Vanuatu presents a compelling opportunity for iGaming operators due to its favorable regulatory environment and business-friendly policies. With recent reforms streamlining licensing and tax structures, Vanuatu aims to attract international online gambling enterprises.

The jurisdiction offers a stable legal framework supporting multiple gambling verticals under a transparent, risk-based regulatory system, providing clarity and long-term operational certainty.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Legal Status | Fully Regulated, Online & Land-based |

| Regulatory Authority | Vanuatu Gaming Authority (VGA) under Department of Customs and Inland Revenue |

| Relevant Legislation | Interactive Gaming Act (2000), Casino Control Act (1993), Betting Control Act (1993) |

| Population | ~300,000 (2025 estimate) |

| GDP (Nominal) | Approx. $1.2 billion USD (2025 forecast) |

| GDP per Capita | Approx. $4,000 USD |

| Internet Penetration Rate | ~55% of population |

| Mobile Penetration Rate | ~75% |

| License Types Available | Interactive Gaming, Bookmaking, Lottery & Bingo, General Online Gaming |

| License Application Fee | €5,000 (~$5,370 USD) |

| Annual License Renewal Fee | €10,000 (~$10,700 USD) |

| License Validity Period | 15 years |

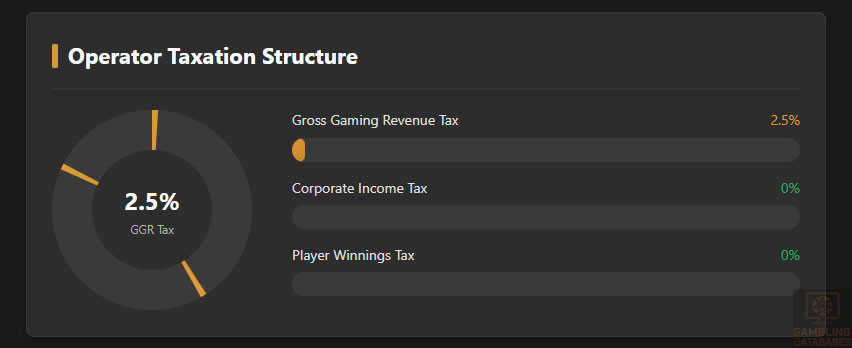

| Gross Gaming Revenue (GGR) Tax Rate | 1% – 2.5% depending on source |

| Operator Taxation Structure | 2.5% GGR tax + annual fees |

| Player Taxation | No tax on winnings |

| Market Entry Timeline | 6-8 weeks licensing decision |

| Minimum Capital Requirement | Not explicitly published; financial stability assessed |

| Mandatory Local Presence | Company registered in Vanuatu with physical address |

| KYC/AML Compliance | Mandatory under AML Act No. 13 (2014) |

| Responsible Gambling Measures | Required, with risk-based approach |

| Audit and Reporting | Annual independent audit, periodic reports to VGA |

| Payment Systems Allowed | Traditional (cards, bank transfers), emerging VASP pending regulation |

| Technology Approval | Mandatory approval of gaming platform, RNG, and game rules |

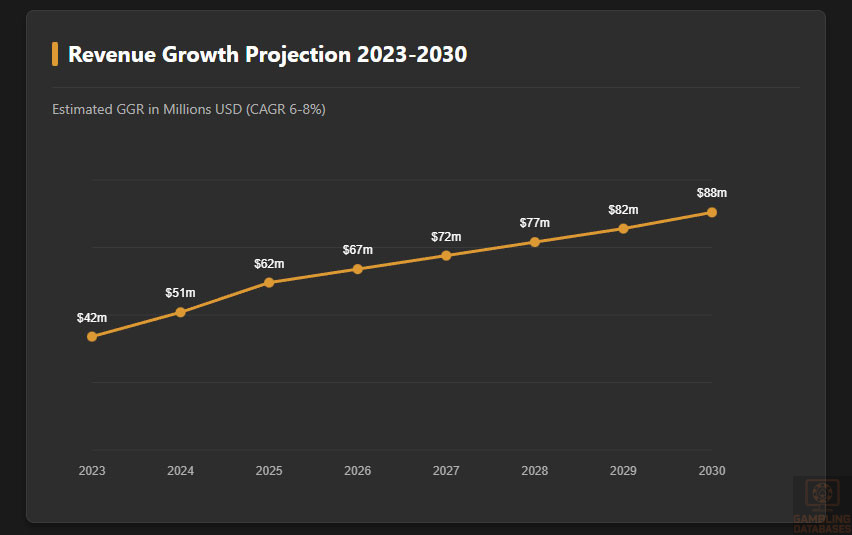

| Market Size Projection 2025 | Estimated $50-70 million USD in GGR |

| Growth Forecast CAGR | Approx. 6-8% through 2030 |

| Average Revenue Per User (ARPU) | Approx. $400-$600 USD annually |

| Ease of Doing Business Rank (Regional) | Top 3 in Pacific Islands |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

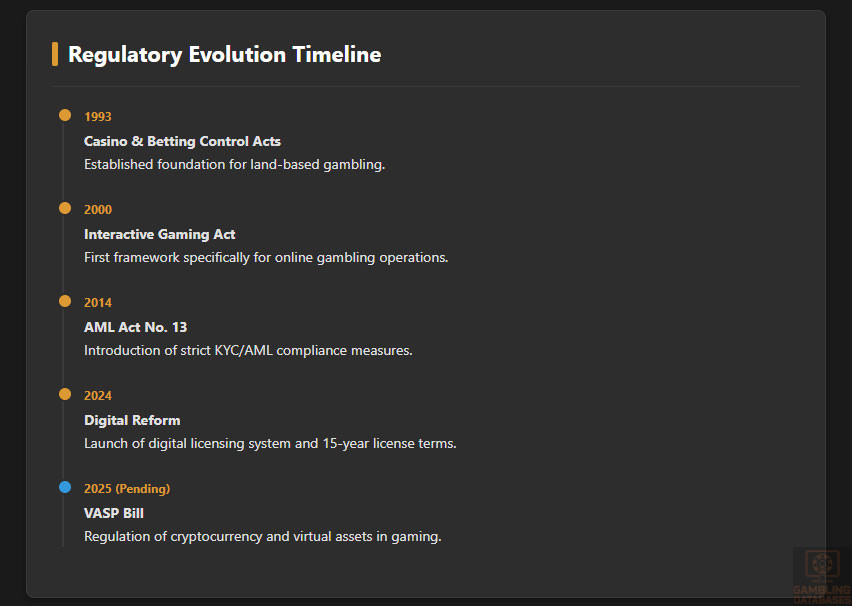

Vanuatu maintains a fully regulated gambling environment covering both land-based and online sectors. The legal framework is anchored by three central statutes: the Casino Control Act 1993, the Interactive Gaming Act 2000, and the Betting Control Act 1993. These laws collectively oversee casinos, sports betting, lotteries, and interactive online gambling.

Land-Based Gambling Activities

Land-based gambling in Vanuatu includes licensed casino operations, sports betting outlets, slot venues, and limited lottery services. Casinos operate under strict licensing conditions, subject to operational standards and financial audits. Sports betting occurs primarily through licensed bookmakers and authorized agents, offering fixed odds and virtual sports betting options.

Operators in land-based venues must comply with customer protection laws, age restrictions, and transparent reporting obligations. The licensing process requires background checks on key personnel and continuous compliance monitoring.

Online Gambling Framework

The online gambling sector in Vanuatu is governed by the Interactive Gaming Act 2000, amended recently to enhance regulatory efficiency. Operators offering online casino games, poker, sports betting, bingo, and lottery services must secure an Interactive Gaming License issued by the VGA.

Digital operators are required to adhere to strict rules regulating game fairness, responsible gambling, player verification, and anti-money laundering (AML) protocols. Prohibited activities include unlicensed online gambling and underage participation.

The regulatory framework emphasizes a risk-based compliance model where operators tailor their controls based on player demographics, geographic reach, and transaction patterns. This adaptive approach balances consumer protection with business facilitation.

Licensed Operators and Market Players

Vanuatu’s market currently hosts multiple licensed operators targeting international markets, particularly in Asia-Pacific, Europe, and North America. Operators benefit from the jurisdiction’s business-friendly tax rates and robust licensing structure with a 15-year validity term.

The competitive landscape is characterized by several medium-sized firms with diverse portfolios in online casinos, sports betting, and lottery gaming. Many entrants adopt strategic partnerships with technology providers to meet licensing requirements and strengthen operational compliance.

Licensing Framework and Requirements

Application Process and Eligibility

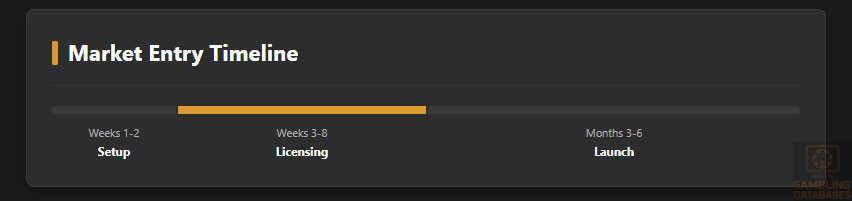

The licensing process is managed by the Vanuatu Gaming Authority (VGA) and involves a fully digital application system launched in 2024 to streamline approvals. Applicants must demonstrate financial stability, technical competence, and transparent ownership structure.

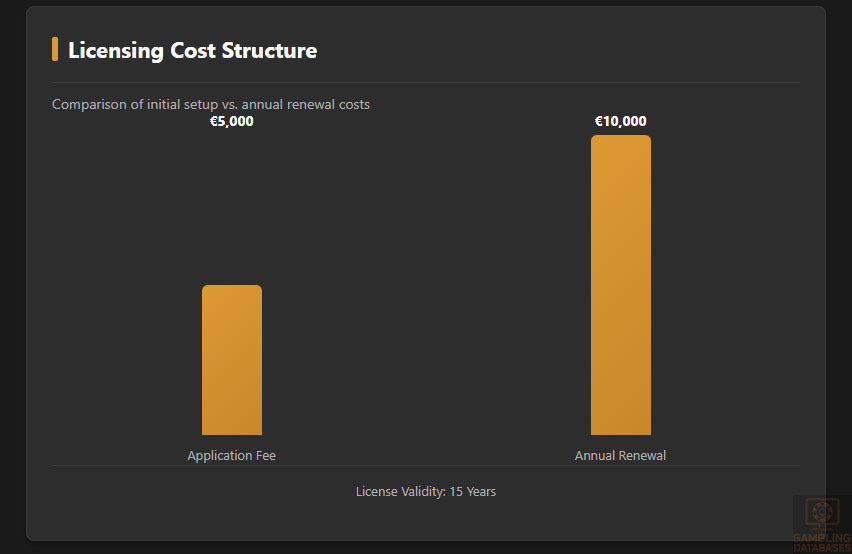

Application fees are set at €5,000, with an annual renewal fee of €10,000. The license term is 15 years, providing long-term operational certainty. Approval timelines average 6-8 weeks, contingent on applicant responsiveness and completeness of documentation.

Applicants undergo rigorous background checks covering criminal records, financial audits, and management experience. The regulator assesses legitimacy of capital sources and operational readiness comprehensively.

The following documents are generally required for license applications:

- Certificate of Incorporation and corporate registration documents

- Audited financial statements for the past three years or business projections for startups

- Detailed business plan including marketing strategy and risk assessment

- Technical documentation on gaming software, RNG certification, and platform infrastructure

- Resumes and background checks of directors, beneficial owners, and key management

- Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) policies

- Proof of local office address and contact information in Vanuatu

Local Presence and Operational Requirements

Operators must be incorporated locally with a physical presence in Vanuatu, including a registered business address. While full operational staff local residency is not mandatory, key contact points and compliance representatives must be established within jurisdiction.

Foreign ownership is permitted without restrictions, but transparency in beneficial ownership and compliance with local laws is mandatory. Maintaining a local bank account for operational transactions is required to aid financial monitoring.

Compliance Obligations and Monitoring

Player Protection and Identification

Player protection is a core focus featuring stringent age verification procedures to exclude minors. Know Your Customer (KYC) and Anti-Money Laundering (AML) controls include identity verification, transaction monitoring, and ongoing risk profiling.

Operators implement responsible gambling measures such as setting deposit limits, self-exclusion options, and providing access to problem gambling resources. The framework mandates transparent disclosure of terms, odds, and payout percentages.

Mandatory player protection measures include:

- Age verification and identity checks before account activation

- Ongoing monitoring for suspicious or high-risk behavior

- Enablement of self-exclusion and time-out features

- Clear display of game rules, odds, and payout information

- Provision of responsible gambling resources and support contacts

- Regular evaluation and updating of responsible gambling policies

Financial Monitoring and Reporting

Operators subject to continuous financial oversight including transaction audits and compliance reporting. Reporting cycles require monthly submission of gross gaming revenue, player activity, and financial health indicators to the VGA.

Annual independent audits must be completed within three months of fiscal year-end and submitted for regulator review. Random on-site inspections and system audits complement document-based oversight to ensure integrity and compliance.

- Submit monthly revenue and player activity reports by the 15th of each month

- Complete annual financial audit by an authorized independent auditor within 3 months of fiscal year-end

- Disclose any significant operational or ownership changes within 7 days

- Allow regulator site inspections and investigations upon request

Taxation Structure and Financial Obligations

Player Taxation

Individual players enjoy a tax-free environment on gambling winnings. No withholding or personal income taxes are applied on payouts, making Vanuatu attractive for high-value gamblers and international clients.

Operator Taxation

Online gambling operators incur a gross gaming revenue (GGR) tax of 2.5%, one of the lowest globally, enhancing competitive advantage. Additionally, the annual license renewal fee and regulatory charges contribute to fixed operational costs.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue (GGR) Tax | 2.5% |

| License Application Fee | €5,000 ($5,370 USD) |

| Annual License Renewal Fee | €10,000 ($10,700 USD) |

| Corporate Income Tax | No additional corporate tax on gambling revenue |

Gambling Market Financial Performance

The market is estimated to generate between $50 million and $70 million in gross gaming revenue in 2025, driven by regional demand and operator expansion. Year-over-year growth is forecasted at 6-8% CAGR through 2030, indicating steady market maturation.

Revenue distribution favors online casino verticals followed by sports betting and lottery games. Tax contributions from operators create a significant revenue stream for the government while maintaining an attractive climate for new entrants.

Advertising and Marketing Restrictions

Advertising is permitted but subject to strict regulations governing content, channels, and target audiences. Promotions must not be misleading or encourage excessive gambling behavior.

Operators must avoid targeting minors or vulnerable populations and comply with restrictions on broadcasting times and sponsorship placements in regulated media.

Advertising restrictions focus on:

- No marketing targeting persons under 18 years of age

- Prohibition of false or exaggerated winning claims

- Restrictions on promoting excessive or irresponsible gambling

- Limited hours for broadcasting gambling-related advertisements

- Transparency in sponsorship disclosures and promotional material

Recent Regulatory Changes and Their Impact

In 2024, Vanuatu modernized its gambling legislation introducing a fully digital licensing system and extended license terms to 15 years. These changes reduced bureaucracy and enhanced regulatory transparency.

The proposed Virtual Asset Service Provider (VASP) bill expected in 2025 will regulate cryptocurrency use in gaming, aligning Vanuatu with global AML and FATF standards. This initiative further reinforces Vanuatu’s position as a forward-looking jurisdiction for innovative gambling technologies.

Enforcement Mechanisms and Penalties

The VGA enforces compliance through regular audits, site inspections, and investigation of complaints. Penalties for breaches include fines, license suspension, or revocation depending on severity.

Key enforcement mechanisms include:

- Financial penalties for non-compliance with reporting or operational obligations

- Suspension or revocation of licenses for repeated or serious breaches

- Criminal prosecution for fraudulent or illegal gambling activities

- Seizure of assets linked to illicit operations

- Mandatory remediation plans for operators failing to meet player protection standards

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

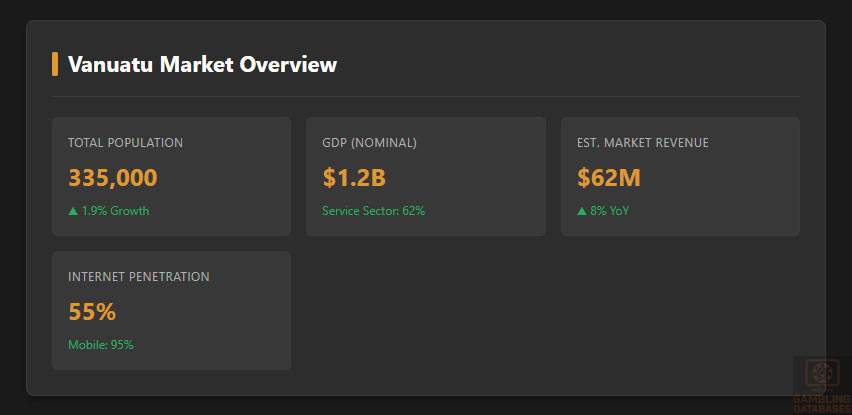

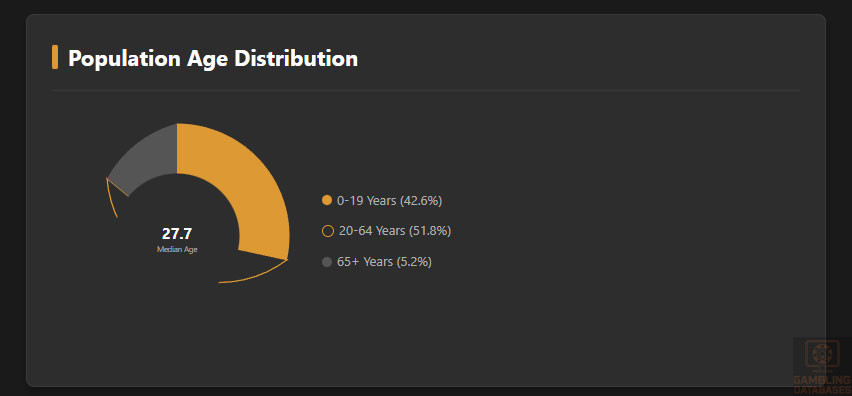

Vanuatu’s total population is approximately 335,000 individuals in 2025, with a steady growth rate of about 1.9% annually. The median age is relatively young at 27.7 years, reflecting a youthful demographic profile ideal for digital adoption and iGaming consumption.

The gender ratio is balanced, with roughly 1,019 men per 1,000 women. Life expectancy is estimated at around 73.9 years, indicating improving healthcare and living standards over recent years.

| Age Group | Percentage of Population |

|---|---|

| 0-19 years | 42.6% |

| 20-64 years | 51.8% |

| 65 years and above | 5.2% |

Urbanization is gradually increasing, with approximately 29.3% of the population residing in urban centers. The capital, Port Vila, is the primary urban hub, representing the epicenter for commercial activities and gambling venues.

Geographic Distribution

Economic and population activities concentrate mainly in the southern islands and the capital city of Port Vila. Rural areas across the archipelago exhibit lower population densities with limited access to broadband internet, crucial for online gaming expansion.

Internet penetration and gambling venue density strongly correlate with urban areas, where infrastructure supports higher digital connectivity and financial transactions facilitating operator growth.

- Port Vila – Population approx. 50,000, principal economic center

- Luganville – Approx. 16,000, secondary urban commercial hub

- Other urban centers – Including Lenakel, Isangel, and Sola, each with populations ranging from 3,000-7,000

- Rural and outer islands – Scattered populations with lower digital connectivity

- Concentration of licensed gambling venues primarily in Port Vila and Luganville

Economic Indicators and Consumer Spending Power

Vanuatu’s GDP was estimated around $1.2 billion USD in 2025, reflecting moderate growth amid regional economic fluctuations. The service sector, particularly tourism and finance, dominates the economy, comprising over 60% of GDP, while agriculture remains a key source of employment.

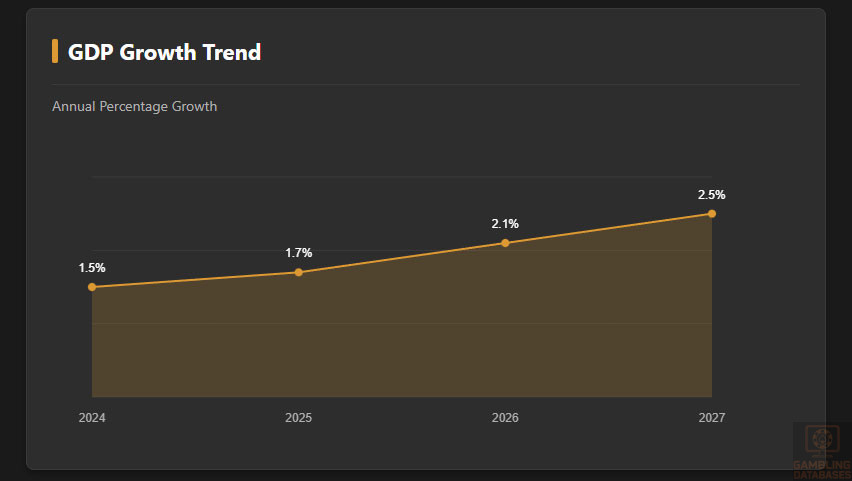

GDP per capita is approximately $4,000 USD, showing steady upward trends reflecting improved economic opportunities. Growth forecasts estimate a gradual recovery to 1.7% in 2025 with potential acceleration beyond 2.5% by 2027, supported by government-led infrastructure projects and expanding digital economies.

Consumer spending demonstrates rising disposable incomes in urban centers, with middle-income households increasingly adopting online services including entertainment and gaming. Variable income distribution exists, with notable disparities between urban professional classes and rural subsistence populations.

Household income distribution highlights a growing consumer base capable of digital expenditures:

- High-income urban professionals with discretionary spending capacity

- Mid-level income earners engaging increasingly with mobile and online commerce platforms

- Lower-income rural populations with limited internet access and gaming participation

| Metric | Value |

|---|---|

| GDP (Nominal) | $1.2 billion USD |

| GDP Growth Forecast 2025 | 1.7% |

| GDP Per Capita | $4,000 USD |

| Service Sector Contribution to GDP | ~62% |

| Agriculture Sector Contribution | ~24% |

| Urbanization Rate | 29.3% |

| Median Household Income | Approx. $7,500 USD annually |

| Unemployment Rate | ~6.5% |

Market Size and Growth Projections

The iGaming market in Vanuatu is nascent but expanding rapidly. Current gross gaming revenues are estimated between $50-70 million USD with a compound annual growth rate (CAGR) forecast between 6-8% through 2030.

Market growth is driven by rising internet adoption, increasing mobile penetration, and favorable regulatory reforms encouraging international operator participation. The average revenue per user (ARPU) is estimated at $400 – $600 annually, with consistent growth in active player base projected.

| Year | Revenue | Growth Rate (YoY) | ARPU (USD) |

|---|---|---|---|

| 2023 | 42 | 6% | 380 |

| 2024 | 51 | 7% | 410 |

| 2025 | 62 | 8% | 450 |

| 2026 | 67 | 7% | 480 |

| 2027 | 72 | 6% | 510 |

Education, Skills, and Digital Literacy

Vanuatu possesses a high literacy rate, exceeding 85%, supported by government initiatives increasing access to education. Secondary education rates have improved significantly, fostering a growing base of digitally literate youth.

This growing digitally competent population facilitates greater online service adoption, benefiting iGaming operators targeting younger demographics with tech-savvy profiles.

Cultural and Social Factors

Communication and Language

Vanuatu is a multilingual society with three official languages: Bislama, English, and French. English predominates in business and digital communication, especially among urban and younger populations.

- Bislama — widely spoken creole and lingua franca

- English — dominant in education, government, and online services

- French — used mainly in certain islands and by older generations

- Over 100 indigenous languages and dialects, influencing regional communication

- Internet content predominantly in English catering to international and educated local users

Cultural Attitudes

Gambling is culturally accepted in urban and tourist areas, seen as entertainment and revenue generator. Religious and traditional influences moderate gambling behavior, especially in rural areas. Foreign operator brands generally enjoy positive perceptions when transparent and compliant.

Entertainment preferences favor social and digital gaming, with esports and mobile gaming rapidly gaining traction among younger cohorts. Recreational gambling is viewed as leisure rather than livelihood, aligning with responsible gaming philosophies emphasized by regulators.

Problem Gambling and Social Considerations

While formal data on problem gambling is limited, awareness and social responsibility initiatives are increasing. Vulnerable populations reside mainly in lower-income urban groups where access to credit and mobile gambling services is rising.

Government and NGOs have developed several programs aimed at harm reduction, player protection, and treatment access.

- National awareness campaigns on responsible gambling

- Support hotlines and counseling services for affected individuals

- Self-exclusion programs mandated for all licensed operators

- Training for gambling venue staff on identifying problem gambling

- Collaboration with health services to address addiction treatment

Political Structure and Governance

Vanuatu operates as a parliamentary democracy within a constitutional monarchy framework. Political stability remains strong, supporting regulatory consistency critical for long-term market confidence.

The government actively pursues economic diversification and digital transformation, strengthening international relationships through Pacific trade partnerships and regulatory cooperation.

Technology Adoption and Digital Behavior

Internet and Digital Usage

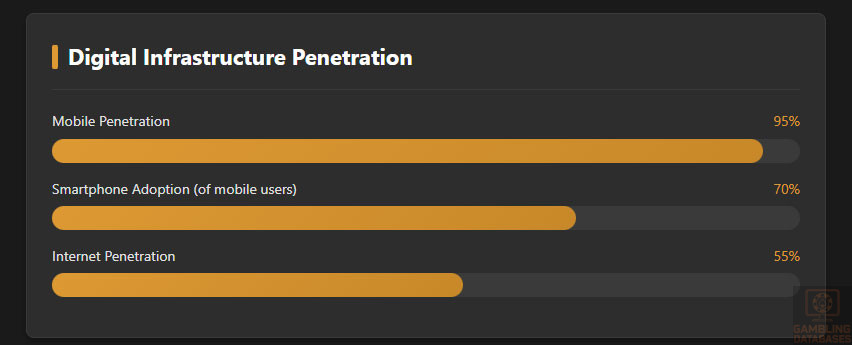

Internet penetration in Vanuatu stood at approximately 45.7% in early 2025, with growing uptake driven by urban areas. Mobile adoption reaches nearly 95% of the population, with broadband capable devices comprising over 96% of connections.

Average daily internet usage spans 3-4 hours, dominated by social media, video streaming, and digital communications. The youth segment shows particularly high engagement on gaming and entertainment platforms.

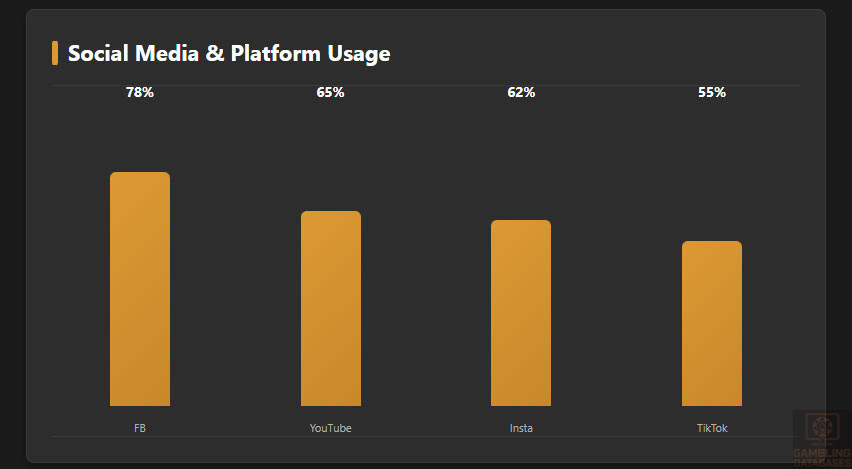

- Facebook – 78% penetration among internet users, key for engagement

- YouTube – 65% penetration, popular for video content consumption

- Instagram – 62%, strong among younger demographics

- TikTok – Growing adoption at 55%, especially for short video content

- WhatsApp – Widely used for messaging and community groups

Digital Payment Behavior

Payment methods for online transactions are evolving, with credit and debit cards leading in adoption. Bank transfers and emerging digital wallets gain traction among urban professionals. Cryptocurrency use remains nascent but showing interest in alignment with regulatory developments.

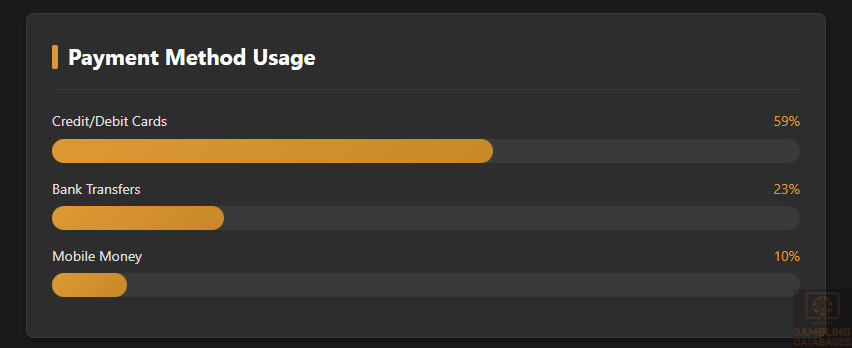

- Credit/Debit cards – 59% share of online payments

- Bank transfers – 23%, favored for larger transactions

- Mobile money platforms – 10%, increasing with smartphone penetration

- E-wallets (PayPal, Skrill) – 6%, used mostly by niche segments

- Cryptocurrency transactions – emerging with pilot projects underway

Gaming and Gambling Preferences

Current Market Participation

Gambling participation rates are moderately growing, with sports betting and online casino games ranking as the most engaged activities. The market exhibits rising multiplayer and skill-based gaming trends, reflecting global shifts.

| Rank | Activity | Participation (%) |

|---|---|---|

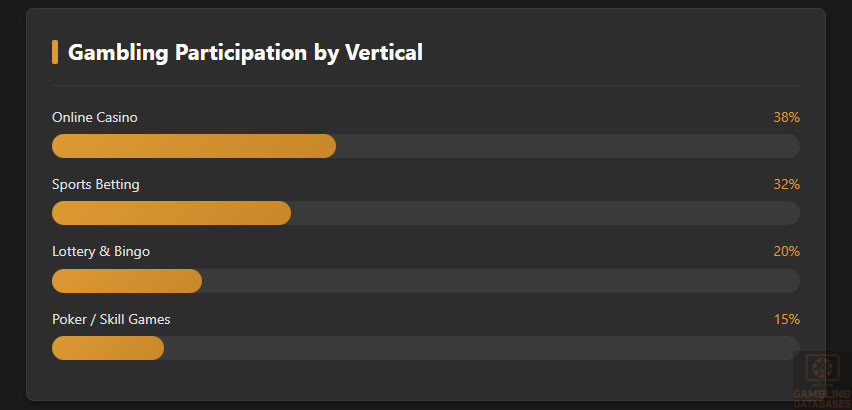

| 1 | Online casino games (slots, table games) | 38% |

| 2 | Sports betting (local and international events) | 32% |

| 3 | Lottery and bingo ticket purchases | 20% |

| 4 | Poker and skill-based games | 15% |

| 5 | Esports betting | 12% |

Consumer Behavior Patterns

Spending habits reveal peak gambling activities occurring during evenings and weekends. Session lengths average between 25-40 minutes, consistent with casual gaming preferences. Retention rates are enhanced through loyalty programs and mobile app accessibility.

Users increasingly prefer mobile platforms offering multi-vertical gaming options, reflecting a trend toward convenience and user experience sophistication. Payment flexibility and localized content also drive engagement and market expansion potential.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Vanuatu’s internet penetration rate stands at approximately 46% in 2025, with a significant divide between urban and rural areas. Broadband is primarily accessible in urban centers, while rural connectivity is heavily reliant on mobile internet services.

The average fixed broadband speed is moderate, averaging around 25 Mbps, whereas mobile networks often provide lower speeds but greater flexibility. Infrastructure investments by government and private sector are ongoing to expand high-speed coverage and improve reliability.

5G and Future Technology Deployment

5G rollout remains in early stages, with initial trials conducted by key network operators in urban hubs like Port Vila. Full 5G commercial deployment is anticipated over the next 3-5 years, parallel to regional Pacific island upgrades.

Network operators prioritize expanding 4G LTE coverage while preparing for 5G demand growth, especially driven by digital services expansion, including iGaming and mobile entertainment.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Vanuatu’s mobile network sector is competitive, dominated by a few major operators providing extensive coverage across inhabited islands. Data costs have decreased steadily, making mobile internet increasingly accessible to the population.

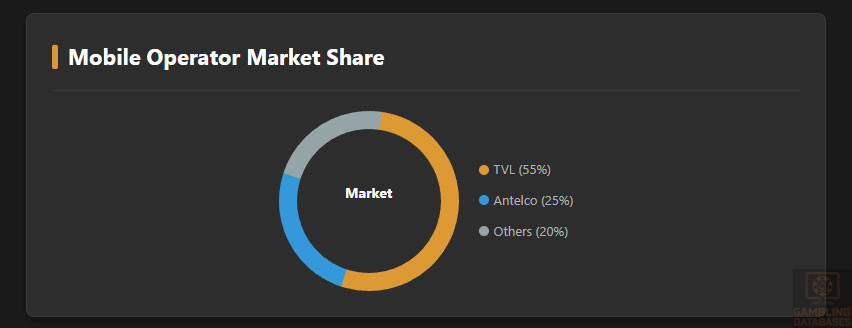

- TVL (Telecom Vanuatu Limited) – Market leader with approx. 55% subscriber share

- Antelco Vanuatu – Controls about 25%, strong in prepaid mobile services

- DigiRont Vanuatu – Emerging player focusing on data-centric packages

- Worldlink Vanuatu – Niche provider with regional coverage focus

- Digicel Pacific – Serving telecommunications needs with broad regional reach

Device Penetration

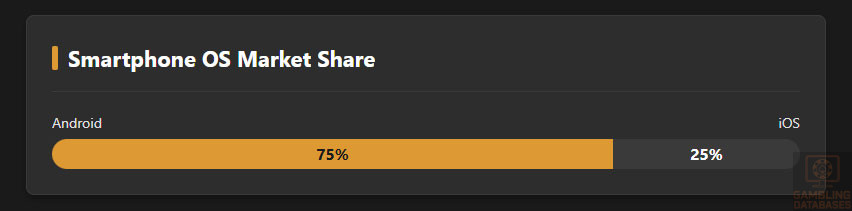

Smartphone adoption is robust, estimated at over 70% of mobile users. Android dominates device market share, favored for affordability and availability, with iOS devices comprising approximately 25%, predominantly in urban affluent segments.

Users engage heavily with mobile applications for communication, entertainment, and increasingly, gaming. Device turnover rates are accelerating as younger demographics demand higher performance and better connectivity solutions.

Financial Services and Payment Infrastructure

Banking System Structure

The banking landscape includes a mix of commercial banks and regional financial institutions. Digital banking adoption is increasing, enhancing convenience for online transaction processing.

- National Bank of Vanuatu – Largest with comprehensive digital platform

- BSP (Bank South Pacific) – Regional presence with strong online banking services

- ANZ Vanuatu – Offers international banking and forex services

- Westpac Vanuatu – Focuses on corporate and retail banking

- Asia Pacific Investment Bank – Emerging digital services provider

Payment Processing Options

Payment infrastructure supports a variety of options, with credit/debit card acceptance widespread and growing e-wallet popularity. Bank transfers remain preferred for high-value transactions.

- Visa and Mastercard widely accepted online

- Bank transfers through major banks

- Mobile money solutions for urban and rural users

- Popular e-wallets such as PayPal, Skrill, and Neteller

- Cryptocurrency payments emerging but under regulatory watch

E-commerce and Digital Economy

E-commerce is expanding rapidly, supported by increasing digital literacy and payment method availability. Online retail primarily focuses on consumer electronics, fashion, and groceries.

Consumer trust in digital services is rising due to reinforced cybersecurity measures and government digital economy initiatives, boosting opportunities for iGaming providers to integrate e-commerce elements like in-game purchases.

Business Environment and Regulatory Framework

Ease of Business Operations

Vanuatu ranks favorably among Pacific nations for ease of doing business, influenced by streamlined registration processes, low operational costs, and supportive government policies encouraging foreign investment in digital sectors.

- Preparation of incorporation documents, including notarizations and translations

- Submission and approval by the Vanuatu Financial Services Commission (VFSC)

- Tax registration with the Department of Customs and Inland Revenue

- Opening corporate bank accounts with local banks

- Compliance registrations, including gaming license applications if applicable

Corporate Structure and Registration

Key entity types include Limited Liability Companies (LLCs), corporations, and foreign branch offices. LLCs are preferred for flexibility and local control, while corporations suit larger operations with complex ownership structures.

Registration timelines typically range from two to four weeks, depending on documentation completeness and government agency responsiveness. There are no restrictions on foreign ownership, facilitating international partnerships and investments.

- Certificate of Incorporation

- Memorandum and Articles of Association

- Director and shareholder identification documents

- Proof of registered office address in Vanuatu

- Taxpayer Identification Number application

Taxation Framework

Corporate Income Tax Structure

The corporate income tax rate in Vanuatu is relatively low, with no additional taxes imposed specifically on gambling revenues beyond the standard gross gaming revenue tax. Special Economic Zones offer tax holidays and incentives for technology-driven businesses.

Double taxation treaties exist with several countries, facilitating foreign investment and cross-border operations.

- Australia

- New Zealand

- China

- France

- Japan

Personal Income Tax

Vanuatu imposes no personal income tax, withholding tax, or social security contributions on salaries, making it attractive for expatriates and senior management working in the iGaming sector. Tax residency is defined primarily by physical presence exceeding 183 days annually.

Market Entry Considerations

Recommended Entry Strategies

Operators entering Vanuatu should focus on leveraging local incorporation advantages and compliance ease. Strategic partnerships with technology vendors and localized marketing are critical for market penetration.

- Establishing a local entity with physical presence and compliance representatives

- Partnering with experienced platform providers with VGA approval

- Adopting robust KYC and AML systems aligned with regulatory expectations

- Focusing on mobile-first gaming solutions to tap into strong smartphone usage

- Implementing targeted responsible gambling initiatives to build consumer trust

Typical Costs and Timelines

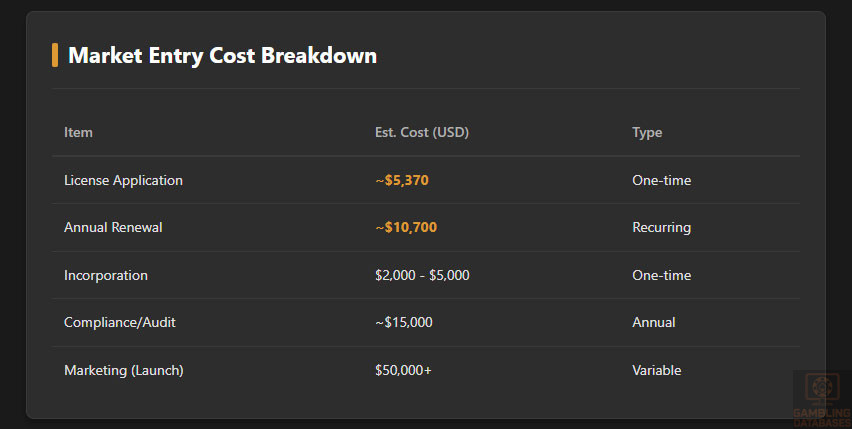

Initial setup investments include license application fees (€5,000), company registration costs, legal services, and working capital. Annual operational budgets should incorporate license renewals, compliance audits, marketing, and staff salaries.

License approvals average 6-8 weeks, and full market launch may require up to 4-6 months, depending on technology integration and marketing rollout.

- License application fee: €5,000

- License annual renewal: €10,000

- Company incorporation and registration: $2,000 – $5,000

- Compliance and auditing: $15,000 annually

- Marketing budget: highly variable, starting $50,000+

Success Factors and Challenges

Success hinges on deep understanding of regulatory nuances, agile compliance management, and cultural alignment with local and international players. Challenges include infrastructure gaps in rural areas, competition from larger jurisdictions, and evolving regulatory frameworks around cryptocurrency.

- Strong regulatory engagement and transparency

- Investment in secure, reliable gaming platforms

- Effective local partnerships and customer service

- Adaptation to mobile and emerging technologies

- Proactive responsible gambling and AML practices

Exit Strategy Planning

Market liquidity is moderate, with license transferability permitted under regulatory approval. Ownership transfers and business sales are subject to detailed compliance reviews and valuation influenced by operational performance and brand recognition.

Operators should maintain accurate financial records and regulatory compliance to maximize exit valuations and facilitate smooth ownership transitions.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Vanuatu?

Yes, online gambling is legal and regulated in Vanuatu under the Interactive Gaming Act 2000. The jurisdiction offers a transparent licensing framework that covers various digital gambling activities, including online casinos, sports betting, poker, and lotteries. Operators must secure licenses from the Vanuatu Gaming Authority and comply with AML and responsible gambling requirements. Illegal/unlicensed operations are prohibited and subject to enforcement.

2. What types of gambling licenses are available and what do they cover?

Vanuatu offers several license types catering to diverse gambling activities. These include Interactive Gaming Licenses for online operators, General Gaming Licenses for lotteries and bingo, Bookmaking Licenses for sports betting, and Casino Control Licenses for land-based venues. License validity extends up to 15 years, facilitating long-term operational planning. Each license type requires specific compliance and technical standards aligned with the gambling category served.

3. How much does an iGaming license cost and how long does it take to obtain?

The license application fee is €5,000, with an annual renewal fee of €10,000. The average time for license approval is between 6 to 8 weeks, assuming full documentation and regulatory clearance. Full market entry timelines, including company registration and platform integration, typically extend over 4 to 6 months.

4. Can foreign companies obtain a gambling license?

Yes, foreign companies are eligible to obtain gambling licenses in Vanuatu. There are no foreign ownership restrictions, but applicants must establish a registered entity with a physical address in the jurisdiction. Comprehensive background checks and financial audits ensure legitimacy and operational readiness. Transparency in ownership and compliance with local laws is mandatory throughout the license term.

5. What are the tax obligations for iGaming operators?

Operators pay a gross gaming revenue (GGR) tax of 2.5%, one of the lowest globally, combined with fixed license renewal fees. Corporate income tax exemptions apply specifically to gambling revenues, enhancing the attractiveness for investment. Annual financial audits and tax filings must be made to relevant authorities, ensuring transparent reporting.

| Tax Type | Rate |

|---|---|

| Gross Gaming Revenue Tax | 2.5% |

| License Application Fee | €5,000 |

| Annual Renewal Fee | €10,000 |

| Corporate Income Tax | Exempt on gambling income |

6. Are gambling winnings taxed for players?

No, individual players do not pay taxes on gambling winnings in Vanuatu. There are no withholding taxes or personal income tax applied to payouts, making it attractive for high-stakes players and international clients. This policy encourages greater player participation without tax burden complexities.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, technology platform expenses, compliance and audit costs, staff salaries, marketing, and payment processing. Marketing budgets vary widely depending on growth strategies but represent a significant expenditure.

- Licensing and renewal fees (€15,000 annually)

- Technology and platform hosting ($50,000+ annually)

- Compliance and audit costs ($15,000+ per year)

- Marketing and customer acquisition (variable, $50,000+)

- Staff remuneration and office expenses ($70,000+)

8. What is the expected ROI timeline for entering this market?

Return on investment typically occurs within 2 to 4 years, depending on scale, market positioning, and regulatory compliance speed. Initial license and setup costs are moderate, but achieving profitability relies on effective customer acquisition and retention. Ongoing regulatory stability supports predictable financial planning and ROI forecasting.

9. What are the local presence requirements for operators?

Operators must establish a registered business entity with a physical address in Vanuatu. While local staff residency is not mandatory, key personnel responsible for compliance and customer support should be accessible within the jurisdiction. Maintaining a local bank account is essential for financial operations, and timely regulatory communication is required.

10. What payment methods are available and recommended?

Available payments include credit/debit cards, bank transfers, e-wallets, and emerging mobile money options. Credit cards remain dominant for convenience, while e-wallets gain popularity among tech-savvy users. Cryptocurrency transactions are emerging but require close regulatory alignment.

- Visa and Mastercard credit/debit cards

- Skrill and Neteller e-wallets

- Bank transfers through major banks

- Mobile money platforms

- Cryptocurrency wallets (regulated use)

11. What are the advertising and marketing restrictions?

Advertising must not target minors or vulnerable populations. Content must avoid misleading claims or encouraging excessive gambling. Broadcast time restrictions and sponsor disclosures are enforced. Operators are encouraged to implement responsible marketing aligned with regulatory guidelines to maintain license compliance.

12. What responsible gambling measures are mandatory?

Operators must provide age verification, self-exclusion options, deposit limits, transparent odds disclosure, and access to support resources. Regular policy reviews and staff training on responsible gambling are compulsory to uphold player protection standards.

- Age and identity verification

- Self-exclusion and time-out programs

- Deposit and loss limits settings

- Clear information on game risks and odds

- Access to gambling addiction support services

13. How large is the iGaming market and what is the growth potential?

The current iGaming market size is approximately $62 million in gross gaming revenues, with growth forecasted at 6-8% CAGR through 2030. Increasing internet access and smartphone adoption underpin scalable growth prospects, supported by a stable and competitive regulatory regime.

14. Who are the main competitors and what is their market share?

The market features several mid-sized operators with diverse offerings, primarily targeting international players. Market share is fragmented, with no single dominant player, creating opportunities for entrants with innovative platforms and strong local partnerships. Competitive dynamics rely heavily on technology integration and marketing sophistication.

15. What are the player preferences and typical spending patterns?

Players favor online casino games and sports betting, with a tendency toward mobile platforms. Sessions mainly occur during evening hours, with average spending modest but growing as product offerings diversify. Retention is driven by loyalty incentives and trusted payment methods.

16. What are the key success factors and main challenges for new entrants?

Success depends on robust regulatory compliance, strong local presence, and effective marketing aligned with cultural dynamics. Challenges include infrastructural disparities, maintaining player trust, adapting to evolving digital payment landscapes, and staying ahead of regulatory changes affecting cryptocurrency and AML policies.

- Engagement in proactive regulatory communication

- Leveraging advanced, secure gaming technology

- Comprehensive responsible gambling programs

- Building culturally relevant marketing strategies

- Overcoming rural infrastructure and digital divide challenges

Sources and References

- Vanuatu Gaming Authority (VGA) Official Website – https://vga.vu

- Department of Customs and Inland Revenue, Vanuatu – https://customsinlandrevenue.gov.vu

- World Bank Doing Business Report 2024 – https://worldbank.org

- IMF Article IV Consultation Report 2025 – https://imf.org

- Digital 2025: Vanuatu Report – DataReportal – https://datareportal.com

- National Statistics Office of Vanuatu – https://vnso.gov.vu

- Telecom Vanuatu Limited (TVL) Reports – https://tvl.vu

- BSP Bank Vanuatu Information – https://bsp.com.vu

- Chambers and Partners Global Practice Guide: Vanuatu Gaming Law 2024

- International Telecommunication Union ICT Data – https://itu.int

- Population Pyramid – Vanuatu 2025 – https://populationpyramid.net

- Vanuatu Ministry of Finance Tax Regulations – https://finance.gov.vu

- Gambling Industry Reports by MGL Solutions and Global Gaming Business

- Pacific Economic Update – World Bank 2025

- Countrymeters: Vanuatu Population Data 2025 – https://countrymeters.info

- TradingEconomics – Vanuatu Internet Usage Stats – https://tradingeconomics.com

- South Pacific Communication Providers – Digicel Pacific – https://digicelgroup.com

- International AML and Gaming Compliance Standards, FATF – https://fatf-gafi.org

- Academic studies on Pacific Island digital economies

- UN Population Fund – Demographics of Vanuatu – https://unfpa.org

- MyGamingLicense – Vanuatu Gambling License Guide

- World Bank Pacific Trade and Investment Reports

- Online Gaming Market Research by YBCase and industry sources

- SDLC Corp – Vanuatu Licensing Process and Costs Report

- Global Law Experts – Vanuatu Gambling License Analysis

- Vanuatu Telecommunications Regulatory Authority Reports

- Various news articles from YOGONet, AGBrief, IGaming Today on recent regulatory developments

🎯 Gambling Databases Country Rating: Vanuatu

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 9.2/10 | 🟢 Excellent 8-10 |

| Player Access Score | 9.5/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 4.0/10 | 🟡 Moderate (High ease, but negligible local market value) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- [Tiny Addressable Market] The local population is only ~300,000 with a GDP per capita of ~$4,000. This is NOT a viable B2C target market for major operators.

- [Infrastructure Limitations] Internet penetration is barely 55%, with rural areas lacking reliable broadband. Digital reach is severely restricted compared to global standards.

- [Banking & De-risking] While Vanuatu regulations are friendly, international Tier-1 banks often classify Pacific Island jurisdictions as high-risk, potentially complicating cross-border settlements and merchant account setup.

- [Reputational Limits] A Vanuatu license is generally considered Tier-2/Tier-3. It provides little to no legal protection or advertising rights in strict jurisdictions like the UK, USA, Germany, or Ontario.

- [Extradition Risks] Vanuatu maintains close legal and political ties with Australia and New Zealand, creating potential extradition pathways for operators targeting those nations illegally.

- [Crypto Uncertainty] While a VASP bill is pending for 2025, cryptocurrency is currently in a “gray/emerging” status. Reliance on crypto processing before full regulation carries legislative risk.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 3.0/3.0 | Fully Legal (+3.0). All verticals (Casino, Sports, Lottery) are legal and regulated under the Interactive Gaming Act 2000. No prohibitions exist. |

| Licensing Process | 25% | 2.5/2.5 | Highly Accessible (+2.0). Process takes only 6-8 weeks. Low Costs (+0.5): Application is €5,000 and annual renewal is €10,000. This is one of the cheapest licenses globally. Validity is 15 years. |

| Taxation & Costs | 20% | 2.0/2.0 | Extremely Low Tax (+2.0). GGR tax is capped at 2.5% (well under the 15% threshold). No corporate tax on gambling revenue. Operational costs are minimal. |

| Operational Requirements | 15% | 1.2/1.5 | Moderate Requirements (+1.0). Local incorporation and physical address required. Deduction (-0.3): While staff residency isn’t mandatory, the requirement for local compliance representatives and physical presence creates logistical friction for purely remote teams. |

| Market Environment | 10% | 0.5/1.0 | Moderate Environment (+0.5). “Ease of doing business” is good regionally, but global connectivity and infrastructure lag behind hubs like Malta or Curaçao. Deduction (-0.0): No current active enforcement against operators, but market size limits the “business environment” score. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully Legal (+4.0). Players can legally access all forms of online gambling. No prohibitions on products. |

| Practical Accessibility | 30% | 2.5/3.0 | Infrastructure Limits (-0.5). While no ISP blocking exists (+3.0), the low internet penetration (46-55%) and rural connectivity issues physically prevent access for half the population. |

| Player Penalties | 20% | 2.0/2.0 | No Penalties (+2.0). Players face no fines or criminal risks. Winnings are tax-free. |

| Market Availability | 10% | 1.0/1.0 | Open Market (+1.0). Multiple licensed operators exist, and players can access international sites without restriction. |

🔍 Key Highlights

Strengths (B2B / Licensing Only)

- Aggressive Tax Dumping: 2.5% GGR tax is among the lowest in the world, designed purely to attract offshore entities.

- Speed to Market: 6-8 week licensing timeline is significantly faster than Malta or Isle of Man.

- Cost Efficiency: €15,000 first-year licensing cost is negligible for established businesses.

⛔️ CRITICAL RISKS AND CHALLENGES

- [Insignificant Local Revenue:] With a total market projection of only $50-70M USD, Vanuatu is statistically irrelevant as a B2C target market.

- [Infrastructure Deficit:] 4G/5G is still rolling out; rural areas are effectively offline.

- [Payment Processing Friction:] “High Risk” jurisdictional tags by Visa/Mastercard can lead to higher processing fees or declined merchant accounts for operators based here.

- [Regulatory Perception:] Licenses from Vanuatu hold little weight with European or North American regulators. It is strictly an “offshore” license.

- [Limited Talent Pool:] With a small population, finding experienced local compliance officers or MLROs to meet physical presence requirements will be difficult.

Player-Specific Issues

- Digital Divide: nearly 50% of the population cannot access online casinos due to lack of infrastructure.

- Income Levels: With $4,000 GDP per capita, average deposit sizes will be extremely low ($10-$20 range).

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: €25,000 – €40,000 (Licensing + Incorporation + Legal).

Monthly Operating Costs: Low ($5,000 – $10,000 for basic local presence).

Effective Tax Rate on Revenue: ~2.5% (GGR Tax) + 0% Corporate Tax.

Customer Acquisition Cost: Low locally, but LTV is also extremely low.

Profitability Assessment:

AS A LOCAL B2C OPERATOR: NO. The market is too small and too poor. You will struggle to cover even basic fixed costs with local revenue alone.

AS AN INTERNATIONAL HUB: YES. The economics are excellent for using Vanuatu as a corporate base to target other unregulated jurisdictions (Asia/LatAm/Africa), provided you can secure banking.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | Medium | Low risk locally, but high risk of international enforcement if targeting strict markets (USA/Australia) using this license. |

| Licensed Sports Betting Operators | Low | Regulatory burden is minimal; risk comes from banking partners de-risking the jurisdiction. |

| Affiliates/Advertisers | Low | Vanuatu does not actively prosecute affiliates, but they must comply with basic age restrictions. |

| Payment Processors | High | Processing for Pacific offshore entities invites intense scrutiny from Visa/Mastercard and potential fines for high chargeback rates. |

| Company Directors | Low | Personal liability is low provided AML compliance is maintained. |

🚨 Extradition and International Enforcement

Extradition Treaties: Vanuatu is a member of the Commonwealth and has extradition cooperation with Australia, New Zealand, and the United Kingdom. It is NOT a safe haven for operators targeting these countries illegally.

Enforcement History: Vanuatu has previously cooperated with Australian authorities regarding cross-border financial crimes. Pressure from the FATF (Financial Action Task Force) forces Vanuatu to comply with international AML requests.

Safe Jurisdictions: Operators targeting Australia or NZ from Vanuatu face genuine legal peril due to geographic and political proximity.

📋 Final Verdict

Vanuatu receives an Operator Ease Score of 9.2/10 and a Player Access Score of 9.5/10, resulting in an overall market attractiveness rating of 4.0/10.

HONEST ASSESSMENT:

“Do not confuse ‘ease of entry’ with ‘market value.’ Vanuatu is an exceptional licensing jurisdiction for startups wanting a cheap, fast, and low-tax legal structure to target unregulated markets in Asia, Africa, or LatAm. However, as a target market itself, it is commercially worthless due to a tiny, low-income population and poor internet infrastructure. Use Vanuatu to get a license, not to find players.”

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Startup Operator with limited capital (<$100k) needing a valid license to sign game providers.

- Targeting “Grey” Markets in Asia or Africa where a Tier-1 license is unnecessary.

- Seeking a Crypto-friendly environment (pending VASP regulation) with low tax overhead.

❌ Definitely Avoid If You Are:

- Looking for Local Players (Market is too small).

- Targeting Tier-1 Jurisdictions (UK/USA/EU) — this license will not help you.

- Targeting Australia/New Zealand illegally (High extradition/cooperation risk).

- Require Tier-1 Banking (JPMorgan/HSBC will likely reject Vanuatu entities).

⚠️ BOTTOM LINE: A cost-effective launchpad for international “grey market” operations, but completely unviable as a local B2C consumer market.