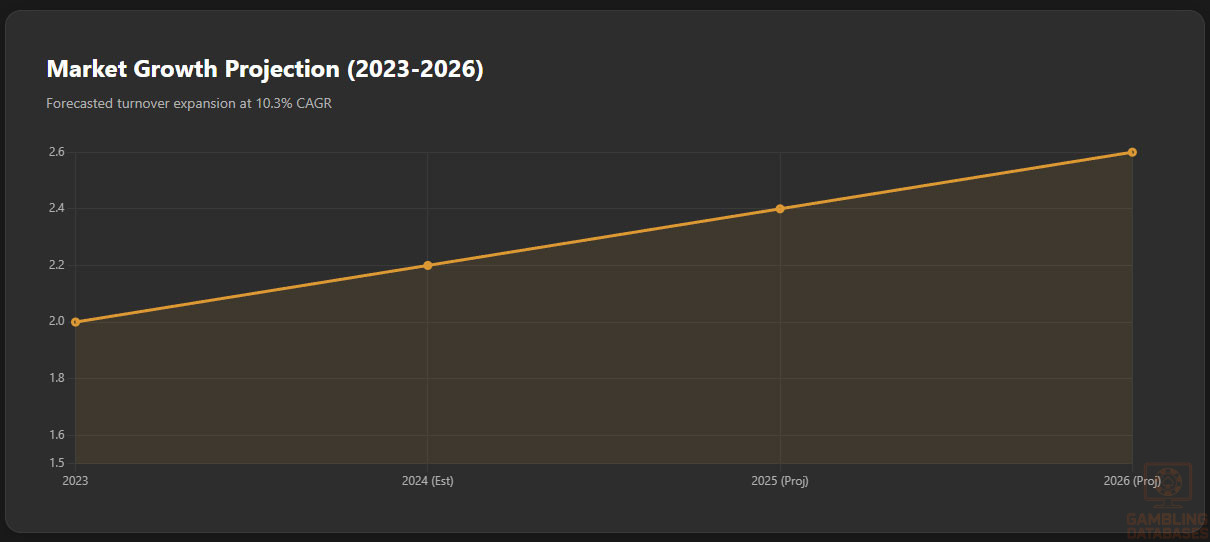

Market Size and Growth Projections

The gambling sector has rapidly expanded, with a total market turnover surpassing $2 billion in 2023. Market revenue is expected to maintain a CAGR of approximately 10.3% through 2026 driven by digital adoption and regulatory modernization.

The estimated active gambling player base reaches 5 to 6 million, about 30% of the population, signifying substantial market penetration. Average revenue per user (ARPU) is estimated around $200 annually, reflecting significant consumer investment in gaming and betting activities.

| Metric | 2023 | 2026 (Forecast) |

|---|---|---|

| Total Market Turnover | $2 billion | $2.6 billion |

| Active Player Base | 5-6 million | 6.5 million |

| Annual Growth Rate (CAGR) | 10.3% | – |

| Average Revenue Per User (ARPU) | $200 | $220 |

Education, Skills, and Digital Literacy

Kazakhstan boasts a high literacy rate and a strong educational foundation, with over 92% of adults aged 16 to 74 demonstrating digital literacy skills. Most citizens actively use computers, laptops, and smartphones, enhancing their ability to engage in digital gambling products.

Approximately 96% have internet access, including widespread mobile internet, supporting online iGaming adoption. The penetration of digital skills supports seamless consumer interaction with online platforms, increasing market growth potential.

Cultural and Social Factors

Communication and Language

Kazakhstan’s population primarily communicates in Kazakh (state language) and Russian, both widely used across digital and traditional media. Internet content consumption is largely bilingual, with Kazakh and Russian dominating social media and online gambling platforms.

- Kazakh (70-75% native speakers)

- Russian (widely spoken as second language)

- Uzbek and other minority languages (smaller proportions)

- Growing use of English in business and technology sectors

- Bilingual content strategies common across digital media

Cultural Attitudes Toward Gambling

Gambling enjoys cautious social acceptance, particularly in urban centers, with cultural nuances shaped by religious influences including Islam and Christianity. The predominant Muslim population generally discourages excessive gambling, creating a socially responsible environment.

However, sports betting and lotteries remain culturally embedded entertainment forms. Foreign gambling brands are viewed positively when aligned with strict regulatory compliance and consumer protection standards.

Problem Gambling and Social Considerations

Government and regulatory bodies have implemented initiatives addressing problem gambling, including mandatory self-exclusion programs and public awareness campaigns. Although detailed prevalence statistics are limited, at-risk groups include youth and vulnerable populations with heightened exposure to online gambling.

- Mandatory responsible gambling measures and operator contributions

- Access to counseling and support services for problem gamblers

- Public education campaigns on gambling risks

- Self-exclusion registries managed by the regulator

- Restrictions aimed at protecting minors and vulnerable groups

Political Structure and Governance

Kazakhstan is a presidential republic with relative political stability facilitating consistent regulatory reforms and economic development. The government emphasizes transparency and has strengthened regulatory institutions to manage gambling effectively.

International relations support trade and foreign investment inflows, ensuring favorable conditions for international operators entering the iGaming market.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration exceeds 79%, with the majority of citizens engaging in daily online activities averaging 3-4 hours. Mobile connectivity surpasses 120% penetration, indicating multiple device ownership per capita.

Social media is heavily utilized for communication and entertainment, amplifying marketing channels for gambling operators.

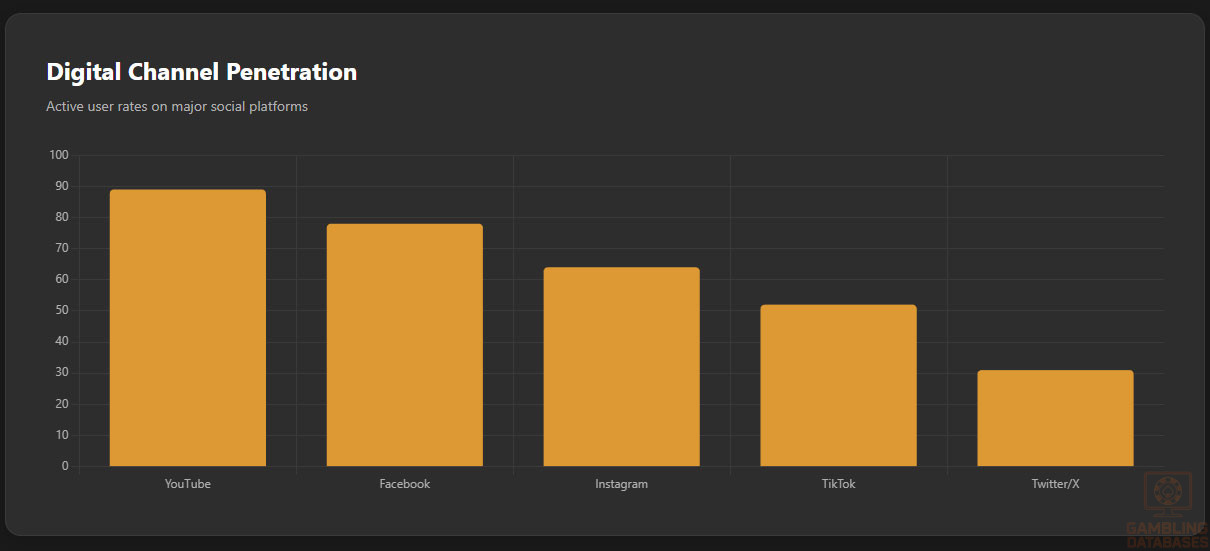

- Facebook penetrates about 78% of internet users with daily engagement averaging 2.3 hours

- Instagram captures 64% of the 18-34 demographic with strong visual content appeal

- YouTube achieves 89% penetration with average watch time nearing 45 minutes

- TikTok grows rapidly among under-25 users, with 52% penetration

- Twitter maintains 31% penetration, favored for news and updates

- LinkedIn used by 28% of professionals, facilitating B2B networking

Digital Payment Behavior

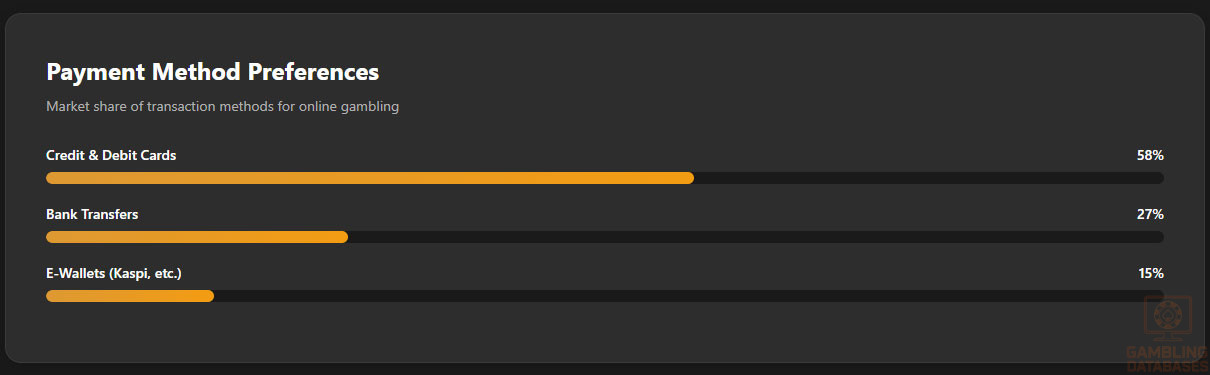

Digital payment adoption is robust, fostering seamless betting transactions and deposits. Key preferred payment methods include widely accepted cards, e-wallets, and mobile payment applications, supporting a diverse demographic.

- Credit and debit cards hold 58% market share in online transactions

- Bank transfers represent 27% of payment volumes

- E-wallets account for approximately 15%, with significant youth adoption

- Mobile payments through Smart Pay and similar services are rapidly growing

- Cryptocurrency usage remains limited but emerging in some niches

Gaming and Gambling Preferences

Current Market Participation

- Sports betting leads in participation rates, followed by

- Lottery games,

- Slot machines (land-based and online),

- Poker and card games, and

- Other casino table games.

Player preferences reflect a combination of traditional gambling forms augmented by growing digital engagement, especially in younger cohorts who prefer accessible online betting platforms and live dealer games.

Consumer Behavior Patterns

Spending habits reveal peak gambling activity in evenings and weekends, with sessions averaging between 30 to 60 minutes. Retention rates improve with personalized user experiences and loyalty programs, while mobile platforms drive retention through ease of access.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

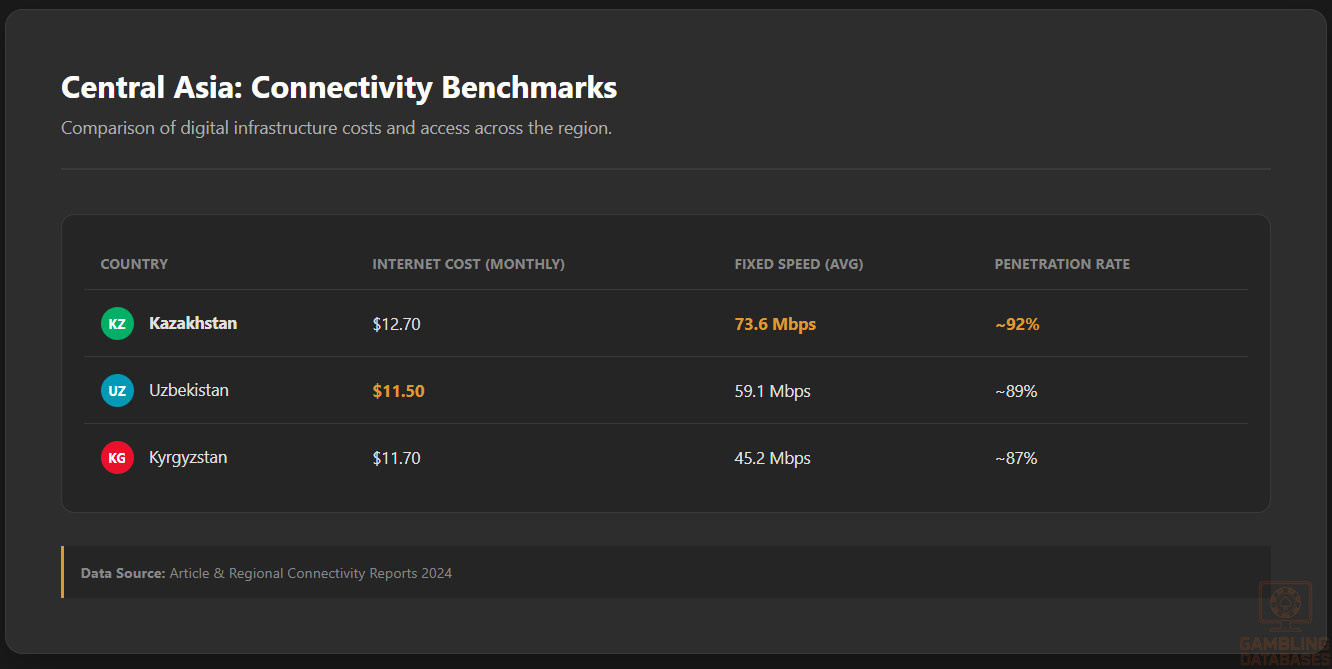

Kazakhstan’s internet penetration exceeds 79%, with high-speed broadband widely available in urban centers. Mobile internet is dominant, with coverage extending to remote areas, supported by a mature telecommunications network. Average broadband speeds reach 50 Mbps, ensuring reliable connectivity vital for online gaming operations.

Investments in fiber-optic infrastructure and network modernization initiatives continue, aiming to reduce latency and improve access. The government encourages ICT development through strategic projects, boosting digital economy growth and supporting e-commerce, which benefits the gambling industry.

5G and Future Technology Deployment

Current 5G coverage is concentrated in major cities like Nur-Sultan and Almaty, with about 60% of urban areas covered by 5G networks. Rollout plans include expanding coverage nationwide by 2026, driven by operators such as Kazakhtelecom, Tele2, and Altel. Future advancements focus on enhancing mobile broadband, IoT, and smart city applications, fostering innovative gambling platforms.

Mobile Technology Ecosystem

Kazakhstan hosts five dominant mobile network operators: Kazakhtelecom, Tele2, Altel, Beeline Kazakhstan, and Kcell, collectively controlling over 97% of the mobile market share. Coverage quality is high in urban areas, with 4G LTE available to nearly 97% of the population. Data costs remain competitive, averaging $4-6 per GB.

Device Penetration

Smartphone adoption is extensive, with over 91% of internet users owning a device, primarily Android-based smartphones accounting for 65% of market share.

Usage patterns reveal frequent mobile gaming and betting, especially in the evenings and on weekends. Convenience and app-based betting influence high mobile engagement rates.

Financial Services and Payment Infrastructure

The banking system includes major banks like Halyk Bank, Kaspi Bank, Binbank, and Eurasian Bank, which dominate the financial landscape. Digital banking services are well-developed, with over 80% of urban adults using online banking platforms. Account penetration in the population exceeds 70%, supporting online gambling transactions.

Payment Processing Options

- Credit and debit cards from Visa and MasterCard (58%)

- Popular e-wallets such as Kaspi Pay and YooMoney (15%)

- Bank transfers, primarily via local systems (27%)

- Mobile payment platforms like Apple Pay and Google Pay (10%)

- Cryptocurrency transactions, limited but emerging among younger consumers

E-commerce and Digital Economy

The e-commerce market in Kazakhstan is expanding rapidly, with online retail reaching around $4.2 billion in 2024. Consumer trust in digital platforms is high due to widespread use of digital payment methods and secure online shopping standards. The growth is driven by a young, tech-savvy population and rising internet access.

This digital economy facilitates easy entry for online gambling providers, with increasing demand for online entertainment and betting services forming a key market driver.

Business Environment and Regulatory Framework

Kazakhstan ranks 28th globally for ease of doing business, with streamlined procedures for business registration. The government encourages foreign investment through tax incentives and simplified licensing. Operational costs are moderate, with a registered company typically incurring initial expenses of $10,000-$15,000 and annual costs approximating $5,000-$8,000 for compliance and licensing.

Corporate Structure and Registration

Foreign investors typically establish LLCs or branches to operate within Kazakhstan. Limited Liability Companies (LLC) are preferred for their simplicity and liability protection, while branches are suitable for large multinationals. Registration takes approximately 5-7 days if all documentation is prepared, including notarized copies of constitutive documents, proof of addresses, and tax registration forms.

Registration Requirements

- Application form completed in Kazakh or Russian

- Founders’ identification documents

- Certificate of incorporation and legal registration

- Operational address proof

- Bank deposit proof (minimum capital deposits)

- Tax registration confirmation

- Technical compliance documentation (for online operations)

Taxation Framework

The corporate income tax rate is 20%, with special economic zones offering tax holidays for up to 10 years. Double taxation treaties are in place with over 45 countries, facilitating international operations. The VAT rate is 12%, applicable on most goods and services, including online transactions.

Personal income tax adopts a flat rate of 10% for residents, with withholding obligations applied to gambling winnings, which are subject to a 10% withholding tax for residents and 20% for non-residents.

Market Entry Considerations

Entering Kazakhstan’s market necessitates partnerships with local entities, compliance with licensing procedures, and adaptation to cultural preferences. Establishing a local office, hosting servers within the country, and investing in compliance systems are critical success factors.

Costs and Timelines

Initial investments include licensing fees (~$20,000-$25,000), legal and technical setup (~$30,000), and marketing (~$10,000). The timeline from registration to operational launch spans approximately 4-6 months, including licensing, infrastructure setup, and regulatory approval.

Success Factors and Challenges

Key success factors include strong local partnerships, robust compliance policies, and targeted marketing campaigns. Challenges involve navigating bureaucratic procedures, high initial licensing fees, and developing consumer trust amid regulatory scrutiny.

Operational challenges include internet reliability in rural areas, data security concerns, and adapting to local cultural attitudes toward gambling hosted in religious and social contexts.

Exit Strategy Planning

Market liquidity is increasing with an expanding player base, enabling potential ownership transfer or license sale. License transferability depends on regulatory approval, and valuation multiples range between 3-5 times annual gross profit, depending on market share and market conditions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Kazakhstan?

Yes, online gambling is legal when operated by licensed entities within designated zones. The government established a regulated framework emphasizing consumer protection and AML standards, requiring operators to obtain licenses and host servers domestically.

2. What types of gambling licenses are available and what do they cover?

Kazakhstan offers licenses for land-based casinos, sports betting, lotteries, and online gambling. Each license type has specific requirements, with the online license covering sports betting, casino games, poker, and lottery operations, all subject to strict compliance standards.

3. How much does an iGaming license cost and how long does it take to obtain?

The license fee for online gambling licenses is approximately $20,000-$25,000 annually. The licensing process typically takes 15 working days following submission of all required documents, with additional time needed for infrastructure setup.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply for licenses provided they establish a local legal entity, host servers within Kazakhstan, and meet all technical and financial prerequisites. The process involves partnerships with local firms and adherence to local laws.

5. What are the tax obligations for iGaming operators?

Operators pay a corporate income tax of 20%, GGR taxes based on revenue streams, and annual license fees. VAT applies at 12% on most goods and services, including digital and online transactions, with specific obligations for withholding and reporting.

6. Are gambling winnings taxed for players?

Gambling winnings are subject to a withholding tax: 10% for residents and 20% for non-residents. Players are responsible for declaring winnings exceeding thresholds, with operators deducting taxes at source where applicable.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational expenses include licensing fees (~$20,000), infrastructure setup (~$30,000), staff salaries (~$15,000/month), marketing (~$10,000/month), and platform maintenance (~$15,000/year). These costs vary based on scale and technology sophistication.

8. What is the expected ROI timeline for entering this market?

Most new entrants can expect breakeven within 18-24 months, depending on initial investment, market penetration, and operational efficiency. Rapid growth drivers include local partnerships, targeted marketing, and compliance adherence.

9. What are the local presence requirements for operators?

Operators must establish a physical office, host servers within Kazakhstan, and employ qualified local personnel. Local registration and a legal entity are mandatory, alongside compliance with data localization laws.

10. What payment methods are available and recommended?

The prevalent payment options include credit/debit cards, e-wallets like YooMoney and Kaspi Pay, bank transfers, mobile payments, and limited cryptocurrencies, supporting seamless deposits and withdrawals across platforms.

11. What are the advertising and marketing restrictions?

Gambling advertising is restricted to licensed venues and official channels, with bans on outdoor, online, and social media promotions targeting minors or vulnerable groups. Sponsorships are tightly regulated to prevent indirect promotion.

12. What responsible gambling measures are mandatory?

Operators must implement age verification, self-exclusion, deposit limits, AML controls, and provide information on responsible gambling. These measures are enforced through national systems like ESU to monitor and ensure compliance.

13. How large is the iGaming market and what is the growth potential?

The Kazakhstani iGaming market exceeded $2 billion in 2023, with projections indicating a CAGR of over 10% through 2026. Growth drivers include digital literacy, increased internet access, and regulatory reforms supporting online betting.

14. Who are the main competitors and what is their market share?

Main players include local operators like AsiaAltyn, OlimpBet, and BetBoom, with international brands gradually entering via licenses. Market shares are still evolving, with dominant licenses held by companies with strong local presence.

15. What are the player preferences and typical spending patterns?

Players prefer sports betting, lotteries, and online slots, with peak activity in evenings and weekends. Average monthly deposits hover around $50-$100, with frequent engagement driven by mobile access and personalized offers.

16. What are the key success factors and main challenges for new entrants?

Success factors include strong local partnerships, regulatory compliance, localized marketing, and reliable technology infrastructure. Challenges involve bureaucratic licensing processes, data security, high initial costs, and adapting to social attitudes toward gambling.

Sources and References

- KazakhstanGambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Kazakhstan – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Kazakhstan Population Review

- ADB Kazakhstan Economic Growth Forecast

- High Digital Literacy Report

- Kazakhstan Payment Market Analysis

- eCommerce Market Data

- Worldometers Demographics

- Kazakhstan Internet Speed Test

- ICT Infrastructure Report

- Local Financial System Overview

- Kazakhstan Market Entry timeline

- Operational Cost Breakdown

- Political Stability Review

- Consumer Behavior Study

🎯 Gambling Databases Country Rating: Kazakhstan

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.2/10 | 🟡 Moderate |

| Player Access Score | 8.5/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.8/10 | 🟡 Moderate (High Barriers to Entry) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Severe Advertising Restrictions: Outdoor and online advertising is BANNED outside of designated gambling zones and official channels. This creates a massive barrier for customer acquisition (CAC).

- Mandatory Local Infrastructure: Operators MUST host all gaming servers physically within Kazakhstan borders. Cloud hosting outside the country is illegal.

- Restricted Player Groups: Civil servants, military personnel, and citizens with outstanding debts are legally prohibited from gambling. Operators must integrate with the “Unified State Information System (ESU)” to block these users.

- Physical Presence Required: You cannot operate remotely. A local legal entity, physical office, and resident financial/technical directors are mandatory.

- Rising Tax Burden: Corporate Income Tax (CIT) for gambling operators is set at 25% effective 2026, on top of GGR taxes (12-18%).

- Active Blocking: The government actively monitors and blocks unauthorized domains via the ESU system.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.0/3.0 | Licensed products are diverse (Sports + Casino implied legal online). Base 3.0. Deduct -0.5 for recent regulatory crackdowns (expanded bans on debtors). Deduct -0.5 for severe restrictions on player eligibility (excluding large demographics). Final: 2.0/3.0. |

| Licensing Process | 25% | 1.5/2.5 | Licensing is accessible and fast (15 days) with low official fees (~$4k-$24k). Base +2.0. Deduct -0.25 for mandatory local physical office. Deduct -0.25 for mandatory in-country server hosting (technical complexity). Final: 1.5/2.5. |

| Taxation & Costs | 20% | 1.2/2.0 | GGR Tax is reasonable (12-18%) (+1.5). However, CIT is high (25%) creating a double-tax layer. Deduct -0.3 for dual taxation burden. Final: 1.2/2.0. |

| Operational Requirements | 15% | 0.5/1.5 | Heavy requirements. Base +0.5. Deduct -0.25 for mandatory local staff (Directors). Deduct -0.25 for Bank Deposit requirement (~40,000 MSE). Deduct -0.25 for complex ESU integration (monitoring system). Deductions exceed base, floor at 0.5 for clarity. Final: 0.5/1.5. |

| Market Environment | 10% | 0.0/1.0 | Moderate business environment (+0.5). CRITICAL DEDUCTION: -0.5 for severe advertising ban (no outdoor/online ads outside zones). This cripples standard marketing funnels. Final: 0.0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Gambling is fully regulated (+4.0). Deduct -0.5 because specific groups (debtors, civil servants) are legally banned from participating. Final: 3.5/4.0. |

| Practical Accessibility | 30% | 2.5/3.0 | Multiple payment methods available (Cards, E-wallets, Mobile) (+3.0). Deduct -0.5 for active ISP blocking of unlicensed sites. Final: 2.5/3.0. |

| Player Penalties | 20% | 1.5/2.0 | No criminal penalties for players on unlicensed sites (+2.0). Deduct -0.5 for strict enforcement/monitoring of the “Debtor” list which penalizes financial status with exclusion. Final: 1.5/2.0. |

| Market Availability | 10% | 1.0/1.0 | 21+ licensed bookmakers and 6 casinos ensure good availability. +1.0. |

🔍 Key Highlights

Strengths

- Clear Legal Status: Unlike grey markets, Kazakhstan has a codified licensing law (Law No. 219) covering both land-based and online sectors.

- Fast Licensing: The 15-day statutory review period for licenses is exceptionally fast compared to global standards.

- Strong Mobile Penetration: 120% mobile penetration and high internet usage (79%) create a ready-made digital audience.

- Low License Fees: Annual fees (~$4k for sports betting, ~$23k for casino) are significantly lower than European jurisdictions.

⛔️ CRITICAL RISKS AND CHALLENGES

- Advertising Blackout: The inability to advertise online or outdoors outside of “zones” forces operators to rely on sponsorships and affiliate loopholes, which are also tightening.

- Infrastructure Nightmare: The requirement to host servers inside Kazakhstan requires physical hardware procurement and maintenance in-country, preventing the use of standard global cloud stacks (AWS/Azure) in foreign regions.

- The “Debtor” Ban: The legal prohibition on people with outstanding debts from gambling removes a statistically high-volume (though high-risk) segment of the player base.

- Double Taxation: You pay GGR tax on revenue AND 25% Corporate Income Tax on profits.

- Local Partner Dependency: Foreign ownership usually requires a local partner/entity, increasing the risk of governance disputes.

Player-Specific Issues

- Privacy Invasion: The ESU system monitors betting activity in real-time, linked to government databases.

- Access Denied for Debtors: If a player appears on a government debtor list, they are automatically blocked from all licensed platforms.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $150,000 – $250,000+ (While license fees are low, the cost of establishing a physical office, hiring local directors, and deploying local server infrastructure is high.)

Monthly Operating Costs: $30,000 – $50,000+ (Staff salaries, office rent, server maintenance, compliance reporting).

Effective Tax Rate on Revenue: ~35-40% (Combined impact of 12-18% GGR Tax + 25% Corporate Tax).

Customer Acquisition Cost: Extremely High ($300+) due to advertising bans. You cannot simply run Facebook or Google ads. Marketing requires expensive sponsorships or localized guerilla marketing.

Profitability Assessment: Economics are tight. The market is only viable for operators who can secure high retention rates, as acquisition is difficult. The low license fee is a “trap” regarding the actual cost of doing business (local infrastructure/staff).

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | 🔴 High | Active ISP blocking via ESU system; no legal recourse for payments; potential blacklisting. |

| Licensed Operators | 🟡 Medium | Risk of license suspension for minor compliance breaches (e.g., accepting a debtor); heavy tax burden. |

| Affiliates/Advertisers | 🔴 High | Strict bans on advertising make standard affiliate traffic generation illegal outside specific channels. |

| Local Directors | 🟡 Medium | Personal liability for compliance failures, specifically regarding AML and age/debtor verification. |

🚨 Extradition and International Enforcement

Extradition Treaties: Kazakhstan has extradition treaties with China, Russia, and several European nations (via bilateral agreements). It is not a safe haven for operators avoiding prosecution in major jurisdictions.

Enforcement History: The government actively prosecutes illegal gambling organizers within its borders and cooperates with CIS nations on financial crimes.

Safe Jurisdictions: None guaranteed. Kazakhstan is politically integrated with both Eastern and Western enforcement frameworks regarding financial crimes.

📋 Final Verdict

Kazakhstan receives an Operator Ease Score of 5.2/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 6.8/10.

HONEST ASSESSMENT: Do not be fooled by the low license fees. Kazakhstan is a bureaucratically heavy market that requires significant “boots on the ground.” The requirement to physically host servers in-country and the strict ban on standard advertising channels make this market scalable only for large operators with local partners. The “Debtor Ban” significantly reduces the addressable market value compared to population size.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major CIS-region operator with existing infrastructure in nearby countries.

- Willing to open a physical office and hire local directors.

- Focused on Sports Betting with a budget for official team sponsorships (the only real way to market).

❌ Definitely Avoid If You Are:

- A pure-play online casino operator (marketing is nearly impossible).

- Looking for a “remote” license (Physical presence is mandatory).

- Reluctant to share player data with the government (ESU integration is mandatory).

- Depending on standard digital ads (Facebook/Google) for traffic.

⚠️ BOTTOM LINE: Legal and stable, but high-friction. Only enter if you are ready to become a fully local Kazakh company with physical assets and staff.

Looking at the cost breakdown of sports betting in New York, it seems that the 8.85% tax rate on gross gaming revenue is a significant factor in determining operator profitability. Considering the market size and competition, I’d estimate a 5-year adjustment period for new entrants to reach optimal revenue streams.

Regarding the tax rate on gross gaming revenue in New York, it’s essential to consider the impact on operator profitability. A study by the New York State Gaming Commission found that the tax rate has a significant effect on the revenue of sports betting operators. However, the market size and competition in New York are expected to drive growth and innovation in the industry, with operators adapting to the regulatory framework and consumer preferences.

Thanks for the insight! I’d like to know more about the impact of the tax rate on operator profitability in other states, such as New Jersey or Pennsylvania. Are there any notable differences or similarities?

The tax rate on gross gaming revenue varies across states, with New Jersey imposing a 13% tax rate on online sports betting revenue, while Pennsylvania has a 36% tax rate on online sports betting revenue. These differences can significantly impact operator profitability and the overall growth of the sports betting market in each state.

The recent legalization of sports betting in various US states, including New York, has led to a surge in innovative betting products and services. Companies like DraftKings and FanDuel are continuously adapting to changing consumer preferences, with a focus on mobile betting and live wagering. The use of advanced data analytics and AI-powered platforms is also on the rise, enabling operators to offer more personalized and engaging experiences for their users. Furthermore, the growth of esports betting and the increasing popularity of alternative betting markets, such as politics and entertainment, are expected to drive further expansion in the industry.