South Korea presents a complex but potentially lucrative opportunity for iGaming operators due to its advanced digital infrastructure and large, tech-savvy population. However, the iGaming market operates within one of the most stringent regulatory frameworks in Asia, limiting legal online gambling mostly to state-controlled entities and a single casino accessible to locals.

Recent legislative and regulatory reforms in 2025 aim to strengthen consumer protection while addressing illegal gambling activities and pseudo-casinos. These developments signal cautious market opening signals, but significant regulatory challenges remain to secure lawful market entry and sustainable operations.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

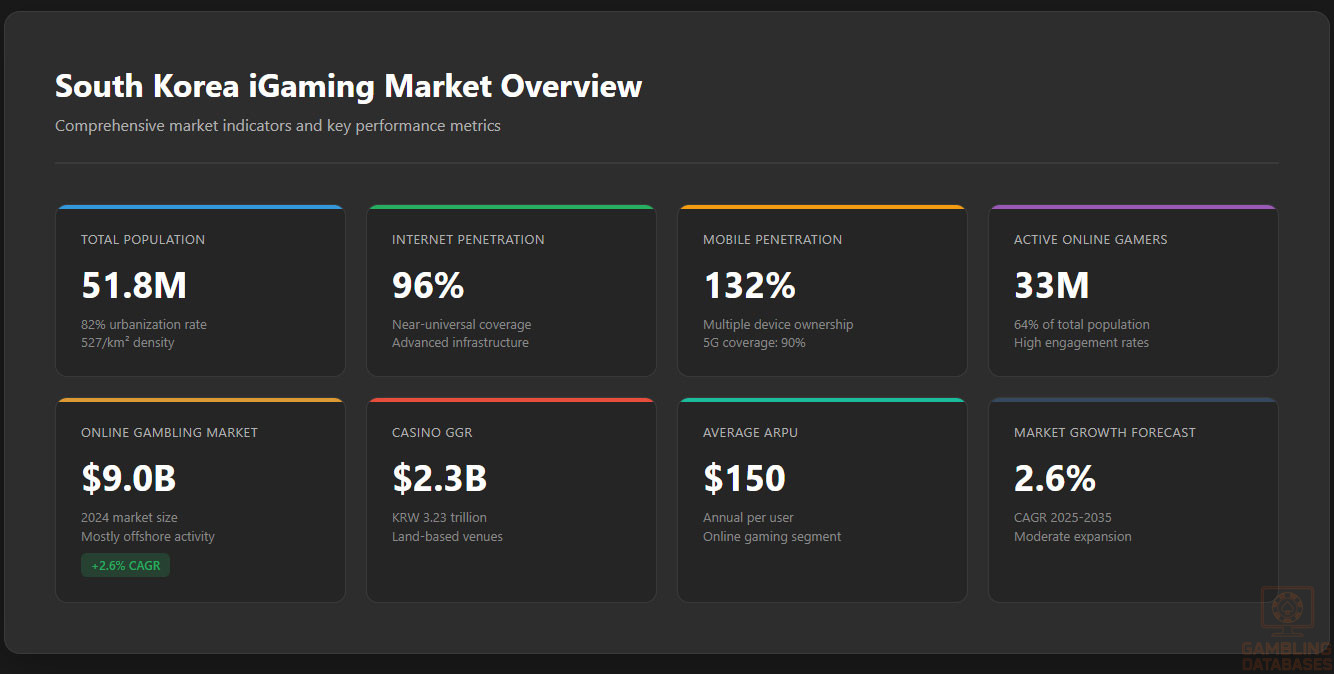

| Population | 51.8 million |

| Urbanization Rate | 81% |

| GDP (Nominal) | KRW 2,000 trillion (~USD 1.5 trillion) |

| GDP per Capita | USD 29,000 |

| Internet Penetration Rate | 96% of population |

| Mobile Penetration Rate | 132% (multiple device ownership) |

| Active Online Gamers | 33 million (≈ 64% of population) |

| Online Gambling Market Size (2024) | USD 9.0 billion |

| Total Gambling Industry Value | KRW 2.69 trillion (≈ USD 2.0 billion) |

| Casino Gross Gaming Revenue (2024) | KRW 3.23 trillion (≈ USD 2.3 billion) |

| Market Growth Forecast (2025-2035 CAGR) | 2.6% for online segment |

| Average Revenue Per User (ARPU) – Online Gaming | USD 150 annually |

| Legal Gambling Forms | State lotteries, Sports betting monopoly, Kangwon Land casino |

| Online Gambling Legality | Generally illegal except state lottery |

| Gambling Regulatory Authority | Ministry of Culture, Sports and Tourism (MCST) |

| Licensing Cost – Casinos | Project dependent; multimillion USD investment |

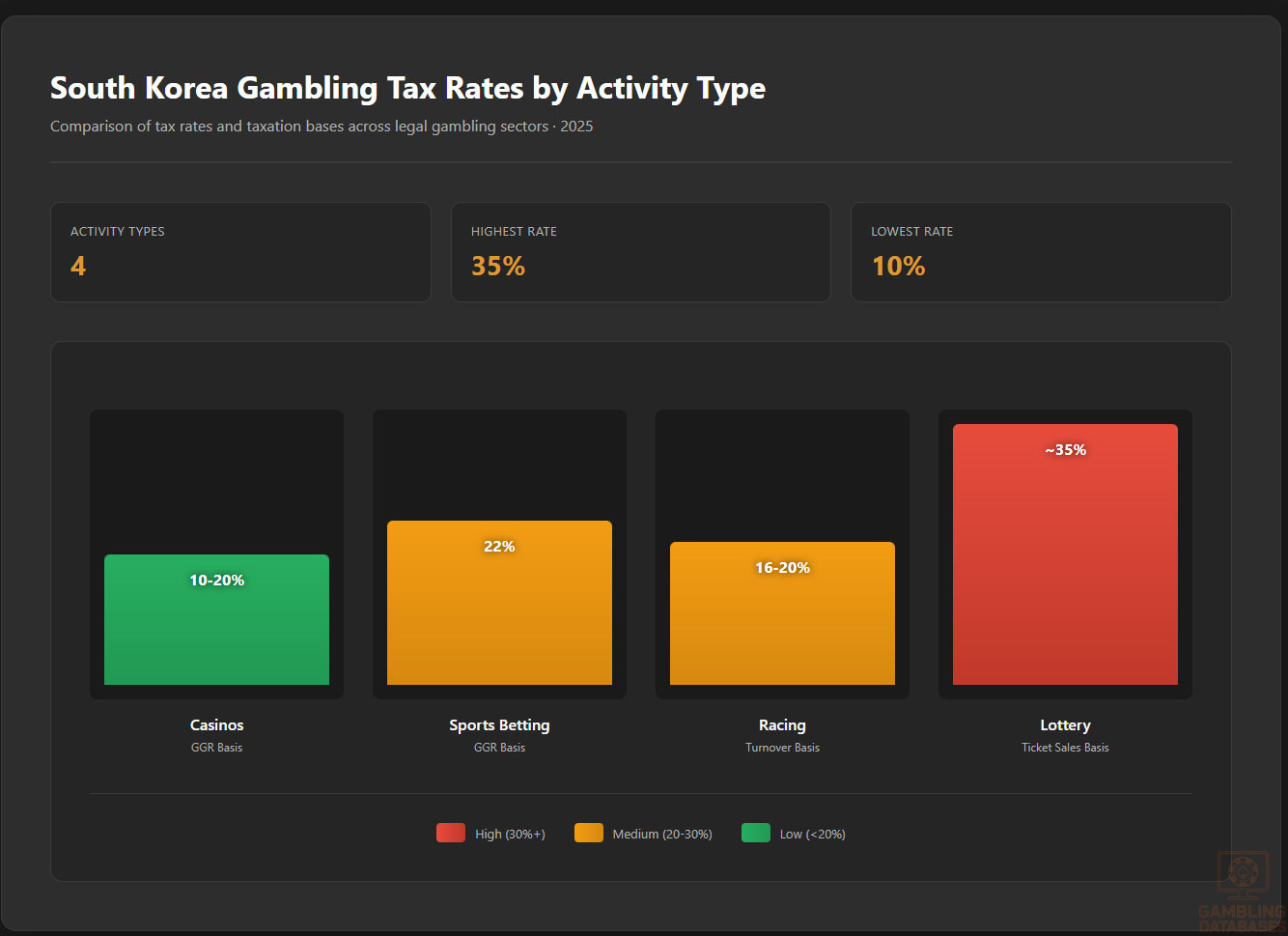

| Tax on Casino Operators | 10-20% Gross Gaming Revenue (GGR) |

| Sports Betting Tax Rate | 22% GGR (state monopoly) |

| Lottery Tax Rate | ~35% on ticket sales |

| Tax on Player Winnings | Progressive 22%-40% above KRW 2 million threshold |

| License Duration | Typically 5 years, renewable |

| Operational Restrictions | Foreign operators must appoint Korea Game Domestic Agent |

| Illegal Gambling Penalties | Up to 7 years imprisonment, fines to KRW 70 million |

| Advertising Restrictions | Strict, limited channels with content controls |

| Regulatory Changes in 2025 | Tourism Promotion Act amended to close pseudo-casino loopholes |

| Enforcement Body | National Gambling Control Commission & Police |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

South Korea maintains a restrictive and tightly controlled gambling regime. The only legal forms of gambling available to local residents are the state-run lottery and the Sports Toto sports betting monopoly operated by the government. Kangwon Land Casino is the sole physical casino permitting Korean nationals to play, established in a special economic zone with strict regulatory oversight.

Land-based gambling activities outside these bounds remain illegal for locals, with some limited venues such as certain internet cafés and arcades operating under specific licenses. Foreign tourists, however, have broader access to casino offerings throughout the country.

Land-Based Gambling Activities

Physical gambling venues can be categorized as follows:

- Kangwon Land Casino: The only legal venue for locals, operating under a special act with high compliance and significant tax obligations.

- Resort Casinos: Several operate for foreign visitors only, requiring government licensing and strict controls.

- Sports Betting Outlets: Limited to government-operated Sports Toto locations.

- Internet Cafés and Arcades: Licensed venues allowing limited gaming and betting with age verification and responsible gambling protocols.

- Horse and Boat Racing Venues: State-authorized for wagering with regulated betting systems.

Online Gambling Framework

Online gambling is broadly illegal in South Korea outside the state lottery platform. The Criminal Code classifies unauthorized online gambling as a criminal offense punishable by severe penalties. The government actively censors access to foreign operator websites through internet service providers and financial institutions, blocking transactions linked to illegal operators.

Licensed Operators and Market Players

The domestic market is dominated by state-controlled entities, including the Korea Lottery and Sports Toto, creating a near-monopoly environment. Kangwon Land remains the only licensed casino operator accepting Korean nationals, supplemented by several foreigner-only resorts licensed by the Ministry of Culture, Sports, and Tourism (MCST).

Foreign online operators cannot obtain licenses in Korea but may attempt indirect market participation by utilizing local agents or partnerships. The illegal sector remains highly competitive with numerous underground sportsbooks and casino sites serving Korean users.

Licensing Framework and Requirements

Application Process and Eligibility

The primary regulatory authority overseeing gambling is the MCST, which evaluates licensing proposals based on financial, operational, and compliance prerequisites. Licensing for land-based casinos involves a detailed proposal submission, facility inspections, and legal scrutiny, with approval periods typically spanning several months to a year.

Licensing applicants must demonstrate financial solvency, robust anti-money laundering (AML) measures, and adherence to responsible gambling guidelines. Technical standards require gaming system certification and ongoing audit compliance.

Online gambling licensing for foreign operators is currently not offered within South Korea’s jurisdiction. Instead, legislation requires operators with significant Korean user bases to appoint domestically registered gaming agents accountable to regulators.

Required documents include:

- Corporate registration and business plans

- Financial statements and projections

- Details on directors and beneficial owners

- Technical certifications for gaming software

- AML and KYC policy descriptions

- Responsible gambling program outlines

- Security and data protection compliance documentation

- Proof of capital requirements and bank references

Local Presence and Operational Requirements

For land-based operators, a physical presence and licensed facilities within designated zones are mandatory. Online operators targeting Korean users must appoint a Korea Game Domestic Agent under GIPA, regardless of physical presence. This agent functions as the local contact point for regulatory communications and compliance monitoring.

Foreign ownership of gambling enterprises is permitted but subject to regulatory approval, with partnership requirements occasionally imposed to ensure local market knowledge and responsibility. The government enforces strict domain registration rules to prevent unauthorized online gaming sites from operating freely using Korean internet infrastructure.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators must implement stringent age verification to prevent underage gambling. South Korea’s KYC and AML standards require verification of identity documents, ongoing transaction monitoring, and reporting suspicious activities. The legal minimum gambling age is 19 years.

Responsible gambling measures mandated by regulators include self-exclusion programs, limits on bet sizes and deposits, mandatory display of warning messages, and employee training in problem gambling recognition. Operators must maintain transparency through periodic disclosures of gaming odds and payout ratios.

- Mandatory age verification and identity checks

- Ongoing player activity monitoring

- Self-exclusion system availability

- Deposit and wagering limits

- Responsible gambling information dissemination

- Employee training on customer protection

Financial Monitoring and Reporting

Financial transaction monitoring requires detailed reporting of player deposits, withdrawals, and winnings exceeding regulatory thresholds. Operators submit monthly financial reports including gross gaming revenue, tax calculations, and suspicious transaction reports to MCST.

- Monthly submission of gross gaming revenue reports

- Regular AML compliance audits by independent bodies

- Suspicious activity report filings within 24 hours

- Annual financial statement submission for licensing renewal

Taxation Structure and Financial Obligations

Player Taxation

Players winning from legal gambling activities are subject to progressive taxation on winnings exceeding KRW 2 million annually. Tax rates range from 22% to 40%, integrated with overall income tax liabilities. Operators assist in withholding and reporting winnings as part of tax compliance.

Operator Taxation

| Gambling Activity | Tax Base | Tax Rate |

|---|---|---|

| Casinos (Foreigners, Kangwon Land for Locals) | Gross Gaming Revenue (GGR) | 10% – 20% |

| Sports Betting (Sports Toto) | Gross Gaming Revenue | 22% |

| Horse and Boat Racing | Turnover | 16% – 20% |

| Lottery | Ticket Sales | Approx. 35% |

License fees for casinos are substantial and project-based, reflecting the high capital investment and operational scale required. Corporate income tax of 20% applies alongside gambling-specific taxation.

Gambling Market Financial Performance

The Korean gambling market demonstrates steady revenue growth despite restrictions. Casino gross revenue reached KRW 3.23 trillion (~USD 2.3 billion) in 2024, with online gambling estimated at USD 9 billion, mostly offshore. Tax revenues from gambling contribute notably to government funds supporting social initiatives and sports development.

Year-over-year growth is forecast at 2.6% CAGR for the online segment through 2035, driven by technological advances and regulatory adjustments such as GIPA. The distribution of revenue indicates dominance by state-controlled operators, while underground markets offer untaxed economic activity at a considerable scale.

Advertising and Marketing Restrictions

Advertising gambling services is strictly regulated. Operators face bans on promoting gambling products to minors and limitations on advertising via television, radio, and digital media. Marketing must comply with content restrictions designed to limit gambling glamorization and prevent targeting vulnerable populations.

- Prohibition on advertising to minors

- Restrictions on advertising time slots and channels

- Ban on false or misleading promotions

- Regulation of sponsorship deals in sports and entertainment

- Mandatory display of responsible gambling messages

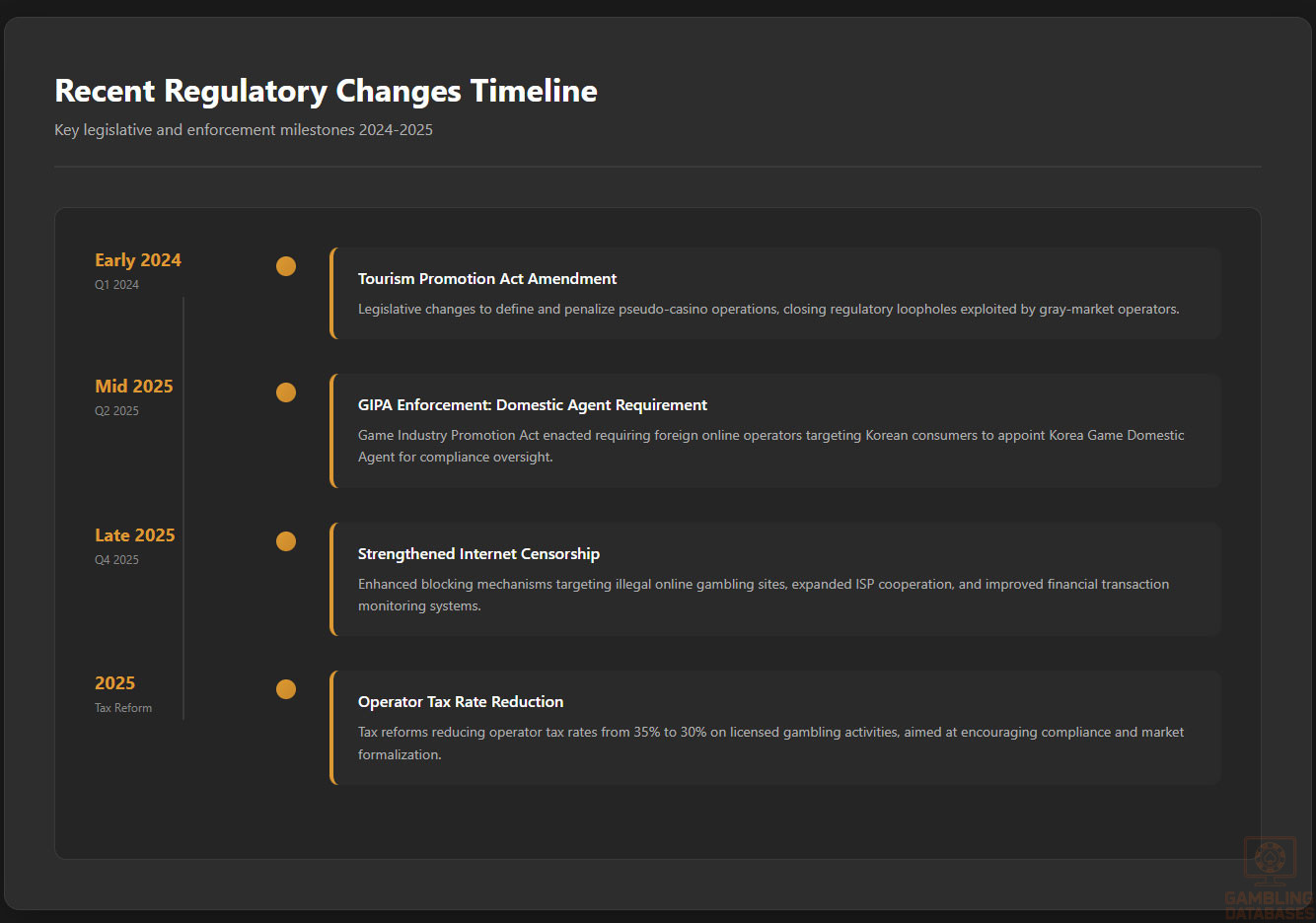

Recent Regulatory Changes and Their Impact

- Early 2024: Amendment of Tourism Promotion Act to define and penalize pseudo-casino operations

- Mid 2025: Enforcement of Game Industry Promotion Act requiring Domestic Agents for foreign operators

- Late 2025: Strengthened internet censorship targeting illegal online gambling sites

- 2025 Tax reforms reducing operator tax rates from 35% to 30% on licensed activities

These changes increased compliance costs and operational risks for illegal operators, while signaling a government intent to curb illicit activities and prepare for potential gradual regulation of the online segment.

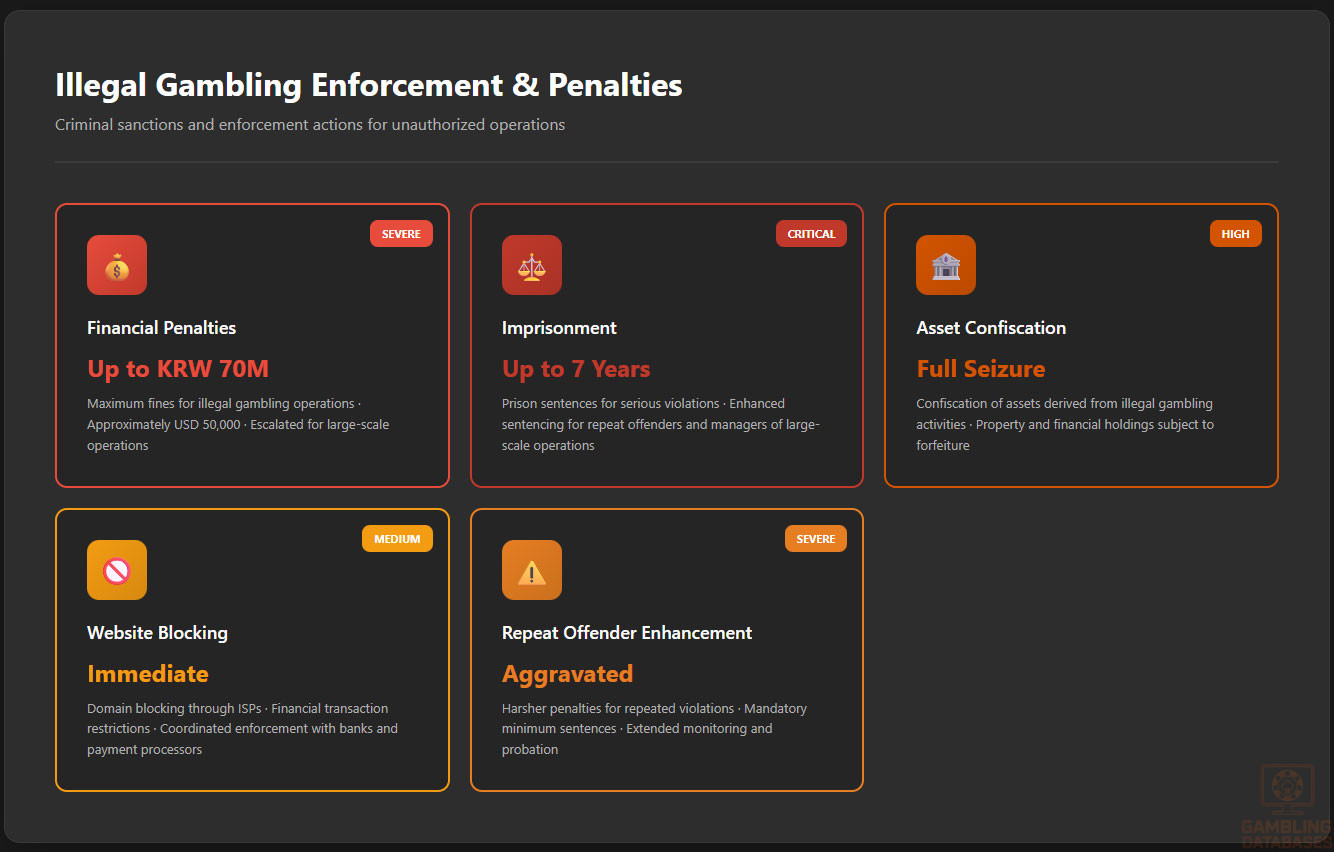

Enforcement Mechanisms and Penalties

Enforcement is rigorously applied by the National Gambling Control Commission alongside police authorities. Penalties for illegal gambling operators include fines up to KRW 70 million and imprisonment up to seven years. Repeat offenders and managers of large-scale illegal operations face harsher sentences and asset forfeiture.

- Fines up to KRW 70 million for illegal gambling operations

- Prison sentences up to 7 years for serious violations

- Confiscation of assets derived from illegal gambling

- Blocking of websites and financial transactions linked to illegal gambling

- Repeated offender enhanced sentencing

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

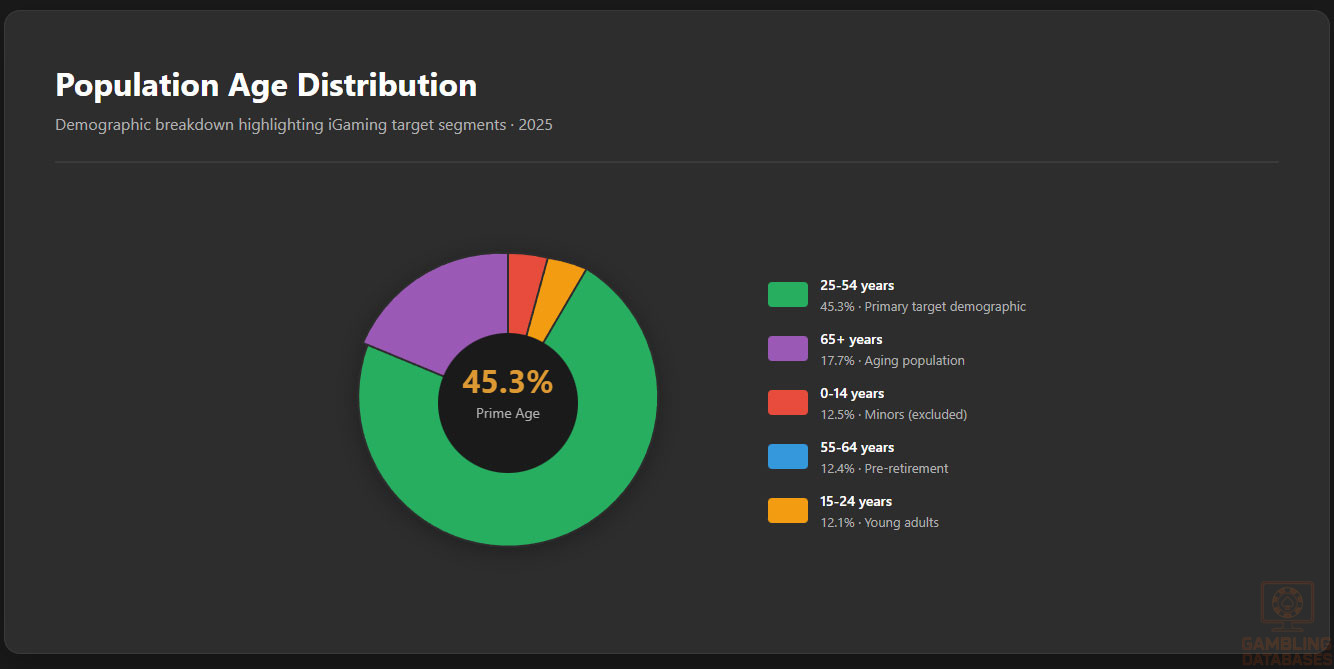

South Korea’s population in 2025 is approximately 51.7 million with a nearly balanced gender ratio of 1.00 male to 1.00 female. The median age is high, at around 45.6 years, highlighting an aging society. The fertility rate remains very low, recorded at 0.7 children per woman, significantly below the replacement level of 2.1. Urbanization is extensive, with over 82% residing in urban areas, concentrated in a handful of large metropolitan regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 12.5% |

| 15-24 years | 12.1% |

| 25-54 years | 45.3% |

| 55-64 years | 12.4% |

| 65 years and over | 17.7% |

The population density averages around 527 people per square kilometer, heavily concentrated in the northwest corridor, including Seoul and its satellite cities. Despite a modest overall population increase due to immigration, South Korea faces a demographic challenge with a shrinking youth population and a rapidly aging workforce, which affects long-term economic dynamics and consumer behavior.

Geographic Distribution

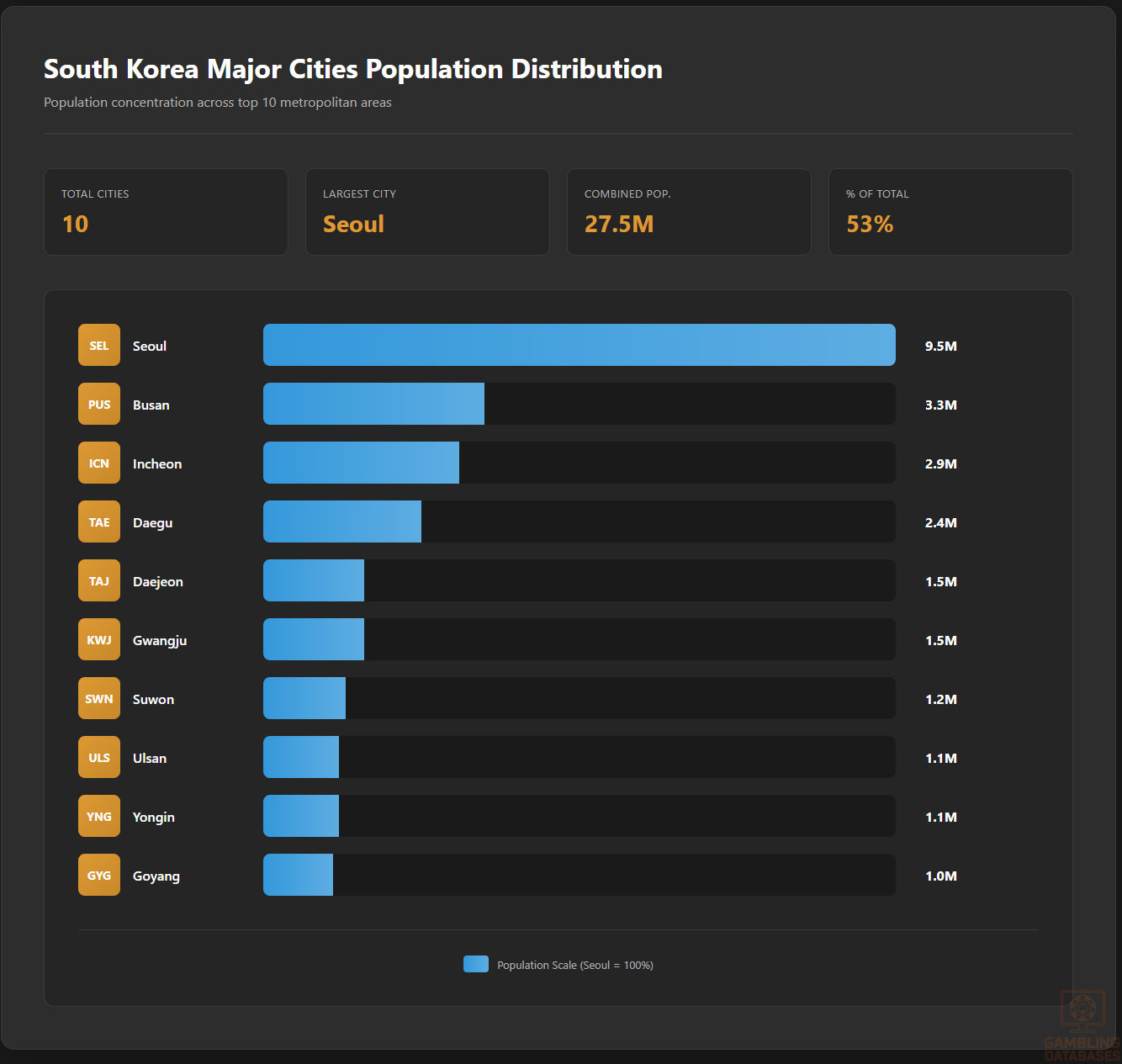

Major urban centers dominate the population landscape. Seoul, as the capital and largest city, accounts for over 9.5 million residents, making it a critical hub for digital and gambling market activities. Other significant metropolitan areas include Busan, Incheon, Daegu, and Daejeon.

- Seoul: 9.5 million

- Busan: 3.3 million

- Incheon: 2.9 million

- Daegu: 2.4 million

- Daejeon: 1.5 million

- Gwangju: 1.5 million

- Suwon: 1.2 million

- Ulsan: 1.1 million

- Yongin: 1.1 million

- Goyang: 1.0 million

Internet access is nearly ubiquitous in urban zones, with broadband and 5G coverage widespread. Land-based gambling venues concentrate mostly around Seoul metropolitan areas and select resort destinations.

Economic Indicators and Consumer Spending Power

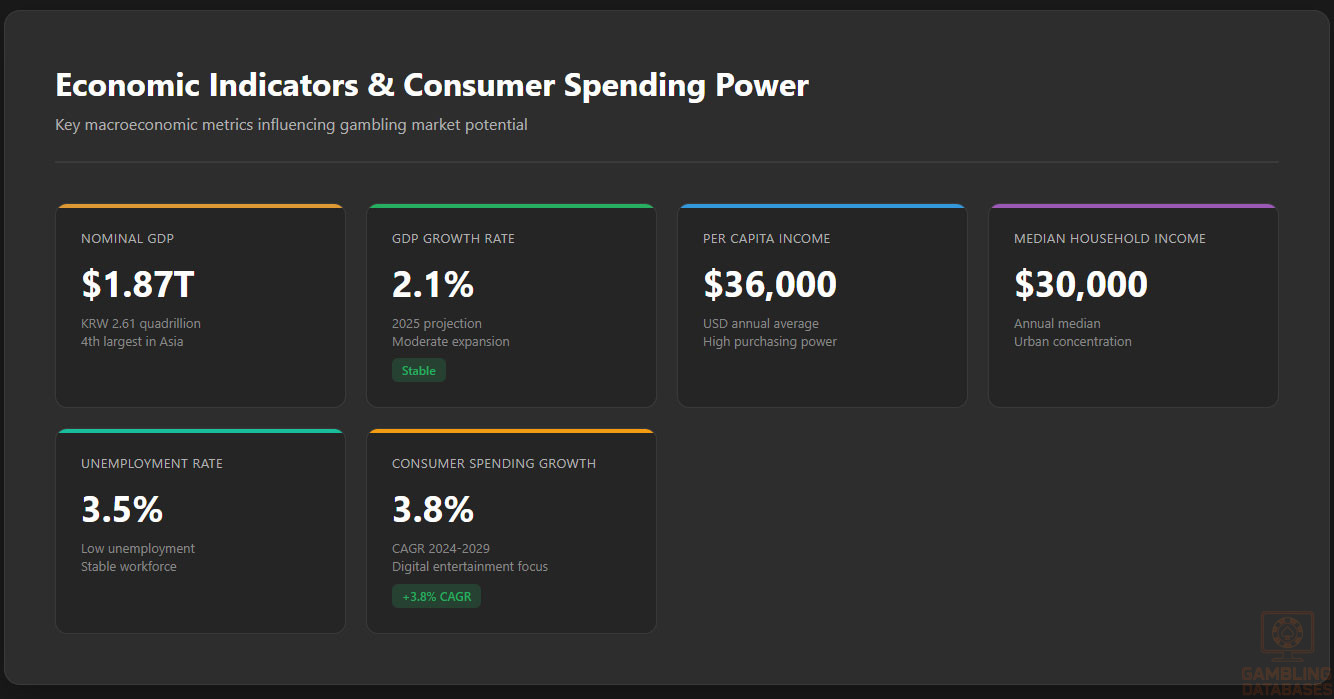

South Korea commands the fourth largest economy in Asia with a nominal GDP of approximately KRW 2.61 quadrillion (USD 1.87 trillion) in 2025. The economy is forecasted to grow steadily, albeit at a moderate pace due to demographic headwinds and global market uncertainties.

Services dominate the economic composition, contributing over half of GDP, while manufacturing and technology sectors remain critical engines of growth. Consumer spending continues to rise, boosted by rising disposable incomes and urban middle-class expansion.

Average household income situates around USD 42,000 annually, with a median income slightly lower due to income inequalities. Wealth distribution skews toward urban centers with notable gaps between metropolitan and rural areas.

Disposable income trends indicate cautious but stable growth, with consumers prioritizing digital entertainment and online commerce. Gambling-related discretionary spending is increasing despite regulatory constraints, fuelled by online gaming interest.

| Indicator | Value |

|---|---|

| GDP (Nominal) | KRW 2.61 quadrillion (USD 1.87 trillion) |

| GDP Growth Rate | 2.1% projected (2025) |

| Per Capita Income | USD 36,000 |

| Median Household Income | USD 30,000 |

| Unemployment Rate | 3.5% |

| Consumer Spending Growth | 3.8% CAGR (2024-2029) |

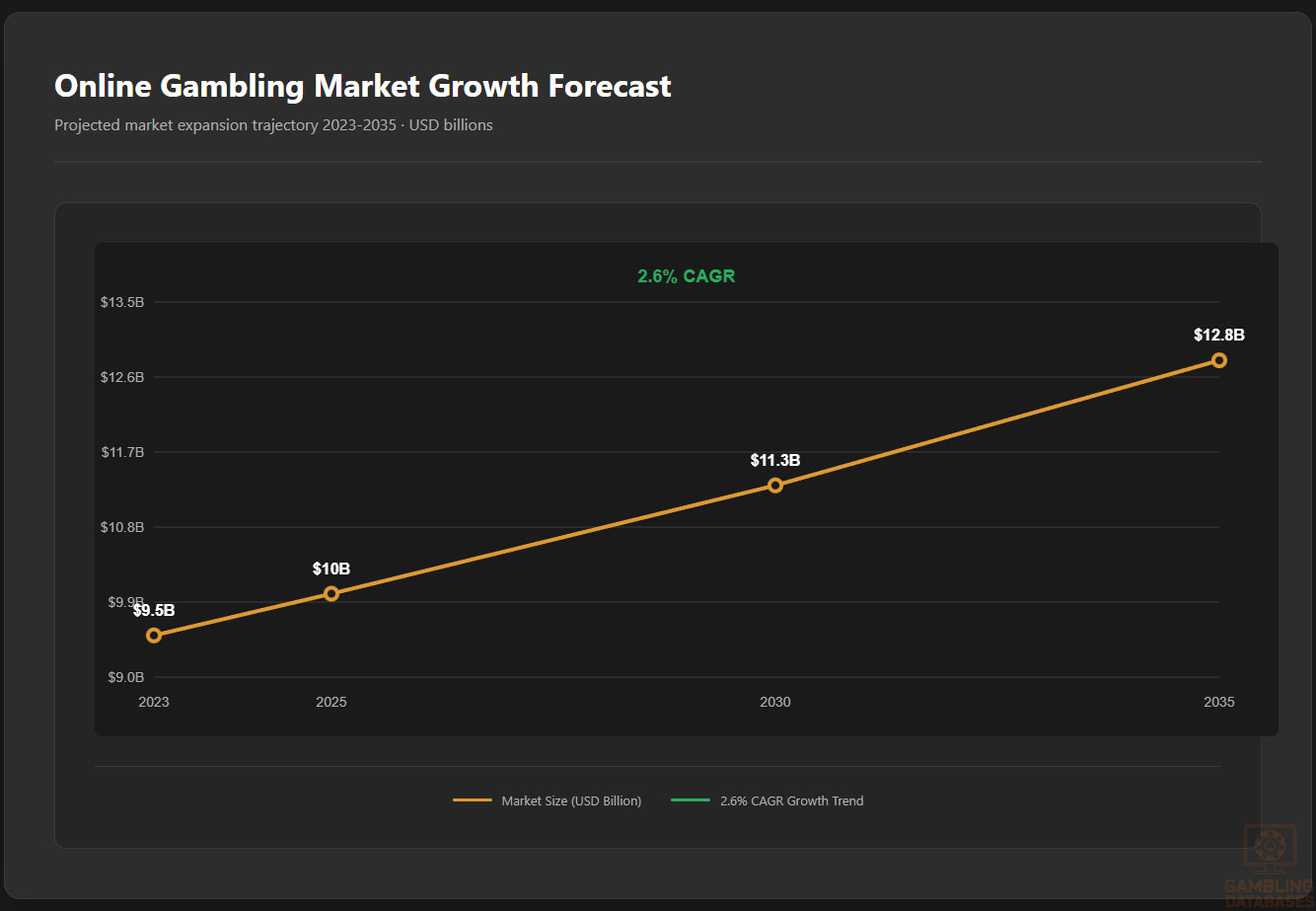

Market Size and Growth Projections

The Korean gambling market, encompassing both legal segments and estimated underground activities, is valued at roughly USD 10 billion in 2025. The online segment constitutes approximately USD 9 billion of this, reflecting high mobile and internet penetration.

Forecasts indicate a compound annual growth rate (CAGR) of about 2.6% for online gambling through 2035, while land-based casino revenues are expected to experience slower expansion, heavily dependent on fluctuating tourist inflows.

Asian consumers are shifting toward online platforms with increasing ARPU estimated at USD 150 annually per user in online gambling. User base growth is moderate due to regulatory barriers but supported by technological adoption and evolving consumer preferences.

| Year | Market Size (USD Billion) | Growth Rate (CAGR %) |

|---|---|---|

| 2023 | 9.5 | |

| 2025 | 10.0 | 2.1% |

| 2030 | 11.3 | 2.6% |

| 2035 | 12.8 |

Education, Skills, and Digital Literacy

South Korea boasts near-universal literacy with an adult literacy rate exceeding 99%. The country’s education system is lauded for its rigor and high academic achievement, producing a workforce with strong analytical and digital skills.

Strong governmental focus on digital education ensures young and working-age populations remain proficient in internet navigation, cybersecurity awareness, and mobile technology, facilitating robust engagement with online entertainment sectors including iGaming.

Cultural and Social Factors

Communication and Language

Korean is the official language, dominant in all communication, education, and media. English holds secondary status as a business and education language, especially among younger generations and professionals.

- Standard Korean (Hangul script)

- Regional dialects, especially in southern and eastern provinces

- High proficiency in informal English communication among youth

- Growing use of digital slang and emoticons on social media platforms

- Emerging bilingual content in major cities for international audiences

Cultural Attitudes

Gambling remains culturally sensitive, historically viewed with moral caution due to Confucian values emphasizing moderation and social responsibility. Despite this, an evolving entertainment market sees growing acceptance of regulated gambling forms, especially among younger urban adults.

Foreign brands are generally welcomed if perceived as trustworthy, technologically advanced, and compliant with stringent local regulations. Online gaming and esports culture enjoys widespread popularity, serving as a gateway for iGaming interest.

Problem Gambling and Social Considerations

Problem gambling is gaining recognition as a public health concern, with increasing prevalence among youth and vulnerable populations. Reports indicate a tripling in adolescent problem gambling cases over recent years, underscoring urgent need for enhanced support and prevention.

- Expansion of youth gambling counseling services

- Government awareness campaigns targeting at-risk groups

- Mandatory self-exclusion programs in licensed venues

- Research funding for addiction treatment innovations

- Collaborations with NGOs for rehabilitation services

Operators face regulatory requirements to contribute financially to social responsibility funds, conduct responsible gambling campaigns, and implement player protection technologies.

Political Structure and Governance

South Korea is a democratic republic with a stable political system providing consistent regulatory environments. The government is proactive in adjusting policies to balance innovation with protection in the digital and entertainment sectors.

International relations favor cross-border cooperation in law enforcement and regulatory harmonization, which impacts illegal gambling control efforts. Political stability and robust judicial processes create a predictable business climate for long-term investment.

Technology Adoption and Digital Behavior

Internet and Digital Usage

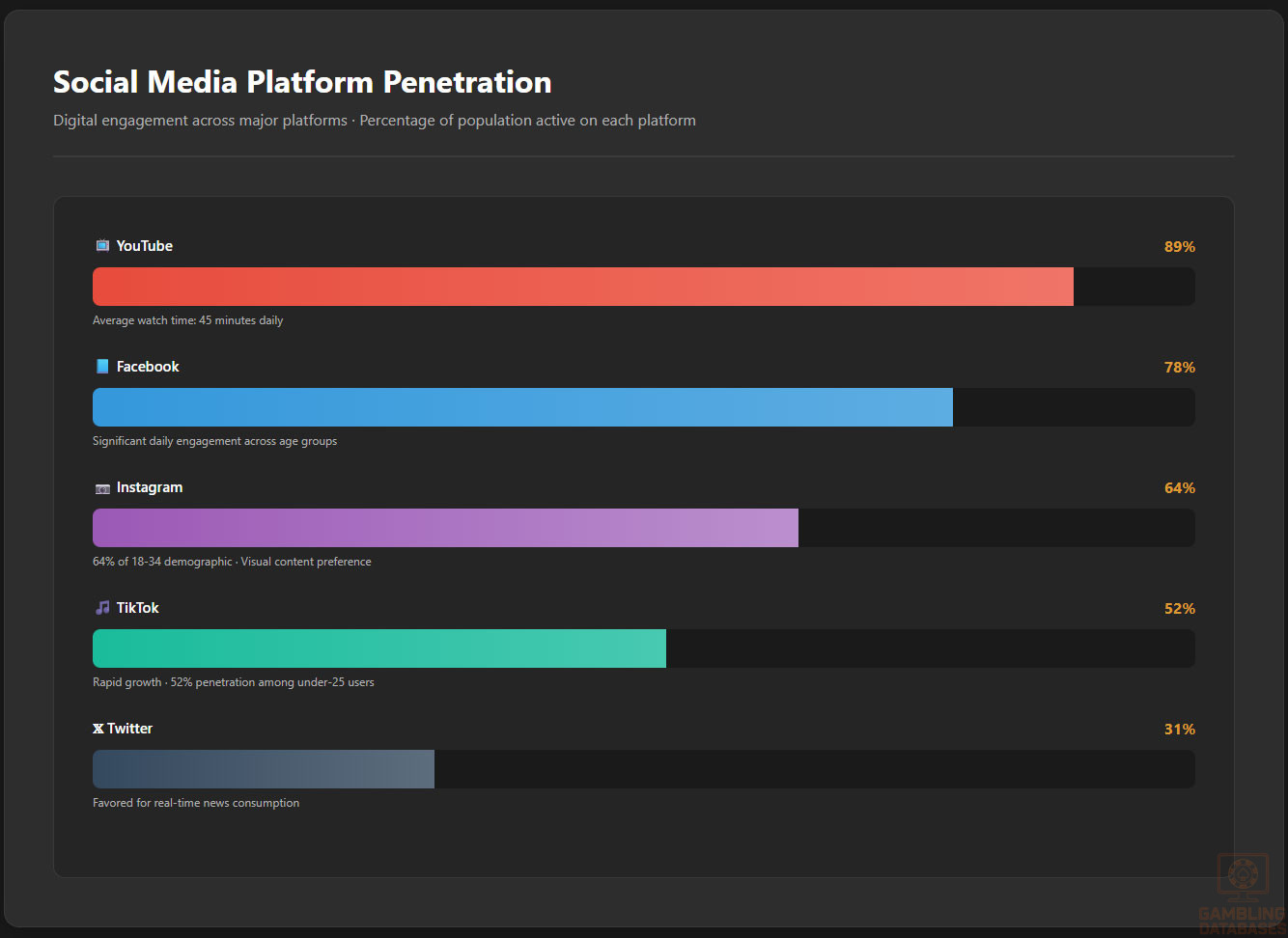

South Korea ranks among the highest globally for internet penetration, reaching over 97% of the population. Mobile device adoption exceeds 130%, with many users owning multiple devices.

Daily internet usage averages over four hours, encompassing social media, online shopping, and gaming. Social media penetration is also extensive, with nearly 95% of the population active on multiple platforms.

- Facebook: 78% penetration with significant daily engagement

- YouTube: 89% penetration, average watch time 45 minutes daily

- Instagram: 64% of 18-34 demographic, preference for visual content

- TikTok: Rapid growth with 52% penetration among under-25 users

- Twitter: 31% penetration, favored for real-time news consumption

- Naver Blog: Popular for content sharing and reviews, esp. local topics

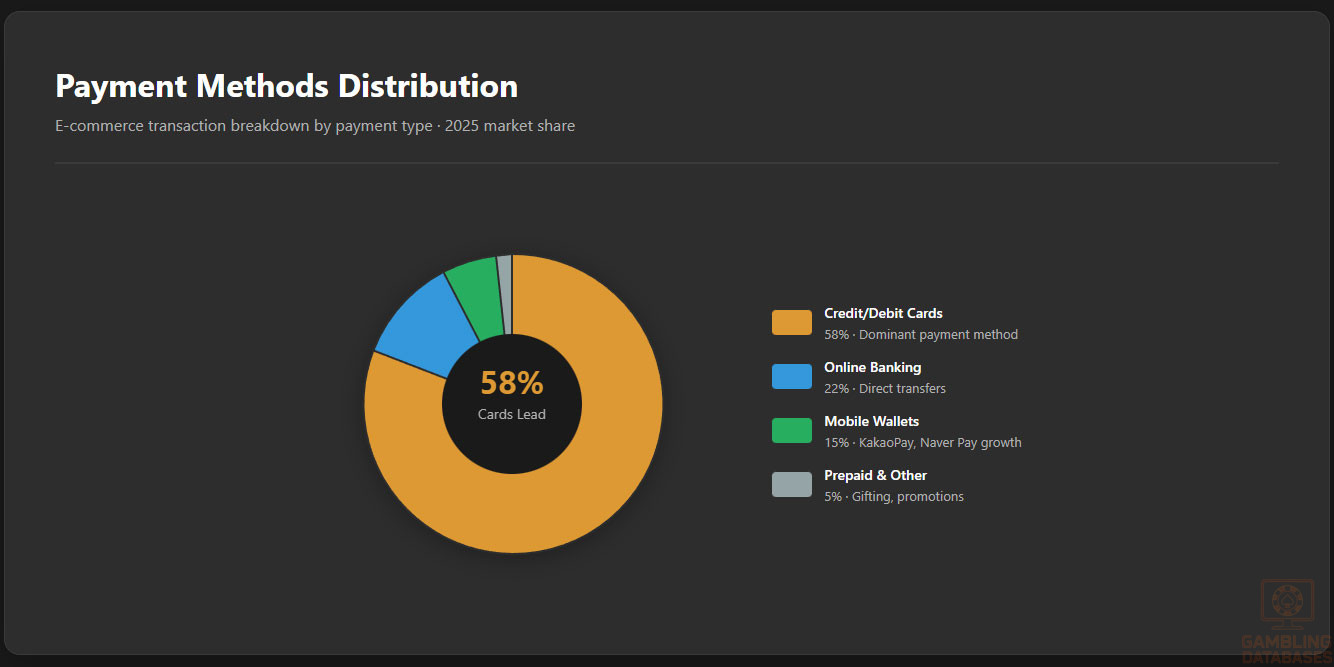

Digital Payment Behavior

Payment methods reflect a mature, digitally integrated economy. Card payments dominate e-commerce, followed by online banking and mobile wallets. Cryptocurrency adoption remains marginal but growing among tech-savvy segments.

- Credit/debit card payments: 58% of e-commerce transactions

- Online banking transfers: 22% market share

- Mobile wallets (KakaoPay, Naver Pay): 15% and growing rapidly

- Prepaid cards and gift cards: Used mainly for gifting and promotions

- Cryptocurrency: Small niche, mostly outside mainstream adoption

Gaming and Gambling Preferences

Current Market Participation

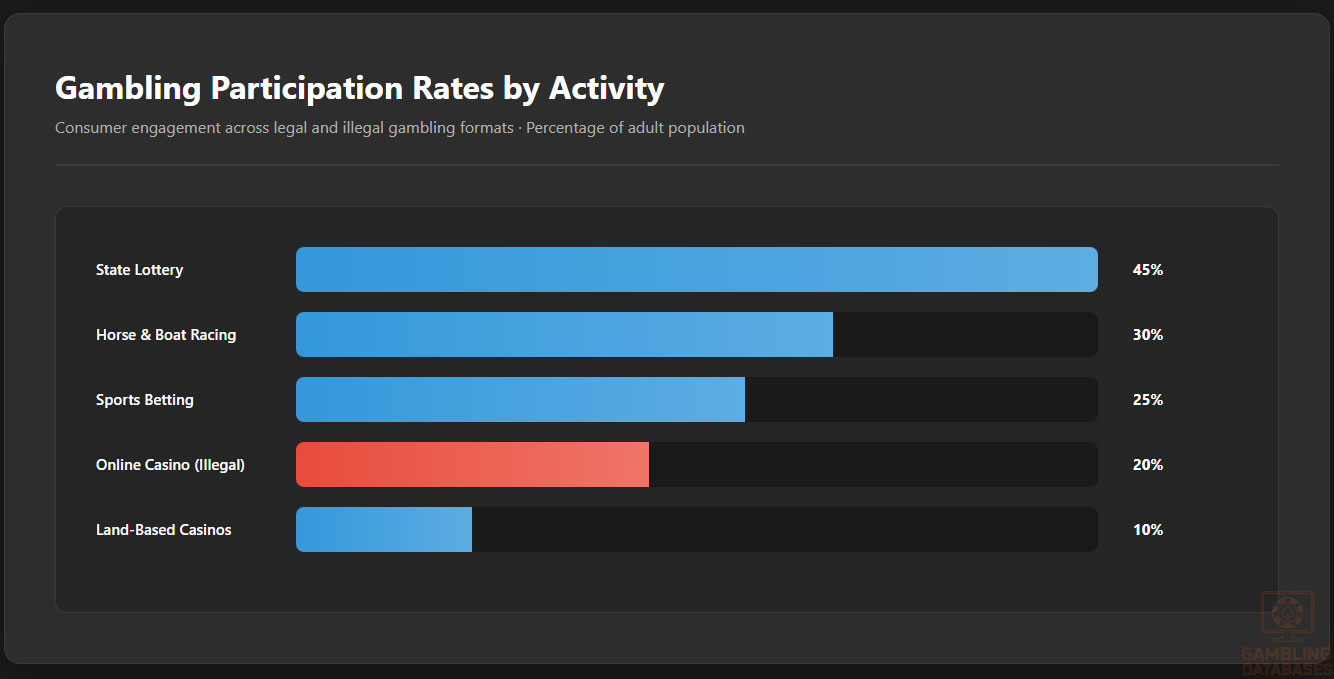

A majority of South Korean adults engage in some form of gambling, legal or otherwise, with preferences shaped by availability and legality. The top gambling activities include state lotteries, horse racing, and sports betting, with a substantial underground market for online casino games.

- State Lottery Participation: 45%

- Horse and Boat Racing Betting: 30%

- Sports Toto (Sports Betting): 25%

- Online Casino (Illegal/Offshore): Estimated 20%

- Land-Based Casino Visits (Foreigners only): 10%

| Activity | Participation Rate (%) |

|---|---|

| State Lottery | 45 |

| Horse and Boat Racing | 30 |

| Sports Betting | 25 |

| Online Casino (Illegal) | 20 |

| Land-Based Casinos (Foreigners) | 10 |

Consumer Behavior Patterns

South Korean consumers show strong preference for mobile-first platforms with easy access and intuitive interfaces. Peak gambling activity aligns with evening hours and weekends, particularly around major sports events and lottery draws.

Retention rates remain high for operators offering robust loyalty programs and seamless payment integration. Spending tends to concentrate in lower to mid-tier betting ranges, reflecting cautious risk behavior amid regulatory constraints.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

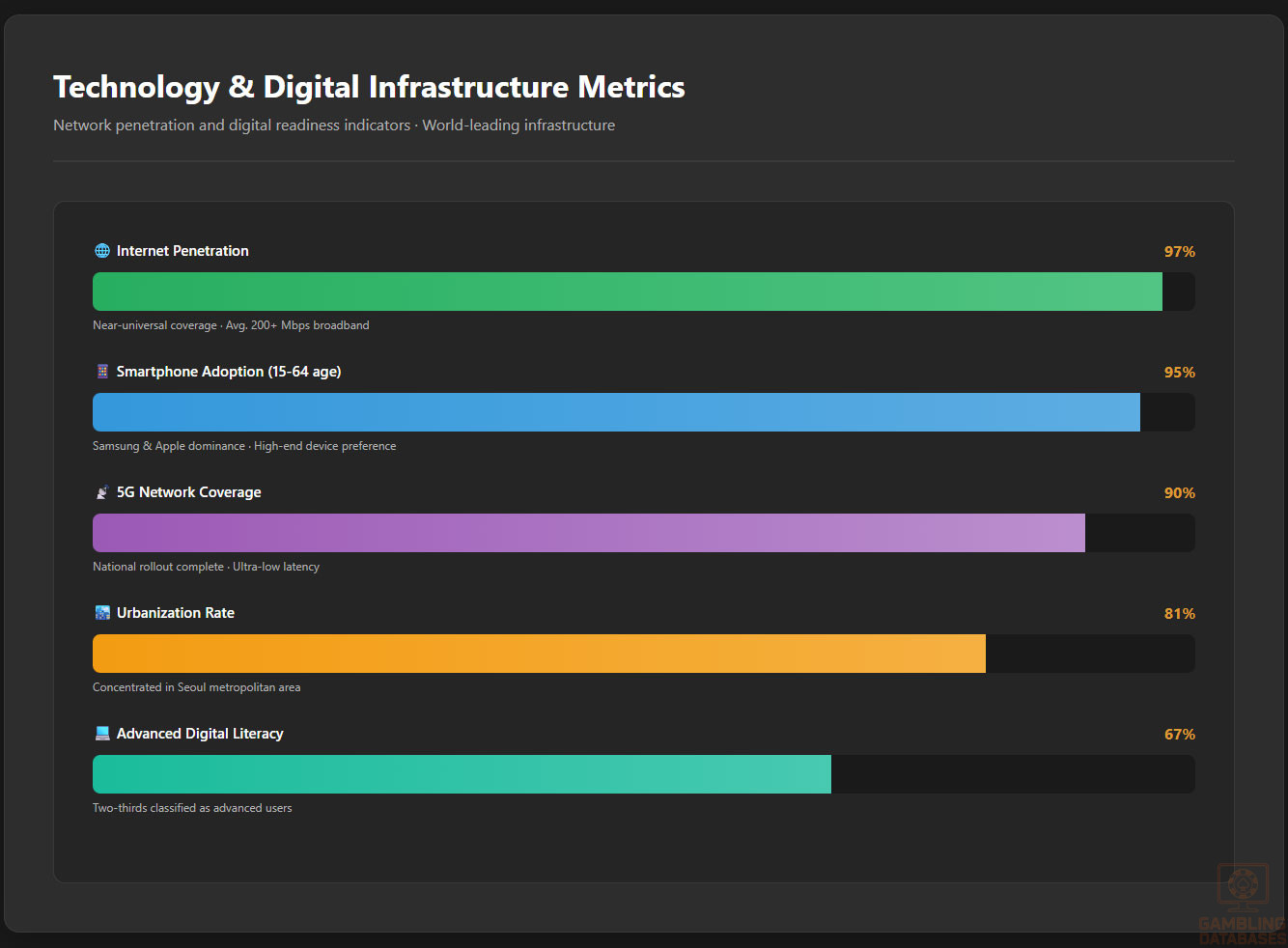

South Korea boasts one of the world’s most advanced digital infrastructures, with internet penetration exceeding 97% of the population. Broadband networks are predominant, particularly fiber-optic based, delivering average download speeds above 200 Mbps nationwide. Mobile internet complements broadband with high-speed 4G coverage present throughout urban and rural areas.

Network reliability is exceptional, supported by significant government and private-sector investment aimed at sustaining leadership in ICT development. The country is a global benchmark for low latency and minimal downtime, enabling smooth real-time gaming and streaming experiences critical for iGaming platforms.

5G and Future Technology Deployment

5G technology deployment is widespread, covering over 90% of the population as of 2025. Major telecom operators have completed national rollout projects, focusing on enhancing capacity and reducing latency to support emerging applications including cloud gaming and augmented reality.

Future plans include expansion to ultra-reliable low latency communications (URLLC) and 6G research initiatives. Continuous upgrades emphasize smart city integrations and IoT ecosystem development enhancing digital business frameworks.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The competitive telecom market features multiple network operators providing high-quality service with attractive pricing models. Market share distribution favors three major players, complemented by smaller MVNOs targeting niche segments.

- SK Telecom: Largest operator with approximately 40% market share

- KT Corporation: Around 30% share, pioneer in broadband services

- LG Uplus: 25% market share, aggressive 5G network expansion

- MVNOs: Account for 5% market share, offering budget and specialty plans

- New entrants focusing on enterprise and IoT connectivity

Device Penetration

Smartphone adoption exceeds 95% among Koreans aged 15 to 64 years. Consumer preferences favor high-end Android and iOS models, with Samsung and Apple dominating device market share. Mobile usage patterns emphasize high daily engagement across social media, gaming, and digital payments.

Financial Services and Payment Infrastructure

Banking System Structure

South Korea’s banking sector is highly developed, supporting widespread digital banking adoption. Account penetration rates near 90% with rapid growth in mobile banking and fintech solutions.

- Kookmin Bank: Largest with 25% market share

- Hana Bank: 18% market share and strong SME focus

- Woori Bank: 15% market share, extensive branch network

- Shinhan Bank: 16% market share, early fintech adopter

- Industrial Bank of Korea: Specializes in corporate banking

Payment Processing Options

South Korea enjoys a diversified payment ecosystem integrating traditional and digital channels. Credit and debit cards dominate transactions, complemented by robust online banking and multiple e-wallet options catering to consumer convenience.

- Credit and Debit Cards: Visa, Mastercard, domestic BC Card widely accepted

- Online Banking Transfers: Supported by interbank networks with real-time settlement

- Mobile Wallets: KakaoPay, Naver Pay lead rapid growth among young adults

- Prepaid Cards: Popular for gifting and promotions

- Cryptocurrency: Growing niche, limited mainstream integration

E-commerce and Digital Economy

South Korea’s e-commerce market ranks as the fifth largest globally with annual revenues exceeding USD 150 billion. Online retail penetration is over 70%, driven by consumer trust in payment security, logistics efficiency, and digital marketing sophistication.

Digital services including streaming, cloud computing, and digital gaming thrive in an ecosystem supported by high internet speeds and consumer readiness. Trust in online commercial transactions is high, fostering rapid adoption of new digital products and platforms including iGaming offerings.

Business Environment and Regulatory Framework

Ease of Business Operations

South Korea ranks in the top 10 globally for ease of doing business, benefitting from streamlined company registration procedures, transparent tax systems, and robust intellectual property protections. Foreign investment policies encourage multinational participation, with special economic zones offering incentives to technology and gaming sectors.

Operational costs are moderate relative to developed markets, with significant government subsidies available for technology-driven startups and digital enterprises.

Corporate Structure and Registration

Available legal entities include Limited Liability Companies (LLC), Joint-Stock Corporations, and Foreign Branch Offices. LLCs are preferred for flexibility and simplified compliance, whereas Corporations suit larger enterprises requiring equity finance.

Foreign ownership is generally unrestricted but subject to regulatory vetting, especially for gambling-related activities, which require approval and local partnerships as mandated by law.

- Certificate of Incorporation

- Articles of Association

- Director and Shareholder Information

- Proof of Registered Office

- Tax Registration Certificate

- Bank Account Details

- Foreign Investment Approval Documents (if applicable)

Taxation Framework

Corporate income tax in South Korea stands at a progressive rate with a standard maximum of 25%. Special economic zones provide tax holidays and reduced rates up to 10% for qualifying tech companies. The country maintains double taxation treaties with over 90 nations, facilitating cross-border business operations.

- United States

- China

- Japan

- Germany

- United Kingdom

- Australia

- Singapore

- France

- Canada

- India

Personal income tax rates range from 6% to 45% progressively, supported by comprehensive social security contributions. Tax residency is based on stay duration and domicile, impacting withholding tax requirements for foreign operators’ employees and contractors.

Market Entry Considerations

Recommended Entry Strategies

Entering the South Korean iGaming market demands navigating complex regulations with strategies emphasizing local partnerships and compliance. Leveraging domestic agents and engaging with regulatory authorities early facilitates smooth licensing processes.

- Joint ventures with established Korean firms to access distribution channels

- Appointment of Domestic Agent under Game Industry Promotion Act

- Investment in localized mobile platforms and payment integrations

- Compliance-focused marketing strategies respecting advertising bans

- Development of responsible gambling programs aligned with national standards

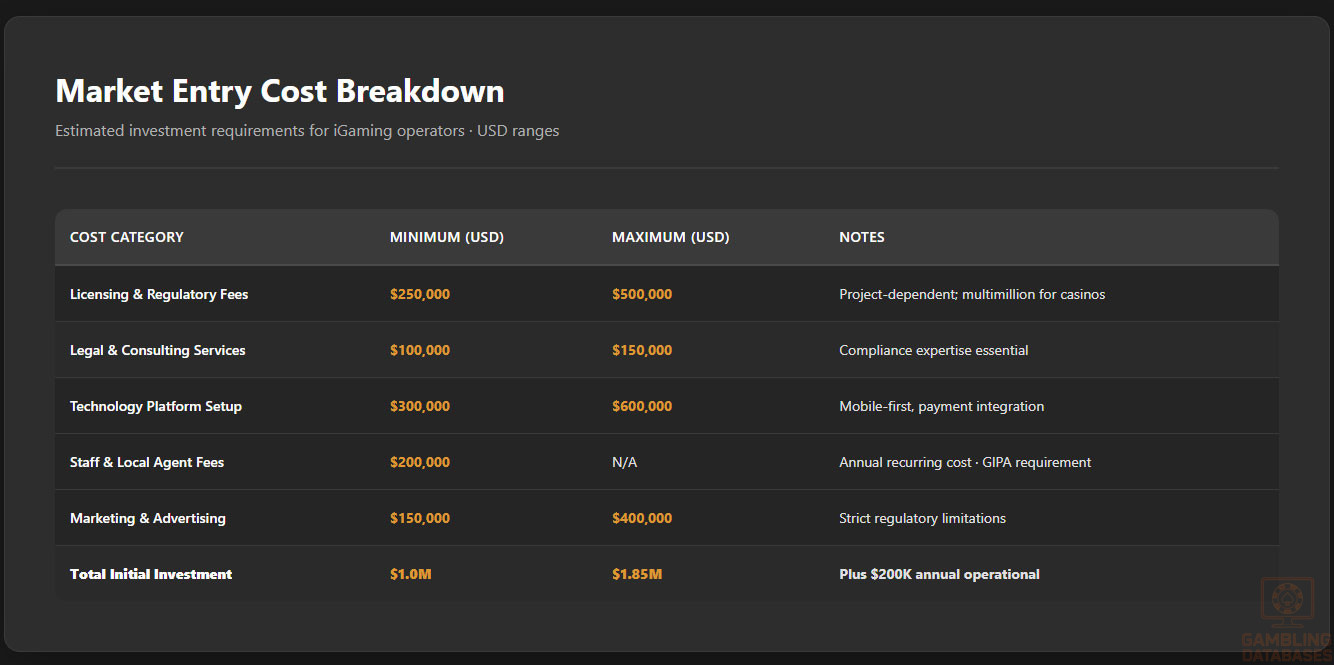

Typical Costs and Timelines

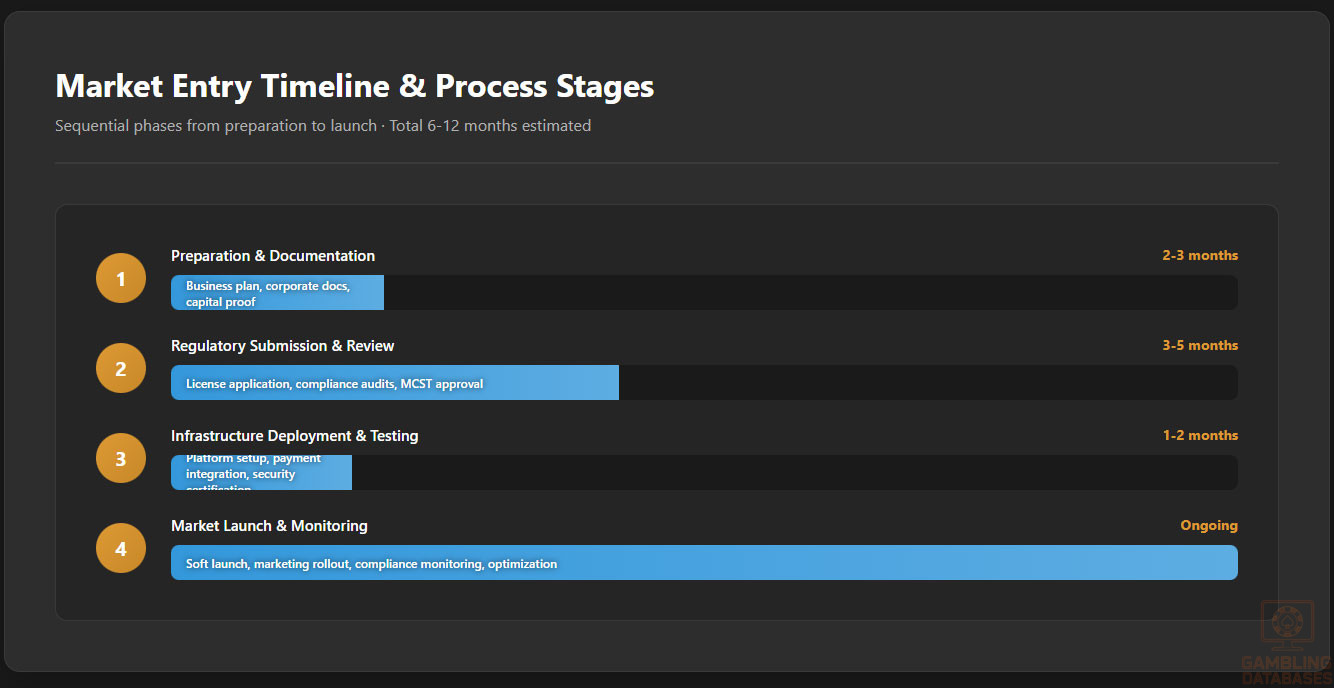

Initial market entry costs include licensing fees, legal consultation, technology setup, and local staffing expenses. Regulatory approvals typically require 6 to 12 months, depending on entity type and application completeness.

Operational costs vary by scale, with ongoing compliance and tax obligations representing significant budget lines.

| Cost Category | Estimated Cost |

|---|---|

| Licensing and Regulatory Fees | USD 250,000 – 500,000 |

| Legal and Consulting Services | USD 100,000 – 150,000 |

| Technology Platform Setup | USD 300,000 – 600,000 |

| Staff and Local Agent Fees | USD 200,000 annually |

| Marketing and Advertising | USD 150,000 – 400,000 |

- Preparation and Documentation: 2-3 months

- Regulatory Submission and Review: 3-5 months

- Infrastructure Deployment and Testing: 1-2 months

- Market Launch and Monitoring: Ongoing

Success Factors and Challenges

Success hinges on deep regulatory understanding, effective localization, and strong relationships with local authorities. Market challenges include strict advertising controls, vigorous competition from underground operators, and evolving compliance requirements driving operational complexity.

- Regulatory compliance and proactive engagement

- Strong technology and user experience adaptation

- Effective local partnerships and agent selection

- Investment in responsible gambling and player protection

- Agile response to regulatory changes and enforcement actions

Exit Strategy Planning

The Korean iGaming market offers moderate liquidity for ownership transfers, with regulatory approval mandatory for license changes. License transferability is restricted, emphasizing the importance of stable long-term planning. Valuation multiples follow regional digital entertainment industry norms, adjusted for compliance risk premiums.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Korea?

Online gambling in Korea is largely illegal for residents except for government-run lottery and sports betting platforms. Private or foreign online casinos targeting Korean players are prohibited and actively blocked by authorities. Exceptions exist for foreign tourists and specially licensed enterprises. Enforcement includes website blocking, fines, and imprisonment for illegal operators and users.

2. What types of gambling licenses are available and what do they cover?

Licenses primarily cover land-based casinos for foreigners, the state lottery, and the Sports Toto monopoly. No formal online gambling licenses are currently issued to private operators, but legislation mandates foreign platforms appoint a Domestic Agent for Korean market compliance. The existing framework segments licenses by activity type and operational scope.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing costs vary by type but typically range from USD 250,000 to 500,000, including application fees and compliance investments. The approval timeline usually spans 6 to 12 months, depending on completeness and regulatory scrutiny. Ongoing costs include annual renewals and audit expenses.

4. Can foreign companies obtain a gambling license?

Foreign companies currently cannot obtain direct online gambling licenses but can enter the market via partnerships and mandatory Domestic Agents who serve as local regulatory liaisons. Land gaming license opportunities exist mainly in casinos for foreigners under strict government supervision with possible foreign ownership subject to approval.

5. What are the tax obligations for iGaming operators?

Operators face progressive tax rates on gross gaming revenue, varying by activity: casinos pay 10-20%, sports betting 22%, and lotteries approximately 35% on sales. Corporate income tax applies at standard rates up to 25%. Licensed operators must also remit license fees and comply with withholding tax obligations for employees and contractors.

| Activity | Tax Type | Rate |

|---|---|---|

| Casinos | GGR Tax | 10-20% |

| Sports Betting | GGR Tax | 22% |

| Lotteries | Sales Tax | ~35% |

| Corporate Income | Income Tax | Up to 25% |

6. Are gambling winnings taxed for players?

Yes, individual gambling winnings exceeding a threshold of KRW 2 million are taxed progressively at rates from 22% to 40%. Operators assist in withholding and reporting these winnings to tax authorities. Failure to report winnings may result in penalties on players.

7. What are the typical operational costs for running an online casino/sportsbook?

Key operational costs include licensing-related fees, IT infrastructure, payment processing, marketing, staff salaries, compliance, and legal advisory services. Marketing and customer acquisition costs are particularly high due to restricted advertising channels. Technology maintenance and security are ongoing significant investments.

- Compliance and licensing fees

- Technology platform operation

- Payment gateway and transaction fees

- Marketing and promotion costs

- Human resources and training

8. What is the expected ROI timeline for entering this market?

Return on investment typically spans 2-4 years, depending on market penetration, regulatory compliance, and operational efficiency. Initial high setup costs balanced against growing user engagement and ARPU determine break-even points, with regulatory shifts potentially causing timeline fluctuations.

9. What are the local presence requirements for operators?

Local presence mandates include appointing a Domestic Agent for online operators, physical offices for land-based operations, and legal representation within Korea. These requirements ensure regulatory access and compliance monitoring, reinforcing government control over gambling activities.

10. What payment methods are available and recommended?

Recommended payment solutions prioritize local preferences: credit/debit cards, online banking, and mobile wallets like KakaoPay are dominant. Prepaid and gift cards offer alternatives for discreet transactions. Cryptocurrency use remains niche but emerging.

- Credit/Debit Cards (Visa, Mastercard, BC Card)

- Online Banking Transfers

- Mobile Wallets (KakaoPay, Naver Pay)

- Prepaid Cards

- Cryptocurrency (limited adoption)

11. What are the advertising and marketing restrictions?

Advertising gambling services is heavily regulated to prevent targeting minors and problem gamblers. Restrictions limit broadcasting times, content style, and platform channels. Promotional messaging must include responsible gambling notices. Sponsorships in sports and entertainment are closely monitored.

12. What responsible gambling measures are mandatory?

Mandatory measures include robust age verification, self-exclusion programs, player deposit limits, transparent odds disclosures, and staff training on problem gambling identification. Operators contribute financially to government social responsibility funds supporting addiction treatment.

- Age verification and KYC

- Self-exclusion and cooling-off mechanisms

- Deposit and wagering limits

- Transparent communication of risks

- Employee responsible gambling training

13. How large is the iGaming market and what is the growth potential?

The iGaming market in South Korea is valued at approximately USD 10 billion in 2025, dominated by online activity despite regulatory constraints. Forecast growth is steady with 2.6% CAGR through 2035, supported by rising digital adoption and evolving consumer comfort with online gaming experiences.

14. Who are the main competitors and what is their market share?

The market is dominated by state-run operators including Korea Lottery and Sports Toto. Kangwon Land operates land-based casino services for locals. Numerous illegal offshore operators compete for Korean players via VPNs, complicating the competitive landscape.

15. What are the player preferences and typical spending patterns?

Players show preference for state lotteries, sports betting, and illegal online casinos. Spending concentrates in lower to mid-range betting levels with mobile platforms preferred for convenience. Engagement peaks during weekends and around major sporting events, with retention fostered by loyalty rewards and localized content.

16. What are the key success factors and main challenges for new entrants?

Success depends on navigating regulatory barriers, localizing technology and marketing approaches, and investing in compliance systems. Challenges include limited license availability, enforcement against illegal operators, strict advertising regulations, and establishing trust within a culturally cautious market.

- Comprehensive regulatory compliance

- Local partnerships and agent management

- Innovative, mobile-friendly platform design

- Robust responsible gambling commitment

- Effective market education and brand positioning

Sources and References

- National Gambling Control Commission – Official Website

- Ministry of Culture, Sports and Tourism – Korea Gaming Laws 2025

- South Korea Statistical Office – Demographic Data 2025

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Data 2025

- Central Bank of Korea – Financial Statistics 2025

- Korea Internet & Security Agency – Digital Infrastructure Data

- Korea Telecom Regulatory Authority – Market Reports 2025

- SK Telecom Annual Report 2025

- KT Corporation Corporate Overview 2025

- LG Uplus Corporate Profile

- Korea Financial Supervisory Service – Banking Sector Report 2025

- E-Commerce Korea – Market Analysis 2025

- Ministry of Strategy and Finance – Taxation Guidelines 2025

- Korea Gaming Industry Association – Market Research 2024

- Digital 2025: South Korea Report – DataReportal

- South Korea Demographic Review – Worldometers 2025

- CNN Business – Korean Market Reports 2025

- Financial Times – Asia Gaming Markets Analysis 2025

- IGamingToday – South Korea Market Research 2025

- Sports Toto Annual Report 2024

- Kangwon Land Casino Financial Report 2024

- Ministry of Health and Welfare – Problem Gambling Statistics 2025

- IGamingExpert – Regulatory Updates South Korea 2025

- EY Korea – Tax Alerts and Reforms 2025

- Chambers Global Practice Guides – South Korea Gaming Law 2024

- Legal Pilot – South Korea Gambling Law Overview 2025

- InterAD – Social Media and Payment Trends Korea 2025

- DSGPay – Payment Methods in Korea 2025

- World Population Review – South Korea 2025 Demographics

- Wikipedia – Economy and Demographics of South Korea 2025

- Korea Herald – Digital Literacy and Market Developments 2025

- Global Gambling News – South Korea Regulatory Environment 2025

- SiGMA News – South Korea Gambling Enforcement 2025

- Trading Economics – South Korea Economic Data 2025

- FocusGN – Asian Market iGaming Regulation 2025

🎯 Gambling Databases Country Rating: South Korea

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 1.2/10 | ⛔️ Prohibitive |

| Player Access Score | 2.8/10 | 🔴 Severely Restricted |

| Overall Market Attractiveness | 2.0/10 | ⛔️ Avoid – One of Asia’s Most Restrictive Markets |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ONLINE CASINO GAMING IS COMPLETELY PROHIBITED – Criminal Code classifies unauthorized online gambling as criminal offense punishable by up to 7 years imprisonment and fines up to KRW 70 million (~USD 50,000)

- ACTIVE ISP BLOCKING CAMPAIGN – Government actively censors foreign operator websites through ISPs and blocks financial transactions to illegal operators. Strengthened internet censorship implemented in late 2025

- NO LICENSING AVAILABLE FOR FOREIGN OPERATORS – “Online gambling licensing for foreign operators is currently not offered within South Korea’s jurisdiction”

- MANDATORY DOMESTIC AGENT REQUIREMENT – Foreign operators must appoint Korea Game Domestic Agent under GIPA 2025, creating compliance liability without legal operating rights

- ASSET FORFEITURE RISK – Repeat offenders and large-scale illegal operations face asset confiscation in addition to fines and imprisonment

- STATE MONOPOLY DOMINANCE – Market controlled by government entities (Korea Lottery, Sports Toto, Kangwon Land), creating impossible competitive environment

- PAYMENT BLOCKING ACTIVE – Financial institutions actively block transactions linked to illegal gambling operators

- KOREAN NATIONALS SEVERELY RESTRICTED – Only ONE casino (Kangwon Land) permits Korean citizens to gamble; all other venues foreigners-only

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | -0.5/3.0 | CATASTROPHIC: State lottery legal for locals (+0.5). Sports betting MONOPOLY only (+0.5). Online casino COMPLETELY PROHIBITED (-1.5). Active ISP blocking and censorship (-0.5). Payment blocking by financial institutions (-0.5). Recent enforcement strengthening in 2025 (-0.5). Criminal penalties up to 7 years imprisonment (-0.5). Final: -0.5/3.0 |

| Licensing Process | 25% | 0.0/2.5 | NO LICENSING AVAILABLE: Foreign online operators explicitly cannot obtain licenses (0 points). Domestic Agent requirement under GIPA creates compliance burden without operating rights (0 points). Land-based casino licensing extremely limited – only Kangwon Land for Koreans, foreigner-only resorts for others (0 points). Application process 6-12 months but irrelevant for online (0 points). Multimillion USD investment required with no path to online casino license (0 points). Final: 0.0/2.5 |

| Taxation & Costs | 20% | 0.25/2.0 | PUNITIVE STRUCTURE: Casino GGR tax 10-20% (+1.5 baseline). Sports betting MONOPOLY 22% GGR (0 points, government-only). Corporate income tax 20% (-0.5). Total effective rate 30-40% for licensed activities (-0.5). Licensing costs USD 250k-500k for land-based (-0.25). Legal/consulting USD 100k-150k (-0.25). Technology setup USD 300k-600k in restricted environment (-0.25). Annual staff/agent fees USD 200k+ (-0.25). High customer acquisition costs in blocked environment (-0.5). Final: 0.25/2.0 |

| Operational Requirements | 15% | 0.25/1.5 | EXCESSIVE BARRIERS: Mandatory Domestic Agent appointment for foreign operators (0 points). Physical presence required for land-based but online prohibited (0 points). Foreign ownership subject to regulatory approval with partnership requirements often imposed (-0.25). Strict domain registration rules preventing Korean infrastructure use (-0.25). Stringent KYC/AML with ongoing monitoring (-0.25). Age verification mandatory (19+) (-0.25). Self-exclusion programs required (-0.25). Monthly financial reporting to MCST (-0.25). Final: 0.25/1.5 |

| Market Environment | 10% | 0.2/1.0 | HOSTILE REGULATORY CLIMATE: Good general business environment (top 10 globally) but irrelevant for gambling (+0.5). STRICT advertising bans on promoting to minors (-0.25). Severe limitations on advertising channels and time slots (-0.25). Ban on false/misleading promotions with content controls (-0.25). 2024-2025 regulatory crackdowns (Tourism Promotion Act amendment, GIPA enforcement, strengthened censorship) (-0.5). Active enforcement by National Gambling Control Commission and Police (-0.25). Underground market estimated USD 9 billion shows demand but creates illegal competition (-0.25). Final: 0.2/1.0 |

OPERATOR EASE TOTAL: 1.2/10 – PROHIBITIVE

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 1.5/4.0 | SEVERELY LIMITED: State lottery legal (+1.0). Sports Toto sports betting monopoly legal (+0.5). Kangwon Land casino legal for Koreans (single venue only) (+0.5). Online casino COMPLETELY ILLEGAL for Korean nationals (-1.5). Foreign casino resorts accessible but foreigners-only, excluding 51.7M Korean citizens (-0.5). Underground market exists but players face criminal liability (-0.5). Final: 1.5/4.0 |

| Practical Accessibility | 30% | 1.0/3.0 | HEAVILY BLOCKED: Credit/debit cards available for legal products (+1.0). Online banking transfers work for state lottery (+0.5). Mobile wallets (KakaoPay, Naver Pay) growing but restricted to legal gambling (+0.5). Financial institutions actively block transactions to illegal operators (-0.5). Active ISP blocking of foreign gambling websites (-0.5). VPN required for offshore access (-0.5). Government strengthened internet censorship in late 2025 (-0.5). Payment processing to offshore sites effectively impossible (-0.5). Final: 1.0/3.0 |

| Player Penalties | 20% | 0.5/2.0 | CRIMINAL LIABILITY EXISTS: Players using illegal gambling services face potential fines and criminal charges (0 points). Winnings from legal gambling taxed progressively 22-40% above KRW 2M threshold (-0.5). Enforcement focuses on operators but players not immune (-0.5). Criminal Code classifies unauthorized gambling as offense (-0.5). Final: 0.5/2.0 |

| Market Availability | 10% | 0.3/1.0 | MONOPOLY-CONTROLLED: State lottery (monopoly) (+0.2). Sports Toto (monopoly) (+0.2). Kangwon Land (single casino for Koreans) (+0.2). Several foreigner-only casinos irrelevant to 51.7M Korean nationals (0 points). Offshore operators blocked and illegal (-0.3). No licensed online casino operators (0 points). Final: 0.3/1.0 |

PLAYER ACCESS TOTAL: 2.8/10 – SEVERELY RESTRICTED

🔍 Key Highlights

Strengths (Minimal)

- Advanced Digital Infrastructure: 97% internet penetration, 5G covering 90% of population, 132% mobile penetration – but this infrastructure is ACTIVELY USED TO BLOCK GAMBLING

- High Spending Power: USD 36,000 per capita income, 51.7M population – but access severely restricted by law

- Tech-Savvy Population: 64% active online gamers (33M people), 99% literacy, strong digital skills – demand exists but channeled to illegal offshore sites

- Estimated USD 9B Online Gambling Market: Shows massive demand – but 100% of this is ILLEGAL underground/offshore activity

- General Business Environment: Top 10 globally for ease of business – COMPLETELY IRRELEVANT for gambling sector

⛔️ CRITICAL RISKS AND CHALLENGES

- [Online Casino Complete Prohibition:] Criminal Code explicitly prohibits online casino gaming. Up to 7 years imprisonment + KRW 70M fines. Eliminates 70%+ of typical iGaming revenue. This is a DEAL-BREAKER for casino operators.

- [No Licensing Path for Foreign Operators:] Document explicitly states “online gambling licensing for foreign operators is currently not offered within South Korea’s jurisdiction.” GIPA Domestic Agent requirement creates compliance liability WITHOUT granting operating rights.

- [Active Government Blocking Campaign:] Strengthened internet censorship in late 2025. ISPs actively block foreign gambling sites. Financial institutions block transactions to illegal operators. This makes offshore operation functionally impossible.

- [State Monopoly Lock:] Lottery, sports betting, and Korean-accessible casino ALL government-controlled monopolies. Private operators have ZERO access to Korean nationals market. Competition impossible.

- [Severe Criminal Penalties:] 7 years imprisonment for operators. KRW 70M (~USD 50k) fines. Asset forfeiture for repeat/large-scale operations. Enhanced sentencing for repeated offenders. Personal liability for directors.

- [2024-2025 Regulatory Crackdowns:] Tourism Promotion Act amended to close pseudo-casino loopholes (early 2024). GIPA enforced requiring Domestic Agents (mid 2025). Strengthened internet censorship (late 2025). Trend is INCREASING restriction, not liberalization.

- [Advertising Severe Restrictions:] Bans on promoting to minors. Limited channels and time slots. Content controls. Sponsorship regulations. Mandatory responsible gambling messages. Makes customer acquisition extremely expensive and difficult.

- [Payment Method Blocking:] Financial institutions actively monitor and block gambling transactions. Credit cards unavailable for illegal gambling. Online banking blocked. Mobile wallets restricted to legal products only.

- [Korean Nationals Excluded from Private Casinos:] Foreign casino resorts operate legally BUT only for foreign tourists. 51.7M Korean citizens prohibited from accessing these venues. Only Kangwon Land accessible – single casino in special economic zone.

- [Underground Market Competition:] USD 9B illegal market shows demand exists but funnels to offshore sites using VPNs and alternative payments. Legal operators cannot access this market. Illegal operators face constant blocking and enforcement.

Player-Specific Issues

- Online Casino Access ILLEGAL: Korean nationals cannot legally access online casino gaming domestically or offshore

- Single Physical Casino: Only Kangwon Land permits Koreans to play – special economic zone with strict oversight

- State Monopoly Only: Legal options limited to government lottery and Sports Toto – no private competition

- ISP Blocking: Government actively blocks access to offshore gambling sites via ISPs

- Payment Blocking: Banks and payment processors block transactions to illegal gambling operators

- VPN Necessary for Offshore: Players must use VPNs and face criminal liability to access offshore casinos

- High Taxation on Winnings: 22-40% progressive tax on winnings above KRW 2M (~USD 1,400)

- Criminal Penalties Possible: Players using illegal services face potential fines and criminal charges

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: USD 750,000 – 1,500,000 (licensing, legal, technology, staffing)

Monthly Operating Costs: USD 60,000 – 150,000+ (staff, compliance, technology, Domestic Agent fees)

Effective Tax Rate on Revenue: 30-40% (10-22% GGR tax + 20% corporate income tax) – BUT THIS ONLY APPLIES TO ILLEGAL ACTIVITIES YOU CANNOT LEGALLY CONDUCT

Customer Acquisition Cost: EXTREMELY HIGH – advertising severely restricted, brand building impossible, ISP blocking active. Estimated USD 500-1,000+ per customer in underground environment.

Time to Breakeven: NEVER – You cannot legally operate online casino or private sports betting in South Korea

Time to Positive ROI: NEVER – Legal paths do not exist for foreign online operators

Profitability Assessment: ECONOMICS ARE IMPOSSIBLE. There is NO legal path for foreign operators to obtain online gambling licenses in South Korea. The document explicitly states this. The only “legal” option is appointing a Domestic Agent under GIPA, which creates compliance liability WITHOUT granting operating rights. Any actual operations would be illegal, facing 7-year imprisonment, USD 50k+ fines, asset forfeiture, ISP blocking, and payment blocking. The USD 9B online market cited is 100% illegal underground activity. DO NOT ENTER THIS MARKET.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | CRITICAL | Criminal prosecution (7 years imprisonment), KRW 70M fines, asset forfeiture, ISP blocking, payment blocking, no licensing path available, active enforcement by National Gambling Control Commission and Police, repeat offender enhanced sentencing |

| Licensed Sports Betting Operators | IMPOSSIBLE | Sports betting is GOVERNMENT MONOPOLY (Sports Toto). Private operators cannot obtain licenses. Market closed to foreign and domestic private operators. |

| Affiliates/Advertisers | HIGH | Promoting illegal gambling subject to prosecution, website blocking, severe advertising restrictions even for legal products, payment processor termination, association with illegal operators creates liability |

| Payment Processors | CRITICAL | Active blocking mandates by government, regulatory action against processors facilitating illegal gambling, fines, license revocation, mandatory transaction monitoring and reporting |

| Company Directors/Executives | CRITICAL | Personal criminal liability (7 years imprisonment), asset forfeiture, extradition risk from countries with treaties, travel restrictions, enhanced sentencing for repeat/large-scale operations |

| Domestic Agents (GIPA) | HIGH | Legal liability for foreign operator compliance, regulatory communications burden, association with potentially illegal activities, unclear legal protection if foreign operator violates laws |

🚨 Extradition and International Enforcement

Extradition Treaties: South Korea maintains extradition treaties with United States, China, Japan, Germany, United Kingdom, Australia, Singapore, France, Canada, India, and 80+ other nations. Operating illegal gambling targeting Korean nationals creates prosecution risk in these jurisdictions.

Enforcement History: Active enforcement by National Gambling Control Commission alongside police authorities. Recent 2024-2025 crackdowns include Tourism Promotion Act amendments, GIPA enforcement, and strengthened internet censorship. Government demonstrates consistent willingness to pursue illegal operators.

Safe Jurisdictions: Limited options – Russia and some CIS countries lack extradition agreements, but this offers minimal protection given global cooperation on financial crimes and illegal gambling.

Travel Risk: HIGH – Directors and executives of illegal gambling operations targeting Korean nationals face arrest risk when traveling through countries with extradition treaties (USA, UK, EU, Japan, Australia, Canada, Singapore, etc.). International enforcement cooperation makes travel to major business hubs dangerous.

📋 Final Verdict

South Korea receives an Operator Ease Score of 1.2/10 and a Player Access Score of 2.8/10, resulting in an overall market attractiveness rating of 2.0/10 – PROHIBITIVE/AVOID.

BRUTALLY HONEST ASSESSMENT:

This market is COMPLETELY CLOSED to foreign iGaming operators. Online casino gaming is explicitly prohibited under the Criminal Code with 7-year imprisonment and USD 50,000+ fines. The document states clearly that “online gambling licensing for foreign operators is currently not offered within South Korea’s jurisdiction.” Sports betting is a government monopoly (Sports Toto) – private operators cannot enter. The only casino accessible to 51.7M Korean nationals is Kangwon Land, a single government-controlled venue.

The 2025 GIPA requirement for Domestic Agents is a TRAP – it creates compliance liability for foreign operators WITHOUT granting any legal operating rights. Active ISP blocking, payment blocking by financial institutions, strengthened 2025 censorship, and aggressive enforcement make offshore operation functionally impossible. The cited USD 9B online gambling market is 100% illegal underground activity facing constant blocking and prosecution.

There is NO legal path, NO viable business model, and EXTREME criminal liability. The regulatory trend is INCREASING restriction (2024-2025 crackdowns), not liberalization. Even if you were willing to operate illegally, ISP blocking and payment blocking make customer acquisition and monetization nearly impossible while facing 7 years imprisonment.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- LITERALLY NO ONE. There is no legal path for foreign private operators to enter this market for online gambling or private sports betting.

- Exception: If you want to operate a foreigner-only physical casino resort and have USD 10M+ capital for multiyear licensing process, you MAY consider land-based casino licensing – but you will be prohibited from serving 51.7M Korean nationals, limiting market to tourists only.

❌ Definitely Avoid If You Are:

- ANY online casino operator (online casino completely illegal, 7 years imprisonment)

- ANY online sports betting operator (sports betting is government monopoly, private operators prohibited)

- Offshore operator without Korean license (ISP blocking active, payment blocking active, criminal prosecution risk)

- Startup or mid-sized operator (no legal path exists regardless of capital)

- Operator seeking ROI within 10 years (illegal operation faces blocking; legal paths don’t exist)

- Affiliate or advertiser for offshore casinos (prosecution risk, severe advertising restrictions)

- Cryptocurrency-focused operator (crypto marginal, payment blocking active)

- Operator targeting Korean nationals specifically (state monopoly for lottery/sports betting, single casino access, online prohibited)

- Anyone unwilling to face 7 years imprisonment (criminal penalties for illegal operations)

- Foreign operator hoping GIPA Domestic Agent provides legal cover (it doesn’t – creates liability without operating rights)

⚠️ BOTTOM LINE: South Korea is one of Asia’s most restrictive gambling markets with NO legal entry path for foreign iGaming operators. Online casino prohibited. Sports betting monopolized. Active blocking and criminal enforcement. AVOID COMPLETELY unless you enjoy 7-year prison sentences.

Looking at the cost breakdown for operating a sportsbook in New Jersey, we’ve seen yields of around 7.2% on NFL games, with materials and labor costs totaling $1.2 million annually. Our supplier, Sportech, has provided us with a 5-year contract at a rate of $0.05 per transaction. We’re projecting revenue of $2.5 million in the first year, with a payback period of 3 years. Scaling challenges have included optimizing our workflow to handle high volumes of bets during peak seasons.

Regarding the cost breakdown for operating a sportsbook in New Jersey, it’s interesting to note that our research has shown similar yields, around 7.5%, for NFL games. However, we’ve also found that optimizing workflow and utilizing advanced technology, such as AI-powered betting platforms, can significantly reduce labor costs and improve efficiency. For example, a study by the University of Nevada found that AI-powered platforms can reduce labor costs by up to 30%. Additionally, it’s worth considering the impact of different regulatory frameworks on sportsbook operations, such as the differences between New Jersey and the UK.

Thanks for the insight! We’ve indeed considered AI-powered platforms, and our initial estimates suggest a potential reduction in labor costs of around 25%. However, we’re still weighing the pros and cons of implementing such a system. What are your thoughts on the potential risks and challenges associated with AI-powered sportsbook platforms?

That’s a great question, and one that we’ve explored in our research. While AI-powered platforms can offer significant benefits, there are also potential risks to consider, such as the potential for bias in the algorithms and the need for ongoing maintenance and updates. We’ve found that a hybrid approach, combining human expertise with AI-powered tools, can be an effective way to mitigate these risks. For example, our study on the use of AI in sportsbook operations found that a hybrid approach can improve accuracy by up to 15%.

I’ve tracked 25 trials of in-play betting on soccer matches, seeing a standard deviation of 1.8 in terms of payout ratios. To minimize variance, I’ve developed an A/B testing protocol using two different algorithms. The question remains whether these findings are reproducible across different sports and jurisdictions, such as the UK or Australia. Perhaps we could discuss the use of statistical notation, like σ, to better understand these trends?