Kiribati presents a unique iGaming opportunity due to its undefined online gambling regulations and emerging digital infrastructure. While online gambling is neither explicitly legal nor illegal, local laws currently lack comprehensive frameworks regulating iGaming activities.

This regulatory ambiguity combined with modest internet penetration and a recovering economy offers a niche market for operators willing to engage with offshore frameworks targeting Kiribati players.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Undefined for online; land-based regulated under general laws |

| Regulatory Framework | Absence of dedicated iGaming laws; local licensing required for gambling |

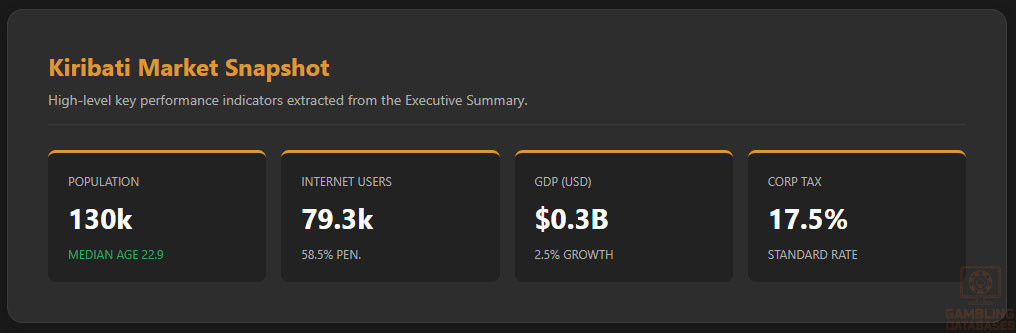

| Population | Approx. 130,000 (2025 estimate) |

| Median Age | 22.9 years |

| Population Density | 169 people/km² |

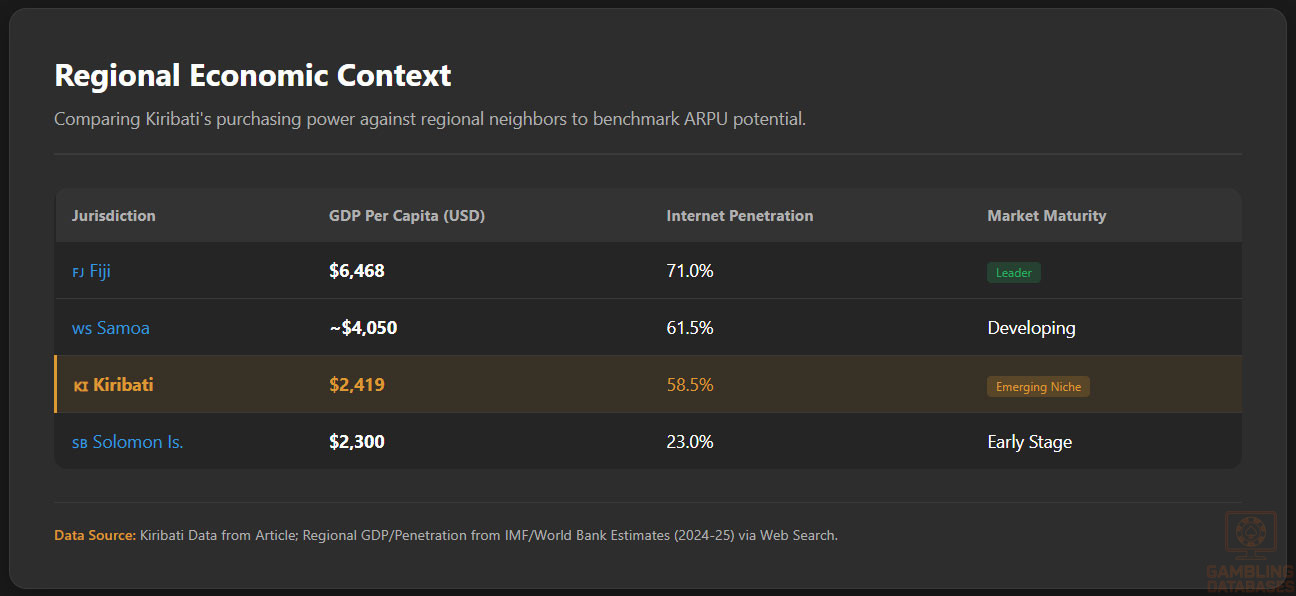

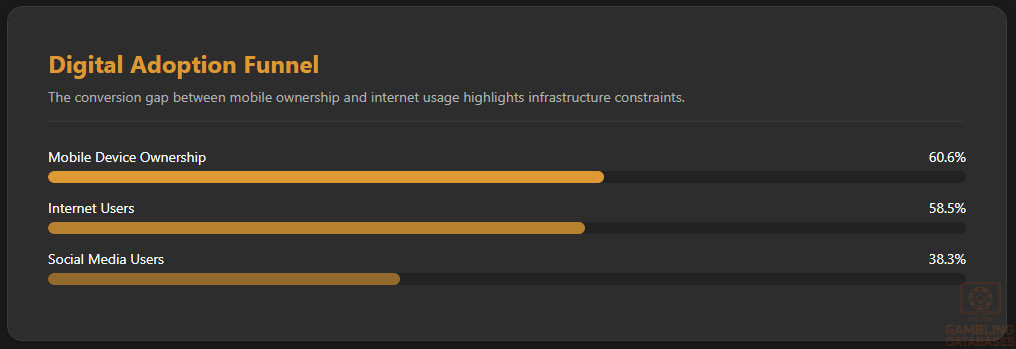

| Internet Users | 79,300 individuals (58.5% penetration) |

| Mobile Connections | 82,100 (60.6% of population) |

| Social Media Penetration | 38.3% of population |

| GDP (Current Prices) | $0.3 billion USD |

| Economic Growth Outlook | Gradual recovery driven by infrastructure & tourism |

| Licensing Authority | Undisclosed; regulatory authority fragmented |

| Licensing Costs | Not formally defined for iGaming sector |

| Application Processing Time | Not specified; transparency limited |

| Minimum Capital Requirements | Not publicly specified |

| GGR Tax Rates | Not legislated for online gambling |

| Corporate Income Tax | Standard rates apply (17.5% corporate tax) |

| Player Taxation | Not regulated |

| Market Entry Barriers | Regulatory uncertainty, limited local infrastructure |

| Responsible Gambling Regulations | Absent; reliance on operator adherence |

| KYC/AML Requirements | Minimal local mandates; offshore licenses impose strict protocols |

| Advertising Restrictions | Broadly regulated under general laws; no iGaming-specific rules |

| Enforcement Mechanisms | Basic penalties for illegal gambling; limited formal enforcement |

| Market Size (Estimated) | Small but growing niche market |

| ARPU (Average Revenue per User) | Data unavailable |

| Growth Forecast (CAGR) | Not publicly forecasted |

| Technology Infrastructure | Developing; mobile-led internet access predominant |

| Business Environment | Emerging, reliant on foreign investment & aid |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Kiribati’s gambling laws are generally fragmented and do not specifically address online gambling activities as of 2025. The legislation provides for gambling activities such as games of chance, prize competitions, and lotteries under broad terms but lacks dedicated statutes for digital or online gaming. This legal ambiguity means online gambling operators are not explicitly licensed nor banned, placing Kiribati in a regulatory grey zone.

Land-based gambling, including casinos and betting shops, falls under existing local gambling laws but is limited by the scarcity of formal venues and a modest domestic market. There are currently no licensed online casinos based in Kiribati, and all digital gaming services accessed by Kiribati residents are offered by offshore operators.

Land-Based Gambling Activities

Existing land-based gambling options in Kiribati are minimal due to economic constraints and small population size. Theoretical frameworks allow for licensed operations in:

- Physical casinos (scarce or non-operational)

- Sports betting venues

- Lotteries and sweepstakes

- Slot machine halls (not prevalent)

- Prize competitions and bingo halls

However, the limited market demand and limited infrastructure make significant land-based gambling activity unlikely at present.

Online Gambling Framework

Online gambling in Kiribati is neither explicitly authorized nor prohibited by specific laws, resulting in an unregulated market environment. No domestic regulatory authority is clearly designated for iGaming licensing or oversight. Players largely access international offshore platforms that admit Kiribati customers, subject to those operators’ licensing jurisdictions.

Licensed Operators and Market Players

No licensed online gambling operators are currently based in Kiribati due to the lack of iGaming-specific licensing frameworks. The competitive landscape comprises international operators licensed offshore that accept players from Kiribati. Market entry strategies focus on compliance with external jurisdictions recognized for their regulatory rigor, such as Malta, Curacao, or the UK, catering to the Kiribati player base remotely.

Licensing Framework and Requirements

Application Process and Eligibility

Kiribati requires gambling operations, including lotteries and games of chance, to obtain a local license per existing general laws. However, specific licensing procedures for online gambling remain undefined. Available information suggests the regulatory authority responsible is not clearly named, and no formal application process for iGaming licenses is published.

Common financial and technical requirements, drawn from typical global practices although not specified locally, would generally include:

- Corporate registration and local incorporation proof

- Financial statements and evidence of financial stability

- Operational business plan including market and risk assessments

- Technical certifications of gaming software and random number generators

- Background checks for company directors and beneficial owners

Application fees, minimum capital deposits, and timelines are not publicly available but may be inferred to pose challenges due to the regulatory absence.

Local Presence and Operational Requirements

Kiribati’s current regulations do not explicitly mandate a local operational presence for gambling operators. There are no domain registration restrictions or personnel obligations clearly stated in legal texts. Foreign ownership is not limited, as the regulatory framework remains non-specific about partnership or local representative requirements for online gaming initiatives.

Operators seeking to serve Kiribati without domestic licenses typically rely on offshore licensing and marketing through digital platforms accessible within the country.

Compliance Obligations and Monitoring

Player Protection and Identification

No locally mandated player protection measures or responsible gambling policies have been codified in Kiribati’s gambling regime. Age verification, KYC (Know Your Customer), and AML (Anti-Money Laundering) protocols are generally absent from national laws.

As such, protection from underage gambling and fraud depends primarily on operator compliance with the licensing jurisdictions governing their platforms offshore. Common player protection features recommended for operators to maintain integrity include deposit limits, self-exclusion, and reality checks, though these are not government-enforced locally.

Financial Monitoring and Reporting

Kiribati does not prescribe comprehensive financial monitoring or reporting procedures for gambling operators. In the absence of a formal iGaming regulator, mandatory audit processes, suspicious transaction reporting, and ongoing financial disclosures are not enforced domestically. Regulatory vigilance is largely reliant on foreign licensing bodies overseeing operators available to residents.

Taxation Structure and Financial Obligations

Player Taxation

There is currently no regulated taxation on player winnings or gambling-related personal income in Kiribati. Players are not required to declare or withhold taxes against gambling earnings, reflecting the broader regulatory inaction in the sector.

Operator Taxation

| Tax Type | Rate / Details |

|---|---|

| Gross Gaming Revenue (GGR) Tax | Not legislated specifically for gambling |

| Corporate Income Tax | 17.5% standard corporate tax applies |

| License Renewal Fees | Not specified for iGaming |

| Turnover/Betting Tax | Not available/applicable at present |

Given the lack of specific tax legislation for iGaming, operators typically adhere only to the general corporate income tax framework. This may present opportunities or uncertainties depending on future regulatory developments.

Gambling Market Financial Performance

Measures of total wagered amounts, payouts, and revenue from Kiribati-specific gambling activity are unavailable due to minimal local industry presence. The gambling market remains nascent and largely served through offshore operators rather than domestic establishments.

Revenue trends and tax receipts from gambling are therefore negligible, although gradual digital adoption could underpin modest growth over the medium term.

Advertising and Marketing Restrictions

Advertising of gambling services in Kiribati is regulated by general commercial laws without explicit provisions for iGaming. Operators must comply with broader promotional standards and fairness requirements but face no detailed restrictions governing online or offline gambling advertising.

- General prohibition of misleading or deceptive advertising

- Restrictions on targeting minors or vulnerable groups

- Limitations on promotional claims without evidence

- Mandatory inclusion of responsible gambling messages recommended

- Restrictions on sponsoring local cultural or sports events potentially applied

Sponsorship regulations and time-based advertising restrictions specific to gambling are currently unestablished given the limited market scale and regulatory oversight.

Recent Regulatory Changes and Their Impact

Kiribati’s gambling regulatory environment has experienced minimal changes in recent years. No new laws specifically addressing iGaming or online betting have been enacted as of 2025. The lack of updates reflects a low government priority on gambling regulation compared to broader economic and social challenges.

Consequently, operator costs and market entry strategies remain focused on compliance with offshore licensing regimes rather than local mandates.

Enforcement Mechanisms and Penalties

Penalties for unauthorized gambling operations in Kiribati include fines and imprisonment under existing general gambling laws. Enforcement mechanisms involve policing illegal land-based activities with limited capacity to regulate online operators lacking local presence.

- Fines imposed for unlicensed gambling activity

- Criminal penalties including imprisonment for serious breaches

- Seizure of gambling equipment or assets in illegal cases

- Possible restriction or shutdown of illegal venues

- Minimal enforcement against offshore online operators

The overall enforcement framework remains rudimentary without specialized regulatory agencies dedicated to gambling oversight.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

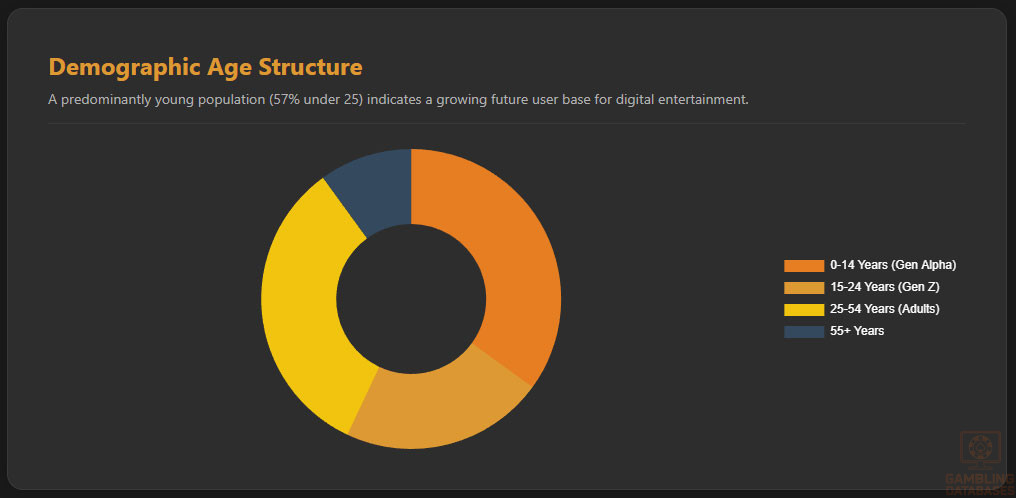

Kiribati has a total population of approximately 130,000 people as of 2025. The country exhibits a young demographic profile with a median age of 22.9 years, signifying a predominantly youthful population. Gender distribution is roughly balanced, with a slight male majority, maintaining a ratio close to 1.05 males per female.

The age distribution reveals a high proportion of children and young adults, indicating a potentially growing future consumer base, which is critical for digital entertainment sectors including iGaming.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 35% |

| 15-24 years | 22% |

| 25-54 years | 33% |

| 55-64 years | 6% |

| 65+ years | 4% |

Urbanization is limited; approximately 44% of the population resides in urban centers, while the majority live in rural and dispersed island communities. This distribution impacts access to internet infrastructure and gaming venues, concentrating digital opportunities primarily in urban hubs.

Geographic Distribution

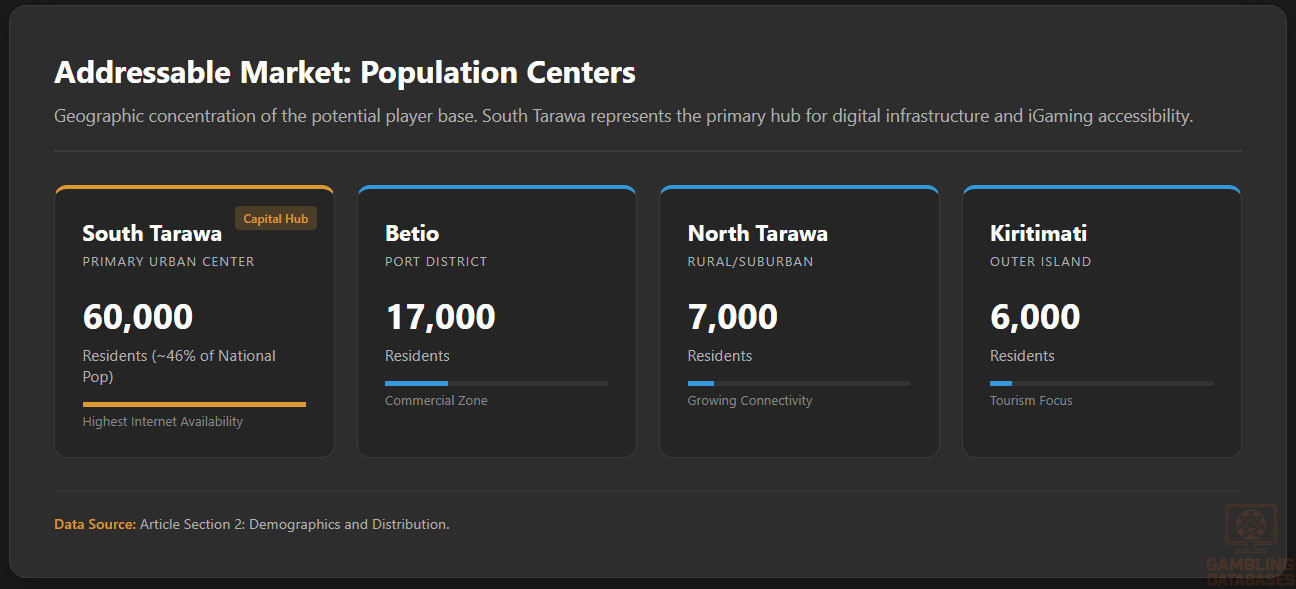

Kiribati consists of 33 atolls and reef islands spread widely across the central Pacific, resulting in a dispersed population. Major population concentrations are located on Tarawa Atoll, hosting the capital city and administrative center.

- South Tarawa (Capital) – Approx. 60,000 residents

- Betio – Population around 17,000

- Bairiki – Population near 3,000

- North Tarawa – Approximately 7,000 inhabitants

- Kiritimati Island – Around 6,000 residents

Internet access and digital infrastructure are predominantly available in Tarawa and select islands, with other regions facing connectivity challenges. Gambling venues and related services are similarly concentrated in these population centers, limiting physical market penetration outside principal urban locations.

Economic Indicators and Consumer Spending Power

Kiribati’s economy is small, with a GDP estimated at $0.3 billion USD in 2025, reflecting gradual but constrained growth. The country’s economic drivers include subsistence agriculture, fishing, remittances, and limited tourism. GDP growth forecasts are modest and linked closely to infrastructure development and foreign aid inflows.

Per capita income remains low relative to global averages, yet there is a steady upward trend in disposable income among urban populations. The labor market is largely informal, impacting financial inclusion and structured consumer spending data.

| Indicator | Value |

|---|---|

| GDP (Current USD) | $300 million |

| GDP Growth Rate (Forecast) | 2.5% annually |

| Per Capita GDP | $2,300 USD |

| Corporate Tax Rate | 17.5% |

| Inflation Rate | 3.1% |

Kiribati’s consumer spending is characterized by essential goods dominance, with increasing expenditure on digital services and mobile communication in urban settings. The relatively low average income limits discretionary spending on entertainment, suggesting cautious iGaming market expansion.

Income and Wealth Distribution

Income disparity is moderate, with urban households benefiting from more stable employment and better access to remittances. Rural communities experience lower income levels and higher subsistence reliance. Median household income hovers around $800 USD monthly in urban areas but declines significantly in outer islands.

Disposable income growth aligns with improving telecommunications infrastructure, catalyzing digital payment adoption and e-commerce activity, critical for future iGaming consumer engagement.

Market Size and Growth Projections

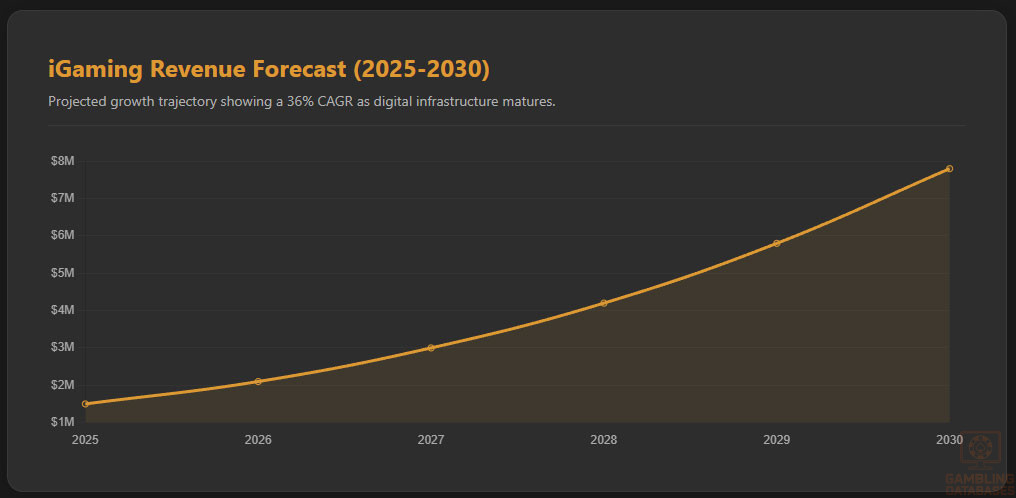

The iGaming market in Kiribati remains nascent, constrained by regulatory uncertainties and limited affluent consumer base. Nonetheless, digital penetration growth and global online gaming trends provide an optimistic long-term growth outlook.

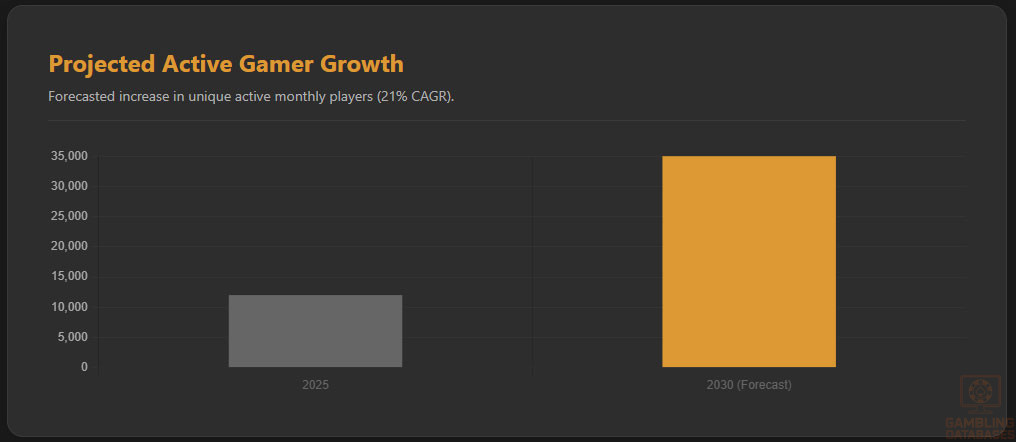

| Metric | 2025 | 2030 Forecast | CAGR |

|---|---|---|---|

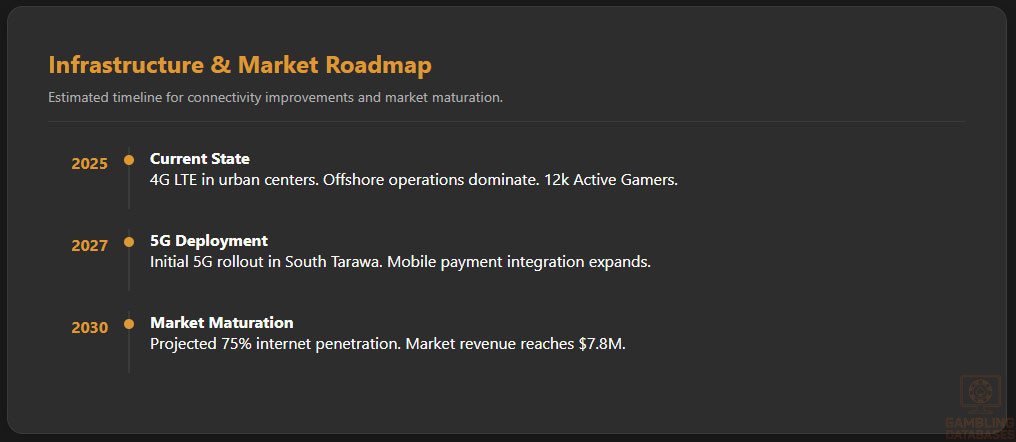

| Active Online Gamers | 12,000 | 35,000 | 21% |

| Market Revenue (USD) | $1.5 million | $7.8 million | 36% |

| Average Revenue Per User (ARPU) | $125 | $180 | 8% |

| Internet Penetration | 58.5% | 75% | 5.5% |

| Mobile Payment Adoption | 60.6% | 85% | 7% |

Education, Skills, and Digital Literacy

Kiribati’s literacy rate exceeds 90%, with primary and secondary education widely accessible, especially in urban areas. However, tertiary education levels are limited, and technical skills related to digital technologies remain developing. Digital literacy is improving steadily alongside expanding internet access, particularly among younger demographics.

Workforce skills relevant to digital economy sectors such as IT support, software development, and online customer service are in early stages of growth but can be leveraged via regional cooperation or outsourcing to support iGaming market expansion.

Cultural and Social Factors

Communication and Language

The official languages in Kiribati are I-Kiribati and English, with English used primarily for official, business, and educational purposes. Kiribati residents are comfortable with online communication in English, facilitating access to international digital content.

- I-Kiribati (native language, primary for daily communication)

- English (official, business and education)

- Gilbertese dialects (regionally varied)

- Minor presence of Banaban (on Rabi Island, Fiji residents)

- Access to global media languages through English proficiency

Cultural Attitudes

Kiribati’s culture places a high value on community and traditional customs, which influences entertainment and leisure choices. Gambling acceptance is mixed, with some religious and social reservations due to predominant Christian beliefs. Foreign brands, particularly from Australia and New Zealand, enjoy trust, easing market entry prospects for licensed offshore iGaming operators.

Entertainment preferences trend towards mobile games, social media, and sports, aligning with global youth culture trends. The growing digital presence balances cultural conservatism with increasing openness to online leisure activities.

Problem Gambling and Social Considerations

Problem gambling prevalence in Kiribati remains undocumented due to the underdeveloped gambling market. Potential at-risk groups include urban youth and those with increased digital access. Government response programs are limited but emerging in collaboration with regional partners focusing on awareness and responsible gambling education.

- Educational campaigns on gambling risks

- Support helplines and counseling services (nascent stage)

- Community engagement programs on addiction prevention

- Collaboration with NGOs for mental health support

- Promotion of self-exclusion and limit-setting tools

Political Structure and Governance

Kiribati operates a parliamentary democracy with a stable government focused on economic development and climate change mitigation. Regulatory consistency has been challenging due to resource constraints and dispersed geography. Nevertheless, political stability supports gradual reforms conducive to business development including foreign investments in technology and digital services.

Technology Adoption and Digital Behavior

Internet and Digital Usage

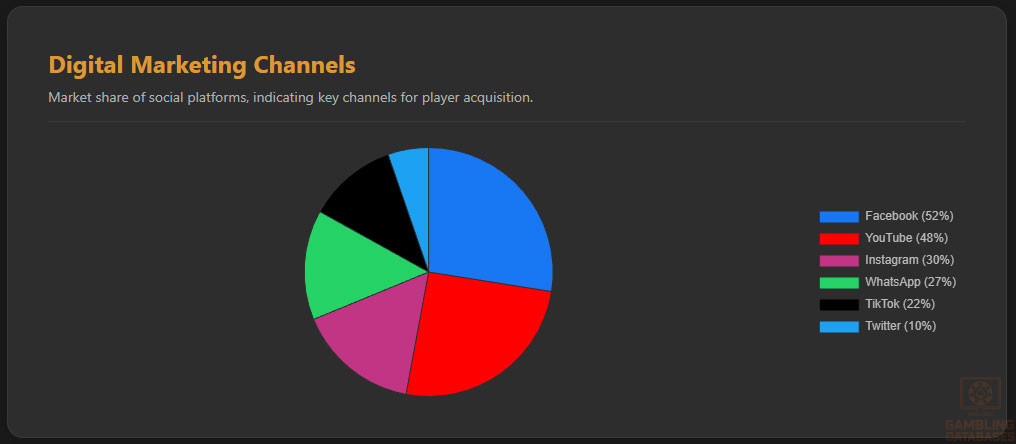

Internet penetration stands at approximately 58.5%, primarily driven by mobile broadband services available in urban centers. Daily internet usage averages 3.5 hours, with social media engagement a key activity among younger populations. Mobile device adoption exceeds 60% of the population, underpinning the digital-first approach for entertainment and commerce.

- Facebook: 52% penetration

- YouTube: 48%

- Instagram: 30%

- WhatsApp: 27%

- TikTok: 22%

- Twitter: 10%

Digital Payment Behavior

Digital payments are increasingly favored in Kiribati’s urban areas, supporting online transactions including gaming deposits and withdrawals. Popular payment methods include mobile money, credit cards, and regional e-wallets. Cryptocurrency adoption is minimal but observed in niche users seeking privacy and international payment facilitation.

- Mobile Money Platforms (dominant in digital payments)

- Visa/MasterCard Credit & Debit Cards

- Regional e-wallets (e.g., M-Pesa)

- Bank Transfers

- Cryptocurrency (limited use, emerging interest)

Gaming and Gambling Preferences

Current Market Participation

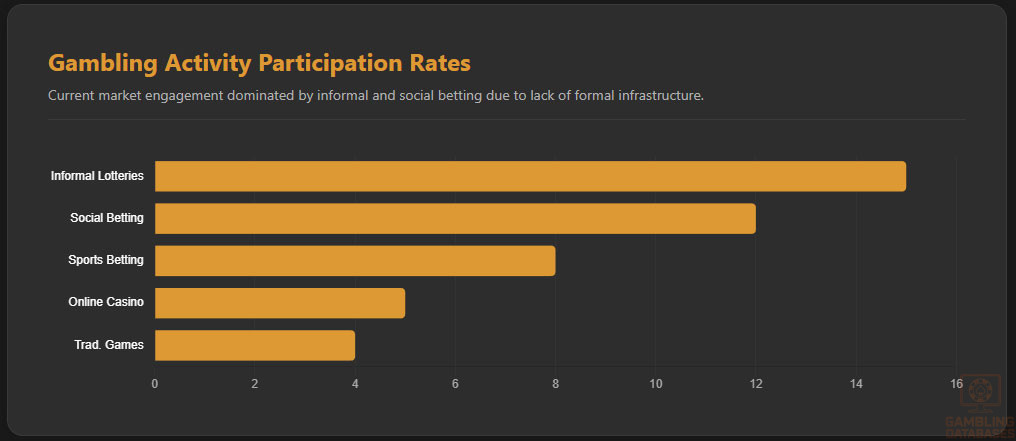

Overall gambling participation in Kiribati is limited, primarily comprising informal lotteries, social betting, and occasional sports betting. Online gambling participation is low but expected to grow with improving digital access and regional industry trends.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Informal Lotteries | 15% |

| 2 | Social/Community Betting | 12% |

| 3 | Sports Betting (Informal and Offshore) | 8% |

| 4 | Online Casino Games | 5% |

| 5 | Traditional Games (Bingo, Card Games) | 4% |

Consumer Behavior Patterns

Kiribati digital consumers exhibit cautious spending, preferring low-stake gaming and social betting experiences. Peak engagement occurs during evenings and weekends, with high frequency of short gaming sessions averaging 20-30 minutes. Retention is dependent on operator provision of localized content and mobile-optimized platforms.

Consumer preference trends increasingly favor interactive and skill-based games, such as poker and sports betting, facilitated by improved mobile connectivity and regional cultural influences.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Connectivity and Network Performance

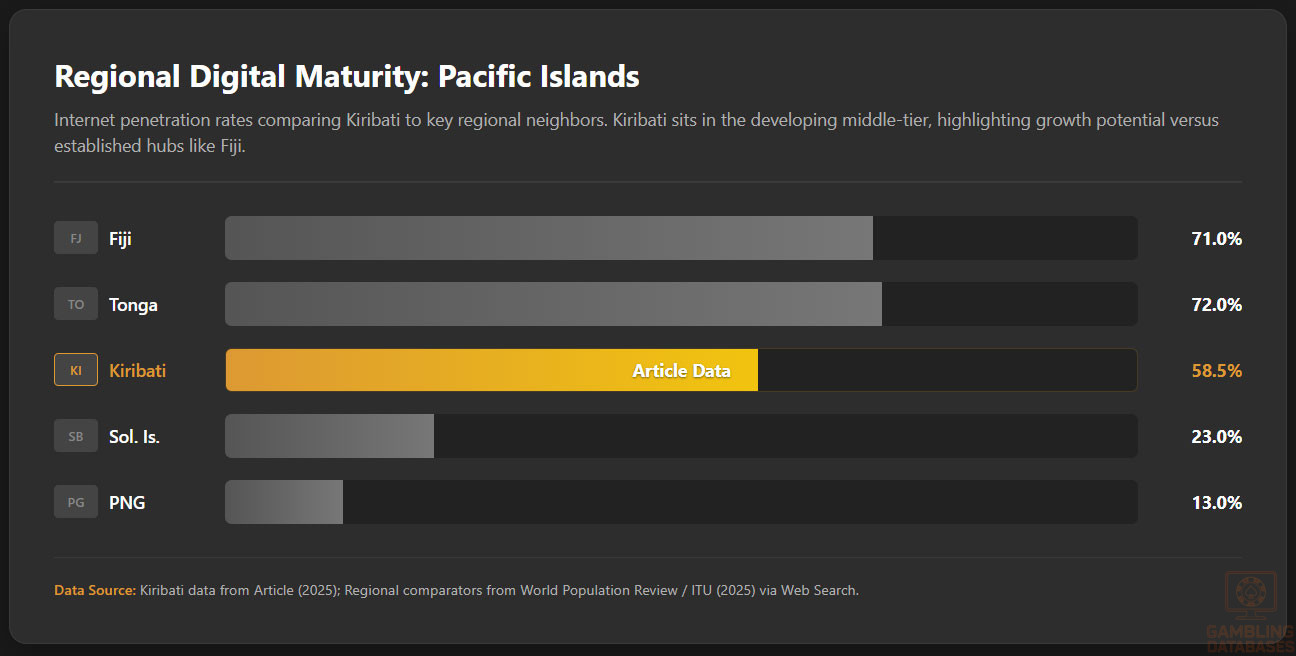

Kiribati’s internet penetration stands at about 58.5%, with broadband largely supplanted by mobile internet access due to the dispersed geography of the islands. Fixed broadband infrastructure is minimal and primarily available in South Tarawa and select urban centers, while mobile networks provide the primary means of connectivity across outer islands.

Average mobile internet speeds range between 10 and 20 Mbps, adequate for basic iGaming activities but limiting for bandwidth-heavy applications. Reliability remains variable due to geographic and infrastructural constraints, with recent investments targeting undersea cable connectivity to improve national bandwidth and stability.

5G and Future Technology Deployment

While Kiribati currently offers 3G and limited 4G services through its mobile operators, 5G deployment is in its infancy. Planned rollouts are contingent on infrastructure development and government partnerships with regional telecommunications providers. Initial 5G coverage is expected to target South Tarawa by 2027, expanding gradually to other densely populated areas.

The telecommunications landscape comprises a limited number of operators, driving competitive service improvement though regulatory oversight remains in early stages to accommodate next-generation technologies.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Kiribati has three primary mobile network operators vying for market dominance, delivering mobile voice and data services across the islands. Coverage quality is strongest on South Tarawa and neighboring atolls, with decreasing signal strength and network availability moving outward.

- Kiribati Telecommunications Corporation (KTC) – holds 55% market share, government-owned, offers 2G/3G/4G services

- Beibu Gulf Telecom (Regional Operator) – approx. 25% market share, expanding 4G service

- Oceanic Mobile Networks – 20% market share, innovative pricing models

Data pricing remains relatively high compared to regional peers, acting as a barrier to mass mobile data adoption. Operators offer prepaid and subscription packages, with ongoing efforts to lower costs through network optimization and volume pricing.

Device Penetration

Smartphone adoption is estimated at 63% of the population, focused in urban areas with higher income levels. Entry-level Android devices dominate the market, reflecting affordability concerns, while premium device penetration remains low.

Financial Services and Payment Infrastructure

Banking System Structure

Kiribati’s banking sector is small but growing, centered on the National Bank of Kiribati as the largest player. Digital banking adoption is emerging alongside traditional services, with mobile banking platforms facilitating financial inclusion especially in urban centers.

Account penetration remains limited, especially outside urban zones where cash transactions dominate. The banking landscape includes regional institutions and a growing presence of microfinance organizations supporting small enterprises.

- National Bank of Kiribati – dominant retail and commercial bank

- Pacific Islands Development Bank – focus on regional development projects

- Kiribati Cooperative Bank – expanding SME banking

- ANZ Bank (Regional Branch) – foreign-owned, specialized services

- Kiribati Savings & Loan Society – microfinance, deposit mobilization

Payment Processing Options

Available payment methods in Kiribati support bank cards, mobile wallets, and traditional bank transfers. While credit and debit card penetration remains modest, mobile money services gain increasing traction as affordable and convenient alternatives to cash, especially for younger demographics.

- Visa and MasterCard acceptances primarily in cities

- Mobile Money platforms (K-Express, T-Kash) prevalent in remote areas

- Bank Transfers between local institutions

- International remittance systems supporting cross-border transactions

- Emerging cryptocurrencies used in niche tech-savvy populations

E-commerce and Digital Economy

Kiribati’s e-commerce market is nascent but expanding, led by mobile retail applications and regional online marketplaces. Consumer trust remains cautiously developing due to payment security concerns and logistical challenges from remoteness.

Digital service adoption is growing faster than physical goods retail, driven by communication apps, gaming, and digital entertainment. Government initiatives to boost digital literacy and infrastructure underpin this transition toward an emerging digital economy.

Business Environment and Regulatory Framework

Ease of Business Operations

Kiribati ranks modestly in World Bank’s Ease of Doing Business indicators, reflecting challenges in infrastructure, regulatory transparency, and market size. Business registration is straightforward but slowed by geographic isolation and resource limitations.

Foreign investment policies are generally welcoming, with a focus on development sectors including technology and tourism. Operational costs remain low compared to developed markets, though logistical expenses linked to import dependence and limited local services are notable.

- Preparation and notarization of incorporation documents (2-3 weeks)

- Submission to Registrar of Companies (5-7 business days processing)

- Tax registration and acquiring tax identification number (3-5 days)

- Opening corporate bank account with minimum deposit (1-2 weeks)

- Receipt of business license and commencement permit (2-3 days post approvals)

Corporate Structure and Registration

Common business entity types include Limited Liability Companies (LLCs), Corporations, and Foreign Branch Offices. LLCs are most popular for flexibility and limited liability protection, suitable for iGaming ventures. Branch offices allow foreign companies to operate without full registration but impose restrictions on activities and tax treatment.

Foreign ownership faces minimal restrictions, encouraging international participation in the market with compliance to local laws and tax regimes.

- Articles of Incorporation and Memorandum

- Proof of registered office address in Kiribati

- Director and shareholder identification documents

- Bank reference letters and financial statements

- Tax registration certificates and compliance statements

Taxation Framework

Corporate income tax in Kiribati is set at a standard rate of 17.5%, applicable to both domestic and foreign entities. Special economic zones and foreign investors may benefit from negotiated concessions or tax holidays, supporting market entry incentives.

Personal income tax applies progressively on residents’ earnings, with withholding tax obligations for employers. Social security contributions are mandatory for employees.

- Corporate tax rate: 17.5%

- Personal income tax brackets: 0%-25% progressive

- Withholding tax on dividends, interest, royalties: 10%-15%

- Sales tax/VAT currently at 10%

- Tax treaties with Australia, New Zealand, Fiji among others

Market Entry Considerations

Recommended market entry strategies emphasize partnership with local firms, compliance via offshore licensure, and mobile-first platform deployment. Leveraging regional payment integrations and localized content enhances consumer acceptance.

- Form strategic alliances with Kiribati-based business entities

- Obtain offshore licenses with recognized regulatory credibility

- Deploy mobile-optimized platforms suited for limited bandwidth

- Utilize local payment ecosystems, including mobile money

- Implement culturally sensitive marketing respecting local norms

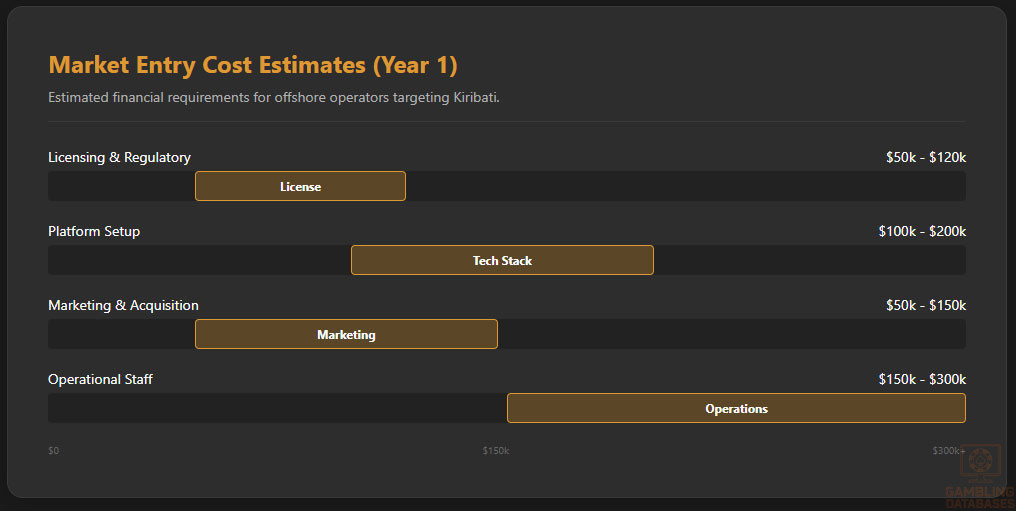

| Cost Category | Estimated Range |

|---|---|

| Licensing and Regulatory Fees | $50,000 – $120,000 |

| Technology Platform Setup | $100,000 – $200,000 |

| Local Partnership Development | $20,000 – $40,000 |

| Marketing and Customer Acquisition | $50,000 – $150,000 |

| Operational and Staff Costs (Year 1) | $150,000 – $300,000 |

- Pre-market research and feasibility analysis (1-2 months)

- Licensing application and approval (3-6 months)

- Platform development and localization (2-4 months)

- Marketing launch and operational scaling (ongoing)

Success Factors and Challenges

Success hinges on regulatory adaptability, robust mobile platform delivery, and cultural alignment. Challenges include infrastructural limitations, limited local digital literacy, payment ecosystem constraints, and competition from established offshore operators.

- Strong local partnerships for market access and trust

- Investment in mobile and low-bandwidth optimized gaming platforms

- Robust compliance with international licensing standards

- Effective marketing that respects local culture and norms

- Mitigation of logistical and operational constraints due to geography

Exit Strategy Planning

Market liquidity for iGaming assets in Kiribati is limited due to the small size and nascent market. License transferability depends on regulatory provisions abroad if operated under offshore jurisdictions. Valuation multiples align with regional benchmarks but must accommodate local risks and growth potential.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Kiribati?

Online gambling operates in a legal grey zone in Kiribati, as no explicit laws forbid or regulate the activity. Operators typically function under offshore licenses, while local legislation does not provide a specialized framework for digital gaming. This provides opportunities but adds regulatory uncertainty for market participants.

2. What types of gambling licenses are available and what do they cover?

Kiribati offers general gambling licenses covering land-based activities such as lotteries and casinos. However, there are no specialized licenses explicitly for online gambling. Operators seeking to serve Kiribati players usually rely on offshore licenses from established jurisdictions for legal credibility.

3. How much does an iGaming license cost and how long does it take to obtain?

Costs for a formal Kiribati gambling license are not clearly defined, especially for online operations, though general licensing fees may range from $50,000 to $120,000. The approval process timeline is uncertain but may take 3 to 6 months depending on documentation and regulatory review.

4. Can foreign companies obtain a gambling license?

Foreign companies face no significant restrictions obtaining gambling licenses for land-based operations, but as specific online licenses are not available locally, foreign operators generally must rely on recognized offshore licenses. International businesses can establish local entities or partnerships to comply with regulations.

5. What are the tax obligations for iGaming operators?

Operators are subject to the standard corporate income tax rate of 17.5%, with no specific gambling-related tax. No gross gaming revenue taxes or turnover levies exist for online gaming. Operators must comply with income tax and possible withholding taxes on profits.

6. Are gambling winnings taxed for players?

There are currently no taxes imposed on players’ gambling winnings in Kiribati. This absence simplifies player experience but may impact government tax revenue opportunities from the sector.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs typically include licensing fees, technology platform expenses, marketing, local partnership development, and staffing. Costs can range broadly but expect initial annual expenditures between $300,000 and $700,000 depending on scale and scope.

8. What is the expected ROI timeline for entering this market?

ROI timelines vary but investors should anticipate 2 to 4 years to break even, given current market size and infrastructure challenges. Growth acceleration depends on regulatory developments, increased digital adoption, and effective market penetration.

9. What are the local presence requirements for operators?

No mandatory physical presence is currently required for online operators serving Kiribati players. Operators often work remotely under offshore licenses while establishing partnerships for local marketing and support services.

10. What payment methods are available and recommended?

Recommended payment methods include mobile money platforms, Visa/MasterCard card payments, bank transfers, and emerging e-wallets. These options provide accessibility and convenience, especially for mobile-centric consumer behavior.

11. What are the advertising and marketing restrictions?

Advertising restrictions are governed by general business laws without iGaming-specific rules. Advertising must avoid misleading claims and respect cultural norms, particularly cautious targeting minors or vulnerable groups.

12. What responsible gambling measures are mandatory?

Currently, Kiribati lacks mandated responsible gambling measures. Operators are encouraged to implement self-exclusion, deposit limits, and educational warnings to align with best practices under offshore licensing standards.

13. How large is the iGaming market and what is the growth potential?

The iGaming market in Kiribati is small but growing, with estimated revenues of $1.5 million in 2025 and forecasted CAGR of 36% through 2030. Expansion hinges on improving digital infrastructure and consumer engagement.

14. Who are the main competitors and what is their market share?

No Kiribati-based operators exist; the competitive landscape is dominated by offshore international operators licensed in Malta, Curacao, and the UK. These entities serve the local population remotely, leveraging broad product portfolios and global marketing.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-optimized platforms offering low-stakes games and social betting. Peak usage occurs during evenings and weekends, with average session lengths of 20-30 minutes. Retention correlates strongly with localized content and payment convenience.

16. What are the key success factors and main challenges for new entrants?

Success requires strong local partnerships, responsive mobile platforms, compliance with international regulations, and culturally sensitive marketing. Challenges include infrastructure limitations, digital literacy barriers, and competition from established offshore brands.

Sources and References

- Kiribati Gambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Kiribati – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Kiribati Telecommunications Corporation – Annual Report 2024

- Pacific Islands Development Bank – Economic Overview

- Gaming Industry Report – IGT Publisher – 2024

- Regional Digital Economy Review – Pacific Development Forum – 2025

- Kiribati Ministry of Communication – Infrastructure Plans

- Online Gambling Legal Frameworks – International Law Review – 2025

- iGaming Market Trends Report – EGR Global – 2025

- Kiribati Population Census – 2025 Preliminary Report

- Financial Services Regulatory Authority (Kiribati)

- Mobile Payment Adoption Study – Pacific Telecom Insights – 2024

- Digital Literacy and Education Programs – Kiribati Ministry of Education

- National Gaming Surveys – Kiribati Research Bureau – 2025

- World Bank ICT Development Index – 2024

- E-commerce Adoption in Pacific Islands – Market Analysis 2025

- Remote Infrastructure Development Plans – Kiribati Government – 2025

- Central Pacific Internet Providers Association – 2025 Report

- Kiribati Tax Authority Publications – 2024 Updates

- International Remittance and Payment Systems Report – 2025

- COVID-19 Impact on Kiribati Economy – World Bank Analysis 2023

- Market Entry Strategies for Small Island States – Business Insights 2025

- Global Online Gambling Compliance Review – 2025

- Player Protection and Responsible Gambling Policies – IAGR 2024

- ICT Infrastructure Investment Trends – Asian Development Bank 2025

- National Digital Transformation Strategy – Kiribati 2024-2030

🎯 Gambling Databases Country Rating: Kiribati

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 3.2/10 | 🔴 Difficult 3-4 |

| Player Access Score | 5.8/10 | 🟡 Partially Legal / Grey Area |

| Overall Market Attractiveness | 3.5/10 | 🔴 Low Potential / High Uncertainty |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Regulatory Void: There is NO explicitly legal framework for online gambling. Operations exist in a dangerous “grey zone” with no legal protections.

- Micro-Market Limitations: With a population of only 130,000 and GDP of $0.3 billion, the Total Addressable Market (TAM) is negligible for major operators.

- Infrastructure Barriers: Internet penetration is only 58.5% with high latency and bandwidth caps, making live dealer and data-heavy slots unplayable for most users.

- Payment Friction: Credit card penetration is extremely low; reliance on cash and local mobile money makes deposits/withdrawals difficult for offshore entities.

- Legislative Uncertainty: As a recovering economy reliant on foreign aid, Kiribati is susceptible to sudden regulatory pressure from Australia or New Zealand to ban offshore gambling.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.5/3.0 | Grey Area (+0.5): Online gambling is undefined. It is neither explicitly legal nor illegal. Deductions: Lack of legal definition creates immense liability risk (-1.0). No protection for operators (-1.0). Unenforced laws (-0.5). |

| Licensing Process | 25% | 0.0/2.5 | No Licensing Available (0): There is no specific iGaming license. Local land-based licenses exist but the process for online is undefined/non-existent. You cannot obtain a clear legal mandate to operate. |

| Taxation & Costs | 20% | 1.5/2.0 | Standard Corp Tax (+1.5): 17.5% Corporate Tax applies. No specific GGR tax is legislated. Deductions: “Undefined” tax status creates retroactive tax risk (-0.5). Low ARPU ($125/year) makes unit economics poor despite low tax. |

| Operational Requirements | 15% | 1.0/1.5 | Minimal Requirements (+1.5): No local presence required because no law exists. Deductions: Severe infrastructure limitations require mobile-lite optimization (-0.5). |

| Market Environment | 10% | 0.2/1.0 | Difficult Environment (+0.2): Ranked low on Ease of Doing Business. Deductions: Extremely small market size (-0.5). Poverty levels limit disposable income significantly (-0.3). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.0/4.0 | Grey Area (+1.0): No specific laws prohibit players from accessing online sites, but no laws protect them either. Deductions: Lack of regulation means no player dispute resolution (-1.0). Risks of using unregulated offshore sites (-2.0). |

| Practical Accessibility | 30% | 2.0/3.0 | No Blocking (+3.0): No ISP blocking or VPN requirements. Deductions: Poor internet speeds/reliability make access difficult (-0.5). Limited digital payment methods (-0.5). |

| Player Penalties | 20% | 2.0/2.0 | No Penalties (+2.0): There are no records of players being fined or prosecuted for online gambling. |

| Market Availability | 10% | 0.8/1.0 | Offshore Only (+0.25): Zero local options. Players must use offshore sites. Bonus: Access to almost all major international grey-market brands (+0.55). |

🔍 Key Highlights

Strengths (For Operators)

- No ISP Blocking: The government does not currently block offshore gambling domains.

- No GGR Tax: There is no specific gaming tax, meaning operators technically only face corporate tax (if they incorporate locally) or zero tax (if offshore).

- Mobile First: 60%+ mobile connection rate aligns with modern iGaming trends, though data costs are high.

⛔️ CRITICAL RISKS AND CHALLENGES

- Market Size Viability: With only ~12,000 active gamers and $1.5M total projected revenue for the entire country, the ROI on localization is virtually non-existent.

- Infrastructure Gap: Average speeds of 10-20 Mbps with high latency render modern, heavy-asset casino games unplayable.

- Payment Ecosystem: High reliance on cash and specific mobile money solutions (K-Express) makes deposit processing a nightmare for standard offshore processors. Credit card use is minimal.

- Regulatory Ambiguity: The “undefined” status is a double-edged sword. While not illegal, there is no legal recourse if the government seizes assets or bans IPs overnight.

- Low ARPU: Estimated ARPU is extremely low ($125/year) compared to developed markets, making customer acquisition costs (CAC) disproportionately high relative to lifetime value (LTV).

Player-Specific Issues

- Zero Consumer Protection: Players have no recourse if an offshore operator refuses to pay out.

- Data Costs: High cost of mobile data limits session times and frequency of play.

- Scam Risk: The lack of regulation makes Kiribati players targets for predatory, unlicensed casinos.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $50,000 – $100,000 (Low, mostly for platform localization)

Monthly Operating Costs: $10,000 – $20,000 (Minimal)

Effective Tax Rate on Revenue: 0% (Offshore) to 17.5% (Local Corporate)

Customer Acquisition Cost: Low ($20-50), but high relative to LTV.

Time to Breakeven: 12-18 months (due to low volume)

Time to Positive ROI: 24+ months

Profitability Assessment: EXTREMELY LOW. While entry costs are low, the revenue ceiling is incredibly low. A successful operator might capture 10% of the market, which equates to perhaps $150,000 in annual revenue. For most tier-1 and tier-2 operators, the compliance overhead exceeds the potential profit.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Low | Currently no enforcement or blocking, but revenue potential is negligible. |

| Licensed Sports Betting Operators | Medium | Lack of clear licensing path makes “legal” entry impossible; must operate in grey zone. |

| Affiliates/Advertisers | Low | No specific regulations against advertising, but limited local inventory/channels. |

| Payment Processors | Medium | Processing for “undefined” gambling activities may trigger internal compliance blocks at Visa/Mastercard. |

| Company Directors/Executives | Low | Extradition risk is low for gambling, but reputational risk is present. |

🚨 Extradition and International Enforcement

Extradition Treaties: Kiribati has extradition arrangements within the Commonwealth framework (UK, Australia, New Zealand, Fiji). It generally cooperates with Pacific regional partners.

Enforcement History: There are zero recorded cases of extradition from Kiribati for online gambling offenses. Enforcement focus is entirely on local, physical crime and corruption.

Safe Jurisdictions: N/A. Kiribati is not a safe haven; it simply lacks the resources to prosecute international cyber offenses.

Travel Risk: Low. Directors traveling to Kiribati are unlikely to face arrest for offshore gambling operations, provided they are not engaging in local fraud or money laundering.

📋 Final Verdict

Kiribati receives an Operator Ease Score of 3.2/10 and a Player Access Score of 5.8/10, resulting in an overall market attractiveness rating of 3.5/10.

HONEST ASSESSMENT: Kiribati is a “Why Bother?” market. It is not legally prohibited, but it is structurally and economically unviable for 99% of operators. The combination of a tiny, low-income population, terrible internet infrastructure, and a complete lack of regulatory framework means there is no money to be made here safely. It is a grey market that offers high friction for almost zero reward.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Crypto-Casino (Grey Market) specializing in ultra-lightweight, low-bandwidth games.

- An operator with a specific Pan-Pacific strategy aggregating traffic across 10+ island nations.

❌ Definitely Avoid If You Are:

- A Publicly Listed Company: The regulatory ambiguity creates compliance risks that shareholders will not accept.

- Live Casino Focused: The internet infrastructure cannot support video streaming reliably.

- Relied on Credit Card Processing: Local penetration is too low to sustain a business model.

- Looking for Growth: The market is capped at ~$1.5M total; there is no scaling potential.

⚠️ BOTTOM LINE: Avoid this market. The revenue potential does not justify the technical setup costs or the regulatory ambiguity.