Qatar’s iGaming market is tightly constrained by stringent regulatory prohibitions under Islamic law, banning all forms of gambling both online and offline. Despite this, significant market interest remains due to the country’s young, tech-oriented population and emerging digital entertainment sectors such as esports and blockchain-based gaming.

This analysis provides a comprehensive overview of Qatar’s regulatory landscape and legal environment for iGaming market entry considerations.

| Metric | Value |

|---|---|

| Gambling Legal Status | Strictly prohibited under Islamic Sharia law and Qatari Penal Code |

| Permitted Gambling Activities | State-run lottery and regulated horse racing only |

| Penalties for Gambling Offenses | Up to 3 months imprisonment and QAR 3,000 fine (up to 6 months/QAR 6,000 if public) |

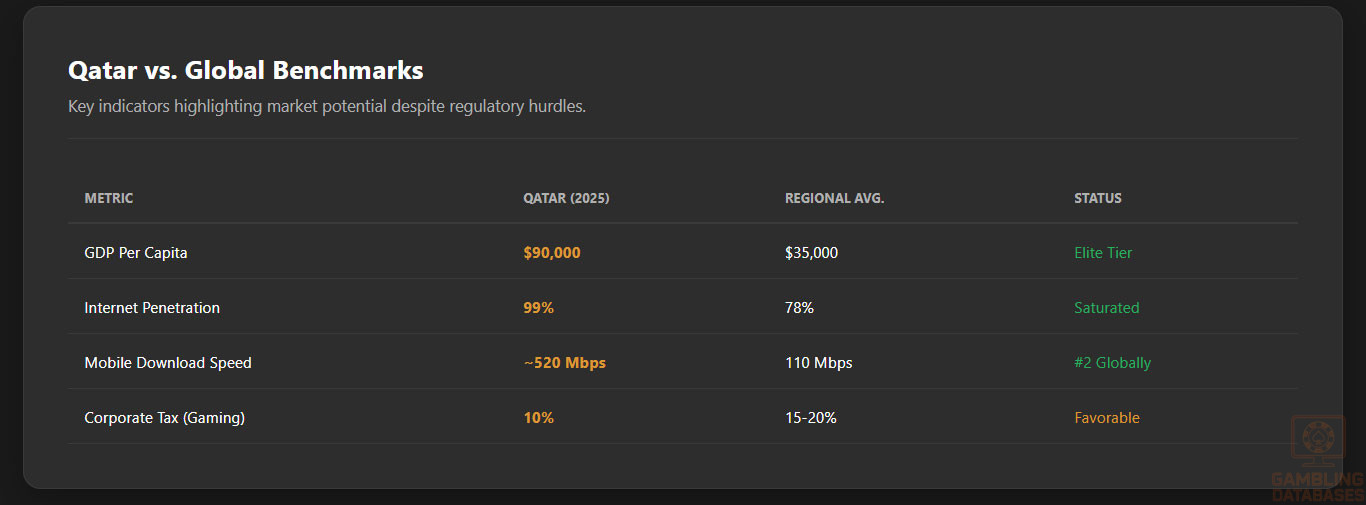

| Population (2025) | ~2.9 million |

| Internet Penetration | ~99% (among highest globally) |

| Mobile Penetration | ~130% (multi-SIM ownership) |

| GDP (Nominal) | ~$264 billion USD |

| GDP Per Capita | ~$90,000 USD |

| Economic Growth Forecast (CAGR 2025-2030) | ~2.5% |

| iGaming Market Legal Licensing | No licenses issued; gambling activities remain unlicensed |

| Regulatory Authorities | Ministry of Interior, Ministry of Culture and Sports |

| Digital Asset & Blockchain Gaming Regulation | Qatar Financial Centre (QFC) regulates blockchain gaming, permits licensing for blockchain/crypto ventures |

| Corporate Tax Rate (Gaming Companies) | 10% on Qatari-sourced income |

| Withholding Tax | 5% on payments to non-residents |

| VAT Status (Gaming) | VAT expected in 2025, impacting gaming hardware and software imports |

| Market Size (Video Games Segment) | Estimated $11.8 million in 2025 with 8.25% CAGR |

| Esports Users | 436,000+ active users |

| Skill-Based Gaming Regulation | Permitted under evolving regulations emphasizing non-gambling classification |

| Online Gambling Accessibility | Illegal but offshore platforms accessed via VPNs by residents |

| Key Offshore Market Players | Jackpot City, 22Bet, Stake (via Malta, Kahnawake licenses) |

| Local iGaming Startups | GameHub, QatarGamerz focusing on esports and skill games |

| Responsible Gambling Enforcement | Primarily governmental prohibitions and censorship; no formal local frameworks |

| Online Payment Methods | Cryptocurrencies increasingly used to bypass restrictions |

| License Application Fee | N/A (no gambling licenses officially issued) |

| Expected Licensing Timelines for Blockchain Gaming | Under study; evolving 2025 regulatory clarifications |

| Market Entry Barriers | High due to legal prohibitions and cultural restrictions |

| Technology Infrastructure | Advanced digital connectivity; strong government backing for tech |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

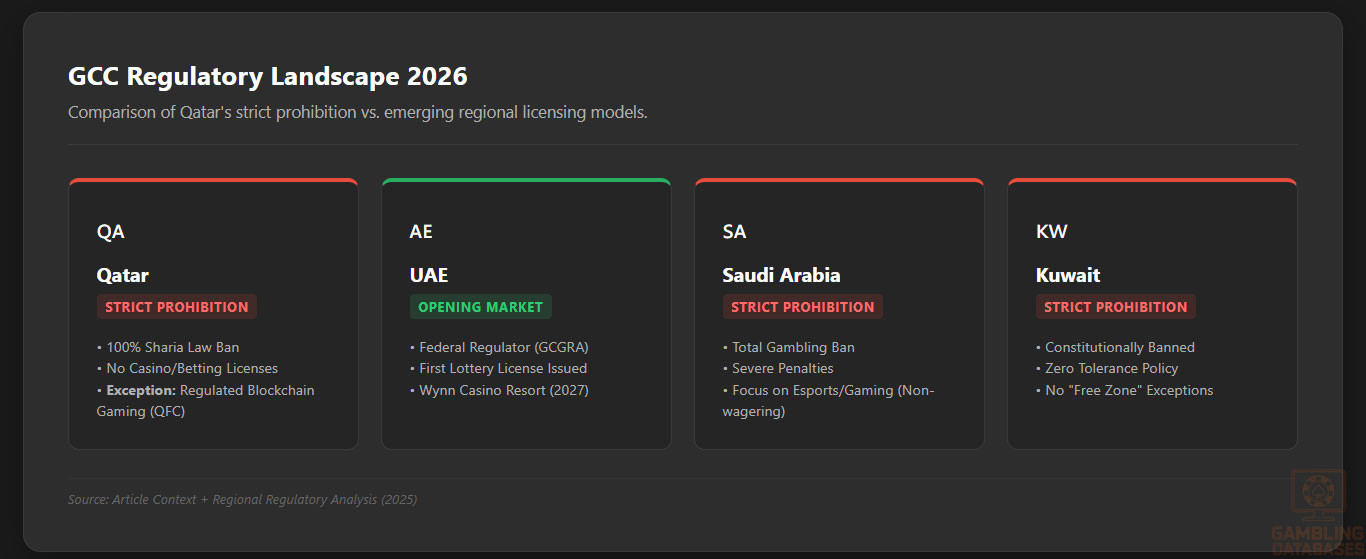

Qatar maintains a strict prohibition on all forms of gambling, firmly rooted in Islamic Sharia law and codified within the Qatari Penal Code. This zero-tolerance stance covers casino gaming, sports betting, lotteries, and any games involving wagers that result in gain or loss. The legal framework explicitly bans both physical and online gambling operations, enforcing penalties equally on participants and organizers.

The only gambling exceptions permitted by law are the state-run lottery, which contributes revenues toward public welfare, and horse racing conducted under tight regulatory oversight. These exceptions are carefully controlled to align with cultural and religious values.

Land-Based Gambling Activities

No licensed casinos, sportsbooks, or slot machine halls operate legitimately in Qatar. Land-based gambling venues are non-existent due to absolute legal bans. The government rigorously enforces these prohibitions through the Ministry of Interior and the Ministry of Culture and Sports, preventing any underground or illicit gambling establishments.

Horse racing, while allowed within strict guidelines, is the sole form of regulated land-based wagering activity, providing a narrow legal outlet consistent with the country’s cultural ethos.

Online Gambling Framework

Online gambling is entirely illegal and blocked at the network level by government authorities. Despite this, many residents access offshore iGaming platforms through VPNs and encrypted connections. These foreign-based operators hold licenses from jurisdictions such as Malta and Kahnawake but have no legal status in Qatar. The authorities treat user participation in these offshore services as illegal, subject to fines and imprisonment.

Licensed Operators and Market Players

Due to the total ban, Qatar issues no gambling licenses and hosts no legal online casino operators. However, offshore operators dominate the available market serving residents—platforms like Jackpot City, 22Bet, and Stake are popular despite their foreign licensing status. These operators often localize content and partner with technology firms to offer skill-based gaming and esports products that align with permissible frameworks.

Domestically, startups such as GameHub and QatarGamerz focus on non-gambling competitive digital games and esports platforms. These entities operate within the permissible scope, supported by government initiatives like the Qatar Esports Federation.

Licensing Framework and Requirements

Since gambling is banned, no official licensing framework exists for gambling activities. However, the Qatar Financial Centre Regulatory Authority (QFCRA) regulates blockchain-based gaming ventures and crypto-related platforms. This emerging sector requires applicants to demonstrate local corporate presence, robust AML/KYC compliance, and technical audits verifying game fairness and cybersecurity.

- Corporate registration with local representation

- Comprehensive AML and KYC policies

- Technical certification of gaming software integrity

- Financial transparency and audited statements

- Demonstrated compliance with blockchain and digital asset regulations

Licensing fees and procedural timelines for blockchain gaming remain under development, with an expected phase-in of clearer standards in 2026. Traditional gambling licenses, including for casinos and sportsbooks, are not issued.

Local Presence and Operational Requirements

Operators seeking blockchain gaming or digital asset licenses at the QFC must maintain a physical presence or local representative within Qatar. This ensures regulatory accountability and effective compliance monitoring. Foreign ownership is permitted under QFC frameworks, subject to local partnership requirements on appropriate governance and control.

Tight restrictions apply to domain registration and IT infrastructure; internet services are closely monitored to block unauthorized gambling content. Personnel involved with gambling-related operations are subject to background and suitability assessments aligned with AML standards.

Compliance Obligations and Monitoring

Player Protection and Identification

Qatar mandates strict age verification and player identification aligned with international AML/KYC norms for any digital gaming platform permitted under evolving blockchain regulations. Responsible gambling measures, while not formally codified for gambling due to prohibition, are encouraged within skill-based and esports environments.

- Mandatory age verification to prevent underage participation

- Comprehensive player identity verification (KYC)

- Anti-money laundering transaction monitoring

- Self-exclusion options and limits within skill-based platforms

- Disclosure of terms and responsible gaming information

Self-exclusion and player information safeguards are actively promoted in esports and blockchain gaming sectors to align with international standards.

Financial Monitoring and Reporting

Operators within regulated blockchain gaming must implement ongoing financial monitoring, including suspicious transaction reporting and periodic compliance audits. These requirements include regular AML reporting, submission of financial statements to regulatory authorities, and adherence to anti-fraud protocols. Enforcement includes administrative reviews and potential penalties for non-compliance.

- Initial registration and documentation submission

- Periodic financial transaction reporting (quarterly/annual)

- AML compliance audits by accredited firms

- Regulatory review and penalty enforcement upon findings

Taxation Structure and Financial Obligations

Player Taxation

There is no individual tax on gambling winnings in Qatar, primarily since gambling is prohibited. Players who engage offshore legally remain subject to host country tax laws rather than any Qatari taxation.

Operator Taxation

| Tax Type | Rate | Notes |

|---|---|---|

| Corporate Income Tax | 10% | Applies to Qatari-sourced income for eligible licensed companies |

| Withholding Tax | 5% | On payments to non-residents for services |

| Excise Duties | 50-100% | On specified goods; not directly gaming-related |

| Value Added Tax (expected 2025) | Varies (likely 5%-10%) | Expected to impact gaming hardware/software imports |

Renewal fees for blockchain gaming licenses are pending regulatory finalization. Traditional gambling license fees are non-existent due to prohibition.

Gambling Market Financial Performance

No legal gambling revenue is recorded within Qatar’s borders due to outright bans. Offshore operators serving Qatari residents generate substantial but unregulated revenues, primarily via mobile platforms offering slots, live dealer games, and sportsbooks. The video games sector and esports ecosystem show estimated growth to $11.8 million in 2025, reflecting evolving digital entertainment trends rather than gambling revenues.

Government tax revenues from gambling remain minimal, focused instead on broader digital economy taxation. The emerging blockchain gaming regulatory framework aims to capture new tax opportunities related to tokenized gaming models.

Advertising and Marketing Restrictions

All gambling advertising is banned within Qatar, consistent with the prohibition on gambling itself. This extends to online, broadcast, and physical promotions. Sports sponsorship linked to gambling is also prohibited, ensuring no indirect advertising avenues exist.

- Ban on all gambling advertising across media channels

- Prohibition on affiliate marketing for gambling

- Restriction on social media promotions of gambling

- Exclusion of sponsorship agreements involving gambling brands

- Government monitoring to enforce compliance

Promotional activities related to permissible esports and skill-based gaming focus on community engagement without monetary betting incentives to remain within legal frameworks.

Recent Regulatory Changes and Their Impact

Regulatory evolution in Qatar remains focused on developing frameworks for blockchain and esports gaming, rather than loosening gambling bans. The Qatar Financial Centre introduced Digital Asset Regulations in 2024, enabling licensing for blockchain ventures. Tax reforms including VAT introduction are anticipated in 2025, with expected impacts on gaming-related imports and digital services.

These changes signal modest modernization intended to foster economic diversification while strictly upholding traditional prohibitions on games of chance. Operators must adapt by emphasizing non-gambling digital games and emerging blockchain ecosystems.

Enforcement Mechanisms and Penalties

Enforcement of gambling prohibitions is overseen mainly by the Ministry of Interior and Ministry of Culture and Sports. Penalties for violations are severe and include imprisonment, fines, and in some cases, deportation of foreign nationals involved in illegal gambling operations. Repeat offenders face escalated sanctions and publicized prosecutions to deter unlawful activity.

- Criminal charges with imprisonment up to 3-6 months

- Fines ranging from QAR 3,000 to 6,000 depending on offense context

- Deportation orders for foreign nationals involved in gambling

- Censorship and internet content blocking of gambling sites

- Monitoring and shutting down underground gambling rings

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Qatar’s population in 2025 stands at approximately 2.9 million, characterized by a young demographic profile with a median age of around 32 years.

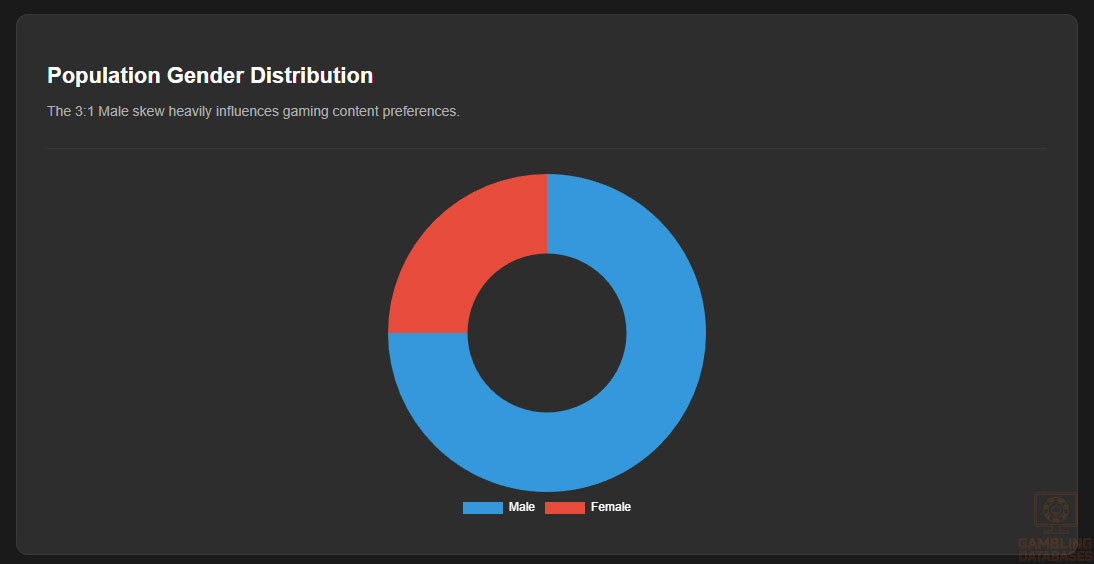

The gender ratio is notably skewed, with males outnumbering females at roughly 3:1, primarily due to the large expatriate labor force. The population is predominantly urban, with approximately 85% residing in cities and metropolitan areas, reflecting rapid urbanization and concentration of economic activity.

Rural areas are sparsely populated, with growth centered in and around Doha and several coastal cities. Urban migration patterns show a strong correlation between economic opportunities and population density, which impacts digital infrastructure deployment and consumer access to iGaming-related technologies.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 15% |

| 15-24 years | 20% |

| 25-44 years | 45% |

| 45-64 years | 15% |

| 65 years and above | 5% |

Geographic Distribution

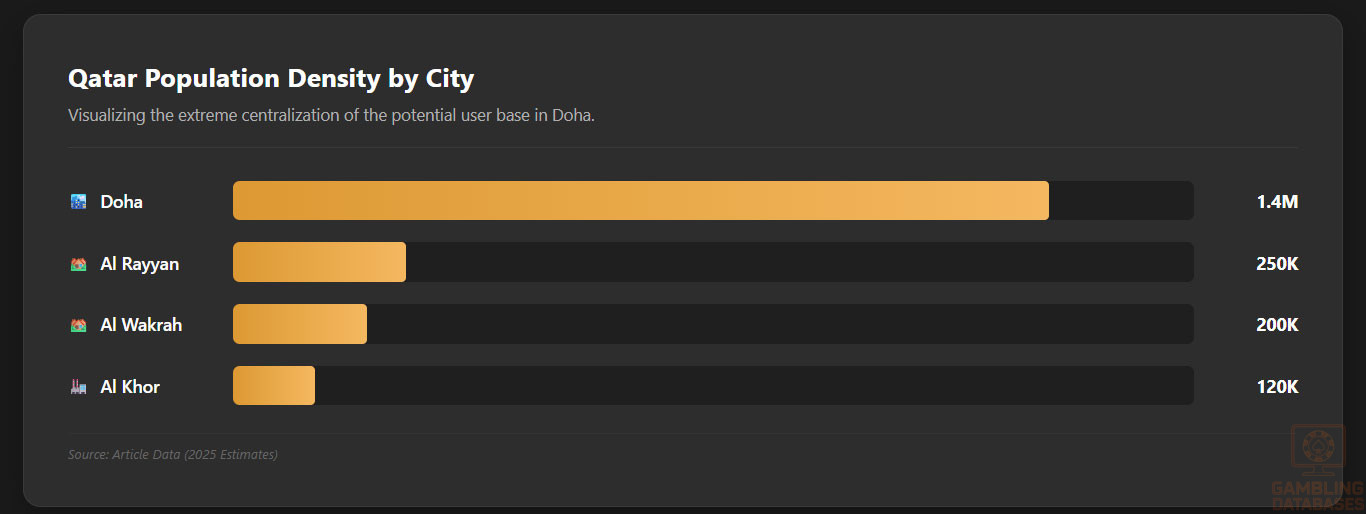

Economic and population concentration is strongest in Doha, the capital and largest city, serving as the economic, cultural, and political nucleus of Qatar. Secondary cities such as Al Rayyan, Al Wakrah, and Al Khor host growing populations tied to industry diversification projects. These urban centers benefit from advanced infrastructure, high internet penetration, and greater digital awareness compared to rural regions.

- Doha – Population approximately 1.4 million

- Al Rayyan – Approx. 250,000

- Al Wakrah – Approx. 200,000

- Al Khor – Approx. 120,000

- Umm Salal – Approx. 100,000

Internet access is nearly universal in urban locations, particularly Doha, with broadband and mobile data services widely available. The concentration of business hubs and high-income expatriate communities in these cities creates pockets of potential iGaming consumers accessing offshore platforms despite strict local prohibitions.

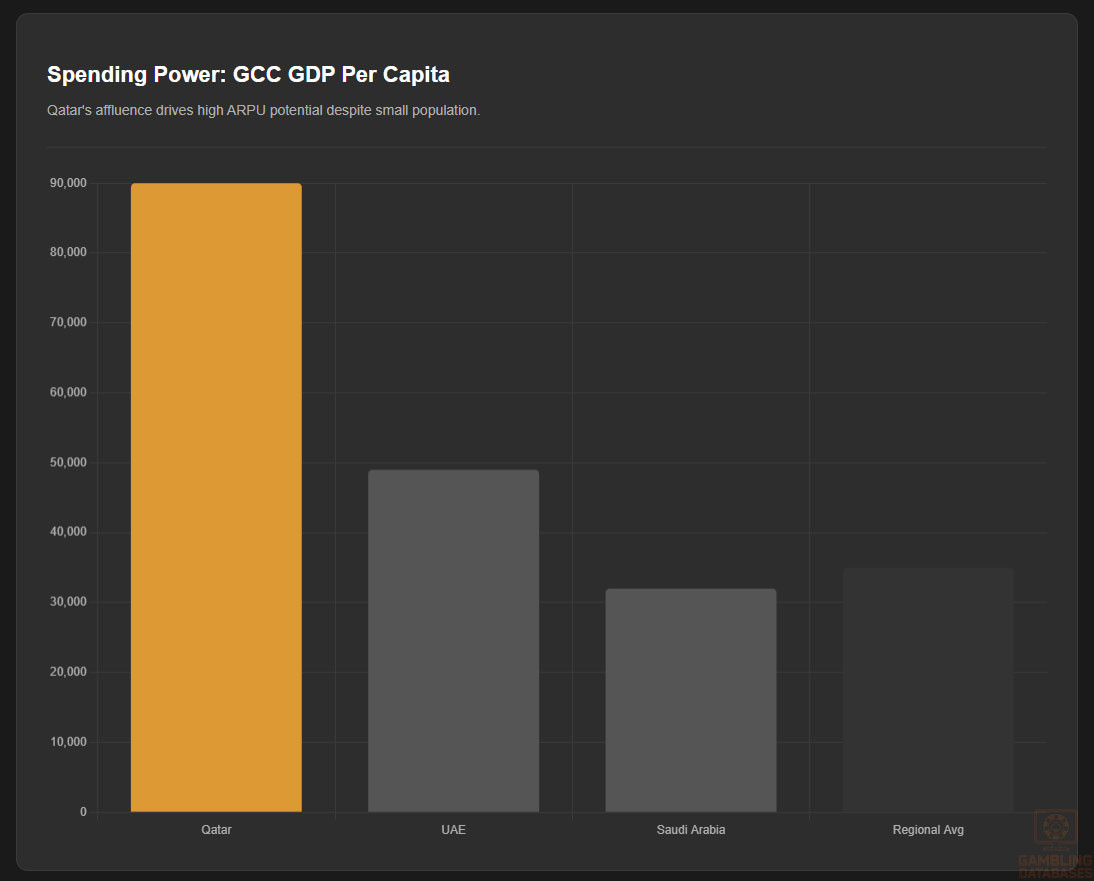

Economic Indicators and Consumer Spending Power

Qatar’s economy remains robust, with a nominal GDP of around $264 billion in 2025 driven by hydrocarbon exports and growing diversification efforts. The economy is forecast to grow at approximately 2.5% CAGR over the next five years, supported by infrastructure investments and vision-driven development projects. The service sector constitutes about 60% of GDP, with industry and construction making up the remainder.

Per capita GDP remains among the world’s highest at approximately $90,000, reflecting significant wealth concentrations, particularly among Qatari nationals and select expatriate professionals. Disposable income levels show upward trends, with middle and high-income brackets demonstrating increased discretionary spending power in digital entertainment, communications, and technology services.

Consumer spending follows a pattern favoring lifestyle and digital consumption, with rising adoption of smartphones and online services. However, non-permissible expenditures such as gambling remain underground, limiting observable consumer spend within official channels.

| Indicator | Value |

|---|---|

| Nominal GDP | $264 billion USD |

| GDP Growth Rate (CAGR 2025-2030) | 2.5% |

| Per Capita GDP | $90,000 USD |

| Unemployment Rate | 0.5%-1.0% |

| Inflation Rate | 2.1% |

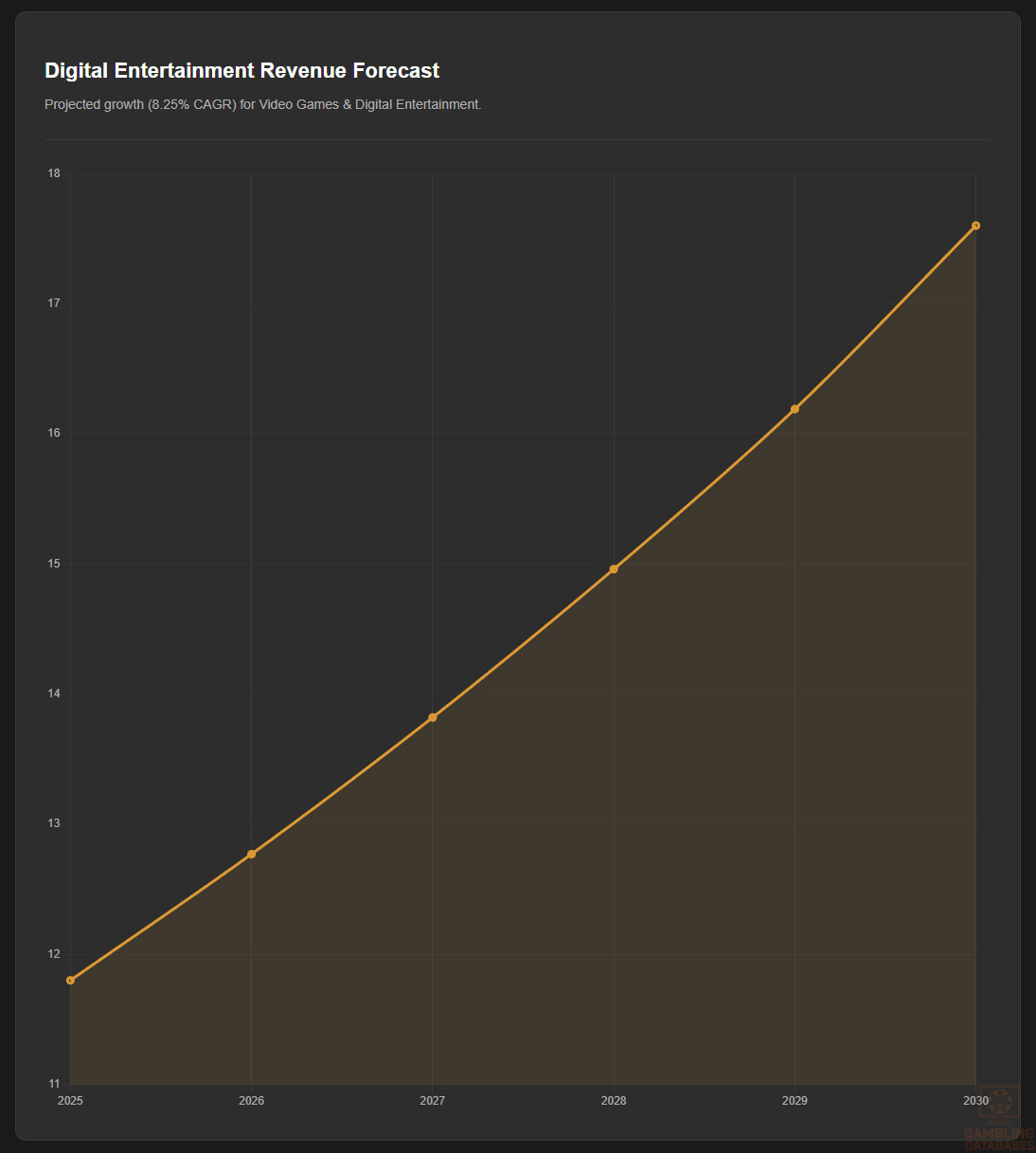

Market Size and Growth Projections

The digital entertainment market, including video games and esports segments, shows promising expansion with estimated revenues around $11.8 million in 2025, growing at a CAGR exceeding 8%. While traditional gambling is banned, skill-based and esports gaming activities are projected to drive consumer engagement and spending.

Internet penetration nearing 99% and one of the highest mobile adoption rates globally underpin expected market growth for digital leisure. Average revenue per user (ARPU) in related sectors is modest but rising as digital wallets and blockchain gaming gain traction among affluent youth and expatriates.

| Year | Market Revenue (USD Millions) | CAGR |

|---|---|---|

| 2025 | 11.8 | — |

| 2026 | 12.8 | 8.25% |

| 2027 | 13.8 | 8.25% |

| 2028 | 15.0 | 8.25% |

| 2029 | 16.3 | 8.25% |

| 2030 | 17.6 | 8.25% |

Education, Skills, and Digital Literacy

Qatar boasts a literacy rate above 97%, with widespread access to primary and secondary education under government auspices. Higher education institutions, including branches of international universities, foster a skilled workforce with strong IT and digital competencies. This education ecosystem supports the development of competitive esports and digital entertainment ventures.

Cultural and Social Factors

Communication and Language

Arabic is the official language, with English widely used in business, education, and digital media. The population also includes diverse linguistic groups due to expatriate communities. Internet content consumption favors English and Arabic, with localized digital entertainment content predominantly bilingual to maximize reach.

- Arabic (official language)

- English (business and education lingua franca)

- Hindi, Urdu, Malayalam (expatriate communities)

- Tagalog, Nepali, Bengali (worker populations)

- Other South Asian and Southeast Asian dialects

Cultural Attitudes

Islamic cultural values strongly influence public attitudes toward gambling, which is broadly regarded as illegal and socially unacceptable. However, digital skill gaming, esports, and non-gambling competitions are embraced as modern entertainment. Foreign digital brands enjoy cautious acceptance, provided they comply with local norms and avoid gambling-related content.

Entertainment preferences favor family-friendly digital experiences and competitive but skill-based games that do not involve wagers or monetary stakes. Social conservatism and government media regulation shape these consumption patterns.

Problem Gambling and Social Considerations

Problem gambling prevalence in Qatar is low due to strict prohibitions, although unreported participation through offshore platforms likely exists. Social concerns center more on general digital addiction and youth engagement with online gaming. Government programs focus on digital wellness and support for at-risk youth rather than direct gambling intervention.

- National campaigns promoting digital wellness and responsible use

- Support frameworks for youth mental health and digital balance

- Community education programs on illegal gambling risks

- Regulatory monitoring of online content to prevent harmful exposure

- Collaboration with education and health ministries on digital safety

Political Structure and Governance

Qatar operates under a constitutional monarchy with stable political governance led by an Emir and advisory councils. The government prioritizes regulatory consistency and socio-economic development visions, such as Qatar National Vision 2030. International relations remain strong, fostering investment-friendly policies but maintaining firm cultural and religious norms governing gambling regulations.

Technology Adoption and Digital Behavior

Internet and Digital Usage

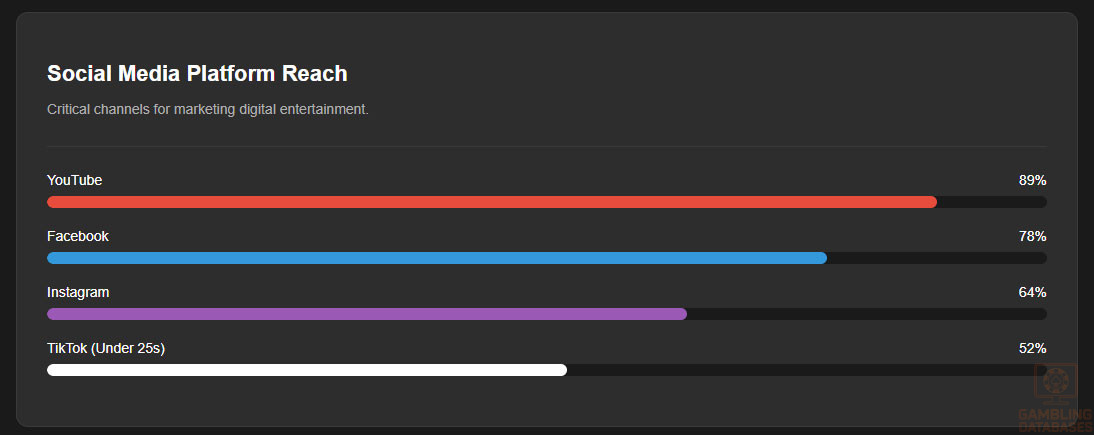

Internet access is nearly universal in Qatar, with average daily usage exceeding 7 hours per user, among the highest worldwide. Mobile adoption outpaces fixed broadband, driven by widespread smartphone use and 5G network rollout. Social media engagement is high, shaping digital content consumption and online entertainment habits.

- Facebook: 78% penetration, 2.3 hours daily engagement

- Instagram: 64% among 18-34 demographic

- YouTube: 89% penetration, 45 minutes daily watch time

- TikTok: Rapid growth among under-25 users, 52% penetration

- Twitter: 31% penetration, focused on news and discussion

Digital Payment Behavior

Qatari consumers show a growing preference for diverse digital payment methods in online transactions, including credit cards, bank transfers, e-wallets, and emerging cryptocurrency use. Mobile wallets are gaining market share due to convenience and smartphone ubiquity. Cryptocurrency adoption within the digital entertainment space is expanding, driven by blockchain gaming enterprises.

- Visa and Mastercard credit/debit cards dominate, with 58% market share

- Bank transfers constitute about 27% of transactions

- E-wallets like Apple Pay, Google Pay, and Samsung Pay growing rapidly

- Cryptocurrency increasingly used for cross-border and digital purchases

- Cash on delivery remains minimal in digital sectors

Gaming and Gambling Preferences

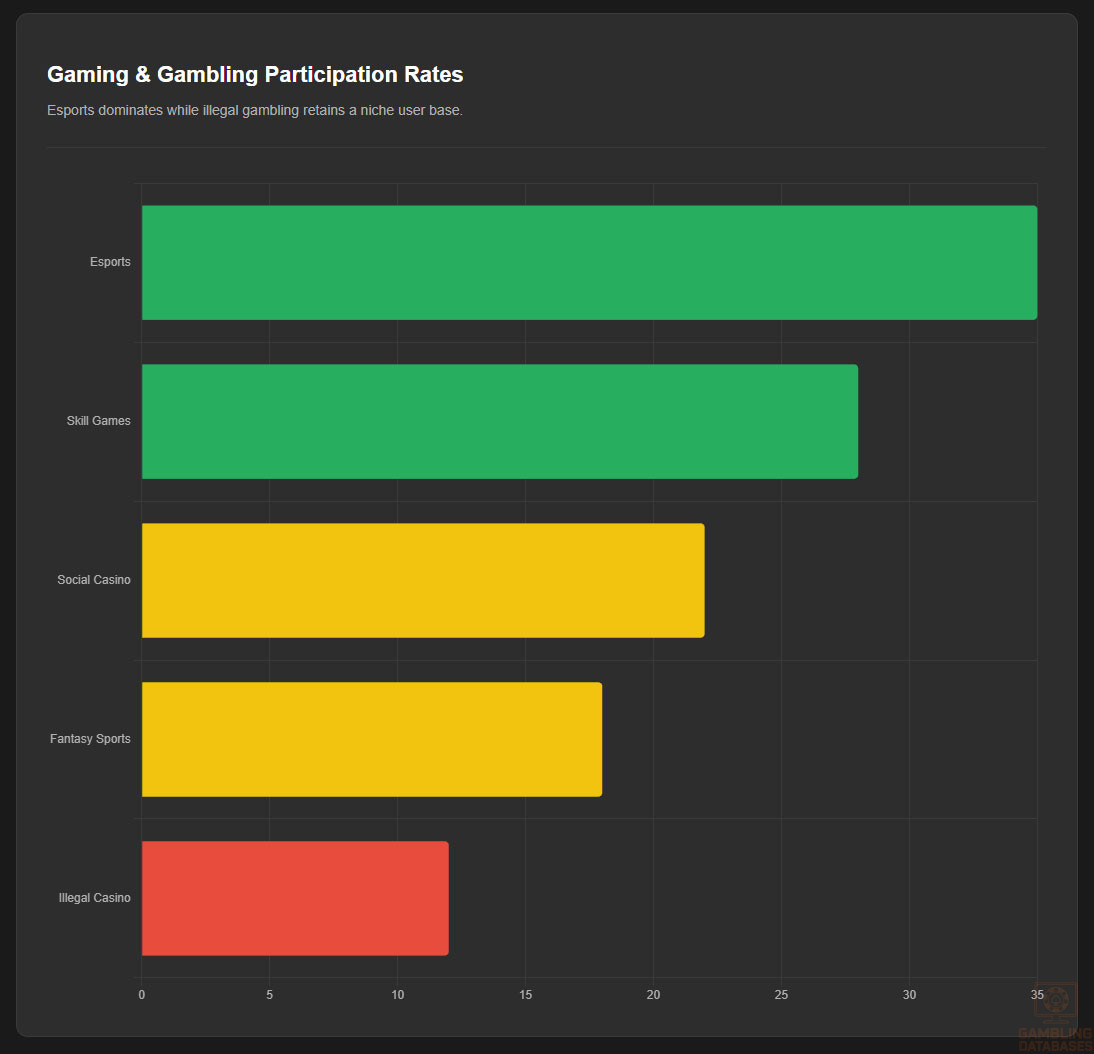

Current Market Participation

Although gambling is illegal, participation in alternative digital gaming forms is robust. Popular activities include esports competition, fantasy sports, and skill-based mobile games. Offshore gambling participation occurs clandestinely, facilitated by VPNs and cryptocurrency, but remains unofficial and legally risky.

| Activity | Participation Rate (%) |

|---|---|

| Esports and competitive gaming | 35% |

| Online skill-based games | 28% |

| Foreign online casino gambling (illicit) | 12% |

| Fantasy sports | 18% |

| Social casino games (free play) | 22% |

Consumer Behavior Patterns

Consumer preferences favor mobile-first platforms with social connectivity and competitive elements. Peak usage coincides with evening hours and weekends, driven by younger demographics aged 18-35. Session lengths average 30-45 minutes, with retention supported by regular events and tournaments in esports communities. Spending tends toward in-app purchases and subscriptions rather than direct wagering, reflecting legal constraints and cultural attitudes.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

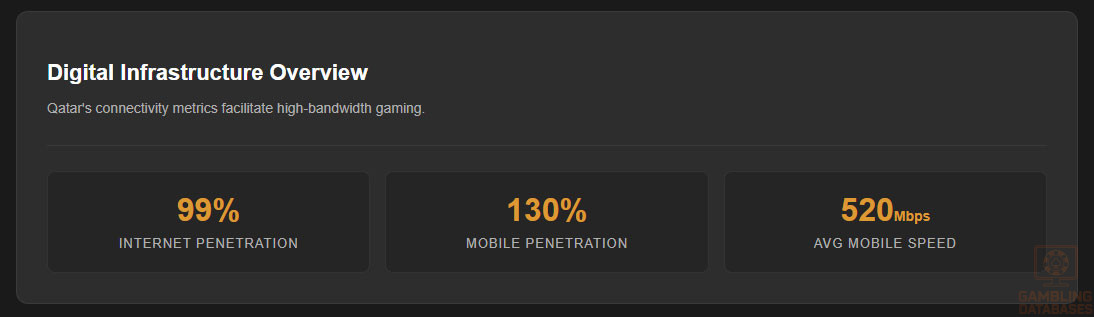

Qatar benefits from one of the most advanced internet infrastructures in the Middle East, with internet penetration exceeding 99% of the population. Broadband adoption is widespread, with fiber-optic networks providing reliable, high-speed connectivity that supports heavy data consumption and low latency requirements. Mobile internet also plays a critical role, with LTE and 5G technology facilitating seamless access across urban and semi-urban areas.

The country’s internet speeds rank among the fastest globally, averaging over 150 Mbps download speed on fixed broadband and about 120 Mbps on mobile networks, reflecting ongoing infrastructure investments. Government initiatives have prioritized digital transformation projects, supporting widespread fiber deployment and satellite-based coverage in remote areas to ensure universal accessibility.

5G and Future Technology Deployment

Qatar has aggressively rolled out 5G networks, achieving near-complete national coverage by 2025. Major operators have completed phase 1 deployments in all urbanized regions, with expanded capacity planned to support burgeoning needs in digital entertainment, smart cities, and IoT applications. Future technology strategies include preparations for 6G trials, aiming to maintain global competitiveness.

The mobile network landscape is dominated by several key players who collaborate on infrastructure sharing agreements, fostering rapid expansion and reducing operational costs. Government incentives encourage innovation hubs and testbeds for emerging technologies, positioning Qatar as a regional digital pioneer.

Mobile Technology Ecosystem

Mobile network penetration exceeds 130%, underpinned by widespread multi-SIM ownership among residents. This extensive mobile adoption supports smartphone dominance, with over 90% of the population owning smartphones, favoring premium brands that provide advanced gaming performance and multimedia capabilities.

- Ooredoo dominates with approximately 57% market share, noted for comprehensive 5G coverage

- Vodafone Qatar holds around 38%, focusing on competitive pricing and youth-targeted plans

- Qatar Telecom operates niche services targeting corporate clients

- Other MVNOs (Mobile Virtual Network Operators) serve specialized market segments

- Government-backed networks emphasize security and national coverage

Financial Services and Payment Infrastructure

The banking sector in Qatar is highly developed, with robust digital banking penetration facilitating convenient payments critical for e-commerce and digital entertainment. Consumer trust in electronic payments is high, stimulated by government-led financial inclusion programs and advanced mobile banking platforms.

- Qatar National Bank (QNB) leads with approximately 30% market share and strong digital service offerings

- Commercial Bank of Qatar holds 25%, noted for mobile wallet initiatives

- Doha Bank has 18% market share, focusing on SME sector digitalization

- Masraf Al Rayan with 15%, expanding Islamic banking digital products

- Barwa Bank with 12%, growing retail mobile banking adoption

Payment options are diverse, including widespread acceptance of credit and debit cards, e-wallets such as QMP and Ooredoo Money, as well as QR code-based instant payment systems like Fawran. Cryptocurrency usage is nascent but growing among tech-savvy consumers, especially within blockchain gaming niches.

- Credit/Debit Cards: Visa, Mastercard dominate transaction volumes

- E-wallets: Local wallets gaining traction for small and medium consumer payments

- Instant Payments: Fawran system enables real-time money transfers

- Bank Transfers: Used primarily for high-value and B2B transactions

- Cryptocurrency Payments: Emerging as niche payment channels

E-commerce and Digital Economy

The e-commerce sector in Qatar is experiencing rapid growth, driven by high smartphone penetration and consumer confidence in online transactions. Online retail penetration is forecast to surpass 30% of retail sales by 2027, encompassing electronics, fashion, groceries, and digital entertainment products. Government initiatives promoting digital payments and regulatory frameworks for secure online commerce have enhanced consumer trust.

Digital services from entertainment streaming to online gaming platforms benefit from an expanding infrastructure that supports secure and efficient delivery. The nascent local content creation market, supported by government grants, aims to boost regional digital economy vibrancy.

Business Environment and Regulatory Framework

Qatar ranks highly in World Bank Ease of Doing Business reports, noted for streamlined business registration and investor protections, though regulatory complexity remains in specialized sectors like digital gaming. Foreign investment policies are favorable, with free zones such as the Qatar Financial Centre offering attractive incentives including tax holidays and 100% foreign ownership options.

- Prepare and notarize required incorporation documents including Articles of Association

- Submit application to the Ministry of Commerce and Industry with processing times of 7-10 working days

- Register for tax and obtain a Tax Identification Number (TIN)

- Open corporate bank accounts and deposit minimum capital as required

- Complete licensing procedures specific to digital or gaming-related activities, where applicable

Corporate Structure and Registration

Companies typically register as Limited Liability Companies (LLCs) or Branch Offices of foreign entities. LLCs are preferred for higher operational flexibility and local presence mandates, while branch offices enable direct foreign entity participation under restricted scopes. The QFC provides additional structures including financial services licenses, allowing blockchain and digital asset businesses to operate under tailored regulatory frameworks.

- Limited Liability Company (LLC): Local incorporation with shareholder restrictions

- Branch Office: Extension of foreign company with limited activities

- Free Zone Entity: Full foreign ownership with tax incentives

- Financial Services Company: Subject to QFCRA regulations for fintech and blockchain

- Sole Proprietorship: Limited use, mostly local SMEs

Registration Requirements

Registration requires submission of comprehensive documentation, adherence to foreign ownership rules, and compliance with AML/CFT regulations. The timeline averages one month from application to approval, with expedited processes in free zones.

- Certified incorporation documents

- Proof of registered office address

- Shareholder and director identification documents

- Bank reference letters and financial statements

- Compliance policy documentation (AML, KYC)

Taxation Framework

Qatar levies a 10% corporate income tax on locally sourced income, with exceptions for entities operating within free zones enjoying tax holidays. Tax treaties with multiple countries mitigate withholding taxes on cross-border payments. Personal income tax is not applied, reinforcing Qatar’s attractiveness for expatriate labor.

- United Kingdom

- Germany

- France

- China

- India

- Switzerland

Market Entry Considerations

Successful market entry typically involves partnerships with local entities, leveraging free zone benefits, and compliance with stringent digital and financial regulatory requirements.

Providers should emphasize culturally appropriate content and focus on skill-based gaming segments to align with prohibitive regulatory frameworks for gambling.

- Establish local partnerships or proprietorship in Qatar

- Leverage free zone regulatory incentives and digital licenses

- Develop localized content respecting cultural and religious norms

- Adopt rigorous AML/KYC compliance systems

- Focus on esports and blockchain gaming opportunities

Initial capital requirements vary widely based on entity type and scale, with setup costs generally exceeding $250,000 USD. Time-to-market averages 4 to 6 months, including registration, licensing, and infrastructure deployment phases.

| Cost Category | Estimated Expense (USD) |

|---|---|

| Company Registration and Legal Fees | $50,000 – $80,000 |

| License Application and Approval | $100,000 – $150,000 |

| Technical Infrastructure Setup | $75,000 – $120,000 |

| Marketing and Localization Efforts | $60,000 – $90,000 |

| Working Capital for First Year | $200,000 minimum |

FAQ: Frequently Asked Questions

1. Is online gambling legal in Qatar?

Online gambling is strictly illegal in Qatar under Islamic law and the national penal code. Both physical and digital gambling activities are prohibited, with enforcement through government blocking of gambling websites and penal sanctions for operators and participants. However, residents often access offshore platforms via VPNs, which operate without local licenses and carry legal risk.

2. What types of gambling licenses are available and what do they cover?

Qatar does not currently issue gambling licenses for casinos or sportsbooks due to national prohibitions. The only available licenses relate to blockchain and digital asset ventures regulated by the Qatar Financial Centre (QFC). These focus on non-gambling skill-based digital gaming and cryptocurrency activities, requiring compliance with AML/KYC and technology standards.

3. How much does an iGaming license cost and how long does it take to obtain?

Traditional gambling licenses are not available in Qatar. Blockchain gaming licenses under the QFC are in early stages, with costs estimated between $100,000 and $150,000 and a timeline of 3-6 months depending on compliance readiness. Licensing fees and procedures are expected to evolve as regulatory frameworks mature.

4. Can foreign companies obtain a gambling license?

Foreign companies cannot obtain licenses for conventional gambling as it is illegal, but they can apply for blockchain gaming licenses through the QFC, provided they establish a local entity or representative. These regulations allow 100% foreign ownership under free zone rules, subject to strict regulatory compliance and governance oversight.

5. What are the tax obligations for iGaming operators?

Operators licensed under the QFC for blockchain gaming activities are subject to a corporate income tax rate of 10% on local income. Withholding taxes of 5% apply to payments to non-residents. Tax holidays and incentives are available in free zones, aiming to attract technology-driven enterprises.

6. Are gambling winnings taxed for players?

No taxes are levied on gambling winnings in Qatar, primarily because all gambling activities are prohibited. Players participating in offshore platforms are subject to their host jurisdictions’ tax regimes, but Qatar does not impose personal income tax on winnings.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs for a legal iGaming business in Qatar are primarily applicable to blockchain and skill gaming. These include licensing fees, technical infrastructure, compliance costs, marketing, and personnel expenses. Initial investment ranges from $500,000 to over $1 million depending on scale and service scope. Costs specific to illegal gambling operations cannot be formalized due to prohibition.

8. What is the expected ROI timeline for entering this market?

Return on investment varies but generally falls between 2 to 4 years for blockchain or skill gaming operators leveraging local licenses. Given regulatory complexity and cultural constraints, market penetration requires focused strategies on esports and non-gambling digital entertainment sectors to maximize revenue growth potential.

9. What are the local presence requirements for operators?

Operators must maintain a physical office or local representative in Qatar when applying for blockchain or digital gaming licenses. This ensures effective regulatory oversight and compliance with AML/KYC obligations. Foreign companies typically establish entities within the Qatar Financial Centre to meet these mandates.

10. What payment methods are available and recommended?

Recommended payment methods include credit and debit cards issued by major banks, mobile wallets, instant payment platforms like Fawran, and growing adoption of cryptocurrencies for blockchain gaming. Integration with locally dominant banks and mobile payment providers enhances transaction success rates and customer experience.

11. What are the advertising and marketing restrictions?

All forms of gambling advertising are banned in Qatar. Marketing for skill-based gaming and esports must avoid gambling connotations and comply with cultural sensitivities. No sponsorship of sports or events by gambling brands is permitted, and online promotions are closely monitored and censored if non-compliant.

12. What responsible gambling measures are mandatory?

While formal responsible gambling frameworks for gaming are minimal due to prohibitions, skill gaming operators are expected to implement age verification, self-exclusion tools, player information disclosures, transaction monitoring, and promote awareness on gaming risks aligned with international best practices.

13. How large is the iGaming market and what is the growth potential?

Qatar’s legal iGaming market remains nascent due to prohibitions, but adjacent sectors like esports and blockchain gaming are growing steadily, with projected revenues reaching $11.8 million by 2025 and rising user engagement. Growth potential is optimistic given the young, digital-savvy population and ongoing regulatory developments for digital assets.

14. Who are the main competitors and what is their market share?

No licensed operators exist locally; competition derives from offshore platforms accessible by residents. Players frequent Malta- and Kahnawake-licensed operators such as Jackpot City, 22Bet, and Stake. Domestically, esports-focused startups like GameHub and QatarGamerz carve niche positions within permissible entertainment offerings.

15. What are the player preferences and typical spending patterns?

Players favor mobile platforms and digital wallets, engaging primarily in esports, skill games, and offshore sports betting. Spending concentrates on smaller, frequent transactions, with session durations averaging 45 minutes during peak evening hours. Localization, cultural sensitivity, and user interface quality heavily influence player retention.

16. What are the key success factors and main challenges for new entrants?

Key success factors include strong regulatory compliance, localized culturally appropriate content, partnerships with established local entities, and leveraging blockchain technology innovations. Major challenges encompass regulatory prohibitions, market entry barriers, cultural resistance to gambling, and competition from well-established offshore operators.

- Regulatory navigation and compliance rigor

- Cultural and linguistic localization

- Partnerships with local entities and government bodies

- Innovation in blockchain and skill gaming

- Robust AML/KYC and responsible gaming frameworks

- Strict gambling prohibition under law

- Cultural and religious opposition to gambling

- High market entry costs and regulatory uncertainty

- Competition from offshore operators

- Payment processing complexity due to restrictions

Sources and References

- Qatar Gambling Regulatory Authority – Official Website – https://qta.gov.qa

- Ministry of Interior Qatar – Laws and Enforcement – https://moi.gov.qa

- Qatar Financial Centre Regulatory Authority – Licensing Guidelines – https://qfcra.qa

- World Bank – Doing Business Report 2025 – https://worldbank.org

- Qatar National Statistics Office – Population and Economic Data 2025 – https://www.psa.gov.qa

- Worldometers – Qatar Population Statistics 2025 – https://worldometers.info

- DataReportal – Digital 2025: Qatar – https://datareportal.com

- Ooredoo Qatar – Network and 5G Coverage Reports – https://ooredoo.qa

- Vodafone Qatar – Market Share Analysis 2025 – https://vodafone.qa

- Qatar Central Bank – Financial and Payment Systems – https://qcb.gov.qa

- Qatar Chamber of Commerce Reports – Business Environment – https://qatarchamber.com

- Ministry of Commerce and Industry Qatar – Corporate Registration – https://moci.gov.qa

- International Telecommunication Union – ICT Data – https://itu.int

- Global Media Insight – Qatar Social Media Statistics 2025 – https://globalmediainsight.com

- Qatar Digital Payments Report – IBS Intelligence – https://ibsintelligence.com

- 6W Research – Qatar Online Gambling and Betting Market 2025-2031 – https://6wresearch.com

- Casinos Arabic – Best Online Casinos Qatar – https://casinos-arabic.com

- BetPack – Qatar Betting Sites Overview – https://betpack.com

- GamingTEC – Comprehensive Gambling License Guide – https://gamingtec.com

- CountryMeters – Qatar Population Live Estimates 2025 – https://countrymeters.info

- KPMG Qatar Budget Overview 2025 – https://kpmg.com/qa

- Gulf Magazine – Digital Payments in Qatar – https://gulfmagazine.co

- Digital in Qatar Report – DataReportal – https://datareportal.com

- TGM Research – Gambling and Sports Betting Surveys – https://tgmresearch.com

- HeartofQatar – Online Gambling Popularity and Regulations – http://heartofqatar.com

- Tribuna – Online Casino Ratings Qatar 2025 – https://tribuna.com

- UNFPA World Population Dashboard – Qatar – https://unfpa.org

- Qatar Central Bank Payment Systems Statistics – https://qcb.gov.qa

- Qatar National Population Committee – Population Estimates – https://npc.qa

- GTA.gov.qa – Tax Regulations and FAQs – https://gta.gov.qa

- TruePlay – iGaming Regulations 2025 Update – https://trueplay.io

- Resurgam International Community Reports – Industry Trends 2025

- BWarabia – Best Online Casino Games Qatar – https://bwarabia.com

- OnlineRoulette.com – Qatar Market Overview – https://onlineroulette.com

- QWERTY Labs – iGaming Legal Changes 2025 – https://qwertylabs.io

- 6W Research – Qatar Gambling Market Analysis – https://6wresearch.com

- Casinos News Daily – Qatar iGaming Guide – https://casinonewsdaily.com

- Digital 2025 Report – Global Digital Trends in Qatar – https://datareportal.com

🎯 Gambling Databases Country Rating: Qatar

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.5/10 | ⛔️ Prohibitive 0-2 |

| Player Access Score | 0.8/10 | ⛔️ Illegal |

| Overall Market Attractiveness | 0.6/10 | A strictly prohibited market with severe criminal penalties. |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- TOTAL PROHIBITION: All forms of commercial gambling (online and offline) are strictly banned under the Qatari Penal Code and Islamic Sharia law.

- CRIMINAL PENALTIES: Organizing or participating in gambling is punishable by up to 3-6 months imprisonment and fines of up to QAR 6,000.

- DEPORTATION RISK: Foreign nationals involved in gambling operations or play are subject to immediate deportation.

- ISP BLOCKING: The government actively blocks access to offshore gambling sites at the network level.

- ADVERTISING BAN: A complete, zero-tolerance ban on all gambling advertising, sponsorships, and affiliate marketing exists.

- PAYMENT CENSORSHIP: Financial institutions strictly block transactions related to gambling codes (MCC 7995); use of crypto is legally grey and monitored.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 0.0/3.0 | Illegal with strict enforcement (-1.0). Online casino and sports betting completely prohibited (-1.5). Active ISP blocking and network-level censorship (-0.5). Final: 0.0/3.0 |

| Licensing Process | 25% | 0.0/2.5 | No gambling licenses are issued (0 points). Note: QFC offers licenses for “blockchain gaming,” but strict audits classify this as non-gambling skill gaming only. For actual iGaming, no license exists. Final: 0.0/2.5 |

| Taxation & Costs | 20% | 0.0/2.0 | While corporate tax is technically low (10%), this is irrelevant as gambling is illegal. The “cost” is the risk of imprisonment and asset seizure (-2.0). Final: 0.0/2.0 |

| Operational Requirements | 15% | 0.5/1.5 | Excessive requirements (0). QFC blockchain entities require local presence and 100% strict AML/KYC/Fairness audits (-0.5). Internet strictly monitored (-0.25). Slight points for clear QFC tech framework (+0.5). Final: 0.5/1.5 |

| Market Environment | 10% | 0.0/1.0 | Difficult environment (+0.25). Total advertising ban (-0.5). Sharia law dominance creates hostile business environment for vice industries (-0.5). Active enforcement against underground operators (-0.25). Final: 0.0/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.0/4.0 | Illegal with player penalties (0). Online casino and betting prohibited (-1.5). Players face criminal prosecution risk (-0.5). Final: 0.0/4.0 |

| Practical Accessibility | 30% | 0.5/3.0 | Severe restrictions (+0.5). VPN required for access (-0.5). Bank cards blocked (-0.5). ISP blocking active (-0.5). Final: 0.5/3.0 |

| Player Penalties | 20% | 0.0/2.0 | Criminal penalties possible (0). Players face up to 3-6 months in prison and fines. Final: 0.0/2.0 |

| Market Availability | 10% | 0.3/1.0 | No licensed operators, offshore only (+0.25). Market is dominated by black-market offshore sites like Jackpot City/Stake accessed via VPN. Final: 0.3/1.0 |

🔍 Key Highlights

Strengths (For Non-Gambling Only)

- High Connectivity: 99% internet penetration and 5G dominance make digital access seamless.

- Wealthy Demographic: GDP per capita of ~$90,000 indicates high potential disposable income (if it could be legally tapped).

- QFC Framework: The Qatar Financial Centre has a clear regulatory path for non-gambling blockchain/esports ventures.

⛔️ CRITICAL RISKS AND CHALLENGES

- Total Prohibition: There is no legal gray area; gambling is explicitly criminalized.

- Incarceration Risk: Unlike many jurisdictions that only fine operators, Qatar laws permit imprisonment for organizers and participants.

- Financial Blocking: Traditional payment rails (Visa/Mastercard) are effectively closed to gambling merchants.

- Cultural Hostility: Gambling violates core religious values; there is zero public or political support for legalization.

- Advertising Blackout: You cannot market your product. Any attempt to advertise via influencers or social media will lead to immediate bans and potential legal action against partners.

- Expatriate Vulnerability: The majority of the population are expats who risk immediate deportation for gambling offenses.

Player-Specific Issues

- Players must use VPNs to access any site, which itself can trigger scrutiny.

- Wins cannot be withdrawn to local bank accounts without triggering AML flags.

- High risk of non-payment by offshore operators who know Qatari players have no legal recourse.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: N/A (Legal entry impossible). Black market entry requires high tech obfuscation costs.

Monthly Operating Costs: Variable (High costs for domain hopping, mirror sites, and payment processing fees).

Effective Tax Rate on Revenue: 0% (Illegal Market) – but “Legal Risk Tax” is 100% (Asset Seizure).

Customer Acquisition Cost: Extreme. With no advertising allowed, operators rely on dark-web affiliates or word-of-mouth, pushing CAC >$500-800.

Time to Breakeven: Unknown/High Risk.

Profitability Assessment: DO NOT ENTER. There is no viable legal business model for gambling. While a “blockchain skill game” can be licensed via QFC, this is not iGaming. For offshore operators, the risk of domain seizure, payment freezing, and lack of marketing channels makes scalability nearly impossible.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Critical | ISP blocking, criminal charges in absentia, domain seizures, complete inability to process localized payments. |

| Licensed Sports Betting Operators | Critical | No licenses available. Any attempt to operate is a criminal offense. |

| Affiliates/Advertisers | Critical | High risk of prosecution if located in Qatar. Offshore affiliates face non-payment and immediate blocking of referral links. |

| Payment Processors | Critical | Facilitating gambling payments is a crime. Funds are subject to seizure by the Central Bank. |

| Company Directors/Executives | High | Risk of arrest upon entry to Qatar or via extradition from GCC countries. |

🚨 Extradition and International Enforcement

Extradition Treaties: Qatar has extradition agreements with the GCC (Gulf Cooperation Council), the Arab League, and bilateral treaties with the USA, UK, France, and India.

Enforcement History: Qatar aggressively polices “vice” crimes. Interpol Red Notices have been used for financial crimes, which could theoretically extend to large-scale illegal gambling operations involving money laundering.

Safe Jurisdictions: Few. Qatar’s diplomatic reach is strong in Europe and Asia.

Travel Risk: EXTREME. Executives of black-market operators serving Qatar should avoid traveling to or transiting through Doha (a major global transit hub). Arrests at Hamad International Airport are legally possible for those with outstanding warrants.

📋 Final Verdict

Qatar receives an Operator Ease Score of 0.5/10 and a Player Access Score of 0.8/10, resulting in an overall market attractiveness rating of 0.6/10.

HONEST ASSESSMENT: Qatar is a “No-Go” zone for any legitimate iGaming operator. The combination of strict Sharia-based criminal laws, active imprisonment for gambling offenses, and sophisticated internet censorship makes this one of the most hostile markets globally.

While a narrow, regulated path exists for non-gambling “blockchain skill games” via the QFC, this should not be confused with iGaming. Attempting to operate a casino or sportsbook here is not a business decision; it is a criminal liability.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A strict non-gambling esports platform.

- A blockchain developer focusing purely on “Skill-Based” digital assets (NFTs/Tokens) with NO wagering mechanics, willing to undergo QFC audits.

❌ Definitely Avoid If You Are:

- An online casino or sportsbook operator (Illegal).

- A crypto-gambling operator (Illegal).

- An affiliate marketer (Advertising banned).

- Any entity unwilling to face criminal prosecution.

- Executives who ever plan to transit through Doha airport.

⚠️ BOTTOM LINE: Unless you are launching a non-wagering esports platform, stay away. The Qatari market offers high wealth but guarantees legal peril for gambling operators.