The United Kingdom represents one of the most mature and lucrative markets for iGaming globally. It combines a strong regulatory framework with robust consumer protection measures, offering a balanced environment for operators. The UK’s comprehensive licensing system, high internet penetration, and advanced technological infrastructure create significant opportunities for online gambling ventures.

Regulated by the UK Gambling Commission (UKGC), the market is notable for its extensive oversight and progressive reforms to limit gambling harm. Operators must navigate stringent licensing, compliance, and taxation regimes, but benefit from access to a large and engaged player base.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling legal status | Fully legal, regulated by UK Gambling Commission |

| Regulatory authority | UK Gambling Commission (UKGC) |

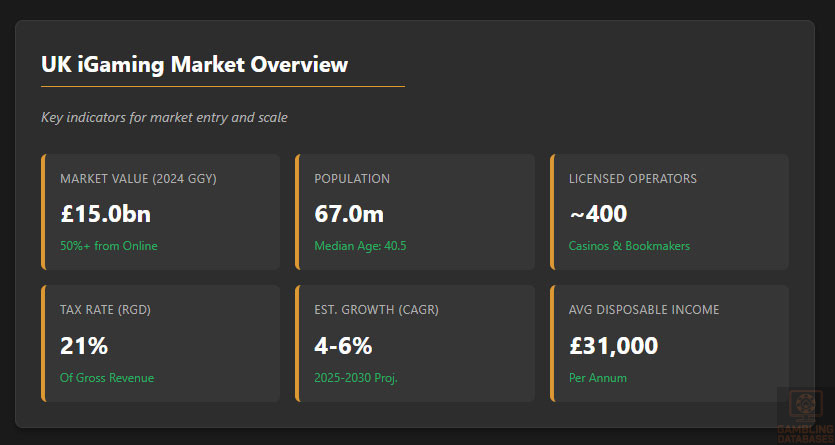

| Population (2025) | 67 million |

| Median age | 40.5 years |

| Gross Domestic Product (GDP) | ~£3.4 trillion (nominal) |

| Average disposable income | ~£31,000 per annum |

| Internet penetration rate | 95%+ |

| Mobile internet penetration | 90%+ |

| Number of licensed online gambling operators | ~200 casinos, 200 bookmakers |

| License application fee | £2,500 to £40,000+ depending on license type |

| License duration | Typically 5 years with renewal options |

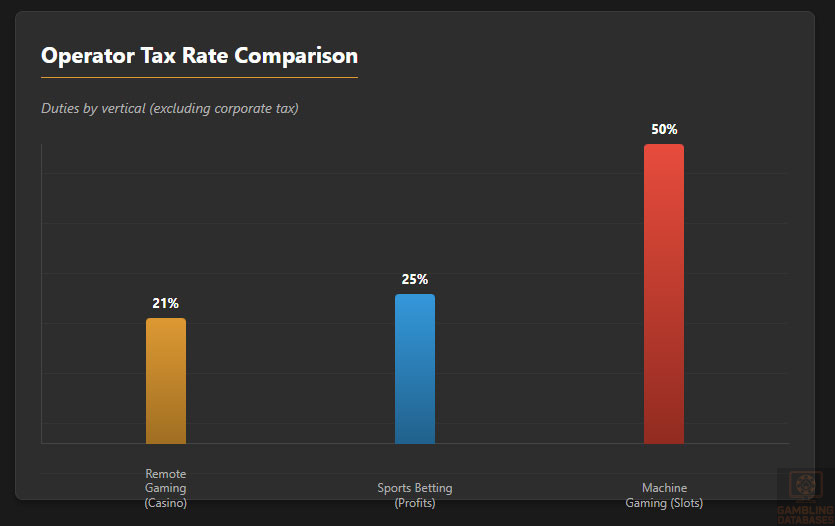

| Gross Gambling Revenue (GGR) tax rate | 21% Remote Gaming Duty |

| General Betting Duty | 25% on gross profits from sports betting |

| Statutory gambling levy on operators | Percentage of GGR; effective October 2025 |

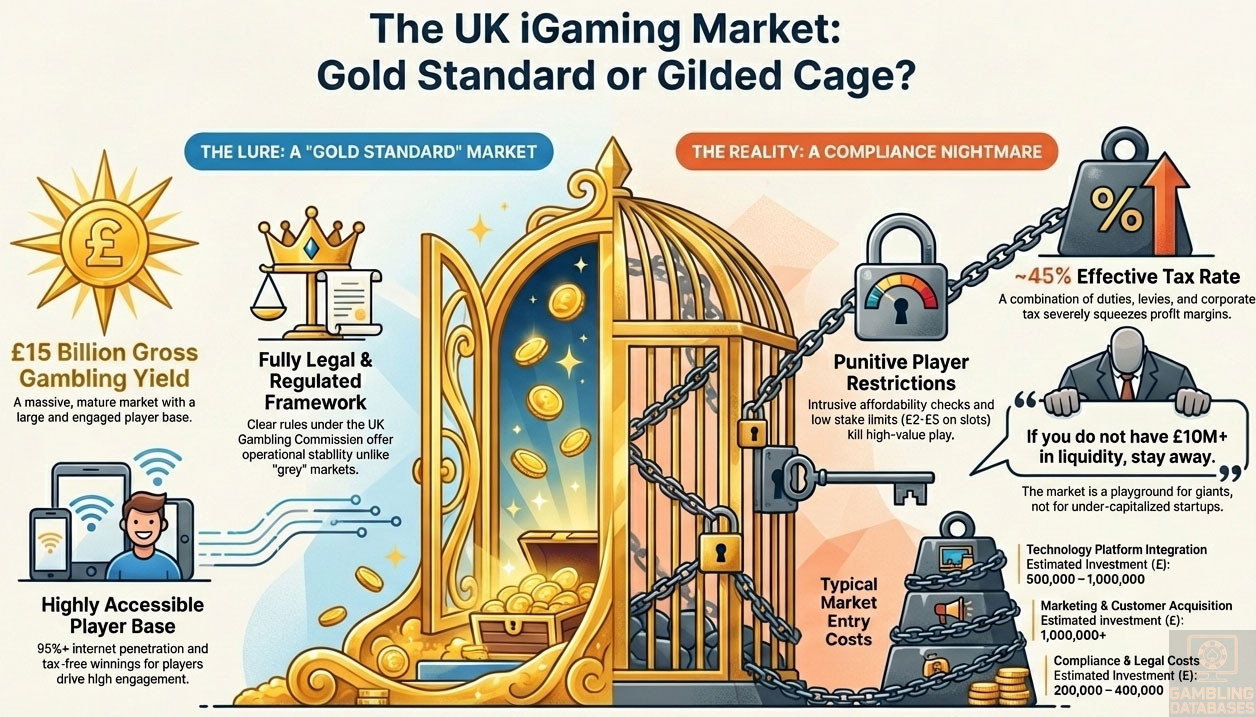

| Market size (2024 Gross Gambling Yield) | £15 billion total, with 50%+ online |

| Market growth rate (CAGR) | 4-6% projected 2025-2030 |

| Average Revenue Per User (ARPU) | ~£550 per annum |

| Entry barriers | High due to strict licensing, AML/KYC compliance, financial checks |

| Average licensing timeline | Approximately 16 weeks |

| Responsible gambling measures | Mandated age verification, deposit limits, self-exclusion, affordability checks |

| Advertising restrictions | Strict marketing rules, opt-in promotions only, restricted messaging times |

| Financial reporting frequency | Monthly submission of detailed financial and compliance reports |

| Technical standards | High standards including RNG certification and software audits |

| Local presence requirements | No mandatory physical presence, but operational transparency required |

| Anti-Money Laundering (AML) standards | Stringent, with continuous risk assessments and enhanced due diligence |

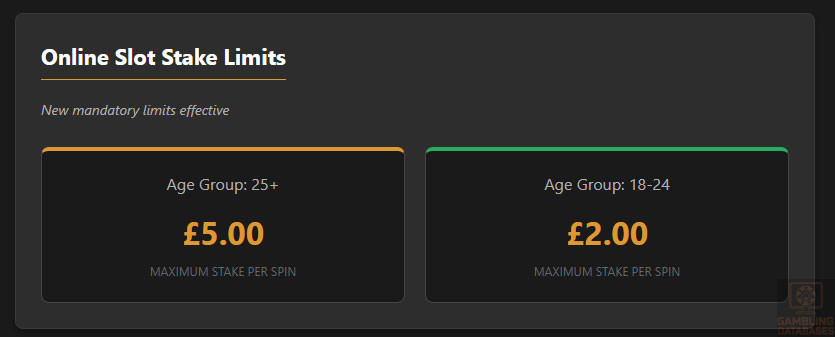

| Player stake limit on slots | £5 maximum for 25+, £2 for 18-24 age group |

| Self-exclusion system | National Online Self-Exclusion Scheme (GAMSTOP) mandatory |

| Enforcement penalties | Fines, license revocation, criminal prosecution |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

The United Kingdom’s gambling sector is fully legal and tightly regulated under the Gambling Act 2005, enforced by the UK Gambling Commission. This applies to land-based and online activities across all gambling formats, including sports betting, casinos, poker, and lotteries.

Regulatory oversight ensures operations are conducted fairly and transparently, with comprehensive measures to protect consumer interests and minimize gambling-related harm. The UK regime is widely regarded as a global benchmark for robust gaming regulation with proactive enforcement.

Land-Based Gambling Activities

Land-based gambling in the UK encompasses multiple categories such as traditional casinos, betting shops, bingo halls, arcades, and slot machine venues. Licensed operators must comply with stringent safety, security, and social responsibility standards.

Slot machine halls and adult gaming centers offer electronic gaming devices under regulated stake and prize limits, coupled with mandatory responsible gambling policies enforced on-site.

Online Gambling Framework

Since the introduction of remote gambling regulation in 2014, the UK has developed a comprehensive framework for digital gambling activities. The UK Gambling Commission licenses and monitors operators providing services to UK residents, regardless of the operator’s physical location.

This framework prohibits certain high-risk products including use of autoplay, fast spins, and other features deemed harmful, with recent 2025 reforms introducing stake limits on online slots (£5 for players 25 and older, £2 for younger adults) to address gambling harms.

Operators must implement stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols, alongside affordability and financial risk assessments to prevent problem gambling and illegal activities. Regulatory scope covers sportsbook, casino, poker, bingo, lotteries, and ancillary services.

Licensed Operators and Market Players

The UK iGaming market is highly competitive, with over 200 licensed online casinos and a similar number of bookmakers legally operating under UK Gambling Commission licenses. Market players range from major global brands to specialized local operators.

Market share is fragmented due to regulatory demands and consumer choice diversity. Leading operators leverage brand recognition and innovation while adhering to compliance-heavy requirements that include financial scrutiny, responsible gambling tools, and marketing restrictions.

- Bet365

- William Hill

- Ladbrokes Coral Group

- GVC Holdings (Entain)

- 888 Holdings

- Paddy Power

- Betfair

- Sky Betting & Gaming

- Kindred Group

Entry strategies often focus on compliance excellence, partnership with software providers meeting UK standards, and investments in player protection technologies.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing in the UK is administered solely by the UK Gambling Commission, which categorizes licenses into remote, non-remote, and ancillary types depending on the operator’s business model.

The application process involves thorough due diligence, including financial viability assessments, business plans, technical certifications (such as RNG testing), and detailed background checks on directors and beneficial owners.

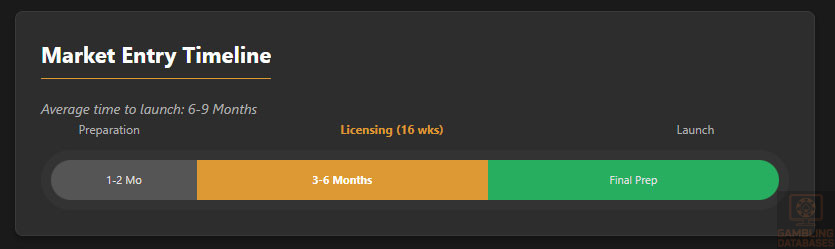

Applicants face tiered application fees generally starting from £2,500 up to £40,000 or more, reflecting the scope and risk profile of the license requested. The typical licensing timeline averages 16 weeks, influenced by the complexity of documentation and regulatory scrutiny levels.

- Submission of business registration and incorporation documents

- Financial statements for last three years audited by recognized firms

- Detailed business plan outlining market approach

- Technical documentation and certification of gaming software

- Criminal record checks and identity verification for all key personnel

- Proof of compliance systems including AML and responsible gambling policies

- Declaration of financial reserves and capital adequacy

- Operational policies for customer service and dispute resolution

Local Presence and Operational Requirements

While there is no absolute physical presence mandate, operators must demonstrate operational transparency and capability to comply with UK regulations. This includes maintaining registered UK addresses for correspondence and record-keeping.

Domain registration must reflect legal ownership and licensing status, and operators need to appoint UK-based responsible persons for compliance management. Partnership with local payment providers is common to facilitate fast transactions and AML controls.

Foreign ownership is permitted without restriction, provided full disclosure of ultimate beneficial ownership is included in licensing applications. Operational responsibilities remain with license holders to enforce all compliance rules effectively.

- Registered UK address for legal and compliance matters

- Local contacts responsible for regulatory communication

- Deployment of UK-specific customer support services

- Regular staff training in responsible gambling and AML policies

- Systems to ensure domain ownership and branding compliance

Compliance Obligations and Monitoring

Player Protection and Identification

Consumer protection is central to UK regulation, overseen through rigorous Know Your Customer (KYC) checks, age verification processes, and mandatory Anti-Money Laundering (AML) controls. Operators must detect and deter underage gambling with high reliability technologies.

Financial affordability checks were enhanced in 2025, with operators required to monitor and intervene when net player losses exceed regulated thresholds (£500 initially, reducing to £150 monthly). Self-exclusion systems like GAMSTOP are mandatory for all licensed entities, allowing players to block access across operators.

- Robust age verification aligned with government standards

- Comprehensive KYC including identity and source of funds verification

- Dynamic affordability and financial risk monitoring

- Mandatory self-exclusion scheme participation (GAMSTOP)

- Regular reporting of suspicious behaviors related to AML

- Deposit and stake limits tailored by age and financial profile

Financial Monitoring and Reporting

Operators are required to maintain transparent financial operations with monthly submission of financial returns, detailing gross gaming revenue, player transactions, and tax liabilities to the UKGC. This encompasses detailed audit trails for winnings, bets, and commissions.

Compliance includes maintaining records for a minimum of six years, internal controls to detect fraud, and adherence to prescribed accounting standards. Audits by the UKGC and independent bodies are routine to verify adherence to all regulatory financial requirements.

- Monthly financial returns submission to UKGC

- Independent annual audits of systems and revenue

- Continuous transaction monitoring and reporting of irregularities

- Preservation of financial records and player data for prescribed periods

- Implementation of risk assessments on financial flows and AML practices

Taxation Structure and Financial Obligations

Player Taxation

The UK does not impose direct taxes on player winnings. All gambling taxes are levied at the operator level, making gambling winnings tax-free for players. This policy enhances player appeal and simplifies the customer experience.

Operator Taxation

| Tax Type | Rate |

|---|---|

| Remote Gaming Duty (online casino, poker, bingo) | 21% on Gross Gambling Revenue |

| General Betting Duty (sports betting, spread betting) | 25% on gross profits |

| Machine Gaming Duty (slot machines, fruit machines) | 50% on profits (increased from 20%) |

| Gambling Operator Levy | Statutory levy from October 2025, percentage of GGR |

Additionally, operators pay corporate income tax on profits calculated after gambling taxes. License renewal fees apply biennially, with amounts determined by the size and scope of operations. The 2025 statutory gambling levy replaces the previous voluntary funding model for gambling harm prevention.

Gambling Market Financial Performance

The UK market generated over £15 billion in gross gambling yield in 2024, with remote gambling accounting for more than half. Year-over-year growth rates are steady at approximately 4-6% CAGR, driven by digital transition and product innovation.

Tax revenues from gambling have risen notably due to recent increases in duty rates and the introduction of mandatory levies, supporting government programs in gambling harm research and treatment.

Advertising and Marketing Restrictions

Advertising in the UK gambling market is tightly regulated to protect vulnerable consumers. Marketing is allowed only on opt-in channels with stringent content restrictions to avoid misleading claims or targeting underage and problem gamblers.

- Prohibition of promotions targeting minors

- Restrictions on use of celebrities and incentivized advertising

- Bans on misleading odds or exaggerated winning claims

- Mandatory inclusion of responsible gambling messages

- Time and channel restrictions for gambling adverts

Sponsorship by gambling operators is permitted but must not breach content codes, and promotional offers must be clear, fair, and not cumulative to avoid player confusion.

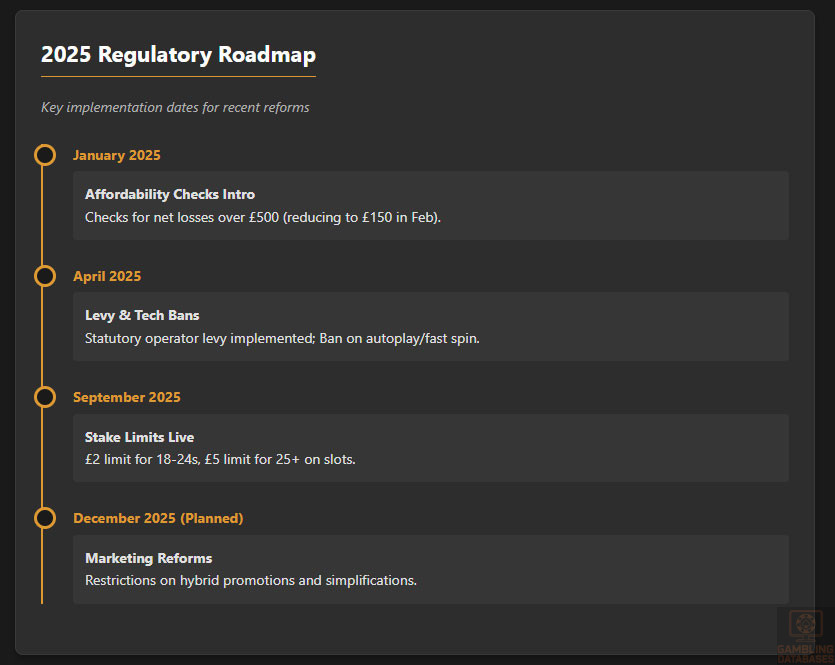

Recent Regulatory Changes and Their Impact

- January 2025: Introduction of financial affordability checks for players with net losses over £500 (to reduce to £150 in February)

- April 2025: Implementation of statutory gambling levy on operators

- April 2025: Ban on autoplay, turbo, and fast spin features on online slots

- September 2025: Stake limits introduced on online slot machines (£5 for 25+, £2 for 18-24 year olds)

- December 2025 (planned): Restrictions on hybrid promotions and marketing simplification

These reforms have increased operator compliance costs but aim to balance market growth with consumer protection and social responsibility.

Enforcement Mechanisms and Penalties

The UK Gambling Commission employs a tiered enforcement system ranging from warnings and fines to suspension or revocation of licenses for serious breaches. Criminal prosecution may be pursued for fraudulent or unlawful activity.

- Financial penalties commensurate with violation severity

- Public naming and shaming of non-compliant operators

- License suspension or revocation for repeated or serious breaches

- Mandatory remediation plans and compliance audits

- Criminal charges for illegal operations or money laundering offenses

Compliance trends emphasize preventive measures, with increasing regulatory scrutiny on AML and responsible gambling adherence.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

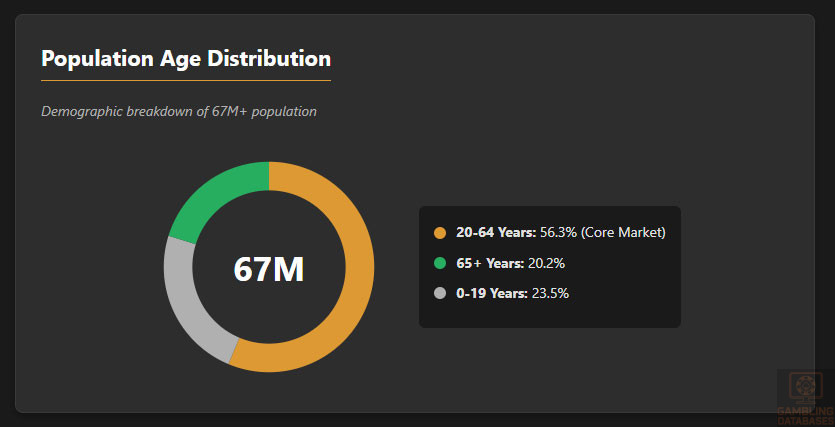

The United Kingdom’s population reached approximately 69 million in 2025, with a steady growth rate of 0.5% annually. The median age is about 41.7 years, reflecting an aging population trend, consistent over the past decade. Gender distribution is balanced, with roughly 981 men per 1,000 women.

Age groups are distributed as follows: nearly 23.5% are under 20 years old, about 56.3% fall between 20 and 64, and the elderly population aged 65 and above comprises around 20.2%. Urban residents make up roughly 85% of the total population, concentrated mostly in England’s major cities and regional hubs.

| Age Group | Percentage of Total Population |

|---|---|

| 0-19 years | 23.5% |

| 20-64 years | 56.3% |

| 65 years and older | 20.2% |

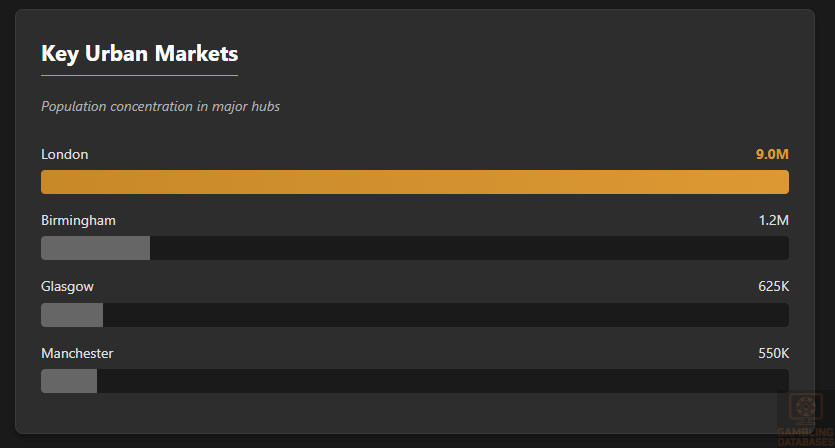

Geographically, the UK displays economic and demographic variations across regions. London remains the largest urban center with approximately 9 million residents, serving as the financial and cultural hub.

Major regional cities harbor significant populations and economic activity, reflecting diverse market dynamics.

- London – 9.0 million

- Birmingham – 1.2 million

- Glasgow – 625,000

- Manchester – 550,000

- Leeds – 510,000

- Liverpool – 500,000

- Sheffield – 580,000

- Edinburgh – 530,000

These urban areas also coincide with concentrated internet access and gambling venue availability, supporting significant market penetration in both land-based and online iGaming sectors.

Economic Indicators and Consumer Spending Power

The UK’s nominal Gross Domestic Product (GDP) approaches £3.4 trillion in 2025, with moderate annual growth forecasted at around 1.5% amid global uncertainties. The economy is primarily service-driven, constituting over 75% of GDP, with finance, information technology, and creative industries as main contributors.

Average household disposable income is approximately £36,700 per annum, but income distribution exhibits notable inequality. The median income is close to this average, while the top 10% of earners make nearly double the median, emphasizing a segmented consumer base with varying spending power and digital access.

Consumer spending remains strong, with a significant portion allocated to entertainment, digital services, and leisure activities including gambling. Market projections indicate continued growth in disposable income, fueling steady expansion in online gaming revenues.

| Metric | Value |

|---|---|

| GDP (nominal) | £3.4 trillion |

| GDP growth forecast | 1.5% annually |

| Average household disposable income | £36,700 per annum |

| Income inequality (top 10% vs median) | Approximately 2x higher |

| Service sector contribution | >75% of GDP |

Market Size and Growth Projections

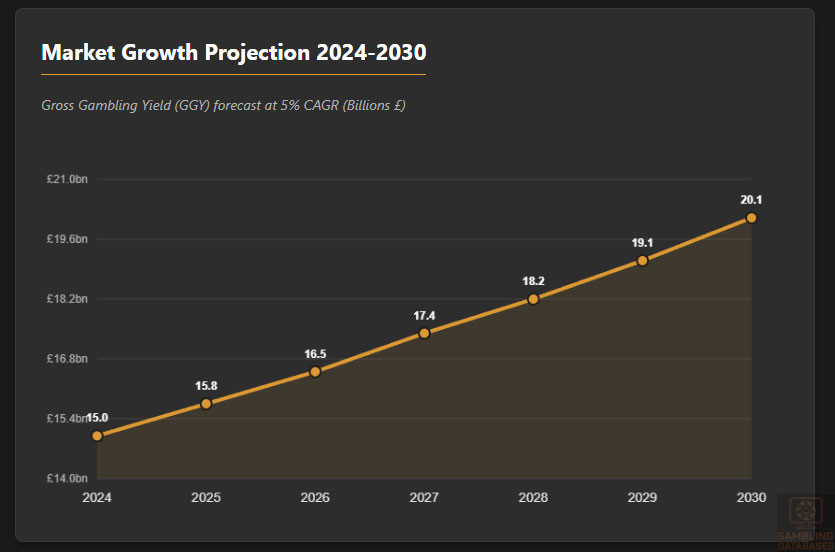

The UK iGaming market’s gross gambling yield stood around £15 billion in 2024, with over half derived from online platforms. Market forecasts estimate a compound annual growth rate (CAGR) between 4% and 6% from 2025 through 2030, driven by innovation, digital adoption, and regulatory evolution.

Average Revenue Per User (ARPU) is estimated at approximately £550 annually, reflective of diversified product preferences and high player engagement. Total active online gambling participants constitute about 17% of adults, highlighting room for growth among broader demographics.

| Metric | Value |

|---|---|

| Gross Gambling Yield (2024) | £15 billion |

| Percentage online | 50%+ |

| Market CAGR (2025-2030) | 4-6% |

| ARPU | £550 per annum |

| Online active players | 17% of adults |

Education, Skills, and Digital Literacy

The UK exhibits a highly educated and digitally literate population, with over 90% literacy and significant tertiary education attainment in urban centers. Workforce skills align with advanced digital technology use, supporting sophisticated online entertainment consumption.

High rates of digital literacy underpin strong adoption of online payment methods, gambling platforms, and engagement with emerging technologies such as AI-driven personalization and live dealer games. Educational attainment correlates positively with online gambling participation and comfort with digital financial tools.

Cultural and Social Factors

Communication and Language

English is the primary language, dominating online content and communication. A diverse population also includes significant communities speaking Polish, Punjabi, Urdu, Bengali, and Welsh, reflecting immigration and regional linguistic heritage.

- English

- Polish

- Punjabi

- Urdu

- Bengali

- Welsh

Cultural Attitudes

Gambling is broadly accepted socially as an entertainment pastime, with the UK having a well-established gambling culture historically. Religious groups influence attitudes differently, but secular trends favor openness to regulated gambling.

Foreign gambling brands generally enjoy positive consumer perception when compliant with UK regulations. Entertainment preferences skew toward sports betting, online slots, and interactive casino formats, particularly among younger demographics.

Problem Gambling and Social Considerations

Problem gambling affects an estimated 0.5% to 1% of the adult population, prompting extensive government intervention. Vulnerable groups include young adults and economically disadvantaged sectors. Nationwide support programs and awareness campaigns aim to mitigate risks.

- GAMSTOP self-exclusion scheme

- National Gambling Treatment Service

- Local authority support initiatives

- Mandatory operator funding for research

- Public awareness and education campaigns

Social responsibility is embedded in licensing conditions, requiring operators to contribute financially to harm prevention and enforce proactive consumer protection measures.

Political Structure and Governance

The UK operates as a constitutional monarchy with a parliamentary democracy. Political stability and consistent regulatory frameworks promote a predictable business environment. The government maintains active international relations and aligns gambling regulations with broader EU standards where applicable post-Brexit.

Technology Adoption and Digital Behavior

Internet and Digital Usage

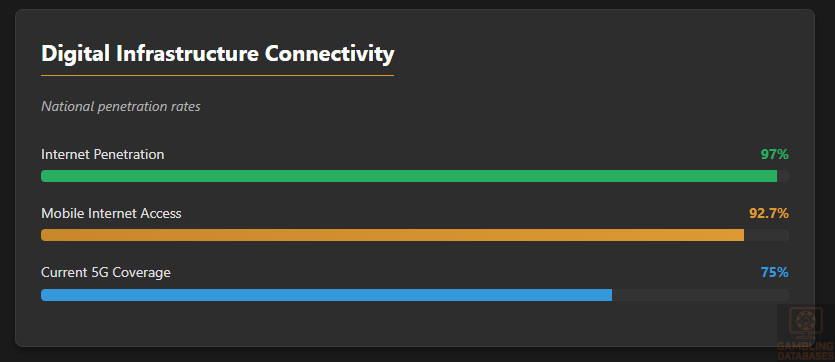

Internet penetration rates exceed 97% nationally, with 92.7% accessing web services via mobile devices. Average daily internet usage approximates 5 hours and 36 minutes, with a slight annual decrease in total usage time but growing emphasis on social media and streaming platforms.

- WhatsApp – 79% monthly active users

- Facebook – 73% penetration

- Instagram – 60% monthly reach

- YouTube – 59.7% penetration

- TikTok – rapidly growing, especially among younger users

- Reddit – emerging distinct niche

- LinkedIn – professional networking growth

Digital Payment Behavior

Digital payment solutions dominate e-commerce and online gambling transactions. Credit and debit cards remain predominant, supplemented by e-wallets, bank transfers, and increasingly accepted cryptocurrencies.

- Visa and Mastercard credit/debit cards

- PayPal e-wallet

- Skrill

- Neteller

- Apple Pay and Google Pay mobile wallets

- Cryptocurrency options gaining traction among tech-savvy players

Gaming and Gambling Preferences

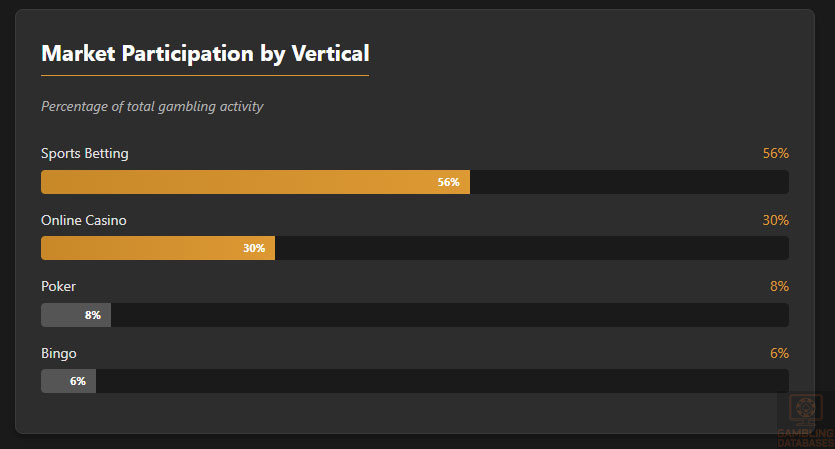

Current Market Participation

- Sports betting – 56% market share

- Online casino games – 30%

- Poker – 8%

- Bingo – 6%

Online slots have seen significant growth, representing one in seven players in the UK participating monthly. Esports betting is an emerging segment, attracting younger, digitally native consumers. Gamification features such as missions and reward levels increasingly drive player retention and engagement.

Consumer Behavior Patterns

UK consumers exhibit distinct gambling patterns characterized by moderate session lengths and high engagement during weekends and major sporting events. Platform loyalty is influenced by user experience, payment options, and responsible gambling features.

Spending is increasingly concentrated on mobile and live casino formats, with social and interactive elements influencing purchase and retention decisions. Retention rates vary by segment but have trended downward recently due to heightened regulatory controls and enhanced consumer protection.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

The United Kingdom’s population is approximately 69 million in 2025, exhibiting moderate growth of about 0.5% annually. The median age is near 41.7 years, reflecting an aging trend consistent with developed economies. Gender distribution is balanced, with about 981 men per 1,000 women.

Age demographics show that 23.5% of the population is under 20 years, 56.3% fall between 20 and 64 years, and the elderly population aged 65 and above constitutes 20.2%. Urban residents are dominant, making up approximately 85% of the total population, concentrated mainly in England’s key metropolitan centers.

| Age Group | Percentage of Population |

|---|---|

| 0-19 years | 23.5% |

| 20-64 years | 56.3% |

| 65 years and older | 20.2% |

Geographically, London leads with nearly 9 million people, followed by other major cities that serve as cultural and economic hubs. These urban centers are focal points for internet access and gambling activity due to their dense populations and infrastructure.

- London – 9.0 million

- Birmingham – 1.2 million

- Glasgow – 625,000

- Manchester – 550,000

- Leeds – 510,000

- Liverpool – 500,000

- Sheffield – 580,000

- Edinburgh – 530,000

Economic Indicators and Consumer Spending Power

The UK’s nominal GDP is close to £3.4 trillion in 2025, with steady growth estimated at 1.5% annually. The economy is predominantly service-oriented, contributing over 75% to GDP, driven by finance, IT, and creative sectors. Economic growth supports consumer spending and disposable income increases.

Average household disposable income is roughly £36,700 per year, though significant income inequality persists. The top 10% earn almost twice the median income, creating diverse consumer spending patterns relevant for iGaming operators targeting different segments.

| Indicator | Value |

|---|---|

| GDP (nominal) | £3.4 trillion |

| GDP Growth Rate | 1.5% annually |

| Average Household Disposable Income | £36,700 |

| Service Sector Contribution | 75%+ |

| Income Inequality | Top 10% earn twice median income |

Market Size and Growth Projections

The UK iGaming market’s gross gambling yield was approximately £15 billion in 2024, with online gambling accounting for over half of this figure. Market growth is forecasted at 4-6% CAGR through 2030 driven by technology, product innovation, and expanding user engagement.

Average Revenue Per User (ARPU) in online gambling is around £550 annually. Active online players constitute about 17% of adults, leaving scope for growth especially among younger demographics.

| Metric | Value |

|---|---|

| Gross Gambling Yield (2024) | £15 billion |

| Online Market Share | 50%+ |

| Forecast CAGR (2025–2030) | 4-6% |

| Average Revenue Per User (ARPU) | £550 |

| Active Online Players | 17% of adult population |

Education, Skills, and Digital Literacy

The UK has a highly educated and digitally savvy population, with literacy rates over 90% and strong tertiary education completion. This foundation supports widespread digital adoption, with many users comfortable engaging with advanced gambling technologies, mobile platforms, and digital payments.

Cultural and Social Factors

Communication and Language

English is the dominant language, underpinning all commercial and online gambling activity. Diverse communities add Polish, Punjabi, Urdu, Bengali, and Welsh as important languages, influencing regional marketing strategies.

- English

- Polish

- Punjabi

- Urdu

- Bengali

- Welsh

Cultural Attitudes

Gambling is widely accepted as mainstream entertainment in the UK, supported by long-standing cultural norms. Secular perspectives predominate, though religious groups impact localized attitudes. Foreign brands licensed in the UK enjoy strong consumer trust when compliant with regulation.

Problem Gambling and Social Considerations

Problem gambling prevalence ranges from 0.5% to 1% among adults, with focused interventions on high-risk groups such as young adults and economically vulnerable individuals. The government and regulators enforce multiple programs to support harm reduction and treatment.

- Self-exclusion through GAMSTOP

- National Gambling Treatment Service

- Local authority support initiatives

- Operator-funded research and preventive programs

- Public education and awareness campaigns

Political Structure and Governance

The UK is constitutional monarchy with parliamentary democracy, ensuring regulatory stability and political continuity. Regulatory frameworks are consistent, aligning partly with European standards post-Brexit, fostering a stable environment for iGaming operators.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration exceeds 97% nationally, with 92.7% of users online via mobile devices. Average daily internet usage is about 5 hours 36 minutes, featuring high engagement with video, social, and interactive content.

- WhatsApp – 79% monthly active users

- Facebook – 73% penetration

- Instagram – 60%

- YouTube – 59.7%

- TikTok – rapidly growing among Gen Z

- Reddit – increasing niche user base

- LinkedIn – professional networking growth

Digital Payment Behavior

Online payments are dominated by credit and debit cards, with rapid uptake of e-wallets and mobile payments. Cryptocurrency adoption is emerging but remains niche.

- Visa and Mastercard

- PayPal

- Skrill

- Neteller

- Apple Pay / Google Pay

- Cryptocurrency options (growing)

Gaming and Gambling Preferences

Current Market Participation

- Sports betting – 56% market share

- Online casino gaming – 30%

- Poker – 8%

- Bingo – 6%

Online slots have gained popularity, engaged by one in every seven UK players monthly. Esports betting is an emerging vertical, drawing younger audiences. Gamification elements like rewards and missions enhance engagement and loyalty.

Consumer Behavior Patterns

UK gamblers display moderate session durations, with peak activity around weekends and major events. Mobile and live casino formats dominate player preference. Recent regulation tightening has affected retention and spending patterns, pushing operators toward enhanced responsible gambling and user experience initiatives.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

The United Kingdom boasts one of the highest internet penetration rates globally, exceeding 97% of the population with reliable access. Broadband connectivity is widespread, with fiber-optic deployments covering over 90% of households, delivering average downstream speeds above 150 Mbps. Mobile broadband complements fixed infrastructure, with 4G serving nearly the entire population and 5G adoption expanding rapidly.

Network reliability is robust, supported by continuous investments in infrastructure by both public and private sectors. Latency and uptime metrics compare favorably with other leading digital economies, underpinning seamless streaming and interactive gaming experiences which are essential for iGaming platforms.

5G and Future Technology Deployment

5G rollout in the UK is advancing swiftly, with current coverage reaching approximately 75% of the population and urban centers prioritized. Major network operators have committed billions in investments to enhance both capacity and reach, targeting near-complete national coverage by 2027.

Beyond 5G, emerging technologies such as edge computing, AI-driven network optimization, and quantum encryption are under experimental phases, promising enhanced security and latency improvements that will benefit high-frequency gaming applications.

Mobile Technology Ecosystem

Mobile Network Infrastructure

The UK mobile market is highly competitive with multiple operators catering to consumer diversity. Coverage areas extensively support 4G with increasing 5G availability, while data costs remain among Europe’s most competitive, promoting heavy mobile device usage across demographics.

- EE – market leader with ~35% share, extensive 5G deployment

- Vodafone – ~27% share, strong urban and rural coverage

- O2 (Telefonica) – ~25% share, focus on business and consumer segments

- Three UK – ~13% share, aggressive pricing strategy

- Virtual Network Operators – emerging niche activity

Device Penetration

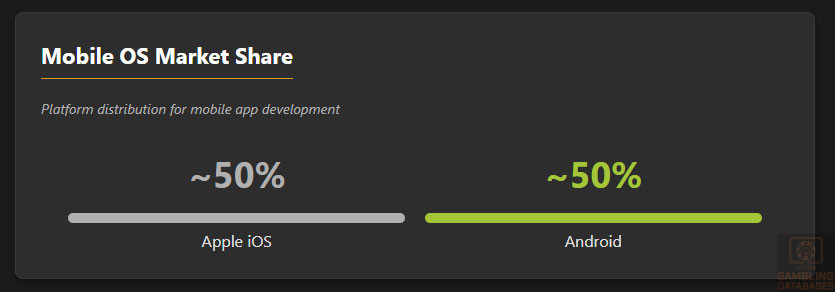

Smartphone adoption is near saturation at about 85% of the population. Apple iOS devices hold approximately 50% market share, with Android comprising the remainder, reflecting diverse device preferences. Mobile gaming, including iGaming, primarily occurs on smartphones, with tablets and connected devices capturing smaller proportions.

Users show high engagement with mobile apps, favoring fluid user experience and instant access favored by mobile-first iGaming operators.

Financial Services and Payment Infrastructure

Banking System Structure

The UK banking sector is deep and diversified, hosting several large multinational institutions alongside fintech disruptors. Digital banking adoption is widespread, with over 90% of adults holding at least one bank account with online banking capability.

- HSBC – one of the largest retail and corporate banks

- Barclays – extensive financial services provider

- Lloyds Banking Group – dominant in retail banking

- NatWest Group – strong SME banking portfolio

- Santander UK – major international bank presence

- Digital-only banks – Monzo, Revolut, Starling rapidly growing

Payment Processing Options

For iGaming operators, the UK payment ecosystem offers a variety of methods ensuring seamless transactions and compliance with financial regulations. Card usage remains paramount, complemented by e-wallets and emerging cryptocurrencies accepted by savvy operators.

- Debit and credit cards (Visa, Mastercard)

- E-wallets: PayPal, Skrill, Neteller

- Bank transfers and Faster Payments

- Mobile wallets: Apple Pay, Google Pay

- Cryptocurrency payments gaining niche adoption (Bitcoin, Ethereum)

E-commerce and Digital Economy

The UK’s e-commerce market is Europe’s largest, valued at over £220 billion annually with penetration reaching 34% of retail sales. Strong consumer trust, advanced logistics networks, and innovative digital marketing foster an environment conducive to online gambling growth.

Digital services have also become critical, with subscription models and streaming services expanding, driving consumer comfort with online payments and digital interactions, favorable to iGaming platform adoption and monetization strategies.

Business Environment and Regulatory Framework

Ease of Business Operations

The UK ranks consistently within the top 10 globally in the World Bank’s ease of doing business indexes, reflecting simplified procedures and transparent regulatory frameworks. Foreign investments are actively encouraged with minimal restrictions beyond standard compliance requirements.

Corporate Structure and Registration

Commonly, international operators establish limited companies or branches to enter the UK market. The recommended structure often is a private limited company (Ltd), offering limited liability and ease of management.

Registration timelines typically range from 7 to 14 business days, with procedures streamlined through digital portals ensuring swift incorporation. Foreign ownership is permitted without quotas but full disclosure of beneficial owners and compliance with regulatory obligations is mandatory.

- Memorandum and Articles of Association

- Proof of registered office address

- Details of directors and shareholders

- Tax registration documents

- Compliance policies including AML and GDPR adherence

Taxation Framework

Corporate income tax is standard at 19%, with no sector-specific relief aside from general economic zones. Numerous double taxation treaties reduce withholding taxes, encouraging foreign direct investment and cross-border business activity.

- United States

- Germany

- France

- Netherlands

- Japan

- Canada

- Australia

Personal income tax follows a progressive system peaking at 45%, supplemented by national insurance contributions. Tax residency is established based on physical presence and domicile tests.

Market Entry Considerations

Successful market entry favors partnerships with local operators, leveraging licensed software providers to meet UKGC technical standards. Embracing mobile-first platforms and embedding responsible gambling features early enhance regulatory acceptance and consumer trust.

- Partner with UK-licensed platform providers

- Establish transparent governance with UK presence for compliance

- Invest in responsible gambling technology and player protection

- Develop mobile-optimized user experiences

- Prepare for advertising compliance and marketing restrictions

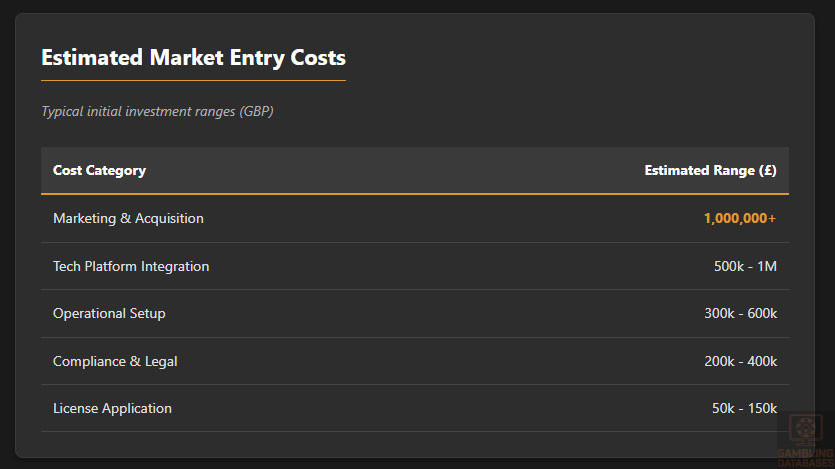

Initial setup costs can reach several million pounds including licensing, technology integration, marketing, and compliance.

Timelines for launch average 6 to 9 months depending on scaling and regulatory speed.

| Cost Category | Estimated Investment (£) |

|---|---|

| License application and fees | 50,000 – 150,000 |

| Technology platform integration | 500,000 – 1,000,000 |

| Marketing and customer acquisition | 1,000,000+ |

| Compliance and legal costs | 200,000 – 400,000 |

| Operational setup and staffing | 300,000 – 600,000 |

Exit strategies must consider regulatory restrictions on license transfer and valuation influenced by operational compliance history and market positioning. License revocation risk, competitive saturation, and changing regulatory landscapes factor into liquidity considerations.

FAQ: Frequently Asked Questions

1. Is online gambling legal in United Kingdom?

Yes, online gambling is fully legal in the UK, regulated by the UK Gambling Commission under the Gambling Act 2005. The licensing framework ensures that operators meet stringent regulatory, technical, and financial standards to protect players. Consumers benefit from regulated gameplay, responsible gambling measures, and dispute resolution mechanisms.

2. What types of gambling licenses are available and what do they cover?

The UK offers several license types, including:

- Remote gambling licenses covering online casinos, poker, bingo, and sports betting

- Non-remote licenses for land-based casinos and betting shops

- Pool betting licenses

- Ancillary licenses for suppliers and software providers

Each license type corresponds to specific operational scopes and compliance obligations tailored to business models.

3. How much does an iGaming license cost and how long does it take to obtain?

License fees range from £2,500 to £40,000 or more depending on the license scope. The full process averages about 16 weeks, involving detailed background checks, financial assessments, and technical reviews. Early preparation of documentation and compliance frameworks can accelerate approval.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible to apply for UK gambling licenses. They must provide full disclosure of beneficial ownership, meet UKGC’s financial and compliance standards, and demonstrate capability to operate within UK laws. No foreign ownership restrictions apply, but operational transparency is key.

5. What are the tax obligations for iGaming operators?

Operators pay a 21% Remote Gaming Duty on gross gambling revenues from online games. General Betting Duty applies at 25% on gross profits for sports betting. Additionally, a statutory gambling operator levy exists to fund harm prevention initiatives. Corporate income taxes apply on earnings after gambling taxes.

6. Are gambling winnings taxed for players?

No, players in the UK do not pay taxes on gambling winnings. The UK tax model places all gambling taxation responsibility on operators, allowing players to receive payouts without further tax obligations.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, platform and software development, customer acquisition, compliance staffing, and ongoing audits. Technology and marketing expenses often dominate, requiring upfront investments of over £1 million in many cases for mid-sized operators.

8. What is the expected ROI timeline for entering this market?

Return on investment timelines vary based on scale and strategy, with an average break-even horizon of 2 to 3 years post-launch. High marketing spend and regulatory compliance costs justify a conservative approach to expansion and customer retention.

9. What are the local presence requirements for operators?

While no mandatory physical office is required, licensees must establish a registered UK address and appoint responsible persons for regulatory communication. Operators need transparent governance and demonstrated capability to comply with UK regulations fully.

10. What payment methods are available and recommended?

Popular payment methods include credit/debit cards, PayPal, Skrill, Neteller, and mobile wallets such as Apple Pay and Google Pay. Increasingly, cryptocurrency options are accepted for niche audiences. High reliability and AML compliance are essential for choice of providers.

11. What are the advertising and marketing restrictions?

Advertising must comply with the UK Code of Broadcast Advertising and CAP Code, restrict targeting of minors, and avoid misleading claims. Promotional offers require transparency and limitation to prevent player exploitation. Time-of-day restrictions and opt-in requirements protect vulnerable consumers.

12. What responsible gambling measures are mandatory?

Operators must implement stringent age verification, deposit and stake limits, affordability checks, self-exclusion systems like GAMSTOP, and ongoing player protection monitoring. Regular reporting of compliance and consumer interaction is mandatory.

13. How large is the iGaming market and what is the growth potential?

The UK iGaming market was valued around £15 billion in 2024 with growth projected at 4-6% CAGR through 2030, bolstered by digital transformation, product innovation, and demographic engagement. Online market share exceeds 50%, with increasing penetration in underrepresented segments.

14. Who are the main competitors and what is their market share?

The market is fragmented with numerous operators; leading players like Bet365, William Hill, and Entain dominate significant portions but face competition from emerging digital-first brands and niche operators. Market share is dynamic and influenced by innovation and regulatory compliance.

15. What are the player preferences and typical spending patterns?

UK players favor sports betting, online slots, and poker, with preference for mobile and live dealer formats. Spending is often moderate but consistent, concentrated during weekends and major events, with gamers demanding seamless UX and responsible gambling guarantees.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, innovative technology integration, strong responsible gambling frameworks, and targeted marketing. Challenges include high setup costs, complex licensing processes, fierce competition, and evolving regulatory requirements demanding agility.

Sources and References

- United Kingdom Gambling Commission – Official website: https://www.gamblingcommission.gov.uk

- UK Government – Gambling Act 2005: https://www.legislation.gov.uk/ukpga/2005/19/contents

- UK Office for National Statistics – Population and Economic Data 2025: https://www.ons.gov.uk

- World Bank – Doing Business Report 2024: https://www.worldbank.org/en/programs/business-enabling-environment

- International Telecommunication Union – ICT Statistics 2025: https://www.itu.int/en/ITU-D/Statistics/Pages/stat/default.aspx

- Ofcom – UK Communications Market Report 2025: https://www.ofcom.org.uk/research-and-data

- UK National Health Service – Gambling Support Services: https://www.nhs.uk/live-well/healthy-body/gambling-problems/

- Financial Conduct Authority – UK Banking Sector Analysis 2025: https://www.fca.org.uk

- UK Department for Digital, Culture, Media and Sport (DCMS) – Gambling Regulation Updates: https://www.gov.uk/government/organisations/department-for-digital-culture-media-sport

- Digital 2025 Report – DataReportal: https://datareportal.com/reports/digital-2025-united-kingdom

- UK Treasury – Taxation of Remote Gambling: https://www.gov.uk/government/consultations/tax-treatment-of-remote-gambling

- Gaming Industry Reports – iGaming Business and EGR Intelligence 2024-2025

- BBC News – Coverage of UK Gambling Tax Proposals 2025

- Statista – UK Online Gambling Market Size 2025: https://www.statista.com/topics/3999/online-gambling-in-the-uk/

- Monzo Bank – UK Digital Banking Market 2025 Analysis

- Lloyds Banking Group – Annual Report 2024

- HSBC UK Market and Infrastructure Report – 2025

- PayPal UK – Digital Payment Trends 2025

- Mobile Network Operators UK – Market Share Data 2025

- GAMSTOP Official Website – National Self-Exclusion Scheme: https://www.gamstop.co.uk

- National Gambling Treatment Service – NHS England

- ICAEW – UK Population and Economic Analysis 2025

- Government Digital Service – UK Business Registration Portal

- UK Intellectual Property Office – Licensing and Regulatory Procedures

- Clifford Chance LLP – UK Gambling Regulation 2025 Overview

- Industry White Papers – Emerging UK iGaming Trends 2025

- Research Reports – UK Digital Consumer Behavior 2024-2025

- Social Media UK Audience Research 2025 – Birdeye Analytics

- Cryptocurrency Regulatory Reviews – UK Payment Systems 2025

- European Telecommunications Network Operators – UK 5G Coverage Maps 2025

🎯 Gambling Databases Country Rating: United Kingdom

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 5.1/10 | 🟡 Moderate |

| Player Access Score | 9.0/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 6.5/10 | High volume but brutally competitive with punishing compliance costs. |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Strict Financial Affordability Checks: New 2025 rules require intrusive checks for net losses over £150/month, causing massive friction and VIP player churn.

- Credit Card Ban: Despite some sources claiming availability, the UK banned credit cards for gambling in 2020. Do not expect to process credit card deposits.

- Punitive Stake Limits: Online slots are capped at £5 per spin (25+) and £2 per spin (18-24), severely limiting high-roller revenue potential.

- Statutory Levy: A mandatory levy on Gross Gambling Yield (effective Oct 2025) adds another layer of taxation on top of RGD and Corporate Tax.

- Market Saturation: With 200+ licensed casinos and bookmakers, Customer Acquisition Cost (CAC) is among the highest globally.

- Active Enforcement: The UKGC actively fines operators millions of pounds for AML/KYC failings. License revocation is a real threat.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Fully legal market for all products (+3.0). Deductions for strictly enforced compliance environment (-0.25) and active blocking/enforcement against non-compliant entities (-0.25). |

| Licensing Process | 25% | 1.5/2.5 | Licensing is accessible and structured (+2.0). Major deductions for high complexity and professional fees (-0.5). While application fees are £2.5k-£40k, the actual cost of compliance consultancy and preparation often exceeds £150k+. |

| Taxation & Costs | 20% | 0.5/2.0 | Remote Gaming Duty is 21% (+1.5). However, effective tax rate is punishing: 21% RGD + 19-25% Corporate Tax + Statutory Levy = ~45%+ effective burden (-0.5). High operational costs (compliance staff, reporting) and extreme CAC (-0.5) reduce score further. |

| Operational Requirements | 15% | 0.5/1.5 | Moderate requirements (+1.0). Severe deductions for Credit Card Ban (-0.25) and intrusive affordability checks (-0.25) which require complex technical integration and reduce player lifetime value. |

| Market Environment | 10% | 0.1/1.0 | Good business environment base (+0.7). Deductions for severe advertising restrictions (-0.5) and regulatory instability (frequent reforms like stake limits/levies) (-0.1). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal. Players can access all verticals (Sports, Casino, Poker, Bingo) without legal risk. |

| Practical Accessibility | 30% | 2.0/3.0 | Multiple payment methods available (+3.0). Deductions for Credit Card Ban (-0.5) and friction caused by mandatory affordability checks and KYC verification before play (-0.5). |

| Player Penalties | 20% | 2.0/2.0 | No penalties for players. Winnings are tax-free. |

| Market Availability | 10% | 1.0/1.0 | Market is flooded with 200+ licensed operators. Players have immense choice. |

🔍 Key Highlights

Strengths

- Market Scale: £15 billion GGY with high internet penetration (95%+) and a wealthy population.

- Legal Clarity: Unlike “grey” markets, the rules are written down. If you follow them, you are safe from closure (though not from fines).

- Tax-Free Winnings: Players are not taxed on winnings, which encourages high turnover.

⛔️ CRITICAL RISKS AND CHALLENGES

- Profitability Squeeze: The combination of 21% RGD, Corporate Tax, the new Statutory Levy, and massive compliance costs destroys margins for smaller operators.

- Affordability Checks: The “£150 net loss” threshold for checks is a conversion killer. It forces operators to demand bank statements from casual players, leading to massive drop-offs.

- Slot Limits: The £2/£5 stake limit removes the “whale” segment from online slots, forcing a high-volume, low-margin business model.

- Regulatory Instability: The rules change frequently (e.g., 2025 reforms). What is compliant today may be fined tomorrow.

- Payment Restrictions: No credit cards. No crypto (for licensed ops). Strict Source of Wealth (SOW) checks delay deposits.

Player-Specific Issues

- Players cannot use credit cards.

- Intrusive “Source of Funds” checks often freeze player accounts/withdrawals.

- GAMSTOP self-exclusion is permanent for the selected duration; no turning back.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: £500,000 – £1,000,000+ (Licensing, Tech, Initial Compliance)

Monthly Operating Costs: £150k+ (excluding marketing) for compliance staff, local rep, and reporting tools.

Effective Tax Rate on Revenue: ~45% (RGD + Corp Tax + Levy)

Customer Acquisition Cost: £300 – £600+ (Extremely High)

Time to Breakeven: 3-5 Years

Time to Positive ROI: 5+ Years

Profitability Assessment: Economics are prohibitive for small/mid-sized operators. The UK is a “Red Ocean.” The margins are too thin to support a new entrant unless you have a unique proprietary product or a massive marketing war chest (£10M+). Most new entrants exit within 24 months due to CAC exceeding LTV.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | High | UKGC actively works with payment processors and ISPs to block unlicensed sites. Prosecution is rare but asset seizure and payment blocking are common. |

| Licensed Operators | Critical | Highest Risk. Paradoxically, licensed ops face the most risk: Multi-million pound fines for “social responsibility failings” are standard. |

| Affiliates/Advertisers | Medium | Strict ASA (Advertising Standards Authority) rules. Promoting unlicensed sites can lead to criminal charges or domain seizure. |

| Payment Processors | High | Processors dealing with unlicensed UK traffic face immediate termination by card schemes (Visa/MC) and potential criminal abetting charges. |

| Company Directors | Medium | Personal Management Licenses (PMLs) can be revoked. Directors can be personally fined for company compliance failures. |

🚨 Extradition and International Enforcement

Extradition Treaties: The UK has robust extradition treaties with the USA, EU member states, Australia, Canada, and many others.

Enforcement History: The UK generally focuses on disrupting payment flows and fining licensed entities rather than extraditing offshore operators. However, executives located in the EU or associated territories should be cautious if targeting the UK illegally.

Safe Jurisdictions: Few. The UK’s diplomatic reach is long.

📋 Final Verdict

United Kingdom receives an Operator Ease Score of 5.1/10 and a Player Access Score of 9.0/10, resulting in an overall market attractiveness rating of 6.5/10.

HONEST ASSESSMENT: The UK is the “Gold Standard” of regulation, which means it is a compliance nightmare for operators. While fully legal, the combination of high taxes (effectively 45%+), punitive stake limits (£2/£5), and intrusive affordability checks makes it incredibly difficult to turn a profit. This market is effectively closed to bootstrapped startups; it is a playground only for publicly traded giants who can amortize compliance costs across massive volume. If you do not have £10M+ in liquidity, stay away.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A major global brand with significant capital (£10M+) looking for stability.

- A proprietary tech owner who can avoid white-label fees to save margin.

- Willing to accept a 5-7 year ROI horizon.

❌ Definitely Avoid If You Are:

- A generic white-label casino (you will bleed money on CAC).

- Depending on “Whale” players (Affordability checks and Stake Limits kill this model).

- Under-capitalized (<£2M budget).

- A Crypto-casino (Crypto is not a standard regulated payment method here).

- An offshore operator expecting to fly under the radar (Payment blocking is effective).

⚠️ BOTTOM LINE: A prestigious but low-margin trap. High volume cannot compensate for the regulatory suffocation unless you have massive scale.