Vietnam presents a cautiously evolving landscape for iGaming market entry, marked by strict regulation and emerging pilot programs. Although most online gambling remains prohibited, increasing government openness to regulated casinos and prize-winning electronic games signals future opportunities for investors.

This analysis provides a fact-dense overview of Vietnam’s iGaming legal framework, licensing requirements, taxation, and operational conditions, supporting informed market entry decisions.

| Metric | Value |

|---|---|

| Gambling Legal Status | Highly restricted; most gambling prohibited except licensed casinos and prize games |

| Online Gambling Legal Status | Casino-style and card-based online games banned |

| Gambling Regulatory Authorities | Ministry of Finance, Ministry of Public Security, Regional authorities |

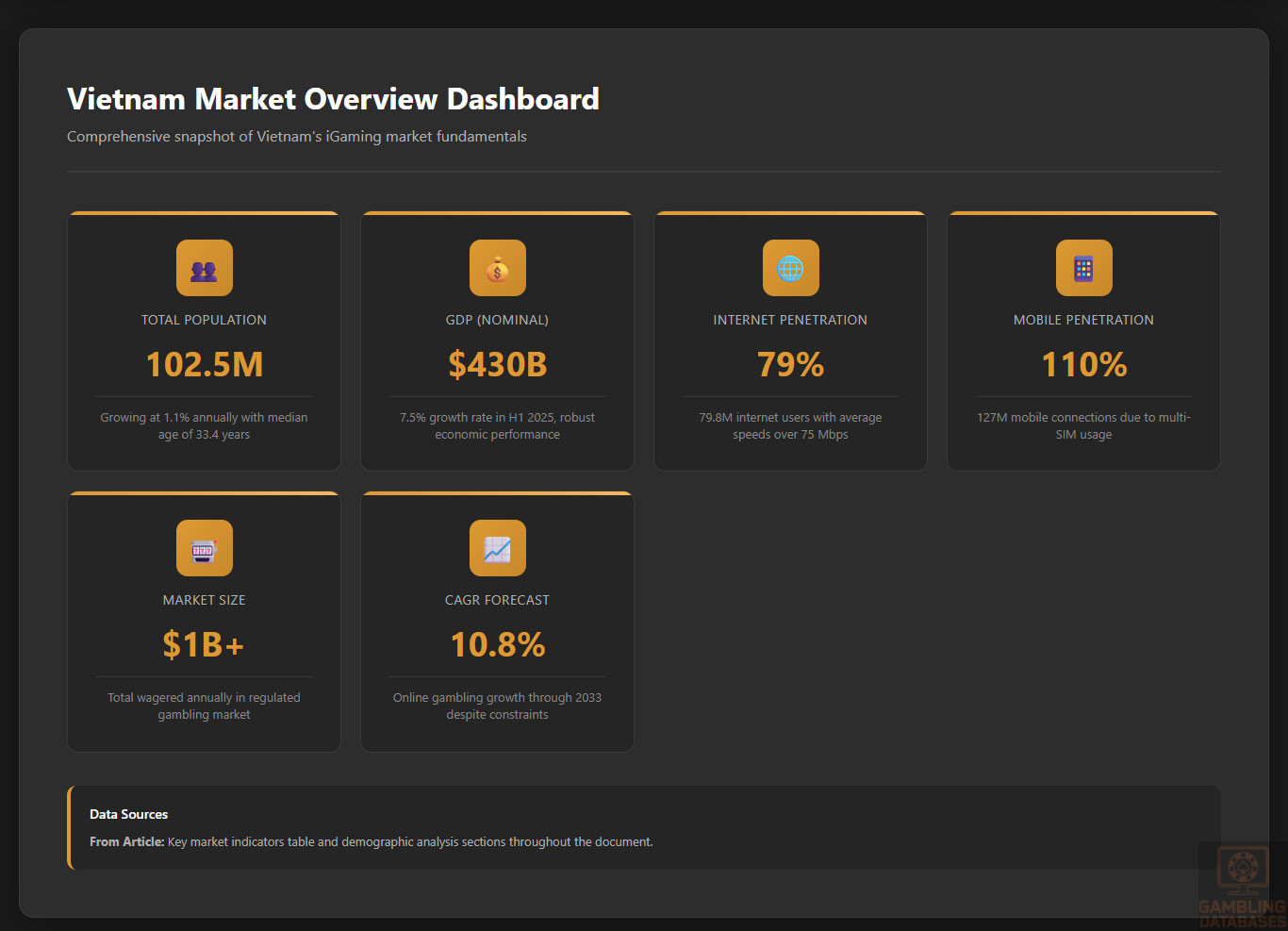

| Population | Approximately 99 million |

| Median Age | 32 years |

| GDP (Nominal) | Approx. $430 billion (2025 est.) |

| GDP Growth Rate | 6.5% annually (forecasted) |

| Internet Penetration | 73% |

| Mobile Penetration | 110% (SIMs per capita) |

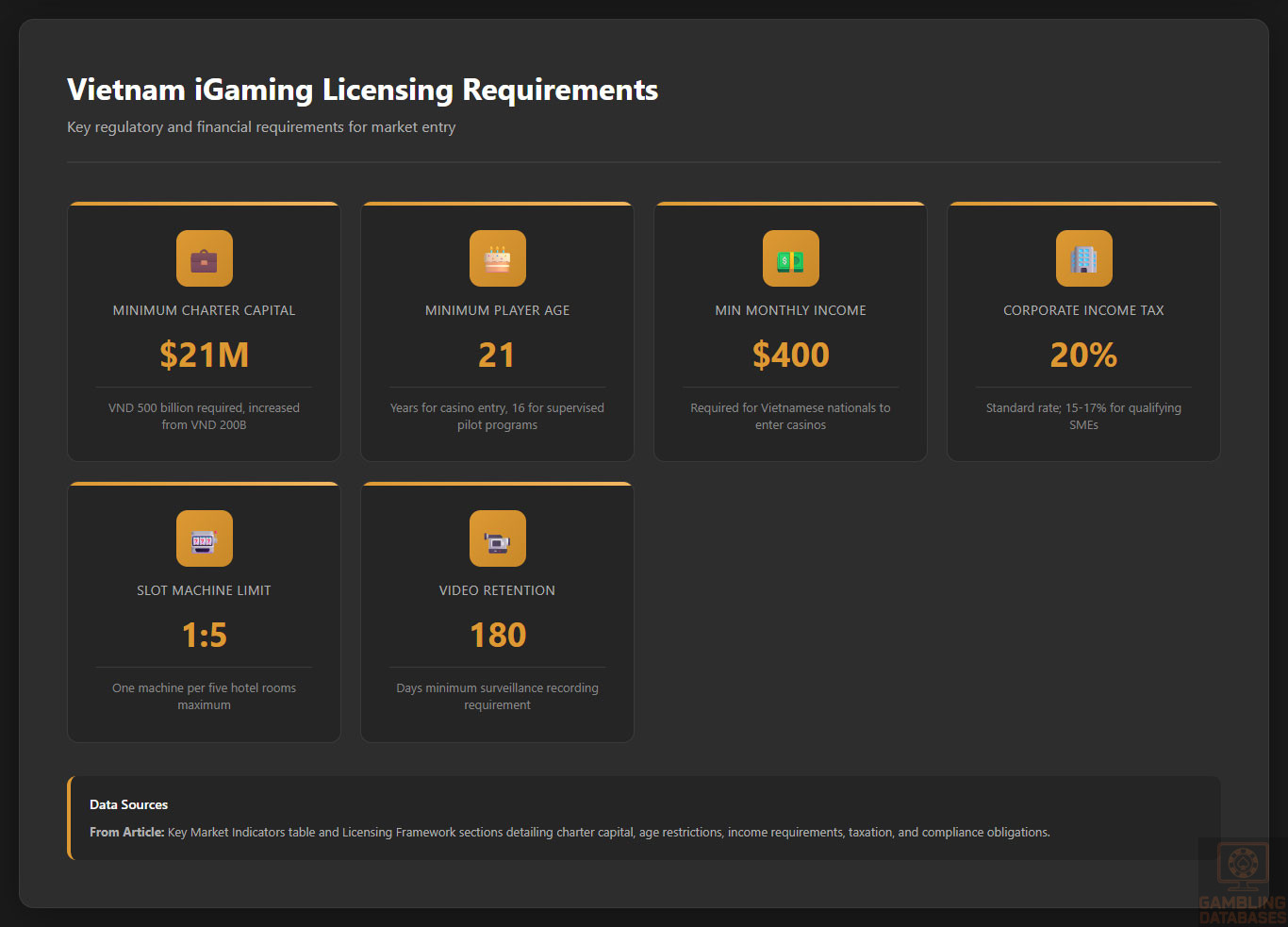

| Casino Entry Age (Local Players) | 21 years minimum |

| Minimum Monthly Income for Casino Entry (Locals) | $400 USD |

| Licensing Authorities | Ministry of Finance (main) |

| License Application Fee | Not publicly disclosed; includes multi-stage fees |

| Minimum Charter Capital for Operators | VND 500 billion (~$21 million USD) |

| Slot Machines Limit | One machine per five hotel rooms |

| Operator Corporate Income Tax Rate | Standard 20%; tiered lower rates of 15% and 17% for SMEs |

| Gross Gaming Revenue (GGR) Tax | Variable by game type; specific rates undisclosed |

| Personal Income Tax on Player Winnings | Withholding applied; taxed at standard PIT rates |

| Regulatory Compliance Requirements | Strict KYC/AML, player verification, surveillance and reporting obligations |

| Player Protection Measures | Age verification, self-exclusion, playtime limits under pilot programs |

| Local Presence Requirement | Mandatory local licensing and physical business location |

| Foreign Ownership | Allowed with licensing and regulatory approval |

| Market Entry Barriers | High capital requirements and regulatory scrutiny |

| Estimated Market Size (2025) | Above $1 billion USD total wagered (offline) |

| iGaming CAGR Forecast | Moderate due to regulatory constraints, 5-7% |

| Average Revenue Per User (ARPU) | Approximately $400 per active casino player |

| Operational License Renewal Period | Annual or multi-year renewal typical |

| Advertising Restrictions | Strict content and channel limitations |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Vietnam’s gambling landscape is characterized by stringent restrictions with limited allowances under controlled pilot programs. The government traditionally prohibits most forms of gambling, focusing on social protection and risk mitigation.

Land-based gambling remains the primary legal avenue, mostly restricted to foreign tourists and a limited number of Vietnamese citizens under strict entry conditions. Online gambling, particularly casino-style and card-based games, is banned nationwide as per Decree 147/2024, with harsh enforcement to prevent illegal operations.

Land-Based Gambling Activities

Casino operations in Vietnam are concentrated in a few licensed venues, primarily catering to foreign tourists. Since 2017, a pilot program allows Vietnamese nationals access to casinos if they meet criteria including being at least 21 years old, demonstrating a minimum monthly income of approximately $400, and paying a significant entrance fee.

Online Gambling Framework

Online gambling remains largely prohibited with explicit bans on casino-style, card-based, and sports betting platforms. The government enforces this through strict licensing frameworks and sanctions targeting unlicensed operators.

Foreign operators wishing to enter Vietnam’s e-gambling market must comply with Decree 121/2021 and associated regulations, allowing business only under licenses issued by the Ministry of Finance after meeting rigorous requirements. Participation in e-gambling is restricted to foreigners and overseas Vietnamese holding valid visas, excluding illegal residents or those overstaying permits.

Licensed Operators and Market Players

The Vietnamese gambling market features a limited number of licensed casinos, primarily large-scale projects in resort areas such as Phu Quoc and Ho Tram. Market competition is regulated with strict licensing caps on slot machines and operational scale.

Foreign investors face high entry barriers, including elevated capital requirements and local partnership obligations. The pilot schemes and evolving regulations suggest gradual market liberalization, but operators must prepare for ongoing government oversight and compliance costs. Market share is highly concentrated among a few flagship operators.

Licensing Framework and Requirements

Application Process and Eligibility

The Ministry of Finance is the principal licensing authority for gambling businesses. Operators must submit extensive documentation proving financial capability, operational competence, and technical compliance.

Key application documents include corporate registration, business plans, technical certifications for gaming equipment, and financial statements audited by recognized firms. The minimum charter capital requirement was raised from VND 200 billion to VND 500 billion, roughly $21 million USD, reflecting efforts to ensure operator stability.

License application fees are multi-stage but are not publicly disclosed. The process typically involves initial eligibility certification, followed by sub-licenses for foreign currency transactions governed by the State Bank of Vietnam.

- Corporate registration certificate and articles of incorporation

- Audited financial statements for the past fiscal year

- Comprehensive business plan outlining market and operational strategy

- Technical documentation and certification for gaming machines and RNG systems

- Criminal background checks for major shareholders and executives

- Proof of minimum charter capital deposit in licensed Vietnamese bank

- Security and surveillance system specifications with recording requirements

Local Presence and Operational Requirements

Vietnam mandates a physical business presence for licensed operators, including a registered office within the country. Internet domain ownership must be local for online-related operations, enabling regulatory control and enforcement.

The regulatory framework requires trained personnel with demonstrated experience, often a minimum of three years in gambling management roles. Foreign ownership is permitted but subject to regulatory approval and compliance with local laws, including operational audits and reporting.

- Physical registered office in Vietnam

- Locally hosted domain names for online operations

- Management staff with verified qualifications and experience

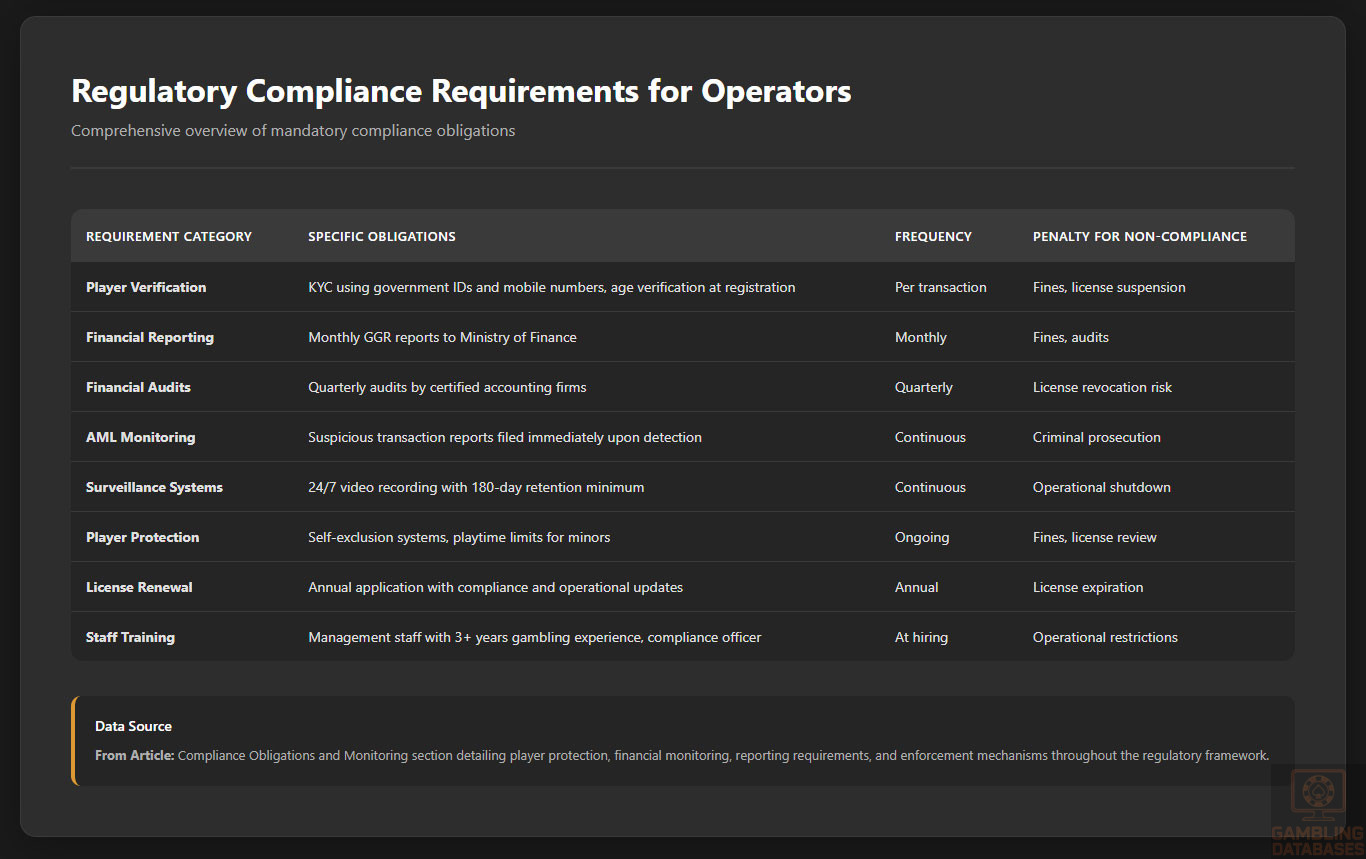

- 24/7 surveillance system with minimum 180 days video retention

- Dedicated compliance officers for KYC and AML oversight

Compliance Obligations and Monitoring

Player Protection and Identification

Vietnam enforces strict player protection measures including mandatory age verification, ensuring players meet the minimum age of 21 for casinos and 16 years for supervised participation in certain pilot programs.

KYC (Know Your Customer) and AML (Anti-Money Laundering) standards align with international best practices, requiring identity verification through Vietnamese mobile phone numbers and documentation checks. Responsible gambling measures include self-exclusion options and limits on playtime for minors.

- Mandatory age verification at account registration and entry

- KYC verification using government-issued IDs and mobile numbers

- Self-exclusion systems accessible to players

- Playtime restrictions for under-18 participants in pilot schemes

- Regular auditing of player protection compliance

Financial Monitoring and Reporting

Operator financial transactions are subject to continuous monitoring, including mandatory reporting of large or suspicious transactions to Vietnamese authorities. Annual and quarterly audits by licensed third parties are common compliance conditions.

Reporting processes require submission of detailed revenue figures, tax payments, and operational metrics. These procedures strengthen anti-fraud and revenue assurance efforts, with penalties for non-compliance ranging from fines to license revocation.

- Monthly submission of gross gaming revenue reports to the Ministry of Finance

- Quarterly audits of financial statements by certified accounting firms

- Suspicious transaction reports filed immediately upon detection

- Annual renewal application including compliance and operational updates

Taxation Structure and Financial Obligations

Player Taxation

Players’ winnings are subject to personal income tax withholding at standard rates, deducted at source by operators. Reporting thresholds aim to capture significant winnings while minimizing administrative burden on low-value prizes.

Operator Taxation

| Game Type | Tax Rate |

|---|---|

| Casino Table Games Gross Gaming Revenue (GGR) | Variable; approximately 20% |

| Slot Machines | Fixed monthly fees and capped machine numbers |

| Sports Betting | Projected rates pending regulatory update |

Operators pay corporate income tax (CIT) standard rate of 20%, with tiered lower rates of 15% and 17% for micro and small enterprises respectively. Licensing fees and renewal costs form part of the financial obligations complementing taxation.

Gambling Market Financial Performance

The total amount wagered in Vietnam’s regulated gambling market surpasses $1 billion annually, predominantly generated by land-based casinos. Market revenues have shown moderate growth driven by tourism and pilot schemes allowing selective local participation.

Year-over-year revenue growth is projected between 5% and 7% despite persistent regulatory constraints on online activities. Tax revenues from gambling form a modest but growing component of national revenues, supporting ongoing regulatory developments.

Advertising and Marketing Restrictions

Gambling advertising is heavily restricted, with permitted channels limited mainly to controlled venues and approved media. Content must avoid targeting minors or vulnerable populations and is subject to government approval before release.

- Limited advertising to licensed premises and authorized media outlets

- Ban on targeting individuals under 18 years old

- Restrictions on promotional content emphasizing social responsibility

- Prohibition of misleading or exaggerated claims

- Time restrictions to prevent advertising during certain hours

Recent Regulatory Changes and Their Impact

Recent regulatory amendments include the 2024 Decree 147 banning online casino-style games and the 2022 Decree 121 tightening electronic gambling business conditions. The government is reviewing pilot program outcomes as of late 2025, considering expanded local access and enhanced oversight mechanisms.

These changes have increased operator compliance costs but aim to balance social protection with economic growth opportunities. Future regulatory evolution likely includes establishing a dedicated gaming authority and modernizing licensing frameworks.

Enforcement Mechanisms and Penalties

The Vietnamese government employs a range of enforcement tools including fines, license suspensions, and criminal penalties for illegal gambling operations. Regulatory inspections and investigations have intensified since 2023 to curb unlicensed activities.

- Fines for unlicensed gambling operations

- License revocation or suspension for compliance breaches

- Criminal prosecution for illegal operators and facilitators

- Seizure of assets used in unlawful gaming activities

- Online blocking of unauthorized gambling websites

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

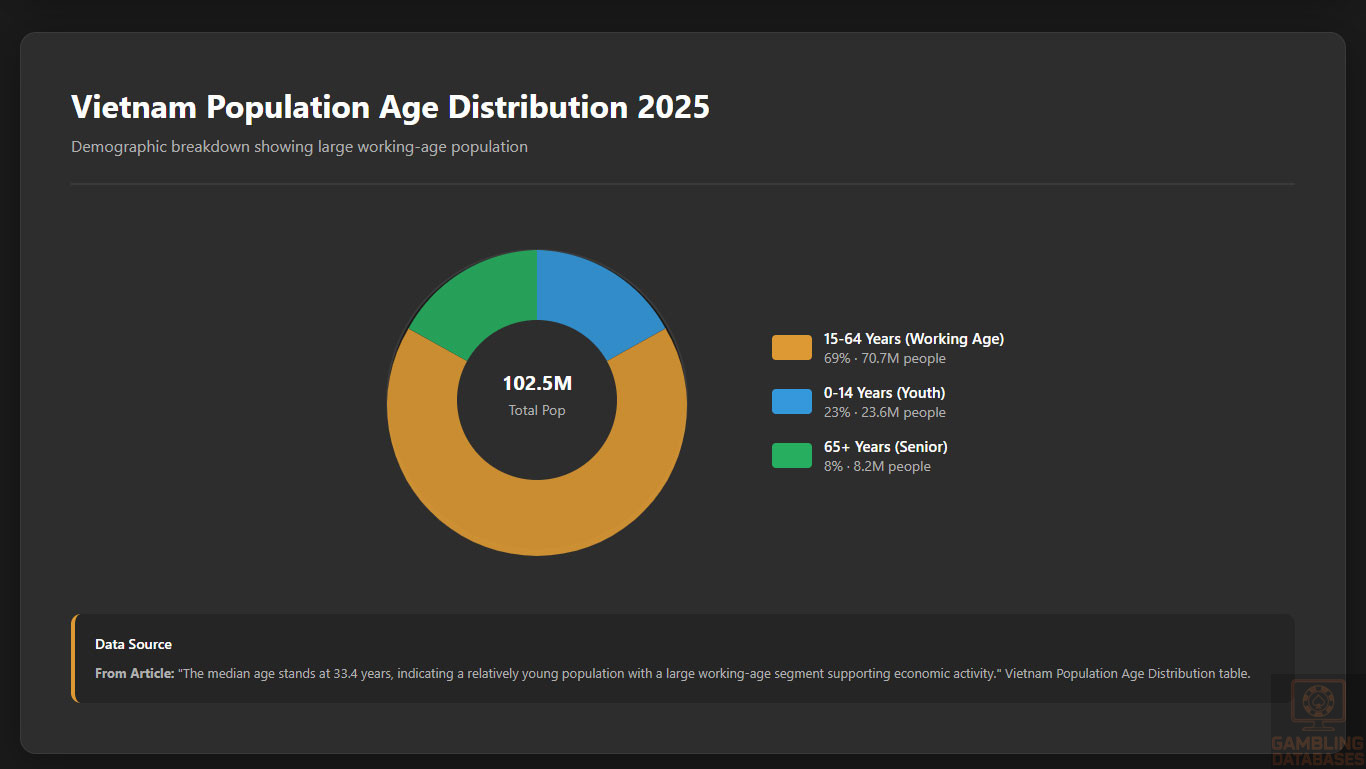

Vietnam’s total population reached approximately 102.5 million in 2025, reflecting a modest growth rate of about 1.1% annually. The median age stands at 33.4 years, indicating a relatively young population with a large working-age segment supporting economic activity.

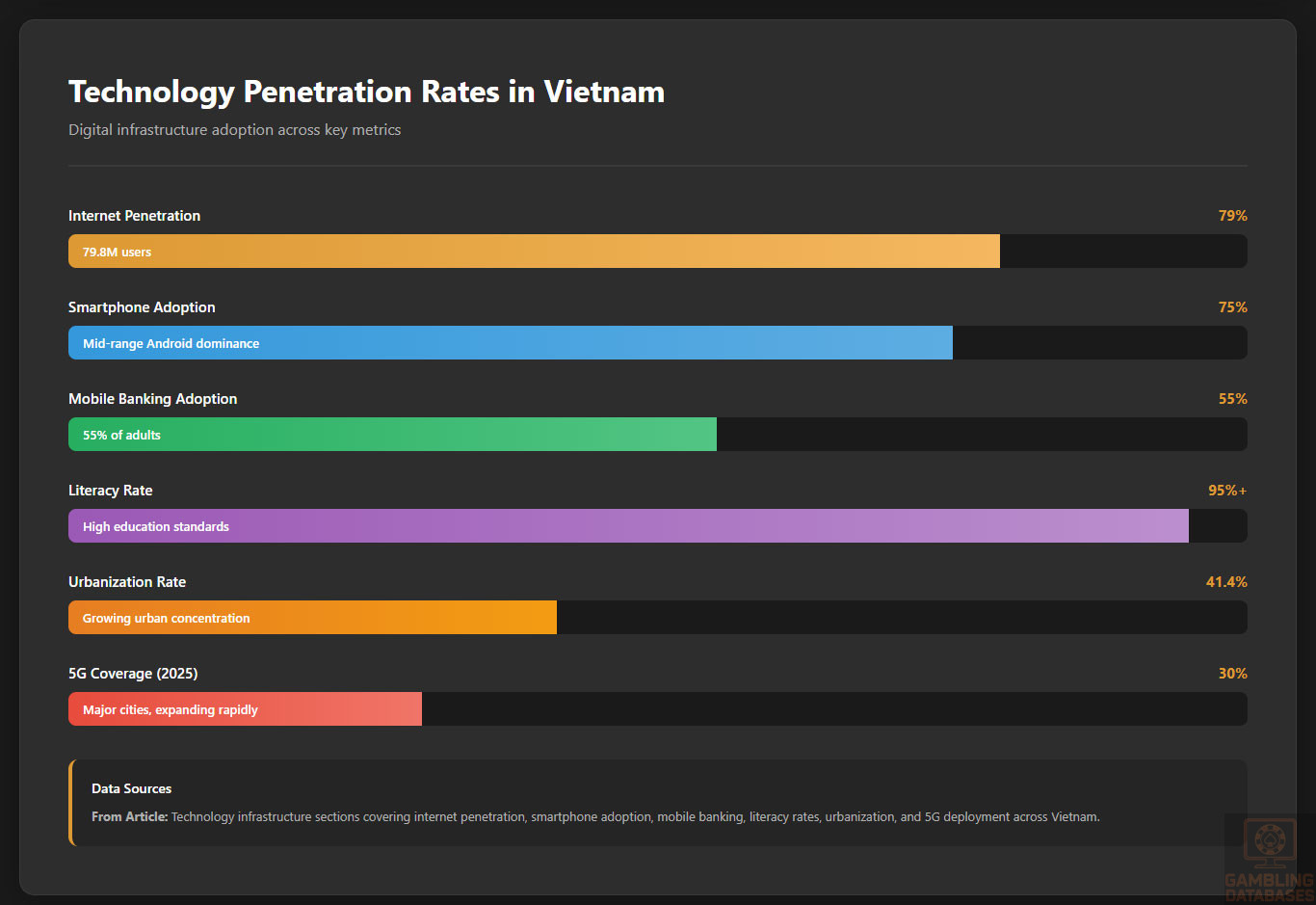

Gender ratio is slightly skewed with about 978 males per 1,000 females, below the global average. Urban residents constitute roughly 41.4% of the total population, with increasing urbanization driving growth in major cities. Rural areas remain home to the majority but are experiencing gradual migration to urban centers.

| Age Group | Percentage of Total Population |

|---|---|

| 0-14 years | 23% |

| 15-64 years | 69% |

| 65 years and over | 8% |

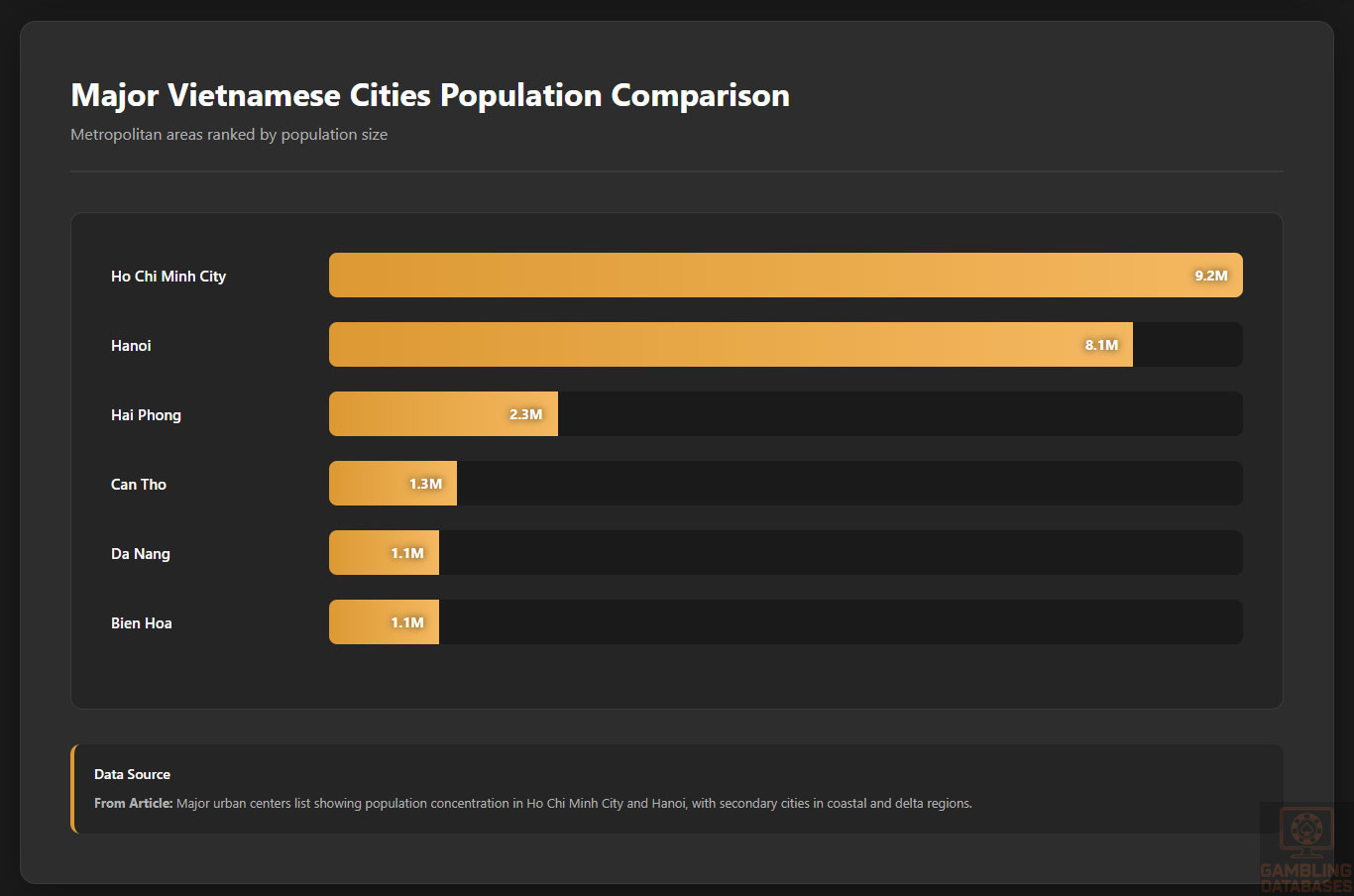

Population density averages 328 people per km², with concentration largely in the fertile Red River Delta and Southeast regions. Major urban hubs like Hanoi and Ho Chi Minh City dominate economic and social life, serving as focal points for digital connectivity and gambling venue presence.

- Ho Chi Minh City (~9.2 million residents)

- Hanoi (~8.1 million residents)

- Hai Phong (~2.3 million residents)

- Can Tho (~1.3 million residents)

- Da Nang (~1.1 million residents)

- Bien Hoa (~1.1 million residents)

Economic Indicators and Consumer Spending Power

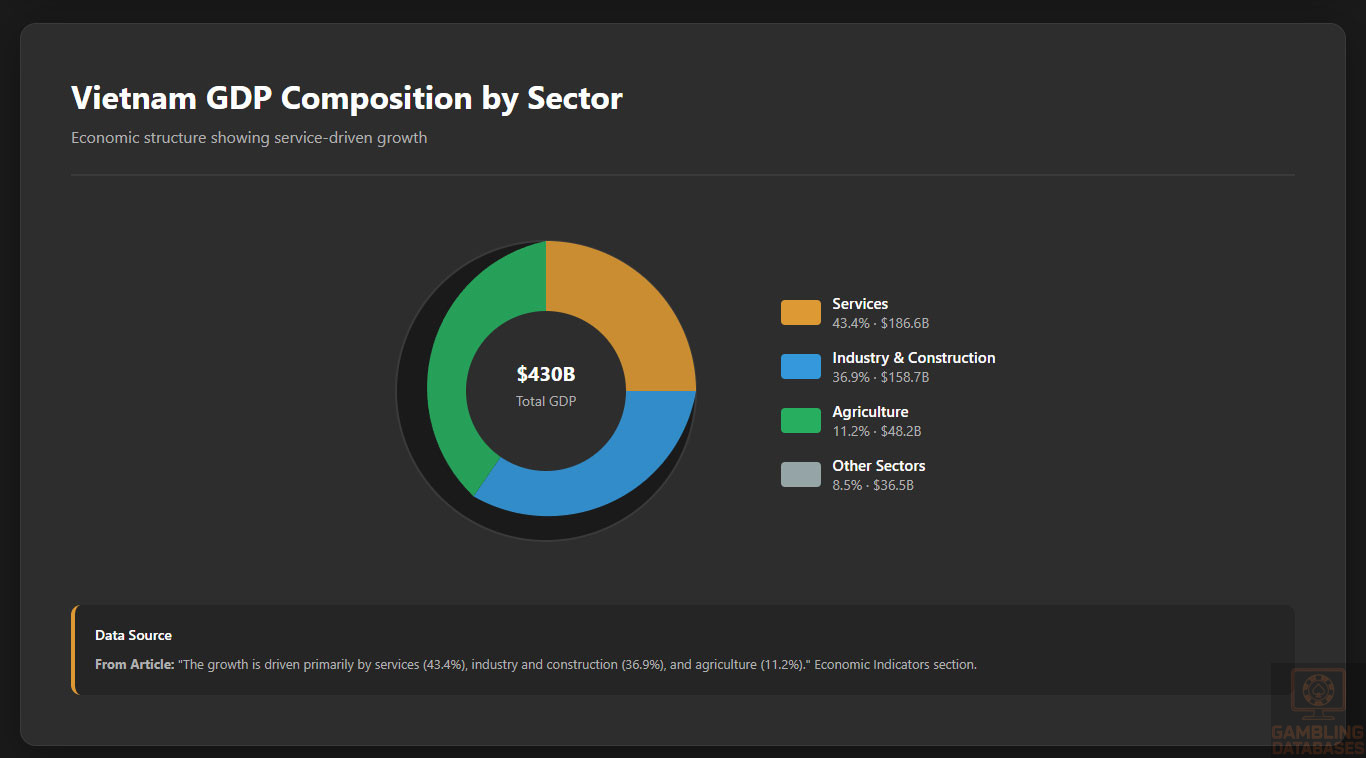

Vietnam’s economy recorded robust performance with a GDP of approximately $430 billion in 2025, growing at a rate exceeding 7.5% in the first half of the year. The growth is driven primarily by services (43.4%), industry and construction (36.9%), and agriculture (11.2%).

Household spending is expected to exceed $138 billion USD in 2025, propelled by increasing disposable incomes and urban consumer demand. Inflation remains moderate around 3.5%, ensuring stable purchasing power, with unemployment low at 2.1%.

Average household income varies widely, with urban centers commanding higher earnings; the national median is around $4,200 USD annually. Patterns show a growing middle class with increased preference for value-based purchases amid cautious consumer sentiment.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $430 billion USD |

| GDP Growth Rate | 7.5% (H1 2025) |

| Inflation Rate | 3.5% |

| Unemployment Rate | 2.1% |

| Average Household Income | $4,200 USD/year |

| Projected Household Spending | $138.5 billion USD |

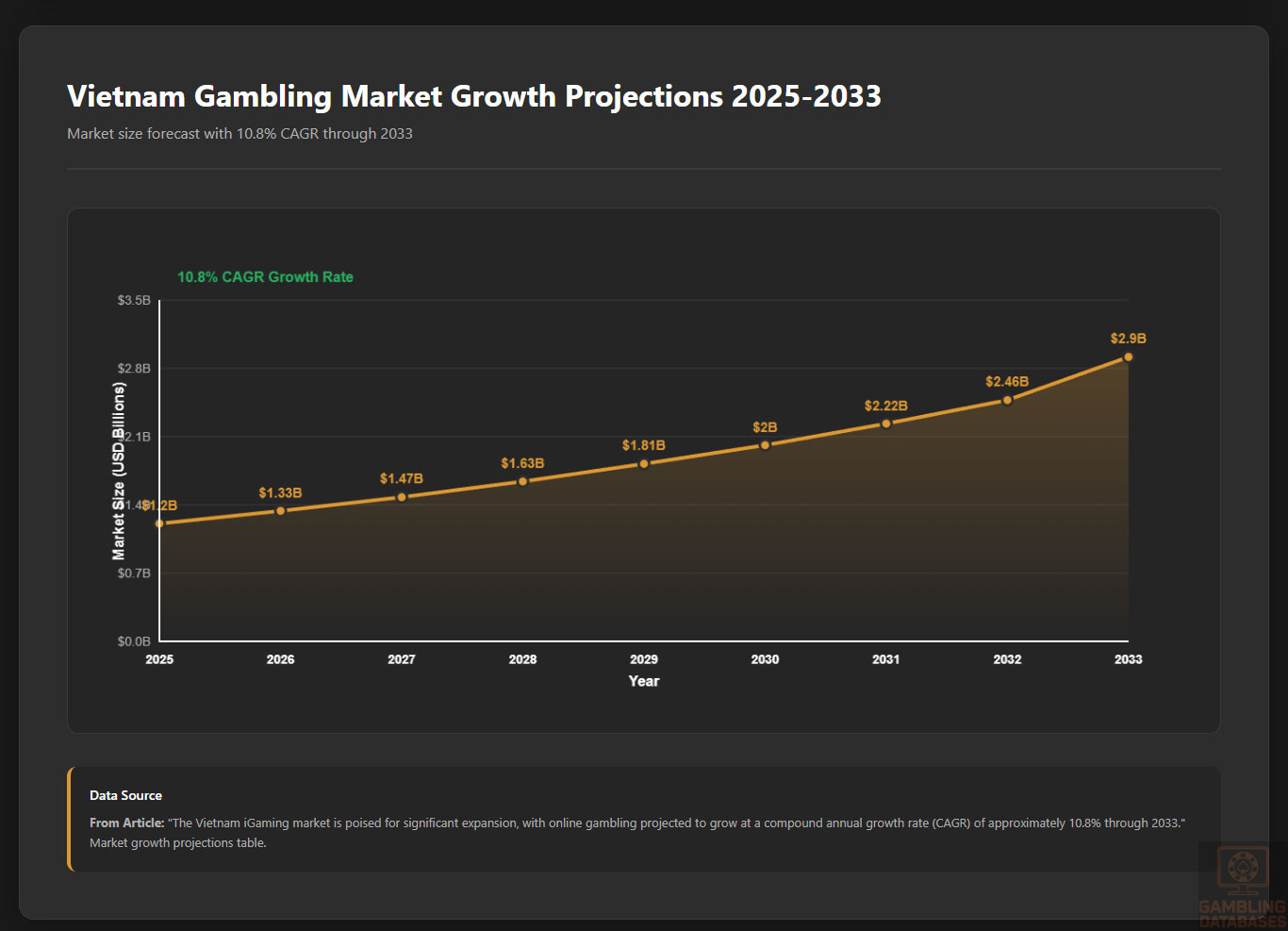

Market Size and Growth Projections

The Vietnam iGaming market is poised for significant expansion, with online gambling projected to grow at a compound annual growth rate (CAGR) of approximately 10.8% through 2033. The total market size of online gambling currently remains nascent but rapidly developing due to increasing internet and mobile penetration.

Offline gambling remains dominant, but online platforms are gaining traction especially in sports betting and casino games like baccarat and slots. Average revenue per user (ARPU) in physical casinos is estimated at around $400 annually, signaling considerable disposable income directed toward gaming activities.

| Year | Market Size (USD Billions) | CAGR |

|---|---|---|

| 2025 | 1.2 | — |

| 2028 (Forecast) | 1.7 | 10.8% |

| 2033 (Forecast) | 2.9 | 10.8% |

Education, Skills, and Digital Literacy

Vietnam boasts a high literacy rate above 95%, with increasingly widespread digital literacy, particularly among the youth and urban populations. Government education reforms and technology initiative programs have raised the quality of ICT (Information and Communication Technology) skills across the workforce.

This digital competence supports rapid adoption of online services, including digital payments and iGaming platforms. Workforce skills are well aligned with the technology sector’s growth, featuring a robust pipeline of IT graduates and trained professionals.

Cultural and Social Factors

Communication and Language

Vietnam’s primary language is Vietnamese, used by over 86% of the population. Several ethnic minority languages coexist across regions, reflecting cultural diversity.

- Vietnamese (majority language)

- Tay

- Thai

- Muong

- Khmer

- Chinese dialects (Hoa minority)

Cultural Attitudes

Gambling is traditionally viewed with skepticism due to social and religious norms anchored in Buddhism and Confucianism, which emphasize social harmony and risk avoidance. However, younger demographics show increasing tolerance influenced by globalization and digital exposure.

Foreign brands in entertainment, including gaming, are cautiously welcomed but face scrutiny to ensure alignment with cultural values and consumer protection. Preference is often given to trusted, secure platforms with strong reputations.

Problem Gambling and Social Considerations

Problem gambling prevalence remains relatively low but is growing, especially with youth engagement via online channels. The government implements social responsibility measures emphasizing prevention and treatment, supported by healthcare institutions and community programs.

- Public awareness campaigns on gambling risks

- Self-exclusion programs in licensed venues

- Mandatory responsible gambling training for operators

- Collaboration with healthcare services for addiction treatment

- Contribution requirements to social welfare funds from operators

Political Structure and Governance

Vietnam is a one-party socialist republic with stable governance and consistent regulatory policies. Political stability facilitates long-term planning for foreign investors despite complex bureaucratic processes. International relations are positive, supporting trade and investment growth, including in regulated gaming sectors.

Technology Adoption and Digital Behavior

Internet and Digital Usage

By early 2025, Vietnam had approximately 79.8 million internet users, representing a penetration rate close to 79%. Mobile subscriptions surpass total population with about 127 million connections, thanks to widespread multi-SIM usage.

Average mobile broadband speeds have steadily increased, with typical download speeds exceeding 75 Mbps, fostering high-quality streaming and interactive online gaming experiences.

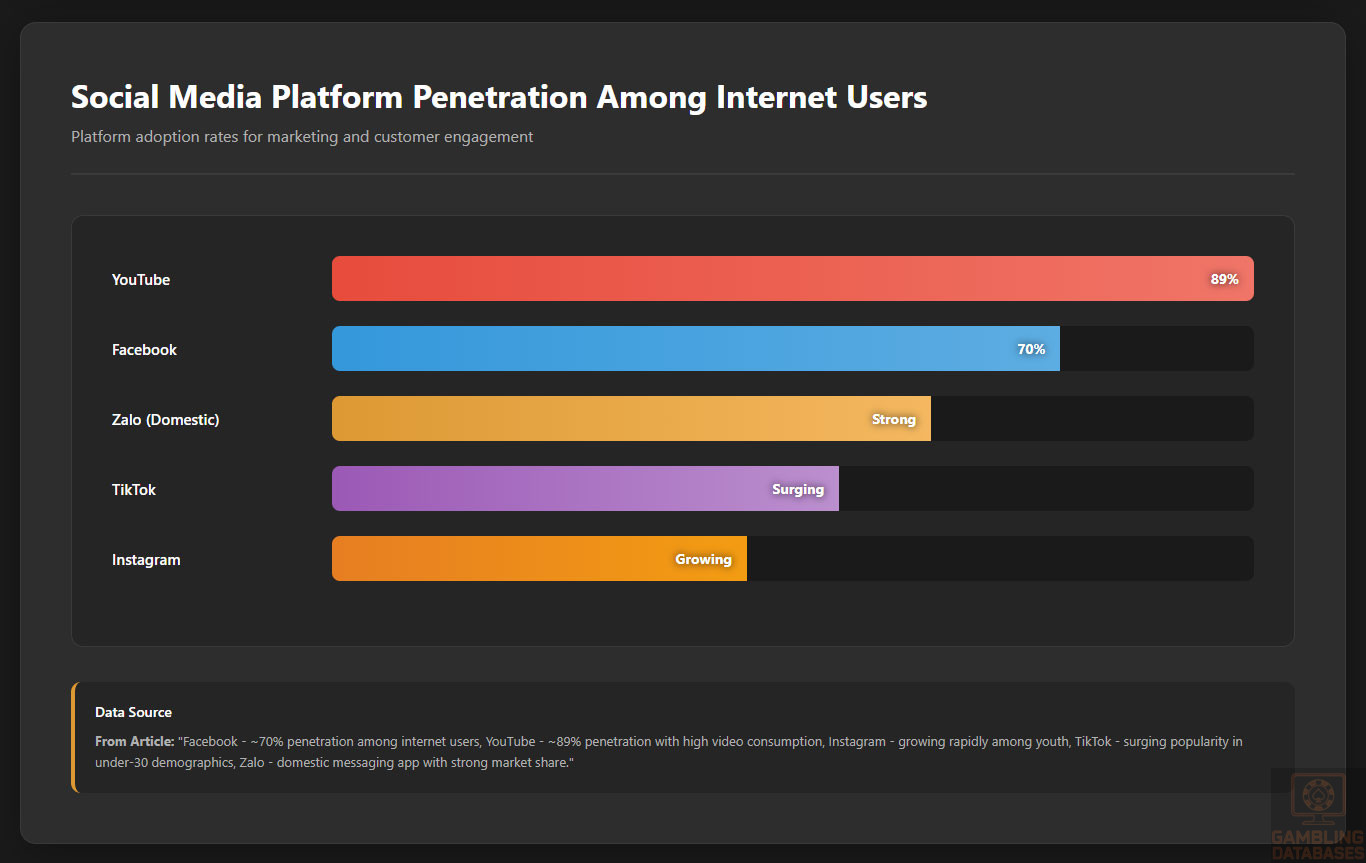

- Facebook – ~70% penetration among internet users

- YouTube – ~89% penetration with high video consumption

- Instagram – growing rapidly among youth

- TikTok – surging popularity in under-30 demographics

- Zalo – domestic messaging app with strong market share

Digital Payment Behavior

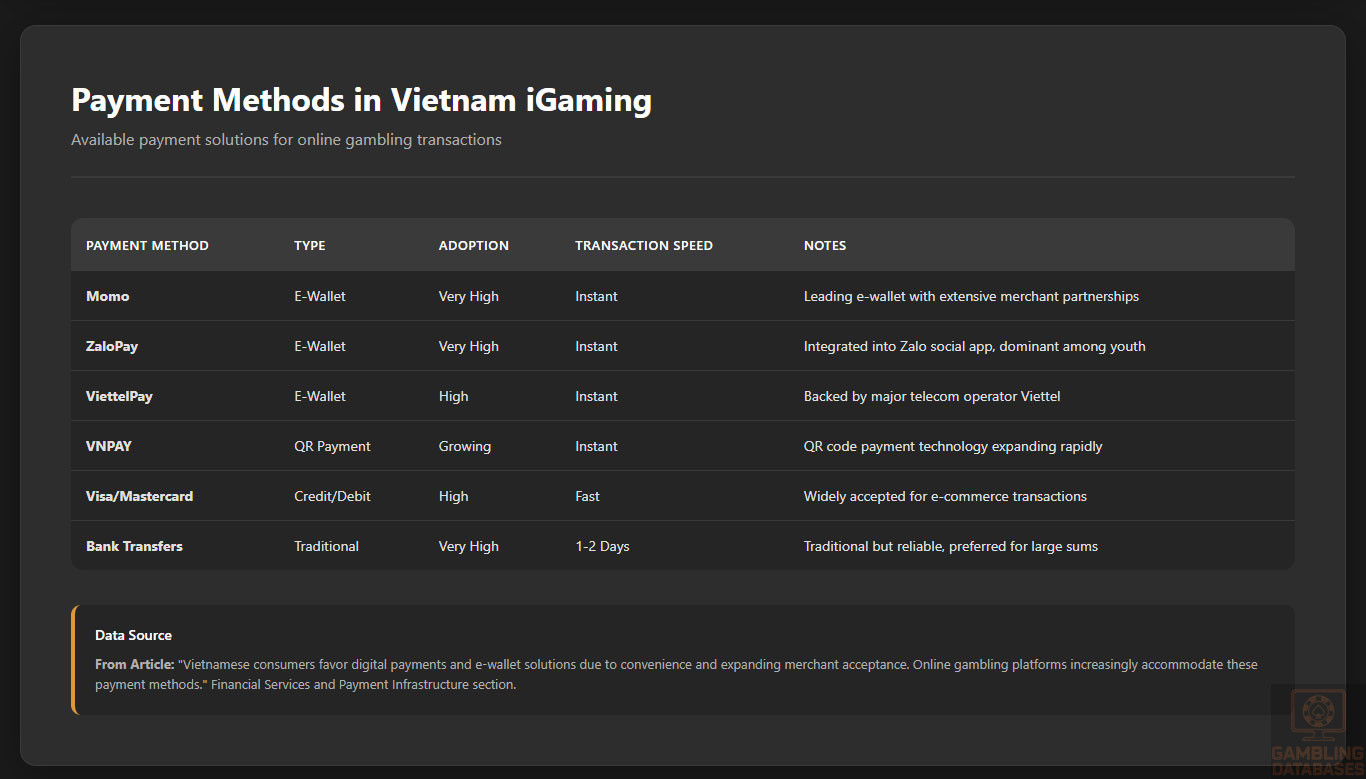

Vietnamese consumers favor digital payments and e-wallet solutions due to convenience and expanding merchant acceptance. Online gambling platforms increasingly accommodate these payment methods, boosting user accessibility.

- Momo e-wallet

- ZaloPay

- ViettelPay

- Bank debit/credit cards (Visa, Mastercard)

- Bank transfers

Gaming and Gambling Preferences

Current Market Participation

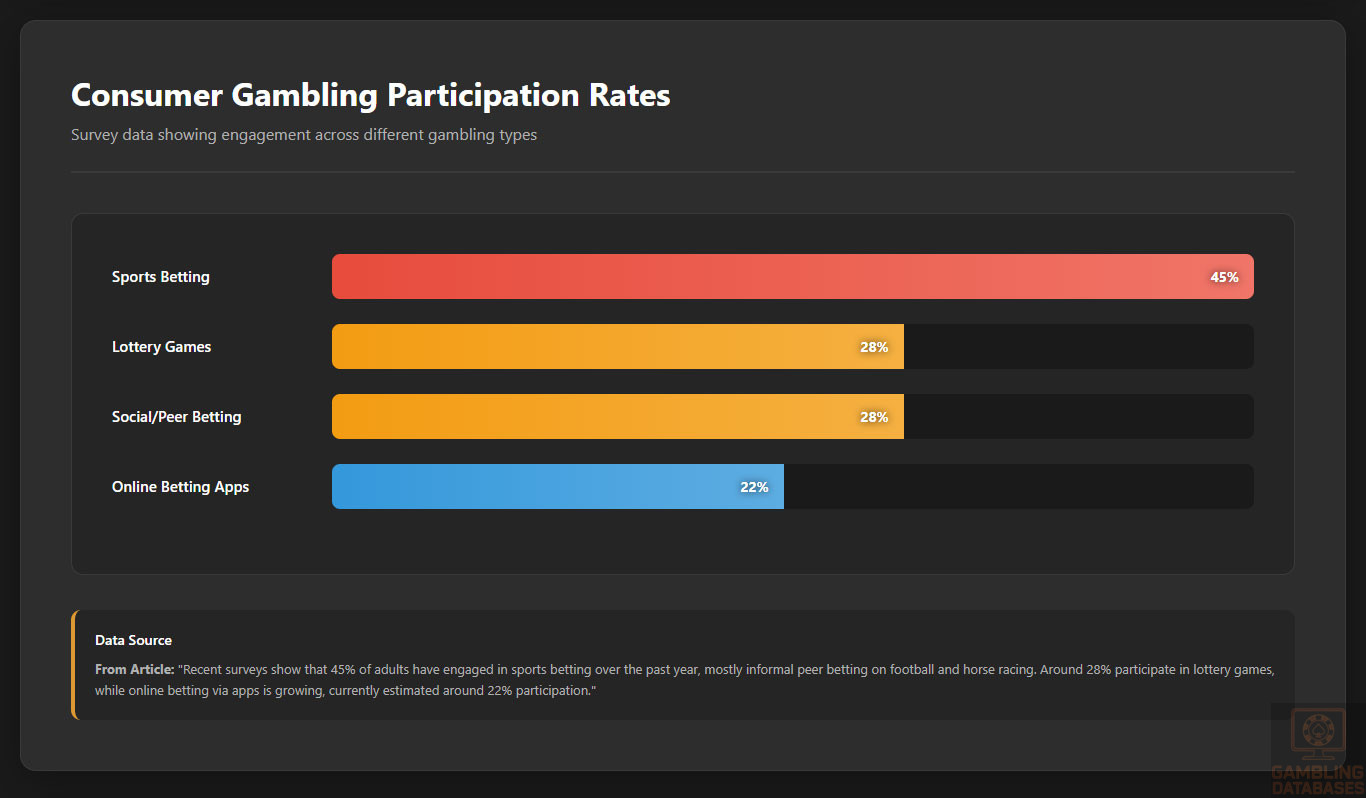

Recent surveys show that 45% of adults have engaged in sports betting over the past year, mostly informal peer betting on football and horse racing. Around 28% participate in lottery games, while online betting via apps is growing, currently estimated around 22% participation.

- Sports betting (informal and online) – 45%

- Lottery and games of chance – 28%

- Social or peer betting – 28%

- Online casino games (live dealers, slots) – increasing rapidly

- Esports betting – emerging segment

Consumer Behavior Patterns

Consumers in Vietnam show a preference for live dealer casino games and real-time sports betting, facilitated by mobile platforms. Peak usage typically occurs during evenings and weekends, with sessions averaging 30-45 minutes. Retention strategies focus on personalized promotions and loyalty rewards.

Spending behavior emphasizes moderate, frequent bets rather than high-stakes gambling, reflecting cautious but engaged consumer profiles aligned with regulatory restrictions and income distribution.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Vietnam boasts robust internet penetration at approximately 79% of the population in 2025, supported by continuous infrastructure investments. Broadband connections primarily concentrate in urban areas, while mobile internet dominates rural connectivity due to geographic challenges.

Average fixed broadband speeds hover around 50 Mbps, with mobile networks delivering speeds up to 35 Mbps on 4G. Network reliability is improving, aided by governmental and private sector initiatives to reduce latency and expand fiber optic coverage nationwide.

Government programs prioritize digital infrastructure expansion in underserved regions, facilitating uniform access to high-speed internet which is critical for online gaming platforms targeting emerging markets across the country.

5G and Future Technology Deployment

As of 2025, 5G coverage exists in major cities such as Hanoi and Ho Chi Minh City, reaching around 30% of the population. Rollout continues rapidly, with projections to reach 60% national coverage by 2027.

Network operators invest heavily in 5G infrastructure to support bandwidth-intensive applications including streaming, cloud gaming, and augmented reality. Plans include integration with IoT ecosystems and smart city initiatives, improving gaming experience quality and operational reliability.

Vietnam’s telecom landscape includes international partnerships accelerating 5G adoption, positioning it as a competitive digital economy within Southeast Asia.

Mobile Technology Ecosystem

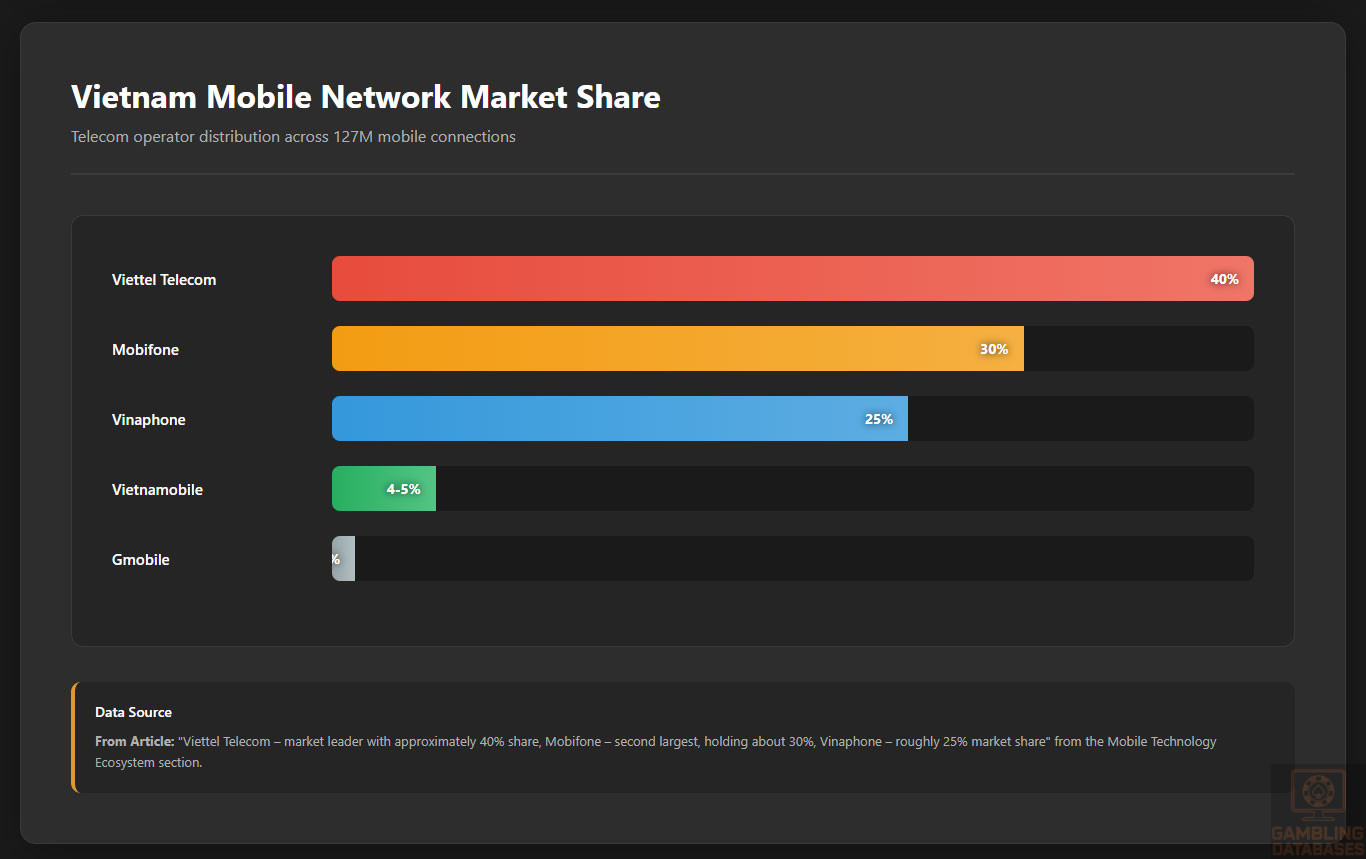

The mobile network market is competitive, composed of a handful of dominant operators serving over 100 million SIM cards, underscoring multi-SIM ownership. Mobile data costs have declined significantly over the past five years, increasing consumer adoption and fostering digital service growth.

- Viettel Telecom – market leader with approximately 40% share

- Mobifone – second largest, holding about 30%

- Vinaphone – roughly 25% market share

- Vietnamobile – smaller player with 4-5% share

- Gmobile – niche operator serving less than 1%

Smartphone adoption exceeds 75% of the population with preference toward mid-range Android devices. Apple products hold premium market segments in urban and affluent consumers. Mobile gaming constitutes a significant share of entertainment apps usage, benefiting from widespread device availability.

Financial Services and Payment Infrastructure

Vietnam’s banking sector is expanding rapidly in digital services, with broad account penetration and mobile banking adoption exceeding 55% of adults. Consumers prefer swift, secure payments supported by robust regulatory frameworks promoting fintech innovation.

- Vietcombank – leading bank with comprehensive digital portfolio

- Techcombank – prominent private bank focusing on SME lending

- VietinBank – state-owned with vast retail network

- MB Bank – strong digital banking innovations

- ACB – major commercial bank with multi-channel services

Payment processing covers credit/debit cards, fast bank transfers, and digital wallets popular among younger consumers. Regulatory efforts emphasize secure e-payments and anti-fraud technologies, essential for iGaming transactions.

- Visa and Mastercard widely accepted for e-commerce

- ZaloPay – dominant local e-wallet with integration into social apps

- Momo – leading rival wallet with extensive merchant partnerships

- VNPAY – growing QR code payment technology

- Bank transfers – traditional but reliable for large sums

E-commerce and Digital Economy

Vietnam’s e-commerce market is booming, valued at over $15 billion in 2025 and growing around 20% annually. Digital consumer trust is rising, facilitated by improved online payment security and logistics infrastructure.

Online services including gaming, entertainment, and content streaming see rapid adoption in urban centers. Government support via digital economy initiatives fuels innovation hubs in Ho Chi Minh City and Hanoi, enriching the business ecosystem for tech-driven gaming ventures.

Business Environment and Regulatory Framework

Vietnam ranks favorably in World Bank ease of doing business reports, with notable improvements in starting a business and registering property. However, regulatory complexity and approval delays occasionally challenge foreign market entrants.

Foreign investment policies have liberalized gradually, allowing 100% foreign ownership in many sectors, including technology and entertainment, though gambling remains tightly regulated within specific parameters.

- Documentation preparation including investment registration certificate (IRC)

- Company registration with Department of Planning and Investment

- Tax registration and obtaining a tax code

- Opening a corporate bank account and fulfilling capital requirements

- Licensing and special permits for restricted sectors (e.g., gambling)

Corporate Structure and Registration

Common business entities include Limited Liability Companies (LLCs), Joint Stock Companies (JSCs), and Branch Offices of foreign firms. LLCs dominate among new entrants due to simplicity and liability protection.

For gambling operations, establishing an LLC with local representation is recommended, ensuring compliance with licensing mandates and tax obligations. Branch offices suit companies seeking limited market presence without full incorporation.

- LLC: Limited liability, flexible management

- JSC: Suitable for larger scale, public funding

- Branch Office: Foreign entity extension with restrictions

- Representative Office: Non-commercial, market research only

- Partnership: Rarely used in regulated sectors

Registration Requirements

Company registration requires substantial documentation and adherence to local laws. Foreign ownership is generally permitted but subject to sector-specific restrictions and approvals.

- Investment Registration Certificate/Application

- Business Registration Certificate

- Articles of Incorporation and company charter

- Proof of legal office address in Vietnam

- Minutes from relevant board/shareholder meetings

- Tax code registration documents

- Bank account opening confirmation

Taxation Framework

Corporate income tax (CIT) standard rate is 20% with preferential rates of 15% or 17% for qualifying SMEs or economically advantaged zones. Tax holidays lasting up to four years apply for investments in special economic zones.

Vietnam has signed double taxation treaties with numerous countries, improving cross-border investment predictability.

- Japan

- South Korea

- Singapore

- France

- Australia

- UK

Personal income tax rates are progressive, ranging from 5% to 35%, with withholding obligations for gambling winnings incorporated under general PIT rules.

Market Entry Considerations

Optimal market entry strategies involve partnerships with local license holders to navigate regulatory complexities. Utilizing established technology platforms customized for compliance and localized language support enhances market acceptance.

- Form joint ventures or strategic partnerships with licensed operators

- Leverage local knowledge for regulatory navigation and marketing

- Deploy mobile-first platforms optimized for Vietnamese consumers

- Utilize multi-channel payment systems catering to local preferences

- Emphasize responsible gambling tools to meet regulatory standards

Initial investment costs are significant, driven by licensing, infrastructure setup, and compliance programs. Timelines from application to operational launch typically span 12 to 18 months.

- Licensing and regulatory approval fees

- Corporate establishment and legal costs

- Technology platform development and localization

- Marketing and promotional budget

- Compliance and auditing expenses

- Initial feasibility study and partner identification (3-6 months)

- Licensing application and government approvals (6-9 months)

- Technology deployment and market testing (3-6 months)

- Official launch and scaling (post-approval)

Key success factors include regulatory compliance, strong local partnerships, culturally tailored marketing, and robust digital infrastructure.

- In-depth understanding of local regulatory environment

- Experienced local operational team

- Flexible technology solutions

- Strong customer service and payment options

- Clear responsible gambling framework

Challenges encompass evolving regulations, high capital intensity, and potential enforcement scrutiny. Entry requires careful risk management and long-term commitment.

- Complex licensing and approval processes

- Stringent compliance and reporting requirements

- Competitive gambling landscape with limited license availability

- Cultural sensitivities around gambling

- High infrastructure and operational costs

Exit strategies depend on license transfer permissions and market liquidity. Regulatory approval is required for ownership changes. Market valuations remain moderate but growing due to expansion prospects.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Vietnam?

Online gambling is largely prohibited under Vietnamese law, especially casino-style and card-based games. However, limited permissions exist for foreigners and specific pilot projects. Regulatory authorities maintain strict surveillance to prevent unlicensed online gambling, making compliance essential for operators. Vietnamese nationals are restricted from most online forms outside regulated environments.

2. What types of gambling licenses are available and what do they cover?

Vietnam issues licenses mainly for land-based casinos, electronic prize games, and limited sports betting. Online gambling licenses are scarce and tightly controlled, requiring Ministry of Finance approval. Licenses cover operational scope, geographic reach, machine limits, and foreign currency transactions. Specialized permits may be required for online platforms targeting foreigners or certain betting formats.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing costs vary widely depending on business scale and scope but involve substantial fees typically in the millions of USD range for large projects. Application timelines range from 12 to 18 months, encompassing multiple government reviews and compliance verifications. Costs include application fees, technical audits, and regulatory contributions. Early planning and local partnerships accelerate the process.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain licenses but must meet rigorous eligibility criteria including local presence and capital requirements. Ownership restrictions may apply, and full compliance with Vietnamese regulations is mandatory. Joint ventures with local partners are common to facilitate licensing and operational integration. Government scrutiny on foreign operators is high due to social policy considerations.

5. What are the tax obligations for iGaming operators?

Operators pay corporate income tax at 20%, with additional gross gaming revenue taxes specific to game types. Licensing fees and turnover taxes complement the tax structure. Operators must comply with reporting and withholding obligations. Preferential tax rates and holidays exist for qualifying enterprises in special zones.

| Tax Type | Rate |

|---|---|

| Corporate Income Tax (standard) | 20% |

| Gross Gaming Revenue Tax (approximate) | 20% for casinos |

| Turnover/License Fees | Variable |

6. Are gambling winnings taxed for players?

Yes, gambling winnings are subject to personal income tax, withheld by operators at standard progressive rates. Thresholds exclude small winnings to reduce administrative burden. Players are responsible for declaring additional income if applicable. The tax system ensures government revenue while promoting responsible gaming.

7. What are the typical operational costs for running an online casino or sportsbook?

Operational costs include licensing and regulatory fees, technology platform expenses, compliance and auditing, staff salaries, marketing, and payment processing fees. Large-scale projects require significant capital for infrastructure and security. Cost efficiency improves with scale and leveraging local partnerships.

- License application and renewal fees

- Technology development and maintenance

- Compliance monitoring and KYC/AML systems

- Marketing and player acquisition expenses

- Employee compensation and training

8. What is the expected ROI timeline for entering this market?

Return on investment generally spans 3 to 5 years, influenced by regulatory approvals, market penetration, and operational execution. Early entrants benefit from first-mover advantages but face initial compliance and education costs. Long-term profitability depends on adapting to evolving regulations and consumer trends.

9. What are the local presence requirements for operators?

Operators must establish physical offices in Vietnam, maintain local staff, and comply with local business laws. Online operations require Vietnamese-registered domains and local server hosting. Regulatory authorities mandate transparent management and onsite compliance officers, reinforcing control and responsiveness.

10. What payment methods are available and recommended?

A broad array of payment options is supported, with dominance of local e-wallets like ZaloPay and Momo, bank transfers, and credit/debit cards. Integration with popular mobile wallets improves customer experience and conversion rates. Cryptocurrency remains niche but strategically emerging.

- ZaloPay and Momo – leading wallets with deep market penetration

- Bank transfers – reliable for larger transactions

- Visa/Mastercard – accepted extensively online

- QR Code payments via VNPAY

- Cryptocurrency – limited but increasing uptake

11. What are the advertising and marketing restrictions?

Advertising is highly regulated, with bans on targeting minors and vulnerable groups. Gambling promotion is limited to licensed venues and authorized media. Content must emphasize responsible gaming and avoid misleading claims. Certain time restrictions apply on broadcast advertising to reduce exposure to unintended audiences.

12. What responsible gambling measures are mandatory?

Operators must implement strong player protection tools including age verification, self-exclusion options, and play time limits. Regular audits for compliance and public education initiatives further support social responsibility mandates. Data on gambling behavior must be monitored to detect and prevent problem gambling early.

- Age verification enforced at registration

- Self-exclusion and cooling-off periods

- Limits on betting amounts and frequency

- Regular compliance reporting to regulators

- Player education and support resources

13. How large is the iGaming market and what is the growth potential?

The iGaming market is estimated at over $1 billion in annual wagers with strong growth potential due to untapped online sectors and expanding middle class. Regulatory easing and technological improvements underpin forecasts of 7-10% CAGR. Urban digital engagement drives digital gambling adoption.

14. Who are the main competitors and what is their market share?

Market competition centers on a few large casino operators dominating land-based revenues. Online space sees emerging licensed operators and foreign entrants under partnership models. Market concentration remains high, with limited licenses constraining new entrants.

15. What are the player preferences and typical spending patterns?

Players prefer mobile-compatible platforms with localized content and support. Sports betting and lottery are most popular, with casino games gaining traction among tourists and high-income locals. Session lengths are short but frequent, accentuated by social features.

16. What are the key success factors and main challenges for new entrants?

Success requires deep regulatory understanding, trusted local partnerships, effective digital marketing, and robust responsible gambling programs. Challenges include navigating complex licensing, high capital requirements, and social sensitivities towards gambling. Infrastructure investment and cultural integration remain vital.

- Strong compliance and legal expertise

- Local market knowledge and relationships

- Flexible and scalable technology platforms

- Responsible gambling integration

- Effective user acquisition and retention strategies

- Regulatory uncertainty and changes

- High initial and ongoing operational costs

- Limited license availability

- Cultural attitudes towards gambling

- Enforcement scrutiny and risk management

Sources and References

- VietnamGambling Regulatory Authority – Official Website – https://legalpilot.com/country/vietnam/

- Ministry of Finance Vietnam – Regulatory Guidelines – https://mofi.gov.vn/

- National Statistical Office of Vietnam – Population and Economic Data 2025 – https://www.nso.gov.vn/en/population/

- World Bank – Doing Business Report 2025 – https://www.worldbank.org/en/programs/business-enabling-environment

- International Telecommunication Union – ICT Statistics 2025 – https://www.itu.int/en/ITU-D/Statistics/

- Vietnam Digital 2025 Report – DataReportal – https://datareportal.com/reports/digital-2025-vietnam

- Statista – Internet Usage in Vietnam – https://www.statista.com/topics/6231/internet-usage-in-vietnam/

- IMARC Group – Vietnam Online Gambling Market Report 2025 – https://www.imarcgroup.com/vietnam-online-gambling-market

- TGM Research – Gambling and Sports Betting Survey Vietnam 2022 – https://tgmresearch.com

- Worldometers – Vietnam Population Data 2025 – https://www.worldometers.info/world-population/vietnam-population/

- Vietnam Ministry of Public Security – Enforcement Reports 2025

- Vietnam National Bank – Financial and Payment Systems Data 2025 – https://www.sbv.gov.vn

- Vietnam Ministry of Planning and Investment – Investment Laws 2025 – https://mpi.gov.vn

- Vietnam Tax Authority – Corporate and Personal Tax Guidelines 2025

- Vietnamese Telecom Operators – Market Reports 2025

- Vietnam Economic Times – Business Environment Report 2025

- Gambling Industry Insights – Industry Analysis 2024-2025

- Academic Studies on Gambling Attitudes in Vietnam – PMC Articles

- Gaming Industry Reports – Market Share and Competitive Analysis 2025

- Vietnam News Agency – Regulatory and Market Updates 2025

- Vietnam Briefing – Economic and Regulatory News 2025

- International Monetary Fund – Vietnam Country Report 2025

- Vietnam Ministry of Culture, Sports and Tourism – Gambling Policy Updates

- Vietnam Internet Society – Digital Literacy and Penetration Reports

- Vietnam Legal Updates and Decree Publications

- Vietnam Investment Review – Foreign Business Entry 2025

- Vietnam Social Media Trends 2025 – Vector Group Report

- Vietnam Banking Sector Annual Report 2025

- Vietnam E-commerce Association – Market Insights 2025

- Vietnam Ministry of Health – Public Programs for Gambling Awareness

- Vietnam Telecommunications Authority – 5G Deployment Plan 2025

- Vietnam Digital Payment Landscape Reports 2025

🎯 Gambling Databases Country Rating: Vietnam

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 0.5/10 | ⛔️ Prohibitive |

| Player Access Score | 3.0/10 | 🔴 Severely Restricted |

| Overall Market Attractiveness | 1.8/10 | ⛔️ One of Asia’s Most Restrictive Markets – Avoid Unless Pursuing Land-Based Casino License |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- ALL ONLINE CASINO AND CARD-BASED GAMBLING IS COMPLETELY PROHIBITED under Decree 147/2024 – This is not a grey area, this is an explicit nationwide ban

- ACTIVE ISP BLOCKING: Vietnamese authorities enforce online gambling bans through website blocking and payment processing restrictions

- CAPITAL BARRIER: Minimum VND 500 billion (~$21 MILLION USD) charter capital required – one of the highest in Southeast Asia, making entry impossible for small/medium operators

- ENFORCEMENT INTENSIFIED: Regulatory inspections and investigations have increased significantly since 2023 with harsh penalties for unlicensed operations including criminal prosecution

- OFFSHORE OPERATORS: Operating without a Vietnamese license subjects you to asset seizure, fines, criminal prosecution, and potential extradition under international cooperation agreements

- EXTREME LOCAL RESTRICTIONS: Even for licensed land-based casinos, Vietnamese citizens can only enter if 21+ years old AND earning $400+ monthly income AND paying entrance fees – this eliminates most of the domestic market

- LIMITED LICENSES: Vietnamese government issues very few gambling licenses with strict caps on slot machines (one per five hotel rooms) and operational scale

- REGULATORY UNCERTAINTY: Laws changed significantly in 2021-2024 period, with ongoing pilot program reviews potentially leading to further restrictions

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | -0.5/3.0 | Started at partial legality (+1.5 for limited land-based casino access). MASSIVE DEDUCTION: Online casino-style and card-based games completely prohibited under Decree 147/2024 (-1.5 points). Active enforcement with ISP blocking and criminal penalties (-0.5 points). Only a handful of land-based casinos allowed with extreme entry restrictions for Vietnamese citizens (21+, $400+ monthly income, entrance fees). Foreign tourists have easier access but this severely limits market potential. Final: -0.5/3.0 |

| Licensing Process | 25% | -0.5/2.5 | Started at extremely limited licensing (+0.5 for complex process taking 12-18 months with Ministry of Finance as sole authority). CRITICAL DEDUCTION: Minimum charter capital requirement of VND 500 billion (~$21 MILLION USD), increased from VND 200 billion – this is over €500k threshold (-0.25 points). Multi-stage application with undisclosed fees but involving extensive documentation, audited financials, technical certifications, background checks, compliance systems (-0.25 points for extreme complexity). High legal and consulting costs easily exceeding €200k given regulatory complexity (-0.5 points). Foreign ownership allowed but subject to intense scrutiny. Very few licenses ever issued. Final: -0.5/2.5 |

| Taxation & Costs | 20% | 1.0/2.0 | Started at GGR tax approximately 20% for casino table games (+1.5 points for being in 15-25% range). Corporate income tax (CIT) standard rate 20%, with potential preferential rates of 15-17% for qualifying SMEs. Total effective tax rate approximately 35-40% when combining GGR and corporate taxes (0 additional deductions as not exceeding 50%). However, MAJOR DEDUCTION for extreme operational costs: $21M minimum capital requirement locked up, extensive compliance infrastructure including 24/7 surveillance with 180-day video retention, dedicated compliance officers, monthly/quarterly reporting, certified audits (-0.5 points). Slot machines subject to both fixed monthly fees and machine number caps adding cost complexity. Final: 1.0/2.0 |

| Operational Requirements | 15% | -0.5/1.5 | Started at 0 points for excessive requirements: Mandatory physical registered office in Vietnam, locally hosted domain names, trained management staff with 3+ years gambling experience, 24/7 surveillance systems, dedicated compliance officers, extensive KYC/AML infrastructure. CRITICAL DEDUCTION: Large capital requirement of VND 500 billion (~$21 million) held as charter capital (-0.25 points). Complex multi-stage compliance including monthly GGR reporting, quarterly financial audits, annual license renewals, suspicious transaction monitoring, player protection systems (-0.25 points). Foreign ownership allowed but requires regulatory approval and local partnerships recommended for navigation. Cannot operate remotely – substantial physical presence mandatory. Final: -0.5/1.5 |

| Market Environment | 10% | -0.25/1.0 | Started at moderate business environment (+0.5 points – Vietnam improving in World Bank rankings but still faces bureaucratic complexity). SEVERE DEDUCTION for advertising restrictions: Gambling advertising heavily restricted, limited to licensed premises and approved media, cannot target under-18, requires government approval before release, prohibited from misleading claims, time restrictions on broadcast (-0.5 points). MAJOR DEDUCTION for regulatory instability: Decree 147/2024 banned online casino games, Decree 121/2022 tightened electronic gambling, pilot programs under ongoing review as of late 2025, government considering expanded oversight – frequent law changes create uncertainty (-0.25 points). Enforcement has intensified since 2023 with increased inspections and investigations. Cultural sensitivities around gambling persist despite gradual liberalization. Final: -0.25/1.0 |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 0.5/4.0 | Started at partially legal (+2.0 for limited legal access to land-based casinos). However, MASSIVE PROHIBITION: Online casino-style games, card-based online games, and online sports betting completely banned nationwide (-1.5 points). Vietnamese citizens face extreme restrictions even for legal land-based casinos: must be 21+ years old, demonstrate minimum $400 monthly income (excluding most Vietnamese whose median income is lower), pay significant entrance fees. Only foreigners and overseas Vietnamese with valid visas can participate in e-gambling under extremely limited licensed operations. Most Vietnamese population effectively excluded from legal gambling. Players using offshore sites face legal risks and enforcement actions. Final: 0.5/4.0 |

| Practical Accessibility | 30% | 1.0/3.0 | Started at some payment methods available (+2.0): E-wallets like Momo, ZaloPay, ViettelPay popular; bank transfers via Visa/Mastercard; VNPAY QR codes. However, CRITICAL DEDUCTIONS: Active ISP blocking of unauthorized gambling websites enforced by Ministry of Public Security and regional authorities (-0.5 points). Payment processing restricted for online gambling transactions with monitoring by State Bank of Vietnam and financial authorities (-0.5 points). While cryptocurrency not explicitly banned for all transactions, heavily restricted for gambling purposes. VPN usage common but adds friction and legal grey area for accessing blocked offshore sites. Mobile penetration 110% and internet penetration 73% provide technical infrastructure, but regulatory barriers prevent practical access to most online gambling. Final: 1.0/3.0 |

| Player Penalties | 20% | 1.0/2.0 | Players participating in illegal gambling activities face fines under Vietnamese law (+1.0 point for fines possible, not criminal penalties). Enforcement focuses primarily on operators rather than individual players, but players are not exempt from penalties. Administrative fines can be imposed for using unlicensed gambling services. Social stigma exists due to traditional Buddhist and Confucian values emphasizing risk avoidance. Government implements problem gambling prevention measures including public awareness campaigns and self-exclusion programs. Players using offshore sites technically violate regulations but enforcement against individual players less aggressive than against operators. Final: 1.0/2.0 |

| Market Availability | 10% | 0.5/1.0 | Very limited licensed operators available (+0.5 point for 1 licensed operator tier): Only a handful of land-based casinos operating under government licenses, concentrated in resort areas like Phu Quoc and Ho Tram. These primarily serve foreign tourists with limited Vietnamese citizen access. No licensed online casino operators – online casino gaming completely prohibited. Market share highly concentrated among few flagship operators like Corona Resort & Casino. Offshore operators actively blocked, though some Vietnamese players access via VPNs despite risks. Total legal market estimated above $1 billion annually but almost entirely land-based and tourist-focused. Final: 0.5/1.0 |

🔍 Key Highlights

Strengths (Very Limited)

- Large Population Base: 102.5 million people with median age 33.4 years provides theoretical market size, though most are legally excluded from participation

- Strong Economic Growth: 7.5% GDP growth in H1 2025, rising middle class with household spending exceeding $138 billion, creating potential future demand if regulations liberalize

- Excellent Digital Infrastructure: 79% internet penetration, 110% mobile penetration, average mobile speeds 75+ Mbps, 5G expanding to 30% coverage – technical infrastructure ready for online gaming if legalized

- Payment Infrastructure: Robust e-wallet adoption (Momo, ZaloPay, ViettelPay), 55%+ mobile banking adoption, growing digital payment comfort among consumers

- Tax Rates Moderate Compared to Capital Requirements: 20% GGR tax and 20% corporate tax are reasonable compared to Western markets, though overshadowed by massive capital requirements

- Pilot Programs Showing Gradual Opening: Since 2017 pilot allowing Vietnamese citizens casino access (albeit restricted) suggests government considering controlled liberalization

⛔️ CRITICAL RISKS AND CHALLENGES

- [Product Prohibitions – MARKET KILLER:] Online casino-style gaming, card-based online games, and online sports betting COMPLETELY BANNED under Decree 147/2024. This eliminates 70-80% of typical iGaming revenue. Only land-based casinos for restricted demographics allowed. This is not a grey area – it is explicit nationwide prohibition with active enforcement.

- [Enforcement Actions – ACTIVE AND AGGRESSIVE:] Government intensified inspections and investigations since 2023. ISP blocking of unauthorized sites actively enforced. Criminal prosecution possible for unlicensed operators including asset seizure. Ministry of Public Security and regional authorities coordinate enforcement. Penalties include fines, license revocation, and criminal charges. Zero tolerance policy toward offshore operators.

- [Financial Barriers – PROHIBITIVE FOR MOST:] VND 500 billion (~$21 MILLION USD) minimum charter capital – increased from VND 200 billion, showing government raising entry barriers. This is among the highest in Southeast Asia, effectively limiting market to major international casino resort developers only. Small and medium operators completely priced out. Add licensing fees (undisclosed but substantial), legal costs (easily €200k+), infrastructure costs (24/7 surveillance, compliance systems), and 12-18 month timeline. Total initial investment likely $25-30M+ before seeing revenue.

- [Customer Restrictions – ELIMINATES DOMESTIC MARKET:] Vietnamese citizens face triple barrier: Must be 21+ years old AND demonstrate $400+ monthly income (median national income only $4,200/year = $350/month, excluding majority of population) AND pay significant entrance fees. Only ~30-40% of Vietnamese adults theoretically eligible, far fewer actually qualify financially. This forces operators to rely almost entirely on foreign tourist market, severely limiting revenue potential and making Vietnam-based operations economically challenging.

- [Payment Restrictions – TRANSACTION FRICTION:] While e-wallets exist, payment processing for online gambling heavily monitored and restricted. State Bank of Vietnam oversees foreign currency transactions requiring sub-licenses. Cryptocurrency effectively banned for gambling. Financial transaction monitoring extensive with suspicious activity reporting mandatory. This creates processing challenges and limits payment options even for legal land-based operations.

- [Advertising Limits – CUSTOMER ACQUISITION NIGHTMARE:] Gambling advertising restricted to licensed premises and approved media only. Cannot target under-18 populations (reasonable but limits channels). Requires government pre-approval. Time restrictions on broadcasts. Content must emphasize social responsibility. No digital marketing to Vietnamese citizens for online products (since online banned anyway). High customer acquisition costs estimated ~$400 per active casino player, though data limited due to small legal market.

- [Operational Complexity – OVERWHELMING COMPLIANCE:] Mandatory physical presence with registered office. Locally hosted domains required. Management must have 3+ years gambling experience. 24/7 surveillance with 180-day video retention. Dedicated compliance officers. Monthly GGR reports. Quarterly certified audits. Annual license renewals. Suspicious transaction monitoring. KYC/AML systems. Player protection measures. Self-exclusion infrastructure. Playtime limits. Age verification. All this creates massive ongoing operational costs making profitability difficult even with license.

- [Regulatory Instability – MOVING TARGETS:] Decree 147/2024 banned online casinos. Decree 121/2022 tightened electronic gambling. Capital requirements doubled from VND 200B to 500B. Pilot programs under ongoing review in late 2025 with uncertain outcomes. Government considering creating dedicated gaming authority and modernizing frameworks, but direction unclear. Frequent law changes create planning uncertainty and compliance costs. Risk of further restrictions or sudden license revocations.

- [Competition – MARKET CONCENTRATION:] Very few licenses issued, creating oligopoly among large resort casino operators. New entrants face established players with government relationships and proven track records. Market share concentrated in Phu Quoc and Ho Tram flagship properties. Competing against major international brands with deep pockets. Slot machine caps (one per five hotel rooms) limit scale even for licensed operators.

- [Cultural Opposition – SOCIAL RESISTANCE:] Traditional Buddhist and Confucian values emphasize social harmony and risk avoidance, creating negative cultural attitudes toward gambling. Government prioritizes social protection over gambling revenue. Problem gambling, though currently low, concerns policymakers. Public perception challenges marketing and normalization efforts. Stigma attached to gambling participation reducing addressable market.

Player-Specific Issues

- Vietnamese Citizens CANNOT Legally Access: Online casinos, online card games, online sports betting, most online gambling products – complete prohibition

- Even Legal Land-Based Casinos Exclude Most: $400 monthly income requirement eliminates majority of population; 21+ age limit; entrance fees; limited number of venues concentrated in tourist areas far from most cities

- ISP Blocking Active: Government blocks offshore gambling sites; VPN required for access creating friction and legal grey area; blocks updated regularly

- Payment Processing Restricted: E-wallets and banks monitor gambling transactions; cryptocurrency effectively banned; international payment processing difficult; limits deposit/withdrawal options

- Legal Risks for Players: Using offshore unlicensed sites subjects players to potential fines (though enforcement focuses on operators); administrative penalties possible; social stigma attached to illegal gambling participation

- Limited Game Selection: Only land-based casino games available legally; no online poker, sports betting, casino games, fantasy sports, esports betting, or other popular iGaming products

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $25-30 million USD minimum (VND 500B charter capital + licensing + infrastructure + legal fees + compliance systems + operational setup over 12-18 months)

Monthly Operating Costs: $500,000-1,000,000+ USD (compliance staff, surveillance systems, audits, reporting, marketing restricted by ad bans, customer service, payment processing, regulatory fees, physical premises)

Effective Tax Rate on Revenue: Approximately 35-40% total (20% GGR tax + 20% corporate income tax on remaining profits, though tiered rates available for qualifying SMEs at 15-17%)

Customer Acquisition Cost: ~$400 per active casino player based on limited land-based market data (likely higher for new entrants without established brand; advertising restrictions severely limit marketing channels driving up CAC)

Time to Breakeven: 5-7 years minimum for large-scale resort casino operations, assuming successful execution and stable regulations (most operators will never break even given capital intensity and market restrictions)

Time to Positive ROI: 7-10+ years for operators who successfully scale and maintain operations (unrealistic for most market entrants; only viable for operators with 10+ year strategic horizon)

Profitability Assessment: ECONOMICS ARE PROHIBITIVE FOR 95%+ OF POTENTIAL OPERATORS. The combination of $21M+ locked capital, 12-18 month licensing timeline, online casino prohibition eliminating 70-80% of typical iGaming revenue, customer restrictions excluding most Vietnamese from legal participation (forcing reliance on volatile tourist market), $500k+ monthly operational costs, advertising restrictions, and regulatory instability creates one of the world’s most challenging gambling markets. Only viable for major international resort developers with $50M+ total capital, established casino brands, ability to attract foreign tourists at scale, and willingness to accept 7-10 year payback periods.

Unless you are Caesars Entertainment, MGM Resorts, or Melco Resorts-level operator with integrated resort development expertise, this market will destroy your capital. Even then, returns will be modest compared to more accessible markets. Small and medium operators have ZERO chance of profitability. Strongly recommend pursuing almost any other Southeast Asian market instead – Philippines, Cambodia, even Myanmar offer better economics.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators (Unlicensed) | 🔴 CRITICAL | ISP blocking actively enforced making market access nearly impossible. Payment processors monitored and blocked. Criminal prosecution possible under Vietnamese law with penalties including fines up to millions of dollars, asset seizure of any Vietnam-based holdings, and criminal charges against executives. Intensified enforcement since 2023. Cooperation with international authorities on cross-border gambling crimes. Zero tolerance policy. DO NOT ATTEMPT UNLICENSED OPERATION. |

| Licensed Land-Based Casino Operators | 🟡 MEDIUM-HIGH | While legal, operators face: Extreme capital requirements ($21M locked), product restrictions (no online offerings), customer restrictions (most Vietnamese excluded), heavy compliance burden (24/7 surveillance, monthly reporting, quarterly audits, annual renewals), advertising restrictions limiting marketing, slot machine caps, regulatory instability with frequent law changes, risk of license revocation for compliance breaches, ongoing operational costs $500k+ monthly. Profitability challenging even with license. Regulatory scrutiny intense. |

| Affiliates/Advertisers (Promoting Offshore Sites) | 🔴 HIGH | Advertising unauthorized gambling services prohibited. ISP blocking extends to affiliate sites promoting offshore casinos. Payment processor termination for affiliate accounts receiving gambling commissions. Potential fines and legal action for promoting illegal gambling operations. Government approval required for all gambling advertising content. Risk extends to influencers, streamers, and content creators. Social media monitoring active. Avoid promoting any unlicensed gambling to Vietnamese users. |

| Payment Processors | 🔴 HIGH | State Bank of Vietnam oversees all foreign currency transactions requiring sub-licenses. Financial institutions face: License revocation for processing illegal gambling transactions, regulatory fines for compliance failures, mandatory suspicious transaction reporting with penalties for non-compliance, AML/KYC violations carry severe penalties, cryptocurrency processors face additional scrutiny. Banks and e-wallet providers (Momo, ZaloPay, etc.) required to block gambling transactions except for licensed operators. Monitoring extensive. |

| Company Directors/Executives | 🟡 MEDIUM-HIGH | Personal liability for corporate violations possible under Vietnamese law. Criminal background checks required for licensing. Directors of unlicensed operations face: Criminal prosecution risk, asset seizure, travel restrictions if charged, difficulty obtaining visas for Vietnam or partnering countries. International cooperation on gambling crimes exists though extradition less common than Western countries. Executives of licensed operators face: Regulatory scrutiny of personal conduct, responsibility for compliance failures, potential personal fines for corporate violations. Reputation risk in conservative Vietnamese business environment. |

🚨 Extradition and International Enforcement

Extradition Treaties: Vietnam has limited extradition agreements compared to Western nations, but maintains cooperation frameworks with: China, Laos, Cambodia, Thailand (ASEAN partners), South Korea (limited cooperation), Australia (limited cooperation). Vietnam does NOT have comprehensive extradition treaties with USA, UK, EU members, Canada making international prosecution less likely than markets like Australia.

Enforcement History: Vietnam focuses enforcement resources on domestic operators and high-profile cases within Southeast Asia. Limited history of pursuing international gambling operators outside Vietnam’s borders. However, cooperation with Chinese authorities on cross-border gambling operations has increased since 2020, particularly targeting operations serving Chinese citizens. Vietnamese enforcement primarily uses ISP blocking, payment blocking, and asset seizure rather than international extradition.

Safe Jurisdictions: Operators based in Russia, most CIS countries, many Caribbean nations, and some Latin American countries face minimal extradition risk. However, assets and operations within Vietnam or ASEAN region remain vulnerable to enforcement. Travel to Vietnam, China, Cambodia, Thailand, Laos carries risk for executives of unlicensed operations.

Travel Risk: LOW to MEDIUM for unlicensed operators based outside Vietnam – Vietnamese authorities focus on domestic enforcement and regional cooperation rather than pursuing international arrests. However, executives should avoid: Vietnam (obvious risk), China (strong cooperation with Vietnam on gambling enforcement), Cambodia and Laos (ASEAN cooperation). Travel through major international hubs like Singapore, Hong Kong, South Korea carries minimal risk but some monitoring possible. Overall international enforcement risk lower than markets like USA, UK, Australia where aggressive cross-border prosecution common.

📋 Final Verdict

Vietnam receives an Operator Ease Score of 0.5/10 and a Player Access Score of 3.0/10, resulting in an overall market attractiveness rating of 1.8/10.

HONEST ASSESSMENT: Vietnam represents one of Southeast Asia’s most restrictive and economically prohibitive gambling markets, suitable only for major international resort developers with $50M+ capital and 10+ year investment horizons. The complete prohibition of online casino gaming, $21M minimum capital requirement, severe restrictions on Vietnamese citizen participation (eliminating most domestic market), 12-18 month licensing timelines, and regulatory instability create insurmountable barriers for 95%+ of potential operators.

Even licensed operators struggle with profitability given operational costs exceeding $500k monthly, advertising restrictions, customer limitations, and reliance on volatile tourist markets. Unless you are building a $200M+ integrated resort comparable to Marina Bay Sands and can wait 7-10 years for returns, avoid this market entirely. Your capital will generate far superior returns in the Philippines, Cambodia, Japan, or even most Western regulated markets.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- Major International Casino Resort Developer with minimum $50M total capital, established brand (Caesars, MGM, Melco, Las Vegas Sands level), and proven track record developing integrated resort properties

- Focused Exclusively on Land-Based Casino Resort Operations targeting foreign tourists and high-net-worth Vietnamese who meet $400+ monthly income requirements – absolutely NO online casino products permitted

- Willing to Accept 7-10+ Year Investment Horizon with patient capital and no expectation of profits before year 5-7, understanding Vietnamese market requires long-term commitment

- Capable of Operating in Resort Destination Markets like Phu Quoc or coastal areas where tourism infrastructure supports foreign visitor volumes necessary for profitability

- Experienced Navigating Complex Asian Regulatory Environments with legal teams capable of managing Ministry of Finance relationships, extensive compliance requirements, and evolving pilot programs

- Able to Invest in Massive Compliance Infrastructure including 24/7 surveillance, dedicated compliance teams, monthly/quarterly reporting systems, certified annual audits

❌ Definitely Avoid If You Are:

- ANY Online Casino Operator or iGaming Platform – online casino gaming, card-based games, and online sports betting COMPLETELY ILLEGAL with active enforcement and ISP blocking (eliminates 70-80% of typical iGaming revenue)

- Offshore Operator Without Vietnamese License – ISP blocking active, payment processing impossible, criminal prosecution risk, asset seizure, zero chance of sustainable operation

- Small or Medium-Sized Operator with less than $30M liquid capital – minimum $21M charter capital plus $5-10M licensing/setup costs plus $500k+ monthly operations means you’ll be bankrupt before achieving scale

- Seeking Quick ROI Within 3-5 Years – Vietnamese market requires 7-10+ year horizon, patient capital, and tolerance for delayed profitability making it unsuitable for typical venture-backed or growth-focused operators

- Affiliate, Advertiser, or Influencer Promoting Offshore Casinos – illegal with prosecution risk, site blocking, payment termination, and regulatory crackdowns extending to marketing partners

- Cryptocurrency-Focused Operator – cryptocurrency effectively banned for gambling transactions, payment processing heavily restricted, incompatible with Vietnamese regulatory framework

- Online Sports Betting Operator – sports betting remains prohibited online in Vietnam despite some ASEAN markets legalizing; only land-based sports betting (football, horse racing) permitted under extremely limited licensing

- Operators Expecting Significant Vietnamese Citizen Revenue – $400 monthly income requirement, 21+ age limit, entrance fees, and social stigma eliminate 70%+ of potential domestic customers forcing reliance on unpredictable tourist demand

- Companies Without Significant Asian Market Experience – Vietnam’s combination of regulatory complexity, cultural sensitivities, bureaucratic challenges, and enforcement unpredictability requires deep regional expertise most Western operators lack

- ANY Operator Considering Vietnam as First Asian Market – Vietnam should be expansion market #5-10, not your entry point; start with Philippines, Cambodia, Japan, or even Malaysia/Singapore first

⚠️ BOTTOM LINE: Vietnam’s combination of online casino prohibition, $21M+ capital requirements, customer restrictions eliminating domestic market access, and regulatory instability make this one of the world’s worst risk-adjusted returns for gambling operators – pursue almost any other market first unless you’re building a $200M+ integrated resort and can wait a decade for returns.

One nuance often missed is payment processing in Vietnam. While crypto adoption is soaring, a huge chunk of the volume still moves through local P2P bank transfers and wallets like Momo. For operators, the challenge isn’t finding players, but maintaining stable payment gateways that don’t get flagged by the State Bank.