Zimbabwe presents a cautiously developing opportunity in the iGaming sector, characterized by evolving legislation and an active regulatory body committed to integrating online gambling within a structured framework. While land-based gambling is well established, the online iGaming market is nascent, with substantial government focus on regulation and taxation reforms to harness industry growth responsibly.

Key attractions include government efforts to modernize gambling laws, a populous base with increasing internet and mobile penetration, and fiscal measures targeting sustainable revenue streams from gambling activities. However, the regulatory environment demands strict compliance and presents both opportunities and challenges for new entrants.

Executive Summary: Key Market Indicators

| Metric | Value |

|---|---|

| Gambling Regulatory Authority | Lotteries and Gaming Board of Zimbabwe |

| Regulating Legislation | Lotteries and Gaming Act, Chapter 10:26; Betting and Totalizator Control Act |

| Legal Gambling Forms | Land-based casinos, sports betting, lotteries, online gambling (regulated emerging) |

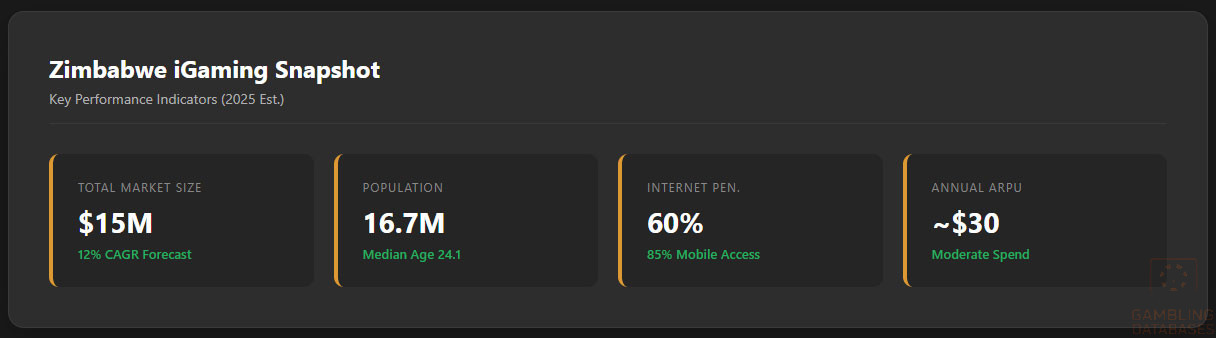

| Population | ~16.7 million (2025) |

| GDP (Nominal) | Approx. $26 billion (2025) |

| GDP per Capita | ~$1,500 (2025) |

| Internet Penetration | 60% of population |

| Mobile Penetration | 85% of population |

| iGaming Market Size (2025 est.) | Approx. $15 million |

| Projected CAGR (2025-2030) | 12% |

| Gross Gaming Revenue Tax Rate | Up to 15% for licensed operators |

| Sports Betting Winnings Tax | 10% withholding tax on gross winnings from January 2025 |

| License Application Fee | Approx. $10,000 – $30,000 depending on license type |

| License Duration | 1 to 3 years depending on category |

| License Renewal Fee | 20-30% of initial application fee |

| Market Entry Timelines | 3-6 months for licensing process |

| Local Presence Requirement | Mandatory local agent or office for foreign operators |

| Compliance Obligations | Robust KYC/AML, player protection, monthly reporting |

| Responsible Gambling Measures | Self-exclusion, player limits, awareness campaigns mandated |

| Enforcement Body | Lotteries and Gaming Board; Ministry of Home Affairs |

| Illegal Gambling Crackdown | Active government action against unlicensed operators |

| Technology Infrastructure | Mobile networks expanding; rural connectivity challenges |

| Currency | Zimbabwean Dollar (ZWL) |

| Corporate Tax Rate | 24.72% |

| Market Penetration Rate | Online gambling still emerging, 5-7% penetration |

| Average Revenue Per User (ARPU) | Estimated $30 per user annually |

| Tax Revenue from Gambling | Approx. $25 million annually (projected) |

| Advertising Restrictions | Moderate restrictions with emphasis on responsible advertising |

Section 1: Regulatory Framework and Legal Environment

Current Gambling Regulation Status

Zimbabwe’s gambling sector is regulated primarily by the Lotteries and Gaming Board under the Lotteries and Gaming Act (Chapter 10:26), alongside complementary statutes like the Betting and Totalizator Control Act. These provide a general legal framework covering both land-based and online gambling forms.

The government maintains a controlled but progressive approach to gambling regulation, ensuring consumer protection, revenue collection, and industry integrity. While land-based gambling has a mature legal environment, online gambling regulation remains an evolving domain with incremental legislative updates aimed at addressing new technological and market realities.

Land-Based Gambling Activities

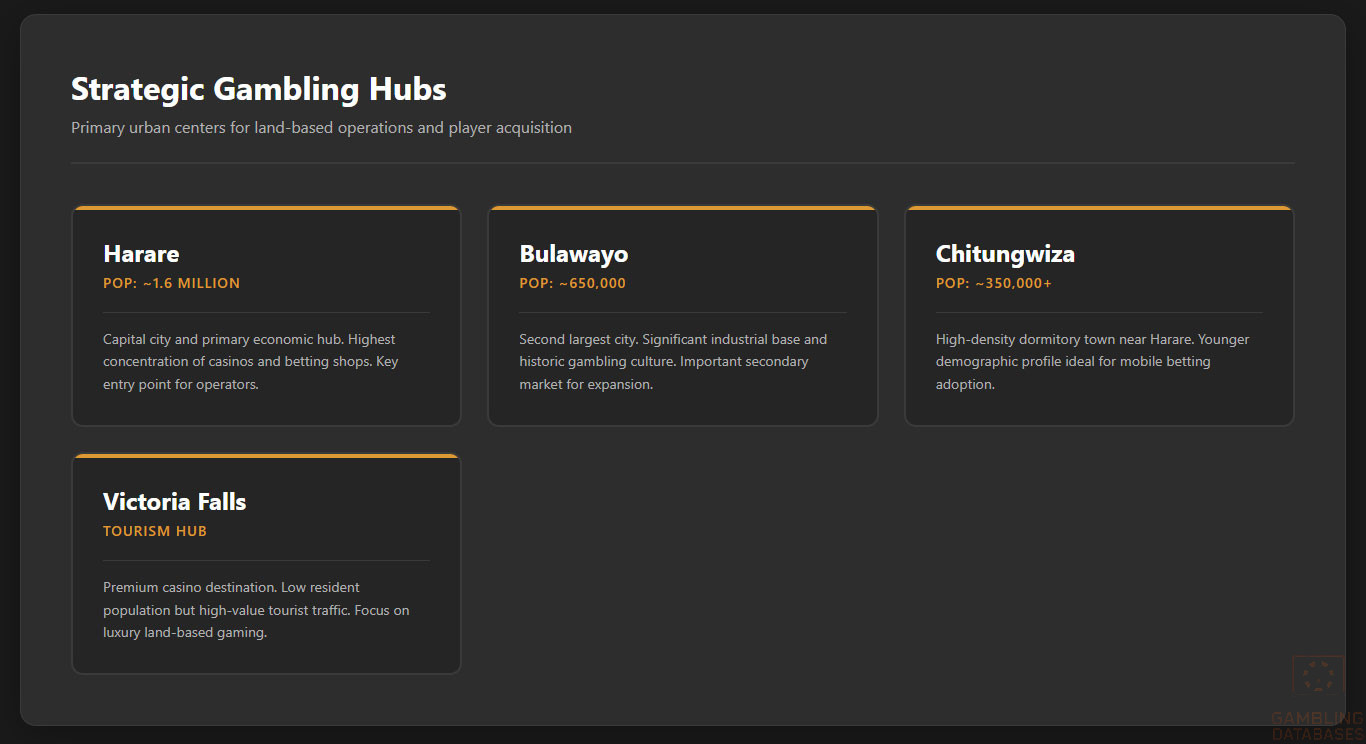

Land-based gambling in Zimbabwe comprises casinos, licensed sports betting venues, slot machine halls, and state-run lotteries. Licensed casinos primarily operate in major urban centers such as Harare and Victoria Falls, drawing both local and tourist patronage.

Sports betting enjoys widespread popularity, fueled by betting shops and outlets regulated closely by the Lotteries and Gaming Board. These venues are subject to rigorous licensing and ongoing government oversight, including anti-money laundering (AML) compliance and social responsibility enforcement.

Online Gambling Framework

Online gambling is acknowledged as a growth segment, though its regulation is less mature compared to land-based gambling. The Lotteries and Gaming Act and related laws apply to online operators, requiring them to obtain licenses and comply with the same standards as physical operators.

Licensed Operators and Market Players

The market contains a mixture of domestic and international operators, with most licensed entities focused on traditional betting and casino operations. The competitive landscape includes established local bookmakers and key regional players expanding their footprint in Zimbabwe.

New market entrants face competition from entrenched operators and must navigate regulatory compliance, including stringent tax obligations and mandatory local presence requirements. Market dynamics encourage partnerships or joint ventures with Zimbabwean entities as part of entry strategies.

Licensing Framework and Requirements

Application Process and Eligibility

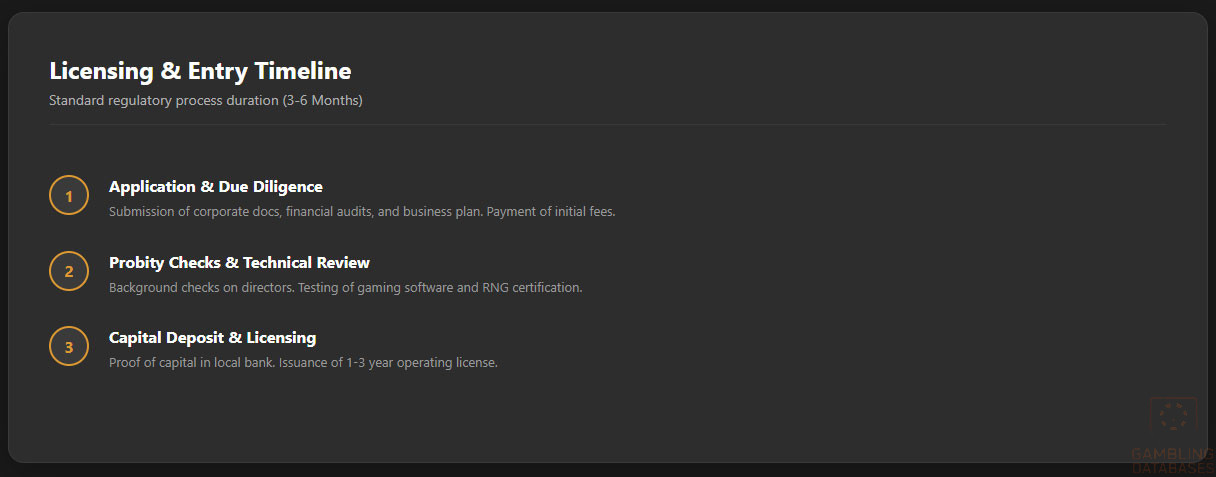

The Lotteries and Gaming Board governs the licensing process. Eligibility requires applicants to demonstrate financial stability, technical capability of gaming platforms, and integrity through thorough background checks. The application undergoes a multi-stage review including due diligence and platform assessment.

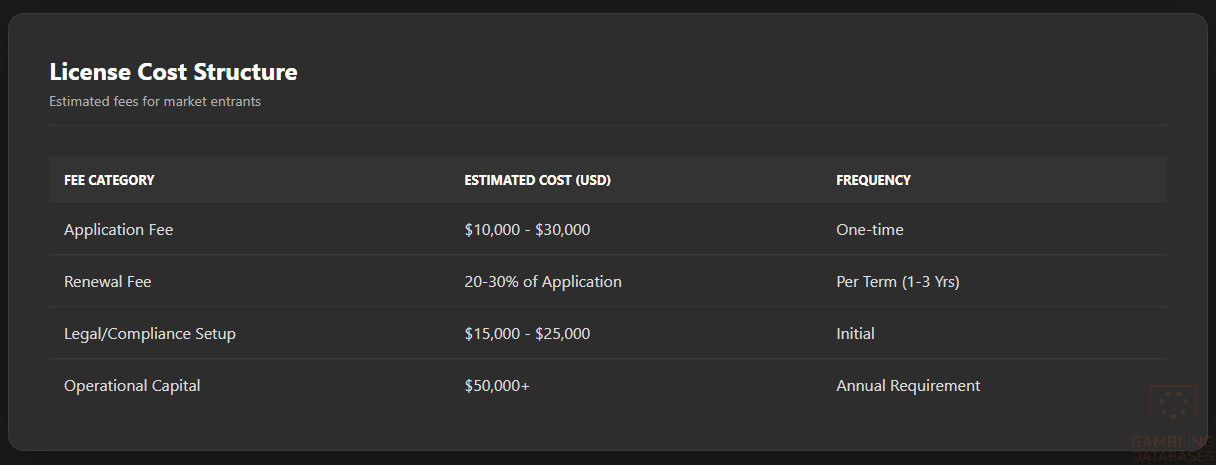

The process typically takes 3 to 6 months, charging application fees between $10,000 and $30,000 depending on the gambling category. Licenses are issued for periods varying from one to three years, contingent on compliance and operational history. Renewal fees amount to roughly 20-30% of the initial application cost.

Applicants must submit a comprehensive set of documents including:

- Corporate registration and shareholder information

- Financial statements audited for the past three years

- Business plan detailing marketing and operational strategy

- Technical documentation on gaming software and Random Number Generator (RNG) certification

- Criminal background checks for directors and beneficial owners

- Proof of capital deposit in a licensed Zimbabwean bank

- Compliance framework for KYC and AML measures

Local Presence and Operational Requirements

Foreign operators are mandated to establish a local registered office or appoint a local agent to interface with regulatory authorities and fulfill licensing prerequisites. This local entity must be capable of handling compliance reporting, customer service, and dispute resolution within Zimbabwe’s jurisdiction.

The regulatory framework restricts foreign ownership indirectly by requiring demonstrable operational presence and accountability within the country. Partnerships with local stakeholders are common, facilitating market integration and adherence to regulatory expectations.

Operationally, licensees are required to maintain transaction logs, player databases, and financial records accessible for regulatory audit. Additionally, operators must demonstrate adequate system security to protect player data and ensure transactional integrity.

Compliance Obligations and Monitoring

Player Protection and Identification

Zimbabwe’s gambling regulations impose strict Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations on operators. Mandatory player protections include age verification restricting participation to individuals 18 years and older, verification of identity documents, and transaction monitoring to detect suspicious activity.

Responsible gambling measures are enforced through:

- Self-exclusion programs for voluntary player withdrawal

- Mandatory player loss and wager limits

- Provision of educational resources on gambling risks

- Monitoring of player behavior to identify problem gambling

- Regular reporting on responsible gambling activities to authorities

Operators must also display clear information about risks and support services for individuals experiencing gambling-related harm.

Financial Monitoring and Reporting

Licensed operators are required to submit monthly reports detailing gross gaming revenues, tax withholdings, and operational data. The reporting process involves several sequential steps: initial compilation of transactional data, internal audit validation, submission to the Lotteries and Gaming Board, and subsequent government review.

In addition to monthly filings, annual audited financial statements and compliance certificates are mandatory. Failure to meet reporting deadlines or submission of inaccurate data can trigger penalties and license review.

Taxation Structure and Financial Obligations

Player Taxation

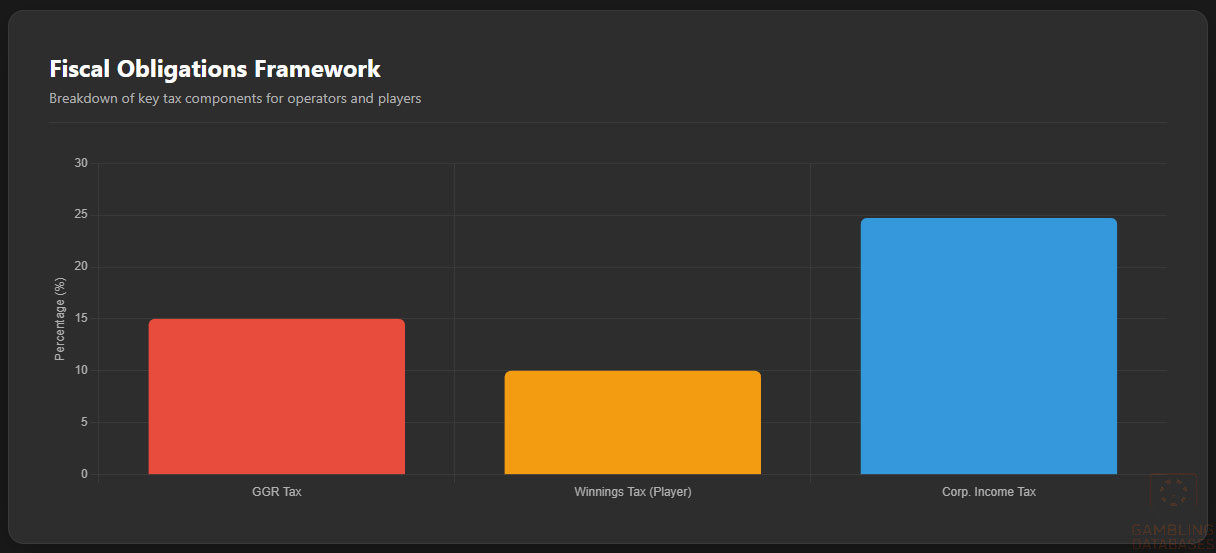

Since January 2025, Zimbabwe imposes a 10% withholding tax on gross winnings from sports betting, both land-based and online. This tax is deducted by operators before winnings are paid to players, ensuring compliance at the source.

The tax applies regardless of wager size, meaning even minimal winnings incur the levy. This approach aims to broaden the tax base but raises concerns about potentially diverting players to unregulated offshore platforms.

Operator Taxation

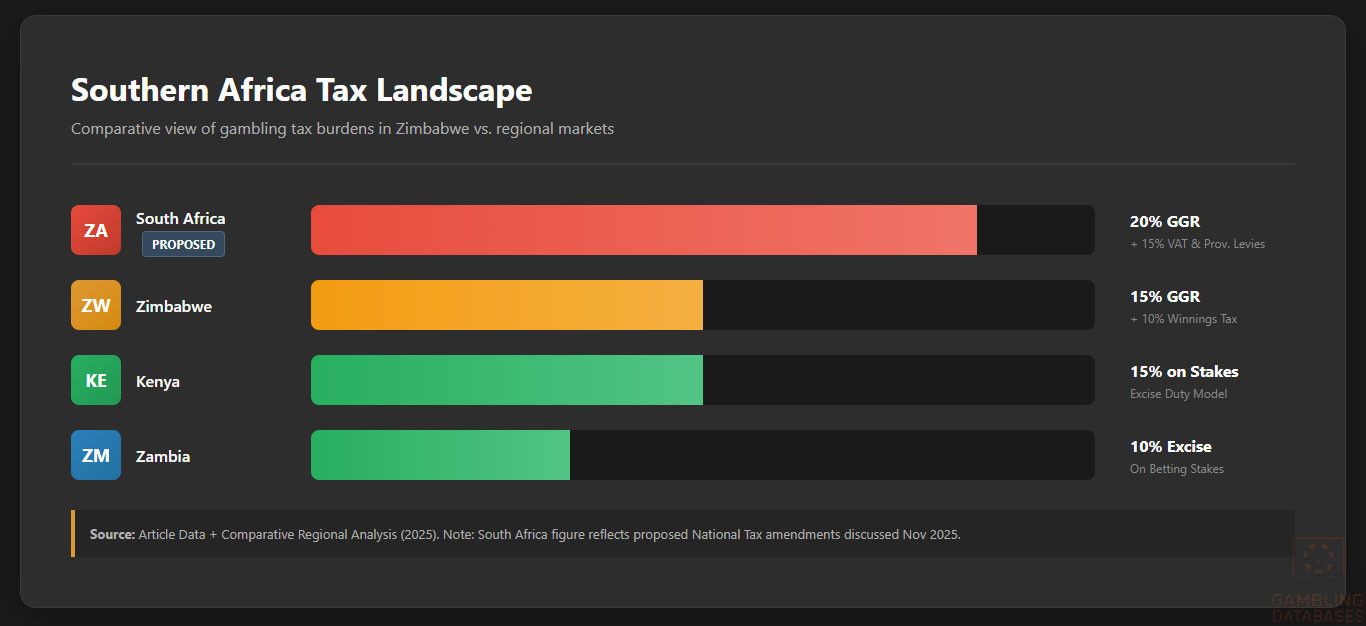

Gross Gaming Revenue (GGR) tax rates for licensed operators typically reach up to 15%. In addition to GGR tax, operators pay license fees and corporate income tax at the prevailing rate of approximately 24.72%.

| Gambling Type | Tax Rate |

|---|---|

| Land-based Casinos | 15% GGR + Corporate Tax |

| Sports Betting | 15% GGR + 10% withheld on winnings |

| Online Casinos | 15% GGR + Corporate Tax |

| Lotteries | 12% GGR + Corporate Tax |

License renewal fees typically represent 20-30% of the initial application fees. Turnover taxes on betting transactions may also apply depending on category and regulatory updates.

Gambling Market Financial Performance

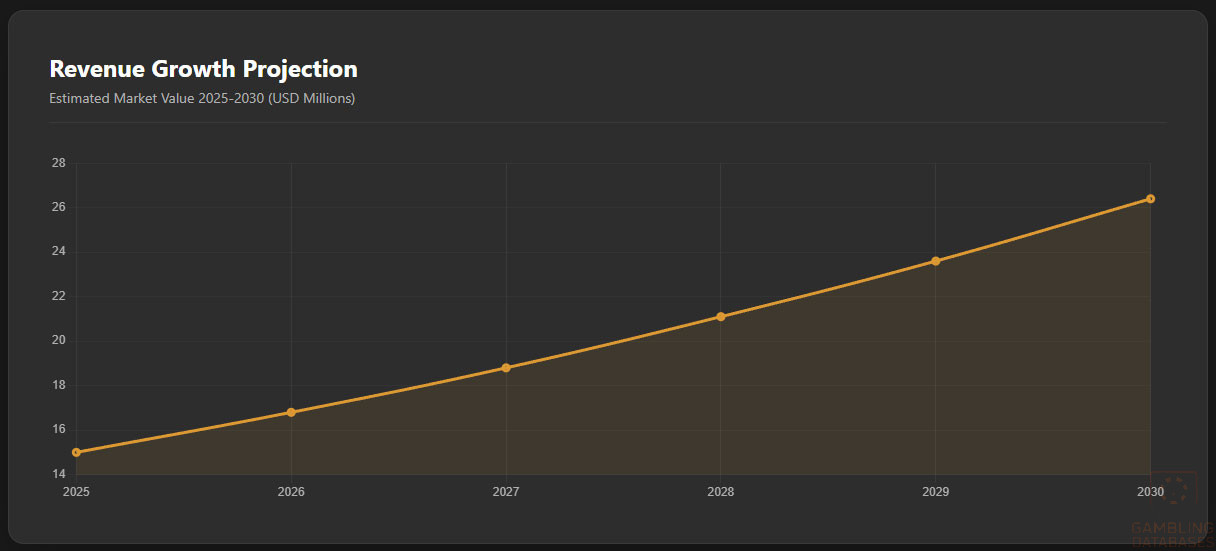

The formal gambling sector in Zimbabwe generates estimated annual revenues around $15 million with forecasted growth at a compound annual growth rate (CAGR) of 12% from 2025 to 2030. Tax revenues from gambling activities contribute close to $25 million annually to the national budget.

Year-over-year growth is driven by rising internet adoption, expanding mobile gaming, and increased regulatory enforcement bringing previously informal activities under supervision. Revenue distribution favors sports betting as the dominant contributor, followed by casinos and lotteries.

Advertising and Marketing Restrictions

Advertising of gambling activities is permitted but regulated rigorously to prevent targeting of minors and vulnerable groups. Marketing content must include responsible gambling messages and avoid misleading claims.

Promotional activities are subject to time restrictions, particularly limiting gambling advertisements during daytime hours accessible to young audiences. Sponsorships by gambling operators in sports and entertainment sectors require regulatory approval to ensure compliance with ethical standards.

Advertising channels monitored include television, radio, digital platforms, print media, and outdoor advertising. Restrictions focus on content accuracy, avoiding inducements for excessive gambling, and ensuring fair representation of odds and risks.

Recent Regulatory Changes and Their Impact

Zimbabwe enacted a significant amendment effective January 2025, introducing a 10% withholding tax on sports betting winnings and tightening licensing enforcement for online operators. This change was designed to increase government revenue and formalize online betting markets.

The amendment also increased penalties for illegal operators and reinforced requirements for transparent financial reporting and player protection. These measures have elevated operational costs but improved market integrity and consumer confidence.

Enforcement Mechanisms and Penalties

The Lotteries and Gaming Board exercises enforcement through license revocation, monetary fines, and criminal prosecution for non-compliance. Penalties target unlicensed operations, breaches in responsible gambling protocols, inaccurate reporting, and tax evasion.

- Monetary fines escalating with violation severity

- Suspension or revocation of operating licenses

- Seizure of gambling equipment used illegally

- Criminal charges for fraud or money laundering

- Public blacklisting of offending operators

Government agencies actively collaborate to detect and dismantle unauthorized gambling establishments, providing a deterrent effect while promoting regulated market growth.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

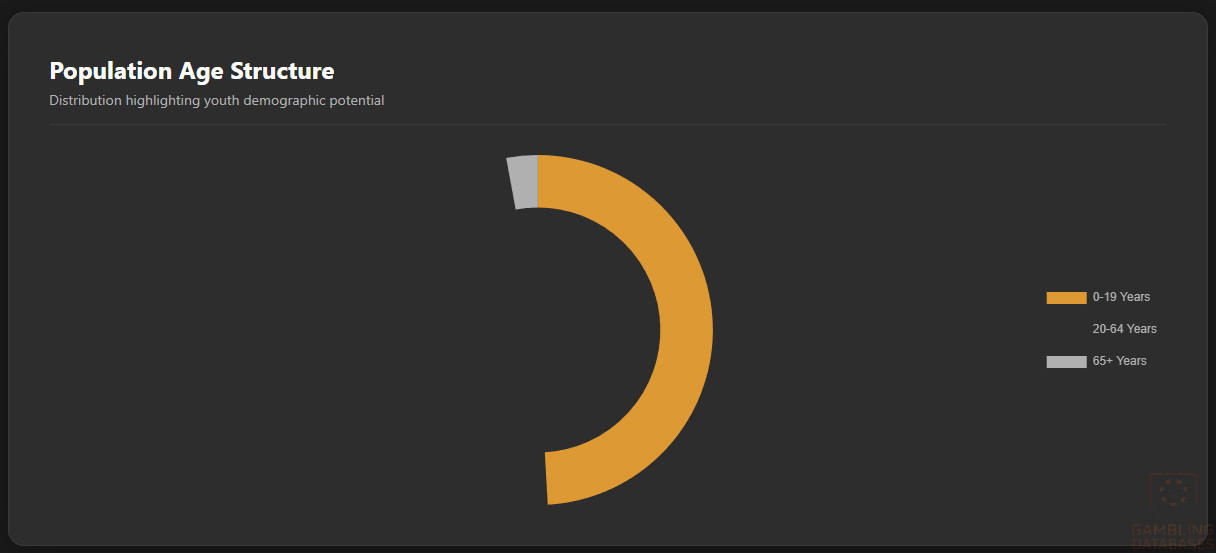

Zimbabwe’s population in 2025 is estimated at approximately 19.57 million, exhibiting a steady growth rate of about 2% annually. The median age is notably young at around 24.1 years, indicating a predominantly youthful population ripe for digital engagement. The gender ratio stands at approximately 957 males per 1,000 females, reflecting a slightly higher female demographic.

Age distribution shows nearly half the population (around 49.1%) is 19 years or younger, while adults aged 20 to 64 account for roughly 48%. The elderly population aged 65 and above remains a small segment, approximately 2.9%. This youthful demographic profile supports the potential for high iGaming adoption, especially among younger age groups.

| Age Group | Percentage of Population |

|---|---|

| 0-19 years | 49.1% |

| 20-64 years | 48.0% |

| 65 years and older | 2.9% |

Approximately 32.6% of the population resides in urban areas, concentrated mostly in cities such as Harare and Bulawayo. The rural population, comprising over two-thirds of residents, faces limited access to digital infrastructure, resulting in geographic disparities in internet and gambling venue access.

Major urban centers are pivotal hubs for gambling venues and internet connectivity, making them strategic focal points for market entry and player acquisition initiatives.

Major Cities and Populations

- Harare – Approx. 1.6 million residents

- Bulawayo – Approx. 650,000 residents

- Chitungwiza – Over 350,000 residents

- Mutare – Around 200,000 residents

- Gweru – Approximately 150,000 residents

- Kwekwe – Near 120,000 residents

Economic Indicators and Consumer Spending Power

Zimbabwe’s GDP is projected to rebound strongly in 2025, with estimates of around $26 billion and growth forecasted at approximately 6%. The economy is weighted towards agriculture, mining (notably gold), and services, which together drive consumer incomes and spending capacity.

The GDP per capita remains modest at roughly $1,500, but recent improvements in macroeconomic stability and remittance inflows are boosting disposable income levels, especially in urban centers. Income inequality persists, with wealth concentrated among a middle-to-high-income urban minority, while a significant rural population experiences lower purchasing power.

Consumer spending on discretionary services such as entertainment and gambling is rising alongside increased mobile money adoption and digital payment infrastructure growth.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $26 billion |

| GDP Growth Rate | 6.0% |

| GDP per Capita | $1,500 |

| Inflation Rate | ~10% |

| Unemployment Rate | ~12% |

Market Size and Growth Projections

The iGaming market in Zimbabwe is emerging, with estimated revenues around $15 million in 2025. Market growth is robust, supported by a Compound Annual Growth Rate (CAGR) forecast near 12% through 2030. The active iGaming user base is expanding alongside mobile internet adoption, improved digital payments, and a strong preference for mobile casino games and sports betting.

Average Revenue Per User (ARPU) is estimated at approximately $30 annually, demonstrating moderate consumer spend aligned with income levels and gaming frequency.

| Metric | 2025 | 2030 (Projected) |

|---|---|---|

| Total Market Revenue | $15 million | $26.4 million |

| Active Users | ~500,000 | ~850,000 |

| ARPU | $30 | $31 |

| Market CAGR | 12% | |

Education, Skills, and Digital Literacy

Zimbabwe boasts a relatively high literacy rate estimated at over 90%, supported by widespread primary and secondary education penetration. Digital literacy among the urban youth is growing rapidly due to increased smartphone usage and internet access, particularly among ages 18 to 35, the core iGaming demographic.

Workforce skills in technology and services sectors are improving, fueled by government and private sector efforts focused on ICT training. However, rural areas lag behind due to infrastructure and educational resource limitations, constraining digital engagement outside urban centers.

Cultural and Social Factors

Communication and Language

English remains the official language and primary medium for digital and iGaming communication. However, several indigenous languages are widely spoken, influencing marketing and customer engagement strategies. The prominent language groups include:

- Shona

- Ndebele

- English (official)

- Sotho

- Tonga

- Venda

Cultural Attitudes

Gambling enjoys mixed cultural acceptance in Zimbabwe. It is generally popular in urban areas, especially among younger males, but traditional and religious communities may express caution or opposition. Christianity and indigenous beliefs influence attitudes toward gambling as a leisure activity. Foreign gambling brands are viewed cautiously but welcomed if aligned with local regulations and responsible play norms.

Entertainment preferences skew heavily toward mobile gaming, sports betting, and interactive casino experiences. Trust in legal and licensed gambling operators is a significant consideration for consumers, emphasizing the importance of strong regulatory frameworks.

Problem Gambling and Social Considerations

Problem gambling prevalence remains moderate, with government and regulatory bodies increasingly addressing public health concerns. At-risk populations include young urban males and those with pre-existing financial vulnerabilities. Public awareness and responsible gambling campaigns are mandated, and treatment resources are being expanded.

- National responsible gambling awareness programs

- Self-exclusion registries

- Mandatory operator contributions to support services

- Collaboration with NGOs on addiction counseling

- Regulatory enforcement of advertising standards to limit exposure

Political Structure and Governance

Zimbabwe operates under a unitary presidential republic with a relatively stable government that has emphasized regulatory reforms, including in gambling. Political consistency fosters a predictable regulatory environment, though macroeconomic challenges remain. International relations support foreign investment with some caution due to currency and policy fluctuations.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration is estimated at around 38.4% of the population (approximately 6.45 million users) as of early 2025, with steady growth despite infrastructural challenges. Mobile internet dominates access, with over 90% of users relying on mobile networks. Urban-rural internet divide persists due to infrastructure and affordability issues.

Social media engagement is significant, with approximately 2.1 million active users (12.5% of the population). The top platforms include:

- TikTok

- Twitter (X)

- YouTube

Digital Payment Behavior

Digital payments are rapidly replacing cash transactions, bolstered by mobile money services like EcoCash and increased point-of-sale infrastructure nationwide. Online transactions in the digital payments market reached estimated values exceeding $2.7 billion in 2025, supporting smoother gambling payments and in-game purchases.

- Mobile money dominates online payments

- Bank transfers are frequently used for larger amounts

- E-wallets are gaining traction among younger users

- Debit and credit card usage remains moderate

- Cryptocurrency adoption is nascent but growing

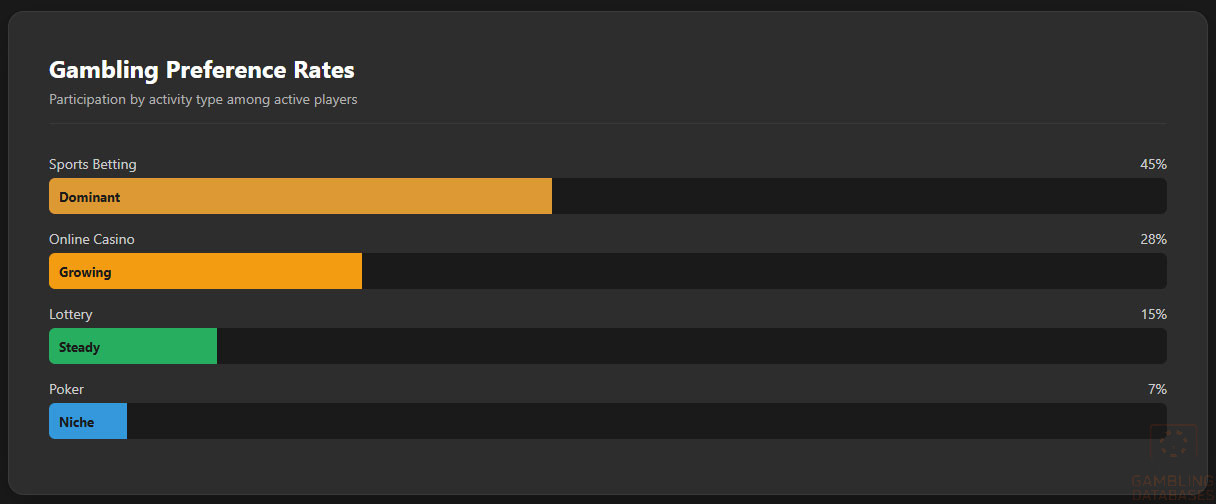

Gaming and Gambling Preferences

Current Market Participation

Gambling participation in Zimbabwe is concentrated among urban youth and middle-aged males, reflecting regional trends favoring sportsbook betting, online slots, and lotteries. User penetration is estimated at roughly 7.4% of the population, with sports betting holding the highest share.

| Rank | Gambling Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 45% |

| 2 | Online Casino Games (slots, roulette, blackjack) | 28% |

| 3 | Lottery | 15% |

| 4 | Poker | 7% |

| 5 | Esports Betting | 5% |

Consumer Behavior Patterns

Spending habits display moderate bet sizes aligned with average incomes, with a preference for mobile platforms driven by smartphone penetration. Peak wagering times coincide with evenings and weekends, while session lengths average between 30 to 60 minutes. Retention is supported by loyalty programs and interactive live dealer games, especially among urban players.

Online casino slots and sportsbook bets are favored for their speed and simplicity, while lottery and poker cater to more casual and social gamblers. The growing interest in esports betting marks an emerging niche attracting younger demographics.

Section 2: Demographics and Consumer Analysis

Population Demographics and Distribution

Zimbabwe’s population in 2025 is estimated at approximately 19.57 million, growing steadily at around 2% annually. The median age is young, at about 24.1 years, with a gender ratio of approximately 957 males per 1,000 females, reflecting a slightly higher female population.

Nearly half of Zimbabwe’s population (49.1%) is 19 years or younger, with adults aged 20 to 64 comprising around 48%. The elderly population (65+) represents only about 2.9%. This youthful demographic favors digital adoption, particularly for iGaming.

| Age Group | Percentage of Population |

|---|---|

| 0-19 years | 49.1% |

| 20-64 years | 48.0% |

| 65 years and older | 2.9% |

Urban population accounts for roughly 32.6%, primarily concentrated in major cities. The majority rural population experiences limited digital infrastructure, affecting access to gambling venues and online services.

- Harare – Approx. 1.6 million residents

- Bulawayo – Approx. 650,000 residents

- Chitungwiza – Over 350,000 residents

- Mutare – Around 200,000 residents

- Gweru – Approximately 150,000 residents

- Kwekwe – Near 120,000 residents

Economic Indicators and Consumer Spending Power

Zimbabwe’s economy is projected to grow by around 6% in 2025, with a nominal GDP near $26 billion. Agriculture, mining, and services sectors underpin the economy, supporting rising consumer income mainly in urban centers.

GDP per capita is modest at about $1,500. Despite economic challenges, disposable incomes are slowly increasing, encouraging discretionary spending including iGaming participation.

| Indicator | Value |

|---|---|

| GDP (Nominal) | $26 billion |

| GDP Growth Rate | 6.0% |

| GDP per Capita | $1,500 |

| Inflation Rate | ~10% |

| Unemployment Rate | ~12% |

The emerging iGaming market is valued at approximately $15 million, expected to grow at a CAGR of 12% until 2030, fueled by digital expansion and rising urban consumer spending power.

| Metric | 2025 | 2030 (Projected) |

|---|---|---|

| Total Market Revenue | $15 million | $26.4 million |

| Active Users | ~500,000 | ~850,000 |

| ARPU | $30 | $31 |

| Market CAGR | 12% | |

Education, Skills, and Digital Literacy

Zimbabwe maintains a literacy rate exceeding 90%, reinforced by widespread primary and secondary education access. Digital literacy, particularly among urban youths aged 18-35, is increasing due to smartphone availability and ICT initiatives, supporting iGaming adoption.

Skilled workforce development in technology sectors accelerates, but rural areas lag due to infrastructural and educational resource constraints.

Cultural and Social Factors

Communication and Language

English is the official language and primary medium for digital engagement. Indigenous languages are also prevalent, influencing marketing and communication strategies.

- Shona

- Ndebele

- English (official)

- Sotho

- Tonga

- Venda

Cultural Attitudes

Urban populations generally accept gambling, while some traditional and religious groups express caution. Foreign brands are cautiously welcomed if aligned with local regulations and responsible gambling culture. Mobile gaming and sports betting are popular leisure activities.

Problem Gambling and Social Considerations

Problem gambling rates are moderate, with focus on awareness and treatment. Government and NGOs provide support, emphasizing responsible gaming practices.

- National awareness campaigns

- Self-exclusion programs

- Mandatory operator contributions to support services

- Partnerships with addiction counseling organizations

- Regulatory controls on gambling advertising

Political Structure and Governance

Zimbabwe is a unitary presidential republic with relative political stability and commitment to regulatory reform. This fosters a predictable environment for businesses, although economic volatility remains a challenge.

Technology Adoption and Digital Behavior

Internet and Digital Usage

Internet penetration is around 38.4%, equating to approximately 6.45 million users. Mobile internet dominates with over 90% of users relying on mobile networks. Social media engagement includes about 2.1 million active users (12.5% of the population).

- TikTok

- Twitter (X)

- YouTube

Digital Payment Behavior

Digital payments are widely adopted, led by mobile money services, which fuel commerce and gambling transaction growth. Payment methods include:

- Mobile money

- Bank transfers

- E-wallets

- Debit and credit cards

- Cryptocurrencies (emerging)

Gaming and Gambling Preferences

Current Market Participation

Estimated gambling participation reaches about 7.4% of the population, driven mainly by sportsbook betting and online casino games. Urban male youth represent the dominant consumer segment.

| Rank | Activity | Participation Rate (%) |

|---|---|---|

| 1 | Sports Betting | 45% |

| 2 | Online Casino Games (slots, roulette, blackjack) | 28% |

| 3 | Lottery | 15% |

| 4 | Poker | 7% |

| 5 | Esports Betting | 5% |

Consumer Behavior Patterns

Players prefer mobile platforms and spend moderately in line with incomes. Peak gaming occurs in evenings and weekends, with session durations averaging 30-60 minutes. Loyalty programs and live-dealer games aid player retention.

Betting on sports and fast-paced casino games is most popular, while lottery and poker cater to casual segments. Esports betting is an emerging niche targeting younger users.

Section 3: Technology Infrastructure and Business Environment

Internet and Digital Infrastructure

Zimbabwe’s internet penetration reaches approximately 38.4% of the population, with mobile broadband constituting the majority of connections due to limited fixed-line infrastructure. Average mobile broadband speeds stand at about 10-15 Mbps, although speeds can vary significantly between urban and rural areas.

5G and Future Technology Deployment

Zimbabwe’s 5G rollout is in initial phases, with limited commercial coverage available in Harare and Bulawayo. The government supports 5G expansion plans targeting full urban network coverage by 2027. Network operators are upgrading infrastructure to accommodate 5G capabilities, which will improve bandwidth and latency essential for advanced iGaming applications.

Besides 5G, plans include enhancing IoT connectivity and adopting cloud data centers to support digital economies, presenting opportunities for technologically advanced gaming platforms.

Mobile Technology Ecosystem

The mobile ecosystem is vibrant, pivotal to digital access. Smartphone penetration approaches 55% in urban areas, with increasing availability of affordable Android devices driving usage. Device preferences favor mid-range smartphones capable of supporting gaming apps with enhanced graphics and speed.

- EcoCash Mobile Network – Largest mobile money operator and network enabler

- NetOne – Major telecom service provider with national coverage

- Telecel Zimbabwe – Growing market share with competitive data bundles

- TelOne – National fixed-line provider expanding into mobile broadband

- Liquid Telecom – Fiber optic backbone and internet services

Financial Services and Payment Infrastructure

Zimbabwe’s banking sector is a mix of state-owned and private commercial banks operating digital banking services. Mobile banking adoption is high, bridging banking access gaps across urban and rural zones. Financial inclusion has improved through digital wallets and mobile money platforms.

- CBZ Bank – Largest bank with wide branch and digital service network

- FBC Bank – Significant digital banking penetration

- Stanbic Bank Zimbabwe – Subsidiary of Standard Bank Group with corporate focus

- Ecobank Zimbabwe – Pan-African bank expanding retail and digital services

- ZB Bank – Established with notable SME financing portfolio

- Agribank – Specialized in agricultural sector financing

Payment Processing Options

Payment methods supporting the iGaming market encompass mobile money wallets, bank transfers, card payments, and cash-based voucher systems prevalent in urban retail outlets. Mobile money is dominant due to widespread smartphone and USSD phone usage, facilitating quick deposits and withdrawals on gaming platforms.

- EcoCash Mobile Money

- Telecash Mobile Wallet

- Bank Transfers via RTGS and SWIFT

- Visa and Mastercard Debit/Credit Cards

- E-wallets such as OneMoney and Steward Bank’s Ecocash-linked wallets

- Cryptocurrency options, although less commonly adopted due to regulatory caution

E-commerce and Digital Economy

Zimbabwe’s e-commerce market is growing steadily, supported by urban middle-class expansion and improved payment infrastructure. Online retail penetration remains below 10%, constrained by logistical challenges and consumer trust issues, but digital services uptake is increasing.

Consumer trust in digital payments is fortified through mobile money, which also integrates with e-commerce, digital media subscriptions, and more, supporting a digital economy that parallels growth in the iGaming market.

Business Environment and Regulatory Framework

Zimbabwe ranks moderately on the World Bank’s Ease of Doing Business index, with ongoing reforms improving administrative efficiency but challenges persist in regulatory complexity and currency volatility. Business registration processes are streamlined though still require thorough compliance with local regulations.

- Submit company registration application to the Registrar of Companies

- Obtain tax identification number from Zimbabwe Revenue Authority

- Register for VAT and social security contributions as applicable

- Open a corporate bank account in a local financial institution

- Apply for required operational licenses, including gaming license if relevant

Corporate Structure and Registration

Entities commonly used for market entry include Limited Liability Companies (LLCs), branches of foreign companies, and standalone corporations. LLCs are preferred for flexibility, liability protection, and ease of management, while branches require direct oversight from parent companies.

Foreign ownership is permitted but often subject to local presence requirements and partnership expectations to align with national economic policies and compliance monitoring.

- Certificate of Incorporation

- Memorandum and Articles of Association

- Proof of physical registered address in Zimbabwe

- Tax clearance and registration certificates

- Director and shareholder identification documents

- Bank statements demonstrating minimum capital requirements

Taxation Framework

Corporate income tax is generally levied at 24.72%. Special economic zones and export-oriented companies may enjoy tax holidays or reduced rates under incentive schemes. Zimbabwe is party to several double taxation treaties that mitigate fiscal burdens for foreign investors.

- South Africa

- Zambia

- Botswana

- Mozambique

- United Kingdom

- China

Personal income tax is progressive, with rates increasing per income bracket. Employers must withhold taxes at source and contribute to national social security schemes on behalf of employees.

Market Entry Considerations

Market entry strategies emphasize partnerships with local firms, leveraging established distribution networks and compliance expertise. Technology adoption requires robust payment integrations and mobile-optimized platforms reflecting consumer device preferences.

- Form strategic joint ventures with Zimbabwean partners

- Invest in mobile-first platform technologies

- Engage in local marketing focusing on urban youth

- Ensure comprehensive compliance with regulatory and tax frameworks

- Adopt flexible payment solutions including mobile money

| Cost Category | Estimated Cost |

|---|---|

| License Application and Fees | $10,000 – $30,000 |

| Legal and Compliance Setup | $15,000 – $25,000 |

| Technical Integration | $20,000 – $40,000 |

| Marketing and Customer Acquisition | Variable, starting at $10,000 |

| Operational and Staffing Costs | $50,000+ annually |

- Pre-market research and analysis — 1 to 2 months

- Company registration and licensing — 3 to 6 months

- Technical platform development and integration — 3 months

- Marketing launch and user acquisition — ongoing

Success depends on understanding local consumer behavior, navigating regulatory nuances, and investing in reliable digital infrastructure. Challenges include infrastructural gaps, competition from informal operators, and currency volatility, which demand strategic agility and localized expertise.

- Strong regulatory compliance and proactive engagement

- Robust mobile platform optimized for varying network conditions

- Flexible payment systems integrating mobile money

- Localized marketing campaigns respecting cultural sensitivities

- Partnerships with trusted local entities for market penetration

Exit strategies should consider the liquidity of licenses, regulatory transferability, and market valuation trends to maximize asset realization.

FAQ: Frequently Asked Questions

1. Is online gambling legal in Zimbabwe?

Yes, online gambling is legal but tightly regulated. Operators must obtain licenses from the Lotteries and Gaming Board, comply with KYC/AML procedures, and adhere to responsible gambling mandates. The government actively monitors to prevent illegal operations, reinforcing licensed market integrity.

2. What types of gambling licenses are available and what do they cover?

Licenses cover land-based casinos, sports betting, online casinos, lotteries, and totalizator operations. Each license type is distinct, with separate applications, fees, and regulatory obligations tailored to the gaming category. Online and land-based licenses require robust compliance frameworks.

3. How much does an iGaming license cost and how long does it take to obtain?

License application fees range from $10,000 to $30,000 depending on license type, with typical approval timelines between 3 to 6 months. Renewal fees amount to 20-30% of initial costs. Additional compliance and operational readiness significantly impact time-to-market.

4. Can foreign companies obtain a gambling license?

Foreign companies can obtain licenses but must establish a local presence via an office or agent. They must comply with ownership and operational mandates, including partnership with local stakeholders in some cases, ensuring regulatory transparency and market adaptation.

5. What are the tax obligations for iGaming operators?

Operators pay corporate income tax at approximately 24.72%, plus a GGR tax up to 15%. Sports betting winnings are subject to a 10% withholding tax. Various fees, including licensing and renewal, and possible turnover taxes, contribute to the fiscal obligations.

| Tax Type | Rate |

|---|---|

| Corporate Income Tax | 24.72% |

| Gross Gaming Revenue Tax | Up to 15% |

| Sports Betting Winnings Withholding | 10% |

| License Renewal Fees | 20-30% of initial fee |

6. Are gambling winnings taxed for players?

Yes, particularly winnings from sports betting are subject to a 10% withholding tax deducted at source by operators. This approach streamlines revenue collection and compliance, though it may influence player preferences toward licensed platforms.

7. What are the typical operational costs for running an online casino/sportsbook?

Operational costs include licensing fees, platform maintenance, staff salaries, marketing, payment processing, and compliance measures. Initial technology setup and ongoing marketing can be significant, with monthly expenses varying widely depending on scale of operations and market penetration efforts.

- Licensing and regulatory fees

- Technical infrastructure and software costs

- Customer support and staffing

- Marketing and user acquisition

- Payment processing fees

8. What is the expected ROI timeline for entering this market?

Return on investment timelines typically range from 18 to 36 months, influenced by regulatory compliance speed, market penetration, and operational efficiency. Strong partnerships and mobile-optimized technology platforms accelerate breakeven achievement.

9. What are the local presence requirements for operators?

Operators must maintain a registered local entity or appoint an authorized local agent with physical offices. This ensures compliance accountability, regulatory communication, and effective player dispute resolution within Zimbabwe’s jurisdiction.

10. What payment methods are available and recommended?

Mobile money services dominate, with EcoCash leading due to widespread user adoption and integration. Bank transfers and card payments also supplement transaction options. Emerging e-wallets and cryptocurrencies provide alternatives but require cautious regulatory navigation.

11. What are the advertising and marketing restrictions?

Advertising must avoid targeting minors and vulnerable groups, include responsible gambling messages, and refrain from misleading claims. Restrictions limit gambling ads during daytime hours accessible to youth, and sponsorships require regulator approval. Digital content is closely monitored.

12. What responsible gambling measures are mandatory?

Operators must implement self-exclusion systems, player limits, educational materials on gambling risks, transaction monitoring for at-risk behaviors, and submit regular reports on responsible gambling activities to authorities.

13. How large is the iGaming market and what is the growth potential?

The iGaming market is valued at approximately $15 million in 2025, forecasted to grow at a 12% CAGR until 2030, fueled by rising internet penetration, mobile adoption, and regulatory maturation.

14. Who are the main competitors and what is their market share?

The market features entrenched local bookmakers and international operators focusing on sports betting and online casino games. Competition is growing with new licensed entrants pursuing joint ventures and technology innovation to capture market share.

15. What are the player preferences and typical spending patterns?

Players prefer mobile platforms, especially for sportsbook betting and slots, with average spend around $30 annually. Peak activity occurs in evenings and weekends, with loyalty programs boosting retention and incremental spending.

16. What are the key success factors and main challenges for new entrants?

Success depends on strong regulatory compliance, mobile-first platforms, effective local partnerships, flexible payment integration, and culturally sensitive marketing. Challenges include infrastructural limitations, competition from informal operators, economic volatility, and enforcement complexity.

- Comprehensive regulatory adherence

- Agile mobile technology deployment

- Robust digital payment integration

- Local market understanding and partnerships

- Proactive risk and reputation management

Sources and References

- Lotteries and Gaming Board of Zimbabwe – Official Regulatory Framework and Licensing Guidelines

- Zimbabwe National Statistics Agency – Demographic and Economic Reports 2025

- World Bank – Ease of Doing Business Reports for Zimbabwe 2024-2025

- International Monetary Fund – Zimbabwe Country Economic Forecasts 2025

- Zimbabwe Ministry of Finance – Taxation Codes and Revenue Reports 2025

- Telecommunications and Postal Services Authority of Zimbabwe – ICT Infrastructure Reports 2025

- EcoCash Zimbabwe – Mobile Money Penetration and Usage Statistics 2025

- Zimbabwe Central Bank – Financial Sector and Banking Overview 2025

- Digital 2025: Zimbabwe Report – Datareportal

- Gaming Industry Reports – African iGaming Market Analysis 2024-2025

- Statista – Zimbabwe Gambling Market and Digital Payments Forecasts

- Zimbabwe Ministry of ICT and Cyber Security – 5G and Technology Deployment Reports 2025

- Ecofin Agency – Zimbabwe Economic Growth Update 2025

- UN Data – Zimbabwe Population and Social Statistics 2024

- Zimbabwe National Responsible Gambling Programs – Government Publications 2024-2025

- Commercial Banks of Zimbabwe – Annual Reports 2025

- Technomag Zimbabwe – Internet and Digital Payment Trends 2025

- Zimbabwe Revenue Authority – Gambling Tax and Compliance Information 2025

- Gambling Today – Zimbabwe iGaming Market Reports 2025

- Gaming Awards Africa – Regulatory Changes and Market Trends 2025

🎯 Gambling Databases Country Rating: Zimbabwe

| Evaluation Dimension | Score | Rating |

|---|---|---|

| Operator Ease Score | 6.8/10 | 🟡 Moderate |

| Player Access Score | 9.0/10 | 🟢 Excellent |

| Overall Market Attractiveness | 6.0/10 | 🟡 Moderate (High Ease / Low Value) |

This rating is calculated using the Gambling Databases Rating (GDR) methodology, which provides transparent criteria for evaluating iGaming markets worldwide. Click the link to learn how we calculate Operator Ease Score, Player Access Score, and overall market attractiveness ratings.

⚠️ CRITICAL RISK WARNINGS

READ THIS BEFORE CONSIDERING MARKET ENTRY:

- Currency & Economic Volatility: Operations are subject to the Zimbabwean Dollar (ZWL), known for extreme volatility. Repatriating profits can be difficult due to foreign exchange shortages.

- 10% Player Winnings Tax: Effective Jan 2025, a 10% withholding tax applies to all gross winnings. This significantly reduces player liquidity and encourages black market usage.

- Mandatory Local Presence: Foreign operators CANNOT operate remotely; a local registered office or agent is strictly required.

- Active Enforcement: The Lotteries and Gaming Board and Ministry of Home Affairs are actively cracking down on unlicensed operators to protect tax revenues.

- Infrastructure Gaps: Severe rural connectivity issues and frequent power outages impact server uptime and player connectivity.

📊 Operator Ease Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal & Regulatory Framework | 30% | 2.5/3.0 | Full product legality (Casino + Sports) (+3.0). Deducted -0.5 for nascent/evolving regulations that are subject to rapid change and increased enforcement against unlicensed entities. Final: 2.5/3.0. |

| Licensing Process | 25% | 2.25/2.5 | Accessible licensing process taking 3-6 months (+2.0). Very low application fees ($10k-$30k) (+0.5). Deduction for mandatory local agent/office requirement (-0.25). Final: 2.25/2.5. |

| Taxation & Costs | 20% | 1.5/2.0 | GGR Tax at 15% is competitive (+1.5). Corporate tax ~24.72%. Major deduction for the new 10% Withholding Tax on player winnings (-0.5) which damages churn and retention metrics. Final: 1.5/2.0. |

| Operational Requirements | 15% | 0.5/1.5 | Moderate requirements (+1.0). Deductions: Mandatory local presence/office (-0.25), Banking and currency volatility risks (-0.25). Final: 0.5/1.5. |

| Market Environment | 10% | 0.0/1.0 | Difficult business environment (+0.25). Deductions: Economic instability and currency risk (-0.25), Infrastructure/Power reliability issues (-0.25). Final: 0.0/1.0. |

👥 Player Access Score Breakdown

| Criterion | Weight | Score | Justification (INCLUDING ALL DEDUCTIONS) |

|---|---|---|---|

| Legal Status for Players | 40% | 3.5/4.0 | Fully legal regulated market (+4.0). Deduction: Introduction of 10% tax on winnings penalizes legal play (-0.5). Final: 3.5/4.0. |

| Practical Accessibility | 30% | 2.5/3.0 | Widespread mobile money (EcoCash) usage (+3.0). Deductions: Rural internet infrastructure gaps and power outages limit access times (-0.5). Final: 2.5/3.0. |

| Player Penalties | 20% | 2.0/2.0 | No criminal penalties for players accessing offshore sites, though the government encourages licensed play. |

| Market Availability | 10% | 1.0/1.0 | Multiple licensed operators available (Domestic and International) (+1.0). |

🔍 Key Highlights

Strengths

- Low Entry Costs: Licensing fees ($10k-$30k) are among the lowest globally.

- Full Product Legality: Unlike many African jurisdictions, both sports betting and online casino are legal and regulated.

- Mobile Money Integration: High adoption of EcoCash makes depositing seamless for the banked urban population.

⛔️ CRITICAL RISKS AND CHALLENGES

- Market Size vs. Effort: The total iGaming market is only ~$15M. The revenue potential is extremely low compared to the operational headache of establishing a local office.

- Player Taxation: The 10% withholding tax on gross winnings (not just profit) is a massive deterrent for high-volume players.

- Currency Risk: The Zimbabwean Dollar is historically unstable. Operators risk devaluation of funds before they can be repatriated.

- Infrastructure: “Load shedding” (power outages) and poor rural connectivity limit peak gaming hours.

- Low ARPU: With an average revenue per user of ~$30/year and GDP per capita of $1,500, player value is very low.

Player-Specific Issues

- Winnings Tax: Players lose 10% of every winning bet immediately.

- Connectivity: Players outside Harare/Bulawayo face reliable internet access issues.

💰 Reality Check: Can You Actually Make Money Here?

Initial Investment Required: $50,000 – $80,000 (Low – covers license, local setup, legal).

Monthly Operating Costs: $30,000 – $50,000 (Low local wages, but high infrastructure/backup power costs).

Effective Tax Rate on Revenue: ~40% (15% GGR + 24.72% Corp Tax + License renewal fees).

Customer Acquisition Cost: Low ($5 – $15), but aligned with very low Player Value (LTV).

Time to Breakeven: 12-18 months.

Profitability Assessment: Questionable. While entry is cheap, the market is tiny ($15M total). A new entrant capturing 10% market share would only generate $1.5M GGR before taxes and ops. This market is likely only viable for: 1) Large regional operators (e.g., from South Africa) expanding footprint, or 2) Low-overhead local startups. Not recommended for European Tier 1 operators due to low ROI.

⚖️ Legal Risk Assessment

| Stakeholder Type | Risk Level | Specific Risks |

|---|---|---|

| Offshore Casino Operators | [High] | [Active crackdown on unlicensed entities, potential blacklisting, inability to use local mobile money rails.] |

| Licensed Operators | [Medium] | [Currency devaluation risk, changing tax laws (e.g., new WHT), compliance with strict KYC.] |

| Affiliates/Advertisers | [Medium] | [Advertising restricted to responsible content; promoting unlicensed brands may attract regulatory scrutiny.] |

| Payment Processors | [High] | [Strict central bank controls on forex; risk of penalties for facilitating unlicensed gambling.] |

| Company Directors | [Low] | [Standard corporate liability, provided local entity is compliant.] |

🚨 Extradition and International Enforcement

Extradition Treaties: Zimbabwe has extradition arrangements with the UK, USA, and Southern African Development Community (SADC) countries (South Africa, Zambia, etc.).

Enforcement History: Enforcement is primarily domestic, focused on shutting down physical illegal venues. International extradition for online gambling offenses is rare but legally possible under fraud/money laundering statutes.

Safe Jurisdictions: No specific “safe haven” status, but enforcement reach outside of Africa is practically limited by resources.

📋 Final Verdict

Zimbabwe receives an Operator Ease Score of 6.8/10 and a Player Access Score of 9.0/10, resulting in an overall market attractiveness rating of 6.0/10.

HONEST ASSESSMENT: Zimbabwe is a classic “Paper Tiger” market. On paper, it looks attractive with low license fees, legal online casinos, and decent tax rates. In reality, the minuscule market size ($15M), currency volatility, and mandatory local presence make it a poor investment for international operators. The newly introduced 10% tax on player winnings further erodes the already low player value. It is easy to enter, but very hard to extract meaningful profit.

✅ Who Should Enter / ❌ Who Should Avoid

✅ Consider Entry If You Are:

- A Pan-African Operator already established in Zambia or South Africa looking to complete regional coverage.

- A Local Entrepreneur with existing retail/betting shop infrastructure.

- Willing to accept ZWL currency risks and have a strategy for local cash utilization.

❌ Definitely Avoid If You Are:

- A European/Global Tier 1 Operator (Market size is too small to justify compliance overhead).

- An Offshore-only operator (Cannot integrate EcoCash/Mobile Money without local entity).

- Dependent on High-Roller traffic (10% winnings tax drives VIPs to black market).

- Unwilling to set up a physical office in Zimbabwe.

⚠️ BOTTOM LINE: Legal and cheap to enter, but the economics are weak due to poverty, currency instability, and a tiny total addressable market. Only viable for regional African specialists.