Kenya presents a rapidly growing iGaming market driven by increasing internet penetration and mobile usage. Its regulatory framework is evolving to balance innovation with legal oversight, making it an attractive but complex environment for market entry.

Understanding local laws, licensing procedures, and compliance obligations is critical for international operators seeking to establish a presence in the country.

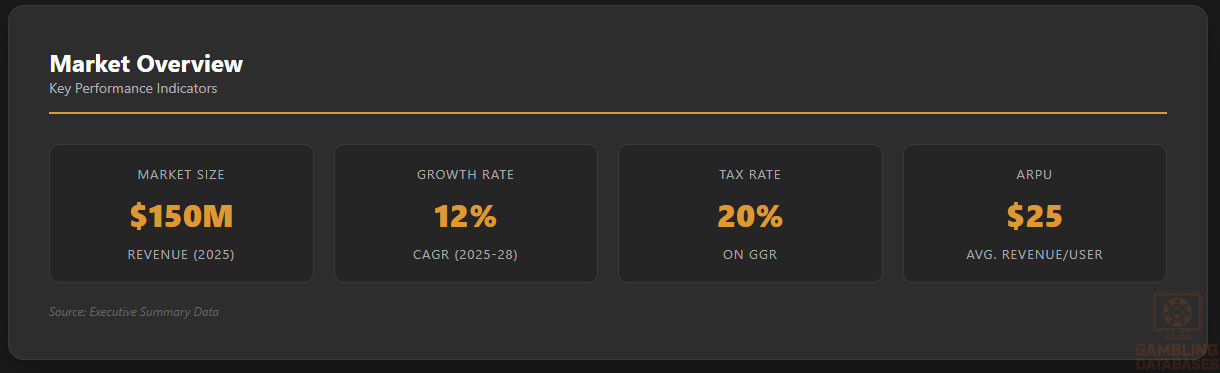

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal Status of Gambling | Regulated with licensing requirements |

| Population | 55 million (2025) |

| GDP | $106 billion USD (2025) |

| Internet Penetration | 82% |

| Mobile Penetration | 76% |

| Average Licensing Cost | $50,000 USD |

| Tax on GGR | 20% |

| Market Entry Timeline | 3-6 months |

| Regulatory Authority | Betting Control and Licensing Board (BCLB) |

| Market Size (2025) | $150 million USD |

| Annual Market Growth | 12% CAGR (2025-2028) |

| ARPU | $25 USD |

| Market Penetration Rate | 4% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Kenya maintains a regulated gambling environment predominantly overseen by the Betting Control and Licensing Board (BCLB). The regulatory scope covers land-based sports betting, casinos, and gaming halls, along with online gambling activities. The legal framework ensures licensing, compliance standards, and consumer protections are enforced across all gambling sectors.

The online gambling framework has been developed to regulate digital platforms, with the BCLB issuing licenses to qualified operators. Digital gambling activities encompass sports betting, virtual games, and casino platforms, with restrictions on unlicensed operators and certain game types being prohibited entirely. The scope of regulation is expanding to include responsible gambling measures and anti-money laundering protocols.

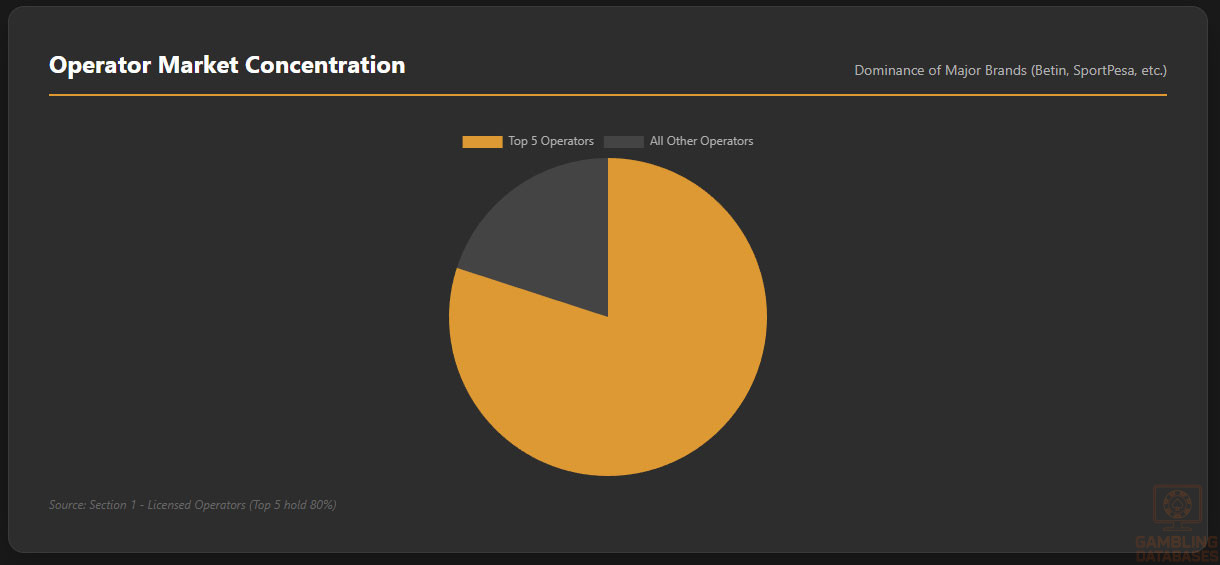

Licensed operators encompass both local firms and international brands that have acquired Kenyan licenses. The market structure is increasingly competitive, with market share concentrated among a few dominant players, but new entrants actively seek licenses to capitalize on market growth. The legal environment is characterized by ongoing adjustments aimed at balancing growth incentives with regulatory control.

Licensed Operators and Market Players

The Kenyan market features several key licensed operators, including local entities such as Betin, Odibet, and SportPesa, along with international companies like Betway and Bet365. These market players dominate the sector, leveraging their established brands and local partnerships to expand their customer bases. Competition is fierce, driven by aggressive marketing and product diversification strategies.

The market shares are concentrated among the top five operators, who collectively hold over 80% of licensed activities. New entrants are required to demonstrate financial stability, technical capacity, and compliance with local standards. Market entry strategies often involve localized content, mobile-first interfaces, and Responsible Gambling compliance to meet regulatory expectations.

Operational licenses are usually valid for periods of 3-5 years, with renewal dependent on compliance and tax payments. The regulatory framework increases transparency and accountability while aiming to curtail illegal gambling practices. Continuous monitoring and certification processes are embedded within the licensing ecosystem.

Licensing Framework and Requirements

Application Process and Eligibility

Operators seeking licenses must submit thorough applications to the BCLB, demonstrating their financial health, technical competence, and adherence to legal standards. The process involves comprehensive documentation, including proof of corporate registration, financial statements, and operational plans. The application fee typically ranges from $10,000 to $50,000 USD, with licensing approval taking approximately 3-6 months depending on completeness and regulatory review.

- Business incorporation certificates

- Financial capacity documentation

- Technical platform certifications

- Anti-money laundering and KYC compliance proof

- Responsible gambling policies

Local Presence and Operational Requirements

Foreign operators are generally required to establish a local registered office in Kenya and may need to partner with local entities. A minimum of one Kenyan resident director is often mandated.

Domains must be hosted locally or in compliant jurisdictions, and staff must include local compliance officers. Foreign ownership restrictions are in place, but partnerships with local firms can facilitate market entry.

Compliance Obligations and Monitoring

Player Protection and Identification

Kenyan regulators impose strict KYC and AML standards, including age verification for players over 18 years old, transaction monitoring, and reporting suspicious activities. Responsible gambling practices include self-exclusion options, player education, and clear disclosure of terms and conditions. Operators are mandated to implement self-exclusion systems and to provide transparent information regarding odds and payout policies.

- Mandatory age verification processes

- AML compliance procedures

- Self-exclusion mechanisms

- Responsible gambling tools and info

- Player account monitoring

Financial Monitoring and Reporting

Operators must establish rigorous transaction monitoring systems and submit regular reports on financial activity, including suspicious transaction reports.

Audits and compliance checks are conducted periodically to ensure adherence to tax obligations and anti-fraud measures. The reporting process involves quarterly submissions, detailed transactional records, and audit certifications.

Taxation Structure and Financial Obligations

Player Taxation

Winning players are subject to withholding tax rates, generally around 20%, applied to payouts above certain thresholds. Tax collection is enforced at the source, with operators responsible for deducting and remitting taxes to authorities.

There are also transparency obligations for informing players about applicable taxes on winnings.

Operator Taxation

| Game Type | GGR Tax Rate |

|---|---|

| Sports Betting | 20% |

| Casino Games | 20% |

| Virtual Games | 20% |

Additional operational taxes include license renewal fees (approx. $50,000 USD every 3 years) and a turnover tax on gross revenue. Corporate income tax rates are standard at 30%. Revenue trends show a consistent increase, with the market generating an estimated $150 million in 2025, projected to grow annually at around 12%.

Advertising and Marketing Restrictions

Advertising channels are restricted to licensed platforms, with particular limitations on promoting gambling through TV, radio, and online. Content must avoid targeting minors and must include responsible gambling messages. Sponsorships and promotional offers are regulated with restrictions on time and audience targeting.

Recent regulatory amendments have tightened advertising restrictions, aiming to prevent gambling-related harm and prevent illicit practices. Enforcement includes penalties for unlicensed advertising, with strict penalties for breaches.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

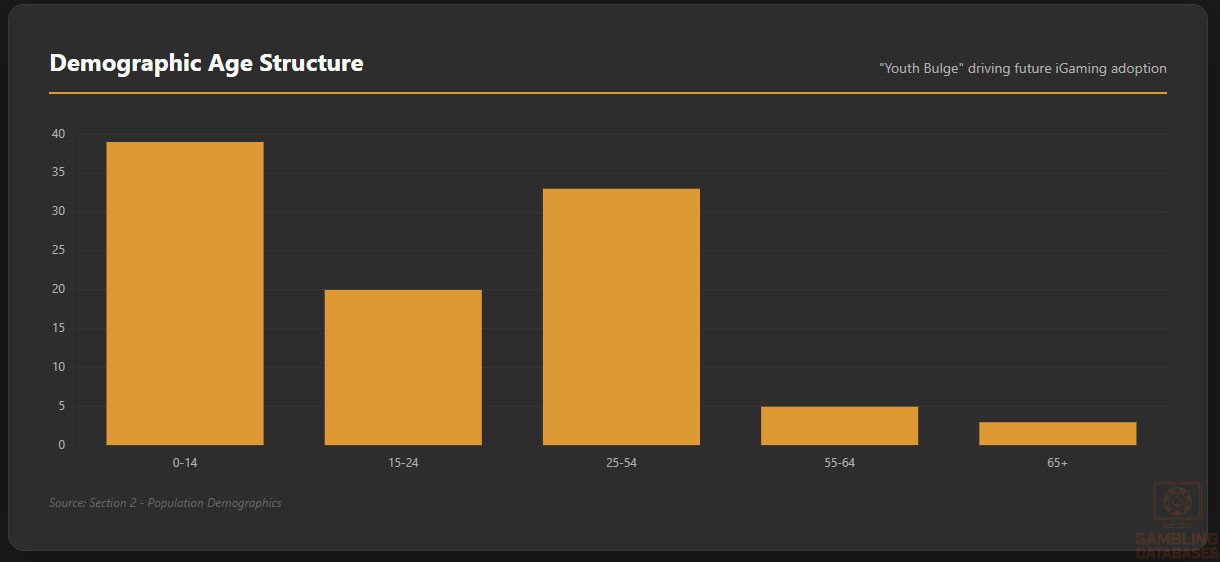

Kenya’s population has surpassed 55 million as of 2025, characterized by a youthful demographic profile with a median age of approximately 20 years. The population is nearly evenly split between genders, with a slight male majority at 51%, reflecting typical Sub-Saharan African patterns. A large proportion of the population, around 60%, resides in rural regions, though rapid urbanization is shifting this distribution.

Urban centers are expanding steadily, concentrated primarily in economic hubs where infrastructure supports digital access and entertainment services including gambling. The youth bulge coupled with increased urban migration fuels demand for digital and leisure services, positioning Kenya as a key emerging iGaming market.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 39% |

| 15-24 years | 20% |

| 25-54 years | 33% |

| 55-64 years | 5% |

| 65 years and older | 3% |

Geographic Distribution

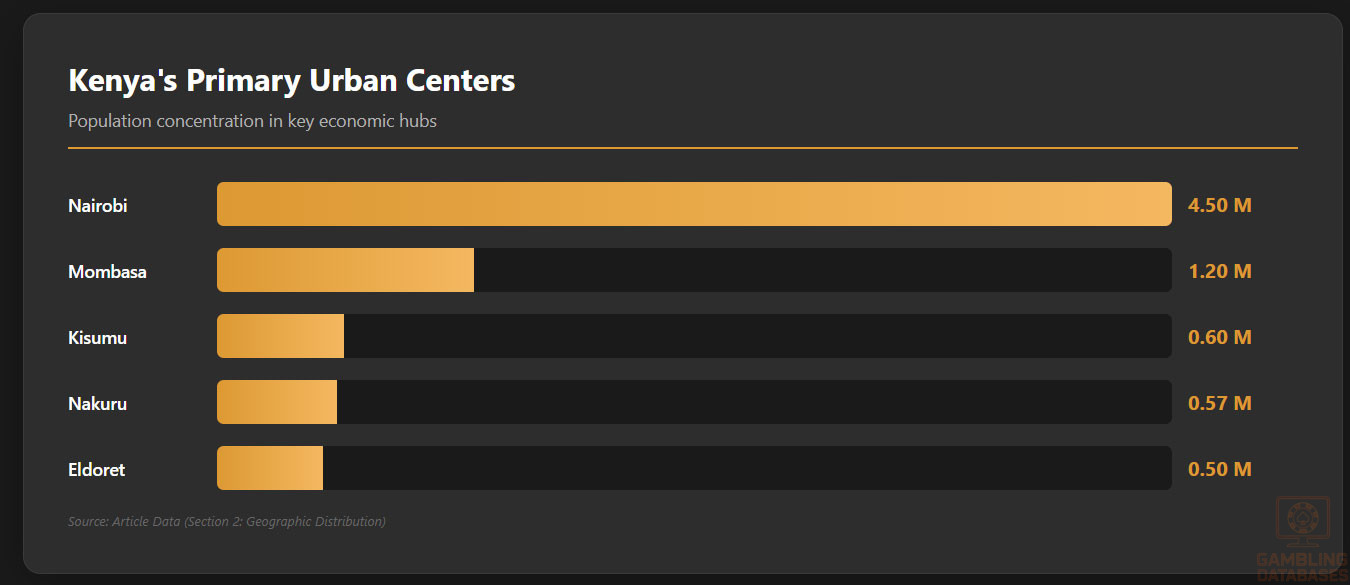

The country’s largest urban populations are concentrated in Nairobi, Mombasa, Kisumu, Nakuru, and Eldoret, which serve as economic and technological hubs fostering consumer activity. Internet access and gambling venue concentration favor these cities, driven by enhanced infrastructure and economic vibrancy.

Regional disparities persist, notably between the prosperous Rift Valley and the more agrarian and less urbanized northern counties.

- Nairobi – Population ~4.5 million

- Mombasa – Population ~1.2 million

- Kisumu – Population ~600,000

- Nakuru – Population ~570,000

- Eldoret – Population ~500,000

Urban centers dominate online gambling activity due to better connectivity, higher disposable incomes, and more robust technological infrastructure. Rural areas increasingly gain mobile internet access, slowly broadening the market base beyond traditional urban strongholds.

Economic Indicators and Consumer Spending Power

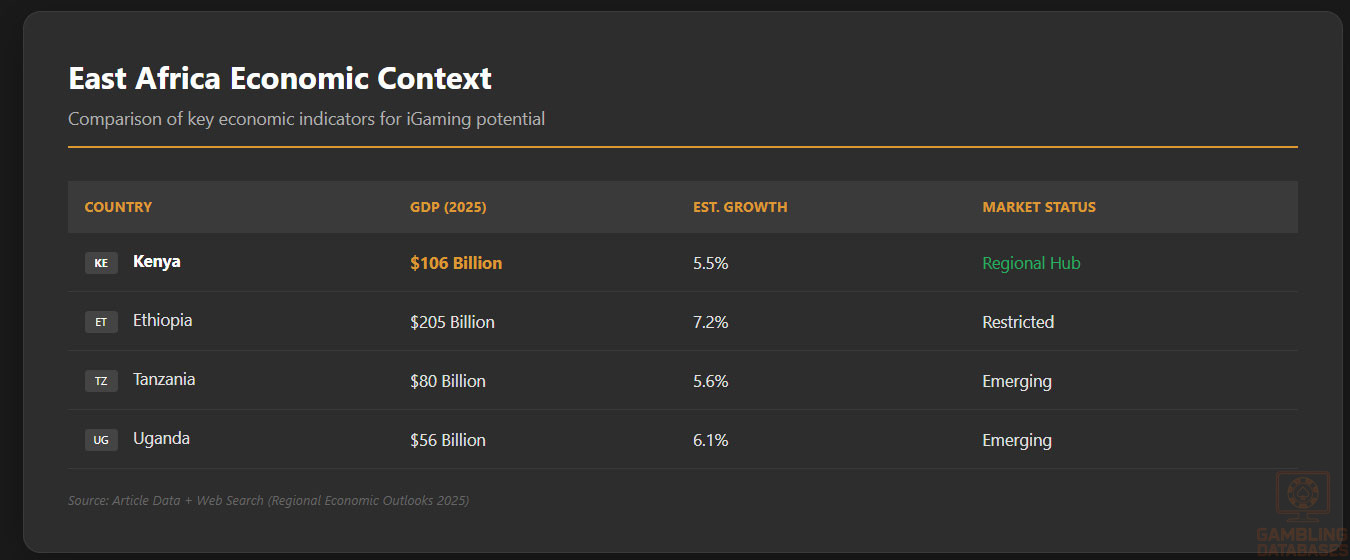

Kenya’s economy exhibits steady expansion with a GDP of $106 billion USD recorded in 2025, growing at an estimated annual rate of 5.5%. The economy is diversified, driven mainly by services accounting for 50%, agriculture contributing 24%, and industry making up 26% of GDP. Forecasts anticipate continual growth, underpinning rising consumer confidence and enhanced spending power.

Disposable income levels vary considerably across regions, but the national average household income stands around $3,200 USD annually. Consumption patterns reveal increasing spending on digital services and entertainment, with middle-income urban populations driving demand for iGaming and other leisure activities. Wealth is concentrated in urban regions, with Nairobi and Mombasa leading in per capita income.

| Indicator | Value |

|---|---|

| GDP (USD) | $106 billion |

| Annual Growth Rate | 5.5% |

| Per Capita Income (USD) | $1,950 |

| Service Sector Percentage | 50% |

| Agriculture Sector Percentage | 24% |

| Industry Sector Percentage | 26% |

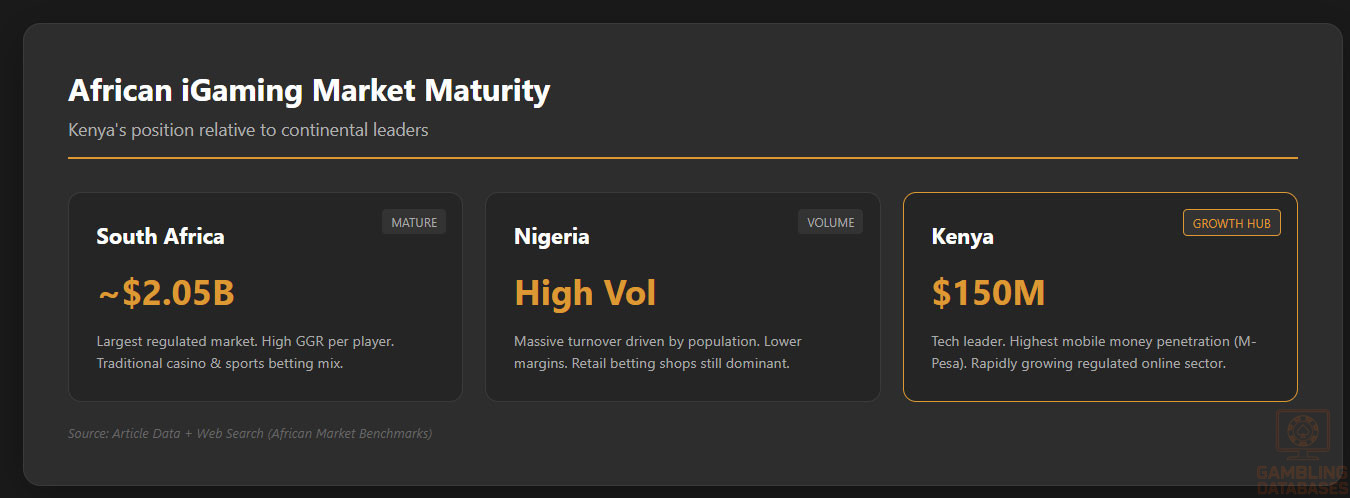

Market Size and Growth Projections

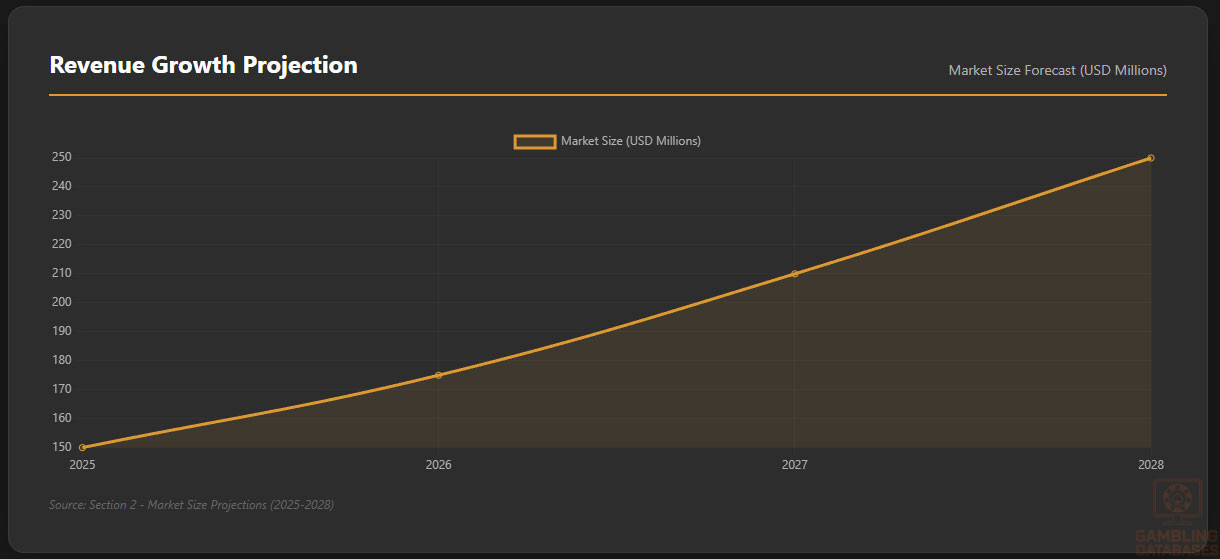

The Kenyan iGaming sector currently generates approximately $150 million USD in revenue, with projections estimating growth to over $250 million by 2028. Annual growth rates of 12% reflect increasing consumer adoption of online betting and casino platforms. The user base is expanding, particularly among younger adults aged 18-35, driven by mobile penetration and wider digital payment acceptance.

Average revenue per user (ARPU) hovers around $25 USD, signaling moderate spending levels with potential for growth as digital literacy and disposable income improve. The market remains underpenetrated at roughly 4% of the total population, highlighting substantial untapped demand.

| Metric | Value |

|---|---|

| Market Size 2025 (USD) | $150 million |

| Projected Market Size 2028 (USD) | $250 million |

| CAGR (2025-2028) | 12% |

| Estimated User Base 2025 | 2.2 million |

| ARPU (USD) | $25 |

| Market Penetration (%) | 4% |

Education, Skills, and Digital Literacy

Kenya boasts a literacy rate exceeding 82%, buoyed by increasing investments in education and youth outreach. Secondary and tertiary education enrollment continues to climb, equipping a growing workforce with technical skills essential for digital economy participation. Digital literacy is notably higher in urban centers where internet access and smartphone usage are widespread, fostering readiness for online gambling platforms.

Cultural and Social Factors

Communication and Language

Kenya is linguistically diverse with two official languages, English and Swahili, serving as primary languages for business and online content. Additionally, numerous indigenous languages exist, though online communication predominantly occurs in English and Swahili. Preferences for digital content lean towards Swahili among rural and youth users, influencing marketing strategies for iGaming operators.

- English

- Swahili

- Kikuyu

- Luhya

- Luo

- Kalenjin

Cultural Attitudes Towards Gambling

Gambling is broadly accepted as a social activity in Kenya, with sports betting especially popular among young adults and urban populations.

Religious influences, especially from Christian groups, advocate caution and encourage moderation, impacting public attitudes and regulatory emphasis on responsible gambling. International brands enjoy mixed perception; trust is higher for operators with strong local partnerships and transparent practices.

Entertainment preferences favor sports-related betting as well as lottery and virtual gaming, reflecting cultural engagement with football and other popular sports. Consumer behavior exhibits both recreational and aspirational gaming motivations.

Problem Gambling and Social Considerations

Problem gambling prevalence is estimated at 3-5%, with young men being the most vulnerable group. Awareness and mitigation programs are increasing but remain in early stages. Government and NGOs advocate for education, support groups, and helplines, while operators contribute to funding social responsibility initiatives.

- National awareness campaigns

- Helpline and counseling services

- Self-exclusion programs

- Support group sponsorships

- Mandatory responsible gambling contributions from operators

Social responsibility obligations are enforced through regulatory conditions linked to licensing, emphasizing consumer protection and harm minimization.

Political Structure and Governance

Kenya operates a stable multiparty democracy with a devolved government structure facilitating regional administration. Political stability has improved, fostering a business climate conducive to foreign investment. Regulatory consistency in gambling oversight supports investor confidence, with clear frameworks managed by the BCLB under the Ministry of Interior and Coordination of National Government.

International relations emphasize trade and technology partnerships, which benefit the iGaming sector’s technology adoption and integration with global ecosystems.

Technology Adoption and Digital Behavior

Internet and Digital Usage

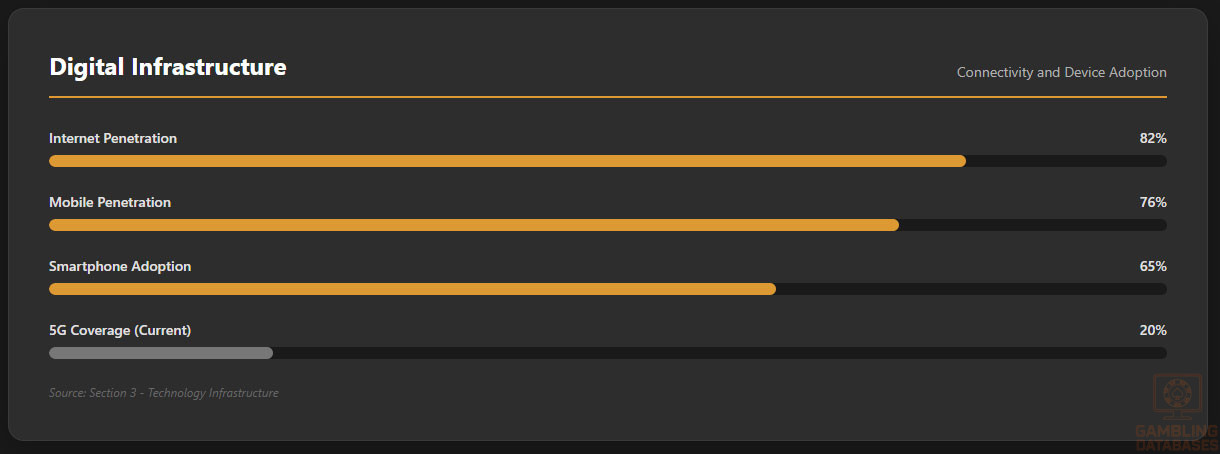

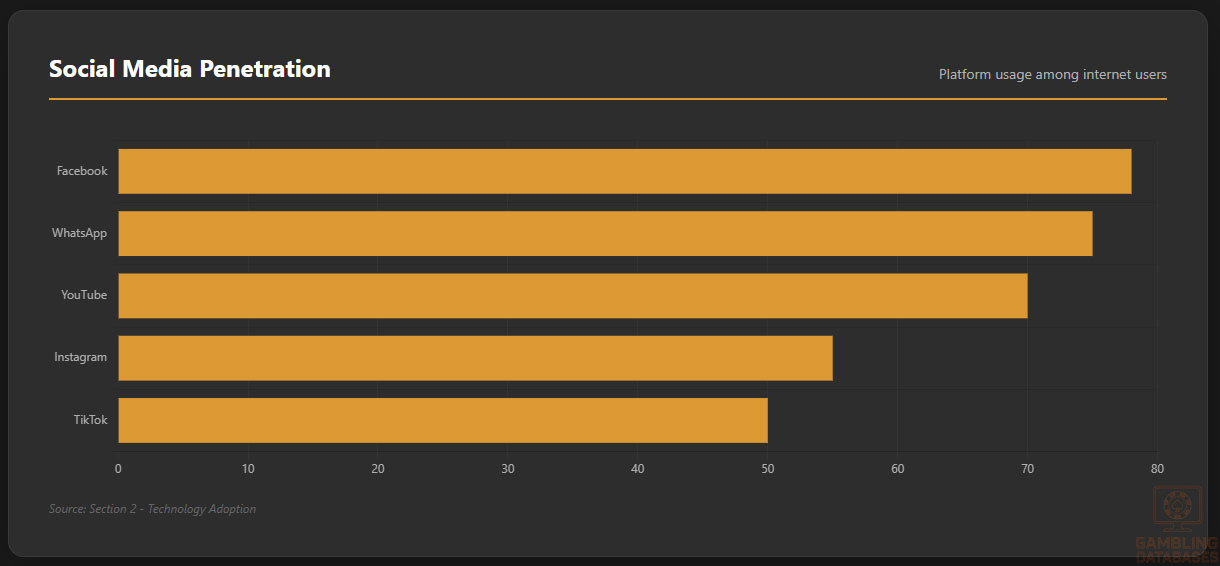

Kenya’s internet penetration stands above 82%, with daily usage averaging 4.3 hours per user driven by affordable smartphones and mobile broadband expansion. Mobile internet constitutes the primary access mode, accounting for nearly 90% of connections. Social media usage is widespread, embedding digital engagement deeply into daily activities.

Leading social media platforms capture extensive user bases, fueling digital marketing potential for iGaming and entertainment sectors.

- Facebook: 78% penetration, average 2.3 hours/day

- WhatsApp: 75% penetration, dominant messaging platform

- YouTube: 70% penetration, 45 minutes average watch time

- Instagram: 55% penetration, strong youth engagement

- TikTok: Rapid growth reaching 50% of under-30 demographic

Digital Payment Behavior

Kenya leads Africa in mobile money adoption with M-Pesa dominating the digital payments landscape, used by over 70% of internet users for online transactions.

Other digital wallets and payment methods are emerging, diversifying the ecosystem and facilitating seamless e-commerce and iGaming payments.

- M-Pesa: 70% market share

- Airtel Money: 12% market share

- PayPal and international e-wallets: 8% combined

- Bank cards (Visa/Mastercard): 7%

- Cryptocurrency adoption: Emerging, ~3%

The proliferation of secure and convenient payment options supports rapid growth in online gambling activity and user spend.

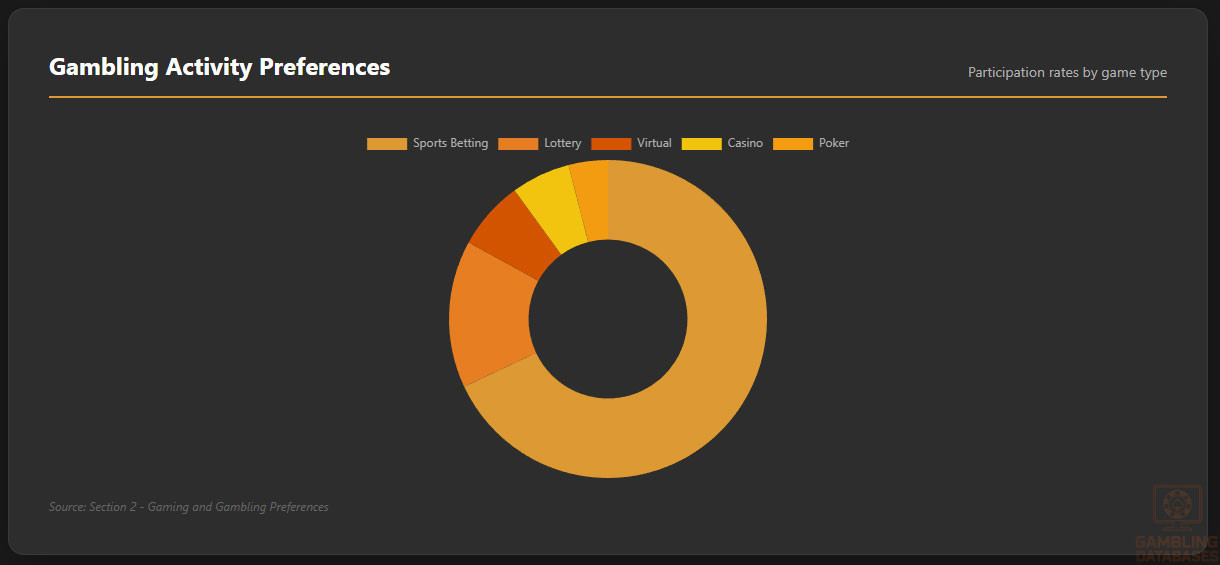

Gaming and Gambling Preferences

Kenyan consumers show a strong preference for sports betting, particularly football, followed by lottery, virtual betting, casino games, and poker. The popularity reflects both cultural affinity for sports and increasing exposure to digital gaming formats. Recent trends point towards higher engagement on mobile devices with peak activity during major sporting events.

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 68% |

| Lottery | 15% |

| Virtual Betting | 7% |

| Casino Games (Online) | 6% |

| Poker | 4% |

Consumer behavior reveals preferences for quick bet placement and immediate result games, favoring platforms with intuitive mobile apps and fast payment turnaround. Session lengths average 25-35 minutes, with frequent repeat usage among loyal players. Retention strategies by operators emphasize bonuses, loyalty programs, and localized content to maintain engagement in a competitive landscape.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Kenya’s internet penetration has risen to approximately 82%, with mobile broadband constituting roughly 90% of all internet connections.

Average fixed broadband speeds are moderate, averaging 25 Mbps, while mobile broadband speeds range from 15 to 30 Mbps depending on location. The network reliability and coverage have improved considerably due to recent investments in fiber optic infrastructure and satellite connectivity, especially in urban and peri-urban areas.

The government, alongside private stakeholders, continues investing in expanding digital infrastructure to rural areas, enhancing last-mile connectivity. This expansion is vital to increasing the potential iGaming market size by bringing underserved populations online.

5G and Future Technology Deployment

Kenya has initiated rollout of 5G services, primarily in major cities such as Nairobi, Mombasa, and Kisumu. Coverage currently reaches about 20% of the population, with plans to extend to over 50% by 2027. The major telecom operators are actively investing in upgrading their networks to 5G, anticipating increased demand for high-speed, low-latency connectivity driven by digital entertainment and e-commerce sectors.

5G adoption is expected to enhance mobile gaming experiences, supporting more complex and immersive iGaming platforms. Ongoing government initiatives encourage the adoption of emerging technologies, including the Internet of Things (IoT) and artificial intelligence (AI), to support digital economy growth.

Mobile Technology Ecosystem

Kenya’s mobile network infrastructure is well-developed, with multiple operators competing intensely on coverage and pricing. The dominance of mobile internet over fixed broadband has shaped digital consumption habits, making mobile optimization critical for iGaming operators.

- Safaricom – Market share approx. 65%

- Airtel Kenya – Market share approx. 25%

- Telkom Kenya – Market share approx. 8%

- Faiba (Jamii Telecommunications) – Emerging operator with 2%

- Greenlight Mobile – Smaller provider expanding in niche markets

Mobile data costs remain competitive, averaging around $0.50 per GB, which facilitates widespread access. Device penetration is high, with smartphone adoption estimated at 65% and rapidly growing among youth. Feature phones remain common in rural areas but smartphones dominate urban usage and digital activities such as online gaming and payments.

Financial Services and Payment Infrastructure

Kenya’s banking sector is mature relative to regional peers, with over 70% of adults holding bank accounts and increasing adoption of digital banking services. Consumer trust in mobile banking, particularly via M-Pesa, underpins the robust digital payments ecosystem. E-banking platforms provide real-time access, simplified transactions, and integration with online merchants.

- Kenya Commercial Bank (KCB) – Largest bank with extensive retail and corporate services

- Equity Bank – Leading in SME lending and digital banking innovations

- Co-operative Bank – Strong regional presence with growing tech adoption

- Standard Chartered Kenya – International bank focusing on corporate clients

- NCBA Bank – Formed from merger, with diverse product offerings

Payment processing options include card networks (Visa, Mastercard), mobile wallets, bank transfers, and emerging cryptocurrencies. Payment gateways are integrated with major banks and fintech providers, accelerating online transaction flow and operator cash flow efficiency.

- M-Pesa – Leading mobile money platform with extensive merchant acceptance

- Airtel Money – Mobile wallet secondary to M-Pesa but growing

- Visa/Mastercard debit and credit cards widely accepted online

- Bank transfers – Common for higher-value transactions

- Emerging cryptocurrencies – Small but growing niche adoption

E-commerce and Digital Economy

Kenya’s e-commerce sector is valued at approximately $4 billion USD, representing 3.7% of GDP, with annual growth exceeding 17%. Consumer trust in digital commerce is high due to secure payment systems and mobile money ubiquity.

The expansion of digital services, including ride-hailing, online retail, and mobile entertainment, aligns well with iGaming growth prospects. Local entrepreneurs and multinational platforms collaborate to refine logistics, payment, and regulatory frameworks, creating fertile ground for digital entertainment sectors.

Business Environment and Regulatory Framework

Ease of Business Operations

Kenya ranks favorably in the World Bank’s Doing Business report, particularly excelling in business registration, credit access, and digital transaction facilitation. Business registration is streamlined, though ongoing improvements target reducing procedural bottlenecks further. Foreign direct investment policies encourage entry while mandating compliance with financial and operational regulations.

- Prepare incorporation documents and submit to the Registrar of Companies

- Obtain a Business Permit from the relevant County Government

- Register for a Personal Identification Number (PIN) and Value Added Tax (VAT) with the Kenya Revenue Authority

- Open a corporate bank account and deposit any required minimum capital

- Apply for sector-specific licenses such as those from BCLB for gaming

Corporate Structure and Registration

Most foreign-operated enterprises opt to register limited liability companies (LLC) due to liability protection and operational flexibility. Branch offices and subsidiaries are also viable but entail varying tax and regulatory implications. Registered entities must appoint local resident directors and comply with annual reporting standards. Foreign ownership is permitted up to 100% but strategic partnerships with local companies are common to ease regulatory navigation.

- Certificate of Incorporation

- Memorandum and Articles of Association

- Tax PIN Registration Certificate

- Business License/Permit

- Compliance certificates from sector regulators (BCLB for gaming)

- Proof of physical registered office address

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate in Kenya is 30%. Special Economic Zones (SEZs) offer reduced tax rates to incentivize investment, sometimes as low as 10% for qualifying companies. Kenya has signed double taxation treaties with over 15 countries, facilitating cross-border business and investor protections.

- United Kingdom

- United Arab Emirates

- South Africa

- India

- China

- Germany

- Netherlands

Personal Income Tax

Individual tax rates are progressive up to 30%, with mandatory National Social Security Fund (NSSF) and National Hospital Insurance Fund (NHIF) contributions. Withholding taxes apply to dividends and certain payments. Tax residency is established by physical presence exceeding 183 days per year.

Market Entry Considerations

Recommended Entry Strategies

Successful market entry frequently combines local partnerships, mobile-first platform development, and intensive regulatory compliance. Building trust with consumers through localized marketing and strong customer service is essential. Leveraging Kenya’s leading mobile money platforms enhances payment efficiency, while integrating social responsibility measures fosters regulatory goodwill.

- Form joint ventures with local operators

- Develop mobile-optimized platforms focused on UX

- Ensure full licensing and compliance with BCLB requirements

- Establish in-country presence with resident directors and staff

- Utilize local payment gateways such as M-Pesa extensively

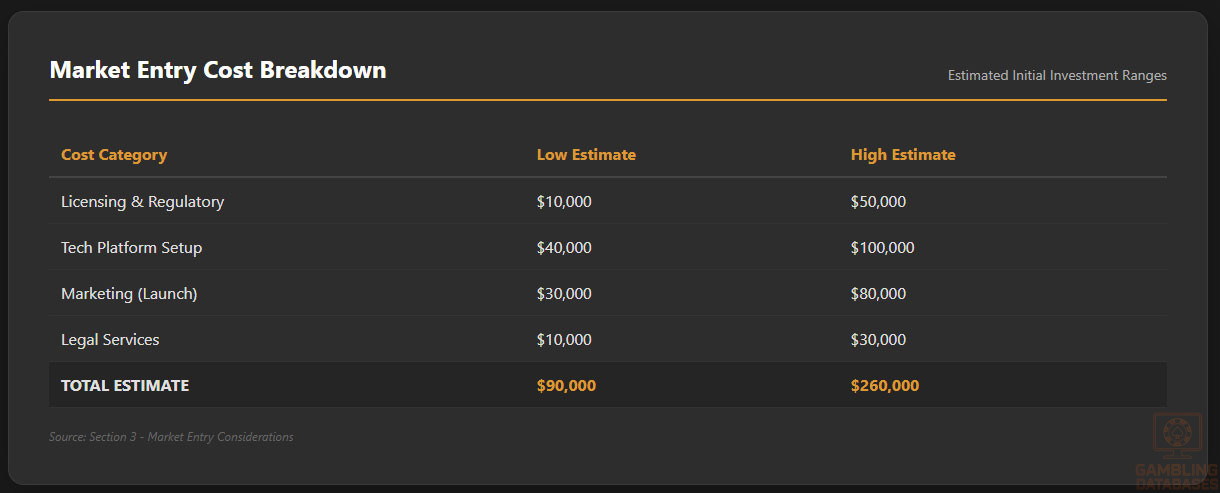

Typical Costs and Timelines

Market entry investments vary but typically require a comprehensive budget covering licensing fees, technology setup, marketing, staff recruitment, and compliance costs. Initial setup can range from $100,000 to $300,000 depending on scope and scale, with operational expenses adding ongoing monthly costs.

| Cost Category | Estimated Range (USD) |

|---|---|

| Licensing and Regulatory Fees | $10,000 – $50,000 |

| Technology Platform Setup | $40,000 – $100,000 |

| Marketing and Customer Acquisition | $30,000 – $80,000 |

| Operational and Staffing Costs | $20,000 – $60,000 monthly |

| Legal and Compliance Services | $10,000 – $30,000 |

- Complete licensing application and document submission (1-2 months)

- Technology platform integration and testing (2-3 months)

- Marketing launch and initial customer acquisition (1 month)

- Ongoing operational scaling and compliance monitoring (continuous)

Success Factors and Challenges

Key success factors include robust mobile platform experience, compliance diligence, localized customer engagement, seamless payment integration, and effective risk management. Operational challenges involve navigating evolving regulations, competition from established operators, volatility in consumer spending, and managing social responsibility obligations.

- Mobile-first user interface and seamless experience

- Strong regulatory compliance and transparent operations

- Localized marketing addressing cultural nuances

- Integration with dominant payment systems (M-Pesa)

- Effective responsible gambling frameworks

Exit Strategy Planning

While Kenya’s iGaming market is growing, operators should plan for liquidity considerations with moderate secondary market activity. License transfers require regulatory approval, emphasizing good compliance history. Valuation multiples for gaming businesses in Kenya tend to range moderately due to market risks but can improve with scale and brand equity.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Kenya?

Yes, online gambling is legal and regulated under the Betting Act, with licenses issued by the Betting Control and Licensing Board (BCLB). Operators must obtain the necessary licenses and comply with strict regulations including KYC, AML, and player protection measures. Activities outside regulatory approval remain illegal and subject to enforcement.

2. What types of gambling licenses are available and what do they cover?

The primary license types include sports betting licenses, casino gaming licenses, and lottery licenses, each covering specific gambling activities. Licenses may be exclusive or combined, and operators must comply with detailed requirements related to technology standards, financial capacity, and operational transparency. Additional permits may cover affiliate marketing and promotional activities.

3. How much does an iGaming license cost and how long does it take to obtain?

License costs typically range from $10,000 to $50,000 depending on the scope of operations. The approval process generally takes between 3 to 6 months, contingent on submission completeness and regulatory review. Operators should budget for additional legal and consultancy fees during the application phase to expedite compliance.

4. Can foreign companies obtain a gambling license?

Foreign companies are eligible to apply, provided they register locally either as subsidiaries or branches and meet licensing criteria including local presence and financial requirements. Foreign ownership up to 100% is permitted, though partnerships with local entities can facilitate market entry and regulatory compliance.

5. What are the tax obligations for iGaming operators?

Operators are subject to a 20% tax on gross gaming revenue (GGR), in addition to corporate income tax at 30%. License renewal fees and turnover taxes may also apply. Taxes must be reported and remitted regularly, with compliance audited by authorities to ensure fiscal accountability.

| Tax Type | Rate/Description |

|---|---|

| GGR Tax | 20% |

| Corporate Income Tax | 30% |

| License Renewal Fee | Approx. $50,000 every 3 years |

| Withholding Tax on Prizes | 20% |

6. Are gambling winnings taxed for players?

Yes, gambling winnings are subject to a withholding tax of about 20%, automatically deducted by operators at payout. Players are responsible for reporting any additional taxable income according to local tax laws. Transparency rules require operators to disclose tax deductions clearly.

7. What are the typical operational costs for running an online casino or sportsbook?

Operational costs vary but major categories include licensing fees, platform maintenance, marketing, personnel, and compliance services. Monthly operational expenses often range from $20,000 to $60,000. Efficient cost management and scale are critical for profitability in the Kenyan market.

8. What is the expected ROI timeline for entering this market?

Operators typically expect to reach break-even within 12 to 18 months, depending on market penetration speed and marketing effectiveness. Strong regulatory compliance and payment integration contribute significantly to accelerated ROI.

9. What are the local presence requirements for operators?

Operators must maintain a registered office in Kenya and appoint at least one resident director. Local staffing for compliance and customer support functions is advisable to meet regulatory expectations and foster trust with consumers.

10. What payment methods are available and recommended?

The dominant payment method is the mobile money platform M-Pesa, favored for convenience and security. Other recommended methods include Airtel Money, Visa/Mastercard, and bank transfers. Emerging cryptocurrency payments may become relevant but remain niche currently.

11. What are the advertising and marketing restrictions?

Advertising must comply with BCLB regulations, avoiding targeting minors or promoting irresponsible gambling. Restrictions apply to TV, radio, and digital advertising, mandating inclusion of responsible gambling messages. Sponsorship and promotional offers are regulated in timing and content.

12. What responsible gambling measures are mandatory?

Operators must implement self-exclusion programs, provide clear information on odds and risks, monitor player behavior for signs of problem gambling, and contribute to social responsibility initiatives. Mandatory measures emphasize consumer protection and harm minimization aligned with global best practices.

13. How large is the iGaming market and what is the growth potential?

The Kenyan iGaming market is currently valued at around $150 million with a compound annual growth rate of approximately 12%. Rising digital penetration, mobile adoption, and youthful demographics underpin strong future expansion potential.

14. Who are the main competitors and what is their market share?

The market is dominated by a handful of major operators including SportPesa, Betway, Betin, Odibet, and Bet365, which collectively hold over 80% of the licensed market. Competition is fierce and dynamic, with new entrants carving niches through innovation and local partnerships.

15. What are the player preferences and typical spending patterns?

Players predominantly engage in sports betting, especially football, followed by lotteries, virtual games, and online casinos. Average revenue per user is moderate at around $25, with spending concentrated in urban and youth demographics. Mobile platforms are preferred for their flexibility and ease of access.

16. What are the key success factors and main challenges for new entrants?

Success hinges on mobile-optimized offerings, robust compliance, strong local partnerships, and seamless payment integration. Key challenges include navigating shifting regulations, fierce competition, managing responsible gambling obligations, and adapting to diverse consumer preferences.

- Mobile-first platform design

- Full regulatory compliance

- Localized marketing and customer service

- Efficient payment processing

- Strong responsible gambling framework

- Evolving regulatory landscape

- High competition density

- Consumer trust building

- Operational cost management

- Societal and cultural nuances

Sources and References

- Kenya Betting Control and Licensing Board – Official Website – https://www.bclb.go.ke

- Kenya National Bureau of Statistics – Population & Economic Data 2024 – https://www.knbs.or.ke

- Central Bank of Kenya – Financial Reports 2024 – https://www.centralbank.go.ke

- Ministry of Finance Kenya – Tax Guidelines – https://www.treasury.go.ke

- World Bank – Doing Business Report 2024 – https://www.worldbank.org

- International Telecommunication Union ICT Data – https://www.itu.int

- Safaricom Annual Report 2024 – https://www.safaricom.co.ke

- Equity Bank Financial Statements 2024 – https://www.equitybankgroup.com

- Kenya Communications Authority – Telecommunications Statistics 2024 – https://www.ca.go.ke

- Kenya Ministry of Interior – Gambling Regulation Framework – https://www.interior.go.ke

- Kenya Revenue Authority – Taxation Policies 2024 – https://www.kra.go.ke

- Kenyan Digital Economy Strategy 2025 – Ministry of ICT – https://www.ict.go.ke

- Oxford Economics Market Analysis – iGaming Africa Report 2024

- GSMA Mobile Economy Sub-Saharan Africa 2024 – https://www.gsma.com

- Kenya Consumer Trends Report 2024 – Nielsen Kenya

- Kenya National Council for Law Reporting – Regulatory Amendments 2024

- African Online Payment Systems Report 2024 – McKinsey & Company

- Gaming Commission Africa Report 2024 – https://gamingafrica.com

- Financial Times – Kenya Economic Review 2024

- Euromonitor International – Kenya Digital Consumer Trends 2024

- Kenya Social Development Council – Problem Gambling Programs – 2024

- United Nations Economic Commission for Africa – Digital Infrastructure Report 2024

- International Labour Organization – Kenya Workforce Report 2024

- Kenya Ministry of Health – Social Responsibility in Gambling

- TechCrunch Africa – Emerging Market Technology Reports 2024

- PwC African Gambling Market Insights 2024

- Deloitte Kenya – Corporate Tax and Compliance Guide 2024

- KPMG Kenya – Business Setup and Regulatory Environment 2024

- International Monetary Fund Kenya Country Report 2024

- Kenya Financial Sector Deepening Trust Reports 2024

- CGTN Africa – Digital Economy in Kenya 2024

🎯 Gambling Databases Country Rating: Kenya

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.8/10 | [🟡 Moderate 5-7] |

| Player Access Score | 8.2/10 | [🟢 Fully Legal] |

| Overall Market Attractiveness | 7.0/10 | [High Volume / High Tax Environment] |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Aggressive Taxation Regime: Operators face a “Triple Threat” of taxes: 20% on GGR, 30% Corporate Tax, AND a mandatory 20% Withholding Tax on player winnings (which severely impacts player retention and churn).

- Local Presence Mandatory: Foreign operators CANNOT operate remotely; you must establish a local office, host data locally, and appoint at least one Kenyan resident director.

- Market Saturation: The top 5 operators (e.g., SportPesa, Betin) control over 80% of the market. Breaking this oligopoly requires massive marketing spend.

- Payment Monopoly: M-Pesa dominates 70% of transactions. Failure to integrate seamlessly with M-Pesa guarantees failure.

- Strict Advertising Limits: Recent amendments have tightened advertising on TV/Radio and completely banned targeting minors, with strict enforcement on unlicensed marketing.

- Financial Liability: License renewal fees are high (~$50,000 USD every 3 years) with rigorous financial monitoring and reporting obligations.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Full Legality (+3.0): Unlike many jurisdictions, Kenya offers a fully regulated path for Sports Betting, Online Casino, and Virtuals. No major product prohibitions. Final: 3.0/3.0 |

| Licensing Process | 25% | 1.5/2.5 | Accessible (+2.0): Clear process via BCLB. Costs (+0.5): Total fees <$100k. Deductions: 3-6 month timeline (-0.5); Complex document submission including financial health/probity (-0.5). Final: 1.5/2.5 |

| Taxation & Costs | 20% | 0.0/2.0 | Base Rate (+1.5): 20% GGR is technically moderate. Deductions: Multiple tax layers (Turnover tax + Corp tax) (-0.5); Effective tax rate >50% when factoring in all burdens (-1.0); High CAC due to saturation (-0.5). Final: 0.0/2.0 |

| Operational Requirements | 15% | 0.8/1.5 | Heavy Requirements (+0.5): Must have local office and resident director. Deductions: Mandatory local director residency (-0.25); Local hosting/domain requirements (-0.25); Strict AML/KYC reporting (-0.2). Final: 0.8/1.5 |

| Market Environment | 10% | 0.5/1.0 | Moderate Environment (+0.5): Stable politics but high corruption risk in region. Deductions: Advertising restrictions (-0.25); Intense market concentration/oligopoly (-0.25). Final: 0.5/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Fully Legal (+4.0): Players face no legal risks for participation. Deductions: 20% Withholding Tax on winnings acts as a financial penalty/deterrent (-0.5). Final: 3.5/4.0 |

| Practical Accessibility | 30% | 2.5/3.0 | High Accessibility (+3.0): M-Pesa is ubiquitous. Deductions: Internet penetration gaps in rural areas (-0.25); Heavy reliance on mobile data vs broadband (-0.25). Final: 2.5/3.0 |

| Player Penalties | 20% | 1.2/2.0 | No Criminal Penalties (+2.0): Deductions: Mandatory tax deduction at source on winnings reduces player value/RTP perception (-0.8). Final: 1.2/2.0 |

| Market Availability | 10% | 1.0/1.0 | High Availability (+1.0): 5+ major operators and numerous smaller entrants available. Final: 1.0/1.0 |

🔍 Key Highlights

Strengths

- Mobile-First Ecosystem: 82% internet penetration with a “mobile-first” population accustomed to digital transactions via M-Pesa.

- Clear Regulation: Unlike “grey” markets, Kenya has a defined path for all verticals (Casino, Sports, Virtuals).

- Volume Potential: $150M market growing at 12% CAGR with a population of 55 million.

⛔️ CRITICAL RISKS AND CHALLENGES

- The “Winnings Tax” Killer: The 20% tax on player winnings is a massive friction point that lowers the effective RTP (Return to Player) and drives high-value players to black-market offshore sites that don’t deduct this tax.

- Oligopoly Dominance: New entrants must fight for the remaining 20% of market share against entrenched giants like SportPesa and Betin.

- Operational Drag: You cannot run this from Malta or Curacao. You need a physical office, local staff, and a Kenyan director, increasing overhead significantly.

- Regulatory Volatility: The BCLB has a history of sudden crackdowns, including suspending licenses over tax disputes (as seen in previous years with major operators).

- Advertising Clampdown: Promoting gambling on mainstream channels is increasingly restricted to protect minors, raising Customer Acquisition Costs (CAC).

Player-Specific Issues

- Tax on Wins: Players legally forfeit 20% of their winnings to the government immediately upon payout.

- Data Costs: While mobile data is cheap ($0.50/GB), it is still a consideration for data-heavy live casino products in rural areas.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $150,000 – $350,000 (Includes licensing, local incorporation, office setup, and legal fees).

Monthly Operating Costs: $50,000 – $100,000 (Staff, office, compliance, server hosting).

Effective Tax Rate on Revenue: ~55-60% (Calculated via: 20% GGR + Turnover Tax + 30% Corp Tax + Administrative cost of collecting WHT).

Customer Acquisition Cost: Moderate ($20-$50), but retention is difficult due to the Winnings Tax driving players away.

Time to Breakeven: 18-24 months.

Profitability Assessment: Economics are TIGHT. While the volume is high, the government takes a massive share of the revenue through various tax layers. This market is viable only for operators who can achieve massive scale (volume) to offset thin margins. Small operators will likely bleed out due to overhead and tax compliance costs.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [High] | [ISP blocking risk, payment blocking via M-Pesa, inability to advertise locally] |

| Licensed Operators | [Medium] | [License suspension risk over tax disputes, heavy compliance burden, regulatory volatility] |

| Affiliates/Advertisers | [Medium] | [Strict penalties for promoting to minors or unlicensed brands; regulatory fines] |

| Payment Processors | [Low] | [M-Pesa is state-sanctioned; risk is low provided AML compliance is perfect] |

| Company Directors/Executives | [Medium] | [Local directors can be held personally liable for tax non-compliance] |

🚨 Extradition and International Enforcement

Extradition Treaties: Kenya is a Commonwealth nation and has extradition arrangements with the United Kingdom, USA, Canada, and Australia.

Enforcement History: Kenya cooperates with international agencies on AML and financial crimes. While they have not historically extradited for “gambling offenses” alone, tax evasion or money laundering charges associated with gambling operations are grounds for extradition.

Safe Jurisdictions: There are no “safe” nearby havens; enforcement is generally strict regarding financial compliance.

📋 Final Verdict

Kenya receives an Operator Ease Score of 5.8/10 and a Player Access Score of 8.2/10, resulting in an overall market attractiveness rating of 7.0/10.

HONEST ASSESSMENT: Kenya is the “Jewel of East Africa” for iGaming, but the sparkle is dimmed by an aggressive tax regime. It is NOT a free-for-all; it is a mature, highly regulated, and expensive market to operate in. The requirement for local presence and the triple-layer taxation (GGR, Corporate, Winnings Tax) means margins are razor-thin. If you cannot compete with SportPesa’s volume or M-Pesa’s integration, you will fail.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major African or International brand with $500k+ startup capital.

- Willing to establish a physical office in Nairobi with local staff.

- Capable of sustaining thin margins via high-volume sports betting.

- Technologically ready to integrate deep M-Pesa functionality.

❌ Definitely Avoid If You Are:

- A “remote-only” operator (Local presence is mandatory).

- A crypto-casino (Crypto is niche/unregulated and hard to scale here).

- Looking for a low-tax jurisdiction (Kenya is a high-tax environment).

- An offshore operator hoping to fly under the radar (Payment blocking and ad restrictions will starve you).

⚠️ BOTTOM LINE: Enter only if you have the capital to set up locally and the volume to survive a 50%+ effective tax rate.