Zambia offers a growing iGaming market characterized by a recently updated regulatory framework amid strong interest in sports betting and land-based casino activities. The nation’s legal landscape is evolving to address digital gambling expansion with clear licensing and taxation provisions. This analysis examines the opportunities and regulatory environment for market entry in Zambia.

| Metric | Value |

|---|---|

| Legal Status of Gambling | Legal and regulated for land-based and online iGaming |

| Regulatory Authority | Betting Control and Licensing Board (BCLB) |

| Gambling Legislation | Betting Control Act, Lotteries Act, Pools Act, Tourism Act (under revision) |

| Population | Approximately 20 million (2025) |

| Minimum Legal Gambling Age | 18 years |

| GDP (Nominal) | ~$33 billion USD (2025 est.) |

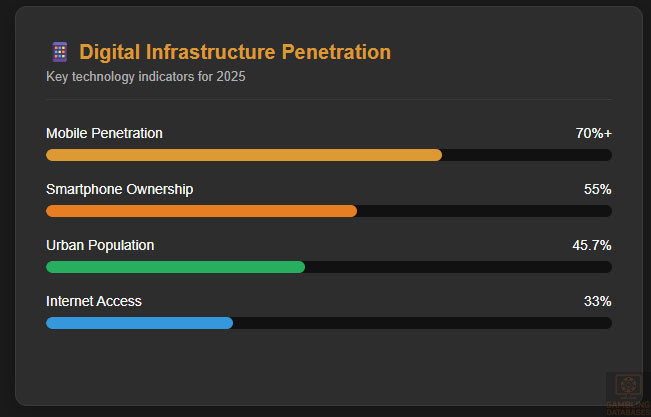

| Urban Population Share | 44% |

| Internet Penetration | 31% overall, growing mobile broadband access |

| Mobile Penetration | 70%+ with expanding smartphone usage |

| Licensed Operators Count | 99 licensed gambling companies (2025) |

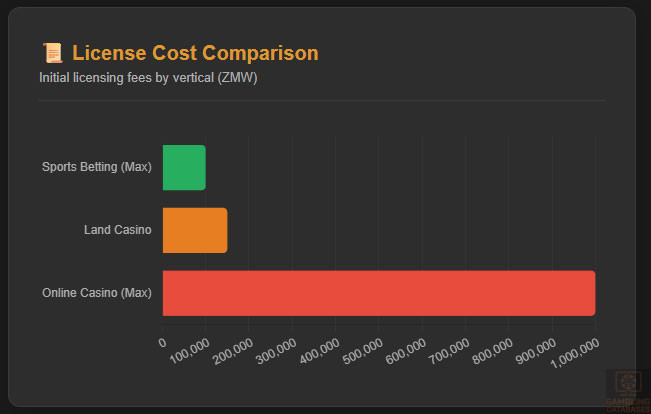

| Casino License Fees | Application: ZMW150,000; Annual Renewal: ZMW50,000 |

| Online Casino License Fees | ZMW500,000 – ZMW1,000,000 (initial fee) |

| Sports Betting License Fee Range | ZMW20,000 – ZMW100,000 |

| License Application Timeline | Approximately 3-6 months |

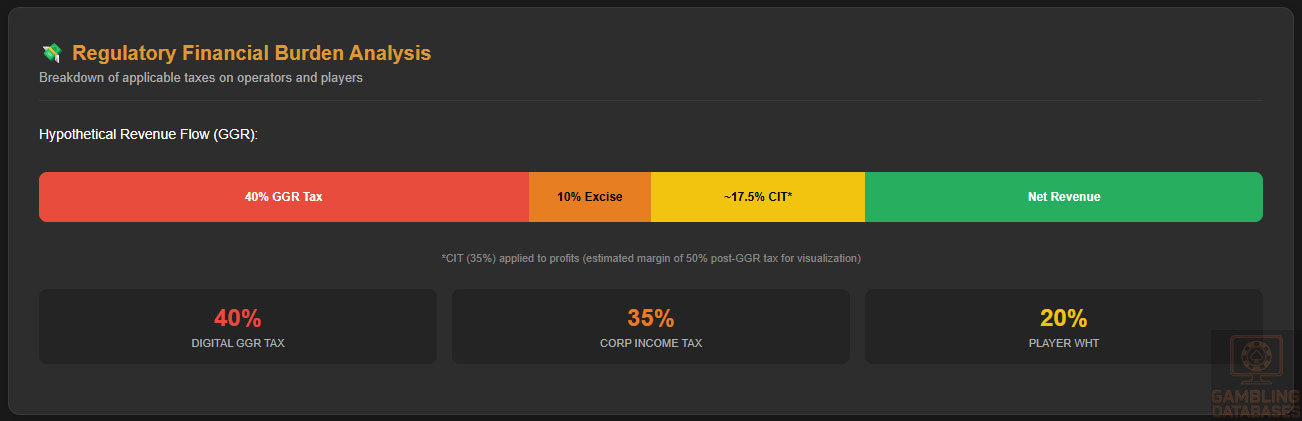

| Tax on Betting Revenues (Excise) | 10% |

| Gross Gaming Revenue (GGR) Tax Rate | 40% on digital gambling revenue |

| Corporate Tax on Operators | Standard corporate tax 35% |

| Fixed Machine Tax | ZMW250-500 per slot/machine monthly |

| Compliance Requirements | AML/KYC, responsible gaming, audited financials |

| Local Presence Requirement | Not mandatory, but regulatory oversight emphasized |

| Foreign Ownership Restrictions | None explicitly, but local partnerships encouraged |

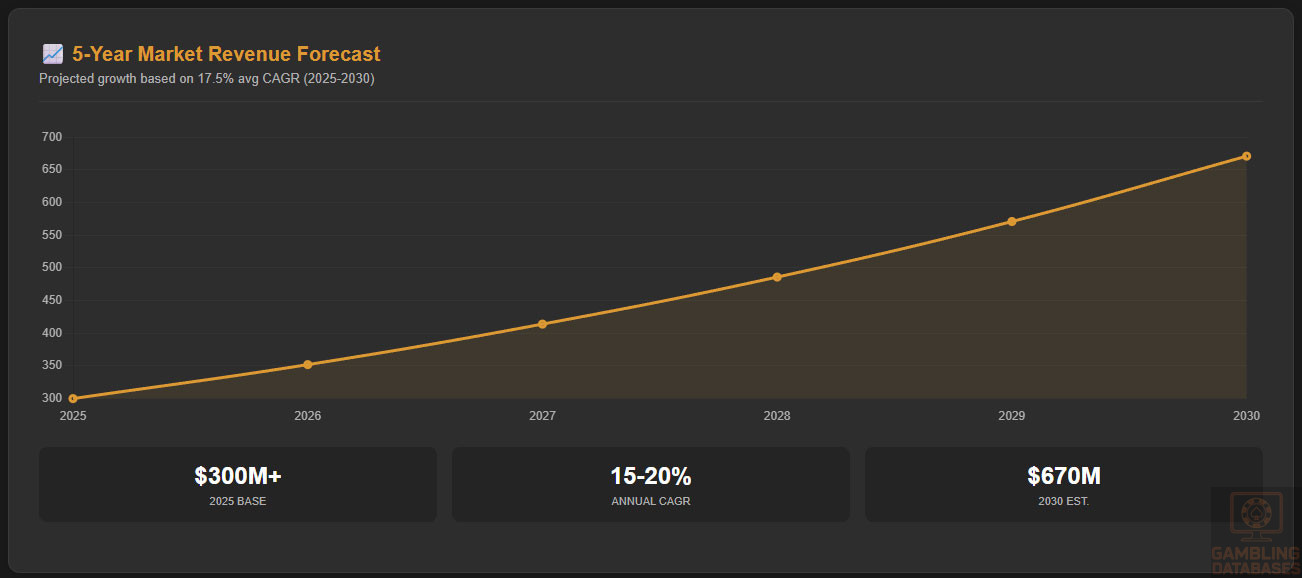

| Market Size Estimate (Wagering) | Estimated $300 million+ annually including betting |

| Market Growth Forecast (CAGR) | 15-20% over next 5 years |

| Average Revenue Per User (ARPU) | Estimated $45 – $55 |

| Responsible Gambling Measures | Mandatory self-exclusion, age verification, advertising codes |

| Advertising Restrictions | Permitted with content and time limitations |

| Recent Regulatory Reform | 2025 Bill approved to modernize and unify gaming laws |

| Enforcement Mechanisms | Fines, license suspension, criminal penalties |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Zambia maintains a legal and regulated gambling sector governed primarily by the Betting Control and Licensing Board (BCLB). The existing set of legislative acts includes the Betting Control Act, Lotteries Act, Pools Act, and Tourism Act.

This modernization reflects the rapid growth of the gaming sector, especially digital gambling, which had presented gaps under previous legislation. All forms of gambling, including lottery, sports betting, casinos, and online platforms, are subject to licensing and regulatory compliance to ensure controlled market development, consumer protection, and integrity of operations.

Land-Based Gambling Activities

Land-based gambling is well established in major urban areas such as Lusaka and Livingstone. Licensed casinos operate with a wide variety of games including table games, slot machines, and live betting facilities. Sports betting shops, both standalone and within larger venues, form a considerable part of the market landscape. Lottery operations are also formally licensed and regulated, supporting national revenue streams.

Operators of physical gambling venues must comply with legal requirements ensuring fairness in play, protection against criminal misuse, and enforcement of the minimum gambling age of 18. The presence of slot machine halls and betting outlets across urban centers contributes to a diversified land-based gaming market in Zambia.

Online Gambling Framework

Online gambling in Zambia is officially regulated under the same legislative framework as land-based gambling but has faced some ambiguity due to the nascent nature of the digital market. The Betting Control and Licensing Board enforces licensing for online operators providing casino games, sports betting, and lottery services through digital platforms. Licensed online operators must adhere to strict standards including financial transparency, player protection, and responsible gaming protocols.

Despite regulation, many players still access offshore platforms not licensed locally, representing an enforcement challenge. However, the government has prioritized closing regulatory gaps by modernizing legislation that specifically targets technological advances such as mobile betting and Internet gambling, fostering safer and more transparent market conditions.

Licensed Operators and Market Players

The competitive landscape in Zambia features nearly 100 licensed operators across various gambling verticals. Key players dominate the sports betting segment with popular platforms offering football betting, while a growing number of online casinos compete for market share in digital slots and table games. The presence of both local companies and international entrants, subject to licensing, shapes a diverse ecosystem focused on compliance and market growth.

Market entry strategies require compliance with licensing regulations and an understanding of consumer preferences, particularly for sports betting which leads the sector. Customer protection and adherence to responsible gambling measures are critical competitive factors. The Licensing Board’s oversight seeks to maintain a level playing field among operators.

Licensing Framework and Requirements

Application Process and Eligibility

Licensing is controlled by the Betting Control and Licensing Board, which requires applicants to submit detailed information regarding financial stability, company ownership, and operational plans. Application fees vary by gambling category: sports betting licenses range from ZMW20,000 to ZMW100,000, casino licenses require an application fee of ZMW150,000 plus an annual renewal of ZMW50,000, and online casino licenses carry initial fees between ZMW500,000 and ZMW1,000,000.

The approval process involves thorough background investigations, financial audits, and evaluation of compliance frameworks. The Board reserves discretion to grant or refuse licenses based on adherence to prescribed criteria. License validity typically extends for one year, subject to renewal and ongoing regulatory compliance.

The application timeline generally spans three to six months, depending on the completeness of documentation and regulatory review processes. Applicants must also provide technical details regarding gaming platforms and demonstrate capability to enforce responsible gambling standards.

Local Presence and Operational Requirements

While Zambian law does not mandate an operational physical presence in the country for foreign operators, establishing a local office or partnership can facilitate regulatory compliance and market access. Licensed operators must maintain accurate records within Zambia and ensure real-time cooperation with regulatory bodies for audit and enforcement purposes.

The regulatory framework encourages local employment and capacity building but does not explicitly restrict foreign ownership. Operators are obligated to prevent illegal activities and ensure transparency in all transactions.

Compliance Obligations and Monitoring

Player Protection and Identification

Player protection is a core compliance area for gambling operators. The minimum legal gambling age is 18 years, with strict age verification procedures required at registration and transaction stages. Anti-money laundering (AML) and know-your-customer (KYC) standards mandate operators to verify player identities and monitor account activity for suspicious behavior.

Operators must implement responsible gambling measures including self-exclusion programs, limit setting, and information disclosures around gambling risks. The regulatory board monitors compliance regularly and may impose sanctions for breaches.

- Verification of age and identity for all customers

- Continuous transaction monitoring for AML compliance

- Mandatory self-exclusion programs available to players

- Regular reporting of suspicious activities to authorities

- Disclosure of responsible gambling information to customers

Financial Monitoring and Reporting

Financial compliance includes detailed reporting of operator revenues, wagering activities, and tax obligations. Licensed entities are subject to regular audits by external certified auditors to ensure accurate accounting and adherence to financial regulations. Transaction records must be preserved for specified periods and made available for regulatory review.

Reporting deadlines require operators to submit monthly and annual financial statements detailing gross gaming revenue, tax payments, and compliance with excise duties. Failure to timely report or discrepancies found during audits trigger regulatory sanctions including fines and license suspensions.

- Monthly submission of gross revenue and tax payment reports

- Annual audited financial statement submission

- Immediate reporting of significant financial anomalies

- Compliance verification inspections by the Licensing Board

Taxation Structure and Financial Obligations

Player Taxation

Zambian law imposes a withholding tax on gambling winnings at 20% except where winnings are below specified thresholds. Players are generally not taxed directly beyond this mechanism, which operators must apply to payouts.

Operator Taxation

Licensed operators face multiple tax obligations. Betting services attract a 10% excise duty on gross betting revenue. Additionally, digital gambling revenues are subject to a hefty 40% tax on gross gaming revenue. Corporate income tax of 35% applies to profits made by operators. Fixed monthly taxes per gaming machine range from ZMW250 to ZMW500 depending on the machine type.

| Game Type | Tax Rate / Monthly Fee |

|---|---|

| Casino Live Games | 20% of gross takings |

| Casino Machine Games | 35% of gross takings |

| Lotteries | 35% of net proceeds |

| Betting | 10% excise tax on gross takings |

| Slot Machines | ZMW250 per machine monthly |

| Limited Pay Out Gaming Machines | ZMW500 per machine monthly |

License renewal fees and other administrative charges apply annually. Non-compliance or delayed payments incur penalties and interest charges.

Gambling Market Financial Performance

Zambia’s gambling sector has experienced double-digit growth driven largely by sports betting and the expansion of online gambling. Total annual wagered amounts exceed $300 million, with growing contributions from digital platforms. Tax revenues from gambling form a significant source of government income, aiding diversification away from traditional sectors.

Revenue distribution is concentrated in urban sports betting outlets, but online growth forecasts indicate a shift toward mobile and Internet wagering as penetration increases. The structure of tax and licensing fees ensures a steady fiscal inflow supporting regulation and market integrity.

Advertising and Marketing Restrictions

Advertising of gambling products in Zambia is permitted within regulated limits. Operators must adhere to content restrictions preventing misleading claims and exposure to minors. Marketing is often restricted by time slots and media channels to limit accessibility to vulnerable populations.

- Advertising prohibited during children’s programming

- No false or deceptive promotional content

- Mandatory inclusion of responsible gambling messages

- Restrictions on sponsorships of events targeting minors

- Requirement for clear licensing information in adverts

Sponsorship activities in sports and entertainment are prevalent but closely monitored to maintain compliance with legal and ethical standards.

Recent Regulatory Changes and Their Impact

In 2025, Zambia’s Cabinet approved a comprehensive bill aimed at repealing multiple outdated laws governing gaming activities. This initiative seeks to unify land-based and online gambling regulation under a single, modern framework. The reform addresses technology-driven market changes, licensing complexities, and consumer protection gaps.

The impact includes increased licensing fees, enhanced compliance requirements, and a clearer tax regime. Operators face higher costs but benefit from a more predictable regulatory environment that supports sustainable growth.

Enforcement Mechanisms and Penalties

The Betting Control and Licensing Board enforces compliance through a combination of measures including fines, license suspensions, and criminal prosecution for serious offenses. Enforcement trends indicate a zero-tolerance approach to unlicensed operations, underage gambling, and money laundering.

- Issuance of fines for regulatory breaches

- Temporary or permanent license suspension

- Criminal charges for illegal gambling activities

- Confiscation of equipment used in unauthorized operations

- Collaboration with law enforcement for enforcement actions

These enforcement actions sustain the integrity of Zambia’s gambling market, protecting consumers and legitimate operators alike.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

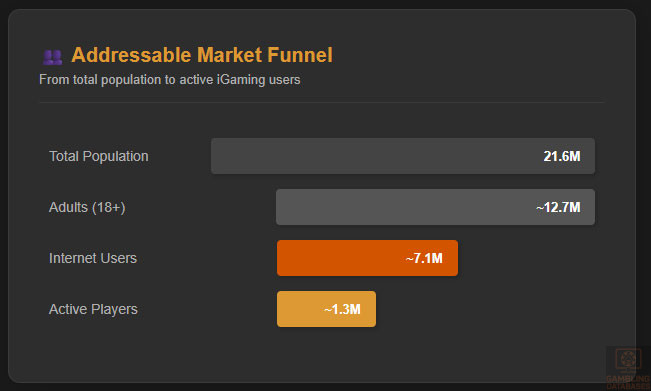

Zambia’s population in 2025 is estimated at approximately 21.6 million people with a young median age of 22.2 years, reflecting a predominantly youthful population. The gender ratio is slightly tilted towards females with approximately 985 males per 1,000 females. More than half the population is under the age of 19, indicating a strong potential future consumer base for iGaming services as this cohort reaches legal age.

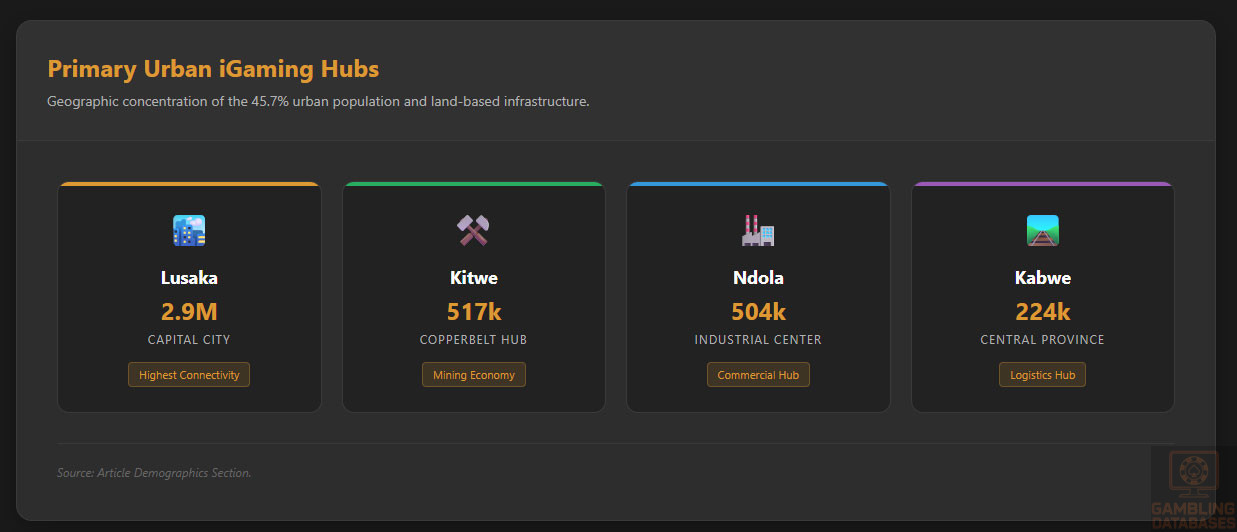

The urban population has steadily increased to 45.7% of the total population, concentrated primarily in Lusaka, Ndola, Kitwe, Kabwe, and Chingola. Rural areas compose the majority of the remaining population, where internet access and digital infrastructure are less developed but growing. This urban-rural divide significantly influences gambling venue distribution and digital service accessibility, with major gambling activities focused in urban centers while mobile and online gaming gradually penetrates rural regions.

| Age Group | Percentage of Population |

|---|---|

| 0-14 years | 41% |

| 15-24 years | 20% |

| 25-44 years | 22% |

| 45-64 years | 12% |

| 65 years and older | 5% |

Major Cities and Geographic Distribution

- Lusaka – Population approx. 2.9 million (capital and largest urban center)

- Ndola – Population approx. 504,000 (industrial and commercial hub)

- Kitwe – Population approx. 517,000 (mining center and growing urban area)

- Kabwe – Population approx. 224,000 (central province economic center)

- Chingola – Population approx. 180,000 (known mining town)

Urban centers house most licensed gambling venues and show higher mobile and internet penetration rates. Internet accessibility is uneven, with Lusaka and other major cities exhibiting broadband access rates exceeding 40% compared to less than 15% in remote areas.

Economic Indicators and Consumer Spending Power

Zambia’s real GDP growth for 2025 is projected at around 5.8% as the economy recovers from prior drought impacts, largely driven by mining, agriculture, and services sectors. GDP nominal value is estimated near $33 billion USD with average per capita income growth around 2% annually, though considerable income inequality remains across regions.

The service sector accounts for nearly 61% of GDP, supported by expanding retail, finance, and telecommunications industries, which bolster consumer spending capacity. Inflationary pressures have subsided but remain a consideration for disposable income trends.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $33 billion USD |

| GDP Growth Rate | 5.8% |

| Per Capita Income | ~$1,530 |

| Inflation Rate | 16.5% (March 2025) |

| Service Sector Contribution | 61% of GDP |

| Industry Contribution | 28% of GDP |

| Agriculture Contribution | 11% of GDP |

Disposable income is concentrated within urban middle-class households, which dominate consumption of entertainment services including gambling. Despite high poverty rates in rural regions, growing mobile money usage is increasing financial inclusion and access to iGaming platforms across socioeconomic groups.

Income and Wealth Distribution

Household income distribution in Zambia is uneven with a small upper-income group, a growing middle class centered in cities, and a large lower-income rural population. Median household incomes have increased moderately, enabling increased discretionary spending on leisure and entertainment.

Consumer spending patterns indicate a preference for cost-effective entertainment options. The middle class has shown growing interest in online betting and gaming, motivated by rising smartphone penetration and mobile data availability.

Market Size and Growth Projections

Zambia’s iGaming market has shown robust expansion with an estimated wagering base exceeding 300 million USD annually. The user base is forecasted to grow at a compound annual growth rate (CAGR) of approximately 15-20% over the next five years, driven by improving digital infrastructure and younger demographics.

Average Revenue Per User (ARPU) currently ranges between $45 and $55, supported by strong participation in sports betting and digital casino games. Historical growth reflects a 21% market expansion over the past decade with projections indicating accelerated online dominance.

| Metric | Value |

|---|---|

| Total Annual Wagering | $300 million+ |

| Growth CAGR (5 years) | 15-20% |

| User Base Size | Approx. 1.3 million active users |

| ARPU | $45 – $55 |

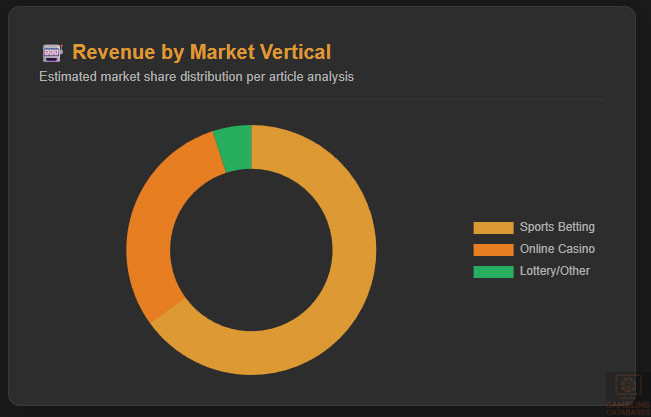

| Market Share Sports Betting | 65% |

| Market Share Online Casino | 30% |

| Market Share Lottery | 5% |

Education, Skills, and Digital Literacy

Zambia’s literacy rate stands at about 87% with ongoing government efforts to improve educational quality and digital skills. Despite growing mobile penetration, digital literacy remains a challenge, particularly in rural areas where access to computers and internet is limited.

Government and NGO initiatives aim to bridge the digital divide through programs targeting ICT training in schools and community centers. However, many citizens lack basic online safety knowledge and digital citizenship skills, constraining full potential for iGaming market participation outside urban hubs.

Cultural and Social Factors

Communication and Language

- English (official language used in business and digital platforms)

- Bemba (widely spoken in urban and rural Northern regions)

- Nyanja (common in Lusaka and Eastern regions)

- Tonga (prevalent in Southern regions)

- Lozi and other regional languages (used in Western areas)

English is the primary language for online interfaces and regulatory communications, although multilingual content is increasingly considered by operators to improve accessibility. Communication norms blend formal regulatory language with localized marketing to enhance consumer engagement.

Cultural Attitudes

Gambling enjoys moderate social acceptance in Zambia, with sports betting particularly popular due to widespread enthusiasm for football and other sports. Religious groups influence attitudes variably, with some advocating caution or restrictions on gambling activities.

Foreign brand entrants are generally welcomed when demonstrating compliance and responsible marketing practices. Entertainment preferences include digital gaming alongside traditional leisure pursuits, reflecting a blend of modern and cultural values shaping consumer behavior.

Problem Gambling and Social Considerations

Prevalence of problem gambling remains relatively low but growing, prompting social responsibility frameworks. At-risk populations include young adults and individuals with limited financial literacy, requiring targeted education and support.

- Government-funded awareness campaigns on responsible gambling

- Mandatory industry contributions to problem gambling support funds

- Access to counseling and helpline services for affected individuals

- Community outreach programs focusing on youth education

- Regulatory monitoring of advertising to reduce youth exposure

Operators are increasingly mandated to integrate social responsibility standards including self-exclusion options and customer risk assessments to mitigate harm.

Political Structure and Governance

Zambia is a stable multi-party democracy with a presidential system and recognized regulatory institutions supporting consistent policy enforcement. The government prioritizes economic diversification and foreign investment attraction, enhancing regulatory transparency in sectors such as gambling.

Political stability, despite upcoming elections, provides a conducive environment for business, with international relations fostering investment inflows and regulatory cooperation in digital economy sectors.

Technology Adoption and Digital Behavior

Internet and Digital Usage

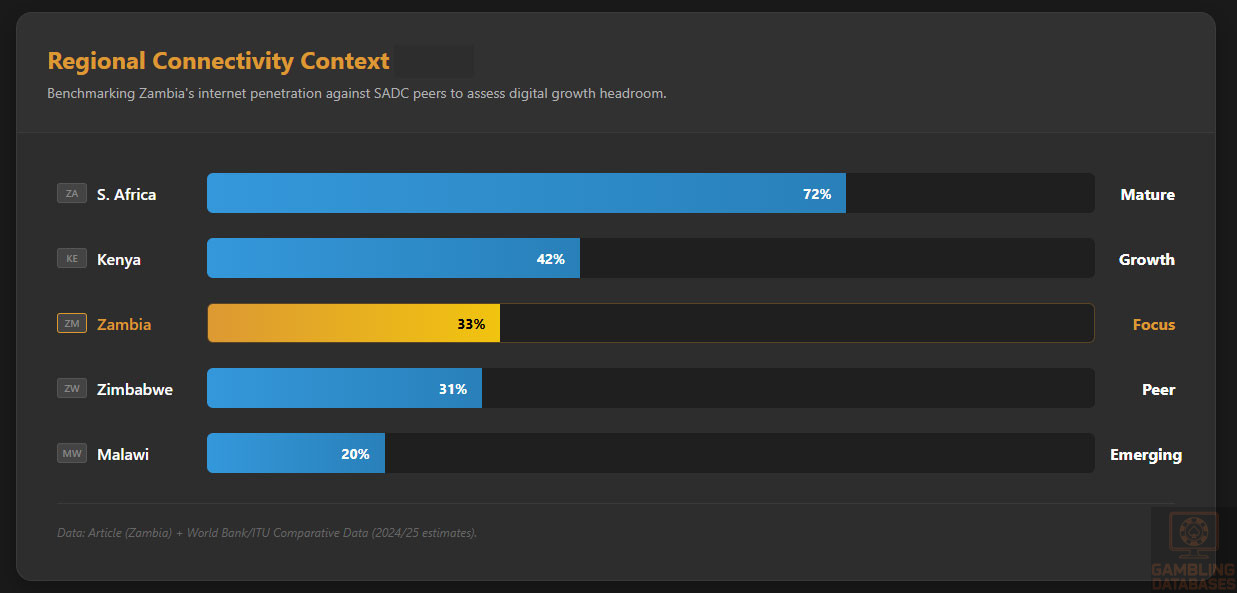

Internet penetration in Zambia is estimated at around 33% as of early 2025, with approximately 7.1 million users. Mobile adoption is widespread, with over 70% of the population owning mobile phones, mostly smartphones capable of supporting online gambling platforms.

Social media engagement is robust, led by Facebook with nearly 2.2 million Zambian users, followed by LinkedIn, Instagram, Twitter, and YouTube, which are essential channels for marketing and customer engagement in the iGaming sector.

- Facebook: ~2.2 million users, primary social media platform

- Instagram: Growing popularity among younger demographics

- YouTube: Widely used for entertainment and educational content

- Twitter: Important for news and sports discussion

- LinkedIn: Used by professionals and industry stakeholders

Digital Payment Behavior

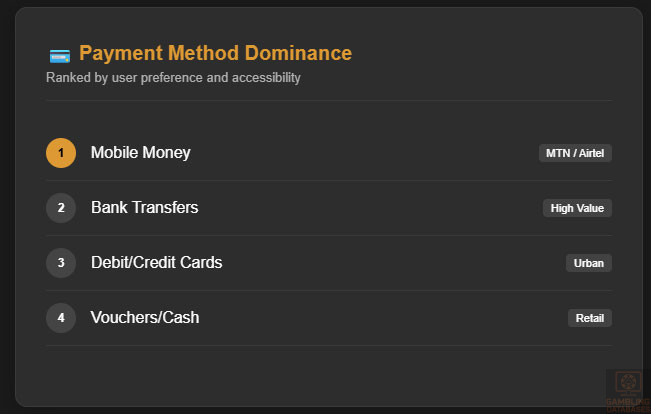

Zambia’s growing mobile money ecosystem drives digital payment adoption for online transactions. Preferences include mobile wallets, bank transfers, and prepaid card solutions tailored to consumer convenience and security.

- Mobile Money (e.g., MTN Mobile Money, Airtel Money): Majority market share in digital payments

- Bank Transfers: Preferred for high-value transactions and withdrawals

- Debit/Credit Cards: Increasing but limited due to banking penetration

- E-wallets: Emerging options among younger users with urban focus

- Cryptocurrency: Minimal but exploratory interest, regulated cautiously

Gaming and Gambling Preferences

Current Market Participation

| Activity | Participation Rate (%) |

|---|---|

| Sports Betting | 55% |

| Online Casino Games (slots, poker, blackjack) | 30% |

| Land-Based Casino Gambling | 15% |

| Lottery and Number Games | 10% |

| Informal/Unregulated Betting | 5% |

- Sports Betting

- Online Casino Slots

- Live Poker and Table Games

- Lottery Participation

- Informal Traditional Betting

Consumer Behavior Patterns

Zambian players favor sports betting during key football matches and tournaments, exhibiting peak activity on weekends and evenings. Online casino players typically prefer slots and live dealer games for entertainment and social interaction.

Session lengths vary, with sports betters often placing multiple bets per game day, while casino players engage in longer, more immersive sessions. Retention patterns reflect moderate loyalty with consumer switching influenced by promotions and platform usability.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Zambia has made significant strides in internet penetration, reaching approximately 33% of the population in early 2025. The internet landscape is predominantly mobile-driven, with mobile broadband accounting for over 70% of connections. Fixed-line broadband remains limited and concentrated in major urban centers such as Lusaka and Kitwe, with average download speeds averaging 14 Mbps in urban areas but falling below 5 Mbps in rural locations.

Despite increasing investment in fiber optics and wireless technologies, connectivity reliability varies significantly between regions. Power supply inconsistencies also affect data center uptime and network performance, posing challenges for digital service delivery, including iGaming platforms.

5G and Future Technology Deployment

5G technology rollout is in early stages, with initial coverage available in Lusaka and a few other urban areas. Major telecom operators have announced expansion plans targeting broader urban and peri-urban deployment over the next 2-3 years. The government supports accelerated digital infrastructure development as part of its national ICT strategy aimed at economic digitization.

The telecommunications landscape is led by several network operators continuing investments in 4G LTE and fiber infrastructure to meet growing demand for high-speed internet, crucial for seamless iGaming experiences across Zambia.

Mobile Technology Ecosystem

Mobile Network Infrastructure

Zambia’s market consists of multiple mobile network operators offering a range of voice and data services. The mobile subscriber base exceeds 70% penetration, driven by competitively priced data bundles and expanding 3G/4G coverage. Operator focus on network quality improvements and customer service underpins rapid mobile data adoption.

- MTN Zambia: Largest market share with dominant urban presence

- Airtel Zambia: Strong regional coverage and growing subscriber base

- CellZ: Regional operator focusing on underserved markets

- Zamtel: State-owned operator with fixed and mobile services

- Smile Communications: Niche 4G LTE provider targeting urban users

Device Penetration

Smartphone adoption has risen sharply, with over 55% of mobile users owning devices capable of supporting advanced apps and mobile gaming platforms. Android dominates the market, favored for affordability and app ecosystem diversity. This high smartphone penetration facilitates widespread access to mobile betting and online casino apps, crucial for market growth.

While feature phones still exist in rural segments, ongoing upgrades to affordable smartphones and increased digital literacy programs are expected to expand the user base over the next five years.

Financial Services and Payment Infrastructure

Banking System Structure

Zambia’s banking sector is characterized by a mix of domestic and international players with growing digital banking adoption. Banking penetration remains under 35% of the population but mobile money services have extended financial inclusion to previously underserved segments.

- Zambia National Commercial Bank (Zanaco): Market leader in retail and SME banking

- Standard Chartered Bank Zambia: Focused on corporate and private banking

- Barclays Bank Zambia: Established with broad branch network

- Citibank Zambia: Serving international business and investment clients

- First National Bank Zambia: Strong SME and retail portfolios

- Agricultural Development Bank: Key role in rural financing

Payment Processing Options

Payment infrastructure is diverse, encompassing mobile money, card payments, bank transfers, and e-wallets. The popularity of mobile wallets such as MTN Mobile Money and Airtel Money enables fast and secure transactions, widely used for gambling deposits and withdrawals.

- Mobile Money (e.g., MTN Mobile Money, Airtel Money): Leading payment option

- Debit and Credit Cards (Visa, MasterCard): Increasingly accepted but limited

- Bank Transfers: Used mainly for large transactions and withdrawals

- E-wallets (e.g., Zoona): Emerging player with niche adoption

- Cryptocurrency: Limited use due to regulatory and market infancy

E-commerce and Digital Economy

Zambia’s e-commerce market remains nascent but growing, supported by increasing internet accessibility and mobile penetration. Online retail penetration is below 10%, as logistical and payment system challenges limit widespread consumer adoption. Nevertheless, digital service sectors, including iGaming and digital entertainment, demonstrate more rapid uptake due to lower physical infrastructure barriers.

Consumer trust in digital payments continues to improve via enhanced cybersecurity, regulatory oversight, and payment dispute mechanisms, critical for sustaining market growth in online gambling and related industries.

Business Environment and Regulatory Framework

Ease of Business Operations

Zambia ranks favorably in the World Bank’s Doing Business Index among Sub-Saharan African nations, with simplified business registration and investment promotion efforts. Registration processes are streamlined but still involve several steps, with moderate transaction costs. Foreign investors benefit from policies encouraging market entry with few explicit ownership restrictions in the gambling sector.

- Preparation and notarization of company documents

- Submission and approval by the Patents and Companies Registration Agency

- Registration with Zambia Revenue Authority for tax identification

- Opening local corporate bank accounts with minimum capital deposits

- Obtainment of all industry-specific licenses such as gambling

Corporate Structure and Registration

Common entity types include Limited Liability Companies (LLCs), Public Companies, and Branch Offices of foreign firms. LLCs are preferred due to limited liability and flexible governance structures. Branch offices allow foreign operators to establish presence without local incorporation but may have operational restrictions.

Registration timelines average 2-4 weeks, and costs vary depending on entity type and legal assistance. Foreign ownership is permitted without quota restrictions in most sectors, including iGaming, but local partnerships enhance compliance and market penetration.

- Certificate of incorporation

- Memorandum and Articles of Association

- Taxpayer Registration Number (TPIN)

- Proof of physical address

- Directors’ identification documents

- Bank references and financial statements

Taxation Framework

The corporate income tax rate in Zambia stands at 35% with concessions available in designated economic zones offering lower rates and tax holidays. The government has active double tax treaties with multiple countries facilitating foreign investment.

- South Africa

- United Kingdom

- China

- Norway

- Kenya

- Sweden

Personal income tax rates are progressive, with withholding tax requirements on dividends and interest. Social security contributions are mandatory for employers and employees, with tax residency rules aligned to OECD standards.

Market Entry Considerations

Success in Zambia’s iGaming market requires tailored approaches accommodating local consumer preferences, regulatory compliance, and robust technological infrastructure. Partnerships with local firms can enhance market knowledge and regulatory navigation.

- Leverage mobile-first platforms targeting urban youth

- Develop multilingual content catering to key language groups

- Implement rigorous AML and responsible gambling measures

- Adopt flexible payment solutions prioritizing mobile money

- Engage in community-driven marketing and sponsorships

Typical initial costs include licensing, platform setup, marketing, and local compliance, with timelines for market entry ranging from three to six months depending on regulatory approval speed.

| Phase | Duration |

|---|---|

| Preparation and Document Submission | 4-6 weeks |

| Regulatory Review and Background Checks | 6-10 weeks |

| Licensing Approval and Fee Payment | 2-4 weeks |

| Operational Setup and Market Launch | 4-8 weeks |

Success Factors and Challenges

Key success factors include strong regulatory compliance, mobile accessibility, and local market adaptation. Challenges entail infrastructure limitations, regulatory costs, competition from unlicensed operators, and socio-cultural sensitivities regarding gambling.

- Robust compliance systems for licensing and reporting

- Mobile-first technology and payment integration

- Local language and culture sensitive content

- Effective customer protection and responsible gaming policies

- Building trust in digital payment and withdrawal processes

Exit strategies should consider license transferability restrictions and market liquidity, with valuations influenced by brand strength and regulatory history.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Zambia?

Yes, online gambling is legal and regulated under the Betting Control and Licensing Board. Both land-based and online operators must obtain licenses to operate lawfully. The regulatory framework ensures player protection, responsible gambling, and operators’ compliance with taxation and auditing standards. Unauthorized gambling activities are subject to legal penalties.

2. What types of gambling licenses are available and what do they cover?

Zambia offers several gambling license categories, including sports betting licenses, casino operator licenses, lottery licenses, pool betting licenses, and online gambling licenses. Each license type defines permitted games, operational scope, and compliance requirements. Operators may hold multiple licenses when offering combined services such as sports betting alongside casino games.

3. How much does an iGaming license cost and how long does it take to obtain?

Licensing costs vary by category: sports betting licenses range from ZMW20,000 to ZMW100,000, casino licenses require an initial fee of ZMW150,000 with annual renewals, and online casino licenses range from ZMW500,000 to ZMW1,000,000 for initial fees. The typical application period is approximately three to six months, depending on documentation completeness and regulatory scrutiny.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain gambling licenses with few restrictions. While local partnerships are encouraged to facilitate market access, foreign ownership is largely permitted without quotas. Applicants must demonstrate financial suitability, local compliance capability, and technical readiness to meet regulatory standards.

5. What are the tax obligations for iGaming operators?

Operators face multiple taxes including a 10% excise tax on gross betting revenue, a 40% gross gaming revenue tax for online gambling, and a 35% corporate income tax on profits. Additional fixed taxes apply to slot machines and other equipment monthly. Compliance requires timely filing and payment to avoid penalties.

6. Are gambling winnings taxed for players?

Players’ winnings are subject to withholding tax at a 20% rate, deducted at source by operators on winnings exceeding defined thresholds. This tax mechanism simplifies obligations for players while ensuring government revenue. No direct player tax filings are typically required.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational expenses include license fees, platform technology costs, marketing and customer acquisition, payment processing fees, staff salaries, and compliance-related expenditures. Marketing, compliance, and licensing represent the largest ongoing costs. Technology costs depend on whether operators build proprietary platforms or use third-party providers.

8. What is the expected ROI timeline for entering this market?

The average ROI timeline ranges from 18 to 36 months, contingent on market penetration rates, operational efficiencies, and regulatory compliance. Early market entrants with localized strategies tend to achieve breakeven faster by capturing significant user bases early and leveraging mobile-first approaches.

9. What are the local presence requirements for operators?

While not strictly mandatory, having a local presence such as a physical office or local representative is advantageous for compliance and operational efficiency. The regulatory board requires operators to maintain records and cooperate promptly with inspections and audits, which is facilitated by local presence.

10. What payment methods are available and recommended?

Mobile money services dominate the payment landscape, with MTN Mobile Money and Airtel Money being most pervasive. Debit and credit cards are growing in adoption but remain secondary. Bank transfers and e-wallets complement the ecosystem. Cryptocurrency remains nascent and cautiously approached by regulators.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and include responsible gambling messages. Time and media restrictions limit exposure during children’s programming and sensitive content areas. Misleading claims and promotions encouraging excessive gambling are prohibited. Sponsorships require regulatory approval.

12. What responsible gambling measures are mandatory?

Operators are required to implement age verification, provide self-exclusion options, educate customers on risks, monitor player behavior for signs of problem gambling, and contribute to support services. These measures aim to protect vulnerable individuals and promote sustainable gaming practices.

13. How large is the iGaming market and what is the growth potential?

The estimated current market size exceeds $300 million annually with a growth forecast CAGR of 15-20% driven by increasing smartphone penetration and digital payment adoption. The younger demographic and expanding internet coverage underpin optimistic market expansion.

14. Who are the main competitors and what is their market share?

The market features nearly 100 licensed operators with sports betting holding approximately 65% market share, online casinos at 30%, and lotteries at 5%. Leading brands span local companies and international operators leveraging licensed platforms with diverse marketing strategies to capture users.

15. What are the player preferences and typical spending patterns?

Players predominantly engage in sports betting timed with football events, complemented by slots, live poker, and lottery play. Higher activity occurs in urban centers with mobile access. Spending per user averages $45 to $55 annually, with peak engagement during major sports tournaments.

16. What are the key success factors and main challenges for new entrants?

Success depends on regulatory compliance, mobile-first technology, local partnerships, and responsible gambling integration. Challenges include infrastructure variability, licensing costs, market competition, and socio-cultural sensitivity to gambling activities.

Sources and References

- Betting Control and Licensing Board of Zambia – Official Regulatory Website

- Ministry of Technology and Communications, Zambia – ICT and Digital Infrastructure Reports 2025

- Zambia Central Statistical Office (ZamStats) – Population and Demographic Data 2025

- World Bank Group – Zambia Doing Business Report 2024

- International Monetary Fund – Zambia Article IV Consultation 2025

- Zambia Revenue Authority – Taxation Regulations and Guidelines 2025

- MTN and Airtel Zambia – Mobile Network Operator Reports 2025

- Zambian Ministry of Finance – Economic and Financial Reports 2025

- SIGMA Africa – Zambia iGaming Market Analysis 2025

- iGaming Today – Zambia Regulatory and Market Reports 2025

- World Population Review – Zambia Demographics 2025

- DataReportal – Digital 2025 Zambia Report

- Central Bank of Zambia – Banking Sector Reports 2025

- Zambia Telecommunications Authority – Network Infrastructure Data 2025

- AfricanTelecom News – Zambia 5G and Mobile Market Updates 2025

- UNFPA – Zambia World Population Dashboard 2024

- LinkedIn Insights – Zambia Digital and Professional Trends 2025

- PopulationPyramid.net – Zambia Population Structure 2025

- Gaming Industry Expert Reports – African Markets 2024-2025

- Zambia Ministry of Commerce – Business Registration Procedures 2025

- PwC Zambia – Tax Summaries and Corporate Taxation 2025

- National Bank of Zambia – Digital Banking Usage Data 2025

- ICT Zambia – Digital Literacy and Education Reports 2024

- African Gamblers Association – Responsible Gambling Framework 2025

- Zambia Ministry of Sport – Sponsorship and Advertising Regulations 2025

- Various Online News Portals covering Zambian Economy and Gambling Industry, 2024-2025

🎯 Gambling Databases Country Rating: Zambia

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.8/10 | 🟡 Moderate |

| Player Access Score | 8.5/10 | 🟢 Fully Legal |

| Overall Market Attractiveness | 7.1/10 | 🟡 High Tax / Low ARPU |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Predatory Taxation: Digital gambling revenue is subject to a 40% Gross Gaming Revenue (GGR) tax, plus 35% corporate tax and 10% excise duty on betting.

- Winnings Tax Impact: A mandatory 20% withholding tax on player winnings significantly depresses retention and pushes high-value players to offshore black markets.

- Infrastructure Instability: Regular power outages and low internet penetration (31-33%) outside Lusaka create severe operational and user-experience bottlenecks.

- Regulatory Volatility: The 2025 regulatory overhaul introduces uncertainty regarding future enforcement strictness and compliance costs.

- Low Player Value: With an ARPU of $45-$55 annually, the volume required to offset the 40% GGR tax is extremely high.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.75/3.0 | Full legality for sports betting and online casinos (+3.0). Deduction for recent massive regulatory overhaul causing transitional uncertainty (-0.25). |

| Licensing Process | 25% | 2.5/2.5 | Licensing is accessible and defined (+2.0). Application fees (approx. $18k-$36k USD) are low globally (+0.5). Timeline is reasonable (3-6 months). |

| Taxation & Costs | 20% | 0.0/2.0 | GGR Tax is 40% (+0.5 bracket). However, multiple tax layers exist: 10% excise on staking + 40% GGR + 35% Corporate Tax + 20% Winnings Tax. Total effective tax rate exceeds 60% of revenue (-1.5 deduction). Minimal score awarded. |

| Operational Requirements | 15% | 1.25/1.5 | No mandatory local office for foreign operators, though local records required (+1.5). Deduction for infrastructure challenges (power/connectivity) complicating reliable service delivery (-0.25). |

| Market Environment | 10% | 0.3/1.0 | Moderate business environment (+0.5). Deductions for low ARPU demographics and ongoing legislative changes (-0.2). |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 4.0/4.0 | Fully legal. Players can access sports betting, casinos, and lotteries without legal risk (+4.0). |

| Practical Accessibility | 30% | 1.5/3.0 | Mobile money is widely available (+2.0). Significant deductions for low internet penetration (31%) and digital literacy issues outside urban hubs (-1.5). Access is legal but practically difficult for the majority. |

| Player Penalties | 20% | 2.0/2.0 | No criminal or civil penalties for players accessing gambling services (+2.0). |

| Market Availability | 10% | 1.0/1.0 | Market is saturated with ~100 licensed operators offering diverse products (+1.0). |

🔍 Key Highlights

Strengths

- Clear Legal Status: Unlike many African nations, online casino is explicitly legal and licensable.

- Mobile Money Ecosystem: High adoption of MTN/Airtel money makes deposits/withdrawals frictionless for the banked population.

- Low Entry Fees: License fees (~$30k range) are significantly lower than European or US standards.

⛔️ CRITICAL RISKS AND CHALLENGES

- Taxation Structure: The 40% GGR tax combined with a 10% excise on stakes destroys margins. It is one of the highest tax burdens in Africa.

- Low Consumer Spending: An ARPU of ~$50/year means you need massive volume to cover fixed compliance costs.

- Infrastructure: “Load shedding” (power cuts) and spotty 4G coverage interrupt live betting and casino sessions, leading to lost revenue.

- Winnings Tax: The 20% tax on player winnings is a major churn factor, encouraging players to find offshore sites that don’t deduct it.

- Competition: With nearly 100 licensees, the market is crowded for its size and economic value.

Player-Specific Issues

- Withholding Tax: Players lose 20% of winnings immediately to the state.

- Digital Divide: Rural players (over 50% of pop) have very limited access to high-speed internet required for modern slots/live dealer games.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $100,000 – $200,000 (License fees, consultancy, initial setup).

Monthly Operating Costs: $30,000 – $80,000 (Low labor costs, but high compliance/reporting overhead).

Effective Tax Rate on Revenue: ~65%+ (When combining Excise, GGR, and Corporate tax).

Customer Acquisition Cost: Moderate ($20-$40), but high relative to the $45-$55 ARPU.

Time to Breakeven: 24-36 months.

Profitability Assessment: Economics are EXTREMELY CHALLENGING. While entry is cheap, the tax regime is designed to extract maximum value from operators. The 40% GGR tax, plus the 10% excise on turnover, leaves very little room for marketing or profit margin. Only viable for operators who can automate everything and run on razor-thin margins at high volume.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | 🟡 Medium | Zambia is modernizing laws to close gaps; expect increased blocking and potential blacklisting. |

| Licensed Sports Betting Operators | 🔴 High (Financial) | Regulatory compliance is safe, but financial risk is critical due to excessive tax burden and potential tax audits. |

| Affiliates/Advertisers | 🟡 Medium | Advertising codes are tightening; promoting unlicensed entities could lead to fines under the new 2025 framework. |

| Payment Processors | 🟢 Low | Standard risk, provided AML/KYC checks are robust. |

| Company Directors/Executives | 🟡 Medium | Standard corporate liability; ensure strict adherence to tax reporting to avoid criminal negligence charges. |

🚨 Extradition and International Enforcement

Extradition Treaties: Zambia is a member of the Commonwealth and has extradition arrangements with the UK, USA, South Africa, and neighboring SADC countries.

Enforcement History: Enforcement is generally focused on physical illegal gambling dens rather than international extradition for online offenses. However, operating without a license while physically present in Zambia carries high arrest risk.

Safe Jurisdictions: No specific “safe” status; standard international law applies.

📋 Final Verdict

Zambia receives an Operator Ease Score of 6.8/10 and a Player Access Score of 8.5/10, resulting in an overall market attractiveness rating of 7.1/10.

HONEST ASSESSMENT: Zambia is a classic “Honey Trap” market. It looks attractive with full legality, low license fees, and a growing population, but the 40% GGR tax combined with a 10% excise tax makes it mathematically nearly impossible to run a highly profitable operation unless you are a market leader. While you can operate legally and easily, the government takes the majority of the revenue while you take all the risk.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A large pan-African operator aggregating volume across multiple countries.

- Able to run a “Lite” version of your product optimized for low-bandwidth mobile data.

- Willing to accept net margins below 10% in exchange for market presence.

❌ Definitely Avoid If You Are:

- A boutique casino operator (ARPU is too low, tax is too high).

- Dependent on high-value VIP players (20% winnings tax scares them away).

- Undercapitalized (<$500k) – you will burn out before achieving the necessary volume.

- Expecting European-style infrastructure reliability.

⚠️ BOTTOM LINE: Legal and open, but the tax regime is predatory. Enter only if volume can compensate for razor-thin margins.

Success in this market is 100% dependent on seamless Mobile Money integration (Airtel and MTN). Credit card penetration is negligible for gambling transactions here. If an operator’s gateway doesn’t offer instant USSD or app-based mobile wallet deposits, the conversion rate will be near zero regardless of the brand strength.