Spain’s iGaming sector has grown steadily, supported by robust regulatory oversight and consumer demand for online betting and casino services. The market is characterized by strict licensing standards and active government regulation aimed at ensuring fair play and consumer protection.

For operators, understanding the complex regulatory environment and compliance requirements is essential for successful market entry.

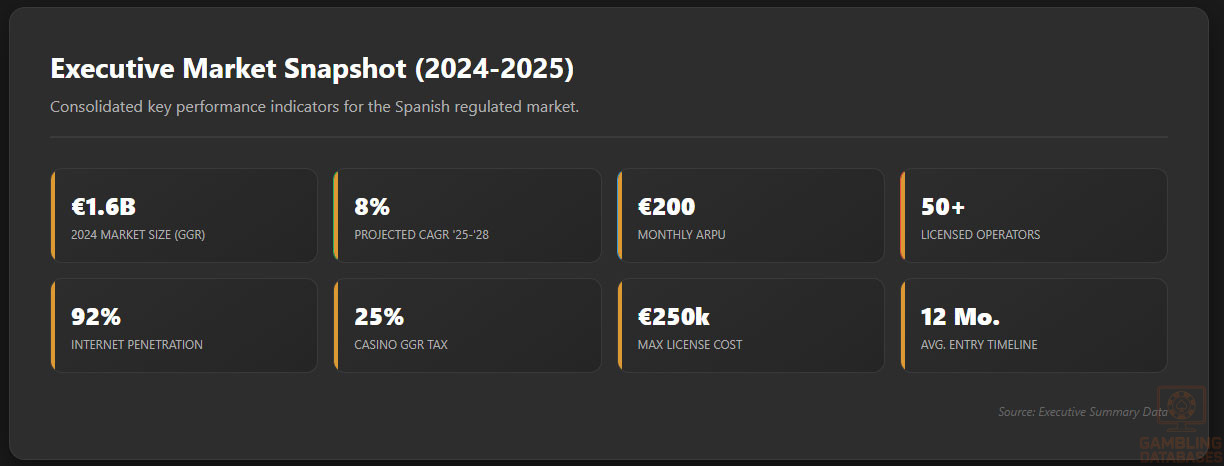

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Legal status of gambling | Fully regulated; licensed online and land-based operations |

| Population | 47 million (2025 estimate) |

| GDP | $1.4 trillion (2025 estimate) |

| Internet penetration rate | 92% |

| Mobile penetration rate | 89% |

| Average licensing cost | €150,000 – €250,000 |

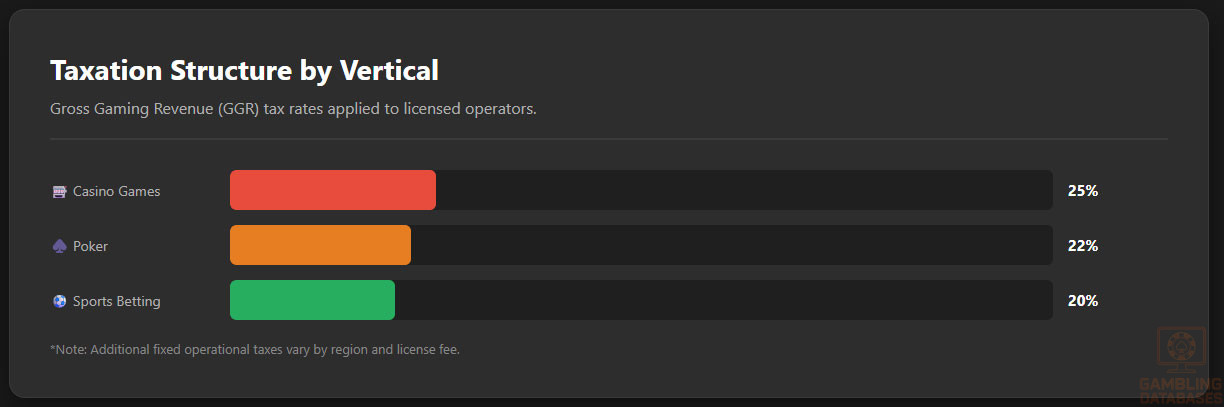

| Tax rate on GGR | 25% (casino games), 20% (betting) |

| Market entry timeline | 6–12 months |

| Number of licensed operators | Over 50 |

| Market size (2024 revenue) | €1.6 billion |

| Projected CAGR (2025–2028) | 8% |

| ARPU | €200/month |

| Market penetration rate | Close to 70% |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Spain maintains a comprehensive regulatory framework for all gambling activities, emphasizing consumer protection and integrity of operations. Land-based gambling includes casinos, sports betting venues, and slot halls, all regulated by the national authorities.

Online gambling laws are governed by specific legislation and licenses issued by the Dirección General de Ordenación del Juego.

Land-Based Gambling Activities

Casino operations are permitted in designated regions, with strict licensing and oversight. Sports betting is widespread, both online and on physical venues. Slot machine halls operate under licenses issued by regional governments, with limitations on machine numbers. Other land-based activities include bingo, poker clubs, and lottery outlets, each regulated separately.

Online Gambling Framework

The digital gambling sector is regulated under the Ley 13/2011, which established the legal basis for online gaming, including sports betting, casino games, poker, and bingo.

Licensed Operators and Market Players

The market features over 50 licensed operators, including major international brands and local companies. The competitive landscape is driven by strict compliance standards, technological innovation, and aggressive marketing strategies. Key players maintain substantial market shares, with new entrants needing to navigate licensing barriers and establish local partnerships to succeed.

Licensing Framework and Requirements

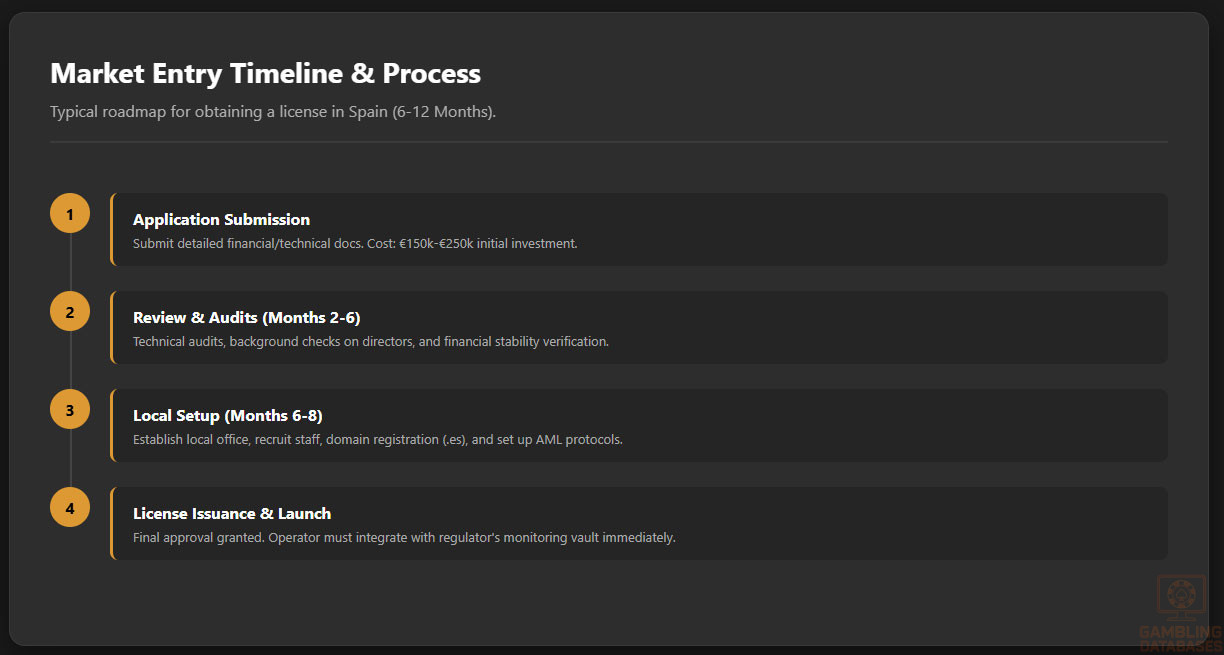

Application Process and Eligibility

Operators must submit a detailed licensing application to the regulatory authority, demonstrating financial stability, technical expertise, and compliance measures. The application process involves an initial review, technical audits, and background checks. Total costs range from €150,000 to €250,000, with license issuance typically taking 6 to 12 months, depending on completeness and complexity.

Local Presence and Operational Requirements

Applicants are required to establish a local presence, including a local office, domain registration within Spain, and employing a minimum number of local personnel.

Foreign ownership restrictions are limited but necessitate compliance with anti-money laundering (AML) and responsible gaming policies. Commercial partnerships with local firms are advantageous for market entry.

Compliance Obligations and Monitoring

Player Protection and Identification

Operators must implement strict KYC/AML procedures, verify player age, and promote responsible gambling through self-exclusion options and public information campaigns. Mandatory measures include setting deposit limits, providing responsible gaming tools, and issuing clear disclosures about game odds and payout percentages.

Financial Monitoring and Reporting

Operators are required to monitor all transactions, report suspicious activities, and submit regular financial audits. Reporting involves several steps, including tracking player deposits/withdrawals, analyzing suspicious transactions, and submitting compliance reports quarterly or upon request by authorities.

Taxation Structure and Financial Obligations

Player Taxation

Winnings above certain thresholds are subject to withholding taxes, with rates depending on the game type and wager size. Players are responsible for declaring taxable winnings in their personal income statements according to Spanish tax law.

Operator Taxation

| Game Type | Tax Rate |

|---|---|

| Casino games (GGR tax) | 25% |

| Sports betting (GGR tax) | 20% |

| Poker and other skill games | 22% |

| Fixed operational taxes | Varies by region and license fee |

Annual license renewal fees are approximately €100,000 to €250,000, with additional revenue-based turnover taxes applied periodically. The combination of taxes influences operational profitability and strategic pricing.

Gambling Market Financial Performance

The total wagered amount in 2024 reached over €12 billion, with payouts estimated at €10.4 billion, yielding gross gaming revenues (GGR) of approximately €1.6 billion. Tax revenues generated from industry activities contribute substantially to regional budgets, with consistent year-on-year growth driven by expanding online participation.

Advertising and Marketing Restrictions

Advertising must adhere to strict content restrictions and cannot target minors or vulnerable populations. Permitted channels include licensed broadcasters, online platforms, and regional sponsorships, but advertisement timings are regulated to minimize gambling promotion during certain hours. Content must include responsible gaming messages and clear rules.

Recent Regulatory Changes and Their Impact

In recent years, regulatory amendments have included increasing licensing fees, tightening player verification procedures, and expanding responsible gaming measures.

These changes have increased operational costs but enhanced market integrity, encouraging more robust compliance practices among operators.

Enforcement Mechanisms and Penalties

Violations of licensing obligations or consumer protection standards can result in fines, license suspensions, or revocation. Enforcement actions focus on curbing illegal activities and safeguarding consumer interests, with penalties escalating based on the severity of non-compliance.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

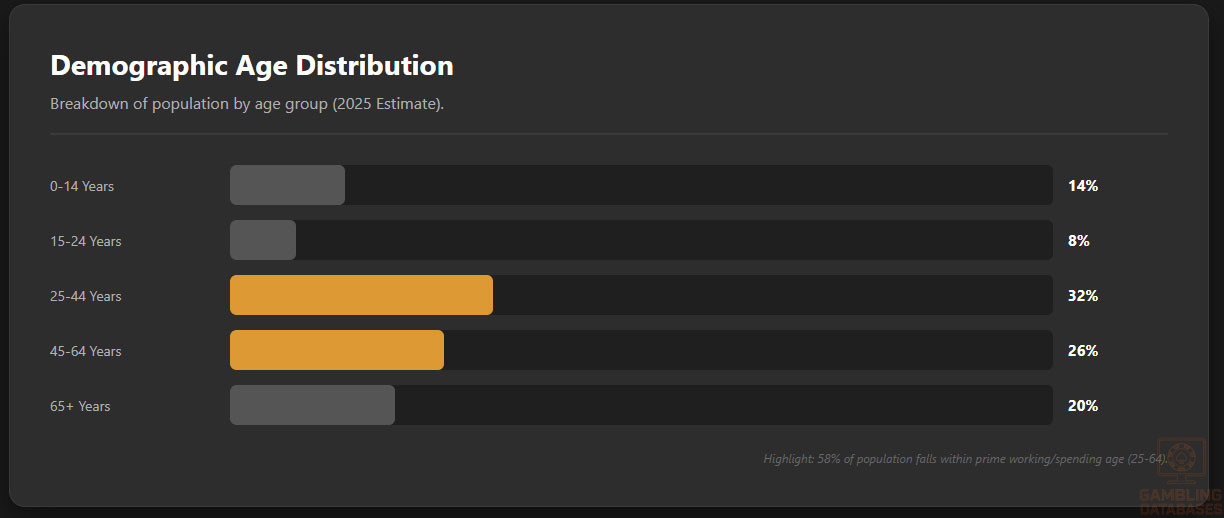

Spain’s total population is estimated at 47 million in 2025, with a median age of approximately 44 years, reflecting an aging demographic trend. The gender ratio is relatively balanced, with a slight female majority at 51%. Youth under 25 years constitute around 22%, while those aged 65 and older represent about 20%, indicating important implications for consumer market segmentation.

Urbanization is high in Spain, with over 80% of the population residing in urban areas, creating concentrated demand hubs for online gambling services and physical venues. Rural areas remain less connected but benefit from improving digital infrastructure, gradually expanding market reach beyond traditional urban centers.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 14% |

| 15-24 years | 8% |

| 25-44 years | 32% |

| 45-64 years | 26% |

| 65+ years | 20% |

Geographic Distribution

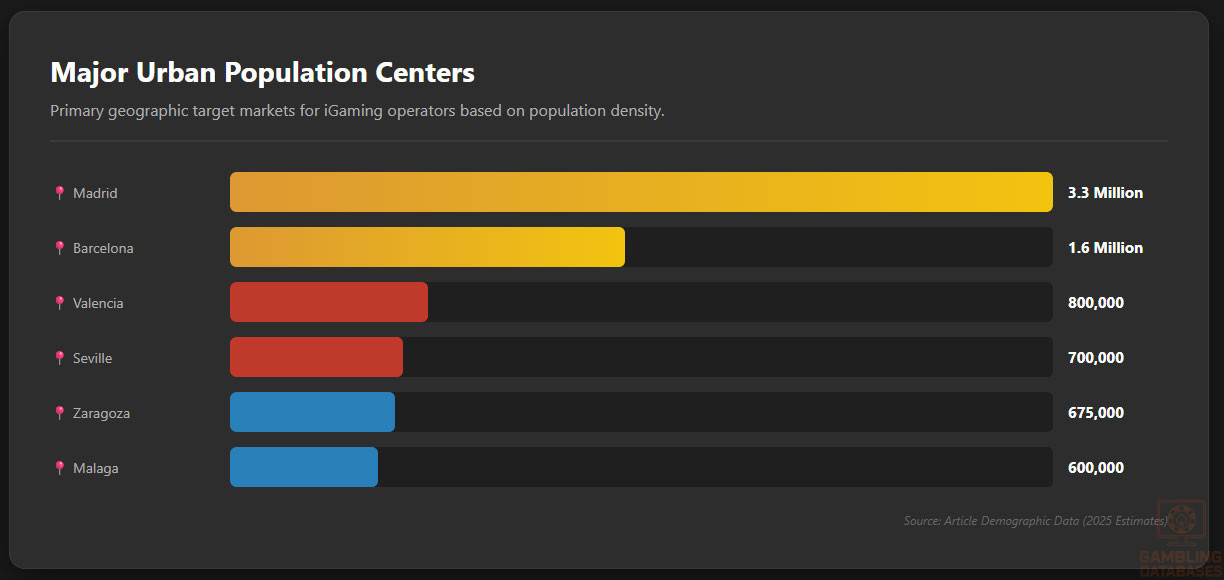

Spain’s population is concentrated in several major cities that serve as economic and cultural centers. These urban areas provide substantial consumer bases for iGaming operators owing to high disposable incomes and internet accessibility.

- Madrid: approximately 3.3 million residents

- Barcelona: approximately 1.6 million residents

- Valencia: approximately 800,000 residents

- Seville: approximately 700,000 residents

- Zaragoza: approximately 675,000 residents

- Malaga: approximately 600,000 residents

- Murcia: approximately 450,000 residents

Major cities exhibit near-universal internet access, while regional disparities appear more pronounced in southern and interior provinces. Gambling venues and betting shops concentrate heavily in metropolitan areas, matching population density and economic activity. Regional variations affect operator strategies, with localized marketing and service adaptations common.

Economic Indicators and Consumer Spending Power

Spain’s GDP reached nearly $1.4 trillion in 2025 with a forecasted annual growth rate of around 2.3% over the next five years. Services dominate the economy, accounting for approximately 75% of GDP, followed by industry at 20% and agriculture at 5%. Economic stability and diversified sectors support robust consumer spending.

Average household income hovers near €28,000 annually, with median income slightly lower due to income inequality. The Gini coefficient of approximately 34 indicates moderate income disparity. Disposable income shows positive trends driven by inflation control and wage growth, favoring discretionary expenditure including entertainment and gaming activities.

| Indicator | Value |

|---|---|

| GDP | $1.4 trillion |

| GDP Growth Forecast (2025-2030) | 2.3% CAGR |

| Average Household Income | €28,000/year |

| Median Income | €24,000/year |

| Gini Coefficient | 34 |

| Service Sector Contribution | 75% GDP |

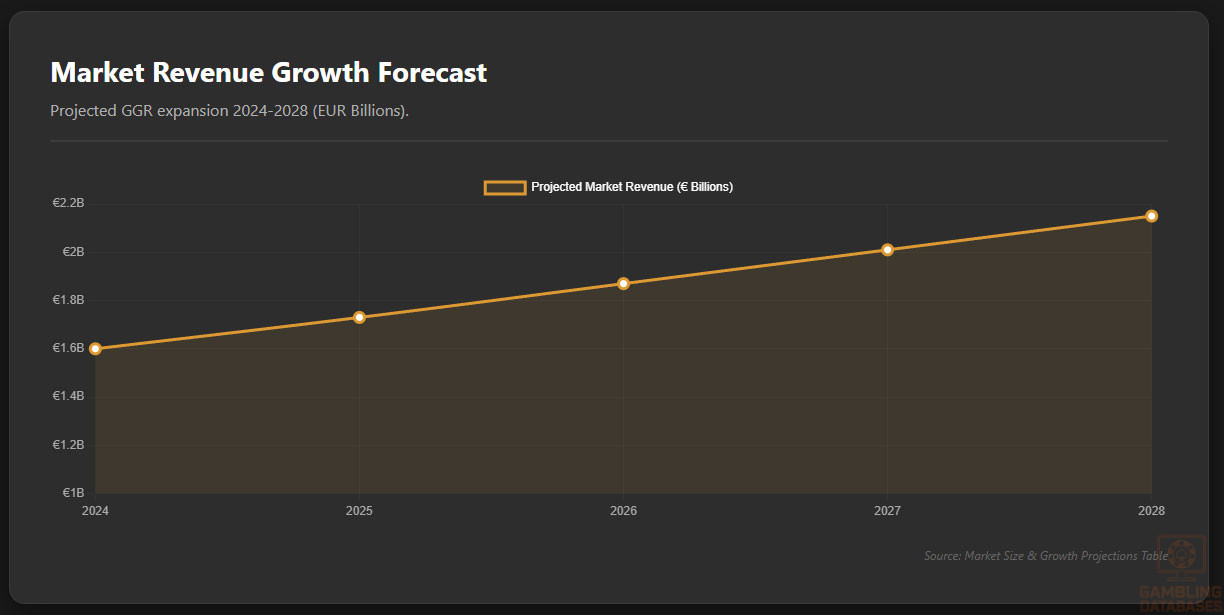

The Spanish gambling market revenue accrued to approximately €1.6 billion in 2024, reflecting an 8% compound annual growth rate projected through 2028. The user base for online gambling is expanding quickly, supported by rising digital literacy and smartphone adoption.

The average revenue per user (ARPU) maintains a robust figure of €200 per month, underscoring strong consumer spending power and engagement in regulated markets.

| Metric | 2024 | 2028 (Forecast) |

|---|---|---|

| Market Revenue | €1.6 billion | €2.15 billion |

| Annual Growth Rate (CAGR) | 8% | – |

| Active Users | ~8 million | ~10.5 million |

| Average Revenue Per User (ARPU) | €200/month | €220/month |

Education, Skills, and Digital Literacy

Spain enjoys a high literacy rate exceeding 98%, supported by mandatory education and widespread access to higher learning institutions. Digital literacy has seen rapid improvements, with extensive digital skills among adults especially in urban areas. The workforce is increasingly technology-oriented, facilitating engagement with online platforms including iGaming services.

The country boasts a growing population of digitally savvy young adults and middle-aged professionals who are comfortable with mobile and desktop online gaming technologies. Continuous educational reforms address skills gaps, particularly in STEM fields, enhancing consumer readiness for innovative gambling platforms and fintech integrations.

Cultural and Social Factors

Communication and Language

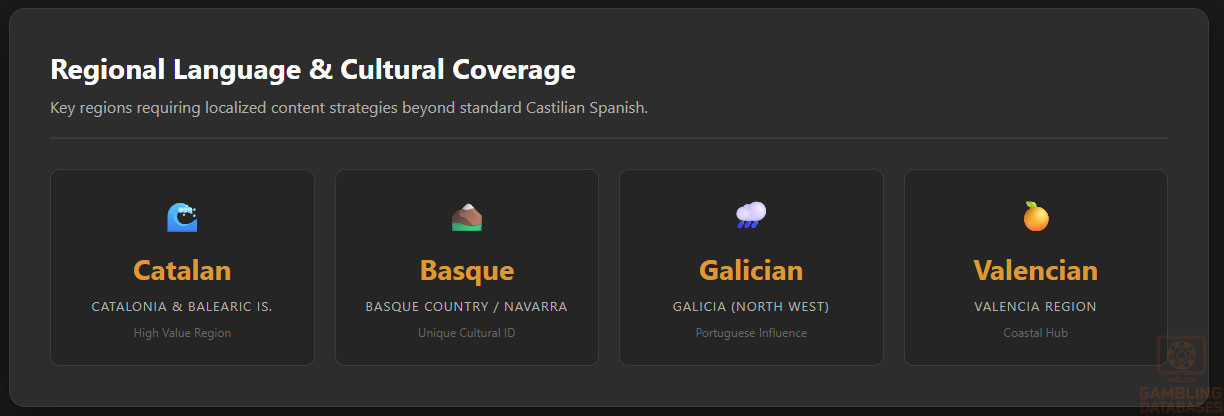

Spanish (Castilian) is the official and dominant language nationwide, utilized in digital platforms, marketing, and user interfaces. Regional languages such as Catalan, Basque, and Galician hold official status in their respective territories and influence localized content strategies for gaming operators targeting these populations.

- Spanish (Castilian) – primary language nationally

- Catalan – spoken in Catalonia and Balearic Islands

- Basque (Euskara) – spoken in Basque Country and parts of Navarra

- Galician (Galego) – spoken in Galicia

- Valencian – variant of Catalan spoken in Valencia region

Cultural Attitudes

Gambling is broadly culturally accepted as a form of entertainment, with traditional land-based activities dating back decades. Religious influences are moderate and generally do not strongly oppose regulated gambling. Foreign gaming brands are viewed with interest, particularly those with strong reputations for safety and innovation.

Entertainment preferences are diverse, with sports betting, lotteries, and electronic gaming machines occupying leading positions. Spaniards demonstrate a preference for platforms offering social interaction and competitive elements, influencing the popularity of live dealer games and esports betting.

Problem Gambling and Social Considerations

Prevalence of problem gambling is estimated at approximately 2-3% of the adult population. Government and industry stakeholders collaborate on initiatives targeting at-risk groups, with mandatory social responsibility contributions from operators financing prevention programs. Awareness campaigns focus on youth, vulnerable adults, and heavy gamblers to mitigate social harms.

- National helpline and counseling services

- Self-exclusion schemes integrated across operators

- Mandatory operator funding for education campaigns

- Research programs to monitor gambling behaviors

- Regulatory audits assessing social responsibility compliance

Political Structure and Governance

Spain operates as a parliamentary constitutional monarchy with stable democratic institutions. Political stability supports consistent regulatory enforcement and progressive policy development.

The government maintains active cooperation with European Union frameworks, fostering regulatory harmonization and cross-border operator oversight.

Technology Adoption and Digital Behavior

Internet and Digital Usage

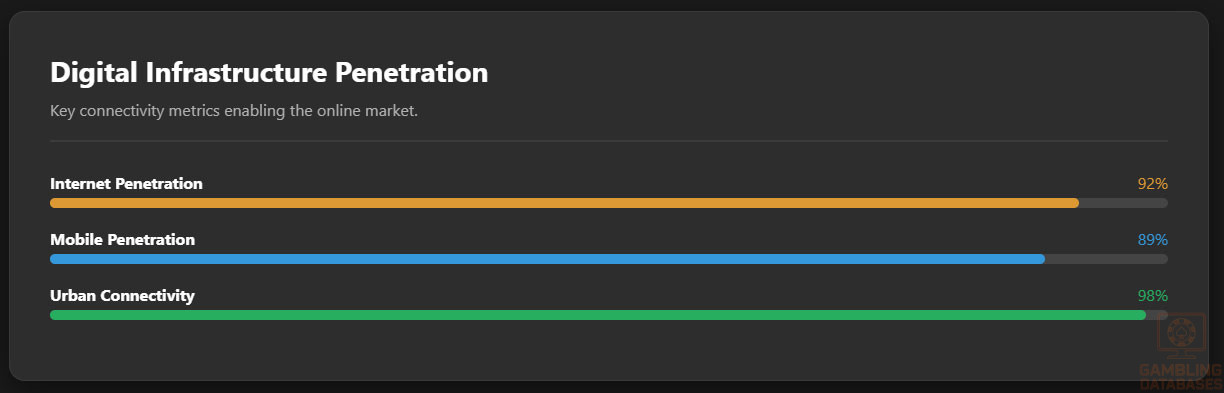

Internet penetration in Spain stands at 92%, with average daily usage of approximately 6 hours per user. Mobile internet adoption is widespread, with 89% of the population accessing services via smartphones. Social media engagement remains high, particularly among younger demographics, creating significant opportunities for digital marketing in iGaming.

- Facebook: reaches 78% of internet users

- Instagram: 64% popularity among 18-34 year olds

- YouTube: 89% penetration with average 45 minutes daily watch

- TikTok: rapidly growing with 52% adoption under age 25

- Twitter: utilized by 31% of online population for news

- LinkedIn: accessed by 28% for professional networking

Digital Payment Behavior

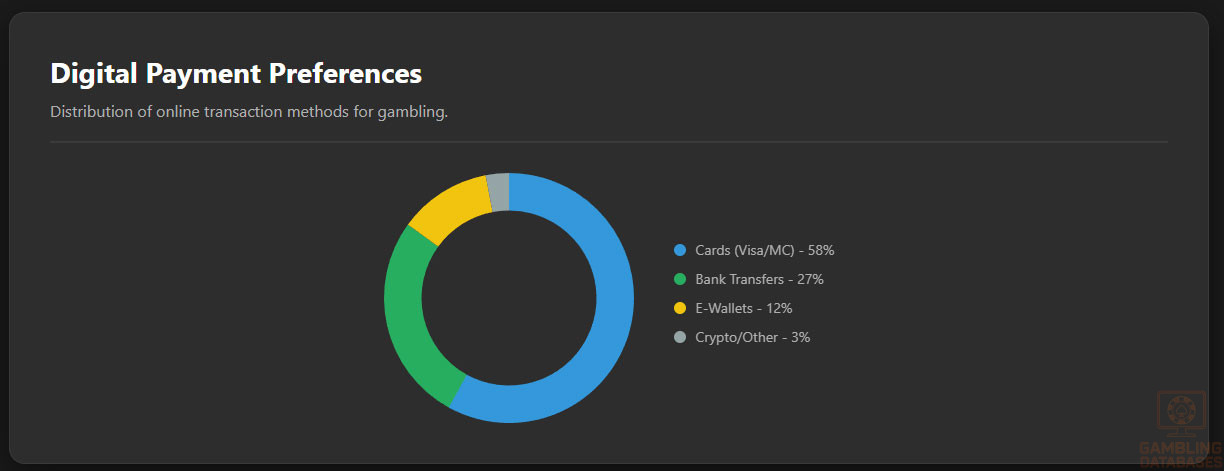

Spanish consumers favor a mix of traditional and digital payment methods. Credit and debit cards dominate online and mobile transactions, followed by bank transfers and fast-growing e-wallet usage. Cryptocurrency adoption is emergent but not yet mainstream, with regulatory caution affecting uptake.

- Credit/debit cards: 58% of online payments

- Bank transfers: 27% of payment volume

- E-wallets (PayPal, Skrill): 12% with young user growth

- Mobile payment apps (Bizum): rapid adoption

- Cryptocurrencies: niche but expanding interest

Gaming and Gambling Preferences

Current Market Participation

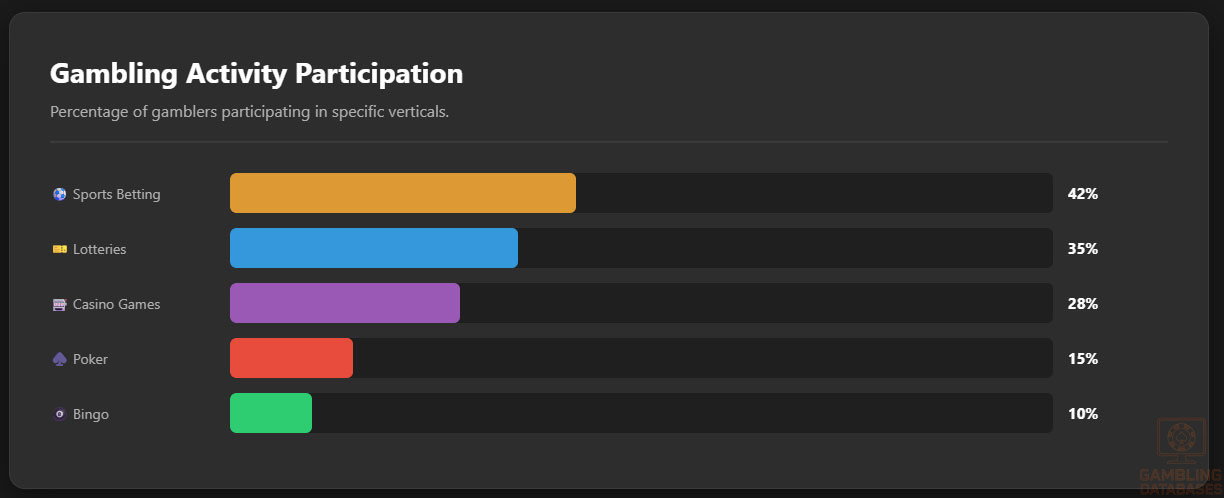

More than 70% of the adult population engages in some form of gambling annually, with online platforms experiencing the fastest growth. Sports betting remains the most popular activity, followed by lotteries, casino games, poker, and bingo. Younger consumers tend toward esports and interactive game formats.

- Sports Betting

- Lotteries

- Online Casino Games

- Poker

- Bingo

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 42% |

| Lotteries | 35% |

| Online Casino Games | 28% |

| Poker | 15% |

| Bingo | 10% |

Consumer Behavior Patterns

Spanish consumers demonstrate strong loyalty to licensed operators offering user-friendly interfaces and local language support. Peak activity periods correspond with major sporting events, weekends, and holiday seasons. Session lengths average between 25-40 minutes online, with mobile platforms driving increased frequency and shorter engagement bursts. Retention strategies focus on gamification, personalized rewards, and social community features.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Spain boasts an extensive digital infrastructure, with internet penetration reaching approximately 92% of the population. Broadband adoption is almost universal in urban centers, supported by a high-speed fiber optic rollout that averages download speeds of 150 Mbps, with some cities exceeding 300 Mbps. The network is reliable, providing stable connections critical for online gambling and digital services.

Investments in infrastructure continue, with broadband expansion extending into rural regions to diminish digital divides. Telecom operators have prioritized upgrades, ensuring low latency and high uptime, essential for live betting and real-time casino platforms.

5G and Future Technology Deployment

5G coverage is rapidly expanding across Spain, with major operators like Movistar, Vodafone, Orange, and MásMóvil committed to nationwide rollouts by 2026. Future plans include increasing capacity, reducing latency, and enabling IoT applications. This deployment will significantly enhance user experiences, enabling seamless mobile betting and augmented reality gaming.

Mobile Technology Ecosystem

The mobile infrastructure landscape is robust, with five leading operators controlling over 98% of the market share. Coverage is comprehensive, with urban areas enjoying high-speed 4G LTE networks and 5G in select regions. Data costs are competitive, averaging around €10-€20 per GB for consumers, supporting high-frequency mobile gambling usage.

Device Penetration

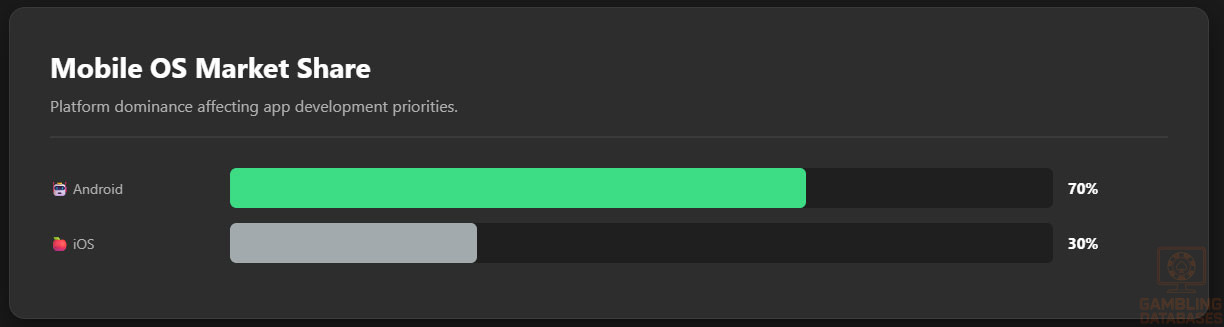

Smartphones have near-saturation in Spain, with over 89% of the population owning a mobile device. iOS and Android dominate, with Android holding approximately 70% market share. Device preferences lean towards high-performance models capable of supporting graphics-intensive casino games and live streams.

Usage patterns show mobile devices being the primary platform for both casual and serious gamblers, especially during peak sporting events or social occasions.

Financial Services and Payment Infrastructure

The banking system is dominated by several major banks, including Banco Santander, BBVA, CaixaBank, Sabadell, and Bankia, which collectively serve the majority of consumers. Digital banking penetration is high, with over 83% utilizing online or mobile banking services. This facilitates fast, secure transactions and supports robust funding channels for online gambling accounts.

Payment Processing Options

- Credit and debit cards (Visa, MasterCard)

- Popular e-wallets (PayPal, Skrill, Neteller)

- Bank transfers with instant processing (Bizum, SEPA transfers)

- Prepaid cards and vouchers

- Cryptocurrency platforms (limited, with growing interest)

E-commerce and Digital Economy

Spain’s e-commerce market is among the largest in Europe, with a value exceeding €120 billion in 2024. Online retail penetration impacts various sectors, from electronics to apparel, contributing to consumer trust and familiarity with digital transactions.

Business Environment and Regulatory Framework

Ease of Business Operations

Spain ranks favorably in global ease of doing business, with streamlined registration processes, efficient legal procedures, and supportive policies for foreign investment. Setting up a business involves registering with the National Registry, obtaining tax identification, and fulfilling compliance requirements. The overall process typically takes 10-15 days, with costs varying based on business complexity.

- Choosing the legal entity (LLC, branch)

- Registering with the Companies Registry

- Registering for taxes and social security

- Securing necessary licenses and permits

Corporate Structure and Registration

Common entity types include LLCs, public and private corporations, and branch offices. LLCs are preferred for their flexibility and limited liability, while branches are suitable for foreign companies seeking swift market entry. Registration requires submission of incorporation documents, proof of capital, and director details, usually completed within a week.

Registration Requirements

- Articles of incorporation and notarized certificates

- Fiscal and legal identification numbers

- Proof of deposit of minimum capital (€3,000 for LLCs)

- Business address registration

- List of directors and shareholders

Taxation Framework

Corporate Income Tax Structure

The standard corporate income tax rate is 25%. Special economic zones and innovation hubs may benefit from reduced rates or tax holidays. Spain has bilateral treaties with about 90 countries, including the US, UK, Germany, and France, easing cross-border taxation issues and facilitating international investments.

Personal Income Tax

Individual tax rates are progressive, ranging from 19% to 47%, depending on income brackets. Withholding taxes apply to gambling winnings, typically at 20% for non-residents. Social security contributions are mandatory for employees and employers, constituting approximately 30% of gross salaries.

Market Entry Considerations

Recommended Entry Strategies

Strategic partnerships with local firms enhance market understanding and regulatory navigation. Licensing and compliance processes are streamlined via regional authorities, with platform localization, multilingual content, and tailored marketing crucial for success. Investing in local customer support fosters trust and loyalty.

- Partner with Spanish operators or affiliates

- Leverage localized platform solutions

- Engage regional marketing channels

- Invest in responsible gaming and CSR programs

- Utilize advanced data analytics for customer targeting

Typical Costs and Timelines

- Initial licensing and registration: €150,000–€250,000

- Platform development and localization: €100,000–€300,000

- Operational expenses (staff, marketing): variable

- Time to market: approximately 8-12 months

- Regulatory approval process: 6–12 months

Success Factors and Challenges

Locally tailored offerings, robust compliance, and effective marketing are key enablers. Challenges include navigating complex licensing, high taxation, and cultural nuances. Establishing trust and maintaining data security are critical for long-term growth.

Exit Strategy Planning

Market liquidity allows for potential acquisition or license transfer. Regulatory frameworks permit ownership and license transfers with approval, enabling strategic sales or restructuring. Valuations often use EBITDA multiples, reflecting growth prospects and regulatory stability.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Spain?

Yes, online gambling is fully legal and regulated in Spain. The sector is overseen by the Dirección General de Ordenación del Juego, which issues licenses for operators. All online gambling platforms must comply with strict standards on player protection, security, and responsible gaming initiatives.

2. What types of gambling licenses are available and what do they cover?

Spain offers several licenses including general online gaming licenses covering casino games, sports betting, poker, and bingo. Specific licenses are required for each activity, with distinct requirements and fee structures. Operators often need separate licenses for land-based and online operations.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing fees typically range from €150,000 to €250,000, depending on the license type and scope. The approval process usually takes between 6 to 12 months, contingent on application completeness and compliance checks.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible to apply for licenses, provided they establish a local presence and meet all regulatory and financial requirements. The process includes demonstrating technical capability and financial stability, with restrictions on ownership structures that comply with local laws.

5. What are the tax obligations for iGaming operators?

Operators are subject to a GGR tax of 25% for casino games and 20% for sports betting. Additionally, corporate income tax at 25% applies, along with license renewal fees, typically about €100,000–€250,000 annually. These taxes influence overall profitability and strategic planning.

6. Are gambling winnings taxed for players?

Gambling winnings are subject to withholding taxes at 20% for non-residents if above certain thresholds. Players must declare winnings for personal income tax purposes, and in some cases, pay additional tax depending on total annual earnings.

7. What are the typical operational costs for running an online casino/sportsbook?

Major costs include licensing fees, platform licensing, technical development, customer support, marketing, and compliance. Setup investment ranges between €200,000 and €500,000, with ongoing monthly expenses varying based on scale and activity volume.

8. What is the expected ROI timeline for entering this market?

Most operators expect breakeven within 18–24 months, with ROI realization typically occurring around the 2-3 year mark. Strategies focusing on local partnerships and customer acquisition accelerate revenue growth, mitigating initial costs.

9. What are the local presence requirements for operators?

Operators must establish a physical office within Spain, register locally, and employ authorized personnel. Establishing a local bank account and domain registration within Spain are mandatory to support license conditions and customer trust.

10. What payment methods are available and recommended?

Popular options include credit/debit cards, e-wallets such as PayPal, Skrill, Neteller, bank transfers, and cash vouchers. Integrating multiple channels enhances customer convenience and engagement, with a focus on secure, fast processing methods.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors or vulnerable groups and cannot promote responsible gaming irresponsibly. Content restrictions on promotional materials, sponsorships, and platform advertising ensure compliance with national standards and protect consumer interests.

12. What responsible gambling measures are mandatory?

Mandatory measures include age verification, deposit limits, self-exclusion programs, responsible gaming tools, and public information dissemination. Operators are also required to fund social responsibility campaigns and regularly audit compliance.

13. How large is the iGaming market and what is the growth potential?

With a revenue of approximately €1.6 billion in 2024, Spain’s iGaming market continues to expand at roughly 8% annually. Increasing digital penetration and consumer engagement support a projection of over €2.1 billion by 2028, with significant growth potential driven by technological advancements and regulation.

14. Who are the main competitors and what is their market share?

Major players include Sportium, Bet365, 888, William Hill, and Bwin. These firms possess established brands, extensive customer bases, and comprehensive local licenses, with market shares varying between 10-20%. New entrants face stiff competition but benefit from licensing transparency and a growing customer base.

15. What are the player preferences and typical spending patterns?

Players favor sports betting, especially during major tournaments, followed by online casino games and poker. Session durations average 30 minutes, with high engagement during live events. Average monthly spend is around €200, heavily influenced by mobile device access and targeted marketing campaigns.

16. What are the key success factors and main challenges for new entrants?

Success hinges on local licensing compliance, effective marketing, and innovative platform features. Challenges include navigating high taxation, complex regulation, cultural differences, and fierce competition. Building trust and delivering responsible gaming services are critical for sustainability.

Exit Strategy Planning

Market liquidity, regulatory flexibility for license transfers, and ownership regulations provide strategic exit options. Valuations are often based on EBITDA multiples, with potential for sale or merger once a strong market presence is established, offering liquidity and growth opportunities.

SOURCES AND REFERENCES

- SpainGambling Regulatory Authority – Official Website

- National Statistical Office – Population and Economic Data 2024

- Central Bank of Spain – Financial Statistics and Reports

- Ministry of Finance – Tax Regulations and Guidelines

- World Bank – Doing Business Report 2024

- International Telecommunication Union – ICT Statistics

- Gaming Industry Report – [Publisher Name] – 2024

- European Telecommunications Network Reports

- Spanish Digital Infrastructure Agency Reports

- International Monetary Fund – Economic Outlook 2024

- European Union Digital Strategy Updates

- Major Industry Analyses by MarketResearch.com

- Spanish Ministry of Industry and Digital Development

- European Gaming and Betting Association Reports

- Spanish National Gambling Habit Surveys

- Global Payment Processing Industry Reports

- Major Telecom Operators Press Releases

- Spain’s e-commerce growth studies

- International Tax Treaties Database

- OECD Digital Economy Reports

- Spanish Financial Market Reports

- European Consumer Behavior Surveys

- Spanish Cultural Attitudes towards Gambling Studies

- Regulatory Changes and Legislative Updates 2023-2024

- Mobile Network Expansion Reports

- European Legal Environment for Online Gambling

🎯 Gambling Databases Country Rating: Spain

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.2/10 | 🟡 Moderate |

| Player Access Score | 8.5/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.8/10 | 🟡 Mature but Saturation & High Costs |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Severe Advertising Restrictions: Advertising is strictly regulated (often limited to 1:00 AM – 5:00 AM windows on broadcast), making customer acquisition extremely difficult for new brands.

- Mandatory Local Presence: Operators MUST establish a local office, hire local personnel, and host data locally/mirror servers, significantly increasing overhead.

- Player Taxation: Players are legally required to declare winnings on personal income tax, a significant friction point that drives high-value VIPs to offshore markets.

- High Fixed Operational Costs: Beyond the 20-25% GGR tax, operators face annual license renewal fees up to €250,000, creating a high breakeven point.

- Strict Enforcement & Fines: The DGOJ is an active regulator; violations of responsible gaming tools or advertising rules result in severe financial penalties and potential license revocation.

- Saturated Market: With over 50 licensed operators including major global brands, market share is calcified; entry without a massive marketing budget is financial suicide.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality (Sports, Casino, Poker all legal +3.0). Deduction for strict enforcement environment (-0.5). While legal, the regulatory burden is heavy. |

| Licensing Process | 25% | 1.0/2.5 | Licensing available but slow (6-12 months +1.0). Costs are moderate to high (€150k-€250k initial +0.25). Deductions for complex technical audits and strict probity checks (-0.25). |

| Taxation & Costs | 20% | 0.7/2.0 | GGR Tax is 20-25% (+1.5). HOWEVER, significant deductions: Corporate tax (25%) applies on top (-0.5). High annual renewal fees (€100k-€250k) act as a fixed tax (-0.3). Total effective tax burden is high. |

| Operational Requirements | 15% | 0.5/1.5 | Heavy requirements (+0.5). Deduction for mandatory local office and local personnel (-0.5). Deduction for strict technical reporting and localized domain requirements (-0.5). This is not a “remote” license. |

| Market Environment | 10% | 0.5/1.0 | Stable political environment (+0.7). severe deduction for Advertising Restrictions (-0.5) which cripples new entrant growth. Deduction for high market saturation (-0.2). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Fully legal and regulated (+4.0). Deduction because players are fiscally liable for winnings, creating a legal burden (-0.5). |

| Practical Accessibility | 30% | 2.5/3.0 | Excellent payment options including local methods like Bizum (+3.0). Deduction for strict KYC/Verification protocols that can delay onboarding (-0.5). Crypto is not mainstream/regulated (-0.0). |

| Player Penalties | 20% | 1.5/2.0 | No criminal penalties for playing (+2.0). Deduction for the financial penalty of taxation on winnings (-0.5). |

| Market Availability | 10% | 1.0/1.0 | 50+ licensed operators available (+1.0). High competition benefits the player. |

🔍 Key Highlights

Strengths (For Established Brands Only)

- Clear Regulatory Framework: Unlike “grey” markets, the rules are written and legally binding. No ambiguity regarding product legality.

- High Player Value: ARPU is strong at €200/month with a culturally ingrained gambling habit.

- Digital Infrastructure: 92% internet penetration and widespread mobile usage (89%) facilitate high engagement.

⛔️ CRITICAL RISKS AND CHALLENGES

- Marketing Straitjacket: Strict restrictions on advertising times (1am-5am) and content inhibit brand building. New entrants cannot buy their way to visibility easily.

- Taxation on Winnings: Unlike the UK where winnings are tax-free, Spanish players are taxed. This incentivizes high-volume/VIP players to seek offshore alternatives or relocate, reducing the LTV of top-tier players for licensed operators.

- High Burn Rate: Between local staff salaries (mandatory), office rent, €100k+ annual fees, and 25% GGR tax, the monthly burn rate is exceptionally high.

- Technical Complexity: The DGOJ requires real-time monitoring and “Vault” systems for data recording, requiring expensive technical integration and maintenance.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €400,000 – €600,000 (License fees + Legal + Setup + First Year Office/Staff)

Monthly Operating Costs: €100,000+ (Minimum for staff, office, compliance, and tech – excluding marketing)

Effective Tax Rate on Revenue: ~45-50% (Combined impact of GGR Tax, Corporate Tax, and fixed annual fees)

Customer Acquisition Cost: High (>€250) due to advertising restrictions limiting inventory supply.

Time to Breakeven: 24 – 36 months

Profitability Assessment: DIFFICULT. The Spanish market is a “Graveyard for Startups.” The combination of high fixed costs, taxes on GGR and profit, and the inability to aggressively advertise makes it nearly impossible for small operators to survive. This market is viable ONLY for large, capitalized operators who can sustain losses for 3 years to build a database.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | DGOJ actively issues blocking orders. Financial blocking is effective. Brand reputation damage is high. |

| Licensed Operators | Medium | Compliance risk is the main threat. Fines for responsible gambling failures or advertising breaches are common and expensive. |

| Affiliates/Advertisers | Medium | Must adhere strictly to advertising decrees. Promoting unlicensed brands can lead to domain blocking and fines. |

| Company Directors | Low | Generally low personal risk if operating legally, but strictly liable for AML failures. |

🚨 Extradition and International Enforcement

Extradition Treaties: Spain is an EU member and has active extradition treaties with the USA, UK, Canada, Australia, and most South American nations.

Enforcement History: Spain actively cooperates with INTERPOL and Europol regarding financial crimes and money laundering. While they rarely extradite solely for “offshore gambling,” any connection to money laundering triggers aggressive enforcement.

Safe Jurisdictions: None within Europe. Travel within the EU is risky for directors of black market operations targeting Spain.

📋 Final Verdict

Spain receives an Operator Ease Score of 5.2/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 6.8/10.

HONEST ASSESSMENT: Spain is a “Pay-to-Play” market reserved for the industry elite. While legally stable and fully regulated, the barrier to entry is financial and operational, not legal. The requirement for local infrastructure, combined with suffocating advertising restrictions and player taxation, wrecks the margins for small-to-mid-sized operators. If you do not have €5M+ in funding and a 3-year runway, do not enter this market. You will likely bleed out before achieving liquidity.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Tier-1 publicly traded operator expanding your regulated footprint.

- Able to acquire a local database via M&A rather than organic growth.

- Willing to accept single-digit margins in exchange for regulatory stability.

❌ Definitely Avoid If You Are:

- A startup or white-label operator with limited budget (<€2M).

- Relying on aggressive bonus marketing or affiliate streamers (heavily restricted).

- Looking for a “remote” license (local office/staff is mandatory).

- Targeting VIPs exclusively (tax on winnings drives them offshore).

⚠️ BOTTOM LINE: Spain is fully open for business, but the “entry fee” is exorbitant and the regulatory handcuffs are tight. It is a market for preservation of wealth, not creation of quick wealth.

Spain’s iGaming market growth is concerning from a youth gambling prevention perspective. What measures are in place to prevent minors from accessing online betting and casino services?

Regarding youth gambling prevention, Spanish regulators have implemented strict age verification systems and operator requirements to protect minors. For example, operators must use verified identity documents and implement robust KYC processes to ensure only adults can access their services.

That’s helpful, thanks. Can you elaborate on the KYC processes and how they’re enforced?

KYC processes in Spain typically involve verifying identity documents, such as passports or national ID cards, and ensuring the customer’s information matches the documentation provided. Regulators conduct regular audits to ensure operators are complying with these requirements.

The 25% tax rate on GGR for casino games seems steep. How does this compare to other European jurisdictions, and what impact does it have on operator profitability?

The 25% tax rate on GGR for casino games in Spain is indeed one of the higher rates in Europe. For comparison, the UK has a 21% tax rate on GGR for online casino games, while Germany has a 5.3% tax rate on GGR for online slots. This can significantly impact operator profitability, particularly for smaller operators or those with thinner margins.

I see. So, how do operators adapt to these different tax rates across jurisdictions?

Operators often adjust their pricing and revenue models to account for differing tax rates. This might involve offering different promotions or bonuses in higher-tax jurisdictions to remain competitive.

The Ley 13/2011 governing online gambling in Spain is quite comprehensive. Are there any plans for regulatory updates or reforms, and how might these impact the industry?

There are ongoing discussions about potential regulatory updates in Spain, particularly regarding advertising and consumer protection. The Spanish regulator, DGOJ, has been actively engaged with industry stakeholders and consumer groups to explore potential reforms and ensure the regulatory framework remains effective and balanced.

The article mentions over 50 licensed operators in Spain. Can anyone provide insight into the market share distribution among these operators, and are there any notable newcomers or exiting players?

I’m intrigued by the average licensing cost of €150,000 – €250,000. What’s the process like for obtaining a license, and are there any specific requirements or hurdles for new operators?